The North American power grid’s resource adequacy outlook is “worsening,” and multiple assessment areas are at high risk of energy shortfalls over the next 10 years, NERC wrote in its 2025 Long-Term Reliability Assessment released Jan. 29.

NERC determined that five of the ERO’s 23 assessment areas — MISO, PJM, Texas RE-ERCOT, WECC-Basin and WECC-Northwest — could develop into high risk between 2026 and 2030, meaning planned resources as of July 2025 would lead to energy shortfalls in excess of resource adequacy targets or baseline criteria for unserved energy or loss of load.

A further eight areas — MRO-Manitoba, MRO-SaskPower, MRO-SPP, NPCC-Maritimes, NPCC-New England, NPCC-New York, NPCC-Quebec and SERC-East — were assessed as elevated risk. These areas met resource adequacy targets but were likely to experience energy shortfalls in extreme weather conditions. The remaining 10 assessment areas were labeled normal risk, indicating sufficient resources under a broad range of conditions.

In a webinar accompanying the release of the LTRA, John Moura, NERC’s director of reliability assessments and performance analysis, called the message of the assessment “pretty straightforward: Reliability risk is increasing … not because we lack awareness, but [because] the system is changing faster than the infrastructure needed to support it.”

This is a common theme among the elevated and high-risk areas, most of which were described in the LTRA with some variation of “demand growth projections are outpacing planned resource additions,” as NERC wrote about NPCC-Quebec. Summer and winter peak demand across the continent are projected to grow more quickly over the next 10 years than in any decade since 1995-2004, reaching a constant annual growth rate of 3% and 2.5%, respectively.

Demand growth in many areas is being driven by multiple factors, including large loads such as data centers and industrial centers in nearly every area, along with the electrification of transportation in the U.S. East Coast and Canada, and the growth of heat pumps in areas such as New England and PJM. Population growth is contributing to demand in NPCC-Quebec and ERCOT.

Another frequently mentioned concern is the nature of new resources, with variable energy resources like solar and wind generation projected to rise from 10.2% of on-peak capacity in 2025 to as much as 20% in 2035, depending on the completion of planned projects. This creates vulnerability in winter, because winter peak demand usually occurs during early morning, when availability of weather-dependent resources is low.

As a result, most areas likely will need to turn to natural gas generation to fill the gap. Utilities are projected to add at least 12 GW of new gas generation through 2035, and possibly as much as 41 GW; 11 to 39 GW of this capacity is expected to be completed within the next five years. This buildout also will require investment in gas infrastructure to ensure the availability of fuel, NERC observed.

The report “shows that there’s still time to act, and the results shouldn’t be taken as an indictment of those [assessment] areas. In fact, the level of industry and policy engagement, and, of course, analytical rigor behind the work is higher than ever,” Moura said. “The challenge is not a lack of effort; it’s really the pace and scale of the system transformation occurring at the same time as demand growth accelerates.”

Reactions to the LTRA among industry stakeholders were varied. Michelle Bloodworth, CEO of coal lobbying group America’s Power, highlighted the report’s projections of coal plant retirements in high-risk regions and warned that “the grid will lose an energy-secure, affordable and reliable source of baseload power” as a result.

Caitlin Marquis, a managing director at renewable energy trade group Advanced Energy United, urged state governments and grid operators “to remove the red tape blocking deployment of the most cost-effective and fastest-to-build resources, including solar, energy storage and demand-side resources.”

“Rather than double down on resources that already dominate the supply stack, adding more affordable, reliable advanced energy technologies like storage paired with renewable energy and demand-side solutions will increase resource diversity and support affordability by minimizing fuel-based price spikes,” Marquis wrote.

Todd Snitchler, CEO of the Electric Power Supply Association, said in a statement that the challenges mentioned in the LTRA “are national in scope and are not limited to any single market or operational structure.” He said the best approach for reliability is “competitive electricity markets that send clear, durable development signals — not by policy interventions that create misalignment between supply and demand.”

A newly published review of utilities serving 81.1 million U.S. customers found $30.5 billion in 2025 rate hike requests — a record high, and twice as much as was sought in 2024.

The report issued Jan. 29 by PowerLines further quantifies what has become a salient political issue: rising energy costs.

“As these costs keep climbing,” PowerLines Executive Director Charles Hua said, “policymakers of all political stripes will face growing pressure to take action and advance solutions to improve our grid and lower utility bills for American consumers and businesses.”

Rate hike requests do not go through unchanged, and state utility regulators of all political persuasions continually announce steps to protect ratepayers.

But even with that regulatory effort factored in, the impact of rising prices is being felt. The report notes that an estimated 80 million Americans struggle to pay their utility bills and more than 50 million keep their homes at unsafe or unhealthy temperatures. More than 20% of American households experience energy poverty, spending more than 6% of their income on energy bills.

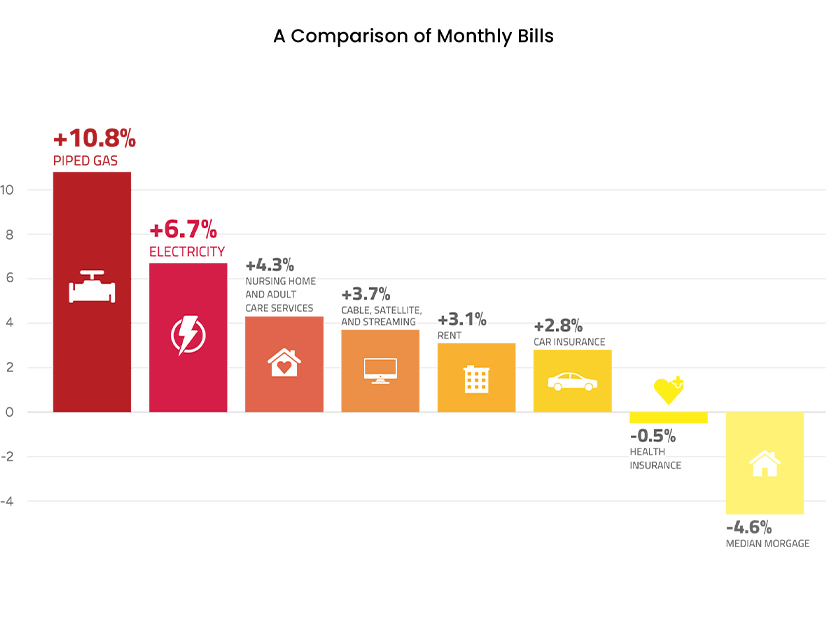

Monthly utility bills — which include charges and/or credits beyond rates — increased 10.8% for piped gas and 6.7% for electricity from December 2024 to December 2025 while the overall U.S. inflation rate was just 3%, the authors write. Since the first quarter of 2021, residential retail electricity prices have increased approximately 40%.

