Empire Wind developer Equinor says it’s optimistic it can complete work on the $7.5 billion offshore wind project and start selling electricity to New York on schedule.

But the court fight continues with the Trump administration, CEO Anders Opedal said Feb. 4 during Equinor’s year-end earnings call.

Work on the 810-MW project has been halted twice by the administration and resumed twice by the Norwegian developer, once with the administration’s permission and once with a federal judge’s preliminary injunction against the stop-work order.

In court papers, Equinor estimated the impact of the April 2025 halt at $200 million. Opedal told financial analysts that the company views both stop-work orders as illegal but said the December 2025 halt was much less costly.

He said work is more than 60% complete, with the offshore substation, nearly 186 miles of cable and all monopile foundations installed.

About $3 billion in capital expenditures remain on the $7.5 billion project, Opedal said. Revenue from operations ($155/MWh) and monetized federal investment tax credits (approximately $2.5 billion) should cover outlay of all known upcoming costs, he said, but added: “We, like other companies, remain exposed to uncertainty when it comes to possible future tariffs.”

A financial analyst asked how Equinor feels now about retaining 100% ownership of Empire Wind, formerly a 50-50 venture with bp that was dissolved after the U.S. offshore wind industry ran into spiraling costs in 2023. (See Offshore Wind Reset Complete in New York.)

“This is definitely something to reflect on,” Opedal said. “We normally don’t take 100% in any license.

“We de-risked it somewhat with higher strike prices, with a financing package, and then as you’ve seen, the political risk with the new administration was higher than anticipated.

“This is a trend now we see in several countries,” Opedal said, not just in the United States: Energy investments have become more politicized and polarized.

He will be looking for strong bipartisan support for future projects and considering carefully how to move forward with any project that proves divisive.

“With the political changes we’ve seen … we probably would have thought differently about Empire Wind in the past,” Opedal said.

An analyst asked him to handicap the court fight in the United States.

“This is a little early to say,” Opedal said. However, he noted the other four U.S. offshore wind projects also won injunctions against the Trump administration’s December stop-work order, which is a promising sign. (See With Sunrise Wind Ruling, OSW Industry now 5-0 Against Trump Admin.)

“But I’m an engineer, not a lawyer,” he added.

Equinor — originally and still primarily an oil and gas producer — also reported record fossil fuel production in 2025.

A financial analyst asked Opedal about Equinor’s commitment to the energy transition amid its recent pullbacks.

“We are signaling a consistency around oil and gas,” he said. The market view about offshore wind, hydrogen and particularly carbon dioxide transportation/storage has changed in recent years, he said, and Equinor’s customers have postponed their emissions reduction plans.

“Everyone had a 2030 target,” Opedal said.

Equinor will focus on wrapping up its existing offshore wind projects and place a “high bar” on any future investments in the sector, including through its investment in offshore wind leader Ørsted, he said.

Equinor reported 2025 net income of $5.06 billion or an adjusted $2.47/share on total revenues of $106.5 billion, compared with 2024 net income of $8.8 billion or an adjusted $3.24/share on total revenues of $103.8 billion.

LITTLE ROCK, Ark. — In preparing his first presentation to stakeholders as SPP’s operations vice president, C.J. Brown said he found himself staring at a blank slide.

“What am I going to talk about?” he had asked himself.

“I’ve regretted that statement because as soon as I thought that, I got a message about Winter Storm Fern,” Brown told stakeholders during the RTO’s quarterly update Feb. 2, referring to the late January frigid precipitation and cold. “Anytime a storm has a name that early in a week, it’s just not going to be a good deal.”

SPP issued a conservative operations advisory — the final notice before calling an energy emergency alert — during the storm, but above-average wind generation saved the day. Brown said forecasts of 11 GW were threatened by a risk of more than half that being knocked offline. However, the lack of icing conditions allowed wind resources to meet projections.

“Wind produced above accreditation by a significant amount … pretty much throughout the event,” Brown said. “Ultimately, we were very strong in that category, which allowed us to be able to support a lot of those in the Eastern Interconnection that were short. Wind was a large part of the story.”

The RTO continually exported energy to the east during the event, Brown said, peaking at around 3,500 MW. Thermal outages reached about 15 GW during the storm, but SPP was able to lean on its extra generation to help other grid operators.

The lowest temperatures came in the morning hours of Jan. 26, when demand reached a winter high of around 46 GW. Brown credited infrastructure investments and generation, system and transmission operators working together to help SPP breeze through the storm.

“It certainly takes a village to get through these storms,” Brown said.

SPP staff and the Market Monitoring Unit have both promised full reports on the grid operator’s storm response.

Nickell Thanks Members

More than 10 inches of snow and sleet fell on Little Rock during the storm. The wintry mix was then sealed by a layer of ice that made removal difficult. A week after the storm, many of the city’s side streets were still impassable, and mounds of white slush were piled high in parking lots.

The city’s school district canceled classes for the week, leaving many residents stranded in their homes amid sub-freezing temperatures. Chuck Hutchison, a member of the Nebraska Power Review Board, noted temperatures were lower in Little Rock than in Omaha the day before the quarterly briefing.

