The return of demand growth is something new in the electricity industry, especially as it is being driven by individual consumers whose load can exceed the peak demand of a small state, and it is giving new life to an old argument in state legislatures: restructuring the industry.

The states that went forward with restructuring in the 1990s and those that opted against it are not necessarily going to switch sides completely, but longstanding rules are being challenged in both.

Utilities in PJM have been lobbying for long-restructured states like Pennsylvania and Maryland to allow them to build generation into rate base, while independent power producers with retail businesses are asking vertically integrated states to open part of their demand to the market so they can build generation to serve those new customers, as well as commercial and industrial customers generally.

Data centers are definitely driving the conversation, said Abby Foster, senior vice president of policy at the Retail Energy Advancement League (REAL), which is trying to open vertically integrated states and maintain restructured markets in others.

“But this would have been happening either way, especially in the vertically integrated states, because we’re hitting this point where you look at especially the states in MISO, there’s a ton of coal assets, and most of those are scheduled for retirement in the next 10 years,” she said in an interview with RTO Insider.

Without data centers accelerating resource adequacy concerns, it would have been more of a slow burn as utilities kept on applying for new rate cases to replace retiring power plants, with consumers facing higher prices for the first time in 20 years in states like Missouri, Indiana or Kentucky, Foster said. That buildout is coming when the costs of new generation have risen sharply in recent years.

“It’s almost like things have come full circle from the late 90s, when states were in the position that they were in, and they chose to restructure,” Foster said. “So, you have load growth; you have a ton of retirements; you have a ton of generation that needs to be built and costs that are just unsustainable and untenable for customers to pay over the long-term.”

REAL met with some West Virginia legislators on their state’s recent trend in average power prices, Foster said.

“They’re still middle of the pack today, but they were like 47th two or three years ago, [and] they didn’t love the idea that West Virginia rates are increasing, second only to California,” she added.

REAL’s model legislation would open 20% of overall load to competition, and consumers would need demand of 1 MW to participate, though C&I facilities with smaller loads could use aggregation of multiple sites to get into the market, Foster said.

“That 20% makes it so that there’s still enough that needs to be built by the utilities; it’s just removing the amount that they have to build that’s new rather than placing costs on the customers who aren’t shopping,” Foster said. “And of course, the customers who are shopping still pay all of the other costs — so transmission, distribution, energy efficiency and low-income programs.” Only the generation part of their bill would go to whatever third-party company they sign up with.

Some states already have a capped level of shopping, and while their experiences varied, often they started to restructure but stopped short. Michigan put a cap of 10% on its market, and it quickly filled up, which meant the market took on the burden of supplying that demand.

“They never had to build what’s the equivalent of seven or eight natural gas plants,” Foster said. “They never had to bill the rest of the ratepayers to build those gas plants to serve those customers, plus their guaranteed rate of return.”

Michigan-headquartered General Motors would like to see a version of that state’s system extended into Missouri, where it employs 4,500 workers, via House Bill 417, the Electric Choice and Competition Law.

“We have invested more than $1.5 billion in our facilities and generated thousands of jobs for related suppliers, contributing to significant baseload demand,” GM Global Energy Strategy Director Rob Threlkeld wrote legislators in a letter in March 2025. “As electricity costs continue to rise, GM supports legislation that ensures reliable and affordable electricity for our operations. HB 417 will assist industrial customers in managing their anticipated rising energy costs.”

Utilities in PJM Want Back in Generation Game

While REAL has been pushing to crack open retail power markets in states that have never opened up, some utilities in PJM have been asking states like Maryland and Pennsylvania to let them rate-base new power plants to help close the widening gap on resource adequacy there.

Exelon hired Charles River Associates to produce a report that argues allowing it and other utilities in PJM to build generation could save consumers $9.6 billion to $20 billion in the 2028/29 delivery year.

“Customers are understandably frustrated about high energy costs, and public utility companies are ready to help bring them under control with utility-generated power such as battery storage or community solar,” Exelon Chief Legal Officer Colette Honorable said in a statement. “Utility-generated power will ensure we have enough electricity to meet skyrocketing demand, address affordability and make sure customers come first.”

Exelon said its report is especially relevant for states like Maryland, where rapid load growth and constrained supply are intensifying affordability and reliability challenges.

While the restructured states in PJM have banned their utilities from building generation in rate base since those laws went into effect in the 1990s, Exelon does not want the change to spark the unwinding of the markets, arguing that any generation it builds can work alongside them. Only some of the states in PJM have fully restructured; West Virginia is fully regulated; and Virginia has a hybrid system with utility-owned generation. Units from those states have operated in the RTO’s markets for years, competing with IPPs.

Advocates of competition argue that letting utilities into the generation business could risk an overbuild of generation, as putting the facilities in rate base guarantees cost recovery regardless, while the IPP model places such risks on generation firm’s shareholders.

“In restructured states, IPP developers do not have an obligation to build,” Exelon Director of Federal Regulatory Affairs Jordan Kwok said. “And, because they may elect not to build for whatever reason, customers may be left with inadequate generation supply and the ensuing reduction in reliability. Put another way, in a competitive framework, IPPs bear the risk of their actions, but customers bear the risk of IPP inaction. Utility-generated power solves for this risk by fostering certainty and providing a tool for our regulators to fall back on if the market is underdelivering.”