Electricity and natural gas prices have become the fastest drivers of inflation, the report states.

Commercial and industrial electric prices did not increase as sharply as residential prices in 2025, only about 5%. But such increases typically are passed on to consumers through higher costs for goods and services.

A March 2025 poll conducted by Ipsos for PowerLines concluded three in five Americans were not familiar with the public regulatory board that controls their utility bills, three in four are concerned about rising utility bills and four in five feel powerless over these costs.

Data from the U.S. Bureau of Labor Statistics shows that utility prices for gas and electricity increased much more significantly than some other major household expenses. | PowerLines

Against this backdrop, it was inevitable perhaps that rising utility bills would become a leading political issue. PowerLines expects these costs to be a top concern for voters in the midterm elections, particularly in competitive 2026 congressional and gubernatorial races.

The report notes that early projections for 2026 do show some moderation: The Energy Information Administration expects electricity prices to increase about 4%, but that still is much more than the Federal Reserve’s projected 2.4% inflation rate.

Collecting data from public databases, news reports, press releases and utility regulatory filings, PowerLines counted $30.5 billion in 2025 rate increases compared with $15 billion in 2024.

The impact was most intense in the Northeast, where $6.5 billion in rate increases spread across 11.5 million customers were sought. The least intense impact was in the Midwest — $3.2 billion in increases affecting 16.7 million customers.

In between were the South ($14.3 billion across 32.9 million customers) and West ($6.5 billion across 20 million customers).

Each of the rate increase requests is different, but four key factors emerged as PowerLines analyzed the data collected: aging infrastructure that needs to be replaced; repairing damage from past extreme weather or making upgrades to prevent future damage; volatile fuel costs; and rising electricity demand, although some utility markets and some investments are structured so that rising demand can lower electricity prices by spreading costs over a broader customer base.

The authors note that utility capital expenditures — a key driver of profit for utilities and costs for their ratepayers — increased more than 14% between 2024 and 2025.

IESO officials held firm on excluding hydro redevelopment projects from the ISO’s Long Lead-Time (LLT) procurement despite objections from potential bidders at a Jan. 28 engagement session.

Officials also attempted to assuage concerns about the use of confidential reserve prices to control costs.

The ISO created the LLT procurement for resources that require longer planning cycles than the four-year lead times in the pending Long Term 2 (LT2) procurement. IESO plans to seek 600 to 800 MW of capacity from storage resources and up to 1 TWh of energy from hydro resources requiring at least five years of lead time. (See IESO Drops Termination Option for Long Lead-time RFP.)

The energy stream of the LLT request for proposals will be open to new-build hydroelectric facilities with a nameplate capacity of at least 1 MW that do not include pumped storage. The ISO said it will not permit bids from hydro redevelopment or expansion projects, despite proponents’ claims that such additions may also require longer design and construction cycles.

Stephane Boyer, of FirstLight Power, said he did not understand the ISO’s rationale for excluding hydro expansions, which he said would be unable to compete against wind and solar projects in IESO’s long-term procurements.

“Why not give the opportunity to bid in [and] get the most cost-competitive hydro you can get in the earlier window that is currently open?” he asked.

IESO officials said hydro expansions and redevelopments should seek 20-year contracts under the upcoming LT2 procurement because they can be developed in less than five years and don’t require the 40-year contracts in the LLT solicitation.

Boyer and Paul Norris, president of the Ontario Waterpower Association, said ratepayers would benefit from the longer contract terms. “We’re artificially eliminating … the participation of some hydro projects in the ISO procurements because they take longer than five years and they’re not greenfield,” Norris said.

John Wynsma, formerly of Peterborough Utilities, said that between 2008 and 2016, the company built one new hydro project while completing one expansion and one redevelopment, each of which took more than five years.

“The new-build was the cheapest of the three, and that’s because of logistics: It’s a clean site,” he said. “The redevelopment cost 40% more than the new-build. The expansion cost more than 50% more than the new-build.”

He suggested IESO allow redevelopments and expansions to submit prices for 20-, 30- and 40-year contracts in the LLT solicitation, with the ISO choosing any it finds attractive. “I think you’re missing an opportunity here,” he said.

IESO’s Ben Weir said ISO officials are still deciding how they will treat hydro redevelopments under LT2. “It’s a bigger piece of work that’s just not going to be done by the time that LLT has to launch,” he said.

“We do want to get a terawatt-hour worth of energy out of new-build hydro facilities in the province,” he continued. “I understand that the timelines for LT2 have not been made public yet, but we do expect to make those public at the end of an engagement in February.

“Whether or not those expansions are going to take five years is a site-specific question,” Weir added. “When we’re talking about upgrades and expansions to existing facility, it’s our position that a 40-year contract … shouldn’t be required in order to recover the investment that’s being made.”

On Jan. 29, IESO held an engagement on its Northern Hydro Program (NHP), which will allow existing hydro facilities of at least 10 MW to win new 20-year contracts. NHP will begin accepting applications on March 31.

Concern over Reserve Prices

Boyer also raised concerns over IESO’s plan to use reserve prices — a confidential price threshold — to ensure it doesn’t pay too much in the LLT solicitation. The ISO said the thresholds will be based in part on prices in the first window of the LT2 procurement and differences in the obligations of LT2 and LLT resources.

Boyer said LT2 “is for different technology with different attributes, which is very different from the baseload hydro that you’re looking at now to procure.”

The reserve price and limited guidance over interconnection timelines is requiring bidders to make “a lot of investment … with a lot of unknowns and uncertainties,” Boyer said.

Weir said the ISO will adjust the reserve price to acknowledge the differences between the LLT and LT2 procurements. “In no way, shape or form is it just the LT2 price,” he said.

