The Dooms-Lexington 500-kV line in Virginia will begin an extended outage next month and through winter to accommodate a rebuild of the 40-mile span.

The rebuild (Regional Transmission Expansion Plan project b1908) was ordered to prevent overloads on the line following the retirements of Chesapeake Units 1-4 and Yorktown Unit 1 generators.

The line will be out of service from Sept. 8 through June 5, 2015, returning to service for summer 2015 and then going offline again from Sept. 7, 2015 through Dec. 31, 2015.

To avoid limiting the output of the Bath County pump storage hydro plant, a special protection scheme (SPS) will be armed as needed to trip the Bath County generating and pump units on the loss of the Bath County-Valley 500-kV line. An existing Bath County “thermal” SPS will continue to be used as needed.

The project will also cause a potential thermal constraint on Valley transformer 1 for loss of the Dooms-Valley or Cloverdale transformers. Low voltages are possible from the loss of Bath County-Valley.

PJM authorized continuing work through the winter to reduce the overall outage duration by at least six months and coordinate it with other RTEP outages: the Cloverdale-Lexington 500-kV line in 2016 (AEP); the Cunningham-Elmont 500-kV line in 2016/2017; the Dooms-Cunningham 500-kV line in 2018; and the Mt. Storm-Valley 500-kV line in 2019/2021.

PJM planners identified no reliability issues during the winter outage. The rebuild is expected to be completed by June 2016.

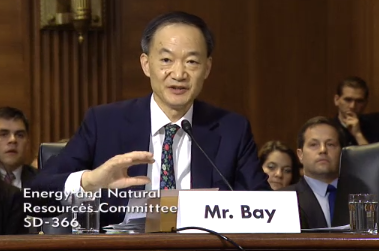

Norman Bay, with Richard Gates looking on, at his Senate confirmation hearing responding to questions about his handling of the Powhatan case.

In 2009, a Ph.D. electrical engineer turned energy trader shared with a suburban Philadelphia portfolio manager a seemingly unbeatable way to make money trading in the PJM market. The key was a poorly designed market rule that overcompensated up-to-congestion (UTC) trades with rebates for transmission line losses.

It was so easy, portfolio manager Kevin Gates said later, that “a monkey throwing darts at a dartboard” could have made money.

Gates feared PJM would realize its mistake before long. But in the meantime, he told his investment partners, they “should drive a truck through that loophole.”

That they did. By ramping up volumes on UTC trades that had little or no underlying risk, they made $4.7 million over five months in 2010 before PJM asked the Federal Energy Regulatory Commission to change the rule.

Four years later, the profits have shrunk, as Gates and his partners have spent more than $1.5 million on lawyers and consultants fighting a FERC investigation.

Last week, FERC staff issued a Notice of Alleged Violations against Gates and his partners, setting the stage for a showdown in a case that some critics say illustrates the excessive zealousness of FERC’s Office of Enforcement under former Director Norman Bay. The notice was filed the day after Bay was sworn in as the commission’s fifth member.

The facts, for the most part, are not in dispute. Thus the case will turn on legal interpretations: Were Gates’ trades riskless, and thus improper, “wash” trades, as FERC contends, or permissible “spread” trades? Did FERC provide proper notice that seeking profits through the line-loss rebates alone was improper? And if FERC thought it had a strong case, why did it wait nearly four years to bring it?

The following account of the case is based on records released by Gates and interviews with some of the principals.

Investment Fund Expands into Energy

Kevin Gates and his identical twin Rich manage private investment funds from an office in the Philadelphia suburb of West Chester, Pa. In 2008, the brothers met Houlian “Alan” Chen, who had emigrated to the U.S. in 1995 after receiving his doctorate degree in power engineering from Tsinghua University in Beijing.

Chen worked for about 10 years as a power analyst for several energy companies, creating models to forecast power prices, before forming his own investment fund in 2007.

Chen mostly traded up-to-congestion trades. UTCs, which load-serving entities use to hedge congestion risk, earn or lose money based on price changes between the day-ahead and real-time energy markets at individual pricing nodes. UTC traders profit if the difference between DA and RT prices is in the direction bid by the trader and the difference was large enough to cover the costs of scheduling the transactions.

Soon after meeting them, Chen began trading on behalf of the Gates brothers and their investors, who wanted to expand their investment options. Chen typically invested $4 of the Gates’ group cash for every $1 of his own.

Chen changed his trading strategy after he began receiving rebate payments, or transmission loss credits (TLCs), in October 2009.

Transmission Line Losses

PJM charges those moving power on its grid a fee to account for line losses — energy lost as heat during transmission. PJM’s method treated every transmission as if it were the last transmission in the system. Because this charged each buyer for the most problematic transmission at the time, it collected far more than actual losses.

Although UTCs don’t involve the movement of physical energy, UTC traders then had to reserve transmission service for each transaction, making them eligible for the line-loss rebates.

Chen discovered the rebates were far more than what he had paid for line losses and thus a potential source of profits. After several months of this found money, Chen and his investors began increasing the volume of their trades in February 2010. They were among a handful of traders who PJM says netted $19 million in unjust profits through the rebates.

