The Supreme Court on Oct. 16 turned down industry and state efforts to slap a stay on the U.S. Environmental Protection Agency’s new rules aimed at cutting carbon emissions at U.S. power plants burning fossil fuels. But the court left the door open for a second attempt pending a decision on the cases from the Court of Appeals for the D.C. Circuit.

Under the final rule EPA released April 24, existing coal-fired power plants nationwide will have to either close by 2039 or use carbon capture and storage or other technologies to capture 90% of their emissions by 2032. New natural gas plants will have until 2035 to similarly cut their emissions through efficient design, carbon capture or a combination of both. (See EPA Power Plant Rules Squeeze Coal Plants; Existing Gas Plants Exempt.)

The brief decision from Justice Brett Kavanaugh responded to a slate of eight cases against the EPA now before the D.C. Circuit, including two separate state challenges: one led by West Virginia, one led by Ohio. Suits also have been filed by the National Rural Electric Cooperative Association, the National Mining Association, NACCO Natural Resources Corp., the Midwest Ozone Group, Electric Generators for a Sensible Transition and the Edison Electric Institute.

With Justice Neil Gorsuch concurring, Kavanaugh said that while the plaintiffs “have shown a strong likelihood of success on the merits as to at least some of their challenges” to the EPA rule, work on complying with the rule would not have to begin until June 2025.

The plaintiffs “are unlikely to suffer irreparable harm before the Court of Appeals for the D.C. Circuit decides the merits,” Kavanaugh said. “Given that the D.C. Circuit is proceeding with dispatch, it should resolve the case it its current term.”

Either the plaintiffs or EPA then could appeal to the Supreme Court, he said.

The decision notes that Justice Clarence Thomas would have granted a stay, while Justice Samuel Alito “took no part in the consideration or decision of these applications.”

The mixed decision got a quick reaction from Michelle Bloodworth, CEO of America’s Power, the coal industry’s trade association, who expressed disappointment that the court did not stay the rule, but also pointed to Kavanaugh’s belief that at least some of the state and industry arguments had merit.

“We have long stated that … EPA’s carbon rule is an illegal overreach of the agency’s authority and would undermine the reliability of our nation’s electrical grid,” Bloodworth said. “By forcing the premature retirement of coal plants, the EPA would reduce needed sources of electricity at the same time electricity demand is exploding. Coal-based electricity is essential to ensuring the United States can develop and deploy artificial intelligence and not fall behind other nations like China.”

The California Energy Commission is offering $43 million in grants to fund waterfront facility improvements to support the development and operation of floating offshore wind energy off the state’s coast.

Eli Harland, energy policy expert and planner at CEC, gave an overview of the solicitation and how to apply during an Oct. 16 workshop.

“The purpose of the GFO [grant funding opportunity] is to fund projects that will plan for offshore wind energy infrastructure improvements that can advance the capabilities of California waterfront facilities, ports or harbors to support the development and operation of floating offshore wind projects,” Harland said.

The solicitation implements provisions of Assembly Bill 209, otherwise known as the Energy and Climate Change Budget bill, that requires the commission to implement a variety of clean energy programs, including the Offshore Wind Waterfront Facility Improvement Program. CEC will obtain the funds in June 2025 and make them available to selected grant applicants by June 2029.

The Waterfront Facility Improvement Program was established in recognition that ports will be crucial to all aspects of the development and operation of floating offshore wind projects, including manufacture of parts such as blades, assembly and transport of turbines, and the operations and maintenance of final products.

The solicitation required by AB 209 works in tandem with several other policy efforts aimed at advancing West Coast wind projects, including AB 525, which directed the CEC to develop a strategic plan outlining offshore wind development. The report was approved in July and includes a chapter covering efforts to improve ports and waterfront facilities.

According to the plan, California’s existing port infrastructure is insufficient to support the offshore wind industry. Individual wind turbines are likely to be anywhere from 12 MW to 25 MW each and can only be transported over water, making staging and integration port sites where turbines are assembled essential.

It also emphasizes that “no single port site in California can support all the needs of the offshore wind energy. Instead, multiple ports will be needed and … [upward] of 16 large and 10 small port sites [could be needed] to support offshore wind development over the next decade or more.”

The CEC will fund offshore wind infrastructure improvements at waterfront facilities in two investment categories. Category 1 covers activities that support developing individual or regional retrofit concepts and investment plans. Category 2 includes activities that support final design, engineering, environmental studies and review, and construction of retrofits.

