Although large loads are not new to California or the West, CAISO is formulating technical standards that address their potential boom over the coming years.

Developing the standards is a critical step to ensure artificial intelligence data center and electric vehicle large loads will reliably and safely interconnect to CAISO’s grid. The ISO established a working group on the issue in 2025 and opened a new large loads initiative Feb. 27.

“Large loads are a topic of extreme urgency and interest lately, especially with the emergence of artificial intelligence,” Danielle Mills, CAISO principal of infrastructure policy development, said at a March 10 workshop. “But we also consider large loads to be more than just data centers and AI. While data centers do present the largest use case, we are also looking at things like electric vehicle charging, electrification of buildings, and industrial processes and agricultural processes and the like.”

CAISO’s 2025/26 transmission plan shows 4.5 GW of data center capacity online currently, with an additional 1.8 GW added by 2030 and 4.9 GW more by 2040.

“We do proactively plan for these types of large loads through the integrated planning process with the California Energy Commission,” Mills said. “We are always trying to stay ahead of any new demand for large loads, but we are aware that this is really dynamic space right now and that we are seeing increasing numbers of large load interconnection service applications at the utilities.”

CAISO is developing a definition of what constitutes a large load and new requirements for voltage and frequency ride-throughs, along with setting limits on rapid ramping and pulsating load levels. (See CAISO Examines ‘Pulsating’ Data Center Loads.)

One topic of concern is how large loads consume power or reduce load during grid disturbances, such as during a post-fault active power recovery (PFAPR) moment.

“Our mission is to ensure large loads continue to draw power from the grid during and following grid disturbances,” Ebrahim Rahimi, CAISO senior adviser for transmission planning, said at the workshop.

During a PFAPR, large loads will be allowed to reduce their power consumption during and immediately after severe faults, Rahimi said. However, after the fault is cleared and voltage returns to normal, the power consumption from the grid should be required to recover to — or close to — pre-disturbance levels within a given time, Rahimi said.

Another concern is persistent small load fluctuations. Even modest but continuous fluctuations in load can produce voltage flicker or unacceptable variations in local power quality, CAISO staff said in a large loads issue paper.

Over time, these load fluctuations might increase mechanical fatigue in equipment, such as in rotating machines and transformers. Requirements will need to ensure that persistent small-signal load variations remain within acceptable limits, staff said.

CAISO is also following NERC’s formulation of national standards for large loads, such as for computation loads from AI training centers. Rahimi said those standards will be ready for approval at the end of 2026, and NERC plans a large load Level 3 alert in May or June.

CAISO has not yet decided where large load technical requirements ultimately will be documented and enforced, he said.

“Although we are coming up with these technical requirements … how these requirements will be documented has not been decided at this point,” Rahimi said. “The whole idea is to come up with these requirements and ensure reliability, and then at a later stage a decision will be made about where to document them.”

CAISO plans to publish a straw proposal in April that includes technical requirements, transmission service offerings and cost-allocation methods for large loads.

New York energy storage and solar trade groups are seeking an immediate end to what they say is an effective freeze on interconnection of distributed storage facilities by the state’s largest investor-owned utility.

The New York Battery and Energy Storage Technology Consortium (NY-BEST) and New York Solar Energy Industries Association (NYSEIA) filed a petition for emergency rulemaking March 11 asking the Public Service Commission to restrict Consolidated Edison from applying an “unlawful and arbitrary” review standard for New York City storage projects.

They charge that Con Edison’s review process was implemented without legal justification, is causing irreparable harm to the storage industry and is exacerbating grid reliability concerns in the region. There was no need to change the way storage is studied under the state’s Standardized Interconnection Requirements, they argue, but if such a need did exist, there are much better ways to address it.

The utility stood by its actions.

“Con Edison supports battery storage as a critical part of New York’s clean energy transition, and the rapid growth in applications reflects strong market momentum,” Vice President for Distributed Resource Integration Raghu Sudhakara told RTO Insider via email March 11. He added, however, that the sector’s expansion must be carried out in a way that does not shift new infrastructure costs onto the utility’s ratepayers.

The disagreement has been fermenting for months, and it spans PSC cases on energy storage (18-E-0130), distributed generation and storage (24-E-0621) and New York City reliability needs (25-E-0764).

Battery energy storage systems (BESS), with their dispatchable output and lack of on-site emissions, are one of the potential solutions in the densely populated region; over 2,000 MW of capacity have been proposed.

On Aug. 15, 2025, Con Edison notified developers that it had placed on hold all BESS proposals seeking interconnection at seven constrained substations. It added 21 more substations to the list Sept. 16.

