The Massachusetts Department of Public Utilities (DPU) on July 9 approved a proposal to expedite the state’s review process for municipal aggregation plans, while also adding transparency requirements and allowing municipalities to update their plans without DPU approval.

Municipal aggregation plans enable communities to purchase electricity in bulk and can reduce ratepayer costs relative to basic utility service in Massachusetts. They also can give ratepayers options to increase the number of renewable energy certificates (RECs) over what is required by the state’s Renewable Portfolio Standard (RPS).

Despite the potential benefits, the DPU has faced criticism for yearslong wait times for aggregation applications to be approved.

Municipal aggregation reforms have been a priority of the DPU under Chairperson Jamie Van Nostrand, who was appointed by Gov. Maura Healey (D) in 2023. The DPU opened a docket on municipal aggregation reform in August 2023, which included draft guidelines, and asked for stakeholder feedback (D.P.U. 23-67-A).

Public comments largely were critical of the draft guidelines, which ultimately led to the creation of a stakeholder working group that advised a group of consultants in the creation of a new proposal.

The consultants jointly submitted the resulting proposal in early June with the backing of key stakeholders including the Green Energy Consumers Alliance, the city of Boston, several state agencies and electric distribution utilities.

“While the joint petitioners did not fully agree on all issues, the joint petitioners agree that the adoption of the guidelines and accompanying documents should significantly improve the effectiveness and efficiency of the department’s review and approval of municipal aggregation plans,” read the proposal.

The DPU approved these new guidelines with only “clarifying, non-substantive edits,” writing that they will “strike an appropriate balance between administrative efficiency … and transparency.”

Under the new guidelines, the DPU will be required to respond to municipal aggregation applications within 120 days of their submission. The department has issued a standard application template intended to help facilitate an expedited review process.

The order also increases the transparency mandates for municipal aggregations, requiring disclosures related to rates, clean energy makeup and certificates, different customer classes, and accessibility.

These measures will enable “increased public scrutiny,” the DPU wrote, adding that they are an important component of allowing increased discretion to each municipality in developing and updating its aggregation.

The new rules will allow municipalities to update their plans “in a manner consistent with these proposed guidelines without department approval, provided that it allows at least 30 calendar days for public review of the revised plan,” the DPU noted.

The department wrote that the rules will enable greater flexibility for municipal aggregations “to respond to market conditions in a timely manner.”

Municipalities filing new aggregation plans also will be required to meet with the Department of Energy Resources to go over their plan and discuss best practices.

The DPU’s approval was applauded by several stakeholders who have focused on the issue.

“Reforming the commonwealth’s municipal aggregation process was a priority in the legislature this session,” said Rep. Jeff Roy (D), House Chair of the Joint Committee on Telecommunications, Utilities and Energy. “The DPU’s thoughtful and collaborative engagement with stakeholders over the past few months has resulted in updated guidelines that will allow for greater flexibility and innovation, supporting both ratepayers and the commonwealth’s clean energy transition.”

Larry Chretien, executive director of the Green Energy Consumers Alliance, said the new guidelines will “help the aggregation movement grow while [continuing] to ensure consumer protections.”

Ten East Coast states signed a memorandum of understanding July 9 to set up a framework to coordinate interregional transmission planning and development.

Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Rhode Island and Vermont will explore mutually beneficial interregional transmission to increase the flow of electricity between the ISO-NE, NYISO and PJM, as well as assessing offshore wind infrastructure needs.

The states have been working on the issues for more than a year, since they sent the U.S. Department of Energy’s Grid Deployment Office a letter asking for help to convene a Northeast States Collaborative on Interregional Transmission. (See Northeast States Detail Early Efforts on Interregional Tx Collaborative.)

Massachusetts Energy and Environmental Affairs Secretary Rebecca Tepper said her state cannot go it alone to address climate change and that interregional collaboration is a top priority of Gov. Maura Healey (D).

“Through partnerships like this collaborative, we will be able to advance more cost-effective transmission projects for the residents of the Northeast,” Tepper said in a statement.

The states agreed to work together on interregional transmission infrastructure and share information. Enhancing ties between the regions should lower prices for consumers by broadening access to the cheapest available power and bolster reliability during periods of extreme weather and system stress, they said in the MOU.

“New Jersey is not alone in experiencing increasingly frequent extreme weather events and record-breaking temperatures that threaten public health and safety,” New Jersey Gov. Phil Murphy (D) said in a statement. “We are also not alone in our response to the intensifying climate crisis, which provides crucial opportunities to leverage interregional partnerships toward improving our collective resilience and economic vitality.”

The collaborative has plans to produce a strategic action plan for promoting interregional transmission projects that can cut the cost of bringing offshore wind to consumers. That plan would involve identifying barriers to such projects and how to address them.

The states intend to provide opportunities for external engagement as they develop the plan. They also want to coordinate on technical standards for offshore wind transmission equipment to ensure interoperability as projects come online in different areas at different times. The states plan to work with DOE, FERC, industry and the three grid operators.

Any decisions that come out of the collaborative will require mutual consent among the states that said they would maintain their independence. That means nothing in the deal prevents them from independently or collectively seeking support or funding, advocating for or participating in any other planning and cost allocation processes.

The six New England states and New York have a pending application at DOE to get some funding through the Grid Innovation Program for National Grid’s Clean Resilience Link, a 345-kV line between ISO-NE and NYISO to increase their transfer capability by 1,000 MW. The $10.5 billion GIP program offers a maximum of $1 billion for projects.

Speaking for himself, Abe Silverman of SilverGreen Energy Consulting, which has been working with the states, said in an interview that the effort helps to formalize a relationship between the states, the federal government and the ISO/RTOs to move transmission forward for offshore wind and interregional transfer capacity.

While federal efforts on interregional transmission also are important, Silverman said that often, when major interregional and even intraregional lines have actually been built, states have been behind the efforts.

“There isn’t a lot of it, and what has been built … has often been the result of concerted state efforts,” he said. “Look at the Competitive Renewable Energy Zone lines in Texas, the Long-Range Transmission Planning Program in MISO, the New York [Public Policy Transmission Need process] and New Jersey’s State Agreement Approach; … those were all major transmission efforts that had their genesis in state agreements.”

