An early-stage collaboration between the Acadia Center and Nergica is intended to bring together communities, tribes, nonprofits, companies, RTOs and government officials from the northeastern U.S. and Canada to increase coordination around interregional transmission.

Dubbed the Northeast Grid Planning Forum (NGPF), the effort is aimed at changing the conversation around transmission planning throughout the broader region to help unlock infrastructure investments, improved planning processes and market changes to help facilitate the clean energy transition.

“If you look out at what states and provinces are trying to achieve with meeting climate goals,” Dan Sosland, president of the Acadia Center, told RTO Insider, “there is a tremendous amount of potential complementary benefits that could be obtained if we step back and look at how the grids might coordinate in a more intentional way.”

The entire region faces the potential for massive load growth over the coming decades, coupled with significant changes in how and where electricity is generated. Hydro-Québec anticipates its demand will double by 2050, while ISO-NEforecasts its peak load to reach up to 57 GW, compared to the 24-GW peak experienced in 2023.

The transmission investments needed to meet this load growth will be pricey: Hydro-Québec has proposed to invest $45 billion to $50 billion by 2035 to expand its transmission capacity, while ISO-NE has estimated that transmission upgrades needed by 2050 could cost up to $26 billion. (See ISO-NE Analysis Shows Benefits of Shifting OSW Interconnection Points.)

“We need to think about the grid in a different way,” Sosland said, adding that transmission infrastructure throughout the Northeast has been developed largely project by project, leading to projects scattered across the map like “a game of pick-up sticks.”

Meanwhile, several studies have found that increased interregional transmission capacity throughout the Northeast could bring cost, reliability and decarbonization benefits to ratepayers.

The U.S. Department of Energy specifically highlighted congestion issues between New York and New England in its 2023 National Transmission Needs Study, which found the need for an additional 3.4 to 6.3 GW of transfer capacity between the regions in scenarios with moderate load growth and high renewable energy penetration.

Along with resource adequacy benefits as intermittent renewables proliferate, increased interregional transmission capacity “provides resilience and consumer savings during extreme weather events,” the study wrote.

The study cited an analysis by Grid Strategies which found that during the “bomb cyclone” cold snap in the winter of 2017/18, ISO-NE, NYISO and PJM each “could have saved $30 [million to] $40 million for each gigawatt of stronger transmission ties among themselves or to other regions.”

Analyses have also projected significant cost benefits of increased two-way transmission capacity between Quebec and the northeastern U.S., with hydropower balancing out intermittent resources and limiting the need to overbuild clean energy.

Notably, the nonprofits behind the effort represent both sides of the border; the Acadia Center is based in New England, while Nergica is based in Québec.

Frédéric Côté, general manager of Nergica, said one of the key goals of the forum is to help projects that address pressing transmission needs to overcome the hurdles that have caused cancellations and delays in recent years.

Transmission planning historically has occurred “mostly jurisdiction by jurisdiction,” Côté said. “We feel that there is a need to rethink how it is done.”

“Time is of the essence if we want to achieve carbon neutrality by 2050,” Côté said. “We think we need to bring as many people as possible around the table to put together a road map for the region.”

In 2023, a coalition of states launched the Northeast States Collaborative on Interregional Transmission, which has since grown to 10 states. (See Northeast States Detail Early Efforts on Interregional Tx Collaborative.) The NGPF is not intended to replace or be redundant with this collaborative, but instead is aimed at engaging a wider set of communities and stakeholders, the organizers said.

The forum is initially envisioned as three roundtables focused on different themes: environmental justice and community mobilization, interregional planning, and clean energy procurement and markets development.

Reflecting on the recent struggles of projects like the Twin States Clean Energy Link, Côté called for a greater focus on tangible community benefits, as well as on market reforms to better facilitate bidirectional power exchanges across the U.S.-Canada border. (See National Grid Backs out of Twin States Clean Energy Link Project.)

“It’s not that easy to envision bidirectional exchanges in the current market state,” Côté said.

Rob Gramlich, president of Grid Strategies, said there is no “magic bullet” to prevent project cancellations, “but having greater regional buy-in on new lines sure would help.”

“Ideally, we need the key policymakers that are engaged in that forum to have some high-level conceptual agreement on a plan and a way to allocate the costs,” Gramlich said.

The forum’s organizers say they hope to hold in-person roundtables over the coming fall or winter and have met with different stakeholder groups to plan and gauge interest.

“We’re in Phase 1 of really testing ideas and getting input,” Sosland said. “We will then do an internal assessment in early May about whether there’s enough interest and support to expand this into a larger phase.”

While nothing is set in stone, Sosland and Côté said they’re encouraged by the feedback they’ve received.

“We’re getting really exciting responses to this,” Sosland said. “If things proceed, we want to be very optimistic about the interest in moving this into an actual forum, actual roundtables and actual discussions.”

California energy officials are attempting to calculate the “nonenergy benefits” (NEBs) and social costs of decarbonizing the state’s electricity grid.

This assessment is a provision of California’s Senate Bill 100, which requires 100% of electric retail sales be supplied by renewable and zero-carbon resources by 2045.

In an April 16 California Energy Commission (CEC) workshop, regulators and advocacy groups dove into the complexities of modeling for and evaluating NEBs, which “represent an array of diverse impacts of energy programs and projects beyond the generation, conservation, and transportation of energy,” according to the CEC.

“All Californians have a stake in this process as we move forward and envision what the world will look like and think about the impacts on health, air quality, greenhouse gas emissions, and of course, how we think about electricity bills and the Californians who are bearing the cost of the energy transition,” said Alice Reynolds, president of the California Public Utilities Commission (CPUC).

In February, a collection of state and local organizations, including the Center for Biological Diversity, the California Environmental Justice Alliance and the Local Clean Energy Alliance, petitioned the CEC to adopt an order requiring the integration of NEBs and social costs into resource planning and decision-making processes.

“The CEC is long overdue in satisfying statutory mandates to consider NEBs and social costs in its decision-making,” the petition states. “Until the agency does, the CEC’s decisions will continue to ignore the local environmental impacts — that fall disproportionately on disadvantaged and other environmental justice communities — of energy production and contribute to leaving the same communities behind in the clean energy transition, risking the overall achievement of SB 100 and other state climate policy.”

SB 100 requires the CEC, CPUC and the California Air Resources Board (CARB) to issue a joint report every four years. The next report, expected in January 2025, will be the first to formally include NEBs and social costs.

Decarbonization Will Bring ‘Vast Health Benefits,’ CARB Finds

Integrating analysis of NEBs and social costs into resource planning and SB100 implementation is a collaborative effort, and each agency discussed its anticipated tools and planning methodologies.