NY-BEST on Jan. 13 petitioned the PSC for “urgent action” on the utility’s move. It supported its call for immediate relief from Con Edison’s new restrictions on BESS interconnection with a white paper outlining suggested changes in interconnection and market rules to better enable storage to provide maximum value to the grid.

The infrastructure upgrade requirements resulting from Con Edison’s changes to the Coordinated Electric System Interconnection Review rendered most of the energy storage projects proposed in New York City economically unviable, NY-BEST said.

The organization also flagged the “fundamental misalignment between utility financial incentives and New York’s energy affordability goals”: A utility earns a regulated rate of return on capital expenses such as infrastructure upgrades, but not for facilitating third-party BESS interconnections.

The PSC on Feb. 20 solicited public comment on the petition but took no action to change or limit Con Edison’s practice.

On Jan. 14, Con Edison told the PSC there were 115 MW of operational BESS and 865 MW with executed interconnection agreements in the utility’s service area as of Dec. 31. But the interconnection queue for BESS proposals with 5 MW or less capacity had reached 2,500 MW, up 300% in two years.

That is a quarter of its 10-GW peak load in 2024, Con Edison wrote.

A problem, it said, was that the BESS proposals were being concentrated in areas with less expensive land and more favorable zoning — 65% of the storage megawatts in the queue would be supplied by just 10 of the company’s 63 substations. More than 20 substations were at or near hosting limits.

Because BESS typically would seek to recharge overnight, full buildout would make night peaks exceed daytime peaks and require new infrastructure that otherwise would not have to be built. Con Edison sought to put the developers on the hook for the resulting costs, which it said could run in the $100 million to $1 billion-plus range.

“As the market scales, storage must deliver real benefits to customers — not drive new infrastructure costs that show up on bills — which is why we are working with regulators and stakeholders to align growth with real-world grid conditions preserving grid reliability while also protecting affordability,” Sudhakara explained. “Without reforms, current policies risk shifting significant new costs to customers, undermining both affordability and the long-term success of storage.”

NY-BEST and NYSEIA in their petition attempt over the course of 26 pages to punch holes in the legality, accuracy and necessity of Con Edison’s steps to carry out the priorities Sudhakara cited.

They ask the PSC for an emergency rule to immediately block Con Edison from using the restrictive requirements for distributed storage applications and keep the ruling in place while it considers NY-BEST’s Jan. 13 petition.

As Nevada regulators consider NV Energy’s request to join CAISO’s Extended Day-Ahead Market, the debate over the independence of EDAM’s governance has reached a critical point.

EDAM proponents and opponents shared their views during a Public Utilities Commission of Nevada hearing March 10. The parties also sounded off in written testimony and rebuttal comments filed with the PUCN in February. The commission is expected to vote April 3 on NV Energy’s EDAM request.

“I recommend that the commission prioritize the independence of the market’s governance over most other factors,” David Patton, president of Potomac Economics, an independent market monitor for four RTOs/ISOs, said in written testimony filed on behalf of Powerex and Wynn Las Vegas, a luxury resort and NV Energy customer. Powerex has committed to joining SPP’s Markets+, a competing day-ahead market.

Through the West-Wide Governance Pathways Initiative and California Assembly Bill 825 of 2025, governance of EDAM and CAISO’s Western Energy Imbalance Market is being shifted to a Regional Organization for Western Energy (ROWE). Some see the ROWE as a means to alleviate concerns among potential market participants that CAISO, whose governing board is appointed by the California governor, plays too large a role in the markets’ governance.

Patton said the ROWE is “a very positive step” in the governance of EDAM and WEIM. But he said the entity is proposed to have minimal staff and that “critical roles,” including market operation, would remain with CAISO.

During the March 10 hearing, NV Energy representatives and intervenors in the case presented witnesses for questioning by the other parties in attendance. PUCN Chair Hayley Williamson presided over the session.

Attorney Curt Ledford with Davison Van Cleve grilled Stacey Crowley, CAISO’s vice president of external affairs, about EDAM governance. Ledford represents Powerex and Wynn Las Vegas.

Ledford asked Crowley to read aloud Section 345.5(a) of the California Public Utilities Code, which directs CAISO to “conduct its operations … consistent with the interests of the people of the state.”

“When you read ‘the state,’ do you understand [that to mean] the state of California, not the state of Nevada?” Ledford said.

“Correct,” Crowley responded.

Ledford asked Crowley about the steps needed to establish the ROWE. While the ROWE has an interim board, it doesn’t yet have staff. A consumer advocate office must be established, and a service agreement needs to be drawn up between the ROWE and CAISO. That agreement must be reviewed by the California Public Utilities Commission for conformance with AB 825 and likely will need FERC approval.