Industry Experts Split on the Issue

Mark Christie, director of William & Mary Law School’s Center for Energy Law and Policy, said in a recent interview that there are no perfect regulatory structures, but the ultimate goal of any has to be delivering reliable power at the least cost to the consumer.

“Whether new generation is financed through rate-basing by load-serving utilities, or through capacity payments to bidders in the PJM capacity market, consumers will still be paying the bill for the new generation,” the former FERC chair said. “So, the line we have heard for 30 years that using the capacity market alone puts the burden on investors to pay for new generation, not consumers, is misleading at best. Consumers pay for capacity payments in their power bills, just as they pay for rate-based generation.”

Christie said that Virginia has a good regulatory model, with its hybrid system where utilities can rate-base power plants and IPPs can build competitive power plants. It is also one of the states that serves a model for REAL’s preferred policy with a cap on shopping that lets some C&I customers pick their supplier.

“When I was a Virginia regulator, we approved at least five combined-cycle gas generators for our utilities,” Christie said. “All were rate-based, all were built, and none of them would have been built without rate-based financing. And we approved continued rate-based financing, including life extensions, for Dominion’s nuclear units. All of these dispatchable generators have been critically important to keeping the lights on in Virginia and PJM, and without rate-based financing, we would not have gotten them built.”

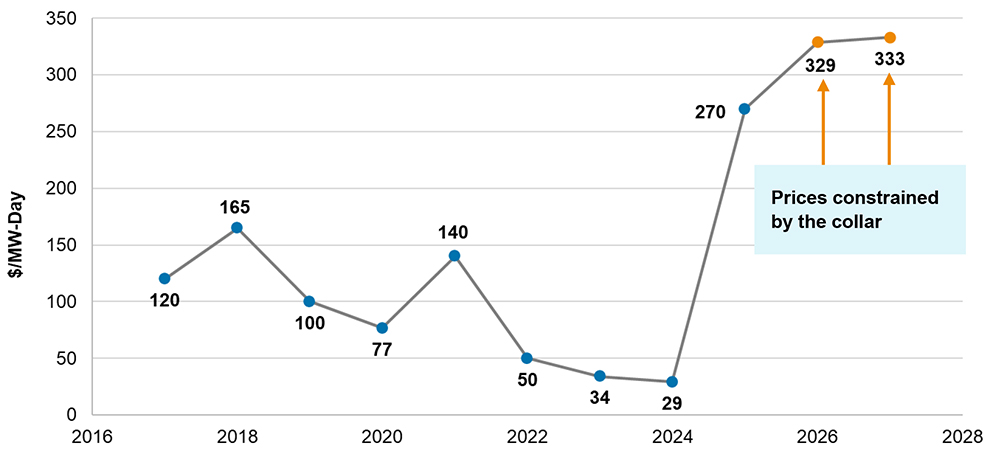

The debates around which way states should go are coming back up now in PJM because its capacity market has seen prices shoot up, and in its most recent auction, it cleared short of the RTO’s reliability target.

“I think the big picture is that the PJM capacity market is simply not obtaining enough generation,” Christie said. “We know that for an absolute fact.”

Former Pennsylvania Public Utility Commissioner John Hanger served when the state passed its restructuring law. Since then he has written reports as a consultant arguing the policy is best for customers, pointing to offers in PECO Energy’s Philadelphia area territory and Duquesne Light Co.’s Pittsburgh territory that are cheaper in nominal dollars than the utility rates in 1996, when the restructuring law passed.

“It is truly stunning,” Hanger said in an interview. “That is a testament to how bad rate-based, rate-of-return regulation worked in Pennsylvania, especially in the Duquesne Light and PECO service territories, and also the success of competitive generation markets.”

While other restructured states, like Maryland and New York, have restricted the market for residential customers, Hanger said that retail competition works well for large customers, in every jurisdiction.

“If legislators in Missouri want to drive down their costs for their commercial/industrial customers, they should allow these customers to shop for electricity and introduce generation competition,” he added. “And they should do it with a sensible transition plan, but they should do it as soon as possible.”

Letting utilities back into the generation business now, even with the resource adequacy issues in PJM, would not be good, he argued.

“It’s an invitation to waste, fraud and abuse,” Hanger said. “It’s an invitation to boondoggles that the captive ratepayers would have to pay for. I cannot think of an approach to the current concerns that is more likely to blow up in the face of any legislator or any governor who supported that.”

Affordability concerns drove the initial wave of restructuring in the 1990s, Hanger recalled. Those same concerns have given the utilities an opportunity to push legislation to let them build generation again, he said.

“They use the lack of information amongst the general public on these questions and, frankly, the fact that legislators are generalists who do not specialize in electricity markets or utility regulation to try to pull the wool over the eyes of those legislators,” Hanger said. “They come in with simple stories that are simply wrong.”

The fastest rising part of the end-use customer’s bill in recent years has been what is still regulated: the payments for transmission and distribution infrastructure, Hanger said.

“We are supposed to believe that the two companies that have been shooting up transmission and distribution rates somehow or another are going to produce lower generation rates,” Hanger said. “Give me a break.”

Exelon pushed back on that last point, saying its investments are regulated by state commissions and FERC, while the resulting system is reliable for consumers.

“While it is correct that transmission costs continue to grow, this critical ongoing investment is taking place after successful operation of transmission assets that were placed in service as far back as nine decades ago and have stood the test of time,” the company said in a statement. “It reflects transmission owners’ efforts to modernize the grid, replace aging assets and to ensure the system is built out to meet expanding electricity needs of modern society.”