Bonnie Holmes-Gen, health and exposure assessment branch chief at CARB, presented tools used in the board’s 2022 Scoping Plan, which sets a 2045 decarbonization goal, that will be central to analyzing NEBs and social costs, including a health analysis conducted for all rules the board considers.

Central to the analysis is the “incidence-per-ton” method that assesses the health benefits of emissions regulations and resultant avoided health outcomes, including asthma, cardiovascular problems and death. CARB used this methodology in its Scoping Plan to analyze the impacts of direct and indirect particulate matter and nitrous oxide pollution associated with fuel combustion., It estimated the regulations needed to meet 2045 climate goals would result in $200 billion in healthcare savings, almost 2,000 cases of reduced mortality, thousands of avoided hospital visits and more than 300,000 cases of reduced asthma symptoms.

CARB used a Climate Vulnerability Metric to identify the economic costs of climate impacts, referred to as the social cost of carbon. The method applies a dollar amount to the long-term damage done by one ton of greenhouse gas emissions in a given year and represents the value of damages avoided by reducing emissions. Using this tool, CARB estimated implementation of the Scoping Plan would avoid $6.5 billion to $23.9 billion in climate damages by 2045.

“In comparison to the estimated direct costs for the Scoping Plan, this provided a very clear picture of the vast health benefits for action that far outweigh the costs,” Holmes-Gen said.

CARB plans to apply these tools to the NEB and social cost assessment for the 2025 report.

CEC’s standard capacity expansion and production cost modeling will produce data that can feed into the nonenergy impacts analysis, as well, said Liz Gill, reliability branch manager at CECs Energy Assessments Division. However, the modeling done so far is at a balancing authority area level, so the data will need to be downscaled. The modeling results also do not include power plant locations.

“This means that without carefully vetted downscaling, we can’t evaluate, for example, how much reduced generation from gas plant X might impact the air quality and community and why,” Gill said. “So, if you take anything away from today’s workshop, that should be that data granularity is really the primary challenge in determining energy impacts at a community scale for this state-level analysis.”

CPUC Approach

The CPUC’s Integrated Resource Planning process is central to procuring the clean resources needed to provide societal benefits, said Dan Buch, energy division branch manager at CPUC. Utility code requires the commission to consider certain societal nonenergy impacts in its cost-effectiveness tests, which are another key tool that could be used to analyze NEBs.

In 2019, the commission authorized a pilot for a societal cost test, which uses values for avoided air pollutants, the social cost of carbon and a social discount rate to identify costs associated with certain resources.

But using the test did not lead to increases in renewable resources or distributed energy resource (DER) procurement, the presentation reads.

“The key finding was that using a societal cost test instead of a more traditional test, like a total resource cost test … didn’t actually lead to significant changes in procurement,” Buch said.

The societal cost adders are similar to the commission’s payments to meet greenhouse gas abatement targets and didn’t change the mix of DER and supply-side resources, he said. And because many clean energy programs and new resources are ratepayer funded, costs must be considered carefully.

“I think the key here is that prudent investments reduce system costs. Other investments that don’t reduce system costs need to be considered very closely because we are certainly facing some affordability challenges in California,” Buch said. “Things that are driving up utility rates both increase that pressure and make it harder for us to induce electrification decisions among customers.”

Perspective from Environmental Groups

Instead of relying on ratepayers, Mohit Chhabra, senior analyst at the Natural Resources Defense Council, suggested funding alternatives, such as the general budget, tax revenues or cap-and-trade programs.

“Higher electric rates mean higher bills. And it also means electricity is more expensive relative to fossil fuels,” Chhabra said. “High rates impact people on the income scale differently.”

Roger Lin, senior attorney at the Center for Biological Diversity’s energy justice program, has a different take.

“I’d like to challenge the assumption that DERs that deliver more community benefits and avoid harms increase rates,” he said. “We need to move past pitting public health and the environment against affordability.”

Rates began to increase in 2013, before the state set official electrification goals, Lin said, resulting in what he refers to as “the big mystery” of skyrocketing prices for power over the past decade.

Lin also disagreed with the CPUC’s analysis that use of the societal cost test did not change the resource mix. The test, he said, is inherently flawed, because it does not consider the millions of dollars in Energy Savings Assistance program funds available and relies on the assumption that ratepayers will fund everything.

“The test results and the methodology assume that only ratepayer funds were used and no federal or state subsidies. Of course, [decarbonization is] going to increase rates if you ignore all these subsidies that especially target disadvantaged communities,” Lin said in an interview with NetZero Insider. “Just assuming that other ratepayers are going to foot the bill is incorrect because there are lots of targeted subsidies for those populations.”

Lin also took issue with the CPUC’s use of a standard value for human life in the test when determining how much an individual would pay to avoid sickness. Because the value is standardized, it doesn’t consider that disadvantaged populations likely would pay less to stay healthy than a wealthier demographic. The test also assumes gas plants, which adversely affect air quality and health outcomes, are not retired.

Excluding these factors leads to skewed results, Lin said, scoring energy projects highly that are considered cost-effective but have adverse social impacts.

“We know that the local air quality around power plants is worse … and so if we’re looking for improvements in local air quality, how can we really track those improvements if we’re assuming those pollution sources are still there? And so that’s why they’re like ‘there’s not that much of a benefit,’” he said. “There’s not that much of a benefit because you’re not taking out the thing that poisons people.”

CEC acknowledged the challenges associated with modeling for NEBs and social costs.

“I just want to say that this is one of those really difficult and nuanced topics,” said Commissioner Siva Gunda. “It really takes a lot of thoughtfulness in making sure we have a conversation that ultimately benefits the people of California and making sure we uplift every community as we go through our clean energy goals.”

The state of Washington has announced financial aid for middle-income residents wanting to buy or lease electric vehicles. “We want to democratize EVs,” said Gov. Jay Inslee (D) at an event April 23 in the Seattle suburb of Tukwila.

Washington is the first state in the nation to fund electric vehicle leasing for people with modest incomes, said Mike Fong, director of Washington’s Department of Commerce, which will handle the grant program. The program is a way to deal with electric cars’ high costs and assist those who fall under certain income thresholds.

The legislature set aside $45 million for fiscal 2024-25 for this program from its revenue from Washington’s cap-and-invest program. To be eligible for assistance, an individual or family can earn up to 300% of the federal poverty level: no more than $45,180 annually for a single person or $93,600 for a family of four.