CAISO wants to wait until the permanent ROWE board is in place before negotiating the service contract, Crowley said.

“Would it be fair to say that this entire ROWE exercise could be for naught if CAISO doesn’t pursue it?” Ledford asked.

Crowley disagreed.

“The [ROWE] could exist without California participation,” she said, later clarifying that the ROWE “could take on other Western services if they so choose.”

In response to Ledford’s questioning, NV Energy attorney Roman Borisov asked Crowley whether the Pathways Launch Committee has the most control over the Pathways Initiative at this time. Crowley said yes, noting that the committee has broad representation from across the West and industry sectors.

Until the ROWE takes over governance, EDAM and WEIM are being overseen by the Western Energy Markets Governing Body, which has shared authority with the CAISO Board of Governors.

Without NV Energy, EDAM would lose a large and central piece of its footprint.

David Rubin, NV Energy’s federal energy policy director, said Section 345.5 of the California Public Utilities Code was adopted before CAISO was running a regional market. He noted that AB 825 added Section 345.6, which allows California utilities to participate in a CAISO market that has independent governance if the FERC tariff for the market includes a requirement to respect the authority of each participating state. That authority includes setting procurement, resource adequacy, environmental, reliability “and other public interest policies.”

The language “reflects a clear recognition that the regional markets — including the EDAM — must accord equal respect to the policy interests of all participating states,” Rubin said in written rebuttal testimony.

Rubin said market participants and regulators must have confidence in the overall fairness of a market’s governance.

He said other key reasons why NV Energy chose EDAM are the company’s positive experience in the WEIM; expected costs of day-ahead market implementation; EDAM’s expected market footprint and interconnectivity of participants; and transmission work within the footprint that will enhance interconnectivity and supply diversity.

Additional reasons are EDAM’s market design and projected financial, reliability and environmental benefits.

“These factors favor the EDAM over Markets+,” he said.

Oregon and Washington lawmakers are exploring ways to build new transmission independent of the Bonneville Power Administration as electric sector stakeholders in the Pacific Northwest worry about the agency’s struggle to build transmission fast enough to keep up with aggressive clean energy laws and increased load.

BPA paused certain planning processes in 2025 to consider how to address nearly 61 GW of transmission service requests. The agency presented several proposals to reduce the queue, but concerns have been raised that many of the efforts would go into effect after the 2030 deadline for utilities in Oregon and Washington to meet strict greenhouse gas standards.

Former BPA Administrator Randy Hardy has argued the issue lies with the states’ respective clean energy laws, which he said set off a “gold rush” among developers, leaving BPA to solve the issue of building enough transmission to keep up. His comments received support from utilities and other organizations during BPA meetings. (See BPA Tx Planning Overhaul Prompts Concern for Northwest Clean Energy Compliance.)

For Gamba, the issue is not the law’s requirements but rather that BPA, which controls approximately 75% of the region’s high-voltage transmission, has failed to build enough transmission.

“I’m less concerned with HB 2021 and the law as I am with the fact that we are still burning fossil fuels in the state of Oregon to supply energy to a rapidly growing load. That needs to come to a screeching halt,” he said. “But the only way that’s going to happen is if we build more transmission.”

As a federal entity, BPA does not have to follow mandates imposed by the Oregon legislature. The agency has focused on its preference customers — publicly owned utilities that rely on it for generation — and failed to realize “they are the backbone of the transmission system in the whole Pacific Northwest,” Gamba contended.

The situation worsened in 2025 after approximately 200 employees accepted a “deferred resignation” buyout offer under President Donald Trump’s effort to slim down the federal government, according to Gamba.

BPA declined to comment for this story, but the agency has noted its efforts to build out transmission and generation.

For example, when BPA paused its transmission planning processes to deal with the 61 GW of generation in its current interconnection study, it identified 16 GW of late-stage projects that are being integrated at a rate of roughly 1 to 1.5 GW/year, with the goal of integrating the full 16 GW by 2035, according to the agency.

As for transmission, the agency secured $773.8 million in transmission capital for 2025 with the goal of doubling transmission capital execution by 2028. It plans to issue awards to contractors in March 2026 that will cover a 10-year period with a maximum value of $25 billion to build and modify lines.

BPA also launched its $5 billion Grid Expansion and Reinforcement Portfolio initiative in 2023 with the aim of building 23 new transmission lines and substation projects.

However, Gamba said BPA was “pretty nonresponsive” even before staffing cuts, adding that he doubts the agency will “start building significant new lines anytime soon.”