‘Buy Local’ Provisions not Final

ISO officials said they hope to complete the LLT RFP and contract by the end of the first quarter — with the bidding commencing in the fourth quarter — but are still waiting for the Ministry of Energy and Mines’ directive on how to apply “buy local” requirements.

Bidders will be required to provide a “local supply plan” identifying their major goods, services and workforce suppliers, an attestation that the proponent plans to source at least 50% from Ontario or other Canadian provinces, and an explanation for what cannot be obtained domestically.

“The feedback that we’re seeking is whether proponents were already planning to source at least 50% of the project spend from Ontario or Canada,” Weir said. “If they weren’t planning on doing that — but could, because there are domestic sources of those good services and workforce — what the cost implications would be to bring that level up to 50%.”

Team Experience

The ISO also rejected requests that it allow proponents’ consultants to help them meet the RFP’s experience requirements.

All bidders will be required to have at least two team members with experience in planning, developing, financing, constructing and operating at least one “qualifying project” — an electric generation or storage facility that has reached commercial operation in the last 15 years in Canada or the U.S.

Proponents of Class II long-duration energy storage (LDES) technologies will be required to have at least two team members with experience on a project of the same technology (at least 1 MW) expected to reach commercial operation by the end of 2029.

IESO said consultants cannot count toward experience requirements because “they may not be enduring members of the project team” and could leave before the project reaches commercial operation.

Tariff Protections

Stakeholders also contended that the ISO should not have absolute discretion to cancel a contract if a developer seeks additional payments to compensate for tariff changes imposed after the deal is signed.

The ISO said developers should only submit tariff adjustment notices if the price change is “absolutely critical to maintain [the] viability” of the project “and should not be used … as a negotiating mechanism.”

Other Issues

In other developments, IESO said it is:

updating resource eligibility rules for storage to require that the instantaneous maximum withdrawal capability of the facility be equal to or greater than the project’s nameplate capacity. For example, a 200-MW nameplate project must be able to withdraw 200 MW during its charging cycle.

removing a requirement for obtaining municipal support confirmations by Aug. 21.

seeking feedback on how to define hydro project sites to reflect impacts on adjacent properties, such as lands that may be flooded.

adjusting its compensation formula to protect hydro suppliers’ revenues during droughts that reduce production. IESO’s Jasdeep Kahlon called it a “tradeoff” that will also reduce hydro projects’ revenue “upside.”

Stakeholder feedback on the Jan. 28 session is due Feb. 12.

The North American grid made it through the winter storm of Jan. 24-26 — dubbed “Fern” by The Weather Channel — relatively unscathed, but the cold weather gripping much of the U.S. and Canada continues, and cold snaps in the future will still stress the interconnected power and natural gas systems.

The industry mobilized ahead of the storm, sending out more than 65,000 workers from 44 states to start damage assessments and repairs as soon as possible, according to a news release from the American Public Power Association, Edison Electric Institute and the National Rural Electric Cooperative Association. As of 9 a.m. Jan. 29, 750,000 customers had their power restored, but work continued, especially in areas that saw an inch or more of ice accumulation.

“This unified effort includes close coordination with federal, state and local officials who share the goal of safely restoring power as quickly as possible,” EEI CEO Drew Maloney said. “The massive mutual assistance mobilization has ensured we have enough workers in place, with crews shared across the region and reassigned to the next priority as soon as they wrap up work.”

The Electricity Subsector Coordinating Council has held three calls to coordinate the response between the industry and federal government.

“Thanks to the work of our industry partners, mutual assistance crews are restoring power as quickly and safely as possible across the country,” Deputy Energy Secretary James Danly said in a statement. “Since Winter Storm Fern began on Jan. 24, the department has issued eight emergency orders to stabilize the electric grid across impacted regions; the department is using all of the available tools at our disposal to mitigate power outages and save lives.”

While the industry wraps up work connecting customers who lost power because of distribution outages and faces some ongoing cold in the coming days, winter reliability will continue to be an issue for the foreseeable future, experts said during a webinar hosted by R Street Institute on Jan. 29.

The biggest risk to bulk power system reliability in the coming years is whether the industry can respond to growing demand from data centers and other sources, but recently retired ISO-NE CEO Gordon van Welie listed the gas-electric issue as a close second.

“The biggest secondary factor is this mismatch between planning and paying for the gas system and the electric system, and the mismatch between the reliability standards for these two systems and the lack of recognition that the gas and electric systems have become one interdependent energy system,” van Welie said. “And we’re still regulating these systems as if they exist in independent silos.”

Winter reliability depends on weatherizing equipment and ensuring adequate fuel during cold snaps, which require strong performance incentives in the wholesale markets, investment in the required fuel infrastructure and some way to recover those costs, he added.

After Winter Storm Uri in February 2021, FERC and NERC made significant improvements to the point where that is “largely solved,” van Welie said. The two industries have worked to improve information sharing, but that has provided only incremental gains, he said.

The real need is for more infrastructure, van Welie argued. But while the two systems have become increasingly interdependent, they are regulated differently.

“The restructuring took different paths with different economic structures for cost recovery,” van Welie said. “And the consequence now, since they’ve become interdependent, is this total mismatch in terms of cost recovery for the underlying network, so I’m not talking about production here of gas, but the networks for delivering the gas.”

Inadequate gas infrastructure can lead to unreliable electricity supply, which compromises all aspects of the economy, including the ability to deliver gas to heat homes during cold snaps. After Uri, van Welie asked RTO staff to work with electric utilities and local distribution companies to estimate how the system in the Northeast would handle similar outages as seen in Texas.

“The biggest alarm bell came from the gas LDCs, who said, ‘There’s no way we can tolerate rotating feed outages, because what we’ll end up doing is a flameout,’” van Welie said. “‘We’ll end up with a flameout on the gas system. It’ll take us weeks to restore the gas system.’”

“I fear we’re going to need another 2003 event to really move the needle on this issue,” van Welie said.

The Northeast blackout in 2003 gave Congress the impetus to create a mandatory reliability system for the grid with the Energy Policy Act of 2005. Van Welie said the same kind of shock could force it to finally better align the gas and electric systems.

New England has been facing gas-electric coordination issues for more than two decades, but as Electric Power Supply Association CEO Todd Snitchler recalled on the webinar, it has been a focus at FERC since at least 2011.

