New solar power surged to record heights in the U.S. in the first quarter of 2023, while energy storage slumped because of a major jump in the already-high number of megawatts sitting in interconnection queues across the country, according to recent reports from industry analyst Wood Mackenzie.

Solar had its best first quarter in the industry’s history, with installations of 6.1 GWdc, up 47% from a year ago, according to Wood Mackenzie’s latest Solar Market Insight report for the Solar Energy Industries Association. Further, solar accounted for 54% of all new generation on the grid in the first quarter.

Drivers for the year-over-year growth include a loosening of supply chain constraints, with a wave of formerly delayed projects being completed, and a rush of first-quarter residential installations in California ahead of the state’s new, lower solar compensation plan, called NEM 3.0, which went into effect April 15, the report says.

At the same time, the full impact of the solar tax credits in the Inflation Reduction Act has yet to really affect the market as installers continue to work through the Internal Revenue Service guidelines that have been issued to date. For example, project developers can get add-on credits for locating projects in “energy communities” — such as areas that have lost employment because of coal plant closures.

The IRS guidelines for the add-on credits are complex and still being issued, the report says.

Storage, on the other hand, added a modest 778 MW/2,145 MWh in the first quarter, down 26% from the fourth quarter of 2022, as reported in Wood Mackenzie’s Energy Storage Monitor for the American Clean Power Association.

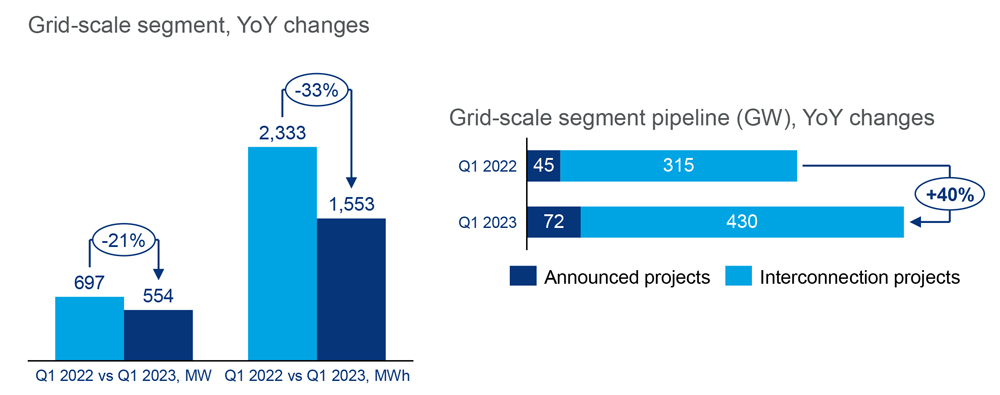

Year-over-year figures in the report are divided by sector, with grid-scale storage taking the biggest hit, declining 21% from Q1 2022, installing 554 MW this year versus 697 MW a year ago. The culprit here is the 40% increase in the new storage capacity added to interconnection queues, the report says, growing from 315 MW in Q1 2022 to 430 MW this year.

The report also notes that more than 1.8 GW of storage projects scheduled to come online in the first quarter have been delayed to later in the year.

Additions came from a 119% increase in the commercial and industrial sector, from 31.6 MW last year to 69.1 MW, and a smaller 7% gain in residential storage, from 145.1 MW to 155.4 MW.

The storage tax credits in the IRA are proving a mixed blessing, the report notes. While lithium-ion prices are down, to get the law’s full 30% tax credit, developers have to meet its requirements for prevailing wages and apprenticeship programs, which are raising labor and other costs.

Big Growth Ahead

Growth in solar and storage markets is seen as critical for President Joe Biden’s goal of decarbonizing the U.S. electric grid by 2035. While the uneven first-quarter results may cause some uncertainty, Wood Mackenzie still expects exponential growth for both sectors.

Solar capacity is expected to nearly triple over the next five years, from 142 MW to 378 MW. In addition, the IRA’s domestic content provisions — which link tax credits to panels with U.S.-made components — have spurred a growing list of announcements of new panel manufacturing in the U.S.

By the end of the first quarter, Wood Mackenzie was tracking 52 GW of new facilities that had been announced, with at least 16 GW under construction. The challenge for the sector is that even if assembled in the U.S., solar panels may not meet the IRA’s domestic content provisions, as manufacturing for other key components will likely lag, the report says.

“There is currently no silicon solar cell manufacturing located in the U.S., and these facilities take at least two to three years to build and ramp up production,” the report says. Only 20 GW of new cell manufacturing facilities have been announced since passage of the IRA, significantly less than the new solar panel capacity already announced, the report says.

Wood Mackenzie is also anticipating a drop in the California residential solar market — with a knock-on effect on national growth — because of NEM 3.0, which slashes the amount of compensation rooftop solar owners will get for the excess power they put on the grid.

While a backlog of installations in California will keep figures up in 2023, Wood Mackenzie expects residential installations in the state will drop 38% in 2024, reducing the national residential market 4%. Boosted by IRA tax credits, solar across other states is expected to grow 12%.

For storage, Wood Mackenzie predicts 75 GW of new capacity will be installed by 2027, up from the current figure of just under 11 GW. More than 80% of the new capacity will be utility-scale storage, the report says.

The growth may start slowly, with supply chain and interconnection roadblocks affecting the market this year and next, but will accelerate to make up for such delays in the following years, the report says.