By Rich Heidorn Jr.

The 36% increase in prices in last week’s ISO-NE capacity auction likely represents the peak for the foreseeable future, analysts say.

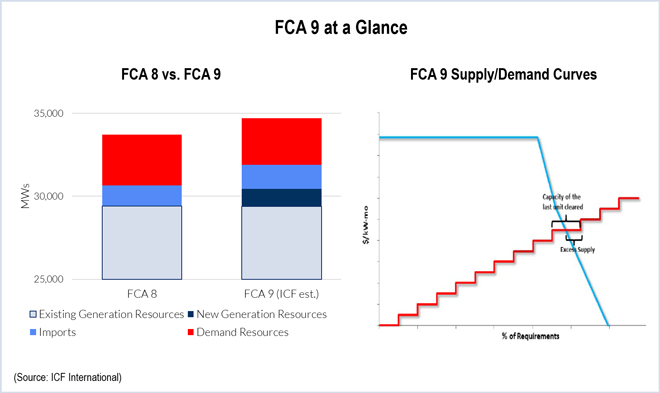

The ninth Forward Capacity Auction cleared at $9.55/kW-month — up $2.52 over FCA 8 — outside of the Southeastern Massachusetts-Rhode Island (SEMA) zone, where prices were administratively set at $17.73/kW-month for 353 MW of new resources and $11.08/kW-month for 6,888 MW of existing resources.

The auction cleared about 1 GW of new generators, which can lock in their initial prices for seven years. During the lock-in period, they take a place at the bottom of the supply stack as zero-bid price takers.

“All else being equal, we believe that in the upcoming auction … the clearing price will decrease and will be set by the de-list bids of existing generators,” analysts for ICF International said, estimating that about 300 MW of excess supply cleared the auction. “Assuming no change in any parameters from FCA 9 … the maximum impact of the excess capacity in FCA 10 prices will be around $2/kW-month. Depending on the de-list bids, the impact may be less.”

Analysts for UBS Securities agreed that last week’s results “[signify] the near-term ‘top’ of this market.”

“We estimate next year’s auction could tentatively be in the ~$6-7/kW-month range … seeing this as the level at which transmission backs out of the auction (1.028 GW of [New York] imports cleared at $7.97/kW-month) as well as expecting a continued decline in demand response,” UBS said.

They also predict that prices in the SEMA region will converge to the pool-wide average as the zone around Boston did this year.

Transmission Didn’t Clear Auction

Analysts said it appeared no transmission cleared last week. “It may be that the combination of transmission and generation costs are too high, the volumes required might be high or additional incentives associated with potential new CO2 regulations may be required to improve the economics of transmission projects,” ICF said. “Alternatively, some transmission projects may not have qualified.”

UBS said merchant transmission is a potential “wildcard” for future auctions, saying a project such as Eversource Energy’s (formerly Northeast Utilities) Northern Pass could offset as much as 400 MW of supply.

Demand Response Continues Contraction

Demand response, which cleared 3,041 MW in FCA 8, fell to 2,803 in last week’s auction, a drop of about 238 MW, or 8%, analysts said. ICF said about 600 MW of existing DR was de-listed while 367 MW of new DR resources — believed to be energy efficiency — cleared.

DR has been on a steady decline in New England’s capacity market since peaking at 3,645 MW in FCA 6.

In contrast, ICF said there appeared to be no significant de-listing of existing generators, indicating that their de-list bids were below clearing prices.

“This implies that existing generators believe that capacity prices are high enough to offset potential penalties from underperformance under the [Pay-for-Performance program] or that penalties will be adequately compensated by credits for performance under scarcity conditions,” ICF said.