Up to $6.75 million will be available for grants for Category 1, with projects eligible to receive a minimum of $750,000 and a maximum of $2 million. Up to $36 million is available in Category 2, with a project minimum of $9 million for each project and a maximum of $27 million. Eligible applicants include port authorities, operators and commissioners and California waterfront facilities and partners. Applicants in both categories must demonstrate site control.

Funding, Site Control Concerns

While commenters during the call largely expressed approval of the program, some industry experts weren’t happy with the way the funding was split between categories.

“We would like to see some additional funding allocated to Category 1 activities, in addition to increasing the overall award size for category one activities from the $2 million cap. That’s really not a lot of money,” said Artie Mandel, director of strategic initiatives at the Port of Los Angeles. “This program is a really unique opportunity for all of the California ports to support the statewide strategy and build out a California supply chain, and we really need to make sure that there’s enough resources there to support all of the ports in undergoing their planning efforts.”

Other meeting participants echoed the request for increasing Category 1 funding.

Jason Cotrell, founder and CEO of Sperra, a company that designs and manufactures offshore wind infrastructure, expressed concern about the Category 1 site control requirement.

“The site control really puts the cart before the horse. I think one thing that we can agree on is that floating offshore wind is very early in terms of supply chain and technology developments, and it will consistently change over the next decade before it’s deployed in California,” Cotrell said. “We really think that site control in Category 1 is an unnecessary requirement that potentially restricts and will discourage participants from participating in Category 1.”

The deadline to submit applications is Nov. 22, and the notice of proposed awards will be announced in December. The anticipated start time for the project agreements is April 2025.

A recently filed proposal by ISO-NE to increase the collateral requirements for generators with capacity supply obligations (CSOs) has received strong pushback from the New England Power Generators Association (NEPGA), which argued to FERC on Oct. 9 that the proposal would violate the filed rate doctrine (ER24-3071).

The policy changes are intended to reduce risks to the market of generators defaulting on pay-for-performance changes, which are accrued if a generator can’t meet its obligations during a capacity scarcity event.

“There is a significant risk to the New England Markets caused by the fact that many [forward capacity market] participants do not have adequate corporate liquidity to satisfy their contractual, financial obligations related to the CSOs they were awarded,” ISO-NE said.

The RTO filed three updates to the policy last year, which were all accepted by FERC. However, the last set of changes have proven controversial and faced significant pushback in the NEPOOL stakeholder process. Neither ISO-NE’s proposal, nor two amendments proposed by NEPGA, passed the two-thirds approval threshold required for NEPOOL support. (See NEPOOL Participants Committee Votes to Support Hourly GIS Tracking.)

ISO-NE is proposing to introduce a new corporate liquidity assessment that would assign each participant a risk level to determine the collateral requirements. The RTO projects the changes would increase market-wide financial assurance costs by $72 million to $90 million for the 2025/2026 capacity commitment period (CCP).

In response, NEPGA protested the effective date of the proposal but not the underlying changes. The association argued that the changes should not apply to existing capacity commitments and should instead take effect for the 2028/2029 CCP. The auction for this CCP will likely take place in early 2028, depending on the results of ISO-NE’s ongoing capacity auction reform project.

“The [financial assurance policy] changes, if applied beginning on June 1, 2025, as ISO-NE requests, would alter the legal requirements associated with capacity supply obligations assumed years ago in violation of the filed rate doctrine,” NEPGA wrote.

The filed rate doctrine prohibits retroactive changes to rates that have been approved. NEPGA argued that ISO-NE’s proposal would add costs for generators with capacity commitments which were not accounted for in the auction bids.

“Denying the opportunity to reflect the full cost of providing capacity by post facto changing the rules governing the costs of holding a CSO, is not just wrong from a policy standpoint, but could contribute to accelerated retirements,” NEPGA said.

“With announced retirements in New England already outpacing new entry over the coming years, exacerbating this mismatch undermines confidence in the market and consequently risks reliability and the resource adequacy of the region,” the group added.

NEPGA requested that if FERC accepts the changes, it should either direct ISO-NE to adopt a June 1, 2028, effective date or schedule a hearing to determine an adequate effective date.

ISO-NE argued its proposal “does not constitute a retroactive rate change” because the changes would not affect auction prices or capacity supply obligations.

