PJM CEO Terry Boston (Source: PJM Interconnection LLC)

By Suzanne Herel

PJM President and CEO Terry Boston announced Wednesday that he plans to retire effective Dec. 31 after seven years at the helm of the RTO.

“Thanks to the outstanding talent of PJM employees, I leave knowing that PJM today is a true leader in the industry — the gold standard for reliable electric service, fair and efficient markets and infrastructure planning,” Boston, who joined PJM in February 2008, said in a letter to the board.

“I am especially proud that the PJM team has successfully managed three ‘one-in-a-hundred-years’ weather events within the past four years,” said Boston, 64, who plans to use this year consolidating improvements PJM has made and serving as chairman of the ISO/RTO Council.

Board of Managers Chairman Howard Schneider, speaking for the board, praised the 43-year electric utility industry veteran for his “strong leadership and extraordinary vision.”

“Terry’s outstanding leadership has been important not only to PJM and the customers it serves but to the development of the grid and markets across the country,” Federal Energy Regulatory Commission Chairman Cheryl LaFleur said in a statement.

The announcement has been in the works for some time. PJM said in a press release that a “rigorous succession process by the PJM board has been underway.”

“Candidates to succeed Boston will be considered based on demonstrated leadership abilities, industry expertise and reputation, as well as commitment to electric system reliability and fair, efficient electricity markets,” PJM said.

Boston came to PJM after serving as executive vice president for the Tennessee Valley Authority.

PJM rejected most of the criticism of its Capacity Performance proposal in comments filed late Friday, but dropped its proposed change in the method for determining the capacity obligations of load-serving entities.

“Based on the comments received … PJM proposes instead to discuss that issue further with stakeholders and report back to the commission in one year on the results of those discussions,” PJM wrote in a filing with the Federal Energy Regulatory Commission (EL15-29). PJM noted that the allocation of LSEs’ capacity obligations does not need to be resolved before the May 2015 RPM Base Residual Auction.

PJM also conceded merit to an assertion by the PJM Utilities Coalition (American Electric Power, Dayton Power and Light Co. , FirstEnergy and East Kentucky Power Cooperative) that there is a problem with a “one-year price” for a multi-year investment in generation.

“PJM did not propose any Tariff changes in the Dec. 12 filing on this issue and does not propose any now. However, given the additional costs of serving as a Capacity Performance resource, the possibility for new environmental rules to require even more investment in existing generation facilities and the commission’s recent approval of an expansion for the new entry pricing available in ISO-New England, the time may be ripe to revisit this issue,” it said.

PJM asked FERC to respond to the coalition’s concerns by directing PJM to explore with stakeholders the subject of new entry pricing and multi-year pricing. PJM would report back to FERC on the issue no later than December.

More than 60 entities filed comments and protests in response to PJM’s proposal, which would increase the reliability expectations of capacity resources with a “no excuses” policy. It is expected to result in both larger capacity payments and higher penalties for non-performance. (See States, LSEs Skeptical, Utilities Split Over Capacity Performance.)

In their comments and protests, states and LSEs were skeptical about the need for a major overhaul, while generators were split over elements they liked and others they said must be changed.

PJM defended its changes to force majeure provisions, which some generators described as unduly punitive.

“Strong performance incentives are a vital part of the solution to poor resource performance,” it said.

“The governing principle of this new approach is very simple and very conducive to innovation and efficiency: resources that exceed expectations will receive higher compensation; those that fall short of expectations will relinquish revenue and face a threat of net payments.”

PJM noted that FERC received equally strong arguments that the proposed charge levels are too high and too low.

“As shown in the Dec. 12 filing, this part of PJM’s proposal closely tracks the structure, and much of the details, of the approach recently approved for ISO-New England,” it said.

PJM also responded to a number of public interest groups who said that renewable, energy efficiency and demand response resources would be disadvantaged in the new structure, saying “the actual suppliers of renewable and energy storage resources recognize that PJM’s proposal to permit intermittent storage, demand response and energy efficiency resources (‘Intermittent/Storage/DR/EE’) to combine their capabilities offers a workable pathway for these resources to qualify as Capacity Performance resources. Parties also recognize that the ability of these resources to receive revenues for superior performance provides a new revenue stream that does not exist under today’s capacity construct.”

As for those who objected to the proposal as a reaction only to last year’s polar vortex, PJM pointed to “deficiencies and disincentives” in the current Tariff relating to resource performance, including a “very weak” non-performance charge.