The states in the collaborative include only a couple led by Republican governors, and many of the quotes from senior officials on it were focused on liberal policies around offshore wind and addressing climate change, but Silverman argued that interregional transmission has bipartisan bona fides.

“I often talk about how transmission policy needs to pass the ‘Joe Manchin press release’ test, which is, this is a set of policies that [Sen.] Joe Manchin [I-W.Va.] would be OK promoting,” Silverman said. “And you look at the benefits of interregional transmission: It’s lower cost for consumers; it’s better reliability — particularly in the face of extreme weather — and it’s about American energy independence and dominance.”

Those factors, which test well with Manchin and others leaning to the right on energy, are enough to justify the investment regardless of the climate impacts, he argued.

NARUC Weighs in on Interregional Transmission with New Study

The National Association of Regulatory Utility Commissioners on July 9 released a new study called Collaborative Enhancements to Unlock Interregional Transmission, which was prepared by Energy and Environmental Economics (E3).

The study highlights strategies for increasing transfer capability, which state regulators increasingly have looked toward because of rising demand and ongoing changes in supply.

“As our existing grid is forced to respond and adapt to emerging needs, regulators are increasingly interested in assessing how new interregional transmission infrastructure can drive value for customers,” Kansas Corporation Commission Chair Andrew French said in a statement. “This timely report provides PUCs a straightforward assessment of existing barriers preventing robust interregional transmission planning and a suite of potential solutions for regulators and other stakeholders to consider.”

Maria Robinson — director of DOE’s Grid Deployment Office, which helped NARUC with the report — called interregional planning critical for providing reliable and affordable power.

“Public utility commissions need practical solutions for identifying crucial interregional transmission projects to ensure power gets from where it’s generated to where it’s needed most, when it’s needed most,” Robinson said in a statement. “We are proud to support NARUC in this effort as partnerships at the federal, state and local levels are needed to meet our shared goal of a more reliable and affordable grid in the face of aging infrastructure, extreme weather and changing energy landscape.”

The study argues that the limited success on interregional lines so far can be attributed to three main issues: the lack of planning motivators, cost allocation, and planning process misalignment and analysis limits.

Regions could expand coordinated planning to identify joint needs and solutions because once the same needs are identified, they would be motivated to reconcile their differing regional planning processes, or develop new ones, to identify interregional lines, the paper says.

They also could standardize universal best practices in regional and interregional transmission solutions to ensure the best projects are identified and thoroughly analyzed, while accurately assigning costs to beneficiaries, to cut friction in interregional planning. The regions also should work to reconcile differences in modeling, tools, data inputs and benefit calculation methods, the paper says.

While projects are planned and cost allocated across multiple states, they are sited by individual state regulators who most often have the final decision on what moves forward. The paper suggests ensuring projects have non-energy benefits to ensure states that bear their physical impact also benefit, which could include jobs, revenue sharing, investment in capital projects and social programs, and economic development opportunities.

States also could use the same analysis for an interregional line’s “need” and coordinate their evidentiary records to synchronize permitting timelines and standardize data collected to inform decision-making, according to the study.

“Different states may still have different priorities and may choose to include different types of benefits in what they consider, but standardizing a common set of underlying facts, models and timelines could help expedite project approvals,” the paper says.

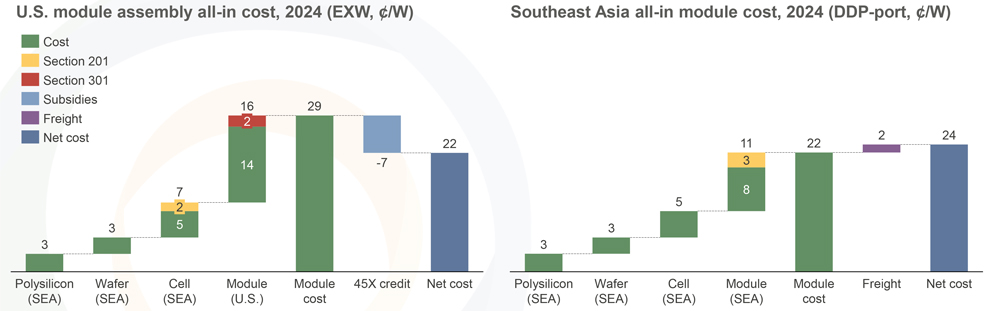

The U.S. solar market may face major domestic supply chain gaps as it heads toward 2030, as incentives from the Inflation Reduction Act spur solar panel manufacturing but leave those factories dependent on imported solar cells, according to a report released July 9.

A joint project of the American Council for Renewable Energy and Clean Energy Associates (CEA), the report estimates U.S. factories may be producing 60 GW of solar panels per year by 2030, but only about 12 GW of solar cells. Further, 97% of the imported solar cells needed to make up the difference are subject to existing solar tariffs, and some soon could have additional duties slapped on them.

If those new duties are imposed, CEA predicts prices for domestically produced solar panels made with imported cells could increase by 10 cents/W, while the price for imported panels could go up 15 cents/W.

“Tariffs increase capital costs, and when you talk about increasing capital costs, [that] increases the cost of delivering electricity, and that of course is going to have an impact on demand” and the country’s ability to meet its greenhouse gas emission-reduction goals, said Daniel Shreve, vice president of market intelligence at CEA.

But during a July 9 webinar launching the report, Shreve said that even with new tariffs and the variability in location and logistics of specific projects, utility-scale “solar is going to be extraordinarily competitive and the lowest-cost source of electricity in most situations,” compared with often volatile natural gas prices.

The report comes just weeks after the end of President Joe Biden’s two-year moratorium on solar tariffs on cells and panels from Cambodia, Malaysia, Thailand and Vietnam. Biden established the moratorium in June 2022, during an International Trade Commission (ITC) investigation of whether imports from those countries were using Chinese components and attempting to circumvent existing tariffs.

The investigation triggered a panic and a spike in prices in the solar market, and Biden justified the moratorium as “a bridge” for the industry to stand up domestic manufacturing. Signed into law in August 2022, the IRA’s solar and clean manufacturing incentives stoked a wave of announcements of new solar factories ― 131 GW of panel factories and 87 GW of cell plants ― but CEA expects “realized capacity” to be significantly lower.

