A report issued Monday lays out a path for the U.S. to follow as it builds a network of offshore wind turbines and presents it as an opportunity to create an entirely new industry.

But there is some urgency to the effort, the report says, as there is limited infrastructure and manufacturing capacity now, and building it will take years. Given the extended lead time involved, most resources would have to be committed by the end of 2023 to create an operational supply chain by 2030.

The vessels and port infrastructure that exist now or are planned to be built would be enough to install only 14 GW by 2030, for example. And components for up to 83% of that first 30 GW of wind equipment would still need to be imported, while factories are being set up in the U.S. and American workers trained to run them, the report says.

“A manufacturing supply chain is already emerging in more than a dozen locations up and down the U.S. coast in support of the offshore wind industry, which will lead to thousands of well-paying jobs,” said Ross Gould of the Business Network for Offshore Wind, part of the partnership behind the report.

“To meet our ambitious clean energy national goals,” he said in a news release, “American manufacturers must play a larger role to accelerate our transition. This road map lays out the challenges and collaborative actions needed to bring more domestic companies into the supply chain and the opportunity those businesses bring to building out the U.S. offshore wind industry.”

Offshore wind has been gaining momentum for several years, with multiple states pressing development of multiple projects, particularly along the Northeast and Mid-Atlantic coasts.

The report’s authors say there is a widespread agreement that a domestic supply chain will be critical for sustainable growth in the new industry, but no clear understanding of what the supply chain should look like, how long it will take to create, what costs it will extract, what benefits it will yield and how much the existing infrastructure will accomplish.

“We demonstrate that if individual states leverage their existing manufacturing capabilities to contribute to the offshore wind energy sector, this conceptual supply chain would generate significant workforce and economic benefits throughout the United States, not just in coastal locations with active offshore wind energy programs,” the report states.

Multiple potential roadblocks were found on the road map, including communication gaps between stakeholder groups; scarcity of space and uncertainty of permitting for manufacturing facilities in ports; stress on supply networks for raw materials and subcomponents; and insufficient incentives for incorporating equity and sustainability into supply chain decision making.

But the most common concern that manufacturers shared with the report’s authors was the difficulty in securing financing to build the components of a supply chain because of perceived risk of cost or schedule overruns, legal challenges, and changes in government policy.

The report did not even look at the complexity of the transmission grid expansions that would be needed.

Details

The project is being overseen by the National Offshore Wind Research and Development Consortium and conducted by the National Renewable Energy Laboratory, the Business Network for Offshore Wind and DNV Energy USA.

A full project summary will be released by NOWRDC late this winter.

Monday’s report quantifies the resources needed to build a supply chain to reach the 30-GW goal by 2030 as follows:

$22.4 billion minimum initial investment

12,300 to 49,000 full-time equivalent workers

6,800 miles of cable

2,100 turbines

2,100 foundations

58 crew transfer vessels

34 new manufacturing facilities

11 service operation vessels

8 East Coast marshaling ports

4 to 8 transport vessels

4 to 6 heavy lift vessels

4 cable lay vessels

2 floating wind integration ports

2 scour protection installation vessels

Recommended near-term actions (2023-2024) to build a foundation are:

Convene working groups focused on local and holistic aspects of the supply chain.

Identify efficient and equitable locations for infrastructure.

Assess the need for additional incentive mechanisms.

Establish mechanisms targeted at floating wind infrastructure.

Establish curriculum and funding streams for workforce training centers.

Increase supplier awareness of offshore wind energy opportunities.

Recommended middle-term actions (2025-2030) to gain momentum are:

Construct the major supply chain facilities to meet demand.

Develop and share supply chain best practices.

Incorporate lessons from early OSW projects into operations and decision-making.

Train a manufacturing workforce.

Evaluate procedural and impact equity metrics for early OSW projects and incorporate best-practices into ongoing supply chain development activities.

Recommended longer-term actions (beyond 2030) to maintain a stable industry are:

Update key supply chain infrastructure to adapt to evolving technologies.

Expand supply chain infrastructure to new regions using lessons learned in early projects.

Add domestic production to fill manufacturing gaps in supply chains.

Continue to expand the offshore wind energy pipeline toward a potential 2050 goal of 110 GW installed capacity.