“The polar vortex provided a dramatic demonstration of these adverse effects. But the shortcomings in the current resource performance rules would still be there, and would still require correction, even if there had been no polar vortex,” it said.

PJM requested that FERC approve the changes by April 1.

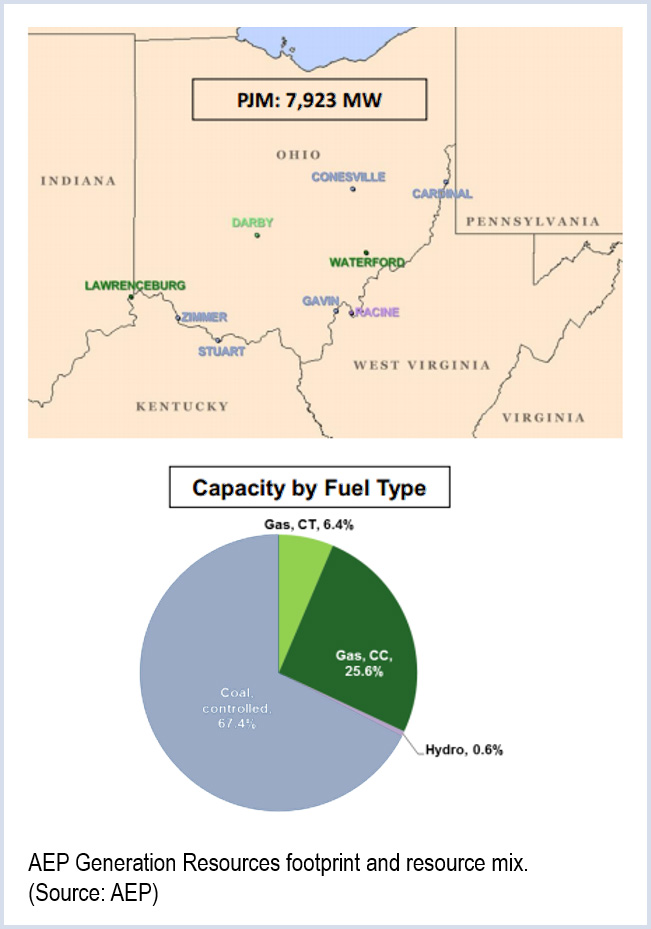

American Electric Power reported fourth-quarter earnings of $191 million ($0.39/share), compared with $346 million ($0.71/share) for the same period last year. Full-year earnings were $1.634 billion ($3.34/share), compared with $1.48 billion ($3.04/share) in 2013.

The Columbus, Ohio-based company attributed the fourth-quarter drop to the termination of a long-term coal contract.

However, CEO Nicholas Akins said the company benefited from successful regulatory proceedings in several states.

“The reliable performance of our generation fleet during colder-than-normal temperatures in 2014 gave us the ability to advance spending from future years into 2014. Those shifts, combined with our initiatives to put in place sustainable process improvements, will help us manage the revenue challenges presented by the Ohio deregulation transition and the 2016-2017 PJM capacity market results,” Akins said.

Chief Financial Officer Brian Tierney referenced PJM’s Capacity Performance proposal, urging the Federal Energy Regulatory Commission to approve the changes quickly to stabilize PJM’s markets and ensure its reliability amid impending coal unit retirements.

“In regards to the challenges we face for 2015, I think you’re well aware of them — from the earnings shortfall from the PJM capacity pricing and the retail stability rider, the lower natural gas prices and power prices and their impact on our system sales,” he said. The rider was approved by the Public Utilities Commission of Ohio to help the company transition to a competitive market.

Tierney also confirmed that AEP has hired an investment bank to help evaluate the company’s alternatives regarding the disposition of its unregulated businesses.