“We really wanted to make our commissioners from North Dakota and South Dakota feel more at home. Plenty of snow,” SPP CEO Lanny Nickell said in welcoming the Regional State Committee. “I’m sure [the snow] makes a lot of you feel more comfortable if you’re coming from the northern part of our region. We don’t like it down here.”

He thanked members with “heartfelt gratitude” for their efforts and collaboration in avoiding regionwide outages.

“It does mean a lot to be able to work as closely as we do with all of you who serve customers and have that responsibility to work with us to keep the lights on,” he said. “The fact that it was a significant winter storm and we survived says a lot [about] the hard work that we have been doing since [2021’s] Winter Storm Uri, the policies that we put in place, [and] the procedures that I know our operators and your operators have improved to make better decisions well ahead of time so that we can keep the lights on, keep people warm and make sure that lives are saved.”

Casey Cathey, vice president of engineering, said staff are hoovering “all things transmission” to accelerate grid infrastructure and capacity through its Project Keystone, including 765-kV and other large transmission projects, the 2026 transmission plan, cost allocation and the transition to the Consolidated Planning Process. (See SPP ‘Blazes Trail’ with Consolidated Planning Process.)

“We’re scooping those up and making sure that we’re working those in tandem and collectively for a successful implementation of what we may need moving forward as a region,” he told stakeholders.

SPP is working with the Economic Studies and Transmission working groups to modify the 2026 Integrated Transmission Plan’s scope and address confusion over the proposed 765-kV overlay. The board approved four 765-kV projects in November 2025 but deferred several others from the $8.6 billion portfolio and committed to analyze the 765-kV overlay in the 2026 ITP assessment. (See SPP Board Approves 2025 ITP with 4 765-kV Projects.)

Staff will codify the overlay’s explanation for the Markets and Operations Policy Committee’s meeting in April. The 2026 assessment is on track, Cathey said, with the 30-day submission window for project proposals opening in late February.

“The 2026 ITP is looking to be our largest portfolio. We are anticipating tens of thousands of needs to solve,” he said. “The forecasts that we see in the 2026 ITP are that much greater than what we see in the 2025 ITP and what drove our four 765 facilities.”

Cathey dismissed talk of an AI bubble and said load requests from the 2025 assessment remain, with some accelerating from Year 5 to Year 2 in plans.

Hanging over Project Keystone is what Cathey calls the “cost problem.”

“It’s billions of dollars that we’re talking about on top of billions of dollars that were already approved, and that’s a lot more than we’re used to as a region,” he said. “We need to do whatever we need to do to make sure that we’re balancing encouraging these loads to show up with the region, but also that we’re fair to the existing ratepayers.”

The Department of Homeland Security’s Cybersecurity and Infrastructure Security Agency has released a resource to help critical infrastructure operators address the risk of threats from inside their organizations.

CISA’s Assembling a Multi-Disciplinary Insider Threat Management Team infographic, released Jan. 28, is aimed at critical infrastructure entities and state, local, tribal and territorial governments, according to a media release. The agency produced the document to provide “actionable strategies [and] guidance to proactively prevent, detect and mitigate insider threats” so entities can “stay ahead of evolving organizational vulnerabilities.”

Insiders — defined by CISA as those “with institutional knowledge and current or prior authorized access” — can do serious damage to an organization’s security by revealing sensitive information to rivals or malicious actors, damaging organizational reputation and even causing harm to employees and other assets. The agency reminded readers that insider threats don’t necessarily involve active malice, because “negligence or simple human errors can open the door to vulnerabilities that adversaries can exploit.”

CISA’s guidance urged organizations to take insider risks seriously and build a threat management team that can handle incidents involving physical security or cybersecurity, personnel challenges and partnerships with the community. Effective insider threat teams should draw from staff members with responsibility for security, including human resources, general counsel, operations and administration; members of leadership like the chief information officer; and external resources such as law enforcement and medical and mental health counselors.

The agency suggested adopting a framework of “plan, organize, execute and maintain” to guide the insider threat team.

Planning means defining the structure of the team and its scope by identifying priorities based on the organization’s risk tolerance, the assets that need protecting and how the team will be organized and fit into the broader entity, among other considerations.

Organizing entails guiding employee awareness of insider risks, encouraging a security and reporting culture, and providing support to departments that identify possible insider threat activity. CISA reminded readers that this aspect of the job “requires discretion” because the team will have to interact with sensitive and personal identifiable information, which should be kept secured and “handled with the highest degree of confidentiality.”

Execution involves the day-to-day work of gathering and managing information and leading the detection and assessment of potential threats. Steps in this work may include mandatory threat mitigation training for team members, establishing a central information hub and working with the organization’s legal counsel to ensure compliance with state, local and federal laws.

Finally, maintaining the team refers to the “ongoing and dynamic process” of adapting the team’s approach to the developing threat landscape. CISA advised readers to hold regular training and exercises to build the team’s capabilities, solicit employee feedback to address new challenges and ensure that insider threat mitigation is incorporated into any new business line or reorganization.

“People are the first and best line of defense against malicious insider threats, and organizations should act now to safeguard their people and assets,” said Steve Casapulla, CISA’s executive assistant director for infrastructure security. “We encourage leadership to draw expertise from across departments for a holistic defense while fostering a culture of trust where employees feel empowered to report concerns and stop threats before they escalate.”