“Well, that was 15 years ago, and we still haven’t solved it,” he added. “I do think we’ve made progress, and I’m happy to say that that’s been the case.”

The current cold snap is affecting a wide swath of the country, and so far, those improvements have borne fruit, with the two industries working well together, Snitchler said.

“I think the information sharing has improved dramatically,” he added. “I think the ability for the RTOs to interact with the gas system and with the power system and speak more common language has improved fairly significantly.”

Getting more infrastructure built would help, but Snitchler said cost recovery is an important issue.

“Markets treat cost recovery differently. Independent market monitors have different views about what’s eligible for cost recovery and what can be bid into the system,” he said. “And I think those questions are yet to be fully resolved in a way that helps to mitigate the volatility and stressful conditions but ensures, ultimately, that reliable system.”

Even outside of the issues in winter, the need to meet data center demand is going to require additional gas pipelines — and electric transmission lines, he added.

Uri hit Texas worse than anywhere else, as ERCOT suffered major outages exacerbated by gas-electric coordination issues, and led to hundreds of deaths. ERCOT’s former Independent Market Monitor and R Street Fellow Beth Garza noted that the gas-electric issues are different in Texas because of the lack of restructuring on the gas side.

“In Texas, the majority of natural gas-powered generation is supplied by intrastate pipelines [that] aren’t required to have the same kind of unbundling and restructuring that has happened in the rest of the country,” Garza said. “I would just point folks to the aftermath of Uri. Look at the profits that Energy Transfer; look at their profits of billions during that event, versus the loss of the largest generator in Texas, Vistra, which were also in the billions. And that, to me, tells a story.”

The oil and gas industry is politically powerful in Texas, and it has not been restructured at all, which is the opposite of what has happened in ERCOT’s electricity market, she added. The biggest thing aimed directly at winter reliability since Uri was that generators started getting paid to keep oil stored on-site at dual-fuel units, but Garza sees a bigger need for stored fuel.

“There needs to be an investment in gas storage,” she added. “It’s not just pipelines. It’s the ability to withstand, particularly in the wintertime, the production decreases that are going to happen because of the cold weather.”

One state that has done well with gas-electric coordination issues is Florida, which has the highest percentage of gas generation and is at the end of the pipeline network like New England, NERC Director of Reliability Assessments John Moura said.

“They build the gas pipeline for the generators,” Moura said. “They’re high-pressure contracts. They have a mandate to have oil backup because there’s a good amount of generation, 16,000 MW, that is south of any other pipeline options —kind of a single contingency there, so there’s dual fuel. So, they’ve done things, worked it into their integrated resource plans, not the markets. But I think there’s things to learn from the signals that they’re putting in them.”

Some MISO stakeholders said an extreme events analysis from the 2025 transmission planning cycle potentially raises a red flag and deserves more attention.

MISO found the possibility for cascading outages in all four of its planning regions in its annual extreme events analysis for its 2025 Transmission Expansion Plan (MTEP 25). The grid operator said its South region contains the most potential for cascading, extreme contingencies.

MISO completed the analysis in late 2025. The analysis contemplates several failures, including loss of large generators, transmission elements, load centers and failures brought on by hurricanes, wildfires, cyberattacks and other catastrophes.

However, there’s not much to glean beyond that. Results are shielded from the public in the confidential appendices of the annual MTEP report and protected by nondisclosure agreement requirements and a Critical Energy/Electric Infrastructure Information designation.

Sustainable FERC Project’s Natalie McIntire asked where stakeholders can go to view a list of transmission solution ideas or remedial action schemes that might be designed because of the findings.

Clean Grid Alliance’s David Sapper seconded the ask. He said 2025’s “concerning results” warrant more discussion, not simply an agenda item without a presentation from MISO staff.

MISO published the analysis results in a “post-only” format without dedicated discussion time at a Jan. 28 Planning Subcommittee meeting.

“‘It is what it is’ suggests too much indifference,” Sapper said at the meeting.

Minnesota Power’s Tom Butz asked if the extreme events analysis findings could be discussed in MISO’s Resource Adequacy Subcommittee.

Butz said the analysis seems to deserve a larger conversation on “system reliability, not just a localized version of reliability” for transmission owners.

“It seems like this is a source for this to come from,” Butz said of a discussion on how to tackle some cascading failures. He said MISO should “connect the dots between the two worlds,” meaning local planning versus regional preparation.

“We’d be more than willing to have more conversations,” MISO engineer Scott Goodwin said.

But Goodwin reminded stakeholders that loss of load is at times an acceptable form of mitigation, according to MISO’s planning standards.

Planning Subcommittee Chair Patrick Jehring, of GridLiance, said he understands the “difficulty” of trying to publish findings while working around privileged information.

“What we heard today is kind of lacking. … It doesn’t really help drive a conversation about ‘what do we do about this?’ What can you show to form a discussion about these extreme events?” Jehring asked MISO staff.

Senior Expansion Planning Engineer Amanda Schiro said she would evaluate what insights MISO might be able to share.

McIntire said MISO might consider sharing aggregated data or “themes of analysis.”

California continues to add in-state renewable energy resources, but the transmission upgrades needed to bring those projects online have been lagging behind, according to the California Public Utilities Commission.

About 8.9 GW of renewable and storage resources are expected to be delayed due to transmission delays in the Pacific Gas and Electric (PG&E) and Southern California Edison (SCE) territories, Edmund Dale, CPUC senior regulatory analyst, said at CAISO’s Jan. 28 transmission development forum.

The 8.9 GW represents about 22% of the total 40.5 GW of new renewable generation and storage resources that have signed interconnection agreements in the PG&E and SCE areas.

For PG&E, about 2.5 GW of these resources are delayed due to “bundling dependencies,” which are chain reactions of transmission project delays, Dale said. PG&E said the interconnection customers are responsible for resolving the transmission delays, he said.

One critical delayed transmission project in PG&E’s territory is the Vaca-Dixon Substation 230-kV circuit breakers 442, 452 and 462 project. About 450 MW of new capacity is delayed due to this project’s lag, with an additional 900 MW at risk.

Material problems are a primary cause of transmission delays, with a supply chain issue resulting in an 11-month delay on PG&E’s Gates 230-kV Reactors Bus E-F transmission project, affecting 2 GW of resources. To address the delays, PG&E will shift material from another project to the Gates project, Dale said.