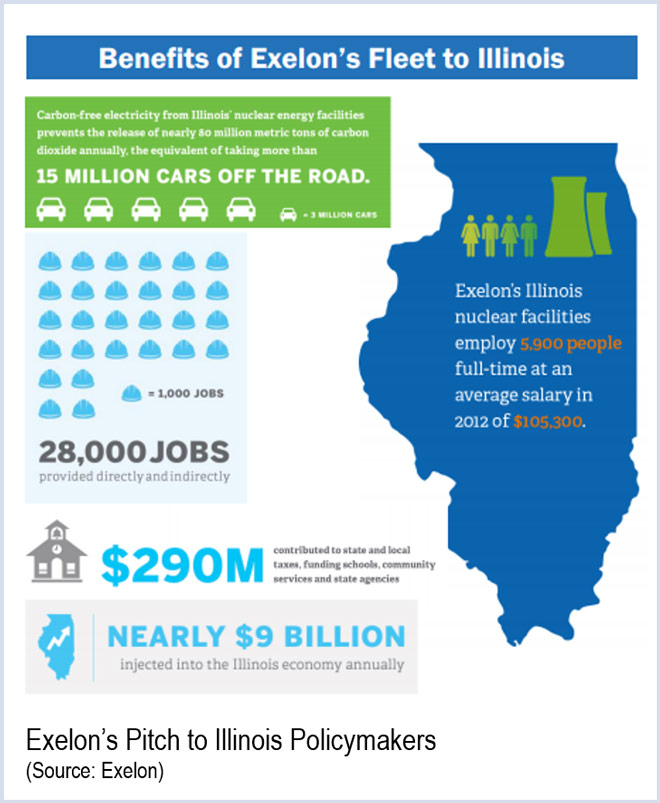

Exelon reported fourth-quarter earnings Friday of $18 million ($0.02/share), compared with $495 million ($0.58/share) in 2013. For the year, the company reported earnings of $1.623 billion ($1.88/share) versus $1.719 billion ($2.00/share) in 2013.

The Chicago-based company attributed the depressed earnings in part to warmer-than-expected temperatures in the last three months of the year.

CEO Chris Crane touted the company’s investments in emerging technology, citing Bloom Energy, whose East Coast manufacturing facility is based in Delaware. Exelon announced last July it would provide equity financing for 21 MW of Bloom Energy fuel cell projects at 75 commercial facilities in California, Connecticut, New Jersey and New York.

He also noted progress in the discussion to improve the finances of its Illinois nuclear plants. A report released by Illinois officials last month underscores their reliability as well as economic and environmental benefits to the state, he said. (See Illinois Considering Carbon Tax, Cap-and-Trade to Save Exelon Nukes.)

Said Bill Von Hoene, chief strategy officer: “We are supportive of any of the options that reward all carbon-free resources equally, but doing nothing simply is not a viable economic option if we are to maintain the operations of those plants that are at risk. As we stated repeatedly, we do not seek a bailout.”

He noted recent approvals of the Pepco Holdings Inc. acquisition by New Jersey, FERC, Virginia and Delaware, saying he expects the deal to close in the second half of this year. (See Exelon-Pepco Deal Moves Forward in NJ, Del..)

“We are continuing the process of review in the remaining jurisdictions of Maryland and Washington, D.C.,” he said.

PPL will file a base distribution rate case this year for its Pennsylvania business, CEO William Spence said during the company’s fourth-quarter earnings call last week.

The company is also seeking rate increases for its regulated Kentucky operations, with the company asking for an additional $30 million annually from Louisville Gas & Electric customers and $150 million from Kentucky Utilities. Spence said he expects new rates, requested for infrastructure investments required for reliability and federal environmental regulations, to become effective July 1.

PPL reported earnings of $1.74 billion ($2.61/share) for the year versus $1.13 billion ($1.76/share) for 2013. The company’s fourth-quarter earnings in 2014 were $695 million ($1.04/share), compared to the loss of $98 million (-$0.16/share) it posted for the same period in 2013.

Spence said the improvement was due to high returns on transmission investments in Pennsylvania and plant environmental projects in Kentucky, as well as increased utility revenues from price increases in the U.K.

Earnings from ongoing operations, however, remained flat from 2013. Higher earnings from the company’s Pennsylvania and the U.K. segments were offset by lower than expected earnings in Kentucky. The company’s total electric sales in the U.S. decreased by 3,769 GWh, or 6.2%, from 2013. Spence said that slow residential growth in rural Virginia and Kentucky played a large role in the decrease.

Spence said he is optimistic about the PJM market. “We see market reforms, such as PJM’s proposed Capacity Performance product, the shift in the variable resource requirement curve and a recent increase in the offer cap, as constructive signals supporting the competitive power business in PJM for the future,” he said.

Spence said that PPL’s deal with Riverstone Holdings to spin off its generation supply business into Talen Energy was the company’s top priority for 2015, but the company said little about it last week, citing a “quiet period” as it awaits a response on its filing with the Securities and Exchange Commission.

The company expects the deal to close on time in the second quarter this year. It accepted the Federal Energy Regulatory Commission’s mitigation plan late last month and it expects approval with the Pennsylvania PUC and the Nuclear Regulatory Commission as it originally projected. (See PPL, Riverstone Accept FERC Mitigation Plan on Talen Spinoff.)