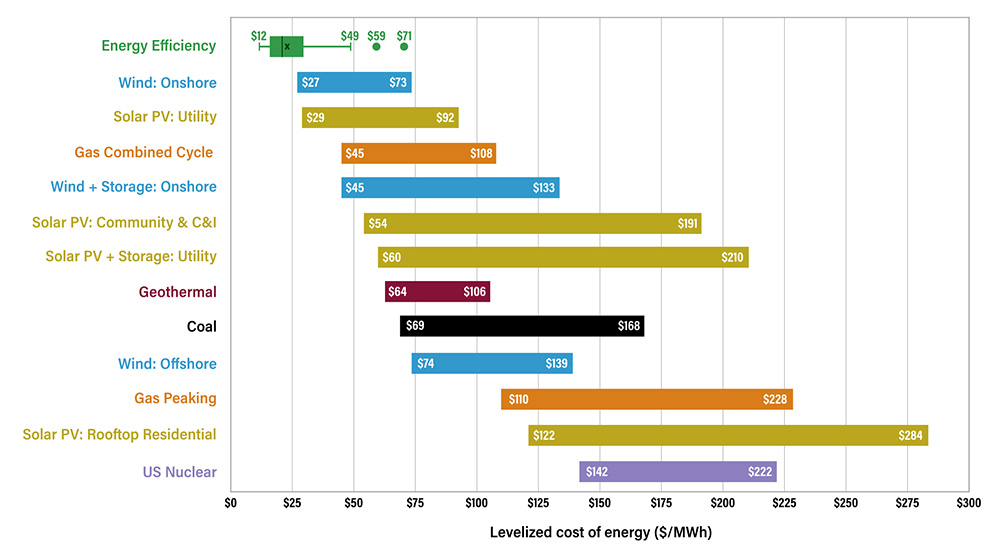

Energy efficiency and load flexibility would be effective and cost far less than the new generation assets many jurisdictions are planning to build to meet anticipated load growth, a new report asserts.

While both efficiency and flexibility have been cited repeatedly as solutions, they remain underused, the American Council for an Energy-Efficient Economy (ACEEE) said Feb. 4 as it released “Faster and Cheaper: Demand-Side Solutions for Rapid Load Growth.”

Analysis of large utility programs showed energy efficiency with a median cost of $20.70/MWh and load flexibility costing less than $40/kW-year, ACEEE said, while the levelized cost of electricity from renewable, fossil and nuclear alternatives is spread across a much higher range.

The authors note that the cost cited for energy efficiency does not factor in significant avoided costs for distribution infrastructure including substations, transformers and lines. They additionally tout demand-reduction measures as quicker and cleaner than building new generation, as well as better at protecting ratepayers.

Comparison of the levelized costs of energy efficiency and supply-side resources | ACEEE

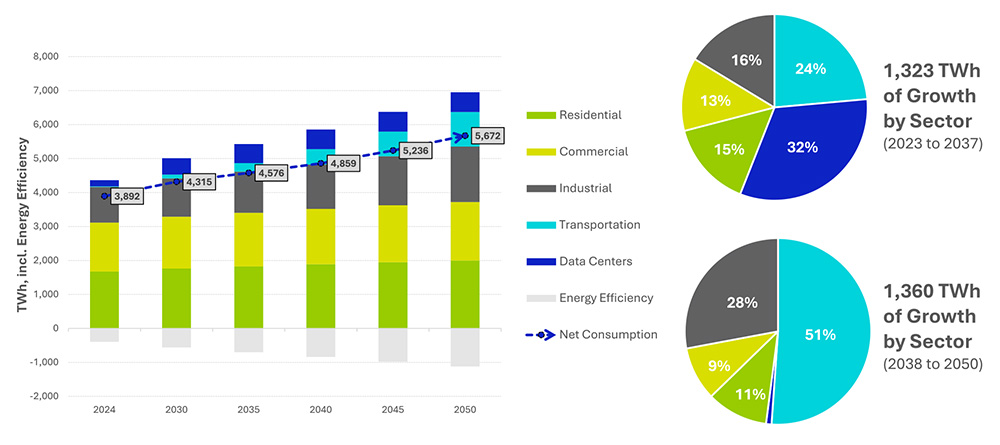

There is wide agreement that the U.S. has begun a period of sharp power demand growth, significantly from data center proliferation, but there is no consensus on how steep and high the growth curve will be. The ACEEE report notes that 10-year forecasts of demand growth range from 20 to 50% and peak demand growth from 19 to 35%.

The most common response by utilities has been to plan new gas-fired generation, the authors say, and given utilities’ historic tendency to overestimate future demand, this creates the risk of stranded generation, transmission and distribution assets.

Demand-side management in the form of energy efficiency and load flexibility is the better response, ACEEE asserts. Aggregated nationally, energy efficiency could reduce electricity consumption by approximately 8% and demand by about 70 GW by 2040, the report asserts, adding that experts estimate 60 to 200 GW of load flexibility nationwide.

The data center buildout is a once-in-a-career opportunity for the decision-makers in the power sector, many of which get a regulated rate of return on every dollar of investment they make. The Edison Electric Institute reported in July 2025 that investor-owned utilities were planning $1.1 trillion of investments between 2025 and 2029, significantly more per year than the $1.3 trillion invested in the preceding decade.