Paired Trades

To profit on the rebates and limit the risk of loss due to the DA-RT price differences, Chen made paired trades, buying a day-ahead position in MISO and selling it at a point in PJM, while doing the same thing in the opposite direction.

At first, Chen chose an A-to-B, B-to-C trading formula, choosing “A” and “C” nodes whose prices closely tracked each other, such as Mount Storm, W.Va., site of Dominion’s largest coal-fired generator, and Greenland Gap, W.Va., the location of a Dominion wind farm 11 miles to the east. One of his favorite trades was Mount Storm to the MISO interface paired with MISO to Greenland Gap.

Had he and the Gateses continued this pattern, FERC might not be pursuing him now.

But on May 30, 2010, Chen and his partners were shocked when the UTC between MISO and Greenland Gap unexpectedly spiked and the Mount Storm-MISO trade that was intended to offset it failed to move.

Chen’s trades lost almost $180,000 on the change in price spreads. The $18,000 in scheduling costs was offset by the $22,000 in line-loss rebates, resulting in a net loss of more than $176,000.

Chen told Kevin Gates that the large volume of his trades may have contributed to the divergence between the two legs, saying “I suspect the trades we put on affected the day-ahead model runs.”

As a result, Chen changed his strategy, frequently dropping the A-to-B, B-to-C formula for a simple A-to-B, B-to-A round trip.

Assuming both legs of the matched pair cleared, this eliminated the risk of any price difference between the two trades. And that, said FERC, made them improper “wash” trades — transactions that involve no economic risk, no net change in ownership and serve no legitimate business purpose.

FERC had encountered wash trades before. Its investigation of market manipulation in the California and Western energy markets in 2000 and 2001 found that several energy trading companies, including Enron, had engaged in wash trades to create the illusion of liquidity and affect price indices to which contracts are linked. Although the commission then had no regulations on wash trading, such trades were prohibited in markets regulated by the Commodity Futures Trading Commission.

Moving the Market

In their preliminary findings, FERC staff told Chen and Gates that their large trading volumes “adversely affected the whole PJM market.” They cited a discussion between Chen and the other investors in which they acknowledged that their volumes were “moving the market.” A Gates associate complained that “we are trading too much and are bumping up against volume” and suggested they “scale back.”

Between February 2010 and early August 2010 — when PJM asked FERC to approve Tariff changes to close the loophole (ER10-2280) — Chen, Gates and their partners acquired 620,000 MWh eligible for the rebates, turning a $4.7 million profit. The rebates were large enough to cover the scheduling and transmission costs in more than 80% of the hours in which Chen used the identical pair strategy, according to FERC.

Legal Debate

Chen and the partners say their trades were not wash trades because they had a legitimate business purpose: Chen and his investors were making money on the trades.

They also faced the risk that one of the legs might not clear and they would be exposed to the DA-RT price differences. That would occur if the price spread they bet on was too low.

FERC rejects that argument, saying that Chen always bid a spread higher than historical experience for his selected nodes and usually bid at the maximum $50/MWh. The matched trades, FERC said, “never failed to clear.”

FERC’s authority to police market manipulation, which was expanded in the 2005 Energy Policy Act, largely mirrors the Securities and Exchange Commission’s trading rules.

The commission said Chen’s trading was similar to the conduct that the SEC and the Third Circuit Court of Appeals found illegal in the Amanat case, in which a trader seeking to collect rebates based on trading volume used a computer program to enter thousands of sham trades that bought and sold the same securities within a very short time period.

Gates and Chen countered with an affidavit from former SEC attorney Richard Wallace, who said that “trading for the purpose of collecting a rebate is considered a lawful and recognized practice in the securities markets.” When the SEC changed rules to prevent rebate-seeking trading, Wallace said, it did not seek to punish the traders who took advantage of the old rules.

FERC also rejected claims that Chen had no notice that profiting from the rebates alone was improper.

In the 2008 Black Oak Energy case, in which the commission confirmed the basis for PJM’s distribution of the refunds, staff said the commission sought to avoid a market rule in which “arbitrageurs can profit from the volume of their trades.”

Chen’s attorney, John N. Estes III, reads the Black Oak case far differently. In his response to the staff’s preliminary findings, Estes said that while the commission acknowledged the risk of arbitrageurs profiting from trading volume, it never said it was improper to do so.

“To conclude otherwise would fundamentally alter the obligations of market participants,” Estes wrote. “Rather than make decisions consistent with existing price signals, Enforcement’s theory of this case expects them to second-guess whether or not certain aspects of the Commission-approved markets are ‘appropriately’ functioning, and then adjust to their behavior accordingly.”

The investors’ attorneys also said their clients made no attempt to conceal their trading strategy. Thus there was none of the “fraud, artifice or deceit” typical of true market manipulation.

FERC said Chen and Kevin Gates were aware that their trading strategy carried regulatory risk.

“It really concerns me if PJM ever reverts back to those days without [transmission loss credits] or the TLC calculation was/is incorrect and we have to pay back all or some of the TLC refunds, we are going to be in big trouble,” Chen said in a message to Gates.

Gates responded: “[i]f you’re really concerned, then I’m really, really concerned” and suggested they “contact a law firm, the FERC or PJM to try to get more insight into this issue.”

They never did so, FERC says.