“If we’re talking about what’s holding some of this capacity back, a lot of it has to do with trying to gather finances associated with these very large capital expenditures,” Shreve said. “You need investors; you need off-takers; and these things take time to develop, and folks have to become comfortable with bringing that supply online.”

CEA’s forecast of just 12 GW of cell capacity by 2030 could increase, he said, “but we need to see some more traction from some of these suppliers first before we make that move in our forecast.”

AD/CVD Headwinds

| CEA

The U.S. solar market is strong, Shreve said, pointing to a compound annual growth rate of 33% between 2010 and 2023. The market hit new highs last year, putting a total of 32 GW of new solar online, including 22 GW of utility-scale projects and 7 GW of residential installations.

But the rate of deployment must step up to meet Biden’s goal of cutting the nation’s greenhouse gas emissions 50 to 52% by 2030. Total U.S. solar capacity hit 177 GW in 2023, the analysis says, but cites multiple reports calling for a threefold increase to between 500 and 560 GW by 2030 to slash emissions in half.

Standing up a domestic supply chain is seen as a critical factor for market growth as the IRA provides bonus tax credits of up to 10% for solar projects that meet the law’s domestic content provisions. To qualify, projects beginning construction this year must meet a 40% domestic content requirement, which will step up 5% per year to 55% in 2026 and beyond.

Solar tariffs and anti-dumping and countervailing duties (AD/CVD) are seen as major headwinds for the market, according to CEA Senior Policy Analyst Christian Roselund.

The end of Biden’s two-year moratorium coincided with a new AD/CVD investigation, again focused on imported solar cells, whether or not already assembled in modules, and targeting Cambodia, Malaysia, Thailand and Vietnam.

In May, Biden also doubled tariffs on solar cells imported from China, from 25% to 50%, and removed an existing exemption for tariffs on bifacial solar panels.

Roselund said the AD/CVD duties could have a significant impact on the market because of their broad unpredictability. Unlike tariffs with set specific rates, these duties are imposed retroactively; so, a company may not know how much it will be charged for cells it is importing, and the rates may change every year.

Suppliers pay an upfront cash deposit on imported panels or cells, he said, but “if you’re importing goods that are subject to an anti-dumping or countervailing duty order, you won’t know how much you actually owe until an administrative review that will come two, perhaps three years later. … You import goods, and then you get the bill several years later.”

In addition, solar cells from the four Southeast Asian countries currently account for 58% of solar cell imports to the U.S. and 78% of imported panels, making them the biggest source of solar imports for the U.S. market, Roselund said.

Projects Canceled, Delayed

Depending on the ITC’s final decision, new AD/CVD tariffs could be imposed starting in September or, under special circumstances, retroactively from June 2023, he said. While not speculating about any potential outcomes, Roselund noted that when the ITC launched its previous AD/CVD investigation in 2022, solar imports had their slowest quarter in two years.

Roselund expects median rates for the duties, if imposed, to range from 9% to 51%, but he said the unpredictability of the rates potentially is the most dampening for market growth.

“Try to run your financial spreadsheets when you have a variable in one of the columns; it’s just very hard to do,” he said. “It hits buyers and suppliers, and then [photovoltaic] projects and manufacturing facilities. … If you have a U.S. module factory and suddenly you don’t know what you’re going to have to pay for cells, that impacts your operations and what you end up with is projects canceled, projects delayed and supply shifts as the market adjusts.”

Even with the generous incentives in the IRA, Roselund noted that in the past AD/CVD tariffs had not stimulated the buildout of a domestic supply chain. “We saw that supply shifted to other low-cost manufacturing locations,” he said.

Roselund also flagged other market headwinds. U.S. solar prices are about double the average per-watt cost in global markets, and under the pressure of the ITC investigation, suppliers are starting to reopen signed contracts and increase prices for imported cells and panels.

“Suppliers are saying, ‘We can’t deliver the product that you signed a contract for previously,’ and they have to bring the prices back up to account for their risk of what they’re going to have to pay,” he said.

The D.C. Circuit Court of Appeals on July 9 directed FERC to apply the Mobile-Sierra doctrine when it reconsiders a series of 2022 orders requiring Western wholesale electricity sellers to refund a portion of the high prices they earned during an August 2020 heat wave.

At issue in the case — and in the related FERC orders — is the commission’s longstanding policy of maintaining a “soft” price cap for short-term electricity sales in the West to prevent the exercise of market power (22-1116). A product of the Western energy crisis of 2000/01, the policy requires sellers to justify the costs behind power prices exceeding the soft cap of $1,000/MWh, or refund any amount earned above the cap.

The case dealt specifically with surging prices associated with tight supply conditions stemming from triple-digit temperatures occurring over Aug. 18-19, 2020, when CAISO struggled to prevent the rolling blackouts it was forced to order Aug. 14-15 — the first such blackouts in nearly 20 years.

Wholesale prices at Arizona’s Palo Verde hub on the Intercontinental Exchange (ICE) hit records of $1,515/MWh on Aug. 18 and $1,750 on Aug. 19. The hub’s average price from June to August of that year, excluding the August price spike, was $52/MWh, according to filings Southern California Edison and Pacific Gas and Electric made with FERC to protest the prices.

Over the course of 2022, FERC issued a series of decisions rejecting the justifications of sellers who sold electricity at those levels during the period, finding that the ICE index prices reflected scarcity conditions and that the selling companies had failed to justify their premiums based on costs.

Those decisions rejected the argument by sellers that FERC should apply the presumptions from the 1956 cases United Gas Pipeline v. Mobile Gas Serviceand FPC v. Sierra Pacific Power — or Mobile-Sierra doctrine — to the sales and hold that the contracts were freely negotiated between the buyers and sellers and did not harm the public interest. Instead, the commission determined the Mobile-Sierra presumption did not prevent it from “enforcing the requirement that sales in excess of the WECC [or Western] soft price cap must be justified and [we]re subject to refund.”

The commission also held that it had the authority to enforce the soft cap through refunds without conducting a Mobile-Sierra public-interest analysis because the soft cap was part of the sellers’ filed rate, a finding reinforced by the 2002 “Soft-Cap Order” establishing the caps in the West.

In its decisions, the commission also rejected requests by some sellers to raise the West-wide soft cap to $2,000/MWh, in line with the cap in place in CAISO, saying that was out-of-scope for the rulings.