It added that the changes are prospective, not retroactive, because they would take effect in June 2025 and would “not alter prior credit reviews or supplant previously calculated inputs into the formula for the [forward capacity market] delivery financial assurance requirement.”

ARLINGTON, Va. ― FERC Order 1920 eventually may provide a structure for long-term, interregional transmission planning, but the anticipated yearslong implementation of the rule could mean states will have to lead in planning for their nearer-term transmission needs, according to a new report from the American Council on Renewable Energy and The Brattle Group.

Rolled out at ACORE’s recent Grid Forum, the report focuses primarily on PJM’s Mid-Atlantic states, which are developing transmission for offshore wind and other renewables. New Jersey’s state agreement approach (SAA) ― in which the state’s Board of Public Utilities has partnered with PJM on project solicitations ― is seen as a model that could cut costs and interconnection times.

Brattle’s Joe DeLosa III laid out seven options states might pursue, ranging from following New Jersey’s lead with a single-state SAA with a single “driver” ― such as meeting state goals for offshore wind deployment ― to waiting for implementation of 1920.

Other SAA options include a single state agreement covering multiple drivers ― say, reliability and a renewable energy target ― and multiple states with single or multiple drivers. Outside of SAAs or 1920, the report looks at “voluntary solicitations” involving either single or multiple PJM states or interregional, multistate efforts, for example, bringing in New York or New England states.

“Building offshore wind at scale in the next decade is essential to meeting electricity demand in a clean and reliable manner, but transmission planning must start today,” said Evan Vaughan, executive director of MAREC Action, in an ACORE press release announcing the report. States must “set their own direction on transmission planning to address multiple needs — reliability, economic growth, clean energy deployment, extreme weather resilience — in the most efficient way possible.”

MAREC Action is an advocacy group representing utility-scale renewable energy developers in the Mid-Atlantic and Appalachia.

ACORE CEO Ray Long agreed that “time is of the essence, and our report lays out the opportunities for states to maximize the benefits of proactive planning, particularly for offshore wind.”

RTO Insider did offer PJM the opportunity to comment on the report, but a spokesperson said the RTO still was reviewing it and would “defer comment at this time.”

The SAA Options

The report sees state leadership as filling a critical gap in PJM’s planning processes.

“Despite recent stakeholder efforts, PJM’s transmission planning process has not yet evolved to the point where it is cost-effectively meeting multiple system needs, including the public policy goals of PJM states. This would require a more proactive and holistic planning approach,” the report says.

Brattle’s analysis of benefits of each approach comes down squarely on going with an SAA, which DeLosa said provides more flexibility. “We just recommend that if a state or states within PJM seek to lead transmission procurement, it makes a lot more sense for them to use the tariff structure and the experience of New Jersey and go with the SAA.”

To date, New Jersey has completed one solicitation under its SAA with PJM, awarding onshore transmission projects, but put a second solicitation on hold this year, according to a recent update from PJM.

Maryland’s Promoting Offshore Wind Energy Resources Act (SB 781), passed in 2023, required the state’s Public Service Commission (PSC) to ask PJM for an analysis of the transmission upgrades that might be needed for offshore and onshore wind. Meetings between PJM, the PSC and other state agencies are ongoing.

At the same time, the PSC has been talking with New Jersey and Delaware about the possibility of regional collaboration on transmission planning. But according to a recent report from the commission, each of the three states is at a different stage of analyzing and considering their options, making collaboration unfeasible.

DeLosa also sees potential for interregional planning between PJM and non-PJM states. “We believe it could be well utilized for targeted procurements, even over a broad geographic scope,” he said. “We envision so-called ‘low-hanging fruit’ projects … that are either well-known or somewhat advanced in their development that would kind of evidently provide benefits.

“If sufficiently targeted, we also believe a cost-allocation approach, which could be a key underlying element of this, could be developed [and] limited to particular projects and the associated benefits case.”

A major caveat for any of these approaches is the “leadership role that is required of the states, the ongoing project management responsibilities for the projects that have been selected,” he said. “They persist over a long period of time, and they don’t go away. … There needs to be some method of supporting the states so that they can actually meet the needs, the leadership needs … under some of these frameworks.”

FERC received dozens of comments on its advanced notice of proposed rulemaking (ANOPR) that would require broad use of dynamic line ratings across the U.S. transmission grid.

