The U.S. solar market may face major domestic supply chain gaps as it heads toward 2030, as incentives from the Inflation Reduction Act spur solar panel manufacturing but leave those factories dependent on imported solar cells, according to a report released July 9.

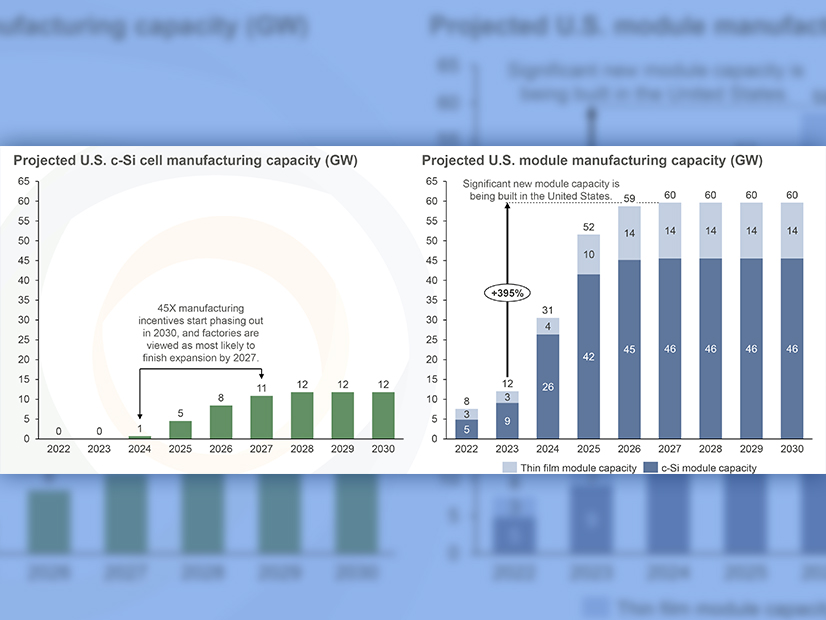

A joint project of the American Council for Renewable Energy and Clean Energy Associates (CEA), the report estimates U.S. factories may be producing 60 GW of solar panels per year by 2030, but only about 12 GW of solar cells. Further, 97% of the imported solar cells needed to make up the difference are subject to existing solar tariffs, and some soon could have additional duties slapped on them.

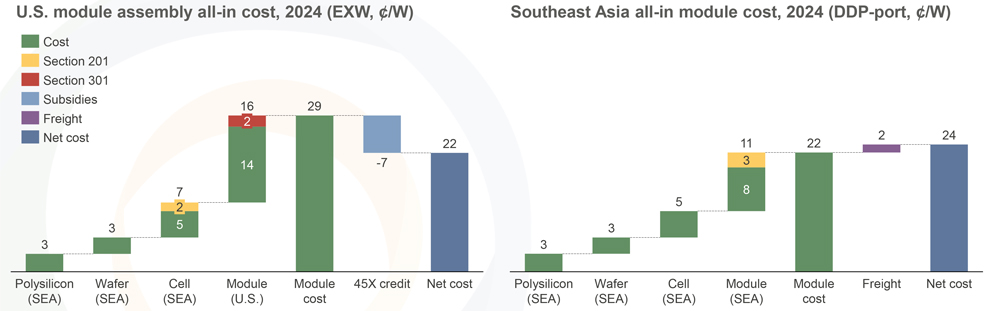

If those new duties are imposed, CEA predicts prices for domestically produced solar panels made with imported cells could increase by 10 cents/W, while the price for imported panels could go up 15 cents/W.

“Tariffs increase capital costs, and when you talk about increasing capital costs, [that] increases the cost of delivering electricity, and that of course is going to have an impact on demand” and the country’s ability to meet its greenhouse gas emission-reduction goals, said Daniel Shreve, vice president of market intelligence at CEA.

But during a July 9 webinar launching the report, Shreve said that even with new tariffs and the variability in location and logistics of specific projects, utility-scale “solar is going to be extraordinarily competitive and the lowest-cost source of electricity in most situations,” compared with often volatile natural gas prices.

The report comes just weeks after the end of President Joe Biden’s two-year moratorium on solar tariffs on cells and panels from Cambodia, Malaysia, Thailand and Vietnam. Biden established the moratorium in June 2022, during an International Trade Commission (ITC) investigation of whether imports from those countries were using Chinese components and attempting to circumvent existing tariffs.