Financing and project redesign delays could also significantly affect renewable and storage resource projects in PG&E’s territory, Dale added.

In SCE’s territory, long lead-time materials, such as circuit breakers, transformers and specialized steel structures, are forecast to delay 4.5 GW of new resources, with an additional 2 GW of resources at risk of delay.

To alleviate some of these delays, participating transmission owners (PTOs) should consider allocating more time and other resources to determining more realistic in-service dates and project costs, Dale said.

CAISO is in frequent and close coordination with the CPUC and the transmission owners about transmission project delays, CAISO spokesperson Jayme Ackemann told RTO Insider.

“Delays do not typically result in changes to the transmission studies or approvals, per se, but such delays are considered in the generator interconnection and deliverability allocation processes,” she said.

The ISO does not anticipate impacts to available resources in EDAM, Ackemann added.

Transmission project delays are now tracked per the requirements of California Senate Bill 1174, passed in 2022. The law requires transmission facility owners to submit a report to the CPUC that shows changes to previously reported in-service dates of transmission and interconnection facilities that are necessary to provide transmission service to certain renewable or energy storage resources.

In November 2025, the CPUC detailed transmission delays in an annual report. It showed 449 delayed transmission projects with associated renewable generation or storage resources.

San Diego Gas & Electric (SDG&E) said it did not have any delayed transmission projects with associated renewable and storage projects.

CPUC staff reviewed SDG&E’s data and “determined it to be incomplete and inaccurate” and requested updated corrections to SB 1174 data from SDG&E, which SDG&E provided, the report says. However, CPUC staff determined that the updated data was “still not sufficient” because SDG&E did not provide data for its in-development transmission projects and provided incorrect original in-service dates, the report says.

Bipartisan leaders of the Senate Environment and Public Works Committee want to pass energy infrastructure permitting legislation, but a Jan. 28 hearing on the subject showed how that might not happen during this Congress.

Senators, including EPW Ranking Member Sheldon Whitehouse (D-R.I.) and leaders from the Energy and Natural Resources Committee, have been working on potential legislation for the past year, but are trailing House colleagues who passed a bill late in 2025 that would alter the National Environmental Policy Act to speed up permitting. (See House Passes SPEED Act to Quicken Infrastructure Permitting.)

“I’d like to begin by thanking my colleagues who are here with me, and in particular, Ranking Member Whitehouse, for their drive to elevate problems in our current permitting regime and to work constructively together,” EPW Chair Shelley Moore Capito (R-W.Va.) said at the start of the hearing. “That’s what we need to do.”

“It’s the never-ending story on permitting, but we’re going to get into that story — I hope,” Moore Capito said.

Any bill needs to be bipartisan to be durable, she said before Whitehouse made his opening remarks, saying he shared that goal but thinks there is a “trust problem” with the Trump administration. He cited the president’s executive orders that temporarily stopped the Empire offshore wind project.

“This all stank, but I remained willing to work on a permitting bill,” Whitehouse said. “In August, stop-work Trump struck again against Revolution Wind off Rhode Island, a project over 80% complete with $4 billion invested, based on supposed national security concerns. That order was instantly thrown out in court as arbitrary and capricious, in part because the Trump administration had been making the opposite arguments about that same project in the same courthouse just weeks earlier.”

Other actions against clean energy continued through 2025.

“So, Sen. Heinrich [D-N.M.] and I have paused permitting reform negotiations,” Whitehouse said. “Let me be clear: We find no fault with Senate Republicans.”

The conflict is entirely between the legislative and executive branches of the government, according to Whitehouse, who said the Trump administration’s “lawless” attacks on clean energy loom over every other industry. The executive can resuscitate the bill’s prospects if it shows it will stop putting up roadblocks to clean energy, Whitehouse said.

The Solar Energy Industries Association is not focused on reforming NEPA, which the SPEED Act and any Senate proposal from EPW would do, because the law is rarely used in litigation against solar projects, said SEIA CEO Abigail Ross Hopper, who said “permitting is essential.”

“SEIA strongly supports these bipartisan efforts to improve the process for energy and transmission projects,” she said. “Permitting reform must begin with this basic principle: Projects that enter the federal permitting process must be allowed to move through that process in good faith and without unfair treatment based on energy source. And once a project receives a permit, that permit should be honored.”

The solar and battery developers that SEIA represents have run into issues with the Trump administration since a July 2025 Department of the Interior memo created “68 new layers of red tape” for their projects, she added. By requiring secretarial approvals on many easy decisions, it effectively amounts to a moratorium on solar.

The bureaucratic roadblocks are endangering 70 GW of solar and 42 GW of battery storage on both federal and private land,” Ross Hopper said. Together they represent 43% of all planned new capacity in the U.S.

“We all know electricity demand is rising rapidly, and without this power and the grid infrastructure to deliver it, electricity prices will continue to rise,” she said.

Sen. Ed Markey (D-Mass.) noted that the tactics being used against solar now could be wielded against the oil and gas industry in the future by a Democratic president. He entered a memo into the record from Evergreen Action laying out how to get that done.

“This administration must be forced to end its punitive treatment through clear legislative text and vocal Republican opposition to any efforts to violate the law,” Markey said.

After Markey’s turn on the mic, Sen. Cynthia Lummis (R-Wyo.) responded that previous administrations from his party had done the same kind of thing against infrastructure they disliked.

“Mr. Markey, we feel your pain. We could take your statement and where you said left — we could put right,” Lummis said. “Where you said right, we could put left. Where you said Trump, we could put Biden.”

One of the first things former President Joe Biden did when taking office in 2021 was to stop construction on the Keystone XL pipeline, she added. Markey countered that Trump has taken more such actions before Chair Moore Capito reminded him it was Lummis’ time to speak.

The way Maryland Del. Lorig Charkoudian (D) sees it, working with other Mid-Atlantic states to study the costs and benefits of withdrawing from PJM is, at this point, the only responsible thing to do.

“PJM is frustratingly slow in changing, if changing at all [and] continues ─ even in a reliability crisis of their own making ─ to double down on their love affair with fossil fuels … at a really significant cost to our ratepayers. And so, you reach a point where it’s almost irresponsible not to say, ‘What are the other options?’”