Then-Commissioner James Danly dissented in each of the orders, questioning the commission’s authority to abrogate bilateral contracts reached between buyers and sellers in a time of tight supply conditions. Danly wrote that FERC instead should have applied the Mobile-Sierra presumptions to the contract and found that the public interest was not harmed by upholding them.

The sellers once again used that line of reasoning in their appeal to the D.C. Circuit, contending FERC erred by not conducting a Mobile-Sierra analysis before ordering the refunds — an argument that swayed the court in its decision to remand the orders back to FERC.

“We agree with the sellers that the commission should have conducted the Mobile-Sierraanalysis prior to ordering refunds, and so we grant the sellers’ petitions for review, vacate the orders they challenge, and remand for further proceedings,” the court wrote. “Because of that holding, the commission necessarily will need to change its refund analysis for above-cap sales going forward, and any decision by this court on the validity of that framework would be purely advisory.”

In its ruling, the D.C. Circuit said FERC’s arguments against administering a public-interest analysis before enforcing refunds “fail for a simple reason.”

“Even assuming that the Soft-Cap Order was incorporated into sellers’ tariffs and contracts, the commission did not displace the Mobile-Sierra presumption in the Soft-Cap Order itself, and so that presumption continues to apply to the Sellers’ contracts,” it found.

“More specifically, nothing in the Soft-Cap Order established that the Mobile-Sierra doctrine would not apply to the commission’s review of any above-cap rates,” the court continued. “As such, the Soft-Cap Order left intact the commission’s burden of overcoming the presumption that ‘a freely negotiated wholesale-energy contract meets the “just and reasonable” requirement imposed by law.’”

The court went on to say that the soft cap “is best viewed as a means for flagging for the commission contracts that may warrant public-interest analysis.”

“The requirement that sellers ‘justif[y]’ their above-cap prices, in turn, facilitates this review by obligating sellers to supply information showing that the conditions for the ordinary application of the Mobile-Sierrapresumption (e.g., the absence of market manipulation) were in place at the time of the above-cap sale,” the court concluded.

‘Consumers’ Petition Rejected

The court additionally rejected a petition by the California Public Utilities Commission and SCE (called the “consumers” in the ruling), which contend that FERC committed errors in its refund calculations that would lead to higher electricity prices in the future.

“We have no occasion to engage with the merits of the consumers’ challenge because it is moot,” the D.C. Circuit found, noting that the petitioners had questioned the way in which FERC had calculated the refunds but that the court already determined the commission had “erred in ordering refunds in the first place without applying the Mobile-Sierrapublic-interest analysis.”

NERC urged the Department of Homeland Security’s Cybersecurity and Infrastructure Security Agency (CISA) to ensure that future rules on reporting cybersecurity incidents are in harmony with existing requirements and that it continue collaborating with utilities and their regulators during the rulemaking process.

Additional ERO Enterprise stakeholders, including the ISO/RTO Council (IRC), the National Rural Electric Cooperative Association and the Electric Power Supply Association, participated in the comment period for CISA’s Notice of Proposed Rulemaking that concluded last week. The agency opened the comment period in April with an initial 60-day deadline, which later was extended to 90 days. (See CISA Seeks Comment on Proposed Cyber Reporting Rules.)

The NOPR stems from the Cyber Incident Reporting for Critical Infrastructure Act (CIRCIA), passed in 2022, which requires entities in critical infrastructure sectors — including energy — to report relevant cyber and ransomware incidents to CISA within 72 hours. CIRCIA left to CISA the authority for defining which incidents would be subject to reporting and which additional sectors, if any, the requirements would cover.

In its proposal, CISA said it would use the authority granted by the law to “fill … key gaps in the current cyber incident reporting landscape” and create a “comprehensive and coordinated approach” to cyber incident reporting.

The NOPR included a web-based form that would be the only official option for submitting incident reports, along with definitions of key terms such as “cyber incident,” “covered cyber incident” and “information system.” It also proposed details of content to be included in incident reports, such as whether victims requested assistance from other entities and their engagement with law enforcement agencies related to the ransomware or cyberattack.

NERC’s response to CISA noted that the ERO’s Critical Infrastructure Protection (CIP) reliability standards already address cybersecurity risks, including requirements for reporting cyber incidents to both the agency and the Electricity Information Sharing and Analysis Center (E-ISAC). Along with the CIP standards, electric utilities also are required to report certain cyber and physical security incidents to the U.S. Department of Energy through Form OE-417; entities may submit their OE-417 reports to the E-ISAC in place of CIP reports.

The ERO said “there are many commonalities between” the CIP reporting requirements, OE-417, and the proposed CIRCIA requirements. Noting CISA’s statement that it is “committed to working with DOE, FERC and NERC” to allow entities to comply with all three reporting regimes through a single report “to the extent practicable,” NERC said it “looks forward to working with its government partners to explore options to reduce regulatory burden and avoid unnecessary duplication.”

NERC also requested that CISA provide a mechanism for sharing CIRCIA reports with the E-ISAC and its counterparts in other industries. The ERO said that “ISACs are uniquely positioned … to amplify CISA’s analysis throughout their respective sectors and to enrich [it] with sector-specific information.”

“The E-ISAC understands that in certain instances there may be privacy-related concerns with sharing attributable information with ISACs without the consent of the submitting entity,” NERC said. “The E-ISAC respectfully requests that CISA develop a process for obtaining consent for sharing attributable information and, where that is not possible, removing identifiable information from the reports and its analysis to be able to share relevant information with ISACs and their members free of any security and privacy-related issues.”

Other Stakeholders Respond

Like NERC, the IRC encouraged CISA to “continue its education, outreach, and collaboration efforts” with NERC and the E-ISAC, other government agencies, and the ISOs and RTOs, specifically by soliciting stakeholder input on future information sharing agreements implemented under CIRCIA. In addition, the IRC suggested CISA hold a technical conference on the design of its web-based reporting form.

EPSA expressed concern about the proposed rule, calling it “extremely broad” and warning it may require “more extensive reporting than the detailed regimes under which EPSA members currently operate.” The association urged CISA to refine its definition of “covered cyber incident” to avoid requiring reports on “less critical incidents” that might take up entities’ time and resources unnecessarily.

