By Michael Kuser and Rich Heidorn Jr.

High uplift costs, market power and the capacity market highlighted the External Market Monitor’s concerns in the 2017 State of the Market report for ISO-NE.

Monitor David Patton of Potomac Economics briefed stakeholders on the report at the annual summer meeting of the New England Power Pool Participants Committee last week.

The Monitor said the energy and capacity markets were competitive, with little evidence of withholding, and that market mitigation was infrequent and effective. However, the pivotal supplier analysis found market power under high-load conditions and in the Boston area — the latter of which will diminish with the completion of the Greater Boston Reliability Project and the addition of the Footprint Power combined cycle plant.

The only mitigation measures that have not been fully effective are those on resources frequently committed for local reliability. “Although the mitigation thresholds are tight, the suppliers have the incentive to operate in a higher-cost mode and receive higher NCPC [net commitment-period compensation] payments,” the report said.

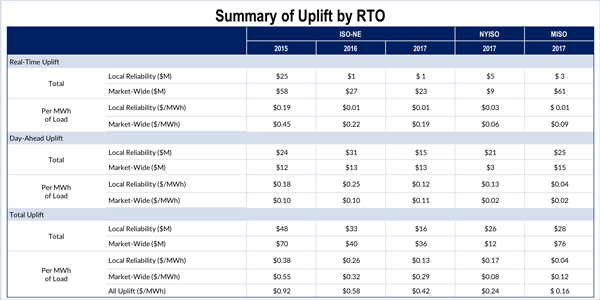

The NCPC payments contributed to high uplift charges of 42 cents/MWh last year, the Monitor said, more than double that for NYISO ($0.24/MWh) and MISO ($0.16/MWh).

The issue prompted two of the Monitor’s eight recommendations, most of which were repeated from its 2016 review. It said the RTO should change the allocation of “economic” NCPC charges consistent with “cost causation” principles and use the lowest-cost fuel — or lowest-cost configuration for multi-unit generators — when making commitments for local reliability.

Reserve Markets

The Monitor also made two related recommendations to reduce uplift, saying the RTO should eliminate its forward reserve market and create a day-ahead operating reserve market co-optimized with the day-ahead energy market.

It said more than three-quarters of day-ahead NCPC charges result from local second contingency protection and system-level 10-minute spinning reserve requirements. Because there is no day-ahead operating reserve market, the Monitor said, the costs are not reflected efficiently in day-ahead prices, resulting in excess reserve commitments and depressed reserve prices.

Creating a day-ahead reserve market would allow the elimination of the forward reserve market, which the Monitor said has “resulted in inefficient economic signals and market costs.”

Capacity Market Concerns

Capacity market issues prompted three recommendations, including a call for market changes to complement the Pay-for-Performance program that began June 1 to ensure fuel security under severe winter conditions.

The Monitor said that although PFP will provide incentives for generators to procure fuel for severe winter conditions, “it will not provide the planning and coordination that may be necessary to ensure that ISO-NE’s seasonal reliability criteria are satisfied. Thus, the ISO should evaluate whether it has seasonal planning needs for the winter that must be met to satisfy its overall reliability criteria.”

It also said it should replace its descending clock auction with a sealed bid procurement and reduce the availability of information about qualified supply before the auction. The current structure provides suppliers with information they can use to recognize when they can benefit by raising capacity prices, it said.

The Monitor recommended several changes to the RTO’s minimum offer price rule (MOPR): eliminating performance payment eligibility for units subject to the rule; capping the minimum price at the net cost of new entry; and exempting resources resulting from unsubsidized private investment.

Under PFP, the Monitor said, most of the value of capacity will come from performance payments. But because resources that skip the capacity auction can still earn the payments by producing energy during shortages, “the MOPR will not likely be an effective deterrent under the PFP framework. In addition, an uneconomic entrant will be able to depress capacity prices without selling capacity because it will lower the expected number of shortage hours.”

The report notes that unlike other RTOs, ISO-NE’s MOPR lacks a competitive entry exemption, which could interfere with private investment in new resources.

And it said the MOPR could raise prices substantially above net CONE (currently about $8/kW-month) because it sets the offer floor at the new resource’s actual entry cost. That could prevent state-sponsored resources from clearing in the Forward Capacity Auction, with the RTO instead clearing a conventional resource. Under the recently approved Competitive Auctions with Subsidized Policy Resources (CASPR) program, “clearing unneeded conventional resources will compel the sponsored resources to pay lower-cost existing resources to retire,” the Monitor said.

In addition to its formal recommendations, the Monitor also noted that several new resources that obtained capacity supply obligations (CSOs) have been delayed in recent years, with some failing to deliver their capacity during the capacity commitment period (CCP).

Consistent delays in delivery of resources have significant implications for market outcomes and efficiency and affect other participants, the Monitor said. “Delayed new projects lower the prices in the FCA(s) in which they cleared, and as a result, FCA prices do not reflect the actual realized supply and demand and the reliability of the system. In addition, other resources that obtained a CSO in the FCA with delayed resources would face additional performance-related risks under the PFP framework,” it said.

The Monitor said it supports the RTO’s efforts to develop tougher penalties for delayed resources but also encouraged it to consider switching to a prompt market, with the auction conducted immediately before the commitment period.

Coordinated Transaction Scheduling

The report recommended the RTO find ways to improve its price forecasting under its coordinated transaction scheduling (CTS) with NYISO, finding that real-time transactions between the two regions went in the wrong direction in 44% of intervals in 2017.

Although CTS’ performance improved last year, the savings were reduced by a small number of intervals with errors of more than $20/MWh.

The Monitor said errors in load forecasting and wind forecasting were the biggest problem, responsible for 23% of price forecast errors. Differences in timing and ramp profiles was the second largest contributor, causing 22% of pricing errors.