The ANOPR (RM24-6) proposes to require utilities to monitor hourly solar and wind conditions and a requirement to enhance data around transmission congestion outside of organized markets to see where DLRs might be cost effective. (See FERC ANOPR Seeks to Move the Ball Forward on Dynamic Line Ratings.)

Many utilities urged FERC to be cautious in mandating specific and additional requirements around DLRs, as the industry is still working to implement Order 881 on ambient adjusted ratings (AARs), which Edison Electric Institute noted comes with a July 2025 deadline. FERC also recently required transmission planners to consider DLRs as part of their compliance with Order 1920.

“EEI members are committed to deploying DLRs and other grid-enhancing technologies (GETs) where they are proven to be cost-effective and produce identifiable benefits for customers,” the investor-owned utility trade group said. “Where EEI members have implemented DLRs, they have been deliberate in their analysis and careful to ensure that costs do not outweigh benefits.”

The value of DLRs will depend on the accuracy and transparency of the line ratings used in AARs, but the industry lacks that benchmark since Order 881 has yet to go into effect, EEI said. FERC should allow some time for the industry to be comfortable with AARs because complying with two mandates at once would create overlapping deadlines, bottlenecks with limited vendors in the space, and tax utility employees working in the space, EEI said.

While the use of DLRs on the American grid has been largely at a pilot level, other commenters noted that the pilots have so far tended to show promise, and many European grids use the technology much more widely already. A group of clean energy trade associations — the Working for Advanced Transmission Technologies (WATT) Coalition, American Clean Power Association, Advanced Energy United and others — say that DLRs can help the industry deal with its most pressing problems.

“It is imperative that FERC act quickly to proceed to a Notice of Proposed Rulemaking (NOPR) and then a final rule requiring DLR under appropriate circumstances,” they said. “The urgent need for more transmission capacity is even clearer now than when FERC opened its Notice of Inquiry into the Implementation of Dynamic Line Ratings in 2022.”

DLRs would help to address lengthening interconnection queues, growing demand and the need to expand the transmission grid. Expanding the grid means shutting down parts of it as new transmission comes online, and DLRs can mitigate side effects there, the clean energy trade groups said.

“Utilities should use all cost-effective approaches to reduce the impacts of unforced and forced outages on ratepayers and markets,” they said. “Congestion and curtailment due to transmission outages should be straightforward to predict and calculate in production cost modeling (which should also be performed outside of RTOs), so an evaluation of GETs to address those outages should also be straightforward.”

A more exhaustive review of the 60-plus comments in the docket will be published in the coming days.

Dominion Energy’s 2024 Integrated Resource Plan, filed Oct. 15 with Virginia and North Carolina regulators, calls for major expansions of offshore wind, solar power and natural gas to meet surging demand in its territory.

The document lays out multiple portfolios to meet that rising demand through significant investments in new power generation, upgrades to the power grid, energy storage and efficiency. It does not seek approval for specific projects, but offers a long-term plan based on current technology, market information and load projections.

“We are experiencing the largest growth in power demand since the years following World War II,” Dominion Energy Virginia President Ed Baine said in a statement. “No single energy source, grid solution or energy efficiency program will reliably serve the growing needs of our customers. We need an ‘all-of-the-above’ approach, and we are developing innovative solutions to ensure we deliver for our customers.”

The IRP included bill forecasts for Dominion’s residential customers in Virginia, who now spend $142.77 a month for 1,000 kWh and could see their bills grow by between $72.85 and $161.13 by 2035.

Power demand is expected to grow 5.5% annually for the next 10 years and to double by 2039, according to a forecast by PJM, Dominion said.

Just under 80% of the plan’s proposed new generation over the next 15 years is carbon-free, including 3,400 MW of new offshore wind on top of the 2,600-MW Coastal Virginia Offshore Wind (CVOW), 12,000 MW of new solar, 4,500 MW of new battery storage and small modular reactors starting in the mid-2030s.

The CVOW project is proceeding on time and on budget, and Dominion has secured offshore leases nearby to build additional power plants. Those include 176,505 acres off Virginia Beach that could support 2.1 GW to 4 GW of wind power and an additional 38,964 acres off North Carolina that could support up to 800 MW.

The utility asked the Virginia State Corporation Commission in a separate filing to approve 1,000 MW of additional solar, which would bring its fleet to 5,750 MW in the state.

The remaining 20% of the plan’s power generation would come from natural gas, which Dominion said was a “critically important source of back-up power” to keep the lights on when wind and solar plants are not producing energy.