Estes said Chen’s trades “added value” to the PJM markets by contributing to price discovery and, “to the extent they caused day-ahead prices to move closer to real-time prices, they promoted market efficiency. They cannot be considered ‘wash’ transactions because they made money and because there was always a nonzero risk that Dr. Chen would be exposed to real-time price spread changes.”

Investigation Begins

FERC began investigating Chen and his partners in August 2010, after being alerted by PJM. Chen had stopped his round-trip trading immediately after receiving a call from PJM Market Monitor Joe Bowring on Aug. 2, 2010.

Over the next three years, Chen and his partners responded to FERC data requests and sat for depositions while their lawyers sparred with FERC’s attorneys and provided affidavits from an economist and an attorney supporting their position.

After one deposition, according to Kevin Gates, a FERC attorney told his lawyer, “He’s a businessman. He should know it’s cheaper to settle than to fight this.”

One company that engaged in similar trades, Oceanside Power, did go that path, agreeing to settle the charges against it by disgorging profits of $29,563 and paying a fine of $51,000 (IN10-5).

But Gates and Chen refused.

In October 2011, FERC said a charging decision was “imminent,” according to William M. McSwain, attorney for the Gates brothers.

FERC did not act, however, until August 2013, when FERC staff delivered a 28-page “preliminary findings” letter summarizing why they thought Chen’s trades were improper. Attorneys for Chen and Gates rejected the arguments and reiterated their demand that FERC end the investigation.

FERC refused.

Gates Goes Public

Frustrated, Kevin Gates began planning a publicity campaign to make the case that he and his partners had been unfairly hounded by FERC.

On Jan. 30, President Obama nominated Bay, then director of FERC’s Office of Enforcement, to fill the seat of former FERC Chairman Jon Wellinghoff.

A month later, Gates went public, launching a website that included much of the correspondence between FERC and the investors’ attorneys and written and video testimonials from an all-star cast including Harvard professor William Hogan and Susan J. Court, Bay’s predecessor as FERC enforcement chief.

FERC critics rallied in support of Gates and Chen, saying the case illustrated the agency’s overzealousness. Former FERC general counsel William Scherman cited the case in a Wall Street Journal op-ed published days before Bay’s Senate confirmation hearing.

FERC Gets More Teeth

When manipulative schemes by traders at Enron and other power marketers roiled the Western energy markets in 2000-01, FERC’s enforcement staff consisted of 20 lawyers in the Office of General Counsel. The maximum penalty FERC could impose was $10,000 per violation per day.

In the 2005 Energy Policy Act, Congress granted FERC expanded authority to police manipulation and increased its maximum penalties to $1 million per violation per day.

FERC’s enforcement unit is now staffed with about 200 economists, accountants, auditors, former traders and attorneys, including former prosecutors.

Under Bay, a former U.S. Attorney, FERC has issued orders demanding more than $1.1 billion in penalties and disgorged profits in market manipulation cases.

At Bay’s Senate confirmation hearing in May, the Gates brothers were sitting in the row behind him. Richard was on camera, over Bay’s shoulder, during the entire two-hour hearing as several Republican senators pressed the nominee to address Scherman’s criticism that Bay was driving Wall Street banks out of energy trading with heavy-handed enforcement tactics.

Bay survived the onslaught and was sworn in last Monday. On Tuesday, FERC issued a “Staff Notice of Alleged Violations,” the commission’s first public acknowledgement of the investigation. Later last week, staff sent the Gateses’ attorney a “1b 19” letter notifying them that staff would recommend the commission seek penalties.

(Although FERC’s preliminary findings challenged $4.7 million in profits the investors made between February and August 2010, the notice issued last week cites only trades made after June 1 on behalf of Chen and the Gateses’ Powhatan Energy Fund.)

De Novo

While most of FERC enforcement cases that become public are quickly settled, Chen and Gates vow that won’t happen in their case. Thus the next step will likely be a commission vote on whether to issue an Order to Show Cause.

If he can’t persuade the commission to drop the case McSwain said, the case will end up in a U.S. District Court.

It would be the third case contested in a de novo court review, joining pending cases involving Barclays bank and Richard Skillman.

Barclays is in federal district court in California, fighting an order that it pay a $453 million fine and disgorge $35 million in unjust profits over alleged manipulation of California and other western power markets. In Maine, energy consultant Richard Silkman is challenging a $1.25 million penalty. One central point of contention is how broad the federal court’s review should be, with FERC arguing for a narrow interpretation. (In addition, BP is challenging a $28 million penalty before a FERC administrative law judge.)

Members of the energy bar say those cases, along with the Chen/Gates case, will help to clarify questions about the limits of the FERC’s expanded enforcement authority.

Their attorneys say Chen and the Gates brothers are looking forward to their day in court.

“If we end up in federal court we start from scratch,” McSwain said in an interview. “It’s the first time we have a neutral decision maker.”

The Market Implementation Committee approved several changes recommended by the Market Settlement and Credit subcommittees regarding data submission deadlines and credit requirements.