Demand-side management is not a large piece of the solution yet. The ACEEE study notes that only 6% of U.S. energy consumers participated in a retail demand response in 2024. FERC in its 2024 assessment of DR and advanced metering said participation in the seven U.S. wholesale markets was 33.1 GW in 2023.

Expected components of U.S. load growth through 2050 contrasted with potential reductions in use through energy efficiency | ACEEE

With its new report, ACEEE is trying to move the needle further, so that more efficient use of existing capacity is considered before expansion.

“Our power system needs to meet rapidly growing electric demand while ensuring reliability and affordability,” said Mike Specian, ACEEE utility research manager and lead author of the report. “The first-line approach should be tapping into our massive reserve of energy efficiency and load flexibility, not spending billions on new power plants.

“Demand-side measures are faster and cheaper to deploy today than new generation. They can be targeted to specific locations to defer or avoid the need to build new infrastructure, saving families and businesses money in the process.”

The West-Wide Governance Pathways Initiative’s Launch Committee asked CAISO to initiate a stakeholder process to create a funding mechanism for the newly incorporated organization that is to assume governance over the ISO’s energy markets.

In a Feb. 3 letter, Launch Committee co-Chairs Kathleen Staks (Western Freedom) and Pam Sporborg (Portland General Electric) asked CAISO CEO Elliot Mainzer to facilitate discussions about creating mechanisms for ISO market participants to cover the debt financing costs for the Regional Organization for Western Energy’s (ROWE).

“We have received generous financial support from stakeholder and philanthropic contributions but will need additional funding for the ROWE implementation efforts,” Staks and Sporborg wrote.

The Launch Committee seeks approximately $8 million to fund ROWE’s implementation costs until the organization can collect funding from members starting in 2028. The $8 million will go toward seating an initial board, hiring key staff and consulting support, according to the letter.

So far, the committee has collected about $1.1 million in stakeholder contributions and grants. To cover the rest, the committee is exploring debt financing with commercial banks “that could be repaid by market participants in 2028 after the anticipated transfer of governance of the markets to the ROWE,” the chairs wrote. (See Pathways’ ROWE Incorporated in Delaware, Board Search Underway.)

“The commercial banks would require ROWE to have a way of guaranteeing repayment of the loan,” according to the letter. “Therefore, the Launch Committee is requesting [that] CAISO facilitate a stakeholder process to develop a proposal to create a funding mechanism for the ROWE’s debt financed startup costs that would be repaid by market participants.”

CAISO spokesperson Gary Delsohn told RTO Insider in an email that under a straw proposal issued by CAISO, the ISO would provide credit backing for a commercial line of credit for ROWE. Beginning in 2028, when ROWE is scheduled to assume governance over markets, CAISO will recover ROWE costs through surcharges on participation in the markets, enabling ROWE to repay the bank.

“The ROWE would be responsible for making payments on the loan after January 2028, with the CAISO serving as guarantor,” Delsohn said. “This is necessary because the ROWE at that point would not be able to obtain such credit until it has become more established. The ROWE would draw upon the loan on an incremental basis throughout the start-up period to cover initial start-up costs.”

“This approach ensures an equitable and broad-based sharing of the ROWE’s start-up costs among market participants throughout the regional market footprint, including market participants effectively utilizing the ROWE within the CAISO Balancing Authority footprint and throughout the [WEIM and EDAM] regional footprints,” he added. “The rate and collection mechanism would be set forth in the CAISO’s tariff and thus subject to approval by FERC.”

ROWE is the product of California Assembly Bill 825, which implements Pathways’ “Step 2” plan to create an independent organization to oversee CAISO’s Western Energy Imbalance Market and soon-to-be-launched Extended Day-Ahead Market, and authorizes the ISO and California’s investor-owned utilities to join ROWE. (See Newsom Signs Calif. Pathways Bill into Law.)

One goal in establishing ROWE was to remove what some in the Western power sector see as a barrier to wider participation in CAISO-run markets by ensuring they are not governed primarily by officials and stakeholders in California.

ROWE was incorporated in Delaware on Jan. 21. The organization is to assume governance over the markets in 2028.

The U.S. electricity sector is at a turning point where after nearly two decades of flat demand, electricity use is projected to surge over the next several years. A major reason is the growth of data centers for artificial intelligence and cloud computing. The country is on the road to build data centers quickly and at enormous scale. AI is a highly critical technology that will shape the future U.S. economy and its place in the world.

State and local government policies to attract data centers seem at odds with many locales opposing the building of new data centers. These policies are offering tax breaks and other inducements to lure data centers, while vocal groups are slamming data centers for various reasons, including their intensive use of land, electricity and water.

Ken Costello

In my home state of New Mexico, there is an active and growing opposition to data center projects. For one proposed facility, Oracle’s Project Jupiter, opponents of the project raised concerns about electricity consumption and air pollution (especially since it will rely on natural-gas-fired microgrids), scarce water resources for cooling and inadequate public input.

