By Rory D. Sweeney

PJM’s markets were competitive in the first nine months of the year and energy prices were up $1/MWh compared to the same period last year, the Independent Market Monitor found in its quarterly State of the Market Report.

“Energy prices in PJM in the first nine months of 2017 were set, on average, by units operating at, or close to, their short-run marginal costs, although this was not always the case during high-demand hours,” the report said. “This is evidence of generally competitive behavior and resulted in a competitive energy market outcome.”

The load-weighted, average LMP in PJM was 3.5% higher in the first nine months of 2017 than during the same period in 2016, rising to $30.36/MWh. The Monitor said the increase was “primarily” due to higher fuel prices.

Coal and natural gas costs rose faster than electricity prices, undercutting generator revenues. Average energy market revenues decreased by 51% for new gas-fired combustion turbines, 28% for new combined cycle units and 17% for a new coal plant, while increasing 6% for nuclear units, the Monitor said.

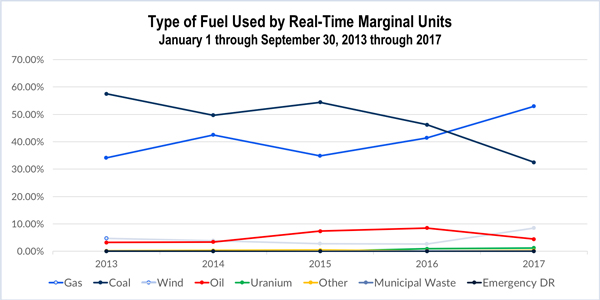

Coal units’ dominance has dipped over time, while gas has risen. In 2008, coal represented 75% of the marginal resources and gas 20%. In the first nine months of this year, coal stood at 32.5% and gas rose to 52.9%, the Monitor said.

Wind continued to depress prices as the marginal unit. In the first nine months of 2017, 74.1% of the wind marginal units had negative offer prices, 18.9% had zero offer prices and 6.9% had positive offer prices.

Total energy uplift charges decreased $16 million (15.7%) to $86.3 million during the nine-month period. Demand response payments also decreased by $167.2 million (31.1%) to $370.6 million, while congestion costs fell $366.8 million (44.6%) to $455.4 million.

The impact of FERC’s ruling on balancing congestion — rejecting the notion that financial transmission rights are only intended to benefit load — was also evident this year. Revenues from auction revenue rights and FTRs offset 98.1% of total congestion costs for load during the 2016/2017 planning period, but only 79.7% of those costs for the first four months of the 2017/2018 planning period. In January, FERC accepted PJM’s compliance filing in response to the commission’s requirement that the RTO develop a method for allocating ARRs that doesn’t consider extinct generators. Under the new rules, PJM assigns balancing congestion to real-time load and exports and regularly updates its ARR allocations to reflect generator retirements. (See FERC Accepts PJM’s FTR Plan, Rejects Rehearing Requests.)