The new program will provide up to $9,000 in an “instant rebate” program for leasing a new electric vehicle for up to three years. It also provides $5,000 for buying a new electric vehicle or leasing one for two years. The program also provides $2,500 for buying or leasing a used electric vehicle.

The state estimates that four electric vehicle models will lease for less than $100 a month, while the most leased gas internal combustion cars cost roughly $500 a month.

Inslee said: “We know once people buy these vehicles, they stick with them.”

“Transportation is the biggest contributor to greenhouse gas emissions and harmful air pollution,” Fong said. “It is important that people who live in our most impacted communities, which tend to be urban and lower-income, have access to cleaner transportation options, including the choice of EV ownership. These rebates can help many more people all across the state buy or lease an EV.”

According to the Department of Commerce, anyone interested in the program would go directly to an EV dealer to learn about offers available in the state’s instant rebate program. If the consumer qualifies under the income requirements, the dealer “deducts the applicable rebate amount from the cost of the lease and then applies dealer, state and local fees to arrive at the total lease amount.” There’s no sales tax because EVs qualify for the state’s zero-emission vehicles exemption.

ERCOT is searching for alternatives to replace capacity that will be lost with the planned retirement of three gas-fired units near San Antonio.

The Texas grid operator issued a market notice April 22 saying it plans to issue a request for proposals for must-run alternatives (MRA) to avoid a more expensive reliability-must-run (RMR) contract with CPS Energy.

“Any decision on whether to enter into an RMR or MRA service agreement must evaluate the costs and benefits of the service,” ERCOT said.

The San Antonio municipality told the ISO last month that it planned to “indefinitely suspend operations” in 2025 of three gas-fired units at its V.H. Braunig facility. The three steam turbines, dating back to the late 1960s, have a combined summer seasonal net maximum sustainable rating of 859 MW. (See CPS Energy Plans to Retire 859 MW of Gas Resources.)

Spokesperson Milady Nazir said in an emailed statement that the units’ retirement is part of the municipality’s board-approved generation plan and that the units were nearing their “operational end of life.”

However, ERCOT’s reliability analysis identified “performance deficiencies” without the CPS resources on the system and determined the power plants are needed to support system reliability. In a filing with the Texas Public Utility Commission, the grid operator’s staff said the units’ retirement would load existing transmission facilities above their normal ratings under pre-contingency conditions.

ERCOT has asked the PUC for a good-cause exception from its protocols’ timeline for RMR and MRA deadlines because of resource constraints.

“We would prefer to come up with a different timeline that still meets all the technical requirements in the protocols but gives us a little bit more time to get that RFP out and work with CPS on what a budget might look like for those units,” General Counsel Chad Seely said at the Board of Directors’ Reliability & Markets Committee.

“We will continue to have collaborative discussions with ERCOT during their review process,” Nazir said.

Seely said the ISO’s exit strategy for the RMR will “ultimately be a transmission solution.”

“Now, if there are other resources that could fulfill an MRA, that would give us the equivalent, then we can substitute for those, and that’s part of the process here,” he told the R&M committee.

The board on April 23 approved the $435 million San Antonio South Reliability II project that addresses issues south of the city. It approved another reliability project last August, proposed by CPS Energy at a projected cost of $329 million, that addresses thermal overloads in the area. (See “$435M San Antonio Project OK’d,” ERCOT Technical Advisory Committee Briefs: April 15, 2024, and “Members Endorse $329M CPS Energy Reliability Project,” ERCOT Technical Advisory Committee Briefs: July 25, 2023.)

An RMR contract would be ERCOT’s first since 2016. ERCOT entered into an agreement with NRG Texas Power over a previously mothballed gas unit near Houston. The RMR contract ended in 2017, thanks partly to transmission facilities that increased imports into the region. (See ERCOT Ending Greens Bayou RMR May 29.)

Because RMR and MRA determinations support ERCOT’s transmission reliability, costs incurred under either agreement are shared by all market participants that serve load. Costs are allocated on a load-ratio basis.

CARMEL, Ind. — MISO announced April 24 that 123 GW of new generation spread across 600 applications are vying to enter its generator interconnection queue under the 2023 cycle.

The 2023 intake, composed nearly exclusively of renewables and storage facilities, is almost 50 GW smaller than the 2022 application cycle MISO has been processing. MISO said while the number of proposed megawatts is still “significantly higher than historical averages,” 2023’s submittals were tempered due in part to its new, FERC-approved suite of tougher conditions on entrants.

Of the 123 GW of 2023 entrants, MISO said 115 GW (93%) represent wind, solar, storage or a combination of renewables and storage facilities. New solar projects account for 50 MW, storage projects total 29 GW, wind projects clock in at 19 GW, and hybrid renewable and storage projects about 17 GW.

MISO said if all the 2023 submittals are certified and accepted, the MISO queue will grow to 348 GW.

MISO required developers of the latest submittals to pay double in entrance and staged queue study fees, be subject to automatic and escalating penalty charges, and confirm they’ve obtained land for projects. The RTO had delayed opening its 2023 queue application window until March to obtain FERC approval to implement the new requirements. (See FERC Rejects MW Cap, Approves MISO’s Other Stricter Interconnection Queue Rules.)

MISO said its stricter requirements will allow for quicker network upgrade studies because it cuts down on the number of speculative projects entering the queue and then dropping out. It said it expects “higher-quality and more viable projects entering the queue.”

“Although these changes have resulted in a reduction from the previous cycle, it still represents a large number of projects for the team to study,” Director of Resource Utilization Andy Witmeier said in a press release. “We will continue working with our stakeholders to refine the queue process.”

Witmeier also pointed out that MISO is awaiting about 50 GW in approved generation projects that have yet to complete construction due to “financing, supply chain issues, delays in permitting and power purchase agreement negotiations.” (See MISO: Reliability Risk Upped by 49 GW in Approved but Unbuilt Generation.)

At an April 24 Planning Advisory Committee meeting, MISO staff said the RTO still plans to file again to implement an annual megawatt cap on project submittals to the interconnection queue. FERC rejected MISO’s first attempt to cap its queue entries annually based on a formula. (See MISO to Try Again for Interconnection Queue MW Cap, Open Window for 2023 Requests.)

The RTO has said annual queue entries as large as 2022’s 171 GW aren’t sustainable for a system that peaks at about 125 GW in the summer.

At the Gulf Coast Power Association MISO-SPP conference in March, MISO’s Scott Wright said the RTO worries about the queue “getting killed by volume,” where it’s nearly impossible to process projects because the queue is in essence “sabotaged” by scores of low-quality projects that aren’t fully fleshed out before being entered.