There also is a political undercurrent from both the left and the right that raises questions on AI and the need for data centers, if only because they are owned by Silicon Valley billionaires. As stated in one article, “just like some Democrats are worried they’re ceding the anti-AI development lane to Republicans, the same is true on the other side.”

We see NIMBYism and corporate welfare at play simultaneously. Each action is misguided by either obstructing the building of new data centers or compelling taxpayers to subsidize them. One challenge is to facilitate the building of new data centers to accommodate AI. NIMBYism can either delay their construction and operation or, worst, terminate their construction. Corporate welfare, besides encouraging wasteful rent-seeking, redistributes wealth from taxpayers to owners of highly profitable data centers.

Three general problems underlie the NIMBY syndrome. NIMBY projects are facilities that increase overall social welfare but inflict net costs (or at least perceived as such) on the citizens living in the host locality. Data centers seem to fall in this category.

First, the risk perceptions of local citizens may be distorted because of faulty information. Better education of citizens can mitigate this problem. While data centers may increase the price of electricity — which is a major concern of policymakers and activists opposed to data centers — this is not a sure outcome.

Proposals to address this potential problem are numerous and seem plausible if policymakers are willing to implement them. They include:

allowing data centers to purchase or produce electricity, free of regulation, from facilities off the grid;

requiring data centers to sign long-term contracts with utilities that include exit fees and minimum billing requirements;

requiring curtailments or time-of-use pricing of power for data centers during peak periods.

The second problem is that the siting/political process may not mirror a locality’s consensus. An active minority of opponents to a facility can dominate the preference of a more passive majority at town meetings or in referenda. This intervention can lead to a decision not representative of the majority preference in the community. The vocal group may be most affected by a facility or have ideological or self-interest reasons for opposing it. The group may perceive no benefits, for example, but only environmental, economic or safety threats from the facility.

The third problem is that the local benefits of a facility may fall short of the local costs. For example, the local area may suffer environmental costs and higher energy costs, while most of the benefits from cloud computing or AI accrue to other areas; a parallel example is the production of shale gas (that emits methane and threatens the local water quality) that benefits out-of-state consumers. Overall, a decision based on faulty information, a defective political process or disregard for out-of-area effects is likely to cause a NIMBY problem.

Corporate Welfare

Corporate welfare (sometimes pejoratively labeled “crony capitalism”) refers to government handouts and special protections granted to certain businesses to locate in a specific jurisdiction. Tax breaks, or as some observers call them tax incentives, have in particular become a popular device for state and local governments. Politicians, whether Democrats or Republicans, have relied on tax breaks to attract new businesses. Several states and locales have taxpayer-funded inducements for data centers.

Proponents argue that tax breaks are necessary to attract businesses and that their costs are offset by the additional tax revenue from increased economic activity. They claim that to compete with other jurisdictions, they need to offer tax breaks or businesses will go elsewhere.

Politicians see themselves entangled in a vicious cycle where they are competing with other jurisdictions to attract new businesses. They don’t want to appear indifferent to attracting businesses that can bring new jobs and other economic benefits.

What we have seen, with Amazon as a prime example (no pun intended), is jurisdictions driving up the tax breaks they are willing to pay to exorbitant levels. Analysts refer to this as the “race to the bottom.”

Studies have shown that these giveaways to businesses most times have little effect on their decision on where to locate. Recipients who receive tax breaks often use their political and economic clout to gain favors at the expense of their competitors and taxpayers. It is a classic example of special interests benefiting at the expense of the general public.

At first thought, it seems audacious for government officials to expect poor households and small, struggling businesses to apportion some of the taxes they pay to large, profitable businesses headquartered outside their state or locality (like Meta, Amazon, Microsoft and Goggle). But their behavior shows that they would rather chance a groundless handout than risk being perceived as anti-job and anti-business.

While governments offer handouts with the hope of realizing greater economic returns, companies often make promises to create jobs they fail to keep. Handouts often are no more than a zero-sum game where one jurisdiction benefits at the expense of another.

For many of them, the added revenue from the recipient business falls short of the tax break. While data centers employ many people during construction, relatively few employees operate the facilities. Their effect on local economic development arguably is minor.

Tax breaks are just as likely to result in perverse behavior and unintended consequences. They can shrink the tax base, shift tax burdens to other taxpayers or reduce public goods valued by the local citizenry.

Tax breaks also open the door to rent-seeking and corruption: Large companies threaten to locate elsewhere unless they receive special treatment and even “bribe” officials with campaign funds in exchange for favoritism.

Of course, one can imagine situations where a tax break could contribute to the economic well-being of the local or state citizenry net of the subsidy cost. But government officials should make that determination before offering tax breaks to any company.

What we frequently observe is the failure of government officials to provide the public with a transparent accounting of the actual costs of the tax breaks offered to businesses. Most states and localities neglect to fully disclose all the details of their “tax break” packages. A good argument can be made that they should either stamp out tax breaks to businesses or make government officials more accountable for their decisions. Their taxpayers deserve no less.

Redressing the Conflict

Real-world experiences have shown the importance of local participation in every aspect of the siting process (for example, economic, safety, environmental). Not only should local individuals or groups have the opportunity to participate, but government and industry should encourage them to do so.

