By Robert Mullin

A new report from CAISO’s internal Market Monitor contends that the ISO’s program for auctioning off congestion revenue rights (CRRs) suffers from inherent design flaws that have allowed speculators to reap enormous gains at the expense of outmatched ratepayers.

Adding to previous calls to reform or eliminate the auction process, the Department of Market Monitoring report spells out flaws in the current system and suggests a possible alternative. (See CAISO Monitor Seeks Congestion Revenue Rights Auction Reforms.)

Skeptics say the Monitor’s conclusions are ill-considered and that more analysis is necessary before the ISO takes any steps to alter the CRR auction process.

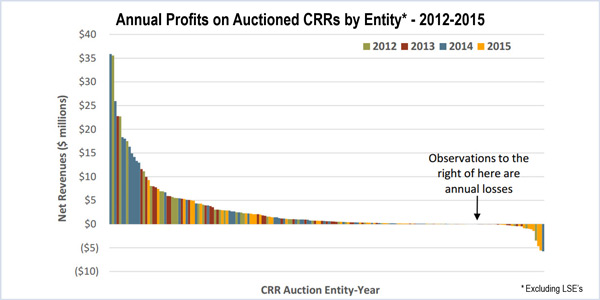

The Monitor, headed by Eric Hildebrandt, said that California ratepayers lost $520 million in 2012-2015 through a market that pays $1 to CRR holders for every 45 cents in revenues received from auctions.

“This consistent underpricing of CRRs calls into question a fundamental assumption of the CRR auction design that competition will drive auction prices to equal the CRR’s expected value,” the Monitor said. “It is unlikely that rules similar to the CRR auction design would emerge in many competitive markets that are not designed by a regulatory process.”

‘No Clear Rationale’

The Monitor contends that there is “no clear rationale” for the ISO to provide a market for price swaps, echoing criticism voiced by PJM Independent Market Monitor Joe Bowring and others. (See Role, Value of Financial Trading Debated by OPSI Panel.)

CAISO’s Monitor says the main beneficiaries of the current system are “purely financial entities” sophisticated enough to identify which CRRs are likely underpriced at auction but stand to pay off handsomely because of a disconnect between how the CRRs are packaged at auction and how they’re compensated at settlement.

To illustrate that disconnection, the Monitor first explicates its view on what exactly a CRR does and doesn’t represent.

“A CRR is not a day-ahead market transmission right,” the Monitor said. “All day-ahead market bidders have access to the transmission system regardless of whether or not they hold a CRR.”

CRRs are not needed to ship power between nodes because the ISO’s centrally cleared LMP market is linked to its transmission operation, meaning that market participants are not responsible for moving power from one location to another.

Rather, a CRR purchased at auction should be understood as a forward contract that allows an auction participant to hedge financial exposure to — or speculate on — day-ahead price differences between two locations, the Monitor explained. The demand for such hedging stems not from the ISO’s own market but from forward power contracting occurring outside the market.

“A supplier may sell a forward power contract at a location different than its generator’s location,” the Monitor said. “When this occurs, the day-ahead price on which the forward contract settles will be different than the day-ahead price the generator receives for selling power into the day-ahead market.”

The differing settlement locations expose the supplier to possible price discrepancies not accounted for in the forward power contract. So it’s the CRR auction that provides for acquiring forward contracts for differences to hedge price differentials between two points.

The problem with this setup?

“Unlike most other forward contract markets, the CRR auction allows participants to take positions without a counterparty offering to take the opposite position,” the Monitor said.

Instead, transmission ratepayers become unwilling counterparties to the CRR contracts because they’re on the hook to provide payment when auction revenues come up short of CRR payouts.

Ratepayers Outgunned

To avoid that outcome, those ratepayers would have to enter the auctions to buy the contracts themselves. This is problematic for a couple reasons, the Monitor points out.