Power Meter and InSchedule

One set of changes, which will be effective June 1, 2015, would extend the deadlines for electric distribution companies (EDCs) to submit Power Meter and InSchedule data to address problems with reporting output for non-utility generators. The delay will allow a higher percentage of actual load data to be reported in InSchedule, particularly for EDCs with smart meters, and reduce the reconciliation adjustments.

Power Meter deadlines would be extended by an hour:

Monday – Thursday Operating Days: Next business day @ 4 p.m. Eastern Prevailing Time (EPT)

Meter correction data deadlines would be extended by one month. The change would allow more time for generators and EDCs to gather data, improving accuracy of submitted corrections and reducing or eliminating later bilateral adjustments. PJM also would gain additional time to process and include the meter corrections in the bill.

In addition, load reconciliation data will be considered in balancing operating reserve (BOR) for deviation calculations. The change will affect all participants with BOR deviations. Load reconciliation billing would be performed under the current 60-day schedule.

Capacity Charge Reconciliation

The MIC also approved a change to provide relief for Pennsylvania EDCs squeezed by PJM and Pennsylvania Public Utility Commission deadlines.

PJM requires EDCs to upload their Peak Load Contribution (PLC) and Network Service Peak Load (NSPL) data to eRPM 36 hours prior to the operating day. The Pennsylvania PUC issued an order in April requiring that EDCs switch customers to new energy suppliers within three business days of notification of the switch. Under the PUC’s previous rules, it took 11 to 40 days to switch electric suppliers.

The new rule gives EDCs only one day to update their records to recognize the change and correct the PLC and NSPL values, raising the possibility of retail suppliers receiving inaccurate capacity charges.

The revised schedule retains PJM’s 36-hour-advance submission deadline but allows corrections to be made until noon the next business day.

Virtual Transactions Credit Requirement Reduced

As a result of improved cleared data availability under the eCredit system, the MIC approved a reduction in the credit requirement for virtual transactions to two days (one day of submitted bids for next market day plus one day of cleared bids) from four days (submitted bids for upcoming market day plus cleared bids for three prior days).

Also changed was the definition of credit available for virtual transactions, which would no longer include “billed” profits. The Credit Subcommittee said such profits cannot be depended on for recovery of transaction losses, because they are being committed to payout at the time a loss would be discovered.

Competitive Power Ventures plans to begin major construction next month on its 661-MW combined-cycle plant in Maryland despite an unfavorable ruling last week from the Federal Energy Regulatory Commission.

FERC rejected CPV’s request that it declare the company’s contracts with regulated utilities in New Jersey and Maryland “just and reasonable.” CPV filed the request in early June, believing that FERC’s approval would nullify appellate courts’ determinations that the contracts violated FERC’s ratemaking powers. (See Rebuffed By Courts, CPV Seeks FERC End-Around.)

Instead, FERC said, “In considering whether the rates, terms, and conditions in a contract are just, reasonable and not unduly preferential or discriminatory under the FPA, the contract must first be a valid contract.” As the contracts had already been found invalid by the courts, FERC rejected the filing.

CPV announced Friday that it has obtained financing from 15 lenders, led by GE Energy Financial Services, for the $775 million St. Charles Energy Center in the Southern Maryland community of Waldorf.

CPV Chief Financial Officer Paul Buckovich told The Baltimore Sun that the costs are much higher than if the company had come to lenders with the original contracts. “The financing is much more expensive and less beneficial to sponsors and ultimately to the ratepayers,” he said.

CPV has already begun preliminary site work on the Waldorf site. The plant will be built under a “medium-term contract financing” that will require CPV to refinance five years after starting operations. The arrangement is similar to that used to build CPV’s Woodbridge, N.J., plant, which is also under construction.

CPV had sought to build two plants supported by contracts with utilities in Maryland and New Jersey. Each contract was based on a benchmark amount; if CPV’s capacity revenue was less than this amount, the utilities would pay CPV the difference. If the revenue was more, CPV would pay the utilities.

The utilities were forced to sign the contracts by each state’s public utilities commission, which led to them filing lawsuits.

If PJM overestimates the Tier 1 resources available, it won’t procure enough Tier 2 reserves.

PJM last week proposed eliminating some generators from the calculation of Tier 1 synchronized reserves, along with an unintended “windfall” the Market Monitor says those units receive in compensation.

Under a proposal outlined to the Market Implementation Committee last week, PJM’s market clearing engine would assume no synchronized reserve contribution from nuclear, wind, solar, batteries and certain hydro units that PJM says cannot be counted on to provide the service.

Although the clearing engine would set those resources’ synchronized reserve contribution to 0 MW, the generators would be credited for reserves they do provide in a spinning event.

The rule change also would eliminate a rule that requires PJM to pay Tier 1 resources when the non-synchronized reserve price rises above zero. Under the revision, only those resources that can “reliably provide” synchronized reserve service would receive that compensation.

“We’re paying Tier 1 a lot of money — in fact, a huge amount of money” for unresponsive resources, Market Monitor Joe Bowring said. “There’s no reason to do it.”

PJM’s 1,375-MW synchronized reserve requirement is equal to the largest contingency in the RTO. Tier 1 resources — online units following economic dispatch that are only partially loaded and thus able to increase output within 10 minutes — provide most of the needed reserves.

Tier 2 resources such as demand response and combustion turbines — which are capable of providing reserves within 10 minutes and have cleared the synchronized reserve market — make up any shortfall.

