By William Opalka

ISO-NE opened its ninth Forward Capacity Auction yesterday amid expectations of high prices as the region deals with plant retirements and tight natural gas supplies due to inadequate infrastructure. Results from the auction are expected this week or next.

Last year, for the first time, the auction failed to clear as much capacity as ISO-NE sought, falling 143 MW short of the 33,855-MW requirement. ISO-NE is seeking more than 34,000 MW for delivery year 2018/19, 334 MW more than last year’s requirement.

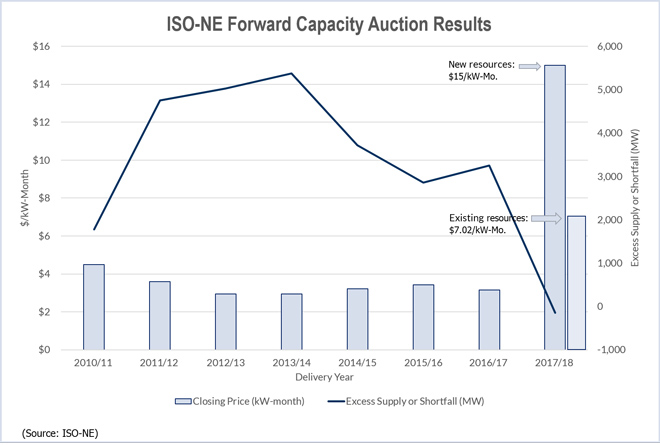

Revenues from FCA 8 totaled $3.05 billion, a 72% jump from 2009’s previous high of $1.77 billion and nearly triple 2013’s $1.06 billion.

FCA 9 the Peak for Prices?

Analysts for UBS Securities released a report yesterday predicting prices will rise higher in this week’s auction, perhaps reaching $11 to $15/kW-month in southeastern Massachusetts and Rhode Island.

The analysts said prices could be limited by new entrants within the RTO or a rebound in transmission imports following a reduction last year.

In either event, they predict new plant construction and possible expansions at existing sites in the constrained Massachusetts market could send prices crashing in FCA 10 next year. “We suspect this is the top of the market for this region, with prices reaching their highs — pushing down prices for future years,” they wrote.

Christopher Tumure, an analyst at JP Morgan, said yesterday the he expects “a bit of an uptick” in prices.

“On the supply side, much of the new generation has already been bid into recent auctions, so we don’t see much change there. On the demand side, there’s about a 300-MW increase year-over-year.”

Two new developments may partially offset each other, he said.

“One of the changes this year is the Pay-for-Performance [program], which may increase prices as it affects the bidding behavior. Another change is the switch to the sloped demand curve instead of a vertical, and that’s not necessarily a good thing for prices.”

NRG Sees Gains

Last month, NRG executives told the company’s annual investors meeting that they expect $1.445 billion in 2018/19 capacity revenue from ISO-NE and PJM, a $565 million increase over 2017/18.

Since FCA 8, the region has lost the Salem Harbor Generating Station in Massachusetts and the Vermont Yankee nuclear plant to retirement. Also unavailable in FCA 9 will be the Brayton Point Generating Station in Massachusetts, which is set to close in 2017. In a recent media briefing, ISO-NE CEO Gordon van Welie said New England will lose about 3,500 MW of generating resources over the next few years.

ISO-NE’s informational filing for 2018/19, which the Federal Energy Regulatory Commission accepted Jan. 16, shows an installed capacity requirement of 35,142 MW (ER15-328). After accounting for 953 MW of Hydro Quebec Interconnection Capability Credits, the RTO seeks to procure 34,189 MW.

Qualified to compete in the auction are 41,102 MW — 8,547 MW of new resources and 32,555 MW of existing resources.

ISO-NE will model four capacity zones in FCA 9:

- Southeastern Massachusetts/Rhode Island (SEMA/RI);

- Connecticut;

- Northeastern Massachusetts/Boston (NEMA/Boston); and

- Rest of Pool (Maine, Western/Central Massachusetts, New Hampshire and Vermont).

ISO-NE determined that SEMA/RI will be modeled as import-constrained in this year’s auction, in addition to Connecticut and NEMA/Boston, which were both modeled as import-constrained last year.

SEMA/RI wasn’t modeled last year, when the four zones were Maine (export-constrained), NEMA/Boston (import-constrained), Connecticut (import-constrained), and Rest-of-Pool.

This year will be the first auction in which ISO-NE will adopt a sloped demand curve, as is used in PJM. FERC ordered the change, which is intended to reduce price volatility, following the shortfall in FCA 8.

Demand Response is In

The New England Power Generators Association had asked FERC to disqualify demand response from participation, citing the D.C. Circuit Court of Appeals ruling voiding FERC’s jurisdiction over DR pricing in the energy markets (Electric Power Supply Association v. Federal Energy Regulatory Commission).

FERC, which has asked the Supreme Court to reconsider the ruling, rejected the generators’ challenge last month (ER15-257). (See FERC Approves New England Demand Response Integration.)

[EDITOR’S NOTE: An earlier version of this story incorrectly said that SEMA/RI was modeled as an import-constrained zone in FCA 8. SEMA/RI was not modeled in last year’s auction.]