By Rich Heidorn Jr.

Market Monitors Joe Bowring (PJM, left) and David Patton (MISO, ISO-NE and NYISO).

WASHINGTON — The RTO stakeholder process came under fire last week as financial traders said it was being used to quash competition and a leading economist blamed it for slowing market reforms.

The setting was a Federal Energy Regulatory Commission technical conference, part of the commission’s Section 206 inquiry into PJM’s treatment of financial transactions (EL14-37).

Section 206 Inquiry

FERC opened the 206 case in August, ruling that PJM may be improperly discriminating in its disparate treatment of virtual transactions. While incremental offers (INCs) and decrement bids (DECs) are charged uplift and subject to the financial transmission rights forfeiture rule, up-to-congestion bids (UTCs) are exempt from both.

UTC trading volumes have dropped by about 80% since Sept. 8 — the date from which FERC said any uplift ultimately assigned to UTCs will be applied. (See PJM Traders Continue to Shun UTCs on Uplift Fears.)

PJM Market Monitor Joe Bowring and David Patton, Monitor for MISO, ISO-NE and NYISO, were among 11 panelists who spoke during the all-day session Jan. 7. They were joined by economists and representatives of several financial trading firms critical of PJM’s rules and Bowring’s interpretation of them. Commissioner Philip Moeller sat in for the afternoon session but asked no questions.

Bowring often found himself alone in defending his views. At one point, Patton waded into a debate between Bowring and Inertia Power’s Noha Sidhom over whether PJM’s enforcement method presumes collusion. After beginning by offering himself as a mediator in the disagreement, Patton ended by criticizing PJM’s method as “arbitrary and capricious.”

“If that’s mediation,” Bowring responded dryly, “I’d hate to see him take a side.”

2013 Tariff Revisions

In 2013, PJM proposed Tariff and Operating Agreement changes to redefine UTCs as virtual transactions and make them subject to FTR forfeitures (ER13-1654). The RTO said the change was justified by the evolution of UTCs from a congestion hedge for physical transactions to a purely financial product.

That didn’t go far enough for FERC, which said it had concerns about differences in the way PJM planned to apply the rule. The commission also questioned why PJM was not assessing UTC uplift charges even though the RTO believes the transactions contribute to uplift.

Last week’s conference featured debates over the similarities between UTCs and paired INCs and DECs, the need for the forfeiture rule, the impact of the decline in UTC trading and the ability to assess market players’ contribution to uplift.

William Hogan, research director of the Harvard Electricity Policy Group and an intellectual forefather of current RTO market designs, was highly critical of FERC for not asserting more leadership.

“I think FERC is not doing its job in setting priorities and … forcing these processes to create efficient markets,” he said. “And it’s deferring too much to stakeholder processes and bottom-up, consensus agreement. It’s a big mistake and it’s hurting us more and more.”

Anticompetitive Motives Alleged

Two panelists accused Bowring and large market participants of having ulterior motives in assigning fees to financial traders.

Sidhom said UTCs cannot bear uplift charges because their profit margins are thinner than those of INCs and DECs. The Monitor’s motive “is to kill the UTC product,” she said.

Wesley Allen of Red Wolf Energy Trading said the cost allocation resulting from PJM’s stakeholder process is akin to Microsoft assigning costs to Apple, with the large utility holding companies using their domination of the stakeholder process to crush competition from small financial traders.

“When it comes to allocation of costs, a Fortune 500 company can allocate some of their costs to another market participant and simultaneously eliminate their competition,” Allen said.

“The stakeholder process is not there to come up with the best results for the market,” he said. “The stakeholder process is about people — Fortune 500 companies largely, who control the voting — managing their costs as best they can. Eliminating their competition as best they can.”

Although the holding companies must select membership in a single sector for sector-weighted votes in PJM’s most senior committees, they have multiple subsidiaries that vote in the lower committees in several different sectors.

PJM, he said, is returning to its monopolistic past. “We’re getting there through the allocation of fees,” he said.