Realistic Estimates

PJM currently estimates Tier 1 resources based on the difference between units’ bid-in parameters (EcoMax) and economic dispatch points, rather than on explicit offers from resources, making it prone to errors. If PJM overestimates the Tier 1 resources available, it won’t procure enough Tier 2 resources.

“We have to make sure we have realistic estimates of what resources can increase output and what couldn’t be relied on,” explained Stu Bresler, vice president of market operations.

Wind units typically operate at their maximum capacity — but that is dependent on weather conditions, Bowring noted. “You have to be able to know [the extra output is] there, and you can’t do that with wind, because the wind may be blowing. It may not be.”

Synchronized Reserve Windfall

In addition, PJM’s synchronized reserve costs are higher than necessary because of the unintended consequence of its shortage pricing rules, which require that Tier 1 reserves be paid the Tier 2 synchronized reserve clearing price any time the non-synchronized reserve clearing price is above $0.

“This rule significantly increases the cost of Tier 1 synchronized reserves with no operational or economic reason to do so,” the Monitor said in the 2013 State of the Market report. “PJM is not actually reserving any Tier 1 but simply paying substantially more for the same product without any additional performance requirements.”

Although the rule doesn’t apply in most hours, when it does, it’s expensive. In 2013, the Monitor said, 40% of payments for Tier 1 reserves were paid when they were not needed. “This is a windfall payment to Tier 1 reserves,” the Monitor said.

Bowring said PJM’s proposal will not eliminate the problem. The RTO would still pay some Tier 1 resources the Tier 2 price when the non-synchronized reserve price is greater than zero, he said.

Ohio electricity consumers paid FirstEnergy $6.9 billion to compensate the company for generation assets “stranded” when its monopoly over energy sales was eliminated in 1999.

Now, FE is asking them to pay again to prop up nuclear and coal generating plants the company says are at risk of closing due to low energy and capacity prices.

While the economics of the proposal aren’t convincing to consumer advocates and environmentalists, the company seems to be betting on its appeal to state lawmakers eager to save the plants’ jobs and tax revenues.

Under a proposal dubbed “Powering Ohio’s Progress,” the company asked the state Public Utility Commission last week to order three of its regulated utilities to sign 15-year purchase-power agreements with the Davis-Besse nuclear plant, the mammoth coal-fired W.H. Sammis plant and two Ohio Valley Electric Corp. (OVEC) units — located in Gallipolis, Ohio, and Madison, Ind. — in which it owns a 105-MW interest.

FirstEnergy Assumptions

In effect, FE wants distribution customers of Toledo Edison, Ohio Edison and The Illuminating Company to subsidize the plants in at least the short term in return for the potential upside in the later years. FE projects market revenue will begin exceeding costs in 2019 and continue to do so throughout the remainder of the program, saving retail customers $2 billion (nominal) or $800 million in net present value — an average of $360 (nominal) per customer — over the 15-year term.

The projected savings are based on layers upon layers of assumptions, including future fuel prices, economic growth and operating expenses. Some of the assumptions, such as an ICF International projection on future electricity prices, have been redacted and cannot be inspected by the public (though the numbers will be available to Ohio PUC analysts).

UBS Securities said the PPA was priced to begin at about $65/MWh — $26 above current market prices —and increase by $2/MWh annually.

FE said the plan will “help mitigate rising retail prices and help ensure that vital baseload power plants built to serve Ohio customers remain available to support the state’s electric consumers and businesses.”

“Ohio’s economic security and quality of life is highly dependent on maintaining a diverse mix of baseload coal and nuclear power plants,” FirstEnergy CEO Anthony Alexander said in a statement. “Powering Ohio’s Progress helps ensure these vital facilities continue powering the state’s energy-intensive economy, helps protect customers against volatility as future prices rise, and preserves $1 billion in annual statewide economic benefits, vital tax revenues for local communities and an estimated 3,000 direct and indirect jobs created by these plants.”

Deja Vu

The proposal makes no sense to the Office of the Ohio Consumers’ Counsel.

“1.9 million consumers paid billions of dollars to FirstEnergy for its transition to deregulated power plants under a 1999 Ohio law,” OCC spokesman Scott Gerfen said. “Fifteen years later, FirstEnergy is again asking consumers to pay charges related to the power plants. FirstEnergy’s requests include asking the government to guarantee profits for what are deregulated power plants whose profits should instead be determined by the electricity market.”

The Sierra Club also was critical.

FE “is essentially asking for a blank check to bail out their dirty, aging coal plants at the expense of customers, the environment and public health,” said Daniel Sawmiller, senior campaign representative for the Sierra Club’s Beyond Coal campaign. “We are urging the PUCO and Gov. [John] Kasich not to make Ohioans pay more every month for dirty coal plants.”

“The fact is,” Sawmiller said, “Ohio is a de-regulated state. They just want to go back to rate base. That is not what the law is in Ohio.”

Volatility Protection

That’s not how FE sees it. Company spokesman Douglas G. Colafella said Friday that the plan is aimed, in part, at preserving the reliability of regional power grid, and protecting FE customers from weather-related price spikes.

