By Steve Huntoon

It’s what you know that ain’t so …

That will get you in trouble.

The February Fortnightly features an article about the German Energiewende (“Energy Transition”) that makes three basic claims: (1) Germany is successfully decarbonizing with renewables, (2) Energiewende is “good news for consumers” and (3) there will be no adverse impact on electric reliability.[1]

The first two claims are simply wrong. The third cannot be correct.

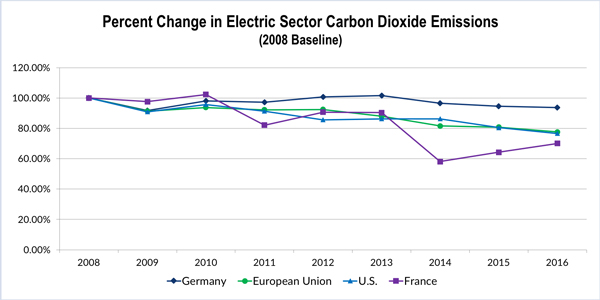

Wrong: German Electricity is Decarbonizing

German electricity isn’t decarbonizing. Because of its tragic decision to close nuclear plants, Germany is substituting coal and renewables for nuclear.

Despite the increase in renewable generation that Fortnightly extols, there has been no material decrease in carbon dioxide emissions from German electric generation. Germany is doing much worse than the European Union generally, much worse than the U.S. and much worse than France, as shown by changes in electric sector carbon dioxide emissions (2008 baseline):[2]

In a nutshell, Germany is substituting coal and renewables for nuclear,[3] while the U.S. and France are substituting natural gas and renewables for coal.[4] Germany isn’t making a serious dent in its carbon dioxide emissions from electricity, while other nations are.

Does Germany “point the way”? No way.

Wrong: Energiewende is Good News for Consumers

Truth is that Energiewende has driven Germany’s sky-high electricity prices even higher. Here are Germany’s residential prices relative to the European Union, France and the U.S. (U.S. cents/kWh):[5]

It may be hard for Americans to get their heads around it, but German residential electric prices are now three times U.S. prices.

For U.S. regulators out there, how many years of a 10% price increase each year would it take for the average U.S. residential price to reach the average German residential price?

The answer is 12 years. But the torches and pitchforks appear long before then. Like Year 2.

By the way, Energiewende hasn’t yet hit stride. Germany is planning much more costly renewable and transmission projects that are estimated to ultimately cost 25,000 euros per family household.[6] That’s $30,750 American.

Does Germany “point the way”? No way.

Cannot be Right: No Impact on Reliability

The Fortnightly article claims that decarbonization has/will have no adverse impact on reliability. This claim is premature and cannot be correct.

The vision seems to be that Germany gets rid of all nuclear plants and all coal plants, and will rely on a combination of renewable resources, flexible fossil (presumably natural gas) generation, demand response and storage (batteries).

Fortnightly seems to think this is feasible because “Germany already produces hours of nearly 100% renewable electricity on the system.” According a German spokeswoman, “‘Baseload is no longer needed,’ otherwise it could ‘block the grid.’”

Say what? The problem isn’t hours when solar and wind generate enough to meet demand. The problem is all those other hours when they don’t, like these sorts of hours and days and weeks:[7]

Renewables generated very little for a two week period. The vast bulk of demand had to be met with existing conventional power plants.

Supposed Reliability Fixes

Now let’s look at the supposed fixes when existing nuclear and coal power plants are eliminated: flexible fossil fuel (natural gas) generation? Creating a new fleet of gas generators with the necessary pipeline infrastructure would be astronomically expensive and make Germany even more dependent on Vladimir Putin’s natural gas.

By the way, the new German coalition agreement’s sole reference to natural gas is: “Make Germany a location for liquefied natural gas (LNG) infrastructure.”[8] No such LNG infrastructure exists, and the one proposed LNG terminal looks like more of a pipe dream.[9] And a very expensive one at that.

OK, how about demand response? An optimistic estimate of theoretically possible DR is about 10% of Germany’s total demand,[10] requiring a new infrastructure and, of course, customers’ agreement.

Not only is the potential small, but the demand reduction is for one or two hours max. The chart above shows solar and wind can take a powder for days on end.

Batteries fall prey to this same problem. The cost of batteries is typically quoted in terms of four hours of stored energy for each hour of maximum output. What if you need battery output to last eight hours? Then the nominal cost of batteries doubles. If you need 24 hours, then the nominal cost of batteries goes up six times.