Instead, the Democratic lawmaker thinks Oregon should take matters into its own hands. Gamba presented a bill in 2025 aimed at creating a transmission authority (TA) and intends to revive that effort in 2026.

“We just need some entity to act like an adult in the room and actually start developing the transmission that we need,” Gamba said.

A map over BPA’s transmission assets within the Pacific Northwest | BPA

The TA would explore where transmission is needed and begin the siting and permitting process. It then would work with utilities or third parties to get lines built. The approach has found success in New Mexico and Colorado, according to Gamba.

When asked about Gamba’s initiative, Oregon Gov. Tina Kotek’s office noted that the governor issued an executive order in November 2025 aimed at streamlining transmission siting and permitting approvals.

The order recognized that “a coordinated, statewide approach to planning and designating transmission corridors is essential to long-term infrastructure development that will support economic growth and ensure clean energy can be delivered efficiently and reliably to consumers.”

The governor’s office is working with the state’s Department of Energy on developing the framework, which is expected to be completed in fall 2026 to support policy discussions next year, according to a spokesperson.

In an email to RTO Insider, JD Podlesnik, Portland General Electric’s senior director of transmission delivery, said the utility is ready to work with BPA and other regional entities to expand transmission.

Podlesnik noted that PGE has added more than 3,000 MW of clean energy and storage to the grid and recently finalized agreements for an additional 1,000 MW of clean energy resources, “making steady progress toward customer-driven clean energy targets.”

“At the same time, transmission capacity remains a key challenge across the region, both for reliability and clean energy targets,” Podlesnik said in the email. “BPA plays an important role in expanding the transmission network and accelerating the interconnection of new generation resources. Continuing to execute on BPA’s Grid Expansion and Reinforcement Portfolio is one of the critical steps in addressing those constraints.”

Washington Issues

Oregon entities are not alone in grappling with transmission constraints and compliance with clean energy laws. Washington utilities face a similar situation.

A study by Energy and Environmental Economics predicts that accelerated load growth and aging power plant retirements will create a resource gap in the Northwest starting at about 1.3 GW in 2026 and expanding to almost 9 GW by 2030. That is approximately the load of the state of Oregon.

For context, BPA’s White Book released in May 2025 projected the Northwest would have about 27.9 aMW of total (not just federal) generation available in 2026.

As is the case nationwide, data centers and electric vehicles are the primary drivers behind the expected load growth.

And just as in Oregon, Washington’s Clean Energy Transformation Act (CETA) requires all electric utilities in the state to become greenhouse gas-neutral by 2030 (allowing for use of offsets and other programs) on the way to generating all power from emissions-free resources by 2045. It also prohibits utilities from serving their Washington customers with any coal-fired generation after 2025. (See Washington Agencies Adopt New Rules to Implement CETA.)

But again, lack of transmission poses challenges for utilities to meet the law’s requirements.

There is collaboration across state lines to build more transmission independent of BPA, according to Washington Rep. Alex Ramel (D).

Washington lawmakers also seek to create a transmission authority under Senate Bill 6355.

“There is this sort of federal government monopoly in the space,” Ramel said.

Relying too much on the federal government as BPA struggles with staffing shortages “is a real concern,” according to Ramel.

“That, to me, is part of the reason why we need to be more expeditious about how we think about putting together these kinds of projects,” Ramel said in referring to a potential Washington TA. “Because if [BPA] is losing staff, that can only … impact negatively our need to be able to increase clean energy transmission opportunities.”

As for CETA, Ramel said he is not ready to “pull the plug on it.” He acknowledged the law was passed when the region did not have the same electricity use that comes with the development of AI and electric vehicles.

“I could be persuaded to have reasonable extensions or extenuating circumstances for utilities that really can’t meet those goals,” Ramel said. “But right now, I haven’t seen anything that persuades me that those goals can’t be met. We could revisit that in the future if we need to. Right now, I think we should stay full steam and let’s build out clean energy and let’s accelerate transmission.”

Puget Sound Energy, which is one of BPA’s largest transmission customers, has removed coal from its energy portfolio in accordance with CETA and is focused on providing 80% of its electricity from renewable or non-emitting resources by 2030-2033, according to Matt Steuerwalt, PSE’s vice president of external affairs.

Still, BPA’s ability to expand transmission capacity and allow new resources to come online “will have a major impact on our progress toward Washington clean energy laws,” Steuerwalt told RTO Insider.

“We also have to consider permitting and siting for energy infrastructure development undertaken by entities other than BPA, which is a major challenge to building any project,” he added. “We have been following the current legislation closely to see the extent to which it can address these and other issues.”

