By Rory D. Sweeney

After its first full year under new CEO Andy Ott, and the last year of its transition to 100% Capacity Performance, PJM heads into 2017 amid continued ferment over the capacity market and angst over the impact of state subsidies to generators.

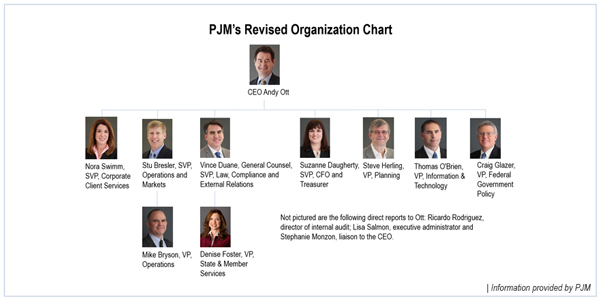

When Mike Kormos — Ott’s main challenger to replace former CEO Terry Boston — left PJM in March, Ott quickly restructured his executive staff, eliminating Kormos’ chief operations officer position and elevating deputy Stu Bresler to control of both the Markets and Operations divisions. The move put Bresler in charge of Kormos’ former deputy, Mike Bryson. Ott also expanded the authority of General Counsel Vince Duane. (See Ott Restructures PJM Divisions, Leadership.)

Ott’s reorganized team faced a series of challenges to the competitive electric model that rules in most PJM states. While the 20th anniversary of retail choice was celebrated in Pennsylvania, the competitive model came under attack elsewhere. (See Crafters of Pa.’s Deregulation Law Look Back After 20 Years.)

Public Policy vs. Markets

PJM has long dealt with state mandates and federal tax credits for renewable generation. The newer challenge is subsidies ordered by state policymakers fearful of losing in-state coal and nuclear generation — and their thousands of jobs — that are imperiled by environmental costs and low natural gas prices.

Michigan legislators voted in December to continue its 10% cap on retail choice. (See AEP Ohio Rate Plan Excludes Merchant Generation.)

Illinois followed New York’s lead in approving zero-emission credits to support Exelon’s two ailing nuclear plants in the state. (See Illinois Lawmakers Clear Nuke Subsidy.)

“The future of PJM markets is at issue,” Independent Market Monitor Joe Bowring said. “The PJM capacity markets cannot work with significant new subsidies. Subsidies suppress both the capacity price and the energy price. Both capacity market and energy market revenues are essential to providing incentives for new entry and for maintaining existing resources.”

PJM outlined its concerns and defended its performance with a 45-page report in May. (See PJM Study Defends Markets, Warns State Policies can Harm Competition.)

In an interview with RTO Insider last month, Ott said he didn’t see the state initiatives as existential threats to competition. “I don’t see a concern being raised within PJM [about whether] it delivered value,” he said. “There has been a lot of benefit to competition. [It] seems to be more the question: How do we manage the entry and exit to make sure it’s being done in a reliable manner?”

Ott pointed out that between 4,000 and 5,000 MW of new generation has entered each of the past four capacity auctions. It’s “not only a swap in fuel, but a swap in technology,” he said, that is driving down costs and forcing legacy assets to consider retirement.

The tension between state policymakers and federally regulated wholesale markets is but one of the issues of 2016 likely to continue making news in 2017.

Planned transmission upgrades to the Artificial Island nuclear complex were put on hold in August after rising costs and complaints over cost allocation, another frustrating delay in what was to be PJM’s first competitive project under FERC Order 1000. (See PJM Board Halts Artificial Island Project, Orders Staff Analysis.)

Following a technical conference in February, FERC ordered changes to PJM’s rules on financial transmission rights and auction revenue rights and rejected the RTO’s first attempt at a fix. (See FERC Finds PJM ARR/FTR Market Design Flawed; Rejects Proposed Fix.)

It all sets up for an eventful 2017. Here’s some of the issues likely to dominate PJM stakeholder meetings in the new year:

The Case for Capacity Performance

No issue is likely to consume more stakeholder attention than continued debate over PJM’s new CP rules. After acquiring 80% CP resources in the 2015 and 2016 Base Residual Auctions, PJM will be requiring 100% CP for the 2017 auction, eliminating base capacity.

Ott defends the need for the increased performance requirements and nonperformance penalties under CP, although he conceded that changes to the market — such as what the minimum offer price should be — need to be considered. “[We were] seeing a lot of new units coming in, but not every one of them was coming in with firm fuel,” he said, referring to the previous rules, under which forced outage rates peaked at 25% during the 2014 polar vortex — the event that led to the tougher rules.

A coalition of cooperatives and municipal utilities has been campaigning for several months for a holistic review of the capacity construct, questioning whether the current model is sufficiently flexible to respond to state initiatives. (See “Stakeholders Remain Skeptical of Campaign to Revisit CP,” PJM Markets and Reliability Committee Briefs.)

Others have called for more specific rule changes, including extending the life of base capacity, incorporating seasonal capacity products and relaxing some of the construct’s strict performance rules. (See FERC Wants More Detail on PJM’s Seasonal Capacity Plan.)

Bowring has continued his call to eliminate demand response as a capacity resource, saying PJM should limit its role to the demand side of the capacity calculations.

Security in All its Forms

A major focus for PJM in the coming year will be analyzing its security. It has completed a multiyear effort to develop a security strategy focused on cyber and physical protections, Ott said. “We’re already one of the leaders in the space, but continuous [improvement] is important to provide value to our customers,” he said. (See “Preview of Security Committee Receives Tepid Response,” PJM Markets and Reliability and Members Committees Briefs.)

The transition in fuel sources for generating units is receiving consideration as well. The rapid expansion of gas-fired and retreat of coal-fired generation has made PJM “more diverse than we’ve ever been,” Ott said, but he added, “Is there a point where we become concerned about being over dependent” on gas? The RTO has undertaken a fuel-security study to find out, the results of which are scheduled to be released by the end of the first quarter, Ott said.

Fixing FTRs and ARRs

FERC’s order requiring changes in PJM’s FTR/ARR market design and rejecting the RTO’s proposed correction sent PJM back to devise a new strategy, which it submitted in a Nov. 14 compliance filing (EL16-6, ER16-121). The order called for shifting the costs of balancing congestion onto load and allocating ARRs in a way that doesn’t consider extinct generators.

PJM filed for the changes to be implemented by June 1 while the Monitor requested rehearing, saying the commission erred in requiring load to shoulder the congestion costs. (See Monitor Says FERC Erred in PJM FTR Ruling, Seeks Rehearing.)

Renewed Turf Battle

Last year also saw a renewal of tensions between the Monitor and PJM management as Bowring took exception to the RTO’s attempt to constrain his unit’s role in the review of cost-based offers. (See PJM Attempting to Usurp Market Mitigation Role, Monitor Says.)

The disagreement is part of a larger dispute over fuel-cost policies, which Bowring defends as a major part of the Monitor’s role. “Fuel-cost policies are core to defining and evaluating competitive offers, which equal short-run marginal costs,” he said.