“Winter Storm Elliott showed the need for every generating unit in the company’s fleet to be dispatched to meet the system peak early in the morning when renewable resources were not producing energy,” the IRP said. “This type of extreme weather event threatens reliability and requires resources to ensure the company can meet customer demands.”

The company is modeling additional combustion turbines, which would function as quick-dispatch, balancing resources and combined cycle units that would operate more often, the IRP said.

The proposal to expand coal, which could mean nearly 6 GW of new fossil-fired power plants, drew opposition from some clean energy interests and environmentalists. Advanced Energy United noted that the Virginia Clean Economy Act requires the state to move to renewable energy and a fully clean grid by 2050.

“Dominion Energy’s latest IRP is a step in the wrong direction,” AEU’s Shawn Kelly said in a statement. “Instead of harnessing the potential of advanced energy to more reliably and cost-effectively meet Virginia’s growing energy needs and clean energy goals, this plan threatens to keep the state dependent on fossil fuels for decades. Dominion is missing a critical opportunity to lead Virginia’s clean energy transition, protect households and businesses from rising costs, and provide more resilient clean energy solutions for all Virginians.”

All four of the plans filed with the SCC would increase emissions, said the group Clean Virginia, which called for the IRP to be rejected.

“Dominion’s latest energy plan blatantly disregards the financial well-being and health of Virginia families,” Clean Virginia Deputy Director of Energy and Operations Kate Asquith said in a statement. “By continuing to invest in gas-burning facilities, Dominion is not just raising bills — it’s locking Virginians into a future of higher costs and greater pollution. This is unacceptable at a time when we need to be transitioning to clean, affordable energy.”

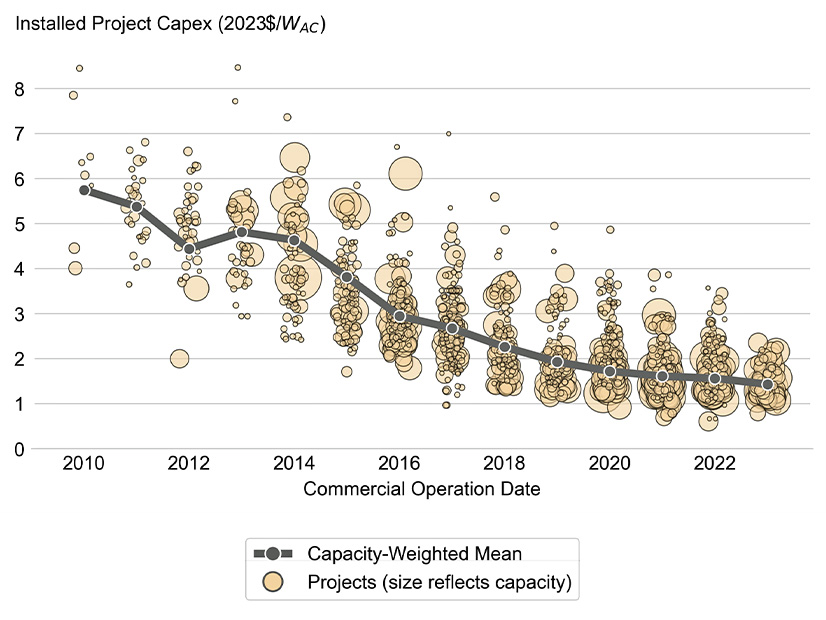

Utility-scale solar construction reached record levels across the United States in 2023 and its cost continued to decline, the Berkeley Lab announced in this year’s edition of its annual report on the sector.

A total of 18.5 GWAC of large-scale solar was brought online last year, bringing total installed capacity to 80.2 GWAC in 47 states, the report says, while capacity-weighted average installed costs decreased 8% to $1.43 per watt AC.

The levelized cost of electricity from these utility-scale photovoltaic systems rose slightly to $46/MWh, not counting tax credits, but decreased slightly to $31/MWh once the federal incentives were factored in.

For the first time ever, more than half of new grid capacity nationwide was solar — 17% distributed and 35% utility-scale.

The report predicts that 2024 will be another record year, with more than 35 GW of utility-scale solar and distributed commercial or residential solar installed.

A whopping 1.09 TW of utility-scale solar is stacked up in the nation’s interconnection queues, but historically, only 10% of requests ever advance to construction, the Lawrence Berkeley National Laboratory noted as it announced the new report Oct. 15.

