By Rich Heidorn Jr.

Market manipulation cases dominated FERC’s enforcement efforts in fiscal year 2016, responsible for more than two-thirds of the probes launched during the year, according to the Office of Enforcement’s 10th annual Report on Enforcement, released Thursday.

The report said the office’s Division of Investigations opened 17 probes in FY 2016, some of which involved multiple subjects: 12 involved potential market manipulation, 11 included potential tariff violations and one each involved potential violations of a commission certificate order, the Standards of Conduct and a commission filing requirement.

Enforcement closed 11 investigations during the year, about half of them because of insufficient evidence and the other half resulting in settlements. One of the companies involved in settlements, Berkshire Power, also pleaded guilty to a criminal violation of the Federal Power Act — the first conviction ever in the 81 years since the law’s enactment, according to FERC.

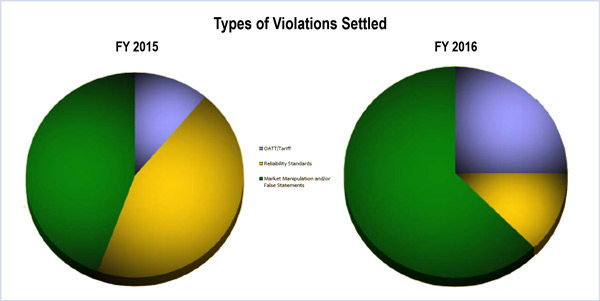

Among the settlements, about two-thirds involved market manipulation, one-quarter involved tariff violations and the remainder involved reliability standards.

In FY 2015, by contrast, reliability standards settlements and those involving market manipulation were about even at more than 40% each, with the remainder attributed to tariff violations.

The annual report includes several other highlights:

- The commission said it spent more time in federal court last year because of two challenges to FERC orders assessing penalties, continuing litigation on four cases from prior years and a commission proceeding on an administrative law judge’s initial decision finding violations of the Natural Gas Act. In all, staff sought to recover $567 million in civil penalties and $45 million in disgorgement through litigation.

- Staff received 110 new self-reports from electric utilities, generators and other market participants, including almost 60 from RTO or ISOs. Including those reports submitted in prior years, staff closed 126 self-reports.

- The Division of Audits and Accounting conducted 14 audits of oil pipeline, utility and natural gas companies, issuing 214 recommendations and ordering refunds and recoveries of $5.3 million. The report highlighted an audit of SPP that found problems with the independence of the RTO’s Internal Market Monitoring unit (PA15-6). (See FERC Calls for Changes to Protect SPP Market Monitoring Unit Independence.) It also singled out its audit of Duke Energy’s compliance with conditions the commission set in approving the company’s acquisition of Progress Energy (PA14-2). The audit found that Duke and its subsidiaries overstated their wholesale power and transmission customers’ revenue requirements by $17.5 million by improperly including merger transaction expenses without making a Section 205 filing showing that the costs were offset by merger-related savings. Auditors also found the company improperly included $2.4 million of lobbying costs in operating accounts.

White Papers

Enforcement also issued two staff white papers based on its 10 years of experience since Congress gave the agency stronger enforcement powers under the Energy Policy Act of 2005.

One, Anti-Market Manipulation Enforcement Efforts Ten Years After EPAct 2005, includes lessons learned in four areas: factors the commission and courts have found to be indicative of fraudulent conduct under the Anti-Manipulation Rule, adopted under Order 670; types of conduct that the commission has found to constitute market manipulation (including cross-market manipulation schemes, gaming and misrepresentations); mitigating and aggravating factors the commission considers in assessing penalties; and examples of market manipulation investigations that staff closed without action and the reasons why.

Staff said it was impossible to provide an exhaustive list of all types of manipulation, “because determining whether certain conduct constitutes manipulation is a fact-specific inquiry.”

“Market participants are increasingly sophisticated,” the report said, quoting from a ruling by the 8th U.S. Circuit Court of Appeals: The “methods and techniques of manipulation are limited only by the ingenuity of man.”

The second white paper, Effective Energy Trading Compliance Practices, is an effort to respond to market participants’ requests for more guidance on creating effective compliance programs to prevent and detect market manipulation. It includes examples of compliance practices that staff found effective and those that it found lacking.

Among the best practices cited:

- Hiring compliance personnel with a variety of professional and educational experience, including legal, operations, risk management and trading.

- Integrating compliance personnel into the organization’s business units (for example, locating compliance personnel on the trading floor and regularly rotating business unit employees into compliance functions).

- Performing background investigations on energy traders for evidence of criminal activity, civil lawsuits, drug abuse, excessive gambling or financial problems.

- Implementing compensation structures that incentivize compliance.

- Implementing rules discouraging traders from using price-setting instruments such as physical natural gas or electric products to benefit open financial positions. It also recommended conducting statistical reviews of position concentrations.

- Recording and retaining all trader communications for at least five years, including emails, instant messages and phone calls.

In contrast, the report says an overreliance on standardized and long annual training is ineffective. It also cautioned against relying heavily on attorneys for training rather than including operational staff. “Operational staff can help tailor compliance trainings and make them more relatable to the traders receiving the training,” the report said.

It also said companies should have ways to resolve disputes between compliance personnel and traders. “Traders should not be permitted to decide which advice to heed and which to ignore,” it said.