Charkoudian was speaking during a recent legislative update call hosted by the Maryland Clean Energy Center (MCEC), where she previewed a package of bills she is sponsoring during the current legislative session, including H.B. 143, calling for the state to work with neighboring PJM states to study possible alternatives.

For example, the states ─ Maryland, Delaware, New Jersey, Pennsylvania and maybe Virginia ─ could start their own RTO or use PJM’s fixed resource requirement (FRR) “to pull ourselves out of the capacity auction,” she said.

Going the FRR route would require utilities in the states to procure their own capacity, rather than relying on PJM’s increasingly expensive capacity auctions, and H.B. 143 also would require Maryland utilities to study the costs and benefits of ensuring they could provide at least 80% of their capacity.

“The idea is to explore doing more capacity procurement through bilateral contracts and then use the PJM auction” as backup, Charkoudian said in an email to Livewire.

The Maryland General Assembly kicked off its 2026 session Jan. 14, and as far as energy policy is concerned, Charkoudian predicts “an adventurous year … [with] a lot of moving parts.”

Like Gov. Wes Moore’s Lower Cost and Local Power Act ─ announced Jan. 27 ─ which could actually tie the state more firmly to PJM by requiring all utilities to join the RTO. The bill has yet to be formally introduced, but a one-page summary argues that having all the state’s utilities in PJM ─ including small municipal utilities that generally have lower rates than investor-owned utilities ─ would lower electric bills.

K Kaufmann

The state’s largest utilities ─ Baltimore Gas and Electric, Pepco Maryland and Delmarva Power, all IOUs owned by Exelon ─ already are members, as is the Southern Maryland Electric Cooperative. (See below for more details about the governor’s bill.)

So, the 90-day legislative session ahead is shaping up as a case study in how states facing explosive demand growth will attempt to build more clean energy, cut electric bills and reduce greenhouse gas emissions as PJM and the Trump administration resist any change that puts more solar, wind and storage online.

Maryland aims for 100% carbon-free power by 2035 but imports 40% of its electricity from the regional grid, making it particularly dependent on PJM’s mostly fossil-fueled power and vulnerable to any swings in the RTO’s market prices. The state’s consumers already are absorbing rate increases due to PJM’s price-spiking capacity auctions, and more pain is ahead with the December auction, for 2027/28, hitting yet another record high, $333.44/MW-day, up from $28.92/MW-day in 2023.

“It’s very easy to get caught up in all the drama around energy right now,” Charkoudian said during the MCEC call. “[But} we have, for the most part, all of the tools that we need, and we need to put them together in the right policy.”

Charkoudian vs. Moore

The politics of the upcoming midterm elections also are a key factor ─ Moore and all state lawmakers are running for re-election in November ─ affecting what new energy policies can be shepherded through the legislature and reach Moore’s desk.

Both the governor and Charkoudian want to get more clean energy online in Maryland, to help wean the state off its dependence on PJM and provide support for local installers, developers and consumers in the absence of federal incentives cut off by the Republicans’ One Big Beautiful Bill Act.

The 30% federal tax credit for residential solar was terminated Dec. 31, 2025. Commercial projects still can qualify for the credit if they start construction by July 4, 2026, and are online by the end of 2027.

The one-page summary of Moore’s bill says it will “create a process for clean energy projects to apply for financing for shovel-ready projects,” which, on the face of it, could primarily benefit utility-scale projects. (Residential and smaller commercial projects are rarely described as “shovel-ready.”)

In contrast, Charkoudian’s Affordable Solar Act (H.B. 345) lays out a detailed plan for Maryland to adopt incentives similar to New Jersey’s, providing different levels of financial support for different kinds of solar ─ utility-scale, commercial, community solar and residential.

Incentives for utility-scale projects would be determined through a competitive auction, with the lowest-cost projects receiving incentives, while the state’s Public Service Commission would set the price for solar renewable energy certificates (SRECs) for residential, community solar and commercial projects under 5 MW.

The PSC would review and adjust the SREC price every three years, or more frequently if warranted by market conditions. Right now, the SREC price in New Jersey has been set at $85/MWh. Maryland SRECs are priced around $50, according to Flett Exchange, an online SREC trading platform.

New Jersey’s utility-scale auctions got off to a rocky start, with the state’s Board of Public Utilities rejecting all the bids in the first solicitation in 2023, saying they were too high. A second auction in 2024 awarded incentives to eight utility-scale projects totaling 310 MW.

Charkoudian described her proposed incentives as the “best bang for the buck from a ratepayer side, from a Maryland side. … We’re going to provide as much subsidy as is needed, but not a penny more, to each different sector of the industry.”

The bill also would make plug-in “balcony solar” legal in Maryland ─ a significant win for cutting home electric bills ─ and ensure that ratepayer dollars intended for the state’s clean energy fund cannot be used to fill holes in the state budget. Moore wants to take $292 million from the fund ─ the Strategic Energy Investment Fund (SEIF) ─ to backfill a 2027 deficit estimated at close to $1.5 billion.

ATTs and Grid Expansion

Both Moore and Charkoudian are bullish on advanced transmission technologies, which can optimize and expand capacity on existing power lines, as a cheaper, faster alternative to building new transmission.

Moore’s bill calls on utilities “to prioritize [ATTs] to expand existing grid capacity and authorize the use of state and interstate highway corridors to co-locate these projects.”

Again, Charkoudian provides a more detailed approach in H.B. 40. Utilities or other transmission owners within the state would be required to identify areas where grid congestion has occurred in the past three years, as well as where congestion may be likely to occur over the next five years, and then develop plans for using ATTs as part of any grid upgrades or expansion.

Developers seeking a certificate of public convenience and necessity for transmission projects also would have to show they’ve considered ATTs as an alternative to building a new line.

Charkoudian acknowledged that implementing the law could be tricky due to the fine line between state and federal regulation of new transmission. But she sees ATTs providing both grid efficiency and affordability.

An additional problem here is the slipperiness of legislative language. Any effort to get utilities to prioritize or consider new technologies tends to lead to highly technical arguments about why said technologies are not appropriate or feasible for any one project or situation. Compensation is another potential roadblock since upgrading wires with ATTs may be considered a maintenance cost that cannot be passed on to a utility’s customers ─ that is, in many places, ATTs cannot be rate-based.