UNION, N.J. — Innovation and in-state project development by engineers and thinkers will be key to New Jersey’s offshore wind future as the state advances its groundbreaking initiative to create an offshore power center that can connect to homes and businesses onshore, according to speakers at the Wind Institute Research Symposium.

The extensive scale of the task, and the lack of history in creating such a major transition, will mean the work of problem-solving engineers, entrepreneurs and academics will be critical to overcoming the expected and still-unknown hurdles, speakers told the audience at Kean University on April 12.

Leading a panel on OSW research and collaboration, Kris Ohleth, executive director of the Special Initiative on Offshore Wind, said that after working for 25 years in the sector, she sees the state at a critical juncture, sitting on the cusp of bringing OSW to reality.

“We said 20 to 25 years ago, ‘OK, we know these are going to be the challenges, and once we get through this development phase of offshore wind and we move to this phase of implementation that we are at today, someone’s going to figure it out,’” she said. “And those someones are you — you folks sitting here today.”

Present in the audience, and among those outlining their work, were many of the 40 participants in the institute’s fellowship program started last year. Among the topics tackled by fellows, and showcased at the forum, were the socioeconomic and policy implications of OSW projects, how to secure public support, the development of a weather station that could predict wind energy generation, and how to make more effective and quieter turbine blades.

Unknown Future

New Jersey is seeking to revitalize its OSW sector after Danish developer Ørsted in October withdrew its two projects planned for the Jersey shore: Ocean Wind 1, the state’s first OSW venture, and Ocean Wind 2, one of two projects awarded in the state’s second solicitation.

The withdrawal left the state with just one active project: Atlantic Shores. The Board of Public Utilities approved two more Jan. 4: Leading Light Wind and Attentive Energy Two. If they come to fruition, the three projects would have a capacity of 5,252 MW, a major step toward the state’s goal of 11 GW by 2040. But getting there is no easy task, Tim Sullivan, executive director of the New Jersey Economic Development Authority, told the group.

“This is not like flipping a switch and it’s going to happen,” he said. “There are big known unknowns that we are counting on innovation to bail us out of, of how we are actually going to deliver on the promise of offshore wind.

“No one’s ever done this before. No one’s ever put an 11-GW power plant off the coast of a major industrial state and plugged it into a grid that is not particularly new and made it come out of people’s houses,” said Sullivan, whose agency helped organize the event and provides financial support for OSW projects. “We don’t know exactly how that’s going to work. You all, and others around the world, are working on those challenges.”

Public Concern

Key to the success of the projects will be the public reaction as construction gets underway and the cost of transitioning to coastal wind generated power becomes clearer.

The most vigorous opposition to the projects has emerged from the commercial fishing industry, local residents and tourist businesses, who fear that turbines in the ocean will damage the local quality of life. Several presenters at the symposium focused on the issue and where the opposition stemmed from.

Dylan Irmiere, a Stockton University student and a fellow of the wind institute, said that in the two public opinion surveys he commissioned and conducted in New Jersey as part of his research, 46% of those polled — including residents in the shore area and the rest of the state — had no knowledge at all of the wind projects, and 41% had slight to moderate knowledge of them.

The research showed positive public support among respondents for OSW as a solution to fight climate change, he said. Only one in five believed there would be environmental harm, and about 58% thought the projects would help the environmental, while about 60% said they believed the farms would help the economy.

However, when the respondents were given additional facts — what Irmiere called “surface-level knowledge” — about project distance from shore, the predicted economic benefits and the background of developers, only 33% said they wanted the projects to continue, and nearly a quarter said they did not support the continuance of the projects.

The fact that nearly a quarter of people had concerns after the intervention “could mean that they are still lacking sufficient information to form an educated opinion,” Irmiere said. He added that even after survey respondents were given information about federal actions to protect marine animals, 31% were neither satisfied nor dissatisfied, suggesting they “could need” more information.

“Learning that providing information to respondents about the environment and the economy helps to form sentiments of offshore wind gains should be something that companies developing these projects, as well as the governments in local communities, focus on,” he said. “To encourage the public to think more positively, sentiments about offshore wind should be constructed in a way that demonstrates their effectiveness on the environment and the economy.”

The surveys also showed how turbine distance from the shore can affect public support: While about 33% agreed that three miles offshore was a “reasonable distance” to site turbines, that figure grew to 55% for 12 miles and 59% for 20 miles.

Aparna Varde, associate professor in the Montclair State University School of Computing, said she and a graduate student, Isabele Bittencourt, studied social media posts about the projects. Their work focused on sentiment analysis, looking at whether the prevailing sentiments expressed are positive or negative to offshore wind; and topic modeling, to see what issues were raised most in posts about the wind projects.

The pair used three different methods of analysis, and all three found that between 37 and 40% of the comments were positive and between 26 and 36% were neutral, Varde said. Between a quarter and a third of the posts were negative, according to her presentation. Still, the positive slant to the comments was far from overwhelming, she said.

Tracking Mammals Underwater

The impact on marine life of wind farms emerged as a potent issue early in 2023 when a series of dead whales washed up on New Jersey shores. Opponents have raised concerns that preliminary work on the wind farms contributed to the deaths, even though no construction has started and federal investigators have found no connection between the deaths and the wind projects.

State officials told the symposium they are taking steps to minimize any harm. Offshore wind developers pay a fee of $10,000/MW to the state Research and Monitoring Initiative (RMI), which to date has been awarded $65 million for research projects, according to speakers from the New Jersey Department of Environmental Protection and the BPU. The RMI has awarded $13 million of that money to research projects, including one that sends “ocean gliders” into the sea to collect data on water temperature, and the level of chlorophyll and pH in the water.

“These gliders are autonomous mobile platforms that are outfitted with a suite of sensors that collect really high spatial and temporal resolution data on water chemistry and physical ocean processes, like the seasonal formation and breakdown of the cold pool,” said Caitlin McGarigal, a research scientist at the DEP, referring to the seasonal stratification of cooler water close to the ocean bottom.

“This just sort of exemplifies the type of data that’s being collected on this project and how these data can be really useful for understanding wildlife movement and behavior,” she said.

Another RMI-backed project is using acoustic telemetry — “like an underwater E-ZPass” — to set up receiver listening stations that can rack species that have been tagged, she said. A third project is helping the National Marine Fisheries Service to expand a project that uses aerial tracking from planes to study the movement of whales in New Jersey waters, she said.

Staff Reveals Error in GI Queue Studies; Clearing Backlog Still on Course

AURORA, Colo. — SPP staff publicly alerted stakeholders last week that it failed to conduct a tariff-required analysis of several generator interconnection queue study clusters as they reduced the backlog of GI requests dating back to 2017.