‘Morass of People’

But for Scott Simms, executive director of the Public Power Council, there are risks with creating separate TAs.

“I think that once you create an additional apparatus to try to do the exact same thing that other organizations are statutorily obligated to do, it’s going to create a morass of people trying to all do the same things,” Simms said.

Instead of solving the transmission challenges, the risk is that additional TAs would “exacerbate the very problem you’re trying to solve,” he added.

Rather, Oregon and Washington should fix the challenging operating environments they have created for consumer-owned and investor-owned utilities alike, Simms contended.

“There’s a variety of things on both the energy policy side with regards to resources and there are fixes on the transmission side when it comes to permitting and the planning process,” he said. “If the states were just to focus on how to best facilitate and streamline the transmission permitting and siting elements, that would be a huge help.”

Artificial intelligence has been framed by the Trump administration as ushering in a “new golden age of human flourishing, economic competitiveness and national security” for the U.S. should it win the race for computing systems that perform tasks normally requiring human intelligence.

But with the country’s drive to build up its AI ecosystem comes increased risks, both digital and physical.

Faruk Dziho, the business intelligence analyst and data solutions lead for the Texas Reliability Entity, says that while AI can strengthen grid reliability, it also creates risks if it is not managed properly.

“At the end of the day, it’s just a tool, and it’s not a replacement for engineers or operators. It excels at pattern recognition and forecasting when there is clean data,” he said during a Talk with Texas RE webinar March 10. “When it comes to some risk-mitigation strategies, there needs to be a robust data governance in building high-quality data pipelines with clear ownership, extensive validation model transparency and oversight.”

Texas RE added AI integration as a “moderate” risk in its 2024 Reliability Performance and Regional Risk Assessment, released in June 2025, saying the risks are “currently relatively unlikely to manifest themselves.”

“As AI increases in scale and integration, however, associated risks may increase in both likelihood and impact,” the regional entity wrote.

“That assessment itself is not set in stone. As adoption expands across the industry, both the probability and severity of those risks may rise,” Dziho said. “We’ll continue to monitor developments and adjust the assessments as the technology evolves.”

The Texas Interconnection grew faster than any other region in 2025, with demand increasing 5% through September when compared to the same period in 2024, according to the U.S. Energy Information Administration. The agency has said it expects demand to increase by more than 9% in 2026.

Dziho told his online audience that AI carries risks that demand robust mitigation strategies. AI-driven load growth could lead to cybersecurity vulnerabilities that can be exploited faster with AI-powered tools and systems, adaptive malicious code that bypasses security controls, and data poisoning.

“Artificial intelligence basically makes it easier for attackers to generate phishing attacks by generating thousands of personalized emails instantly or scanning for vulnerabilities faster,” he said.

Because AI systems use massive amounts of data collection and typically include confidential and/or sensitive information, data privacy controls must be effective in reducing the risk of breaches, Dziho said.

“We need to secure artificial intelligence workflows,” he said. “The field is changing constantly. There are new threats that we find out daily.”

FERC has initiated a show cause proceeding based on concerns about the lack of provisions in ISO-NE‘s tariff enabling fixes to incorrect payments to or from market participants.

The order, issued March 10, comes following multiple recent requests from participants for waivers to return improperly accrued funds to the RTO.

The commission wrote the ISO-NE tariff “appears to be unjust and unreasonable because it lacks provisions that would enable ISO-NE to return amounts that it erroneously charged to market participants and to accept payments from market participants that were erroneously or improperly received in ISO-NE’s markets.”

FERC established settlement procedures in 2024 for a waiver request by Canal Marketing to return improperly accrued funds from the RTO’s Inventoried Energy Program. The commission approved a settlement between ISO-NE and Canal in early 2025. (See FERC Establishes Settlement Procedures for ISO-NE IEP Exit Request.)

In fall 2025, Brookfield Renewable Trading and Marketing requested a waiver to refund ISO-NE for four months of improperly received capacity market revenues. FERC established settlement proceedings for this waiver request on the same date as its show cause order.

ISO-NE has 60 days to justify its existing tariff rules or explain what changes it would make if FERC requires it to make tariff changes addressing the issue.

“If ISO-NE prefers to propose revisions to the tariff on the subject of this order, then it may do so pursuant to its applicable [Federal Power Act] Section 205 filing rights,” FERC added.