Industry acts as a good citizen when responsive to the concerns of local people over a facility that can, or is perceived to, cause substantial harm. Education and public understanding are critical in subsiding opposition and fear and gaining support for a facility. Frequently, the fears are irrational; but the political reality remains that if the public is wary of a new facility in their locality, the owner will need to address those fears or face strong opposition.

One often suggested remedy to the NIMBY syndrome is to shift jurisdiction to a less local authority, such as the state and federal government. Of course, that may have its own problems and should be used only as a last resort.

Instead of tax breaks, governments should create a good business climate with reasonable tax rates and regulations, and pro-growth public expenditures like for infrastructure development. States and locales can better satisfy this goal by broad-based tax cuts than by discriminatory and wasteful tax breaks where they play the role of picking winners and losers.

If governments continue to offer handouts to businesses, they should at least do a cost-benefit analysis. Experience has shown that public officials often understate the true costs of tax breaks and overstate the benefits, which should be no surprise.

For data centers, the two wrongs of NIMBYism and corporate welfare don’t make a right: They drive up the costs of data centers, delay or even terminate their construction, dampen the benefits to the economy from AI and cloud computing, and unfairly burden taxpayers. All of these outcomes will harm society, and for what purpose?

Kenneth W. Costello is a regulatory economist and independent consultant who resides in Santa Fe, N.M.

As the West appears to move toward two separate day-ahead markets, data center developers like Google and clean energy companies are investing with the intent to mitigate seams and ensure operational consistency, panelists at an Advanced Energy United webinar said.

Representatives from Google, Leap Energy and Pattern Energy discussed the newly incorporated Regional Organization for Western Energy (ROWE) during a Feb. 3 webinar in conjunction with the release of a new AEU report on the advantages of a unified Western market.

The West-Wide Governance Pathways Initiative created ROWE as an independent organization to remove what some see as a barrier to wider participation in WEIM and EDAM by ensuring they are not governed predominantly by officials and stakeholders in California.

However, EDAM is not the only day-ahead market under development. Despite ROWE, a significant number of entities have opted to join SPP’s Markets+, which is scheduled to go live in 2027. (See BPA Outlines Next Steps in Markets+ Implementation.)

For Google, the split between EDAM and Markets+ could make moving clean energy “complicated and expensive,” according to Sydney Henry, the company’s data center strategic negotiator.

“This fragmentation will make specific clean firm projects financially unviable if we have to cross market borders to reach our key investments, in this case, likely our data center investments,” Henry said.

One issue is the market seams that will arise between EDAM and Markets+. The seams are created by different policies and separate dispatch between neighboring markets, which can result in additional costs for transferring energy across the boundary.

Google now looks at its data center investments in the context of how markets are likely to be structured and how to mitigate seams risk by, for example, ensuring that power purchase agreements are “in the same market or within the same structure as the data center,” she said.

“That’s always opportune, because then they’re operating under the same rules and the same constraints,” Henry said. “So, it’s both an opportunity and a bit of a risk mitigation effort as we continue to see how the different states land and the different utilities land within their preferences. But I think it would definitely be preferable, from our perspective, to have it as regionalized and stable as possible.”

Meanwhile, independent governance reduces seams costs and regulatory friction, which is important for large-scale energy investors like Google, Henry noted.

“We are investing in new markets,” she said. “This isn’t investments that we were maybe seeing five or 10 years ago in the couple million dollars. It’s now billions of dollars of investments.”

Resource Developer Challenges

Jack Wadleigh, senior regulatory and market affairs manager at clean energy developer Pattern Energy, likewise said the “multi-market landscape” introduces challenges for both existing projects and meeting contractual obligations.

Changes to Pattern’s settlement points within the markets for resources that are “pseudo-tied or dynamically scheduled” can significantly impact developers, Wadleigh said.

“And these issues are kind of ongoing, especially when we talk about things like congestion, revenues and whether you’re settling with the market operator or settling with the balancing area,” he said. “So, these are all kind of high-priority topics for Pattern as we’re thinking about the future state as we go into a world with multiple markets in the West.”

Instead of having a standardized approach, market fragmentation forces providers to adapt to the different markets’ bidding rules, timelines and performance metrics, according to Collin Smith, regulatory affairs manager at Leap Energy.

Leap’s operations are “largely limited to California because of the difficulty of integrating across multiple different types of participation in other states.”

“If you are creating multiple markets across the region, you’re just slowing down the ability for companies like Leap to be able to operate in those areas and make use of the different technologies that are already being adapted by customers across the West for their own purposes … losing the ability for those to be quickly integrated into the grid,” Smith said.

WASHINGTON — All five FERC commissioners faced questions from the House Energy and Commerce Subcommittee on Energy on how to balance reliability and affordability as demand grows.

“FERC stands at a critical juncture in history, domestically and in the world,” FERC Chair Laura Swett told the subcommittee during an oversight hearing Feb. 3. “We’re in a global energy arms race created by the rise of technology, its tremendous load growth, and our push to onshore manufacturing and jobs. I want the United States to lead that race.”

FERC is working to streamline its processes, cut connection times and ensure efficient, durable infrastructure development, she added.

The commission’s main job is to deliver affordable and reliable energy for Americans while upholding Congress’ vision for a bipartisan, independent and resource-neutral regulator, Commissioner David Rosner said. That is easier said than done, especially with all the changes the industries it regulates are facing, he said.

