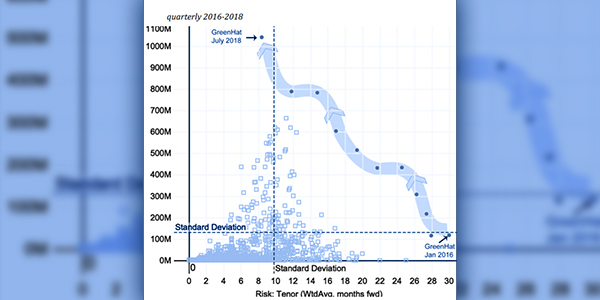

FERC announced Wednesday it will hold a staff-led technical conference Feb. 25-26 on best practices for managing credit risks in organized wholesale electricity markets, an effort to prevent a repeat of PJM’s GreenHat Energy default (AD21-6, AD20-6).

The conference, which was requested by the Energy Trading Institute (ETI) last December, will consider the credit and risk management infrastructure of RTOs and ISOs; best practices and principles for capitalization requirements, financial security requirements and unsecured credit allowances; the applicability of “know your customer” protocols and other counterparty risk management tools; considerations for implementing financial transmission right-specific credit policies, such as a mark-to-auction mechanisms; and the relationship between credit policy and wholesale electric market design.

ETI asked the commission to conduct a rulemaking to update the requirements of Order 741 and section 35.47 of the commission’s regulations on credit and risk management in RTO/ISO markets.

Order 741 resulted in shortened settlement cycles; limits on the use of unsecured credit in some markets; a prohibition on unsecured credit for all FTR-type markets; minimum criteria for market participation; and clarification on when ISOs and RTOs could demand additional collateral from market participants.

“Good credit policy is the cornerstone of any market, and the commission’s guidelines in section 35.47 were appropriate at the time,” ETI said. “However, given the recent GreenHat default and the evolution of these markets over the last decade since the issuance of Order No. 741, ETI strongly believes that the commission and industry should engage in a dialogue to ensure that credit and risk management practices and procedures in the ISOs and RTOs are robust, do not create unnecessary barriers to entry or compliance burdens, and ensure that organized markets are secure in order to meet the commission’s goals of open access, competition and transparency.”

ETI asked FERC to hold the conference by March 30 so that it could inform RTO/ISO initiatives to consider revisions to their credit policies. But the ISO/RTO Council (IRC) opposed the request, saying a rulemaking could upset stakeholder proceedings. (See RTO Council Balks at Credit Rulemaking.)

The council, which includes the six FERC-jurisdictional RTOs/ISOs, said FERC should allow the grid operators and their stakeholders to address their credit and risk management issues individually before considering a conference or rulemaking.

“At a minimum, these RTOs and ISOs should have time to gain experience with those rules before the commission facilitates a dialogue of best practices, schedules a technical conference and/or commences any rulemaking proceeding to examine further enhancements to credit policies and practices in organized electricity markets,” IRC said.

The Edison Electric Institute said it did not oppose a technical conference but said a rulemaking would be “premature.”

In June, FERC approved PJM’s proposal to require companies seeking to participate in its markets to provide the RTO with more financial records, corporate information and details of prior defaults. PJM said it will determine whether a company presents an “unreasonable credit risk” based on factors including a history of market manipulation, financial defaults or bankruptcies within the past five years. It also will consider market and financial risk factors such as low capitalization, future material financial liabilities and low credit scores. (See FERC OKs Tougher PJM Credit Rules.)

In September, NYISO Management Committee Briefs: Sept. 23, 2020.)