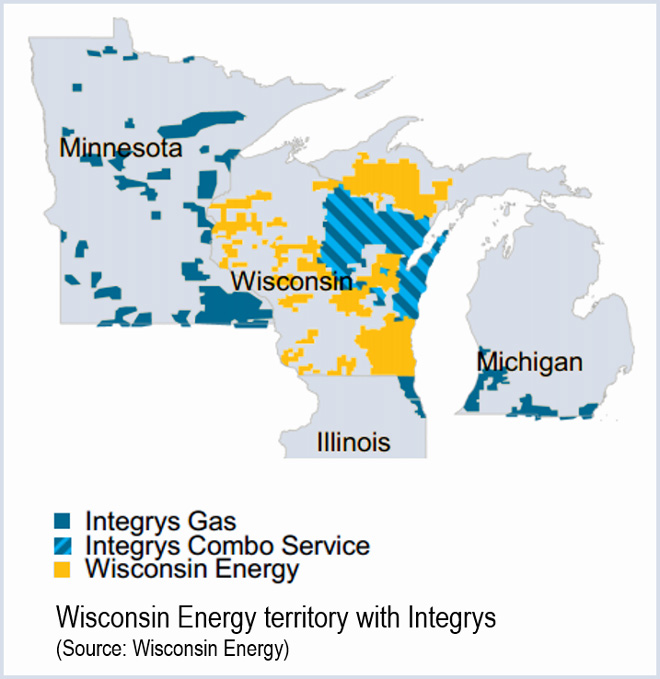

Wisconsin Energy Corp. profits fell 16% in the fourth quarter on warmer weather and $6 million in costs related to its proposed acquisition of Integrys Energy.

The Milwaukee-based gas and electric utility earned $121.4 million ($0.53/share) versus $144.3 million ($0.63/share) in the fourth quarter of 2013. Revenue rose to $1.23 billion from $1.18 billion during the same quarter last year.

For the year, earnings rose 2%, to $588.3 million, or $2.59 a share — dinged 6 cents due to Integrys acquisition costs.

Full-year results were buoyed by colder weather in early 2014 that increased demand for natural gas. The utility also cited cost controls and lower employee health care costs.

During a Feb. 11 conference call with analysts, Wisconsin Energy Chairman and CEO Gale Klappa pointed to a 1.3% growth in electricity sales to large commercial and industrial customers, excluding iron ore mines.

Including mines, electricity deliveries in the sector rose 3.8%. “That’s pretty strong industrial growth in 2014,” he said.

Given the large uptick in 2014, the utility is projecting flat growth in the key large commercial/industrial segment in 2015, he added.

Integrys Deal Progressing

Wisconsin Energy’s planned $9 billion acquisition of Chicago-based Integrys needs approval from regulators in Wisconsin, Michigan, Illinois and Minnesota.

The company cleared a big hurdle in January under a settlement with Michigan regulators, who dropped their objection to the acquisition.

Under the deal announced by Michigan Gov. Rick Snyder, Wisconsin Energy and Integry’s Wisconsin Public Service would sell their electric distribution assets serving 28,000 Upper Peninsula residents to Upper Peninsula Power Co. That includes the 400-MW coal-fired Presque Isle generating station, which is operating under a costly system support reliability agreement (SSR) to prevent its retirement. UPPCO said it would “step into” exiting rates and that the SSR would be eliminated this summer, saving U.P. ratepayers from an estimated $97 million in annual SSR costs.

Pressed by analysts for more guidance on the timing of the merger, Klappa said the latest expected decision is likely to come from Illinois Commerce Commission on or about July 6.

“We’re making very good progress on all regulatory fronts,” he said.

The acquisition will result in a company with 4.3 million customers served by seven electric and gas utilities. The resulting WEC Energy Group will also own the nation’s eighth-largest natural gas distribution operation.

Becoming a Bigger Transmission Player

The combined company also will own 60% of American Transmission Co., with Integrys currently holding 34% and Wisconsin Energy a 26% stake. ATC plans new investments between $3.3 billion and $3.9 billion through 2023.

Wisconsin Energy officials said they took an unspecified fourth-quarter reserve against an expected adjustment to return-on-equity rates for electric transmission operators in MISO.

Last June, the Federal Energy Regulatory Commission changed the way it sets ROE rates for electric utilities, tentatively setting the “zone of reasonableness” at 7.03 to 11.74%. Currently ATC has a base rate of 12.2%.

In addition to taking the fourth-quarter reserve, Wisconsin Energy has also embedded in its 2015 guidance slightly lower earnings in anticipation of an ROE ruling from FERC.