Capital costs of building utility-scale solar generation have steadily decreased over the past decade, as measured by cost per output. | Lawrence Berkeley National Laboratory

The 2023 report and its executive summary drill down on the state of the utility-scale solar sector. Among the details, data points and conclusions:

Average energy and capacity value nationwide was $45/MWh; average market value ranged from $27 MWh in CAISO, where solar has the largest market share, to $67/MWh in ERCOT, where summer heat waves and record electricity demand were seen during peak solar production hours.

Only 4% of utility-scale PV capacity added in 2023 was installed on a fixed-tilt mount; the rest used single-axis tracking. Fixed-tilt is relegated mainly to challenging sites and least sunny regions of the Northeast; tracking mounts add 20 cents per watt to the cost on average but can boost capacity significantly in sunny regions.

Projects larger than 50 MW cost 13% less per megawatt on average than their counterparts rated at 5 MW to 50 MW.

Plant output still declines with age, but more recent projects are showing a slower decline than earlier projects did at the same points in their lifespans.

Projects in the regions with the lowest solar insolation have the highest levelized cost of electricity — ISO-NE and NYISO were $76 and $78/MWh, respectively — while the sun-rich ERCOT, CAISO and non-ISO West ranged from $37 to $42. (Project costs and size contributed to this disparity.)

Solar power purchase agreements have largely closed the gap with onshore wind PPAs — both were much more expensive 15 years ago, but solar PPA prices have declined more sharply than wind. Lower natural gas prices, meanwhile, have given existing combined-cycle gas-fired generators a near-term cost advantage over solar.

Concentrating solar thermal power has been lagging, with no U.S. installations since 2015. The newest of the existing installations have underperformed expectations.

With the recent completion of the first phase of the New Jersey Wind Port, the state’s offshore wind sector looks to take a key role in the East Coast turbine industry despite the closure of the state’s two most advanced projects, speakers said at the state’s annual OSW conference.

A year after Ørsted stunned state officials and abandoned the state’s first two offshore wind projects, New Jersey has adapted to changing circumstances and developers are better prepared to weather the still difficult environment, speakers said at the Time for Turbines conference Oct. 11 in Atlantic City.

Atlantic Shores Offshore Wind, now the most advanced project in the portfolio approved by the New Jersey Board of Public Utilities (BPU), is moving ahead with its previously approved project, Atlantic Shores South 1, and a second one, Atlantic Shores South 2, Joris Veldhoven, the developer’s CEO, told attendees.

The Bureau of Ocean Energy Management (BOEM) on Oct. 1 approved the two projects’ construction and operations plan. And the company is close to awarding the last contracts and subcontracts for the first project, he said.

Veldhoven, in what emerged as a central theme among conference speakers, cited developers’ need to secure a strong supply chain pipeline, and the state’s ability to provide it, as key factors in their ability to move projects to completion, and for the sector to advance.

“In the current market, it is so critical that we locate these packages,” Veldhoven said. “Having that maturity, having the certainty that the supply chain is for you, is absolutely critical.”

In some respects, the state’s OSW sector is better able to get projects done than in the past, because developers such as Atlantic Shores are “more aware of the supply chain risk,” he said.

Likewise, regulators have recognized — and adapted to — the financial pressures that developers can face, among them the rise in interest rates, he said.

“What regulators have done over the last few years, and kudos to them, here in New Jersey and other states, there’s now a bit more of these inflation adjustment mechanisms that take into account various factors, and they started to even take into account cost of money,” he said. “Is that perfect? No, it’s not. But it shares some of the risk.”

‘Miracle’ Port Advance

Tim Sullivan, CEO of the New Jersey Economic Development Authority, which oversees port construction and funds much of the state’s OSW initiatives, said completion of the first phase of the wind port shows the state is a serious player in the East Coast wind sector.

The fact the first phase of the project came in “on time and under budget,” he said, is “close to a damn miracle.”

Other state competitive strengths include a “steady diet” of new project procurements, a “real commitment” from Gov. Phil Murphy (D) and — in the EEW monopile factory in Paulsboro — the only manufacturing facility that’s active in the U.S. for offshore wind components.

“Despite having fallen behind on the generation side a bit, we’re going to catch up,” Sullivan said. “We are still in the best position long term, and we are investing for the long term. … This is not a one-, two-, three-, four-, five-year ambition. This is a 50-year ambition. A century-long ambition.”