So when we think about the need to cover days of renewable non-generation, we should understand that the cost of batteries is many times the current publicized cost. And we can understand why no sophisticated industry player is flocking to batteries (unless subsidized by Other People’s Money — in which case they’re a great idea of course).

The claim that Germany can maintain reliability without nuclear and with only “very small amounts of fossil fuels,” as the article says, sounds like it came from the breatharians, who believe they only need air, and not food, to survive. We don’t hear from them too often — at least not the same ones. For the obvious reason.

The Fortnightly article goes on to cite customer outage and loss-of-load expectation (LOLE) data and projections supposedly demonstrating continued reliability under Energiewende. But the vast bulk of customer outages are attributable to distribution and transmission problems, not resource problems (as the article itself notes at the outset citing a Rhodium Group report). So outage data, especially with renewables still a minority of total resources, says nothing about future resource adequacy.

As for LOLE projections, the article relies on studies that assume that more than 30 GW of coal plants remain in Germany[11] — which is the opposite of the article’s premise that they are eliminated. You can’t eat your cake and have it too.

In summary, Germany’s future without nuclear and without coal has no plausible means of meeting customer demand.

Does Germany “point the way”? No way.

Bottom Line

Energiewelde isn’t decarbonizing German electricity, only increasing sky-high electric prices, which it will continue to do indefinitely. And reliability can’t be sustained on the equivalent of thin air.

Energiewende does point a way. The wrong way.

Steve Huntoon is a former president of the Energy Bar Association, with 30 years of experience advising and representing energy companies and institutions. He received a B.A. in economics and a J.D. from the University of Virginia. He is the principal in Energy Counsel, LLP, www.energy-counsel.com.

- https://www.fortnightly.com/fortnightly/2018/02/how-german-energiewendes-renewables-integration-points-way. ↑

- 2008 emissions set at baseline of 100% for all data which is tons of carbon dioxide emissions. First year is 2008 because that is the first year of Eurostat data here, http://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=env_ac_ainah_r2&lang (“Electricity, gas, steam and air conditioning supply.”) I thank Aldyen Donnelly of Vancouver for pointing me to the Eurostat database. U.S. emissions from EPA data here, https://www.epa.gov/ghgemissions/inventory-us-greenhouse-gas-emissions-and-sinks (Table 2-4, EPA inventory archives used for years 2008-2011). ↑

- For discussions of this phenomenon, http://www.eiu.com/industry/article/1205236504/is-germanys-energiewende-cutting-ghg-emissions/2017-03-20, https://www.economist.com/news/europe/21731171-thanks-panicked-decision-shut-its-nuclear-plants-germany-carbon-laggard-germany. ↑

- https://www.edf.fr/en/the-edf-group/our-commitments/corporate-social-responsibility/doing-even-more-to-reduce-co2-emissions. ↑

- European prices from Eurostat data here, http://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=nrg_pc_205&lang=en (select time frame back to 2008 and prices including all taxes and levies; prices converted to U.S. cents/kWh at 1.23 euro/dollar exchange rate). U.S. prices from Energy Information Administration data here, https://www.eia.gov/electricity/monthly/epm_table_grapher.php?t=epmt_5_03. ↑

- http://energypost.eu/energiewende-running-limits/. ↑

- http://energypost.eu/end-energiewende/. ↑

- https://www.cleanenergywire.org/factsheets/climate-and-energy-germanys-government-coalition-draft-treaty. ↑

- http://interfaxenergy.com/gasdaily/article/29453/german-lng-terminal-plans-draw-mixed-response. ↑

- https://www.diw.de/de/diw_01.c.532689.de/presse/diw_roundup/demand_response_in_germany_technical_potential_benefits_and_regulatory_challenges.html. ↑

- https://www.entsoe.eu/Documents/TYNDP2018_MAF2017_Market%20Data_provisional.xlsx (Tab BE 2025, Germany columns for “Hard coal” and “Lignite” assume 31.3 GW of coal capacity and, by the way, 27.6 GW of natural gas capacity); https://www.entsoe.eu/Documents/SDC%20documents/MAF/MAF2016_market_modelling_data.xlsx (prior year version with similar coal and gas natural capacities); https://www.bmwi.de/Redaktion/DE/Downloads/V/versorgungssicherheit-in-deutschland-und-seinen-nachbarlaendern-en.pdf?__blob=publicationFile&v=3 (pdf page 32). ↑