“Recent weather events, such as last winter’s polar vortex and September 2013’s unseasonable heat wave, have exposed potential vulnerabilities on the electrical grid serving Ohio and surrounding areas — in some cases resulting in severe retail price spikes,” he said. “In addition, a significant number of baseload power plants are being prematurely retired due to a variety of factors. Together, these issues are putting Ohio’s energy future at risk by challenging the reliability and affordability of electricity in our region.”

Under the plan, FE’s regulated Ohio utilities will buy the plants’ output from unregulated FirstEnergy Solutions, the power plant owners, and then sell it into PJM’s capacity, energy and ancillary services markets from June 2016 through May 2031.

The regulated utilities would pay all of the plants’ expenses, including fuel, operations and maintenance, depreciation and taxes, plus a “reasonable” return on invested capital of 11.15%.

The three utilities would net the revenues against costs, with the difference being passed along to customers through a “retail rate stability rider” that would act as a charge or credit on their monthly bills based on the fortunes of the plants in PJM’s markets. The utilities would freeze distribution rates, which they say have increased only 1% since 2009, through 2019.

“As power prices increase as projected over time, proceeds from the market sales that exceed costs from the purchased power agreement will be applied as credits on customers’ electric bills to mitigate volatility and address rising retail prices,” FE said in a press release.

The company predicts that its regulated utility customers in Ohio would pay higher prices for the first three years — about $3.50 per month for the first year — and then the market prices would increase and the surcharge would transform into a credit. None of it, however, is guaranteed.

Tough Sell

UBS analysts, who last month changed their outlook on FE from “hold” to “sell,” issued a report last week expressing skepticism that the company will win commission approval for the proposal, although a smaller, less expensive plan might pass muster.

“Given the PUCO staff’s rejection of AEP’s proposal to add just its OVEC ownership into a PPA rider, we suspect a similar reaction from staff,” UBS said. “The fundamental question for Ohio remains how politically palatable will it be to continue to allow substantial coal and nuclear retirements?”

FE is portraying the plan as an attempt to save two of its largest generation assets — the 2.2-GW Sammis plant and the 908-MW Davis-Besse nuclear plant. But UBS said the company’s leverage with state officials was reduced by the disclosure that the two plants cleared PJM’s Base Residual Auction in May.

In its quarterly earnings filing last week, FE reported that it cleared 8,930 MW in the capacity auction, up from 7,440 in the 2013 auction but down from the more than 10,000 MW that cleared in the prior three auctions.

Mansfield Retirement Risk

FE officials said that because its 2.4-GW Bruce Mansfield coal-fired plant had not cleared the auction, it would delay spending on a dewatering facility it needs to continue operation beyond the end of 2016, when the plant’s coal ash waste impoundment must close. The plant is Pennsylvania’s largest generator.

The Ohio PUC has not yet set a hearing date on the 1,000-page filing; the company has requested a decision by next April.

There are certain to be many eyes on the plan going forward.

“Needless to say, we are concerned for consumers,” OCC’s Gerfen said. “We are analyzing FirstEnergy’s new request, including its claim that there will be future cost savings. We then will make recommendations on behalf of consumers to the PUCO.”

PJM has created a new emergency procedure and is testing a software fix following poor generator response to a minimum generation event July 5, officials told the Operating Committee last week.

Extremely mild temperatures and a holiday weekend resulted in an RTO peak of 61,300 MW — unusually light but in line with PJM’s forecast — forcing PJM officials to curtail 2,000 MW of imports and order cuts of 100% of reducible generation.

Of about 200 generation owners, only 31 (16%) responded to the eDart minimum generation report. Of those that responded, only half reported an emergency reducible value greater than 0 MW.

But only 1,458 MW of the 1,665 MW of reducibles — units that said they were willing to go below their economic minimum — responded, PJM’s Chris Pilong told the committee.

Among combined-cycle owners that responded, all reported economic minimum ratings — the lowest level a unit can achieve while following economic dispatch — equal to their emergency minimum — the minimum generation that can be produced by a unit while maintaining stability.

“We only know what the generation operators, owners tell us,” said Mike Bryson, executive director of system operations.

Pilong said the responses indicate the need for additional training. “We really need to be sure we have the right rules in place so that people are reporting the real emergency min and not the eco min.”

Low Prices

Pilong said many generators entered low-priced offers for the weekend, wanting to keep running over the holiday to capitalize on hot weather forecast for the following week. Pilong said operators also were stressed by the inability of PJM’s dispatch engine to set proper price signals for wind units bidding below $0/MWh.

The RTO is testing a software fix to allow prices as low as -$60/MWh, which should help incent wind units to respond automatically via automatic generation control (AGC). Currently, some wind operators do not respond to AGC signals, requiring phone calls from PJM operators.

In addition, PJM has created a new minimum generation advisory procedure that it can issue one or two days in advance of anticipated light load days.

Minimum Generation Event Chronology

PJM declared a minimum generation alert at 10:25 p.m. July 4, saying the RTO was within 3,286 MW of normal minimum energy limits.

At 12:25 a.m. July 5, a Saturday, operators issued a minimum generation emergency declaration, reducing prices to $0/MWh and indicating a need to cut generation at 3 a.m.