SPP’s Casey Cathey, senior director of asset utilization, quoted his late father, a salesman, as he broke the news some members already were aware of during the Markets and Operations Policy Committee on April 16. He said SPP discovered it “inadvertently” failed to conduct a contingent facility review for five clusters, beginning with the 2017-001 grouping through the 2020-001 collection.

“[My father] would say, ‘You don’t lose customers by making mistakes; you lose customers in how you handle those mistakes,’” Cathey said. “We made a mistake. That’s just plain and simple.”

SPP plans to handle this mistake using two processes dependent on the cluster study’s progression. Once SPP has determined which interconnection requests in the affected clusters are contingent on previously assigned network upgrades, it said generator interconnection agreements will have to be amended to include the contingent facilities.

Until then, GI requests in the affected clusters that were not identified by SPP during the study process may be contingent. Those projects may be subject to limited operations until the contingent facilities are in service. Additionally, requests in the clusters in question could be assigned the cost of those facilities should higher-queued GI requests not build them.

“This is a big deal, and it’s a big deal with a number of tentacles to it,” the Advanced Power Alliance’s Steve Gaw said. “When this first came out, it really did send shock waves through the developer community. We are still in the mode of dealing with, ‘What does this do?’

“What we want we don’t know yet, and what’s going to be yet to develop is what the ultimate impacts are to the generation that’s in this queue, and to the investments that have already occurred,” he added.

The grid operator includes clearing the GI backlog of all requests submitted through 2022 by the end of the year as a priority for 2024. According to a timetable, it would post the last contingent facilities remedy, for the 2020-001 cluster, in August. The active queue contains 421 requests for 87 GW of capacity; it numbered 1,139 requests for 221 GW when the backlog-clearing effort began.

“We’re still very much pushing to make that goal by the end of this year,” Cathey said. “We have to resolve this. We recognize how important this is and we have to resolve that in a way that minimizes the impact to the customers.”

He said SPP will post contingent facilities cluster study reports and amend GIAs as required. Developers with GI requests should review all their projects, especially those in affected study groups, he said. Those nearing commercial operating dates or subject to 0 MW due to contingent facilities can request the RTO perform a limited operation system impact study (LOSIS), with a group LOSIS offered to those in service or expected to be in service within 18 months.

“This is a serious error and we’re working with the developer community to come up with a very tight remedy plan to rectify this,” Cathey said, adding that he welcomes other novel ideas to accelerate the plan.

Record Tariff Changes?

Members took up 26 tariff revision requests during the two days, leading MOPC chair and ITC Holdings’ Alan Myers to posit that the number may be a record. The committee took no action on one of the RRs, but the other revisions and voting items passed with an average 96% approval.

A proposed revision incorporating western entities into SPP’s resource adequacy process when they join the RTO’s markets failed initially, securing only 53.4% of approving votes. When the motion’s language was amended to clarify that deliverability across the DC ties would only include firm transmission service, the motion passed with 83.1% approval.

MOPC also delayed action on RR620, which would implement SPP cost-allocation policies for Joint Targeted Interconnection Queue (JTIQ) projects. However, the RTO’s staff, transmission owners and SPP’s JTIQ partner, MISO, have been unable to reach consensus over the rate template in pursuit of a more efficient “direct billing” approach. The committee agreed to a conference call April 26 to wrap up the tariff revision, but the meeting was cancelled April 22. Staff said the work to finalize RR620 is ongoing.

SPP and MISO have agreed to assign 90% of the JTIQ portfolio’s $1.06 billion in costs for its five projects to generation. Load will cover the remaining 10%. (See MISO, SPP Propose 90-10 Cost Split for JTIQ Projects.)

The committee endorsed five other RRs that, if approved by the board, would:

RR600.8: Add an incremental market-efficiency use charge to provide revenue offsetting incremental DC tie operations costs due to their market dispatch. The charge would be levied proportionally to all market participants’ activity, including those with export and virtual transactions.

RR605: Define an authorized outage and criteria, add requirements for resources’ availability during both the summer and winter seasons (unless on an authorized outage), help load-responsible entities and generation owners better understand when to submit resource adequacy (RA) capacity when providing workbooks to meet the RA requirement.

RR608: Allow new generation resources to operate with fewer restrictions during seasons where interconnection studies did not identify transmission constraints prior to the completion of all network upgrades, while still restricting those generators in seasons where interconnection constraints were identified.

RR612: Modify the multiday economic commitment to allow long-lead resources to receive market commitments for purposes beyond reliability.

RR616: Ensure any outage not approved by the SPP balancing authority and not an outside management control event is accounted for in performance-based accreditation (PBA).

MOPC also approved separate measures imposing resiliency options and correlated changes to the 2025 Integrated Transmission Plan and removing the voltage stability analysis from the 2024 ITP study. It also endorsed a price-formation policy to dispatch resources based on the true obligation and price the system using the obligation without the impact of the load shed and emergency pricing assistance.

SPC OKs Forecasting Task Force

Meeting after MOPC, the Strategic Planning Committee endorsed staff’s recommendation to create a task force to improve regional load forecasting that tends to come up short.

Staff said even its lowest scenarios for peak load in winter forecasts exceed members’ load expectations for resource adequacy. Summer load forecasts during ITP submissions exceed the lowest growth assumptions and remain below trends for more rapid growth, they said.

“Can we be better?” SPP’s Cathey asked, drawing responses of agreement from several members. “From a regional perspective, it’s 100% driven by the responsible entities and populated by members, so it’s fully through member input. The question is, how can we put a little bit more attention to this to get a little bit more accuracy in the use cases and providing better data with changing, unconventional loads?”

Pointing out that some members have more sophisticated tools than others, “depending on the size of their shop,” Cathey said staff has reached out to some members as well as SPP’s fellow grid operators to gather data for the task force. He said SPP intends to keep the task force’s membership small, but open, and focused on employees with planning responsibilities.

Cathey said staff believes defining improvements to regional planning would take eight months. He promised a checkpoint at year’s end, with some long-term solutions handed to other stakeholder groups.

The SPC meeting was conducted with a somewhat unusual seating arrangement. The committee’s leadership headed a U-shaped arrangement with SPP’s rostered members. Behind the main table, another U-shaped arrangement gave interested onlookers a view of the backs of the committee leadership’s heads.

“Sorry, I have worked my way up from coach in the back,” quipped SPP’s Robert Fox, director of enterprise architecture, as he belatedly joined the main table to comment.