“Our energy systems face these pressures at a time when families and small businesses have been struggling with high prices, including their utility bills,” Rosner said. “While meeting this moment presents challenges, it also creates opportunities for us to modernize America’s energy infrastructure.”

While the demand growth, largely from data centers, does present the opportunity to modernize the grid in a way that increases reliability and efficiency, FERC has work to do to make that a reality, Commissioner Judy Chang said.

“To date, the system buildout has contributed to high prices for customers, whose utility rates have already increased in recent years due to other factors,” she said. “Thus, as regulators, the commission has a responsibility to guide the industry’s efforts towards cost-effective and durable solutions that address these pressing challenges while protecting customers from adverse reliability and cost impacts.”

The hearing was held as the district is still digging out from the late January winter storm, and many members of Congress noted it took out power to more than 1 million customers. Ranking Member Kathy Castor (D-Fla.) noted that the storm knocked out some transmission lines owned by the Tennessee Valley Authority. But the bulk power system largely held throughout the winter weather, FERC Commissioner Lindsay See said.

“Though information is still coming in, I’m encouraged to see good results from better winterization and prep work, and coordinating across the gas and electric industries,” See said. “We have more to do in these areas, but the progress so far is real.”

Subcommittee Chair Bob Latta (R-Ohio) asked his standard question of whether the U.S. needs more power — to which all five commissioners answered “yes” — before asking Swett how FERC is working to ensure regulatory certainty to help that happen.

“We are taking a hard, holistic look at the open items at FERC,” Swett answered. “First of all, I shut down quite a few lingering dockets at my first meeting with the help of my colleagues here. That is one way to eliminate uncertainty that has come from previous administrations. Another way is to end the flip-flopping of FERC’s regulatory paradigm and the uncertainty that’s created by increasing regulation that has built up over the years that far exceeds what FERC’s mission is under the law.”

Castor asked what FERC was doing to speed up the interconnection of new power plants on the grid.

Chang answered that the commission has been working on that for years, with Order 2023 requiring a first-ready, first-served approach with cluster studies for interconnecting projects. Progress is being made to speed up the queues, she said.

“No matter how fast we can study the projects in the generation interconnection process, one of the bottlenecks I talked about in my opening statement is the transmission system,” Chang said. “So, if the transmission system is not ready, or if it’s inadequate for interconnecting the generator and the load, that becomes the bottleneck.”

Affordability was the focus of many questions, with Swett noting that the aspects of the power system that FERC regulates are responsible for about one-third of the average customer’s bill.

“Increasingly Americans are struggling in paying those utility bills,” Rep. Alexandria Ocasio-Cortez (D-N.Y.) said. “In 2024, more than a third of households skipped out on necessities to pay an energy bill, and close to a quarter of households kept their homes at hazardous temperatures to avoid the cost of heating or cooling. Yet the energy utilities charging Americans are among some of the most powerful and profitable companies on earth.”

She then started asking Swett questions about the average return on equity FERC approves for utilities engaged in interstate commerce. She ran short of time for questions, but later Rep. Greg Landsman (D-Ohio) picked up where she left off.

“Most Americans don’t know how much power you all have in terms of adjusting down the profit margin in order to adjust down some of these utility bills,” Landsman said.

He asked Swett what kind of debates FERC is having about lowering power bills for consumers considering their ability to trim utility profits.

“The heated debate we are having is a contest to see who can save ratepayers more money,” Swett said. “Every time we have a docket come before us, every single one of them has raised, ‘Well could we lower this, or can we lower that? How is this going to pass through to consumers?’”

Landsman then asked how quickly FERC could act to lower utility profits by trimming their rates.

“Every single rate that comes before us, we do look at what rate of return the utility has,” Swett said. “And that can help Americans, but like I said, that’s only one-third of the bill that they pay every month.”

Forty years after adopting a public involvement policy, the Bonneville Power Administration is reviewing the document with an eye toward modernizing it.

BPA held a workshop Feb. 3 to start gathering feedback on the 16-page policy, issued in 1986.

“It is quite aged. There are things in it that are not really part of how anybody does business anymore,” said Kim Thompson, BPA’s vice president of Northwest requirements marketing.

The policy was written before the arrival of spellcheck, and one task will be to correct typos.

At the same time, BPA wants to rewrite the policy so it holds up in coming years despite changes such as technology advancements.

BPA wrote the policy in response to requirements of the 1980 Northwest Power Act. The policy applies to “major regional power policy formulation.” It also allows for varying levels of public involvement on issues such as transmission, renewable resources, energy conservation, and fish and wildlife.

The public involvement policy exempts certain other processes, such as ratemaking and major resource acquisition, which follow their own specific procedures. The policy also preserves the BPA administrator’s discretion to react quickly when warranted.

BPA plans to review the 1986 document’s definition of “major regional power policy,” as well as the list of exemptions. Tariff changes under the Federal Power Act are a possible new exemption.

Another area for review is the best method for publishing notices of intent. Depending on the situation, BPA might publish a notice in the Federal Register, mail it to landowners or use another means.