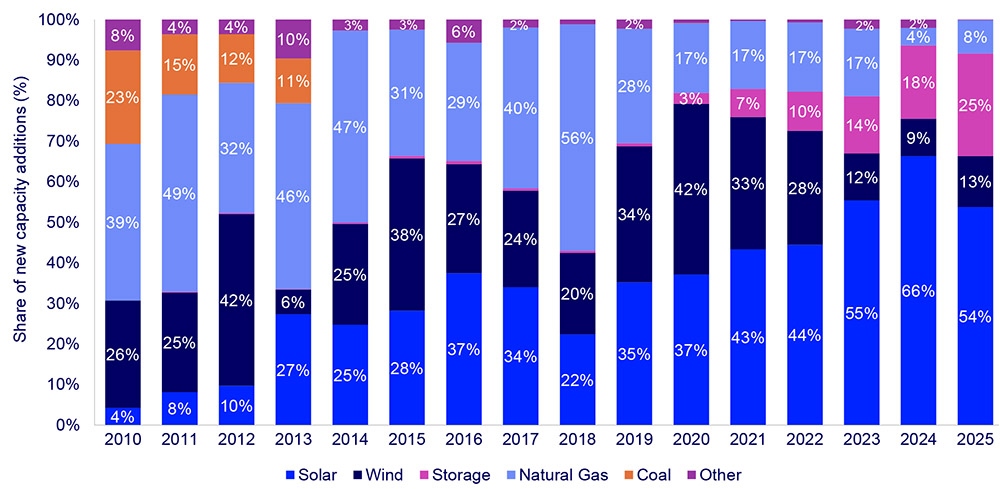

Nearly 40% fewer U.S. solar power projects reached completion in the fourth quarter than in the third quarter as developers pivoted to start new projects in time to qualify for tax credits.

But while the 43.2 GW of solar capacity installed in 2025 was 14% less than in 2024, it nevertheless made up 54% of all new capacity added to the U.S. grid in 2025, the Solar Energy Industries Association (SEIA) and Wood Mackenzie said in a new report March 10.

2025 was the fifth straight year solar was the top source of new U.S. power generation capacity.

Looking ahead, the analysis predicts nearly 500 GW of additional photovoltaic capacity will be installed nationwide through 2036, even with the headwinds created by a president hostile to renewable energy. The costs of alternatives are high enough that solar remains a value proposition even without the lucrative investment and production tax credits that are being sunsetted sooner than originally planned.

“It’s clear that solar will continue to be the dominant source of new power capacity in the United States, even as gas generation continues to grow,” said Michelle Davis, head of solar at Wood Mackenzie and lead author of the report. “Strong demand growth combined with escalating costs of new gas plants will allow solar to remain competitive, even without tax credits.”

The “U.S. Solar Market Insight 2025 Year in Review” acknowledges the many uncertainties facing solar power. The baseline prediction of 490 GW more solar capacity by 2036 could be 11% higher or lower due to a series of factors, but the projected variation for utility-scale solar (6-7%) is much less than for distributed solar (23-28%).

Distributed solar is more sensitive to changes in retail rates and cost-impacting policies such as tariffs and import guidance, the authors state, while utility-scale projects are more likely to be affected by interconnection bottlenecks, supply chain constraints and power demand growth.

Another unknown factor is President Donald Trump.

Trump’s signature on the One Big Beautiful Bill Act in July 2025 moved forward the expiration of tax credits in the Inflation Reduction Act.

Projects now must start construction before July 4, 2026, or be placed into service by Dec. 31, 2027, to qualify for full tax credits. This led to significantly fewer completed projects in 2025 than expected — the value of completing them was outweighed by the imperative of beginning work on the next projects in the pipeline in order to safe harbor their tax credits.

While the president relentlessly boosts fossil fuels over renewables, he does not show the same level of hostility to solar panels as to wind turbines. There even have been a few hints in early 2026 of solar opposition softening among some MAGA influencers.

Solar power’s growth as a U.S. power generation technology is shown. | Wood Mackenzie

Whatever the motive for this turnaround, solar has some effective selling points in 2026: It is faster and less expensive to deploy than gas or nuclear; U.S. solar component manufacturing has expanded greatly; and battery energy storage systems to smooth out its intermittent performance are proliferating in number while decreasing in price.

SEIA interim President Darren Van’t Hof indicated that while the federal uncertainty has not gone unnoticed, it is not insurmountable: “Solar and storage continue to dominate new capacity additions to the grid despite policy headwinds. American households and businesses of all sizes are demanding solar + storage because they deliver fast, affordable power to help meet rapidly rising demand,” he said.

“Washington must deliver policy certainty for the market to work and to keep pace with growing energy demands. Without this certainty, less solar will get built and Americans will pay the price with higher energy bills.”

Even with this churn, all of Wood Mackenzie’s U.S. power projections show solar constituting nearly half of all U.S. capacity additions each year through 2060.