Last MOPC for Dowling

The MOPC meeting was the last for Midwest Energy’s Bill Dowling, who is retiring after 39 years sitting in the committee and other SPP meetings — or, as Midwest’s vice president of engineering and energy supply said in referring to the number of years he has spent with the RTO, “a lot.”

Myers began the meeting by singling out Dowling for recognition. Like Myers, Dowling has served as the committee’s chair.

“I’ve gotten to know a lot of really great people,” he said. “It’s been a pleasure working with some really smart people. It makes me look good.”

Committee Consents to 19 RRs

MOPC’s unanimous approval of the consent agenda endorsed 19 RRs, 10 of which will go to the board for further consideration:

RR555: Adds requirements to the operating criteria addressing FERC cold-weather recommendations.

RR600.7: Integrates western entities seeking RTO membership under SPP’s terms and conditions with updates that include a DC tie access charge.

RR600.9: Adds a separate balancing authority area on the western side of the DC ties to the SPP BA.

RR600.10: Awards auction revenue rights and transmission congestion rights to the alternating current portion of transmission service that cross DC ties between the Western and Eastern Interconnections. Settling the rights will occur in two stages, with the AC portions settling in the respective interconnection.

RR600.11: Renames the tariff’s Attachment AN to Addendum 1 and adds language specific to western entities joining SPP as members of the West BAA.

RR600.12: Includes a separate BAA on the western side of SPP’s DC ties and other necessary market design clarifications adding policies necessary to integrate western parties into SPP.

RR600.13: Bases some rates for point-to-point and network service on the western side of the DC ties and the associated revenue distribution on the amount of annual transmission revenue requirement specific to the facilities in an interconnection. This accommodates Western Area Power Administration’s Upper Missouri and Rocky Mountain Region zones, which have facilities in both interconnections.

RR600.14: Adds language clarifying West DC ties as constraints, similar to other transmission constraints that are part of the market power test and frequently constrained areas validations.

RR600.16: Revises contract services agreements with WAPA-Upper Great Plains by removing language related to the Western Energy Imbalance Service market and narrowing the list of WAPA-UGP facilities to only those that are and will remain in the NorthWestern Energy BAA.

RR607: Implements the Regional State Committee’s change to the tariff’s safe harbor provisions, from 125% to 100% plus the higher of summer or winter season planning reserve margin plus 10% (but not less than 125%).

NEW YORK ― In recent years, fossil fuel industry leaders have been extremely careful and strategic with the words they use when talking about the role that, in their view, the industry should play in the global energy transition. Public messaging has argued for a “low-carbon” future, rather than no carbon or even net zero.

A series of presentations and panels on the second day of the annual BloombergNEF Summit last week provided a measure of the industry’s success in crafting a narrative based on a “balanced” and well-paced transition that includes cutting its most egregious emissions ― methane ― and scaling carbon capture and storage technologies.

For methane, the focus is first on accurately measuring emissions that clearly have been underestimated and then developing best practices that will allow the industry to certify that its natural gas is “responsibly sourced.”

Scaling carbon capture is simultaneously a more pressing and difficult challenge. BNEF predicts the still-emerging sector for direct air capture (DAC) must be able to suck 1 billion tons of carbon dioxide out of the atmosphere by 2050, but the current pipeline of projects will capture only 11 million tons by 2030.

CCS, used for capturing emissions from fossil fuel plants and other hard-to-abate industrial facilities, has a stronger pipeline, with federal and private backing for a range of projects, from a demo at a U.S. Steel plant in Indiana to a major multistate effort gathering emissions from 57 ethanol plants.

The subtext throughout was that the industry’s approach to decarbonization is bottom-line-driven and based on its traditional business models.

The Industry Argument

Her job title notwithstanding, Anna Mascolo, executive vice president of low-carbon solutions at Shell, deftly avoided the term “low carbon,” talking instead about a “balanced” transition to “lower-carbon” technologies. Similarly, she spoke of Shell’s “traditional business,” not fossil fuels, oil or gas.

The energy transition “is not a switch you can do on [or] off,” Mascolo said in an onstage discussion April 17 with Alix Steel, co-anchor of Bloomberg Markets. “We need to deliver energy today for our customers and then help them transition towards the lower-carbon options.”

Joining Mascolo and Steel, Jeff Gustavson, president of Chevron New Energies, argued for a longer-term, all-of-the-above energy transition. “The energy system has always been in transition, and typically, it’s not one energy source completely replacing another source,” he said.

Both Shell and Chevron have set targets for becoming net-zero businesses by 2050.

But as the demand for energy and the global population continue to grow, so will the need for reliable, affordable and “ever cleaner” power, Gustavson said. “To grow these new global businesses, we need collaboration; we need to lower the cost of these resources; and we need all of the capabilities that companies like ours have today and more to make this successful.”

He pointed to CCS projects Chevron has in the works ― often partnering with other companies, including Shell ― where the company can use its “deep … technical, commercial [and] operating capabilities.”

Shell is looking for markets in transition where “we feel we can play [to] our strengths,” Mascolo said; for example, the niche market for lower-carbon aviation fuel. “We won’t be everything for everyone, and we’re looking for products as well as customers in sectors where we can really have a competitive advantage and … [can] build on the current customers we have today.”

The company also is focused on “making sure [it] gets the pace right,” Mascolo said. “So, then you are investing as your customers progress and as society progresses, as the regulatory environment progresses, and then the utility position is different in different places.”

Last year, Shell invested $5.6 billion in low-carbon solutions, or about 23% of its capital spending, Mascolo said.

Gustavson said Chevron continues to be “inundated with opportunities” in the low-carbon sector, but to invest billions in any new technology, the company expects to see “attractive returns. So, for us, that’s double-digit returns. …

“We look for two things,” he said. “Will it scale? Is it a solution that works? And that comes down to cost primarily. And do we offer something that adds value,” where the company can use its capabilities for competitive advantage?

Right now, the answers to those questions are “yes” for renewable fuels, hydrogen and CCS, he said.

“Scaling CCS is the next challenge, and I see that happening in the years to come,” Gustavson said. “Hydrogen is the most exciting. It’s also the hardest to effect because you’re changing an entire energy system and entire value chain, from production [and] transport to consumption.”