Company officials also provided stand-alone guidance for full-year 2015 earnings — excluding Integrys — at $2.67 to $2.77 a share. That assumes normal weather and excludes transmission-related costs.

Earnings for the first quarter of 2015 are projected by the company at 79 to 81 cents. That’s lower than the 91 cents for the quarter last year, which benefitted from higher sales due to the polar vortex.

Capital Spending Drive

Klappa said Wisconsin Energy plans capital spending of $3.3 billion to $3.5 billion for 2015-2019.

Also, a rolling, 10-year capital spending plan of $6.6 billion to $7.2 billion is about $100 million more than previously estimated, he said.

Projects include an 85-mile natural gas pipeline project in the western part of Wisconsin. Capital spending of about $700 million in 2014 will rise to about $770 million this year, compared to an estimated $600 million to $650 million in 2016 and 2017.

“You’ll see 2015 as being an outsized year for natural gas distribution spending,” Klappa said.

Some of that is to supply natural gas to sand-mining operations in the state, which have flourished due to demand for the material in fracking. Wisconsin has become the No. 1 supplier of fracking sand.

Over time that capital spending will shift more toward electric infrastructure, which is aging, Klappa said.

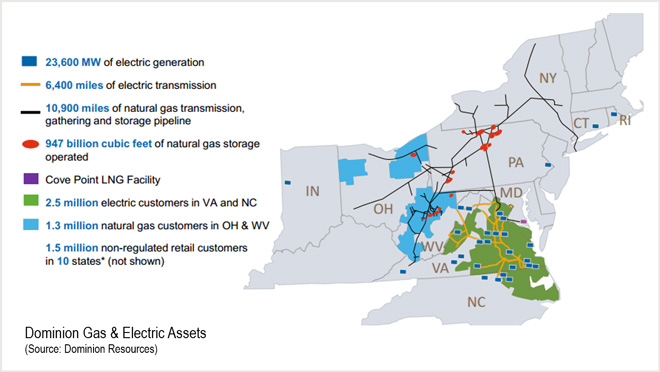

Dominion, a company that has made some dramatic shifts in direction in the past year, announced a significant drop in reported earnings for the fourth quarter of 2014.

Fourth-quarter earnings were about $243 million in 2014, compared to $431 million in 2013. Full-year earnings saw a similar dip at $1.31 billion ($2.24/share) compared to $1.7 billion ($2.93/share) for 2013.

According to Dominion’s earnings report and an analyst presentation made last week, much of the dip shows a company preparing for its future as it pushed a lot of costs into 2014. Its operating earnings were about twice its reported earnings for Q4 and about 50% higher for the year.

The results reflected its decision to pay down debt and take a number of charges in the year. Costs excluded from operating earnings included:

A $248 million charge associated with Virginia legislation enacted in April that permits Dominion Virginia Power to recover 70% of the costs previously deferred or capitalized through Dec. 31, 2013, for development of a third North Anna nuclear unit and offshore wind facilities as part of its 2013 and 2014 base rates;

A $193 million net charge from the termination of natural gas trading and some energy marketing activities;

A $74 million charge related to future ash pond closure costs; and

A $31 million goodwill write-off related to the company’s exit from the unregulated electric retail energy business (sold to NRG Energy).

While earnings took a hit, CEO Thomas F. Farrell II said it is investing in its future, and its leadership is betting on a bright one. “Our management team owns the highest percentage of stock [of] any … company in the sector,” he told analysts last week.

Dominion issued a successful IPO for its natural gas export business, Dominion Midstream. It gained the final permit from the Federal Energy Regulatory Commission for its Cove Point LNG export facility, and construction started the same day. The facility is expected to go into service in 2017, he said.

It bought a pipeline company, Carolina Gas Transmission, from Scana Corp. for $429.9 million, acquiring 1,500 miles of interstate natural gas pipeline in the deal.

Dominion is also a major partner in the Atlantic Coast Pipeline project, a planned 550-mile natural gas pipeline that would bring Marcellus and Utica shale gas to Virginia and North Carolina.

Farrell said the company plans to invest $700 million in solar in the coming years. And while the company has sliced its merchant generation fleet from about 11,000 MW three years ago down to 3,643 MW now, it is boosting its regulated generation fleet.

It put one new $1.1 billion gas-fired, combined-cycle plant, the 1,342-MW Warren plant, in operation in December. It is building a second, a 1,358-MW plant in Brunswick, representing another $1.2 billion investment. Farrell said on the call that the company is planning a third, which at 1,600 MW would be the largest gas-fired plant in the U.S. It would be built in Greenville County, Va., east of Brunswick.