Murphy has set a goal for the state to have 11 GW of OSW capacity by 2040. Atlantic Shores is one of three companies awaiting the BPU’s decision in the state’s fourth offshore wind solicitation, which is expected by the end of 2024. The state is preparing to launch a fifth solicitation in early 2025. (See 3 OSW Proposals Submitted to NJ.)

The BPU approved Ørsted’s Ocean Wind 1 in the first solicitation in 2019 and the developer’s Ocean Wind 2 in the second solicitation in 2021, in which the 1,510-MW first part of Atlantic Shores also was approved. The BPU backed two projects — the 1,342 MW Attentive Energy Two and Leading Light Wind, with two phases of 1,200 MW each — in the third phase and is expected to announce the designated projects in the fourth solicitation by the end of 2024.

That fourth solicitation allowed developers awarded contracts in the first or second procurement — of which Atlantic Shores is the only remaining project — to submit a rebid that would enable them to adjust for rising costs. Atlantic Shores took that opportunity and also submitted the second half of the project, Atlantic Shores South 2.

The other applicants awaiting the BPU’s decision are Attentive Energy, with a second project, and Community Offshore Wind, for a 1,300-MW project.

Supply Chain Building

Yet the sector still is challenging, as shown by the difficulty Leading Light Wind has experienced in finding an economically viable turbine. On Sept. 25, the BPU approved a request by developer Invenergy to delay the project by three months because none of the three turbine manufacturers initially selected by the developer — GE Vernova, Siemens Gamesa Renewable Energy or Vestas — are able to supply suitable new turbines.

Abby Watson, president of The Groundwire Group | Christian Fiore

Some projects are moving to mitigate risk and create key elements of their own supply chain, conference speakers noted.

Attentive Energy, which hopes to begin construction in two to three years and complete the project by 2031, is vying for space in the wind port, said Karen Imas, the company’s senior external affairs manager. If Attentive’s bid is successful, the company plans to execute project marshaling and work with a manufacturer to build a factory there, she said.

Attentive also has committed $58.85 million into the third phase of EEW’s Paulsboro factory building monopiles, part of the foundations of offshore turbines, Imas said in an interview with NetZero Insider after her panel.

The arrival of Attentive and other developers in a second OSW wave may make them better placed to handle future challenges, she said.

“We are able to maybe anticipate a little bit more supply chain, timelines, projections,” she said. “We bid in with a certain price that we think is realistic today, and you know, maybe that sets us up with a little more stability than those awarded two, three years ago.”

Mitigating Risk

Imas pointed to the developer’s recent partnership with the New Jersey Manufacturing Extension on a policy paper published in October analyzing the readiness of the state’s manufacturing sector to adapt to the needs of the offshore wind sector. The extension interviewed 18 manufacturers about their capacity and interest in shifting gears.

The study found the companies can “pivot and provide some of the materials, the widgets, the products that would be needed for the larger Tier One, Tier Two manufacturers,” she said. Yet the study also found that 66% of the companies interviewed would require “targeted funding for process or technology upgrades” to take part in the sector.

“They need some technical assistance,” she said. “They may need increased staffing. They may need some special certifications and trainings. And that pivot will take some work. So we as a developer are taking note of this survey and what’s been reported, because we want to work hand in hand with these companies and really help arm them with the tools they need to participate.”

Those kinds of supply chain challenges are enhanced by the steady advance of a wave of OSW projects from different states all moving head and seeking the same resources, said Abby Watson, president of The Groundwire Group, a consultancy that focuses on sustainable energy.

“We have a lot of projects now that are all looking at building within a fairly short period of a couple of years,” Watson said, speaking on a panel entitled “Navigating Choppy Financial Waters.” “And that is an incredibly challenging commercial environment in which to build a successful business case for a manufacturing facility that’s going to be viable in the long term.

“I think we’re seeing that in some of the ways that different states are kind of redesigning some of their procurements to emphasize viability” and looking for ways to “de-risk that project.”

NYISO on Oct. 16 presented its updated modeling for combined-cycle gas turbines that employ duct firing to produce additional electricity and advanced a motion to recommend that the Management Committee revise the tariff in accordance with the model.

Stakeholders were unhappy that NYISO did not factor multiple “ramp rates” into its model, which they fear could result in improperly applied penalties for over- or under-generating in response to dispatch. NYISO had included multiple ramp rates in its original considerations but dropped them during model development.