Methane

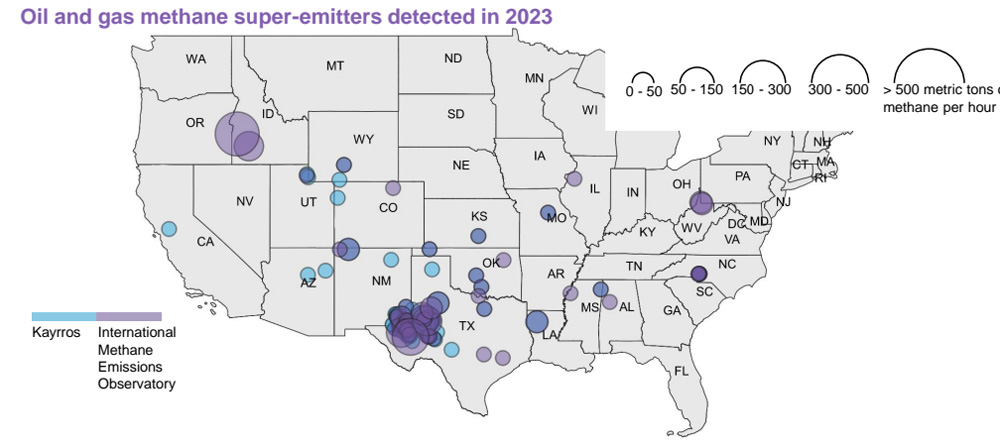

With 84 times the warming power of carbon dioxide but a much shorter lifespan, methane sets the pace of global warming and could have a major impact on whether the world’s nations can limit climate change to 1.5 to 2 degrees Celsius, said David Doherty, BNEF head of oil and renewable fuels research.

The problem, he said during his April 17 talk, is that methane emissions are difficult to measure and therefore almost universally underestimated.

EPA has produced two different measurements of methane emissions, one from its Greenhouse Gas Reporting Program (about 3 million metric tons (MMT)), and another from its inventory of greenhouse gas emissions (close to 9 MMT), according to BNEF.

Those figures may not include outliers, such as super emitter events in which significant amounts of methane are emitted in a short period of time. Super emitters account for only 5% of emission events but as much as 50% of emissions, Doherty said.

Similarly, low-production, or marginal, wells pump out just 7% of the nation’s oil and gas but make up 80% of total wells, and they also produce “a disproportionately large amount of methane,” Doherty said. He cited a study from the Department of Energy, which found that marginal wells produce an estimated 1 million tons of methane emissions per year, 60% from natural gas and 40% from oil.

BNEF estimates that super emitters make up 5% of methane emitting events but about 50% of methane emissions. | BNEF

The reason for this wide range of figures is that counting methane “is very complicated,” Doherty said. “It works off of a series of very simplistic estimations and assumes that business is operating as normal, continuously, with minimal methane leakage. We know this is actually not the case. …

“You can have a barrel of oil with very similar specifications but completely different methane emission profiles,” he said.

Getting a solid grip on methane emissions will require a set of best practices, such as the standards developed by the U.N.’s Oil and Gas Methane Partnership (OGMP) 2.0, which includes 95 oil and gas companies producing 35% of the world’s oil and gas.

The partnership has developed a five-phase, measurement-based reporting system, going from country or state level to specific site level, backed up with satellite or other monitoring systems, Doherty said.

Using OGMP figures, BNEF estimates that in 2024, 45% of U.S. gas will be certified as “responsibly sourced” or gas with a low methane footprint, which could provide a price premium as “emission-savvy and emission-sensitive buyers” seek out low-emission gas, Doherty said.

Certainly, greater scrutiny of methane emissions is coming, and companies that have yet to do so might want to get to work on measuring their methane footprints, he said. “Because if you don’t, somebody else is apt to do it for you.”

Direct Air Capture

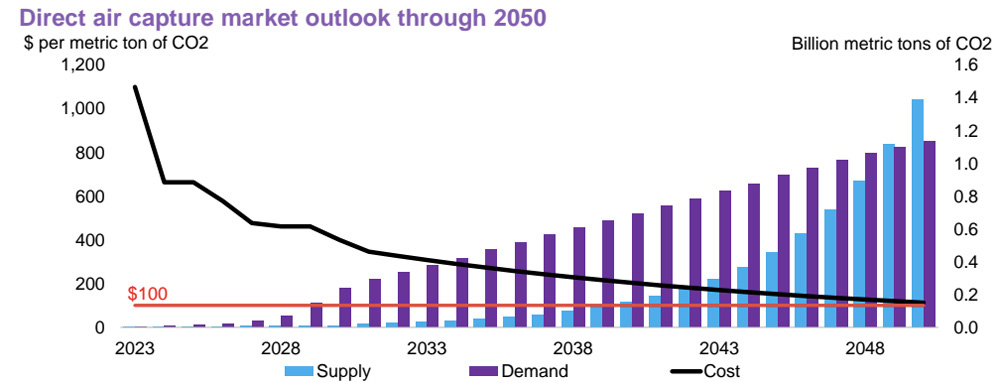

Getting a clear idea of 1 billion tons of CO2 requires a serious exercise of the imagination, according to Brenna Casey, a BNEF carbon capture analyst.

BNEF’s target for DAC by 2050 is “equal to roughly 175 million male African elephants,” Casey said during her April 17 presentation. Lining them all up, trunks to tails, “you could stretch from the Earth all the way to the moon and then some.”

Right now, the sector is nowhere near on track for that target, she said. “All the direct air capture capacity is limited to these small-scale plants,” Casey said. The largest is Climeworks’ Orca plant in Iceland, which is capturing 4,000 metric tons (MT) of CO2 per year, she said.

The largest in the pipeline is 1PointFive’s Stratos project in Texas, which broke ground in June 2023 and will be able to capture 500,000 MT of CO2 per year when it is slated to come online in 2025. 1PointFive is a subsidiary of Oxy, formerly Occidental Petroleum.

According to Casey, scaling DAC likely will depend, first, on developing technologies that bring down cost and, second, building a market for the carbon credits produced by the monetization of the carbon captured and stored.

Early DAC projects have used amine and absorbent technologies, while other developers are working with metal oxides and zeolites, Casey said. Used in the Orca plant, amines are based on a derivative of ammonia and can capture carbon molecules. Zeolites combine silicon, aluminum and oxygen and can be used to absorb CO2.

The main difference between older and new DAC technologies is their energy use. Metal oxides and zeolites require about a third less power than amines and other older absorbent methods, according to BNEF.

BNEF pegs the average price for DAC right now around $1,100/MT. The target price point for reaching that 1 billion ton scale by 2050 is $100/MT, Casey said, with economies of scale and lessons learned through construction and operation playing a vital role in moving down the cost curve.

BNEF predicts that by 2050, demand for direct air capture projects will outstrip demand and prices will fall to about $100/MT. | BNEF

Most of the early, first-of-a-kind plants, like Stratos, are “large, fully integrated … like oil refineries in the sky,” she said. “So, they’ll achieve economies of scale naturally, but at the same time, this forfeits the ability to be highly modular, and we’re likely to see [lower] learning rates.”