The investigation triggered a panic and a spike in prices in the solar market, and Biden justified the moratorium as “a bridge” for the industry to stand up domestic manufacturing. Signed into law in August 2022, the IRA’s solar and clean manufacturing incentives stoked a wave of announcements of new solar factories ― 131 GW of panel factories and 87 GW of cell plants ― but CEA expects “realized capacity” to be significantly lower.

“If we’re talking about what’s holding some of this capacity back, a lot of it has to do with trying to gather finances associated with these very large capital expenditures,” Shreve said. “You need investors; you need off-takers; and these things take time to develop, and folks have to become comfortable with bringing that supply online.”

CEA’s forecast of just 12 GW of cell capacity by 2030 could increase, he said, “but we need to see some more traction from some of these suppliers first before we make that move in our forecast.”

AD/CVD Headwinds

The U.S. solar market is strong, Shreve said, pointing to a compound annual growth rate of 33% between 2010 and 2023. The market hit new highs last year, putting a total of 32 GW of new solar online, including 22 GW of utility-scale projects and 7 GW of residential installations.

But the rate of deployment must step up to meet Biden’s goal of cutting the nation’s greenhouse gas emissions 50 to 52% by 2030. Total U.S. solar capacity hit 177 GW in 2023, the analysis says, but cites multiple reports calling for a threefold increase to between 500 and 560 GW by 2030 to slash emissions in half.

Standing up a domestic supply chain is seen as a critical factor for market growth as the IRA provides bonus tax credits of up to 10% for solar projects that meet the law’s domestic content provisions. To qualify, projects beginning construction this year must meet a 40% domestic content requirement, which will step up 5% per year to 55% in 2026 and beyond.

Solar tariffs and anti-dumping and countervailing duties (AD/CVD) are seen as major headwinds for the market, according to CEA Senior Policy Analyst Christian Roselund.

The end of Biden’s two-year moratorium coincided with a new AD/CVD investigation, again focused on imported solar cells, whether or not already assembled in modules, and targeting Cambodia, Malaysia, Thailand and Vietnam.

In May, Biden also doubled tariffs on solar cells imported from China, from 25% to 50%, and removed an existing exemption for tariffs on bifacial solar panels.

Roselund said the AD/CVD duties could have a significant impact on the market because of their broad unpredictability. Unlike tariffs with set specific rates, these duties are imposed retroactively; so, a company may not know how much it will be charged for cells it is importing, and the rates may change every year.

Suppliers pay an upfront cash deposit on imported panels or cells, he said, but “if you’re importing goods that are subject to an anti-dumping or countervailing duty order, you won’t know how much you actually owe until an administrative review that will come two, perhaps three years later. … You import goods, and then you get the bill several years later.”

In addition, solar cells from the four Southeast Asian countries currently account for 58% of solar cell imports to the U.S. and 78% of imported panels, making them the biggest source of solar imports for the U.S. market, Roselund said.

Projects Canceled, Delayed

Depending on the ITC’s final decision, new AD/CVD tariffs could be imposed starting in September or, under special circumstances, retroactively from June 2023, he said. While not speculating about any potential outcomes, Roselund noted that when the ITC launched its previous AD/CVD investigation in 2022, solar imports had their slowest quarter in two years.

Roselund expects median rates for the duties, if imposed, to range from 9% to 51%, but he said the unpredictability of the rates potentially is the most dampening for market growth.

“Try to run your financial spreadsheets when you have a variable in one of the columns; it’s just very hard to do,” he said. “It hits buyers and suppliers, and then [photovoltaic] projects and manufacturing facilities. … If you have a U.S. module factory and suddenly you don’t know what you’re going to have to pay for cells, that impacts your operations and what you end up with is projects canceled, projects delayed and supply shifts as the market adjusts.”

Even with the generous incentives in the IRA, Roselund noted that in the past AD/CVD tariffs had not stimulated the buildout of a domestic supply chain. “We saw that supply shifted to other low-cost manufacturing locations,” he said.

Roselund also flagged other market headwinds. U.S. solar prices are about double the average per-watt cost in global markets, and under the pressure of the ITC investigation, suppliers are starting to reopen signed contracts and increase prices for imported cells and panels.

“Suppliers are saying, ‘We can’t deliver the product that you signed a contract for previously,’ and they have to bring the prices back up to account for their risk of what they’re going to have to pay,” he said.