FERC on Monday rejected PJM’s proposal to modify the calculation of the financial transmission rights credit requirement and opened a show-cause proceeding to examine the justness and reasonableness of the existing requirement (ER22-703).

PJM establishes the FTR credit requirement for market participants on a portfolio basis that considers five factors, including:

- a financial exposure calculation for each FTR path based on its historical value;

- the addition of an increment for portfolios considered to be undiversified;

- the application of a 10-cent/MWh volumetric minimum charge;

- the subtraction of auction revenue rights (ARR) credits in an FTR participant’s account; and

- the subtraction of the mark-to-auction value.

The proposal included several changes, including:

- replacing the current approach of calculating collateral based on FTR historical value with an initial margin calculation from a historical simulation (HSIM) model using a 97% confidence interval;

- removing the undiversified adder;

- removing the component relating to the long-term FTR credit recalculation, because prices will be updated in real time under the HSIM model;

- revising the 10-cent/MWh volumetric minimum charge to apply after ARR credits or mark-to-auction value adjustments; and

- revising the tariff to provide that, at time of settlement, gains result in a decrease to, and losses result in an increase to, the credit requirement.

PJM filed its proposal with the commission in December after stakeholders endorsed it in October. (See PJM Stakeholders Endorse Initial Margining Proposal.) It was part of a two-year stakeholder process at the Financial Risk Mitigation Senior Task Force (FRMSTF) and resulted from efforts to strengthen the RTO’s FTR credit and collateral rules in response to a report by expert independent consultants on the GreenHat Energy default in 2018.

PJM said that the proposal addresses one of the last recommendations in the report that it has yet to implement: “eliminating the undiversified adder.” The RTO said it would be “a major step forward in advancing the overall recommendation to move the tariff’s FTR credit policy toward credit and collateral best practices in the energy commodity and financial derivatives industry.”

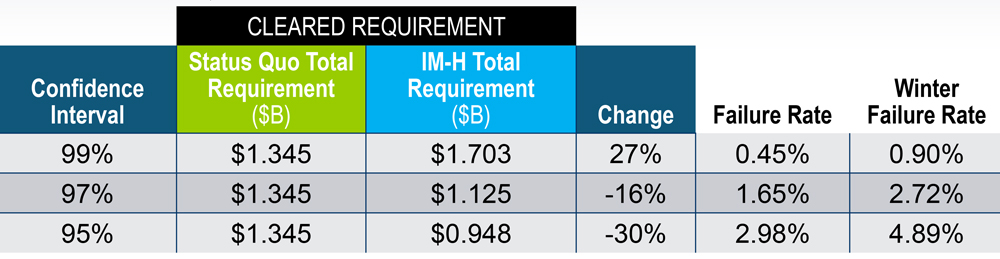

But much of the stakeholder debate in October centered around the confidence interval, with some advocating for 95% and others for 99%, ultimately settling on 97% as a compromise. The confidence interval refers to the “statistical certainty that a given value will exceed the range of possible outcomes (i.e., the losses in portfolio value over the margin period of risk) produced by the HSIM model,” according to PJM.

That proved to be the main sticking point for FERC, which said PJM “failed to demonstrate” that the proposal “reasonably calibrated to ensure that market participants will be required to provide adequate collateral relative to the risks of their positions.”

“Further, based on that record, we are concerned that PJM’s existing FTR credit requirement may no longer be just and reasonable,” the commission said.

Confidence Interval

The RTO argued that imposing a 99% confidence interval instead of 97% might “force some market participants to unwind market positions or to decide not to continue participation in the FTR auctions and FTR markets entirely.” A 97% interval “is designed to converge at a 3% failure rate over time,” it said, explaining that back-testing results are “satisfactory” if the total failure rate “agrees with the confidence interval used in the model.”

Estimated confidence intervals for total FTR collateral | PJM

Estimated confidence intervals for total FTR collateral | PJM

It conducted back-testing for 10,724 zonal path prices and found 139 failures for a 1.3% failure rate, which was less than the 3% failure rate expected with a 97% interval. The RTO said back-testing found the current FTR credit requirement has a potential 8% market failure rate.

“PJM contends that the FTR credit revisions increase collateral for some FTR market participants when the new methodology calculates those positions represent unreasonable credit risk to PJM and its members,” the commission said. “PJM asserts that it must be a market risk manager to protect PJM members from the risks of FTR defaults that potentially result in losses to PJM members that are not active participants in FTR markets.”

Stakeholder Responses

A group of stakeholders, including DC Energy, American Electric Power, Appian Way Energy Partners, Exelon, Old Dominion Electric Cooperative and Shell Energy N.A., jointly filed comments saying the proposed revisions would “better protect ratepayers” and “bring PJM closer to standards used in commodities and futures markets.”

They said there could be “unintended consequences” for PJM’s FTR markets because of “significant differences” in initial margin under a 99% confidence interval that “may cause some participants to reduce participation in the FTR market or liquidate FTR positions.”

The Independent Market Monitor said it supported PJM’s filing but requested FERC direct the use of the 99% confidence interval instead of 97% “based on industry standards.” A 97% confidence interval means that market participants “will be provided a subsidy of collateral-related costs and will not be required to cover a significant portion of their potential default risk at the expense of the entire PJM membership,” it said.

The Organization of PJM States Inc. also advocated for the use of a 99% confidence interval. It argued that the commission needs to protect load-serving entities “from uncovered losses that are directly or indirectly passed along to electric ratepayers” and that PJM “does not provide sufficient detail of the impacts on protection of nonparticipants and, ultimately on electric ratepayers, from the consequences of default risk exposure.”

Findings

The commission said it agreed with OPSI and the Monitor that the record “fails to support” a 97% interval, saying the RTO conceded that its independent auditors “validated the HSIM model at a 99% confidence interval rather than the 97% confidence interval as proposed.”

“Given that the proposed FTR credit revisions would result in lower aggregate collateral levels than PJM’s current collateral levels, we find that the lack of support regarding how the HSIM model used at a 97% confidence interval establishes reasonably calibrated collateral levels for riskier portfolios means that PJM has not met its burden to show that the FTR credit revisions are just and reasonable, particularly in light of the significant recent defaults involving the FTR market, and we reject the revisions on that basis,” FERC said.

The commission directed PJM to make an informal filing within 60 days of the date of the order to either show cause why its FTR credit requirement remains just and reasonable and not unduly discriminatory or preferential or explain what tariff changes will remedy the commission’s concerns. Stakeholders may respond to PJM’s filing within 30 days.