First, the load-serving entities that effectively act on behalf of ratepayers in ISO markets may obtain CRRs to hedge risk, but they are explicitly barred from financial speculation in any transactions. In any case, LSEs would lack the incentive to manage ratepayers’ CRR forward contracts in the auction because they can pass on CRR costs to those ratepayers.

Second, participation in CRR auctions as a speculator requires knowledge of power flow analysis, finance and transmission/generation outages and operations, as well as meeting collateral requirements to engage in the market. In short, ratepayers would be outmatched by the companies that employ electrical engineers and other experts to transact in the highly complex market.

The most fundamental problem with the ISO’s CRR market, the Monitor contends, is its financial structure and lack of a consistent definition for a particular set of CRRs. Although CRRs are auctioned as “a bundle of forward contracts on specific transmission constraints,” they are not settled as the same bundle at day-ahead market prices. That’s because the day-ahead market network model that forms the basis for settlement cannot be known when the auction is run. New transmission constraints can be introduced after the auction,” effectively making the CRR a different product when bought than when it is settled.

“A CRR will only be consistently defined if the bundle in the auction is the same as the implied bundle from the day-ahead market price differences,” the Monitor said. “When the transmission models are different in the auction and day-ahead market, the bundles will not be the same.”

Proposal

As an alternative to the CRR auction, the Monitor proposes a bilateral or exchange market for forward contracts-for-difference for pairs of ISO nodes — otherwise known as locational basis price swaps. The swap buyer would pay the seller a price in the forward market and in return be paid the spot price difference between the two locations.

A key difference from the current CRR market: Price swaps would be traded between willing counterparties. And unlike the inconsistently defined CRR contract, the swap would be consistently defined in both the forward and day-ahead market.

‘Robust’ Analysis Needed

Gary Ackerman, executive director of the Western Power Trading Forum (WPTF), said his organization “strongly” disagrees with the Monitor’s call for ending CRR auctions.

“The CRR platform is a market,” Ackerman said. “Buyers and sellers value risk and opportunity differently. Scrapping it is a FERC question and seems like a radical step when indeed the CAISO makes the rules.”

Ackerman pointed out that FERC requires organized wholesale power markets to provide instruments that allow participants to hedge risk.

“This isn’t about who is getting what money or under-collecting the transmission revenue requirement,” Ackerman said. “It’s about [providing] market value for relieving congestion.”

Carrie Bentley with Resero Consulting, which frequently works on behalf of the WPTF, elaborated on the group’s position.

“If the CAISO had more transparency surrounding the transmission system — and in particular how the CAISO represents the transmission system in both the CRR model and the day-ahead market model — participants would have information at the time of the auction about the expected day-ahead market and any differences between the day-ahead market and the CRR market,” Bentley said.

Increased transparency could incentivize bidders to offer a higher value for CRRs in the auctions, Bentley said, noting that recent improvements in the ISO’s transmission outage reporting might account for the reason that CRR auction revenues exceeded payouts during the third quarter of this year.

Both Ackerman and Bentley dismissed the Monitor’s proposal for a new bilateral market for price swaps.

“There cannot be an effective market without buyers and sellers fluidly engaging in commerce, and there does not appear to be buyer interest in long-term power and power basis hedging,” Ackerman said.

Bentley said the CRR auction process is “invaluable” because it allows market participants to adjust their CRR positions “to get just the right hedge” based on portfolios and risks.

“Because the grid is so complex, achieving this fine tuning of one’s CRR holdings would be nearly impossible if participants had to trade bilaterally,” Bentley said.

Bentley also contends that market participants have not been provided with “robust analyses” on the precise cause for the revenue shortfalls in the auctions.

“It seems to make more sense that [the Monitor] could perform further analysis — or make such analysis public if they have already performed it — and then parties could consider how the CAISO could converge the day-ahead and CRR markets and models as a first step — before jumping to the conclusion the auction simply isn’t useful,” Bentley said.