The 2025 outlook calls for an average annual addition of 44 GW through 2036, which is an increase over previous projections based on the increase in the near-term utility-scale pipeline and continued growth in energy demand expectations.

Speakers at a SERC Reliability-hosted webinar praised the commitment by utilities and other stakeholders to address the grid’s ongoing and emerging risks but warned that their adversaries also remain inventive and committed.

“There’s this saying, ‘A rising tide lifts all boats,’” Chad Kitchens, senior lead analyst at Entergy, said at the regional entity’s 2026 Regional Risk Webinar on March 10. “It seems every year the tide is coming in higher, and we have to keep our head above water, [which] requires a greater investment in newer technologies [and] newer control measures.”

The webinar focused on risks identified in SERC’s biennial Regional Risk Report, last released in 2025 and covering the years 2024 to 2026, with a focus on extreme physical events including sabotage and attacks, and exploitation of cybersecurity vulnerabilities. (See Weather, Supply Chain Top SERC Risk Rankings.) Participants included security specialists from electric utilities, law enforcement and consulting firms.

In the first panel, Kitchens joined Jon Carstensen, utilities vertical manager at security firm IQSIGHT, and Mike Hazell, private sector coordinator for the Florida Fusion Center, an information-sharing program managed by the Florida Department of Law Enforcement, to discuss the industry’s response to physical threats. Hazell warned listeners that recent news about attempts by violent extremists to target electric infrastructure showed “the age of security through obscurity is over for us.”

“As the industry adapts and starts to invest in [security], our adversaries are also adapting, and they’re adapting to the point where they’re doing deliberate targeting,” Hazell said. “They are doing the research to understand what … a critical asset is for, not only the energy sector, but the sectors that have interdependencies with the energy sector.”

Hazell pointed to a worrying trend of extremists borrowing tactics and even motivations from each other in what he called “a salad bar approach to rhetoric and ideologies.” He said the attack in February by a New York man against a substation in Boulder City, Nev., was an example of this development.

After Dawson Maloney of Albany, N.Y., drove his rented car, loaded with weapons, through the substation fence and killed himself with a shotgun, authorities found several documents in a hotel room he rented, including military pamphlets on improvised weapons, books on magic from the 17th century and novels promoting white supremacy and terrorism. (See Police, FBI Seeking Motive in Nevada Grid Attack.)

Hazell said the incident shows the need for collaboration among utilities, law enforcement and the cybersecurity community “to outpace our adversaries” by sharing threat intelligence while protecting sensitive information that adversaries could use for their attacks.

Kitchens agreed that “we have to up our game,” suggesting that utilities consider machine learning and artificial intelligence technology to help keep up with threats. As an example, he mentioned video monitoring systems with analytic functions that can classify observed objects and notify operators to anything out of the ordinary.

“I think the biggest thing that I’m excited about is just being able to [use] those analytic and AI capabilities to filter out the noise that traditionally you get when you do that,” Kitchens said. “It’s making more efficient use of the people you have, which allows you the potential to ingest more sites into your [security operations center] and provide a larger sense of protection.”

ISO-NE has proposed to reduce its performance payment rate (PPR) by more than 60% in response to concerns that excessive penalties will have unintended consequences for the capacity market.

Capacity resources in New England have incurred significant performance penalties during scarcity events over the past two years. These penalties have been particularly consequential for slower-start fossil units. Over two events in 2024, net penalties for combined cycle gas and oil generators totaled $44.3 million, while penalties for steam turbine residual-oil units totaled $25.8 million.

Some participants have argued the risk of these penalties could drive up capacity prices in future auctions and push resources out of the market.

The performance rate determines penalties and credits during scarcity events. The RTO’s Pay-for-Performance (PFP) construct is designed to insulate ratepayers, with underperforming resources paying for the incentives for overperforming resources.

The RTO’s per-megawatt-hour performance rate has grown in recent years, increasing from $2,000 to $3,500 in 2021, to $5,455 in 2024, and to $9,337 in 2025.

ISO-NE announced at the NEPOOL Markets Committee meeting March 10 that it plans to cut the rate back to $3,500. It also plans to move forward on an expedited schedule to implement the changes as quickly as possible, targeting a technical committee vote in May.

“Some resources may find the increased PPR, and the volatility associated with it, makes the risks and potential costs of selling capacity too high,” said Chris Geissler, director of economic analysis at ISO-NE. “This could result in retirements from resources that can still make meaningful contributions to system reliability.”

He added that a high performance rate increases the risk that individual resources hit their stop-loss limits, which cap the total penalties each resource can accrue per month. When resources hit this limit, ISO-NE charges unrecovered penalties to all capacity resources that have not hit the stop-loss limit.