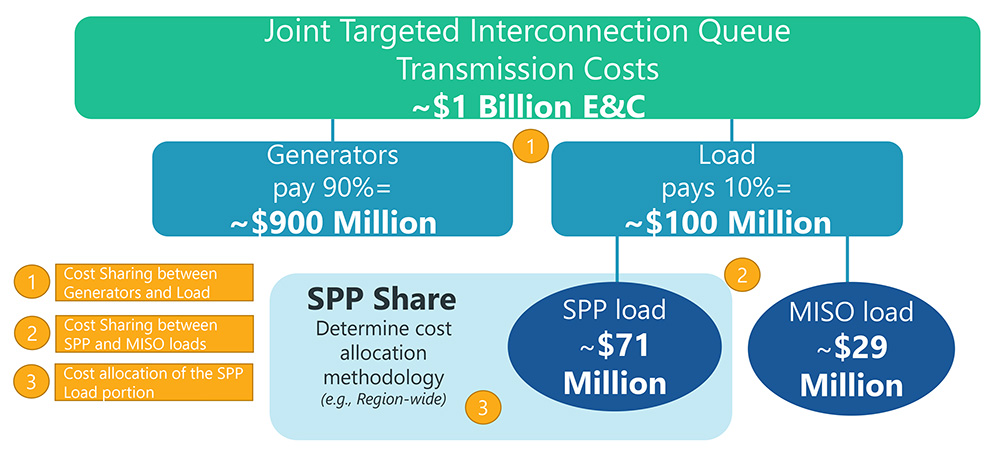

SPP, MISO Applying for DOE Funds to Help with JTIQ Portfolio

OKLAHOMA CITY — SPP told its members last week that it will apply for grants from the U.S. Department of Energy to help fund transmission projects recently identified with MISO along their seam that could unclog their generation interconnection queues.

David Kelley, the RTO’s newly minted vice president of engineering, said DOE’s $10.5 billion Grid Resilience and Innovation Partnerships (GRIP) program aligns neatly with SPP’s Joint Targeted Interconnection Queue (JTIQ) study with MISO.

GRIP, authorized under the Infrastructure Investment and Jobs Act, is designed to accelerate the deployment of “transformative” projects that improve the grid’s flexibility and resilience against the growing threats of extreme weather and climate change. It includes a focus on interregional projects, investments that accelerate the interconnection of clean energy generation, and using distribution assets to provide backup power and reduce transmission requirements. (See DOE Opens Applications for $6B in Grid Funding.)

The JTIQ study resulted in five projects on the MISO-SPP seam that should help reduce congestion and allow additional resources, primarily wind farms, to interconnect with the RTOs’ systems. Their staffs have proposed a cost allocation that assigns most of the portfolio’s $1.06 billion in costs to generation. (See MISO, SPP Propose 90-10 Cost Split for JTIQ Projects.)

“We have still yet to find the magic unicorn of developing transmission along the seams,” Kelley said. “When we looked at [the GRIP] program and what it was intended to do, it almost reads as if it was written for something like what JTIQ was trying to do. It was kind of a no-brainer for us to seek to receive some of this money on behalf of our members.”

Kelley said an initial concept paper has already been filed with the program’s administrators, meeting a Jan. 13 deadline. DOE will review the applications to determine whether they are worthy of full applications, providing that feedback to applicants. Final applications will be due May 19.

Under DOE’s Grid Innovation Program, applications must come from a state or a group of states, regulatory commissions or tribal or local governments. That has led SPP and MISO to collaborate with the Minnesota Department of Commerce and the Great Plains Institute (GPI) on the effort. The state of Minnesota, as a potential eligible recipient of the funds, made the filing. The institute is coordinating the effort by holding discussions with utilities that will build the projects and those utilities and states that will be affected.

“Our job has been to facilitate all potentially affected folks to kind of vet the DOE requirements,” Matt Prorok, GPI’s senior policy manager, told RTO Insider. “How might those be fulfilled? Are [the JTIQ] projects a good fit for this funding bucket?”

The proposed cost allocation for JTIQ projects. | SPP

Kelley pointed out that the GRIP program is a partnership involving federal and private dollars.

“We feel pretty good about it. We’ve talked to DOE a number of times, and they were very interested in what we’re doing here,” Kelley said. “We are being encouraged by what we’re hearing. But again, because this is a partnership, we do think it’s important that we lay the groundwork that not only are we pursuing DOE funds, but that we also have a commitment from SPP, MISO and our customers in our membership that we have the other half of this bill covered.”

Under the staffs’ proposed JTIQ cost-sharing methodology, generators will pay 90% of the portfolio’s cost and load will pay 10%. SPP load will pay about $71 million and MISO load about $29 million, without the DOE funding.

As with any discussion about allocating costs, several stakeholders raised concerns.