Shortly before 3 a.m., operators declared a minimum generation event, ordering a 50% cut in reducible generation. Generators were encouraged to sell energy outside the control area.

Thirty-five minutes later, operators upped the call for reducible generation cuts to 100%. It remained there until shortly before 8 a.m., when it was reduced to 50%.

Before then, at 3:30 a.m., operators manually ordered all remaining wind (1,000 MW) to zero and ordered three other generators offline. All hydro was either offline or pumping into storage.

Hot Water Heaters

John Farber of the Delaware Public Service Commission said the incident illustrated why PJM should create a resource category for thermal storage, such as hot water heaters, that can provide load. “PJM could help [the Department of Energy] move off the dime,” Farber said.

Farber was referring to DOE’s pending decision on whether to exempt large capacity grid-interactive water heaters from current energy efficiency standards or regulate them under a separate category.

A federal judge approved a $27.8 million settlement between the Tennessee Valley Authority and property owners harmed by the utility’s massive coal ash spill in 2008. The spill occurred when a dike burst at TVA’s Kingston Fossil Plant and released more than 5 million cubic yards of toxic ash sludge from a containment pond. The sludge flowed into a river and fouled hundreds of acres along the river about 35 miles west of Knoxville, affecting about 800 property owners. U.S. District Court Judge Thomas Varian found TVA at fault in 2012.

The Federal Energy Regulatory Commission last week approved a consent agreement that its Office of Enforcement and the North American Electric Reliability Corporation reached with the Imperial Irrigation District relating to a Sept. 8, 2011 blackout that left more than 5 million in the dark. NERC and FERC found that the IID violated four Reliability Standards in its operations leading up to the blackout that spread from Southern California to Arizona and Baja California, Mexico. The settlement mandates that the IID spend at least $9 million on system reliability improvements, with the remaining $3 million going to the U.S. Treasury and NERC.

The Department of Energy has developed an Internet-based portal to a trove of its scholarly publications and research data. The Public Access Gateway for Energy and Science – PAGES – provides free access to manuscripts and published scientific journal articles within a year of publication.

“Increasing access to the results of research … will enable researchers and entrepreneurs to capitalize on our substantial research and development investments,” Secretary of Energy Ernest Moniz said. PAGES already contains a collection of accepted manuscripts and journal articles, and more data and links to articles and accepted manuscripts will be added as they are submitted. DOE hopes it grows by up to 30,000 articles and manuscripts a year.

The Environmental Protection Agency last week named Lisa Feldt as acting deputy administrator, the second highest position in the agency. She replaces Bob Perciasepe, who served in the position since 2009. Perciasepe is leaving to become director of the Center for Climate and Energy Solutions, an advocacy group. Feldt’s appointment was among several staffing announcements at the agency.

EPA Chief: Climate Change Should Be Taught in Schools

Gina McCarthy

Environmental Protection Agency Director Gina McCarthy said in an interview she thinks the science behind climate change should be taught in the nation’s schools. “I think part of the challenge of explaining climate change is that it requires a level of science and a level of forward thinking and you’ve got to teach that to kids,” McCarthy said in an interview published last Friday in the magazine Irish American. Observersbelieve her remarks will generate controversy, especially among Republican lawmakers who remain skeptical of the idea of man-caused climate change.

The Nuclear Regulatory Commission is expected to issue the final rule governing storage of nuclear waste, a rule that has impacted nuclear generating stations’ ability to store used fuel on site. The U.S. Court of Appeals for the D.C. Circuit in 2012 found that the NRC rule allowing on-site storage for up to 60 years violated the National Environmental Policy Act and ordered the NRC to come up with a new rule. The new rule is expected to be released within a month and will be named “Environmental Impacts of Continued Storage of Spent Nuclear Fuel Beyond the Licensed Life for Operation of a Reactor.”

The Nuclear Regulatory Commission last week cited Exelon, operator of the Calvert Cliffs nuclear station in Lusby, Md., for a miscalculation that could have led to an unnecessary evacuation. Radiation detectors at the plant were accidentally set to trigger an alarm at radiation levels 100 times lower than what would have posed a safety threat. The alarm was never activated, and workers discovered the mistake and corrected it four months later.

NRC inspectors said the mistake could have caused an unnecessary evacuation and deemed it a safety violation. “Ideally, we want them to be in the right zone if they have an emergency event,” NRC spokesman Neil Sheehan said, “not under-classifying it but not over-classifying it, either.” The violation could result in increased NRC scrutiny of the plant.

PJM received 106 proposals to fix about 50 reliability problems in the first Regional Transmission Expansion Plan window for 2014.

Fifteen companies made proposals in the window that closed July 28. PPL was the most ambitious, offering 16 projects totaling almost $3 billion.

It was the first full-scale reliability window opened by PJM under the Federal Energy Regulatory Commission’s Order 1000. Last year, PJM opened a window for a single reliability problem at Artificial Island and one for “market efficiency” proposals intended to reduce congestion.

The PPL projects include the reliability portion of a 725-mile, 500-kV transmission line that would run from Western Pennsylvania into New York and New Jersey, with a spur running south into Maryland, at an estimated cost of $4 billion to $6 billion. PPL said the line would address reliability problems on three 230-kV lines, as well as relieve congestion and move power from planned generators fueled by shale gas in northern Pennsylvania.