Chief Financial Officer Mark McGettrick said the company plans a total of about $20 billion in capital investments over the next six years.

“2014 was a year of significant accomplishments for Dominion as we completed several major capital projects and made significant progress to advance the next round of infrastructure growth,” Farrell said.

Eversource Energy reported higher year-end earnings fueled by a strong fourth quarter and a drop in operating costs. The company (formerly Northeast Utilities) also announced a 30% increase in its transmission build-out program, adding $900 million to an existing commitment of $3 billion.

Eversource reported 2014 earnings of $819.5 million ($2.58/share) compared with 2013 earnings of $786 million ($2.49/share). Fourth-quarter earnings were $221.6 million ($0.69/share) compared with $177.4 million ($0.56/share) in 2013.

Excluding integration costs, Eversource earned $841.6 million, or $2.65 per share, in 2014, compared with $799.8 million, or $2.53 per share, in 2013.

The company began 2015 by announcing it was integrating Northeast Utilities’ six affiliates into one company under the new name Eversource. It will take the new ticker symbol “ES” beginning Feb. 19. (See Northeast Utilities Rebranding as Eversource Energy.)

In a call with analysts, Chief Financial Officer Jim Judge denied that the name change suggested the company had plans to expand beyond New England. “It truly was trying to bring together six different operating companies — each of whom had their own identity or culture or brand,” Judge said. “It really was driven by that. The speculation about it being driven by an appetite to have a bigger footprint really isn’t based on the situation here.”

“Operationally and financially, we had a very strong finish to 2014, which provides us with considerable momentum heading into 2015 as we continue to address and resolve the most difficult energy supply challenges facing New England,” said Thomas J. May, Eversource Energy chairman, president and chief executive officer.

Transmission Spending

The company last year spent about $723 million on electric transmission projects, including completion of most of its section of the Interstate Reliability Project in northeastern Connecticut, making its 2014-2018 projected total $4.6 billion.

Eversource and its partner, National Grid, were selected by ISO-NE on Feb. 12 over a competing proposal to enhance reliability in the suburbs north of Boston and into New Hampshire. The $739 million AC Plan will use 25 miles of right-of-way and bury another 16 miles of cable.

Northern Pass

Company officials told an analysts call last week that the draft environmental impact statement from the U.S. Department of Energy for the $1.4 billion Northern Pass transmission project is expected in April. The 187-mile project would bring 1,200 MW of hydroelectric power from Hydro Quebec into New Hampshire, with an in-service target of the second half of 2018.

“We’ve made great progress with Hydro Quebec,” May said. “They’ve started very aggressively in Canada licensing their side of the line.”

However, its route, already reconfigured, cuts through the White Mountains and has drawn fierce opposition.

Access Northeast

Separate from its electric infrastructure expansion, Eversource in 2014 partnered with Spectra Energy to propose the $3 billion Access Northeast pipeline expansion that would secure supplies to 5,000 MW of power generation. A tax proposed by New England governors to fund the project has run into political headwinds. Open season is expected this spring and operations are planned for November 2018.

DTE Energy’s fourth-quarter earnings soared 141%, largely on growth in its non-utility operations.

The Detroit-based company serving 3.3 million gas and electric customers posted a profit of $299 million, or $1.68 a share, compared with $124 million, or 70 cents a share, for the fourth quarter last year.

DTE Electric’s operating earnings in the fourth quarter rose 27%, to $128 million. DTE Gas operating earnings fell 40%, to $31 million.

But operating earnings of DTE Energy’s non-utility units — gas storage and pipelines, power and industrial projects and energy trading — increased 70%, to $66 million.

For the full year, DTE Energy’s net income rose 37%, to $905 million or $5.10 a share.

Full-year operating revenues were $12.3 billion, up 27% from 2013.

Upward Expectations

DTE Energy increased its 2015 operating earnings per share guidance to $4.48 to $4.72, from the $4.43 to $4.67 outlook provided in November. Most of that increase is predicated on higher-than-expected prospects in the non-utility segments of gas storage and pipelines, and power and industrial projects.

During a conference call with analysts on Feb. 13, DTE Energy Chief Executive Officer Gerard Anderson said the company was embarking on a “capital investment era.”

DTE said its investments in non-utility units could amount to $1.5 billion to $1.9 billion in 2015-2019.

That includes DTE’s participation in the Nexus Gas Transmission pipeline that will run from Michigan through northern Ohio and then south to the border of the West Virginia panhandle.

