Nearly 40% fewer U.S. solar power projects reached completion in the fourth quarter than in the third quarter as developers pivoted to start new projects in time to qualify for tax credits.

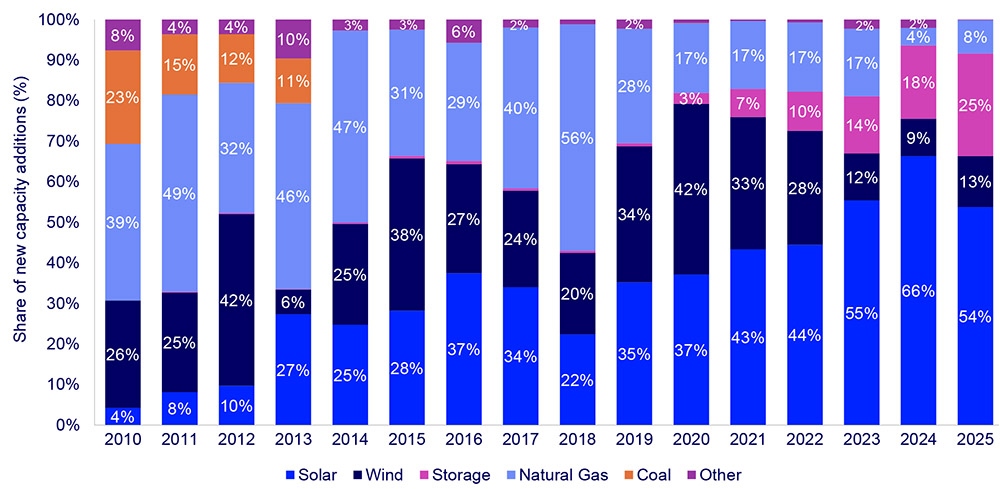

But while the 43.2 GW of solar capacity installed in 2025 was 14% less than in 2024, it nevertheless made up 54% of all new capacity added to the U.S. grid in 2025, the Solar Energy Industries Association (SEIA) and Wood Mackenzie said in a new report March 10.

2025 was the fifth straight year solar was the top source of new U.S. power generation capacity.

Looking ahead, the analysis predicts nearly 500 GW of additional photovoltaic capacity will be installed nationwide through 2036, even with the headwinds created by a president hostile to renewable energy. The costs of alternatives are high enough that solar remains a value proposition even without the lucrative investment and production tax credits that are being sunsetted sooner than originally planned.

“It’s clear that solar will continue to be the dominant source of new power capacity in the United States, even as gas generation continues to grow,” said Michelle Davis, head of solar at Wood Mackenzie and lead author of the report. “Strong demand growth combined with escalating costs of new gas plants will allow solar to remain competitive, even without tax credits.”

The “U.S. Solar Market Insight 2025 Year in Review” acknowledges the many uncertainties facing solar power. The baseline prediction of 490 GW more solar capacity by 2036 could be 11% higher or lower due to a series of factors, but the projected variation for utility-scale solar (6-7%) is much less than for distributed solar (23-28%).

Distributed solar is more sensitive to changes in retail rates and cost-impacting policies such as tariffs and import guidance, the authors state, while utility-scale projects are more likely to be affected by interconnection bottlenecks, supply chain constraints and power demand growth.

Another unknown factor is President Donald Trump.

Trump’s signature on the One Big Beautiful Bill Act in July 2025 moved forward the expiration of tax credits in the Inflation Reduction Act.

Projects now must start construction before July 4, 2026, or be placed into service by Dec. 31, 2027, to qualify for full tax credits. This led to significantly fewer completed projects in 2025 than expected — the value of completing them was outweighed by the imperative of beginning work on the next projects in the pipeline in order to safe harbor their tax credits.

While the president relentlessly boosts fossil fuels over renewables, he does not show the same level of hostility to solar panels as to wind turbines. There even have been a few hints in early 2026 of solar opposition softening among some MAGA influencers.

Whatever the motive for this turnaround, solar has some effective selling points in 2026: It is faster and less expensive to deploy than gas or nuclear; U.S. solar component manufacturing has expanded greatly; and battery energy storage systems to smooth out its intermittent performance are proliferating in number while decreasing in price.

SEIA interim President Darren Van’t Hof indicated that while the federal uncertainty has not gone unnoticed, it is not insurmountable: “Solar and storage continue to dominate new capacity additions to the grid despite policy headwinds. American households and businesses of all sizes are demanding solar + storage because they deliver fast, affordable power to help meet rapidly rising demand,” he said.

“Washington must deliver policy certainty for the market to work and to keep pace with growing energy demands. Without this certainty, less solar will get built and Americans will pay the price with higher energy bills.”

Even with this churn, all of Wood Mackenzie’s U.S. power projections show solar constituting nearly half of all U.S. capacity additions each year through 2060.

The 2025 outlook calls for an average annual addition of 44 GW through 2036, which is an increase over previous projections based on the increase in the near-term utility-scale pipeline and continued growth in energy demand expectations.