Four other companies – Public Service Enterprise Group, Transource Energy, ITC Holdings and LS Power’s Northeast Transmission Development – each proposed projects totaling more than $500 million.

They include 61 greenfield projects (total $5.7 billion) and 45 transmission owner upgrades totaling $522 million. Targeted were 18 transmission zones in 10 states, with Atlantic City Electric (AE), PPL, American Electric Power and American Transmission Systems Inc. each attracting 10 or more proposals.

The proposals are intended to address reliability violations that would occur through 2019. Some problems may be moot by that time, however, according to Paul McGlynn, general manager of system planning. Some violations in the AEP transmission zone, for example, will be eliminated by the planned retirement of AEP’s Tanners Creek generators, scheduled for mid-2015.

“We may not act on [all of] these issues,” McGlynn said. “There’s a lot of failings that won’t actually be problems.”

Conversely, problems identified in the AE zone because of capacity injection rights for the BL England generator may not manifest if the plant retires and is not replaced, planners said.

PJM plans to open a “long-term” window in November for market efficiency and reliability proposals addressing problems over a 15-year horizon.

Artificial Island Update

Meanwhile, McGlynn told the Transmission Expansion Advisory Committee that PJM will be sending Artificial Island project finalists Public Service Electric & Gas, Dominion Resources and Transource letters next week asking them whether they will join finalist LS Power in agreeing to cap the costs of their proposals.

McGlynn said the finalists would have no more than two weeks to respond and that PJM is still planning to make a selection by year’s end. “The answers we get back from the finalists may lead to more questions,” he said, promising an “open and transparent” process for comparing any revised proposals.

The allocation was split 50/50 based on load-ratio share and a distribution factor (DFAX) analysis. Planners said the original DFAX analysis assumed flows for a new 500-kV line between Artificial Island in New Jersey and Red Lion, Del., would be predominantly west to east when they are actually the reverse.

Although revised calculations have not been completed, planners said they expect allocations for transmission zones west of Artificial Island to increase.

The original allocation would have assigned costs to among two dozen transmission zones and merchants with the Jersey Central Power & Light zone responsible for about 27% of the project and the AE zone picking up almost 20%.

The error did not affect the cost allocation for LS Power’s proposed 230-kV line between Artificial Island and Cedar Creek, Del., all of which would be allocated to the Delmarva Power & Light zone, according to PJM.

PJM dropped a proposal to consider changes to the regulation market after receiving a cool reaction from stakeholders and the Market Monitor.

PJM officials drafted a proposed problem statement in response to the polar vortex in early January, when regulation market prices spiked to 4.5 times normal levels.

Regulation prices hit $3,296/MWh at the peak of the polar vortex as real-time energy prices rose above $1,800/MWh. Including lost opportunity costs — for example forgone revenue in the energy market — PJM rang up a $65 million bill for regulation in January.

PJM’s Jeff Schmidt said the jump was due in part to the fact that high-performing generators were being used for energy and reserves instead of regulation, leaving the RTO to rely on poorer-performing generators to maintain system frequency at 60 hertz. Regulation market prices can be influenced by poorer-performing resources because the calculation uses a “historic performance score” in the denominator.

The issue was first raised in PJM’s analysis of the system’s performance during January’s cold. PJM said stakeholders should consider whether the division by the performance score is appropriate and whether the minimum participation requirements are high enough. It also said they should consider whether to go short on regulation during system peaks.

But the 4x jump in regulation prices was actually far below the increases in operating reserve (10x) and synchronized reserve (9x) costs for the same period.

“I don’t understand why it’s a problem,” Market Monitor Joe Bowring said during a discussion before the Market Implementation Committee last week. “Poor-performing resources raised the prices. That’s exactly the way it’s supposed to work.”

Brock Ondayko of American Electric Power Energy Supply agreed with Bowring. “If we start weeding out the slower performers I guess you would end up with no regulation resources,” he said.

“That certainly could happen,” Schmidt acknowledged.

Public Service Enterprise Group’s John Citrolo said it was improper for PJM to take an “administrative role” in controlling volatility “rather than letting the market handle it.” He said load-serving entities can hedge against such risks.

John Webster of Icetec said increasing the performance requirement for regulation resources might actually increase prices.

After an extended discussion, MIC Chair Adrien Ford said she would table the matter, though PJM may bring it back at a later meeting.

Performance-Based Pricing

In response to the Federal Energy Regulatory Commission’s Order 755, PJM switched in October 2012 to performance-based regulation, which is intended to pay resources based on the accuracy, speed and precision of their response.

In the 2013 State of the Market report, the Monitor said that the changes had improved the regulation market, but that the market’s design remained “flawed,” including an incorrect definition of opportunity cost and an inconsistent implementation of the marginal benefit factor — a conversion calculation — in optimization, pricing and settlement.

The Dooms-Lexington 500-kV line in Virginia will begin an extended outage next month and through winter to accommodate a rebuild of the 40-mile span.

The Dooms-Lexington 500-kV line in Virginia will begin an extended outage next month and through winter to accommodate a rebuild of the 40-mile span.