The 250-mile Nexus will tap into shale gas production in the tri-state region. DTE, which is partnering on the pipeline with Spectra Energy, said it has made a pre-filing submission with the Federal Energy Regulatory Commission and has engaged an engineering firm.

Anderson said gas and pipeline operating earnings, which totaled $82 million in 2014, could grow to $145 million by 2019.

The company also has been investing in generation, including plans to acquire the 732-MW Renaissance power plant in Carson City, Mich., for $240 million.

Anderson said that MISO planning has shown a 900-MW summer capacity shortfall in Michigan. He noted that Gov. Rick Snyder recently called for Michigan to develop a comprehensive energy policy this year.

In December, DTE filed its first electric rate case in four years. If approved as proposed, the average residential customer would pay $3.25 more a month, or about a 1.5% increase annually.

David Cruthirds brings this report from the Gulf Coast Power Association’s Feb. 5 special briefing: “Challenges & Changes in Energy on the Bayou.” Among the topics discussed were Entergy’s growth plans, Year 1 in MISO South and the RTO’s ongoing seams battles.

Entergy’s Growth Plans: Room for Competitors?

NEW ORLEANS — Entergy Louisiana CEO Phillip May talked about Louisiana’s industrial growth, saying Entergy will need to build or acquire additional generation to serve 1,700 MW of new load by 2017. He noted Entergy is reviewing bids for long-term resources in one request for proposal (RFP) and expects to issue one or more RFPs in the future. May said declining reserve margins in MISO North/Central are expected to absorb the excess generation capacity in MISO South, so Entergy would need new steel in the ground, whether in the form of self-build projects or long-term power purchase agreements (PPAs).

May said Entergy’s needs also would be impacted by expiring PPAs and possible generation retirements.

May also said the company needs to be able to act quickly. He noted it took three years to construct the recently completed Ninemile Unit 6 combined-cycle project, but the overall process took six years, including the time for the RFP and permitting. Entergy is evaluating ways to accelerate that process, he said.

Comment – Skrmetta and May provided interesting perspectives on plans to build new generation to serve growing loads in Louisiana. Skrmetta’s view was that Entergy would be building the new generation itself, while May was careful to say the company would be issuing RFPs to measure bids against self-build projects. The Louisiana PSC requires jurisdictional utilities to test self-build proposals against the market under the oversight of an independent monitor, but the “market-based mechanism” rules were adopted years ago and none of the current commissioners are very strong supporters of wholesale competition.

Entergy’s comments on recent earnings calls clearly indicate the company plans to meet its ambitious earnings growth targets by building the new generation itself, so the company likely will structure its RFPs in a way to favor its self-build projects. Entergy single-handedly decimated the once-thriving merchant sector in its footprint through its “market foreclosure” strategy, prompting the U.S. Department of Justice to conduct an as-yet unresolved investigation of the company’s transmission and power-procurement practices. As a result, there aren’t any merchants left to compete, and non-affiliated suppliers know of Entergy’s predisposition toward self-dealing, so no one should expect very robust participation in the upcoming RFPs. That increases the chances that Entergy’s self-build proposals will “win” upcoming RFPs.

Skrmetta Throws down Gauntlet on FERC and MISO

The outspoken Skrmetta came out swinging with his opening keynote speech at the briefing. Skrmetta, who defeated challenger Forest Wright in a hotly contested and closer-than-expected run-off last December, attacked the Federal Energy Regulatory Commission and the Environmental Protection Agency, saying that the federal government is trying to supplant the state’s authority.

Skrmetta wasn’t alone in his criticism of the federal government. Some speakers questioned the impact the EPA’s proposed carbon emission rules would have on Louisiana’s industrial renaissance. Baker Botts lawyer Pam Giblin lamented the “meteoric shower” of EPA air emission regulations that likely will be extended to the chemicals, oil and gas sectors “if the EPA gets away with it” in the power sector.

In later remarks, Skrmetta turned his attention to MISO’s transmission cost allocation policies, noting Louisiana is expected to export a significant amount of power to the RTO’s North and Central regions because environmental regulations are expected to leave them 2.6 GW short of generation, while Louisiana is expected to have a surplus of the same amount. Skrmetta wants to make sure those who benefit from those imports pay their share of the estimated $1.25 billion of transmission investment needed.

MISO CEO John Bear countered in a subsequent talk that low-cost wind generation from MISO North/Central is lowering energy costs in states without renewable mandates such as those in MISO South. Bear contended that consumers in those states shouldn’t object to paying their share of transmission needed to obtain wind generation.