The reduced PPR still should provide adequate incentives for performance, Geissler said, estimating that incentives from PFP and elevated energy market prices likely would total around $6,000/MWh.

“History suggests that resources make investments and perform strongly at this rate,” he said.

Stakeholders generally reacted favorably to the proposal, while some expressed concern that a $3,500 rate may be too low to adequately incent performance during scarcity conditions.

Treatment of Exports

Also at the MC meeting, ISO-NE detailed its plans to subject certain exports to the performance rate.

This change, recommended by both of the RTO’s market monitors, is intended to prevent a market loophole that could allow participants to earn performance credits without sending any power.

Under the current rules, during a capacity scarcity event, if a participant schedules exports that equal imports scheduled by a different participant, the export would not be charged performance penalties, but the import would earn performance credits.

“These two transactions collectively result in no power flowing but do not net in settlement because they are submitted by different market participants,” said Enrico De Magistris, economist at ISO-NE. “The market participants could transact outside the ISO-NE system to share the PFP credits.”

He noted that ISO-NE is not aware of any instances in which a participant has exploited this loophole.

To fix the issue, the RTO proposes to charge the performance rate during scarcity conditions to all exports “not associated with a specific generator in the ISO-NE system.”

Unlike “system-backed exports,” exports associated with a specific generator would not be charged the performance rate. These exports would reduce the amount of performance revenues the associated generator could earn or subject it to performance penalties for not meeting its capacity supply obligation (CSO).

De Magistris said ISO-NE likely will remove system-backed exports from the calculation of its balancing ratio, which it uses to determine capacity resources’ obligations during scarcity events.

ISO-NE calculates the systemwide balancing ratio by dividing load and reserve requirements by total CSO. System-backed exports are currently included in the calculation as load, while generator-backed exports are excluded.

Balancing Ratio Cap

ISO-NE also discussed its proposal to cap the PPR balancing ratio in compliance with an order issued by FERC in January.

In designing the tariff changes, ISO-NE has tried to “keep the ‘effective’ payment rate for overperformance as close to the tariff-specified [PPR] as possible,” said Megan Sweitzer, lead analyst at ISO-NE.

Under the proposal, if the cap on the balancing ratio leads to the under-collection of performance charges, this deficit would cut into the performance credits allocated to overperforming resources.

“This change ensures resources performing at their CSO megawattage are not charged” and “lowers the ‘effective’ PPR for overperformance when a deficiency exists,” Sweitzer said.

Notably, the treatment of deficits caused by the balancing ratio cap would differ from the treatment of deficiencies caused by the stop-loss mechanism, which will still be charged to all capacity resources.

While NEPGA argued against ISO-NE’s allocation of stopped losses in its complaint, FERC sided with ISO-NE’s argument that the stop-loss mechanism benefits all capacity resources and therefore it is fair to charge capacity resources for the costs of its implementation.

Duke Energy has entered a pair of settlements in North and South Carolina on its proposal to combine Duke Energy Carolinas and Duke Energy Progress, which still needs approval from both states’ regulators.

The deal before the North Carolina Utilities Commission was filed in late February and signed by North Carolina Public Staff, the North Carolina Attorney General’s Office, Google, Nucor, Walmart and others.

“We’re pleased that public staff and the attorney general’s office agree our customers will see significant future cost savings and other meaningful benefits from combining our two utilities,” Duke Energy North Carolina President Kendal Bowman said in a statement on March 10. “It reduces customer costs, simplifies operations, promotes regulatory efficiencies and supports economic growth across the Carolinas.”

The deal pending before the Public Service Commission of South Carolina was filed on March 6 and was endorsed by the state’s Office of Regulatory Staff, Nucor, Walmart, Vote Solar, the Sierra Club and others.

“Our engagement has been laser-focused on consumer protections and affordability for South Carolina families and small businesses, and one of the best ways to do that is by investing in alternatives to building new costly and polluting resources,” Sierra Club’s Paul Black said in a statement. “Duke’s regulators at the Public Service Commission must turn their attention to establishing strong consumer protections that require tech companies, not families, to pay for all of the energy and infrastructure costs for new data centers, and the Sierra Club has laid the groundwork to make that happen.”

Duke Energy Carolinas owns 20.8 GW of generation and serves 2.9 million customers across a 24,000-square-mile territory, while Duke Energy Progress owns 13.8 GW to supply 1.8 million customers across a 28,000-square-mile territory.

The filings with both states include commitments from the utility to save hundreds of millions of dollars through lower production costs from more efficient operations and lower capital costs from more efficient planning.