One would have thought this answered many times over the last 25 years. Most recently with the poster child of the Vogtle nuclear plant in Georgia that is seven years late and a mere $16 billion over budget.[1] And with regulatory capture resulting in regulated equity returns greatly exceeding the true cost of equity.[2] But every so often the utility monopolies manage to get the opposite proposition back on the public policy radar screen.

So it was with a New York Times story in January this year claiming that 35 states that deregulated some or all of their electric system tend to have higher rates than the other 15 states.[3] Where to begin?

What Matters

The sea change over the last 25 years has been the introduction of competition in the generation of electricity in some states — this is where the big money is and what warrants study. This should not be confused with the introduction of retail competition in some states — retail prices largely reflect generation (supply) prices. Or whether a state’s utilities are in an RTO — largely irrelevant to whether generation remains a monopoly. Or whether competition in transmission is a good thing — which, by the way, I have argued ad nauseum is yes.[4]

Reporting by RTO Insider revealed that the Times story relied on an analysis that defined as “deregulated” all states with utilities in RTOs — regardless of whether the utilities still had monopolies to supply customers with their rate-regulated generation.[5] This is, for example, generally the case with the states/utilities in SPP and MISO. So the Times story was way off base at the get-go.

The Energy Institute Rebuttal

Two weeks after the Times story came out professor James Bushnell at Berkeley’s Energy Institute posted a crushing rebuttal with these four insights:[6]

-

- Deregulation is best defined as the “the degree to which generation is compensated by market-based prices rather than cost-based regulation,” a proposition Bushnell and Berkley professor Severin Borenstein established in 2015.[7] A cogent statement of what I suggested above.

- Retail prices in states that deregulated generation were already very high. As Bushnell says, “That’s a big part of why they deregulated!” So the measure of success isn’t whether deregulated states’ rates are still higher than other states, it’s whether their rates are lower than they would have been if they hadn’t deregulated. This is a subject I will return to below.

- Prices in deregulated markets more closely follow the marginal cost of fuel, typically natural gas, so those prices are more volatile. When gas is expensive, deregulation can look bad. When gas is cheap, deregulation can look good. So when you measure makes a difference.

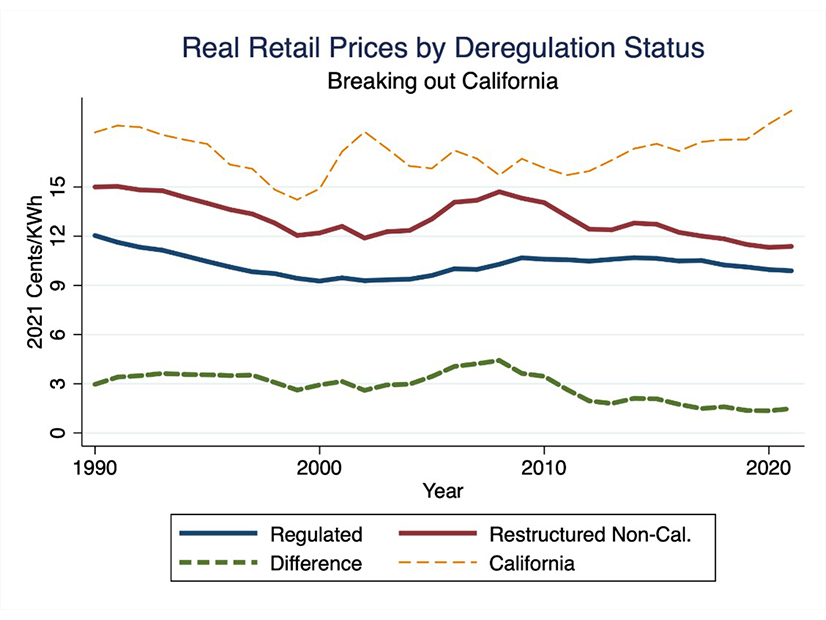

- Generation is at most half the retail price of electricity. California has adopted policies dramatically increasing retail prices, as I’ve discussed in past columns.[8] When Bushnell removed California from the “deregulated” group because of these policies, the data shows that the difference in price between the deregulated states and the regulated states has decreased over the years. As Bushnell says, “The gap between those two groups, in real terms, is now about half of what it was in 1998.” In this graphic it’s the bottom line (no pun intended) that matters.

Competition works!

Wait, There’s More

I could stop here, and rest the case on Bushnell’s insights and data. But I think there is another way to look at available data, based on the experience of the 13 PJM states.