Skrmetta acknowledged the MISO relationship has been beneficial to Louisiana, but he said MISO needs to be more cognizant of the Louisiana PSC’s jurisdiction, calling that a “paramount concern.” He called on MISO to have more interaction with the commission and its staff, noting that the PSC is “laser-focused on serving consumers” rather than on executing federal programs. Skrmetta cautioned that the long-term success of MISO’s relationship with Louisiana requires “great deference” by MISO to Louisiana’s goals and objectives.

MISO South ‘Year in Review’

Bear was the keynote speaker following lunch, providing MISO’s views on a number of topics.

Bear said MISO’s surplus generation margins meant the RTO didn’t need to move very quickly in the past, but shrinking margins as a result of the EPA rules and issues that arose during last year’s polar vortex are forcing it to reexamine its processes and respond much faster.

Bear also provided a recap of the first year for MISO South, saying things went well overall, but that MISO needs to continue to improve and examine its processes, especially for transmission planning. He said the net economic benefits for MISO South during the first year were 50 to 60% more than initial projections of $524 million.

Lauren Seliga, a MISO analyst for Genscape, provided a very interesting recap of power trading, pricing, flows and market barriers during the first year of MISO South’s integration. Contrary to the expectations of many, she said power flowed from MISO North/Central to MISO South more often than South to North. She said the MISO-SPP seams dispute is a significant barrier to trading and efficient power flows, but that the scheduled March 1 launch of market-to-market integration should help. (See SPP, MISO Move Ahead on Flowgate Rules.)

Patton Slams Seams Management

Bear tiptoed around the ongoing seams disputes with MISO’s neighbors, asserting the disputes are driven by fundamental differences between organizations that are equally convinced they have the best models. He acknowledged the need to compromise and resolve the disputes, and that he expects a settlement on the MISO-SPP dispute to be reached this summer. (See MISO Seeks FERC Review on ‘Hurdle Rate’ for SPP Seam.)

MISO Independent Market Monitor David Patton was extremely critical of the way the MISO-SPP seams dispute has been handled, scoffing at the notion that operational transmission congestion was the problem. Patton said it is very clear the issue is a “generation imbalance” situation between MISO North/Central and MISO South rather than physical congestion on the grid. Patton was very critical of the “completely ridiculous” constructs approved by FERC, calling the situation a “nightmare” that likely would get worse. Patton said there is “nothing physical” about the MISO-SPP constraint, asserting it is “totally fictional” to describe it as “congestion.”

Patton also criticized SPP for trying to get MISO to pay for SPP’s embedded transmission costs. He lamented that the current construct is undermining reliability based on a cost dispute. Patton said the “hurdle rate” approach helped, but the $10/MWh hurdle rate isn’t economically efficient and leaves a lot of savings on the table. He said raising the hurdle rate to $40/MWh would totally shut down flows and hurt customers.

Patton went on the attack again by sharply criticizing MISO’s lack of progress on transitioning to a capacity market that would send price signals for where new generation and transmission upgrades are needed. Patton acknowledged the opposition to capacity markets in MISO, but he also blamed FERC for not clearly addressing and providing guidance on capacity market issues.

Load Pockets Generate Discussion

Bear said MISO is performing economic studies to address the WOTAB (West of the Atchafalaya Basin) and Amite South load pockets in Louisiana. He said high “voltage and local reliability” (VLR) payments (known in some regions, including PJM, as reliability-must-run generation) prompted MISO to study whether transmission upgrades to address those areas would be economical. He said MISO sees $70 million in uneconomic generation dispatch costs, but the transmission upgrades don’t appear to be economic based on the current analysis. MISO expects to finalize its recommendations later in 2015.

Patton agreed that the make-whole VLR payments probably don’t justify transmission investments, which leaves the regions vulnerable to reliability risks because of their reliance on old, inefficient generation, he said. Patton said the situation “cries out for a market solution” rather than MISO’s transmission planning approach. MISO needs to develop a 30-minute planning reserve product that would attract developers to build new gas-fired combustion turbines in the load pockets, he said.

Jennifer Vosburg, NRG Energy’s senior vice president for the Gulf Coast Region, said that the load pocket issues aren’t new, but — “setting aside the lack of historical transmission investment by Entergy” — transmission may need to be built for the long-term. She agreed with Patton’s concern about the cost and risk to ratepayers if the problems are solved by utility self-build generation.

Can’t get enough Cruthirds? Click here for a more detailed account of the GCPA conference.