NRECA also described CISA’s proposal as too broad, saying it applies “to all electric utilities regardless of size, location or resources, [which] includes hundreds of small distribution cooperatives that serve a relatively small number of meters.” This broad applicability “exceeds Congress’ intent in the CIRCIA legislation,” NRECA said, suggesting CISA limit its criteria to be risk-based so it covers entities that can provide the “most relevant and actionable information.”

A new report predicts the U.S. offshore wind buildout will fall short of President Biden’s 30-GW-by-2030 goal despite investment of a projected $65 billion over the next six years.

The American Clean Power Association’s 2024 Offshore Wind Market Report projects the 30-GW milestone will be reached in 2033 and that only 14 GW will be operational by 2030.

The industry ran into serious problems with costs, component availability and infrastructure just as it was gaining some momentum in the United States with the help of federal and state policymakers.

Contracts for numerous projects were canceled, injecting uncertainty and delays into their construction timelines.

But ACP sees a bright future for offshore wind in the United States:

A total of 56.3 GW of capacity is in some stage of development in 37 leases, and the U.S. Bureau of Ocean Energy Management plans to hold four auctions this year for 1.9 million acres of federal waters that hold a potential capacity of more than 20 GW.

BOEM has greenlighted 12 projects in nine lease areas and is reviewing seven other projects.

Offtake agreements are in place for 12 GW of electricity generated offshore, and active solicitations underway in the Northeast could yield 8.8 GW to 12.2 GW of additional contracts in the second half of this year.

South Fork Wind, the first utility-scale offshore wind farm, was commissioned this year and three larger projects with a combined capacity of 4 GW — Coastal Virginia Offshore Wind, Revolution Wind and Vineyard Wind — are under construction.

Infrastructure investment announcements now exceed $9 billion, with $3 billion in 2023 alone; more than 40 new support watercraft are on order or under construction, including two types of installation vessels.

The sector is projected to support 56,000 U.S. jobs by 2030.

In a news release July 9, ACP Chief Policy Officer Frank Macchiarola said:

“After the successful startup of the 132 MW South Fork wind farm earlier this year, and with 136 MW operational at Vineyard Wind, offshore wind is gaining momentum with three projects under construction and 37 more in development. Harnessing America’s offshore wind resources will boost economic activity, create jobs, reduce pollution providing environmental and public health benefits, and strengthen America’s energy security by enhancing grid reliability and energy independence.”

ACP in its announcement did not mention the possibility of a second presidency for Donald Trump, an outspoken wind power opponent.

November election notwithstanding, there are some bright points ahead in 2024:

New Jersey’s fourth offshore wind solicitation is active.

New York plans a dual solicitation this year — one for offshore wind farms, one for supply chain investments to support offshore construction and operations.

Connecticut, Massachusetts and Rhode Island expect to announce the results next month of a joint solicitation for up to 6 GW of new projects.

BOEM plans lease auctions in the Central Atlantic region in August, the Gulf of Mexico in September, and Oregon and the Gulf of Maine in October.

Construction is expected to begin on Sunrise Wind.

FERC has approved ISO-NE’s proposal of a new process to solicit, select and allocate costs for transmission projects that address needs identified in long-term planning studies (ER24-1978).

Developed in coordination with the New England States Committee on Electricity, the new process establishes a regionalized cost-allocation method for transmission projects that are projected to bring long-term net benefits to the region. (See NEPOOL TC Approves Process for States’ Transmission Needs.)

FERC Chair Willie Phillips and Commissioner Mark Christie concurred with the July 9 order in separate statements. Phillips commended the proposal and wrote that it does not conflict with Order 1920. Christie applauded the central role of the states within the proposal and contrasted it with Order 1920, which he argued needs “major revisions.”

The approval marks the completion of Phase 2 of ISO-NE’s longer-term transmission planning project; Phase 1 created a process to evaluate long-term transmission needs associated with state policies and mandates and was approved by FERC in 2022 (ER22-727).

In the new process, NESCOE can direct ISO-NE to issue a request for proposals for solutions to long-term needs. After soliciting proposals, ISO-NE will select a preferred solution, and NESCOE will have the option to either proceed with the default regionalized cost allocation method, submit an alternative cost-allocation method or terminate the process.

For projects to be eligible for selection, ISO-NE’s analysis must indicate the quantified benefits of the project outweigh its costs.

FERC also approved a supplemental process the states can use if no proposal exceeds the cost-benefit test, allowing one or more states to cover any costs of a project that exceed this cost-benefit threshold.

FERC wrote that the tariff changes “represent a just and reasonable alternative voluntary process that will not conflict with or otherwise replace ISO-NE’s Order No. 1000 regional transmission planning process.”

While the comments submitted to FERC on the proposal largely were supportive, some stakeholders argued the requirement for proposals to be complete — not reliant on any additional transmission upgrades from incumbent transmission owners not included in the proposal — equates to a de facto right of first refusal. (See Stakeholders Support ISO-NE Long-term Tx Planning Filing, with Caveats.)

FERC ultimately rejected arguments by clean energy trade groups and merchant transmission developers that the new process would give an unfair advantage to incumbent transmission owners.

Since the process is supplemental to ISO-NE’s regional transmission planning process required by Order 1000, it “need not comply with the nonincumbent transmission developer reforms established in Order No. 1000, including the requirement to eliminate any federal right of first refusal,” FERC wrote.

At the request of ISO-NE, FERC also directed the RTO to submit an additional filing to fix errors in the original submission.

Phillips wrote in his concurrence that the new process is not in conflict with Order 1920 and that it “includes many of the significant components of Order No. 1920, such as multifactor planning on at least a 20-year time horizon, an ex ante default cost allocation method, the option for states to agree on alternative cost allocation methods and the option to voluntarily pay for the portion of a project that exceeds the identified benefit-cost ratio.”

“The state role in this proposal is utterly contrary to the insufficient one allowed in Order No. 1920, which does not require that states consent to planning and selection criteria, does not require that states consent to an ex ante cost allocation formula, and does not even require that transmission providers have to file a state-agreed alternative to an ex ante formula,” Christie wrote.

Christie noted the strong state support for the proposal and argued it eventually could be undercut by the requirements of Order 1920, which is on track to “force all projects, including public policy related projects, into the same bucket with other types of projects for planning and cost allocation purposes.”