We can divide the 13 PJM states into generation-deregulated states and generation-regulated states. For that I’ll adopt the Energy Institute’s division from a 2015 paper by Borenstein and Bushnell.[9] Deregulated states are Delaware, Illinois, Maryland, New Jersey, Ohio and Pennsylvania. Regulated states are Indiana, Kentucky, Michigan, North Carolina, Tennessee, Virginia and West Virginia.

According to EIA data,[10] the average retail price in the deregulated PJM states was 7.42 cents/kWh in 2001 and 10.98 cents/kWh in 2021, an increase of 3.56 cents/kWh or 48%. The average retail price in the regulated PJM states was 5.71 cents/kWh in 2001 and 9.93 cents/kWh in 2021, an increase of 4.22 cents/kWh or 74%. So the absolute price increase in the deregulated states, 3.56 cents/kWh versus 4.22 cents/kWh is less, and the relative price increase in the deregulated states, 48% versus 74%, is much less.

Is this proof positive that competition works? No. There are many factors and plenty of ways to slice and dice data. To paraphrase Ronald Coase, if you torture the data long enough it will confess to anything.[11] But it is one more data set that supports competition over monopoly.

And Relative Carbon Emissions

I’ve discussed before how generation competition in PJM has dramatically decreased carbon emissions, largely by market-driven natural gas displacing coal.[12]

I took a look at whether this might show up in relative carbon emissions of the deregulated states versus regulated states. According to Energy Information Administration data, average carbon emissions in the deregulated states went from 1,423 pounds/MWh in 2003 (first year of reported data) to 851 pounds/MWh in 2021, a 40% reduction. Average carbon emissions in the regulated states went from 1,641 pounds/MWh in 2003 to 1,214 pounds/MWh in 2021, a 26% reduction. Again, lots of factors, but I think this shifts the burden to those who claim that competition isn’t good for the climate.

Key Takeaways

Deregulation/competition in generation works. And it’s good for the climate. Win, win.

Columnist Steve Huntoon, principal of Energy Counsel LLP, and a former president of the Energy Bar Association, has been practicing energy law for more than 30 years.

[1] https://www.bloomberg.com/graphics/2023-vogtle-nuclear-largest-clean-energy-plant-in-us/#xj4y7vzkg.

[2] https://energy-counsel.com/wp-content/uploads/2022/10/Nice-Work-If-You-Can-Get-It-Take-2.pdf; https://www.energy-counsel.com/docs/Nice-Work-If-You-Can-Get-It-Fortnightly-August-2016.pdf.

[3] https://www.nytimes.com/2023/01/04/business/energy-environment/electricity-deregulation-energy-markets.html.

[4] https://www.energy-counsel.com/docs/FERC-Order-1000-Need-More-of-Good-Thing.pdf; please see also https://www.energy-counsel.com/docs/waste-not-what-not.pdf.

[5] https://www.rtoinsider.com/31452-a-deregulation-debate-by-the-numbers/ (“In our interview, McCullough said the analysis he provided the Times wasn’t really a comparison of retail electricity prices in deregulated versus regulated states, but between states operating inside and outside of organized markets.”)

[6] https://energyathaas.wordpress.com/2023/01/17/more-breaking-news-california-electricity-prices-are-still-high/

[7] http://bushnell.ucdavis.edu/uploads/7/6/9/5/76951361/electricityindustry.pdf.

[8] https://energy-counsel.com/wp-content/uploads/2023/06/How-Many-Deaths.pdf; https://www.energy-counsel.com/docs/No-Carb-California.pdf.

[9] http://bushnell.ucdavis.edu/uploads/7/6/9/5/76951361/electricityindustry.pdf, footnote 16.

[10] For 2001, https://www.eia.gov/electricity/state/archive/062901.pdf. For 2021, https://www.eia.gov/electricity/state/. If you email me at huntoon@comcast.net I’ll gladly send you my compilation of the underlying data (albeit in handwritten scribbles).

[11] https://en.wiktionary.org/wiki/if_you_torture_the_data_long_enough,_it_will_confess_to_anything; https://quoteinvestigator.com/2021/01/18/confess/.

[12] https://www.energy-counsel.com/docs/we-see-through-a-glass-darkly.pdf; https://www.energy-counsel.com/docs/NRDC-Prescribes-More-Carbon-Emissions.pdf; https://www.energy-counsel.com/docs/Scary-wrong.pdf.