Moore’s bill acknowledges that ATTs must be part of a bigger grid expansion strategy. The governor wants the Department of Transportation to use $10 million from the SEIF “to identify opportunities for high-voltage transmission lines and battery storage projects along state and interstate highways.”

The focus on existing rights-of-ways could be a potential vote winner for the governor in the face of the well-organized and vehement local opposition to the Maryland Piedmont Reliability Project ─ a 70-mile transmission line approved by PJM, which could run through agricultural land in the central part of the state. The fact that the project is being built by an out-of-state utility, Public Service Enterprise Group of New Jersey, has intensified community outrage.

High Bills and Data Centers

Differences between Moore and Charkoudian are more pronounced when we get to the nitty-gritty of high electric bills and data centers.

Besides taking $292 million from the SEIF to balance the budget, Moore also wants to use $100 million for direct bill rebates to “Maryland families burdened by high energy costs” ─ yet another major vote winner. Both those withdrawals will leave the fund with a balance of about $164 million, according to an analysis by Inside Climate News.

What the governor doesn’t mention is that in 2025, more than $94 million in SEIF dollars went to state programs providing bill assistance to more than 70,000 low-income families, according to the Maryland Energy Administration’s 2025 report on the fund. Projected spending for bill assistance programs in 2026 is $150 million. Whether Moore’s rebates would go to upper-income households that really do not need them is unclear.

While Moore’s bill is mum on data centers, the governor signed onto President Donald Trump’s recent proposal that PJM hold a one-time emergency auction to deliver more long-term “baseload” power for data centers across its service territory ─ wording that assumes a traditional reliance on fossil fuels and nuclear.

Charkoudian tackles the data center dilemma in in her fourth bill, which proposes multiple strategies ─ and a preference for clean energy ─ to protect consumers from paying for any new generation or power lines needed to connect these megawatt-guzzling facilities to the grid.

The bill is being finalized, but according to a fact sheet from Charkoudian’s office, the core provisions include:

Accelerated permitting and interconnection for new data centers or other large loads that supply 100% of their power.

A voluntary demand response program for large load customers ─ defined as any facility with a demand of 25 MW or more.

An inventory of surplus interconnection capacity in the state, conducted by the Maryland Energy Administration. The information gathered by MEA “will be shared with large load customers who can then use this surplus interconnection to build new battery storage or other zero-emission resources to avoid having to go through the PJM queue,” according to a fact sheet on the bill.

A requirement for all new large load customers seeking interconnection in Maryland to cover the capacity for at least 25% of their power demand with either behind-the-meter resources, storage or carbon-free power.

A community benefit fee of $1,000/MW to be paid by any large load project applying for interconnection in Maryland. The fee would cover the cost of interconnection studies and be used to provide consumers with assistance for high utility bills and energy-efficient home upgrades.

Both Moore and Charkoudian appear to be moving in the same direction, tackling critical challenges for the state ─ in this case, how to develop a reliable, affordable electric power system with growing amounts of clean energy, an optimized, flexible grid and various pathways for data centers and other large loads to get the power they need.

Charkoudian tends to go big, ambitious and strategic on the bills she introduces, while Moore is smart, but perhaps a bit more cautious, with an eye on the election and Maryland’s mix of liberal and more conservative voters. Pressure from the White House, PJM, utilities and hyperscalers will be intense.

The challenge ahead for both will be getting their bills through a legislature that, even with a large Democratic majority, leans toward consensus, watering down more liberal bills with cuts, rewrites and amendments ─ or letting them die in committee.

In other words, the fate of clean energy, data centers and utility bills in Maryland and other PJM states will depend on the difficult, frustrating but absolutely vital process of making laws in a democratic society, with a free, independent press looking on. Thank goodness, in Maryland, we still have both.

Cybersecurity firm Dragos has blamed Electrum, a threat group linked to Russia’s intelligence service, for a Dec. 29 cyberattack against Poland’s power grid that it said could be a preview of future attempts to compromise critical infrastructure.

The attack occurred Dec. 29 and 30, according to a government statement published Jan. 15, and targeted a system for managing renewable energy sources as well as two combined heat and power plants. Polish Prime Minister Donald Tusk said that “at no point was critical infrastructure threatened,” and no outages occurred as a result of the attack. However, he said, the incident showed Poland’s energy system “requires further strengthening.”

In a report published Jan. 27, Dragos said it was called in by CERT Polska, Poland’s cyber incident response team, to analyze “one of the numerous incidents across the Polish system that are part of this attack.” The firm called the event “the first major coordinated attack targeting distributed energy resources at scale” and said it can “assess with moderate confidence that … Electrum is responsible.”

Electrum is associated with Unit 74455 of Russia’s Main Directorate of the General Staff of the Armed Forces (also known as GRU). Analysts have also dubbed the unit Sandworm and Voodoo Bear, though these may be separate groups within the unit. Unit 74455 is believed to have carried out attacks around the world, including against the Ukrainian grid in 2015 and 2017. (See Six Russians Charged for Ukraine Cyberattacks.)

In its 2024 Year in Review report, Dragos called Electrum one of three active threat groups capable of reaching Stage 2 of SANS Institute’s ICS Kill Chain, meaning “a capability that can meaningfully attack” a target’s industrial control systems. (See Dragos: Attacks on ICS Increased in 2024.)

The December cyberattack targeted systems managing communication and control between grid operators and DERs, meaning both CHP facilities and systems for dispatching renewable energy, Dragos wrote. Through these tactics, the attackers were able to “gain access to operational technology systems with direct connections to generation assets.”

“Taking over these devices requires capabilities beyond simply understanding their technical flaws. It requires knowledge of their specific implementation,” the firm wrote. “The adversaries demonstrated this by successfully compromising [remote terminal units] at multiple sites, suggesting they had mapped common configurations and operational patterns to exploit systematically.”

Although communication was lost, the default behavior of the affected devices was to remain on; this is why no outage occurred. Dragos wrote that because of limited logging of network communications and commands at the affected sites, investigators have not determined whether Electrum tried to issue operational commands to the generation assets.

The firm warned that the Poland attack could indicate a change in adversaries’ tactics to target DER monitoring and control systems. Attackers gained a “foothold that could enable operational impacts, particularly when similar access is achieved across larger numbers of sites simultaneously or if adversaries develop deeper knowledge of specific site configurations.”