FTR Forfeiture Rule’s Genesis

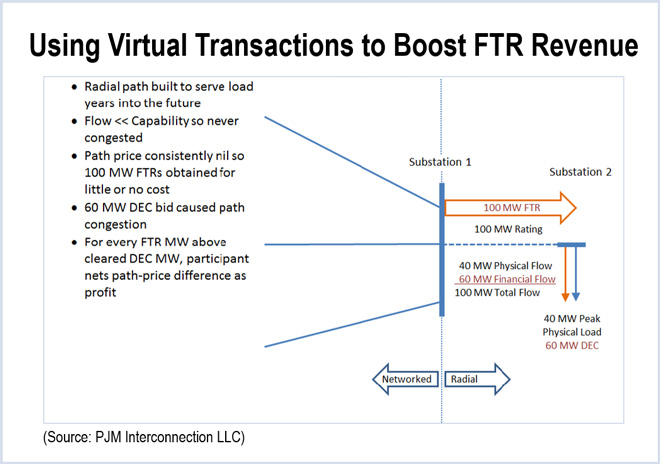

PJM moved swiftly to implement the FTR forfeiture rule in December 2000, filing it for FERC approval just two weeks after discovering that some traders were using INCs and DECs to create artificial congestion.

PJM moved swiftly to implement the FTR forfeiture rule in December 2000, filing it for FERC approval just two weeks after discovering that some traders were using INCs and DECs to create artificial congestion.

The traders were using radial paths — ones designed for future growth, which have few or no network connections. “They would increase or decrease congestion to increase FTR revenues in locations where we never saw congestion before,” said Stu Bresler, PJM vice president of market operations. The traders didn’t mind losing some money on the virtual trades because they were making more on the artificially created congestion.

“It is about manipulation,” Bowring told the conference.

Traders: ‘Worst-Case’ Selection Unfair

Under the rule, traders of INCs and DECs forfeit profits on FTRs when their virtual trades increase congestion and day-ahead/real-time price divergence. PJM identifies offending trades by first screening for those deemed to be “at or near” the constrained FTR paths. Then it determines whether the participant’s FTR profits are likely to have increased as a result of the virtual transactions by determining whether the day-ahead congestion revenues on the FTR paths increased relative to real-time revenues.

To estimate the effect of a transaction on flows, PJM must identify both the source and sink buses of the transaction. But because INCs and DECs have only one bus, PJM must select a second bus to complete the analysis.

To estimate the effect of a transaction on flows, PJM must identify both the source and sink buses of the transaction. But because INCs and DECs have only one bus, PJM must select a second bus to complete the analysis.

For the second bus, PJM uses what it deems the “worst-case” bus to determine the potential impact of the trade on the FTR path. The worst-case bus is the one that has the highest net distribution factor — the percentage of the total energy of the transaction that flows on the FTR path. Trades with distribution factors of 75% or higher are deemed “at or near” the constrained FTR paths. (The worst-case identification is not necessary for UTCs, which have explicit sources and sinks.)

Harry Singh of J. Aron and Co. told the conference that PJM’s method is unfair. “Power doesn’t sink at the worst-case connection,” he said.

Inertia Power’s Sidhom also was critical. By using the worst-case bus, PJM is often attributing to one trader the actions of another, she said.

“The fundamental flaw is taking another person’s transmission into consideration,” she said. “Don’t have a rule that I can’t screen for.”

Referring to calls to extend the rule to UTCs, she asked: “Do we want to take a flawed rule and apply it to another transaction?”

The financial traders found support from Patton and Bresler.

“PJM’s opinion at this point is that we probably went too far with that,” Bresler said, “because we’re evaluating one participant’s activity against somebody else’s, of which assumedly they don’t have knowledge.”

Patton said using the worst-case bus leads to one of two results. “It’s either irrelevant or it’s leading you potentially to a bad decision,” Patton said.

But Bowring was unyielding, saying it is better to err on the side of over-enforcement rather than under-enforcement.

“The consequences of over-mitigation are very small,” he said. “The consequences of under-mitigation are very large.”

Bowring also insisted the rule is more efficient than a case-by-case review.

Bowring has recommended modifying the rule by evaluating traders’ portfolios. He also favors applying the rule to UTCs and counterflow FTRs in addition to the prevailing-flow FTRs now covered.

Bresler said there is no need to subject counterflow FTRs to the rule. “It’s much more difficult to manipulate through counterflows,” he said. He said he has concerns that a portfolio approach would result in false positives — “catching too many fish in the net.”

No Forfeiture Rule in Other RTOs

Unlike PJM, NYISO, ERCOT and MISO do not have a forfeiture rule, and ISO-NE has one that Patton said is never applied. “Whenever we’ve looked at it we’ve found the costs outweigh the benefits,” he said. The fact that it took FERC several years to act against Louis Dreyfus Energy Services for using virtual trades to boost its FTR revenues “illustrates it’s hard to develop a bright-line test,” he said.

Patton said generic market manipulation rules provide sufficient protection against gaming of FTRs. The scheme, he said, is easy to spot. “I’m not worried about the bank robber who comes wandering in without a mask on and stands in front of the security camera. And that’s effectively the people who would be caught by this rule.”