Casey predicted prices for such projects to be about $200 to $300/MT. At least one obstacle to further cost cuts is a lack of a “leading technology,” she said. “So maybe the industry has to pick a winner and coalesce around one or two technologies and develop those supply chains in tandem.”

CCS, Make or Break

The case for CCS is rooted in the need to cut emissions from “hard to abate” industries such as cement and steel and has therefore been a focus for both federal and private funding. Technologies that can help move the sector down the cost curve will be vital for CCS as projects face make-or-break points, as detailed in another April 17 panel.

Kelly Cummins, acting director of DOE’s Office of Clean Energy Demonstrations (OCED), ran down a list of CCS projects that have received federal funding. Three of the seven hydrogen hubs OCED announced in October will be using “large-scale carbon capture,” she said.

OCED also recently announced $6 billion in funding for 33 industrial decarbonization projects, and “a large swath of those projects … are going to be using CCS,” she said. For example, Ørsted received funding for a carbon capture project that will turn the CO2 from an industrial plant into ethanol to be used to make an alternative fuel in the shipping and transportation sector, she said.

Projects in the private sector include U.S. Steel’s efforts to decarbonize its plant in Gary, Ind., which produces 5 million tons of steel per year, and the associated emissions, said Erika Chan, the company’s head of sustainability.

The company recently signed a memorandum of understanding with CarbonFree, a carbon capture developer focused on the industrial sector. According to CarbonFree, its technology will capture 50,000 MT/year at the Gary plant, turning it into nontoxic calcium carbonate that can be used for a range of manufacturing applications, from paper and plastics to building materials.

Summit Carbon Solutions has grabbed national headlines with its plans for a CCS project gathering CO2 emissions from 57 ethanol plants across Iowa, Minnesota, Nebraska and the Dakotas and transporting them via pipelines to an underground storage site in North Dakota.

CEO Lee Blank emphasized that local education and community engagement have been critical to getting the project close to shovel-ready, with 2,100 public meetings across the region. Summit now has about 75% of the rights of way it needs for the entire project, including 80% in North Dakota, he said.

But beyond cost and technology, Claude Letourneau, CEO of Canadian CCS developer Svante, said the industry needs a shift in perspective from the energy transition to an industrial transition that takes the whole CCS process into account, from collecting and transporting emissions to storing or reusing them.

The industry should focus on measuring and reducing the carbon intensity of emissions, he said. “Every single industry needs to have a carbon intensity target that is regulated, and then you’ve got to go down that curve over time,” he said. “You’ve got to manage the CO2 emissions associated with industries and … until we do this, it will be very difficult” to scale CCS.

FERC once again has said it needs more information on clearing price caps before MISO can proceed with sloped demand curves in its capacity auctions.

The commission issued a second deficiency letter April 23 on MISO’s plan to swap in sloped demand curves for its current vertical curve in its seasonal capacity auctions (ER23-2977).

FERC asked about the sloped demand curve design’s opt-out provision to preserve state authority and lack of clearing price caps, among other details, late last year. (See FERC Wants More Detail on MISO Sloped Demand Curve Plan.)

This week, the commission again zeroed in on MISO’s removal of its annual price cap for auction clearing prices as part of the move to sloped demand curves. It said it needs more explanation behind the RTO’s proposal to eliminate the yearly cap.

MISO has said once it implements the new curve design, the total annual price for a local resource zone could reach as high as four times the cost of new entry (CONE), depending on whether capacity shortages occur in all four seasons of the auction. However, the RTO has not explicitly listed an annual price cap in its new tariff language, telling FERC it is not necessary because its plan is clear that clearing prices will be capped at the seasonal CONE. It also said there’s only a small chance a zone would experience shortage conditions in all four seasons and if that occurred, the more-than-$1,300/MW-day prices that ensue would properly reflect an “extreme” situation.

MISO’s current auction design employs a 1.75-times-CONE price cap for a local resource zone. This year’s CONE averages $330/MW-day. The RTO has said its sloped demand curves would not allow prices to jump automatically to CONE values for small capacity shortages below reserve requirements, unlike the current, unyielding vertical demand curve.

Nevertheless, FERC asked MISO to shed more light on why it believes it is appropriate for prices to go as high as four times the cost to build new generation and how those price signals could incent more generation to show up.

FERC also asked for MISO to better explain why its current CONE cap would “degrade market efficiency and transparency when implemented with price-sensitive demand curves” like its sloped demand curve. The commission said it needed to hear more justification for the four-times-CONE construct versus the existing annual cutoff. It also questioned MISO’s stance that any “ex post adjustment of prices could lead to suboptimal resource adequacy outcomes.”

Projected load growth nationwide from data centers, electrification and increased domestic manufacturing will drive increasing demand for renewables through the next decade, NextEra Energy CEO John Ketchum said during the company’s first-quarter earnings call April 23.

“We believe the U.S. renewables and storage market opportunity has the potential to be three times bigger over the next seven years compared to the last seven, growing from roughly 140 GW of additions to approximately 375 to 450 GW,” Ketchum said.

Ketchum said the domestic solar supply chain is “much improved from two years ago,” asserting that manufacturing capacity has increased and inflationary pressures are easing.

“The U.S. will need a significant and growing amount of electricity over the next decade and beyond, a large part of which will be powered by new renewables and storage,” Ketchum said.

Ketchum said the ability to put solar and battery resources wherever needed will make them especially valuable in meeting demand from data centers in coming years.

The company reported that subsidiary Florida Power & Light placed in service 1,640 MW of solar in the first quarter, while NextEra Energy Resources had its best quarter for solar and storage origination, adding 2,765 MW to its backlog.

CFO Kirk Crews said FPL now owns and operates more than 6,400 MW of solar resources, “the largest utility-owned solar portfolio in the country.”

FPL’s 2024 10-year plan also doubled its battery storage deployment target compared to 2023, with the target now totaling 4 GW. The utility also plans to deploy 21 GW of solar over 10 years.

Crews also announced NextEra Energy Partners plans to repower an additional 100 MW of wind capacity, increasing its wind repowering target to about 1,085 MW through 2026.

Responding to a question about the potential of small modular reactors to help meet data center demand, Ketchum said he is “a real skeptic in SMRs coming into the picture to satisfy data center demand anytime in the near future. … SMRs are still a decade to 15 years away.”

NextEra reported GAAP net income of $2.27 billion ($1.10/share) for the quarter, an 8.72% increase over the same quarter last year. This was off a 14.67% decrease in total revenue for the quarter from last year’s $6.716 billion.