Christie concluded that the proposal “is the type of planning and cost allocation construct for public policy projects that the commission should encourage and approve,” and called for reforms to Order 1920.

Dominion Energy announced July 8 that it is positioning itself to potentially build another wind farm near its Coastal Virginia Offshore Wind.

It has agreed to buy the lease area where Avangrid’s Kitty Hawk North has been in the planning stages.

As part of the deal, Dominion would rename it CVOW-South. Avangrid would retain rights to the Kitty Hawk name, and plans to continue developing the adjacent lease area, which it calls Kitty Hawk South.

The deal requires the approval of the U.S. Bureau of Ocean Energy Management and the city of Virginia Beach. The two companies expect to close the transaction in the fourth quarter of 2024.

The deal is valued at about $160 million, which is substantially more than the original lease price but reflects development expenditures in the seven years since the auction.

In a March 2017 BOEM auction, Avangrid Renewables LLC beat out three other bidders in 17 rounds with a $9.07 million bid for the 122,405-acre lease area designated OCS-A 0508 and began planning what it called the Kitty Hawk Offshore Wind Project.

In 2022, Kitty Hawk Wind LLC divided it into two projects in two areas: Kitty Hawk North in the newly designated OCS-A 0559 and Kitty Hawk South in the remainder of OCS-A 0508.

In the construction and operations plan submitted to BOEM, Kitty Hawk North is proposed to have up to 69 wind turbine generators, one offshore substation, one onshore wind station and export cables making landfall in Virginia Beach. It would stand 24 nautical miles off the northern part of the barrier island that forms the North Carolina coastline.

Kitty Hawk South and Kitty Hawk North still have a long way to go in their permitting processes, and they need to overcome local opposition.

In late 2023, the city of Virginia Beach rejected the cable landfall routing. Three months later, Avangrid appealed to the region’s pocketbook, issuing a 29-page report estimating that the two Kitty Hawk projects would bestow a $4.8 million economic benefit on Virginia over their operational lives and that a quarter of that would flow to Virginia Beach, which would reap $274 million in tax payments alone.

Dominion said if CVOW-South were approved and built, it would have a roughly 800-MW capacity and would feed into the Dominion transmission grid. It offered no estimates of in-service date or construction budget.

Both companies acknowledged the potential roadblock in Virginia Beach.

Dominion said it’s aware of community concerns about the export cable’s proposed landing site and is committed to working closely with the community, the city and the state.

Avangrid said Kitty Hawk South could generate up to 2.4 GW of power and could be delivered to North Carolina, other states or private companies, not just to Virginia.

The two companies already have steel in U.S. waters, and both can lay claim to the mantle of “largest.”

Avangrid owns 50% of Vineyard Wind 1 under construction off the Massachusetts coast. With 10 turbines connected to the grid, it is by a tiny margin the largest offshore wind farm by capacity in the United States.

Dominion owns 50% of CVOW, which with a nameplate rating of 2.6 GW is by far the largest offshore wind farm approved in the United States.

Dominion CEO Robert Blue said in a news release: “With electric demand in our Virginia territory projected to double in the next 13 years, Dominion Energy is securing access to power generation resources that ensure we continue to provide the reliable, affordable and increasingly clean energy that powers our customers every day.”

Avangrid CEO Pedro Azagra said in a news release: “As Avangrid continues the construction of our nation-leading Vineyard Wind 1 project and the development of our diverse portfolio of offshore and onshore renewable projects, this transaction advances our strategic priorities by providing significant capital infusion for reinvestment.”

FERC on July 5 approved LS Power’s purchase of an 810-MW natural gas plant in central Pennsylvania despite some qualms from PJM’s Independent Market Monitor (EC24-42).

The deal has LS Power setting up an affiliate, Hunterstown Gen Holdings, to buy the plant, which was owned by Kestrel Acquisition, a subsidiary of the investment firm Platinum Equity Partners.

LS Power already owns 6,865 MW of electric generating capacity, but the merger would raise the Herfindahl-Hirschman Index (HHI) of market concentration by only 12 points, which is not meaningful when a market qualifies as concentrated starting at 1,000 points on the index, Kestrel said in its application. Once the deal closes, LS Power will control 7.17% of installed capacity, its analysis showed.

The Monitor argued FERC should take into account different local markets, which are changing frequently along with transmission congestion and more accurately reflect the operation of PJM’s wholesale power markets.

The merger increases LS Power’s structural market power in the aggregate energy market and the capacity markets as well, the Monitor said. It argued for some restrictions on LS Power’s bidding to get around those issues, which would have dealt with market power concerns.

LS Power and Platinum argued the Monitor failed to show the deal is inconsistent with FERC policy or precedent and that its claims are based on a nonpublic dataset that is not available for evaluation.

FERC agreed the Monitor failed to offer enough evidence that it should use smaller geographic markets based on congestion. Some of the constraints are in place for just 100 hours a year, which FERC has said is too low to show the persistence the commission requires for a new submarket to be considered.

Others are well above that threshold, but FERC said the Monitor failed to provide enough information for the potential boundaries of a new submarket around the Nottingham transmission constraint in its analysis. The Monitor also used the three-pivotal-supplier test, which is important for market power in PJM, but FERC said it never has used it in a merger case.

Increasing LS Power’s market share from 6.71% to 7.17%, while increasing the HHI by just 6 points, shows the deal will have a limited impact on the aggregate energy market, FERC said.

“With respect to the PJM IMM’s request that the commission impose behavioral mitigation measures, we decline to require the requested mitigation measures or to otherwise address general issues concerning the PJM markets in this proceeding,” FERC said.

Broad arguments about the inadequacies of FERC’s merger review process and PJM’s market power mitigation are the basis for the Monitor’s requested behavioral limits. But “as the commission has previously found, arguments based on general concerns about certain elements of PJM’s market design that are not specific to a proposed transaction under review are beyond the scope of the commission’s review of the proposed transaction,” FERC said.

None of the parties raised issues with the deal’s impact on vertical market power, rates or regulation, and the deal did not raise issues around cross-subsidization, the commission found.

Commissioner Mark Christie concurred with the order, agreeing the deal satisfies FERC’s merger review process while also saying the Monitor highlighted a real issue.