Bresler said PJM favors replacing the worst-case test with the use of a load-weighted reference bus for INCs and generation-weighted reference for DECs.

Sidhom said she supported such a change. “We’re not that far apart on the forfeiture rule,” she said. “I really don’t know if we need wholesale changes here.”

Assessing UTCs for Uplift

The other major issue at the conference was whether UTCs should be assessed uplift charges. Bowring believes they should, saying the disparity in treatment is a major reason why UTC trading volumes have increased in recent years while INC and DEC trading has declined.

Stephanie Staska, chief risk officer for Twin Cities Power Holdings, said no virtual trades should be assessed for uplift related to “deviations,” a term she notes is not defined in the PJM Tariff.

Based on the dictionary definition — “an action different from what is usual or expected” — uplift is properly charged to those whose real-time physical positions differ from their day-ahead positions, such as load that is under- or over-forecast and generation and demand response that fails to meet the scheduled output.

In contrast, Staska said, traders entering into financial contracts receive both a day-ahead and a real-time position that cannot be cancelled or altered after the day-ahead market closes.

Bowring disagreed, saying virtuals affect dispatch and commitment decisions. The Monitor said UTCs were responsible for 64% of the deviations corresponding to negative balancing congestion in 2013 and INCs and DECs added another 24%.

Bowring said virtuals’ uplift “allocation should be reduced … but there’s no reason to exempt anyone, including UTCs.”

Bowring said billing UTCs $0.57 to $0.65 per megawatt-hour would allow PJM to cut uplift charges on INCs and DECs by more than 80% and by more than half for day-ahead load.

PJM Charges Higher than Other RTOs

PJM’s current uplift charges are more than three times those in MISO, CAISO and ERCOT, according to a summary compiled by Allen, who said PJM has rejected traders’ request for a cost causation study.

PJM’s current uplift charges are more than three times those in MISO, CAISO and ERCOT, according to a summary compiled by Allen, who said PJM has rejected traders’ request for a cost causation study.

Harvard’s Hogan said attempting to assess cost causality on uplift results in circular logic.

He recommends day-ahead transactions be exempt from uplift. Instead, he said, uplift should be allocated to real-time transactions with the lowest demand elasticity. “Then spread it wide” so the charges are small, he said.

PJM and Bowring are working on a joint proposal on uplift that they will present to the RTO’s Energy Market Uplift Senior Task Force, said Adam Keech, director of wholesale market operations. “Hopefully that can garner some support” among stakeholders, he said.

Fixed Fee

Keech said the task force’s consideration of replacing the current uplift formulas with a fixed fee was abandoned for lack of support.

“A fixed rate is simple. It’s also wrong,” Bowring said. “Every day it’s wrong.”

Abram Klein of Appian Way Energy Partners said a fixed fee is “not a horrible outcome. … That’s a proposal we could ultimately live with.”

Impact of Drop in UTC Trading

The panelists also sparred on the impact the drop in UTC trading since September has had on uplift and price convergence.

Scott Holladay, senior economist for Yes Energy, said the “before/after” analyses conducted by PJM and Bowring overlooked the fact that PJM’s load curves dropped as summer turned to fall. Holladay said his own analysis, which controlled for seasonality, showed that the decline in UTCs has resulted in a drop in price convergence and increased uplift. Allen said that Holladay’s analysis indicates the loss of UTCs has resulted in $1.2 billion in “increased inefficiency.”

Scott Holladay, senior economist for Yes Energy, said the “before/after” analyses conducted by PJM and Bowring overlooked the fact that PJM’s load curves dropped as summer turned to fall. Holladay said his own analysis, which controlled for seasonality, showed that the decline in UTCs has resulted in a drop in price convergence and increased uplift. Allen said that Holladay’s analysis indicates the loss of UTCs has resulted in $1.2 billion in “increased inefficiency.”

Bowring said the $1.2 billion figure “has no basis in fact.”

Keech also rejected Holladay’s conclusion, saying uplift was at “historically low” levels since March 2014, averaging $30 million a month less than in 2013, thanks in part to a mild summer and low fuel prices. “I don’t want people saying that we took UTCs out of the market and uplift went up. That is not the case.”

It was difficult to determine the impact of the drop in UTCs, Keech said. “It’s not really clear that price convergence has gotten better or worse.”

Keech also said assigning cost causation “is extremely difficult.”

“We haven’t done a cost-causation analysis because frankly we haven’t defined what that term even means in the context of this discussion,” he said.