ISO-NE on Tuesday advanced the idea of excluding competitive new resources from functioning as demand in a proposed “substitution” capacity auction, which is designed to enable generators with retirement bids that cleared in a primary Forward Capacity Auction to transfer their obligations to subsidized resources that did not clear because of the must-offer price rule.

The grid operator proposed the exclusion to help keep Forward Capacity Market prices competitive and maintain its “cash for clunkers” framework for retiring aging fossil fuel generators.

ISO-NE economist Christopher Geissler presented the RTO’s conceptual approach to Competitive Auctions with Sponsored Policy Resources (CASPR) to the New England Power Pool Markets Committee, which met Aug. 8-10 at Cape Neddick, Maine.

CASPR is designed to accommodate the entry of “sponsored” resources — such as resources mandated by a renewable portfolio standard or other state policy — into the FCM over time, while maintaining competitively based capacity prices for other resources. The RTO’s latest proposal comes in response to stakeholders concerned that sponsored policy resources could unfairly reduce primary FCA prices and crowd out competitive generation. (See Public Power Skeptical of ISO-NE Two-Tier Capacity Auction.)

Part of the grid operator’s Integrating Markets and Public Policy (IMAPP) initiative, the latest proposal is intended to head off stakeholder concerns about competitive resources “walking down the demand curve” of the FCA by ensuring that the substitution auction coordinates entry of sponsored resources and exit of older generators.

To limit the potential ability of public entities to reduce consumer costs by sponsoring lower-cost (e.g., combined cycle/combustion turbine) resources, stakeholders had suggested imposing additional restrictions on the types of capacity eligible to participate as supply or requiring additional documentation to show that the resource was being built to meet a public policy need.

ISO-NE said it does not plan to propose rules that would require the RTO to evaluate whether a sponsored resource meets public policy needs. The grid operator said its two-tier auction proposal “incents the continued participation of competitive new resources in the FCM, when market conditions allow.”

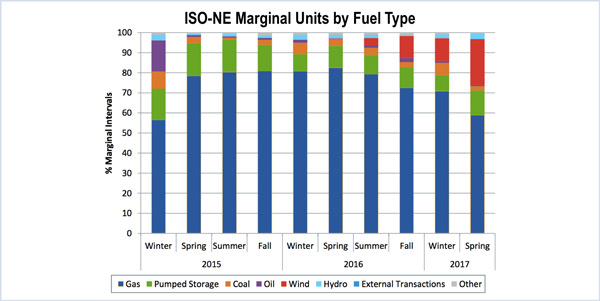

IMM: Spring 2017 Energy Costs up on Gas Prices

Higher natural gas prices drove ISO-NE wholesale market costs up 26% this spring compared with a year earlier, to $1.3 billion.

ISO-NE Director of Market Monitoring and Compliance Robert Laurita presented the Internal Market Monitor’s Spring 2017 Quarterly Markets Report, attributing most of the gas price increase to March, when gas prices jumped 127% from the same month in 2016 because of significantly colder temperatures.

Gas prices averaged $3.59/MMBtu, up 54% compared with spring 2016, which saw unusually low prices because of increased production, above-average storage and low heating demand during the winter. Spring 2017 gas prices were 18% below 2015 levels.

Hourly electricity demand averaged 12,853 MW, comparable to last spring because of similar weather conditions, the report said. March was unseasonably cold, while April and May saw slight reductions in load compared to the same months in the previous year.

Day-ahead and real-time energy market prices at the New England Hub averaged $30.78/MWh and $31.92/MWh, respectively, up 32% and 44% from last spring. Energy prices continued to closely track underlying natural gas prices. The positive deviation in real-time prices for the period was driven by several days with high loads and unit outages during early April, as well as two days in mid-May when high temperatures resulted in higher loads than forecasted. In addition, several units experienced forced outages.

Northern Discounts

Energy prices among the load zones deviated only in Maine, New Hampshire and Vermont, which had lower average prices than the hub. These discounts were the largest — in both dollar and percentage terms — over the two-and-a-half-year period assessed by the Market Monitor. Discounts from the hub ranged from 6% in Vermont to 16% in Maine.

The report attributed the differentials to the prevalence of renewable generators in those export-constrained areas, as well as “various planned and unplanned line reductions or outages during the period that further reduced the transmission capability available to export power to the rest of the system.” The discounts were “less pronounced” in the day-ahead market.

Real-time reserve payments for the season totaled $8.9 million, well more than last spring’s total of $700,000 and 33% above the 2015 total of $6.7 million. This spring’s payments primarily accrued over May 18-19, which accounted for 54% ($4.8 million) of the credits. Those two days saw the grid operator frequently redispatch generation to maintain reserves. Deficiencies several times triggered the reserve constraint penalty factors for 10-minute spinning reserves and 30-minute operating reserves.

FCA Payments Stable

Spring 2017 coincided with the last three months of the commitment period associated with FCA 7, in which the NEMA-Boston zone cleared at $15/kW-month for new resources and $6.66/kW-month for existing resources, while Rest-of-Pool cleared at the floor price of $3.15/kW-month. Capacity payments for the season totaled $287 million and were within 1% of spring 2016 payments. Peak energy rent adjustments remained relatively high at $26 million because of the high real-time energy prices occurring in August 2016.

ISO-NE in April held the forward reserve auction for the summer 2017 delivery period, which saw supply offers exceed the requirements for both the 30-minute operating reserve and 10-minute non-spinning reserve, with no pivotal suppliers. The clearing prices for offline 30- and 10-minute reserves for the control area were $1,000/MW-month and $2,000/MW-month, respectively. Summer 2016 10- and 30-minute reserves cleared at $2,000/MW-month and $2,498/MW-month, respectively. Of the three local reserve zones, only NEMA/Boston had a different price than the control area. Because of inadequate supply (meaning all suppliers were pivotal suppliers), the 30-minute reserve price for NEMA/Boston was set to the auction’s offer price cap of $9,000/MW-month, the same outcome as the summer 2016 auction.

— Michael Kuser