“Generators should not have to waste a lot of time and expense fighting an improperly applied penalty that results from … NYISO not recognizing the ramp rate that a generator has already given the ISO,” said stakeholder representative Mark Younger of Hudson Energy Economics.

“Let me be clear upfront: I have no assurances that resources that are dispatched in their duct from a less-than-feasible ramp rate reflection will not be subject to penalties,” said Shaun Johnson, director of market design for NYISO. “I will point out that there are some wrappers around those penalties that make it less likely.”

“I totally agree it’s less likely,” Younger said. “The problem I’m having is that it’s totally inappropriate if it ever happens.”

When the motion was raised, the New York Power Authority seconded but encouraged NYISO to figure out a way to satisfy the concerns. Younger voted in opposition, noting that the dropped multiple ramp rates was effectively “moving the goalposts” to say the project had been completed, when it hadn’t.

East Coast Power and two other stakeholders abstained from the vote. The overall motion passed with a “vote by exception.”

Background

NYISO has been working since 2022 to improve modeling it uses to better accommodate combined-cycle gas turbine generators equipped with duct firing. Current models don’t account for the additional power generated by plants that use the technology.

Combined-cycle gas turbines burn gas to spin combustion turbines. Exhaust gas is directed to a heat recovery steam generator to pressurize steam and generate power in a steam turbine. Plants with duct burners may burn additional fuel to heat the exhaust gas, which can help maintain the generation of the heat recovery steam generator.

In 2020, according to the U.S. Energy Information Administration, about 75% of the U.S. combined cycle plant capacity used duct burners. In New York, about 79% of the power generated from natural gas plants came from plants with duct burners.

Johnson said the tariff revisions represented an incremental improvement in the way NYISO models ramp rates for duct firing combined-cycle plants.

“It doesn’t address all scenarios, and we need to keep working on that,” Johnson said. “I understand your frustration that not all scenarios were fixed, but this is an improvement, and we want to proceed forward with the incremental improvement where we continue to work on future improvements.”

Clarification: A previous version of this article mentioned JERA Americas as abstaining from the vote. Marie Pieniazek, director of regulatory affairs for JERA Americas, said she was voting for East Coast Power, which is a NYISO market participant. JERA Americas is not a NYISO market participant.

CARMEL, Ind. — MISO maintains that a member request to create a multiday gas purchase requirement for use during extreme cold is unnecessary but offered financial assurances for resources whose commitments are canceled.

MISO’s Jason Howard said instead of a multiday fuel purchase requirement for market participants, MISO wants to develop two new financial guarantees to resources committed days in advance of upcoming grid situations.

The first would be a canceled startup cost provision, where a resource would be guaranteed a portion of startup costs depending on when MISO cancels within the startup window. The second would be an “as-committed/as-dispatched” lesser of settlements rule, which would move multiday commitments into the day-ahead solution of an effective operating day and allow generators to earn make-whole payments based on the lesser of a real-time or day-ahead offer cost.

“We feel these are ideal to provide more security and assurance to resources,” Howard said at an Oct. 10 Market Subcommittee meeting. He said the rules are simpler than instituting a multiday market and that they help members feel more comfortable when they must contract for gas.

“When you compare this solution to doing the necessary software changes in our settlements system, that’s a huge cost benefit,” Howard said.

Howard also said the rules’ wording will establish assurances that extend beyond gas units.

MidAmerican Energy Co. — which serves natural gas customers in Iowa, Illinois, Nebraska and South Dakota — had argued that owners of natural gas units “undertake significant risk in purchasing or not purchasing natural gas when natural gas supplies are very tight” and are faced with either capacity loss or financial loss. MidAmerican said on rare occasions, there isn’t any natural gas available to buy after next-day trading in some portions of MISO. (See MISO’s MSC to Debate Multiday Gas Requirements.)

While some stakeholders have said the time is right for such a requirement, others said they worried about over-procurement of gas and whether the requirement would lead to pricing spikes at hubs.

Howard has said MISO already runs a multiday reliability assessment and commitment engine — the RTO’s Forward Reliability Assessment Commitment process — every day to position generation owners for upcoming obligations.

MidAmerican representative Dennis Kimm said he was happy with MISO’s compromise. He asked if the guarantees could be in place for upcoming cold weather.

“It might be a tough sell for this winter,” Howard said, referencing the settlements and tariff changes the rules will require.