“Taken together, the PJM IMM’s evaluation and conclusion signal that the commission’s policy and regulations implementing [Federal Power Act] Section 203 may miss the forest for the trees and fail to see the larger impacts that transactions may have on the health of RTO markets,” Christie said.

Christie added that he would welcome a review of FERC’s policies that implement Section 203.

ARLINGTON, Va. — Industry leaders, experts, policymakers and regulators gathered near the nation’s capital June 25-27 to discuss how recent FERC orders will affect regional transmission planning, cost allocation, permitting, advanced transmission technologies and other factors that could improve the ability to quickly add capacity to the grid.

Over the last two years, FERC has issued several orders designed to revise transmission planning, cost allocation and permitting processes, including:

Order 2023, which revises the commission’s pro forma generator interconnection queue rules to speed up the backlogged process. It has already led to a flurry of interconnection and queue reforms by grid operators and utility balancing areas. (See FERC Updates Interconnection Queue Process with Order 2023.)

Order 1977, which implements FERC’s new congressionally mandated authority to site transmission lines in a National Interest Electricity Transmission Corridor, despite state regulators’ rejections.

While the actions have begun to bear results, the extent of the reforms and their pace vary significantly in the nation’s organized markets.

Joseph Rand, an energy policy researcher at Lawrence Berkeley National Laboratory, kicked off the summit by sharing the lab’s annual analysis of interconnection data from all seven RTOs and ISOs and 44 non-RTO utilities, representing more than 95% of the U.S.’ currently installed capacity.

The report found potential new capacity in interconnection queues is growing dramatically, with nearly 2.6 GW of total generation and storage seeking connections to the grid last year. More than 95% of that capacity is for zero-carbon resources. Solar and battery storage are the fastest-growing resources, accounting for over 80% of new capacity entering queues last year.

“I’ve been working in the energy and electric industry for maybe about 15 years now, and I don’t often get to use the unit of terawatts. One terawatt — my mind was blown,” Rand said. “Then we got to 2 TW last year and now we’re at 2.6 TW, and my mind continues to be blown by this number.

“To put that in context a little bit,” he added, “that’s actually more than two times the installed capacity of our entire electric generation fleet in the United States.”

Rand urged attendees not to place too much importance on recent industry chatter regarding concerns with load growth, resource adequacy, data center energy needs and the impulse to quickly build gas generation. He said there’s enough capacity in grid operators’ queues to meet rapidly increasing load.

“I think that kind of indicates that, again, it’s not necessarily a need to kind of shove through a lot of generation,” he said. “There’s, in fact, a need to kind of unlock this bottleneck that we’re seeing in the interconnection process to meet that resource adequacy. But, like I just alluded to with the word ‘bottleneck,’ we have some problems in this process, right?”

The chief problem, Rand said, is the “very low” completion rates for projects. He said researchers have found that only about 20% of projects that enter queues reach commercial operation and over 72% have withdrawn their applications.

Not that low completion rates are “entirely a bad thing,” Rand said.

“Low completion rates could be a sign of a very active and competitive interconnection process and a competitive market,” he said. “But on the other hand, when you see very low completion rates, those of you from ISOs and RTOs could probably attest to this, it’s really a drain on transmission provider resources to have to study all of these requests. It might be an indicator of so-called exploratory or speculative requests being in this process.”

The other problem? Timelines, especially in FERC-jurisdictional regions, and the rising cost of interconnections.

“This stuff matters and it’s important and it’s why interconnection is sort of top of mind and getting headlines in The New York Times these days,” Rand said.

ERCOT Offers GI Lessons

If there’s a model to ease the bottlenecks in GI queues, it could be ERCOT’s “connect and manage” approach to transmission interconnection. The Texas grid operator focuses its studies on the local upgrades needed for a project to connect to the grid. It manages grid congestion caused by a new generator through market redispatch and curtailment.

ERCOT has added more generation to its system than any other grid operator and transmission provider during the last few years. It connected 14.2 GW of capacity during 2021 and 2022. PJM, with demand twice as large as ERCOT’s, added 5.6 GW during that same period. ERCOT says its lack of FERC jurisdiction status allows it to energize transmission lines in three to six years, compared to seven-and-a-half to 13 years elsewhere.

During a panel discussion on the “connect and manage” approach, Mario Hayden, Enel North America’s transmission director and a former ERCOT staffer, said familiar concepts in other regions get thrown out the window in the grid operator.

“There’s no such thing as a queue priority, which is sort of a fundamental concept in other parts of the country. There’s no sense of other readiness milestones, the concept of site control being a big barrier of entry,” he said. “You do not have a sense of withdrawal penalties, a sense of harming your competitors next to you, direct-cost allocation as a part of the negotiating process, but no idea of transmission upgrades that may cause high costs and make people want to withdraw.

“If you’re a lucky generator, the process is fairly simple,” Hayden said.

Except allocated transmission costs come later. Zero Emission Grid founder Mike Tabrizi said that without a cluster-study process, developers are connecting to the grid at their own risk.

“You’re not going to be responsible for transmission operating costs upfront but once the project becomes operational, then you’re fully exposed to what’s going to happen to the transmission from the congestion … especially if you’re a network resource,” he said.

“[ERCOT lacks] any sort of proactive transmission planning which, as we’ve seen, there can be [generation transmission constraints] that pop up and that will lead to cascading outages if they’re not managed properly,” Pine Gate Renewables’ Regan Fink said, referring to ERCOT’s South Texas constraints.

Tyler Norris, formerly with Cypress Creek Renewables and now working on a doctorate at Duke University, calls the ERCOT’s use of curtailment for renewable energy “flexible interconnection,” although he would prefer the curtailment be “occasional.”

“Once you’ve decided to use the interconnection process to identify and allocate funds for network upgrades, that introduces a lot of complications and sort of the fundamental linkage that we’ve made as we have linked interconnection service to capacity eligibility,” he said. “That’s sort of what I think is driving a lot of the issues that we’re seeing in our interconnection queues.”

FERC staff have scheduled a workshop Sept. 10-11 on GI innovations and efficiencies, Norris noted. He expects flexible interconnection options to be part of the discussion.

“There’s ever more pressure to get more generation on the system,” Norris said. “The FERC staff generally really get that there are a lot of colliding trends. … FERC will be interested in exploring reform options for energy-only interconnection service and provisional service to streamline them and make them more aligned with generator willingness to be curtailed, to get online more quickly.”