Historically, cyberattacks against power grids have required targeting substations or centralized systems, Dragos wrote, citing the Ukraine grid attacks in 2015 and 2016, which involved “large, centralized control points that manage significant portions of the grid.” The global shift from large generation facilities to smaller distributed facilities has opened new attack vectors, leading the firm to warn that “as your DER portfolio grows, so does the attack surface.”

Grid operators don’t just have more points of vulnerability to worry about with DERs; renewable generation facilities also lack the inertia that traditional thermal plants provide, which helps stabilize grid frequency. More than 50% of Poland’s generation fleet is coal-fired plants, Dragos observed, with wind and solar accounting for about 25% of capacity.

The firm suggested the relatively high amount of inertial generation, coupled with strong AC interconnections to neighboring countries, made the attack “unlikely to cause a nationwide blackout in Poland.” But this built-in stability is not guaranteed, the firm warned, particularly in countries pursuing aggressive decarbonization strategies.

Dragos wrote that the Poland attack “represents both continuity and evolution.” Continuity comes from the technical similarities with previous Electrum operations, including the choice of targets and the malware used. The evolution is represented by the change to target “the distributed edge of the grid,” meaning communication systems that enable the compromise of “dozens of smaller generation sites.”

Based on the attackers’ behavior, the firm judged the incident to have been opportunistic rather than “precisely planned … with specific outcomes.” Dragos wrote that Electrum seems to have “exploited whatever opportunities their access provided.” This indicates that the attackers were rushed, but the firm could not determine why.

From direct evidence and public statements, Dragos is certain of at least 12 sites that were affected, and the firm believes the actual total may be at least twice this number, representing as much as 1.2 GW if they had been operating at full capacity. Poland reported record electric consumption of 30 GW on Jan. 17, meaning that if the affected sites had gone down simultaneously and without warning, it could have had a “noticeable impact on the system frequency [of the kind that] have caused cascading failures in other electrical systems.”

Operational technology/ICS incident response: Organizations must have a plan to prioritize restoring connectivity across dozens of sites at once, performing forensics on corrupted systems and detecting the level of control that attackers achieved.

Defensible architecture: Companies should work to prevent adversaries using common weaknesses to easily compromise multiple sites at once.

OT/ICS network visibility and monitoring: Distributed generation operators must ensure they have constant visibility into their systems and the ability to detect abnormal activity.

Secure remote access: Organizations must ensure remote access is protected through multifactor authentication, automatically expiring logins and other security measures.

Risk-based vulnerability management: Companies should be aware of vulnerabilities in distributed generation assets and enable rapid patching across all remote sites.

SPP staff say they still are waiting for an order from FERC before they can begin distributing millions of dollars in compensation to transmission upgrade sponsors from its beleaguered Attachment Z2 process and unwinding billions of dollars in settlements.

The numbers are huge.

The grid operator says it owes about $147 million in refunds, plus an additional $46 million or so in interest to transmission users that made payments under the Z2 process as far back as 18 years ago. It says it also will have to unwind and recalculate more than $20 billion in market settlements dating back to 2015 to resettle that Z2 activity.

Only about 1 to 2% of the latter resettlements are related to the Z2 process, staff told stakeholders during a Jan. 26 virtual meeting.

“This will impact both network and point-to-point activities, so if you’re a transmission customer or transmission owner, you will be impacted, most likely,” said Steve Davis, SPP’s settlements manager. “It’s a large mountain that we’re chiseling away to have a smaller impact.”

That mountain has grown to Everest proportions since 2008, when SPP received FERC’s approval for its tariff attachment that awards credits to sponsors from upgrade sponsors whose service could not be provided “but for” the upgrade. The attachment also required the RTO to invoice the charges monthly and to make any adjustments within one year.

However, software problems delayed Z2’s final implementation for eight years before 2016, during which the RTO did not invoice any upgrade charges. FERC approved a waiver request to settle more than 365 days in arrears, but in 2019, the commission reversed course and said SPP should have settled Z2 activity from only September 2015 forward. (See FERC Reverses Waiver on SPP’s Z2 Obligations.)

SPP General Counsel Paul Suskie has called the Z2 resettlement headache “the most litigated, drawn-out process we’ve ever had.”

The RTO proposed a solution to unwind credit payment obligations assessed under Z2 and made an informational filing at FERC in 2024. In September, the commission ordered the grid operator to make a compliance filing for the proposal. (See FERC Requires Additional Z2 Filing from SPP.)

SPP answered with a filing in November (ER16-1341). It also issued updated refund balances with accrued interest to entities affected by FERC’s remand.

Asked when SPP expects to see the commission’s order, Davis said, “I wish I knew, and that’s probably the best answer we could give. We would love it to be tomorrow, but honestly, I don’t know that we have any indication from FERC.”

SPP’s Charles Locke reminded stakeholders that FERC’s initial order in the proceeding indicated SPP was not to act on the Z2 refunds “until it was specifically authorized to do so by FERC.”

Davis said whenever a favorable order comes, “We plan on hitting the ground running.”

About a month after FERC’s order, SPP will issue final invoices for the refund period. Staff then will complete and deploy an interim Z2 resettlement system and calculate and administer the revised credit payment obligations.

When that process is complete — about eight to 12 months, SPP says — resettlement invoices will be issued for the 2015-2020 operating days. Staff said more than $580 million in Z2 credits have been applied since Sept. 1, 2015; undoing and refunding those historical settlements will require recalculating each operating day since, a process projected to take about two years.

“I keep calling it ‘reshaking of the snow globe,’” Davis said. “We have to recalculate inputs into the Z2 process as if the 2009 period through the September 2015 really never happened.”

Market participants facing big bills will be able to take advantage of a five-year payment plan, using FERC’s interest rate. The commission’s rate for the first quarter of 2026 is 7.20%.

At some point, SPP will transition to the current settlement system for production invoices. Additional resettlements will be run on that system monthly, with staff expecting to resettle three historical operating months each month. They expect to be in sync with normal monthly settlements in 2031.

Ironically, SPP no longer uses the Z2 process. Stakeholders recommended, and the grid operator approved, eliminating Z2 credits in 2020 and replaced them with incremental long-term congestion rights (ILTCRs) for new upgrades. The ILTCRs will limit total compensation to each upgrade’s directly assigned upgrade costs and interest.