Historically Warm Last Winter

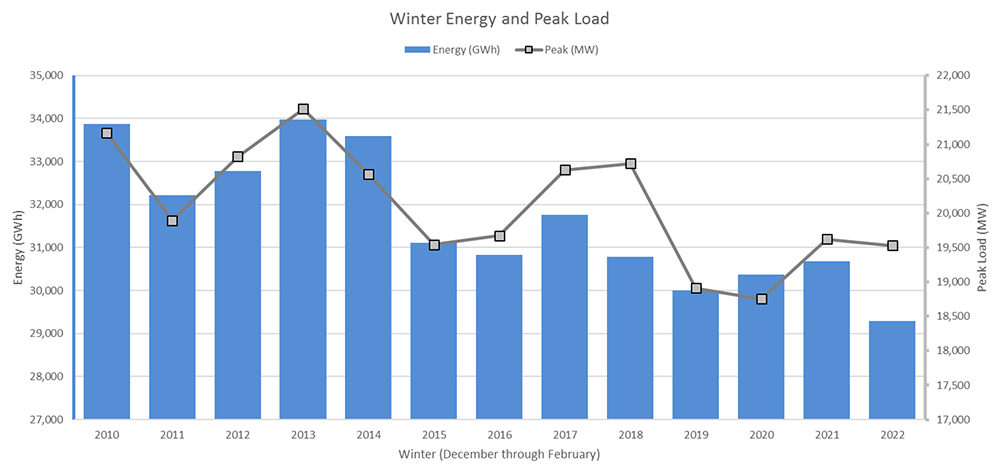

ISO-NE COO Vamsi Chadalavada on Thursday told the NEPOOL Participants Committee that New England’s overall energy demand was down during the past winter, coming in at approximately 29,300 GWh, compared to the 31,600 GWh average since 2010.

This is the lowest winter energy total reported by ISO-NE going back through 2010, punctuating a clear downward trend over this time period.

Chadalavada highlighted how the expansion of behind-the-meter solar energy, which has significantly outperformed ISO-NE projections in recent years, has helped to ease winter demand.

The low demand was also in part from abnormally high temperatures, which averaged 4.8 degrees Fahrenheit above “normal” — defined as the average temperature over the past 30 years — from December through February. This includes a 35-consecutive-day stretch of above-normal temperatures, nearly extending through the entire month of January.

These warm conditions could increasingly become the new normal in the region, as research has indicated that New England is warming faster than average global temperatures, with the greatest impacts being felt in the winter.

2023/24 Projection

Looking forward to this coming winter, Chadalavada presented a variety of scenarios modeling the impacts of different severities on the grid. These generally found the region well positioned, with sufficient energy and capacity to meet demand in mild and moderate winter scenarios.

In the case of a harsher winter, with lower-than-normal overall temperatures and several extended cold stretches, the RTO projected that some capacity deficiency actions may need to be taken for a few days, but that emergency measures will likely not be necessary.

He also noted that the Inventoried Energy Program, which compensates generators for storing up to three days of fuel, will remain in place in the winters of 2023 and 2024.

Winter Without the Everett LNG terminal

Chadalavada also presented the RTO’s modeling of the winter of 2024/25 with and without the LNG import terminal in Everett, Mass., owned by Constellation Energy. The reliability-must-run agreement for the Mystic generating plant, the terminal’s “anchor tenant,” will expire in June 2024. (See Narrow Set of Options for Retaining Everett LNG Terminal.)

The RTO, along with the gas distribution companies, have argued that the terminal is necessary for the reliability of the region’s gas and electric systems, while environmental groups have challenged this conclusion, saying that these needs could be covered by storage investments and demand response programs.

ISO-NE’s modeling, which looked at how the grid would perform under moderate and severe winter scenarios, found “limited exposure to energy shortfalls” without the terminal, compared to essentially no exposure to energy shortages with the terminal. The projected severity of the shortfall depends on the size of the fuel oil inventory and how much additional clean energy — offshore wind in particular — is added prior to the loss of the terminal.

Winter energy and peak load in New England from 2010 to 2022 | ISO-NE

Winter energy and peak load in New England from 2010 to 2022 | ISO-NE

The RTO concluded that an increased fuel oil inventory could fully cover the energy shortfall in the case of a moderate winter, and mostly mitigate the shortfall in the case of more extreme winter conditions.

Despite these findings, Chadalavada cautioned against jumping to the conclusion that the terminal will no longer be necessary following the expiration of the existing contract, owing to potential impacts the loss would have on the gas system, as well as on the electric system in the winters following 2024/25.

“The ISO doesn’t have the expertise to assess the operational capability of the regional pipeline system without Everett and will rely on the expertise of pipelines and the [local distribution companies] to identify any operational concerns,” Chadalavada said.

The RTO has been collaborating with the Electric Power Research Institute to study the potential long-term effects that the loss of the Everett terminal would have on reliability in the region. The first phase of this study, projecting out to 2027, is set to be released this Friday.

Order 2222 Compliance

The committee endorsed tariff revisions to comply with FERC Order 2222 in response to a commission directive, with a filing expected Tuesday.

The PC voted along the same sector lines as the Markets Committee did when it endorsed the revisions last month, with almost exactly the same amount of support: about 78.6%. (See “Compliance Filing on DER Aggregation,” ISO-NE Stakeholders OK DER Aggregation Plans, Generator Relief.)

FERC in March rejected certain elements of ISO-NE’s original proposal to comply with Order 2222, which directed RTOs and ISOs to allow distributed energy resource aggregations to fully participate in their markets. The commission ordered further revisions by several different deadlines, depending on the element.

The new revisions are those due 60 days from FERC’s March 1 order. (ISO-NE was granted a week extension to file them.) They would clarify that the relevant electric retail regulatory authority authorizes customers of small utilities to participate in a DER aggregation and that the RTO will resolve disputes that are within its authority and subject to its tariff.

The filing will also include an explanation of why ISO-NE’s proposal to require measurement of behind-the-meter DERs at the retail delivery point, rather than allowing submetering, minimizes barriers to entry for resources. The RTO has requested a rehearing of FERC’s rejection of its proposal to designate the DER aggregator as the entity responsible for providing any required metering information.

LS Power CSO Proposal

Finally, the committee rejected endorsing proposed tariff revisions by LS Power to allow its gas-fired Ocean State Power plant to unwind a 64-MW capacity increase while maintaining its existing 270-MW capacity supply obligation.

The plant had cleared Forward Capacity Auction 15 at 334 MW, but the company has become concerned that it will not be able to complete the uprate by the June 1, 2026, deadline. Under the RTO’s tariff, that would mean the plant would also lose its CSO for the existing capacity.

LS Power’s proposed revisions were intended to allow market participants to “unwind” promised capacity increases, allowing the plant to continue participating in the capacity market. Despite the RTO and its Internal Market Monitor opposing the proposal, the MC last month overwhelmingly endorsed it, with 83.3% in support. (See “LS Power’s Dilemma” in linked article above.)

But the company failed to achieve even a majority of the PC’s support, with only 45.7% voting in favor; it needed 60% for endorsement. All of the Generation sector was in favor, and minor support came from the Supplier, Alternative Resources and End User sectors. The Publicly Owned Entity sector was unanimous in opposition. Every sector had numerous abstentions.

LS Power may file a complaint with FERC under Federal Power Act Section 206. Before the vote, NEPOOL clarified to committee members that if they endorsed the revisions, it would indicate its support for LS Power’s revisions in the docket but not weigh in on the just and reasonableness of the current tariff.