More Transmission Coming

A panel discussing the effects of Order 2023’s compliance plans said many regional markets are already a step ahead of FERC. That and competition between the states will continue to lead to strong projects, they said.

Matt Pawlowski, vice president at NextEra Energy Transmission and a “transmission guy” who wants to “build more transmission,” pointed to reforms SPP has made in its GI process to eliminate a backlog of project requests that dated back to 2017. The RTO hopes to clear all requests submitted through 2022 by the end of this year. (See “Staff Reveals Error in GI Queue Studies; Clearing Backlog Still on Course,” SPP Markets and Operations Policy Committee: April 16-17, 2024.)

“[SPP’s reforms] increased site control requirements, increased study deposits and more at-risk study deposits. We supported that because we felt like that would create stronger projects in the interconnection queue,” Pawlowski said. “It certainly sharpened the pencils on our side for ensuring other projects that get into the queue are some of our top projects that we’ve that we’re looking at from both from a demand standpoint, but also from site control and other aspects. Having a little bit more stringent requirements … just forced developers to just think harder about their projects.”

Bill Bojorquez, a former ERCOT executive and now CEO of technology firm Splight, said competition between states for transmission solutions has increased, with siting decisions “taken in by more and more regulatory and government forms.”

“If they don’t do something, we’ll have transmission in other states, wherever is more proactive in justifying that addition,” he said.

“I can’t agree with you more,” Pawlowski said. “I think the states that are being proactive right now in thinking about economic development first and then the steps that are needed in order to fulfill those jobs and economic development plans are going to win. [States] like Oklahoma and California, with some of their plans, are recognizing these. These [massive data centers and cloud infrastructure] want to be close to eyeballs and there are certain areas that they want to pick. If you’ve got them in that area and you don’t have the ability to serve them, they will go somewhere else, because they don’t have the power needs that serve them. It’s as simple as that.”

Allocating Costs the Issue

Finding herself sitting next to FERC senior energy industry analyst David Tobenkin, North Dakota Commissioner Sheri Haugen-Hoffart, an apparent opponent of Order 1920, was quick to respond after his explanation of the order and the states’ role in its cost allocation.

“For full disclosure, when David sat down, he said, ‘Be nice.’ I said, ‘I promise. I will,’” she said as Tobenkin allowed himself a smile. “But I kind of have to give you a look. 1920?”

“We are an export state. We have different challenges compared to other states, but cost allocation — and I wish I wrote down every time I heard cost allocation is challenging — is very challenging and complex,” Haugen-Hoffart added. “We have viewed it in North Dakota as cost-causation principles must be a year two, transmission and interconnection investment caused by companies that state a desire to new generation, regardless of type, should be paid by those parties, the cost causers. To allocate costs of such investment to all customers, in particular RTOs, we see as unjust and unreasonable.”

Yes, allocating costs for transmission is tricky, said WIRES’ executive director, Larry Gasteiger.

“The two biggest obstacles we keep seeing with getting transmission built, and this is really a gross oversimplification, are nobody wants to see it and nobody wants to pay for it,” he said. “Believe me, I get it. We’re talking about a lot of investment. We’ve got a lot of policies going on concerning the issues of paying for this infrastructure, and frankly, it’s going to cost a lot of money.

“I think it’s going to require a conversation and being more honest with ratepayers about what we may be seeing down the road,” Gasteiger added. “That doesn’t mean we don’t look at ways to try to minimize the costs associated with building this infrastructure, absolutely. We have to do that. But we’re not going to cheap our way out of this.”

Speaking on a panel focused on grid-enhancing technologies (GETs), EDF Renewables’ Temujin Roach shared similar opinions.

“People are going to start talking about transmission. It’s become a bigger and bigger issue because it’s going to become a bigger part of their bill. Before it was just pennies. Nobody cared about whatever transmission is,” Roach said. “Now, it’s that much more, so we’ve got to find a way to cut some of the costs while we’re increasing the costs, because we are going to increase the cost. It is going to cost more. We are going to have to charge people to build this transmission, period. So now it’s about how can we manage the cost?”

Clements’ Contributions Recognized

Conference organizers thanked outgoing FERC Commissioner Allison Clements, making her annual appearance to the Infocast summit on her penultimate day on the job, for being “a champion of the industry.”

The WATT Coalition went one better, presenting its 2024 Grid Innovation Champion Award to Clements for being “a true leader in embracing innovation” and advancing transmission technology policy at FERC.

“[Clements] has looked for opportunities to use common-sense solutions like [GETs] to support the FERC’s mission to ensure just and reasonable rates and reliable power,” WATT Chair Hilary Pearson said. “The WATT Coalition thanks Commissioner Clements for taking the time to understand the value of [GETs] on the transmission grid and for consistently advocating for policy to address the structural barriers to grid modernization … we hope her colleagues on the commission will carry forward after her term ends.”

Clements has been an outspoken supporter of GETs. She has praised the technologies in FERC Orders 881 and 2023, in letters to legislators, and in her remarks at NARUC’s Federal-State Joint Task Force on Electric Transmission and other forums. (See FERC’s Clements Gets GETs’ Benefits to Grid.)

“I didn’t think I’d become a champion for grid-enhancing technologies. I didn’t know what one was, and I feel like this real Pollyanna running around cheering for this hardware and software,” Clements said. “But it kind of came on to me because you get one group come in and they say, ‘These are the actual results in savings. These are the actual congestion-cost savings that we got in one year. And this is how much it costs to put it in place.’

“And then you get the advanced conductor guys coming in and saying, ‘This is actually the difference you can make to what’s happening on the grid, whether it be related to sag and wildfire safety, whether it be to making more training or sending more electrons through what-have-you’ … the numbers are so staggering. I think there are pretty credible studies related to the opportunity that hardware and software have to create space and even especially to increase reliability,” she added.

A day before leaving FERC, Clements took solace in her award.

“This just means the world to me. I really appreciate it,” she said with a final commission meeting still on her schedule. “I’m going to take a long vacation and then I’ll be back cheering for grid-enhancing technologies in one capacity or another.”

The vacation began early. Clements stayed around after the ceremony, greeting well-wishers while clutching her award in one arm and a beer in her other hand.