One workshop participant said it would be helpful to Bonneville’s “core audience” if notices were included in BPA tech forums — an email distribution group — even if they’re published in other ways.

Another attendee asked if notices could include links to relevant documents so stakeholders could get a head start on reviewing materials.

A section that’s being eyed for deletion pertains to public comment forums, in which members of the public gather to comment on an issue in person. A verbatim transcript of the forum is then prepared to be added to the record.

Although BPA still occasionally holds a public comment forum, written comments have become the standard.

The 1986 policy specifies a 30-day window for submitting written public comments, a period that allowed for mailing materials back and forth, BPA representatives said. Even though comments may now be submitted more quickly by electronic means, workshop participants seemed to favor keeping the comment period at 30 days.

“It’s not just about the time it takes to review and write comments,” said Fred Heutte, senior policy associate with the NW Energy Coalition. “Many organizations have internal processes that they have to go through to respond to an important formal proposal by Bonneville.”

BPA plans to hold at least one additional workshop on its public involvement policy. A draft policy would then be released in early April followed by a public comment period. BPA hopes to finalize the policy around July 1.

Feedback on the scope of policy changes may be submitted by Feb. 11 to communications@bpa.gov.

Picture this: It’s late on a school night and a kid asks their parents for a last-minute trip to the store. There’s a project due the next day, and without an emergency run to the market, disaster looms. What follows is familiar: some back-and-forth about how this happened, a short lecture on procrastination and finally a reluctant agreement to make an exception.

Lately, it’s hard not to feel like state and federal energy regulators are playing this game, facing utilities that waited too long and now insist everything is urgent.

A clear example is FERC’s recent approval of ERAS processes in both MISO and SPP (the Expedited Resource Addition Study and Expedited Resource Adequacy Study, respectively). These new processes allow certain power plants to effectively jump the interconnection line, skipping ahead of hundreds of other projects already waiting their turn. (See FERC Dismisses Rehearing Ask for SPP’s ERAS Process.)

When ERAS was proposed through stakeholder processes, the underlying rationale was widely understood: Utilities had not planned far enough ahead, particularly for new natural gas plants, and now wanted a faster path forward.

When ERAS was proposed in 2024, MISO and SPP together had more than 300 GW of generation projects in their queues. The vast majority were wind, solar and battery storage by competitive developers, with relatively little natural gas by the utilities. In fact, MISO’s queue grew so large that the grid operator was forced to cap new entries altogether. Yet at the same time, utilities and planners began warning of an imminent reliability crisis.

Simon Mahan

Integrated resource planning (IRP) processes exist specifically to avoid this outcome. Many utilities conduct IRPs every two to three years to forecast demand and identify future resource needs. Those plans routinely show large additions of solar, wind and battery storage, often alongside some natural gas.

The labyrinth of interconnection studies can take three to four years. Renewable projects often can be built in one to two years once contracted. Natural gas plants frequently take much longer. Utilities know this all too well, yet many failed to submit gas projects early enough to align with their own forecasts.

Now, with electricity demand rising from data centers, industrial growth and electrification, utilities are asking regulators to let them cut in line.

MISO already has received more than 60 ERAS project requests, with nearly three-quarters of the proposed megawatts coming from natural gas. These projects often skip competitive solicitations, too. They are self-identified by utilities as “needed” and advanced on an expedited basis. Entergy alone has submitted more than 8,500 MW of gas generation through ERAS. (See MISO Accepts 6 GW of Mostly Gas Gen in 2nd Queue Fast Lane Class.)

Traditionally, state commissions approve new power plants only after reviewing a full certificate application, including cost estimates, alternatives analysis and transmission impacts. ERAS turns that structure upside down. Under these expedited processes, regulators are asked to effectively bless projects before a formal application is even filed. Once a project receives accelerated interconnection treatment, it becomes far harder to later reject it or disallow its costs.

After all, once you’re already standing in the checkout line with emergency school supplies in hand, it’s difficult for a parent to say, “You’re on your own, kid.”

In this case, tens of billions of dollars are at stake.

To be clear, ERAS technically is resource neutral. Wind, solar, battery storage, gas and even nuclear projects are eligible. A few have been submitted. But they pale in comparison to the surge of utility-owned, non-competitively selected natural gas plants now racing ahead of the queue.

Fast-tracking these projects risks rewarding exactly the behavior regulators should be discouraging.

So, what can regulators do instead? Here are three practical solutions:

IRPs must be more than a paper exercise. They provide value only if regulators are actively engaged, assumptions are realistic, load forecasts are transparent and modeling reflects real-world timelines.

Competitive procurement is essential. Requiring utilities to issue requests for proposals ensures that regulators and consumers can see what the market is offering. Competition disciplines costs. Sole-source generation does not.

Diversification and transmission expansion must remain central to reliability planning. A grid built around a narrow set of resources is inherently more fragile, not less. Maybe there’s merit in a connect and manage interconnection option, like what ERCOT has.

ERAS may be described as a temporary emergency valve, but history suggests that “temporary” exceptions have a way of becoming permanent precedents.

If regulators aren’t careful, today’s emergency trip won’t be the last time.

And that’s a lesson ratepayers shouldn’t be forced to pay for.

Simon Mahan is executive director of the Southern Renewable Energy Association.