“I think all of us are seeing this DOE funding opportunity as a way to facilitate mitigating some of the concerns the stakeholders are expressing and the opportunity for that mitigation to really help make this a success,” the Advanced Power Alliance’s Steve Gaw said. “The second round of that application process, if the application makes it there, will be a very opportune time for additional comments of endorsement.”

The Cost Allocation Working Group (CAWG) on Friday unanimously endorsed and recommended that the Regional State Committee approve the 90-10 allocation. It also recommended that:

the 10% load portion of the JTIQ’s annual transmission revenue requirement (ATRR) be based upon adjusted production costs, as outlined by the RTOs’ joint operating agreement;

the load portion of the portfolio’s ATRR be regionally allocated on a load-ratio share basis consistent with previous RSC policies;

each building transmission owner recover the non-capital cost component allocable to generation interconnection customers through a formula rate template in the building TO’s region; and

SPP’s load share in the current portfolio and for the next study of the southern party of the MISO-SPP seam be regionally allocated on a load-ratio share basis consistent with previous RSC policies.

The motions all passed unanimously except for the last one, which Louisiana, North Dakota and Oklahoma opposed.

The RSC meets Jan. 30. Kelley said SPP plans to make the appropriate filings after the April round of governance meetings.

“We have to ensure we’re in lock-step with MISO and its processes,” he said.

GI Queue Continues to Expand

The JTIQ work will only result in more generation interconnection requests as SPP staff continue to work on reducing the backlog of requests in its queue.

Kelley said the SPP and MISO queues have grown since the JTIQ work began, with no end in sight.

“While we’ve made significant progress in clearing our existing backlog, there continues to be significant interest in developing new generation, both within the SPP footprint as well as MISO’s,” he said.

The backlog, which once stood at 651 requests and nearly 120 GW, had been reduced to 370 and 68.2 GW, respectively, in mid-December. However, the 2022 study cluster that closed in early January added 53.8 GW of requests, pushing the backlog to about 122 GW.

Many of those requests have yet to be validated by staff, leaving the active queue at 463 requests and just over 88 GW.

“It’ll take a couple of months to evaluate the impact of this cluster. It’s really, really big,” SPP’s Juliano Freitas told members, noting that the 2022 cluster exceeded forecasts by about 10 GW.

He said the new cluster is about 50% solar and 25% wind, in line with the active queue. Solar requests (39.2 GW) account for almost half the queue, with wind requests at 23.1 GW and storage at 12.9 GW.

SPP currently only has about 250 MW of installed solar capacity, said Casey Cathey, director of system planning. “That is kind of our next frontier.”

Freitas said that considering only about 40% of GI requests result in signed interconnection agreements, SPP could add more than 45 GW of capacity by 2028. The grid operator has added 27.7 GW of capacity since January 2017, executing 143 GI agreements.

Members Defer on PRM Deficiency RRs

The committee deferred action on a pair of revision requests related to deficiency penalties by load-responsible entities unable to meet the grid operator’s new 15% planning reserve margin (PRM).

Following late changes to the two requests by stakeholder groups the night before the MOPC meeting began, committee members agreed to wait until a special conference call Friday to consider the change requests. That will give additional time to several stakeholder groups who have yet to approve the proposed revisions; the committee will then be able to endorse a recommendation for the RSC and the Board of Directors when they meet next week.

SPP is hopeful FERC will approve the revision requests in time to accredit resources for the summer.

Staff have been working on the mitigation strategy at the board’s direction since July. It became necessary when the board increased the PRM from 12% to 15%, effective next year, which left some members complaining they would not have enough time to meet the requirements. (See SPP Board of Directors Briefs: Dec. 6, 2022.)

COO Lanny Nickell has said the mitigation concepts include reducing the deficiency payment charge, extending the timeline to cure deficiencies and adding mechanisms to assure capacity.

RR536, proposed by SPP’s Market Monitoring Unit, would replace the sufficiency valuation methodology’s current penalty framework with a sufficiency valuation curve similar to the curve that NYISO uses to value capacity in its market. The curve starts at twice the cost of new entry (CONE) until regional accreditation reaches the sum of total noncoincident peak loads, then slopes downward to a net CONE value when regional accreditation reaches the PRM.

When accreditation exceeds the PRM, the curve continues its downward slope until it reaches $0 when regional accreditation reaches 1.15 times the PRM. By focusing on how valuable excess accredited capacity is to the market given the regional level of accredited capacity, this methodology shifts from a punitive approach to a tool that manages the current deficiency and properly rewards LREs with excess accredited capacity.

Staff worked with the MMU on RR536 and also drafted RR537, which clarifies that an LRE making the deficiency payment will be sufficient for this year’s resource adequacy requirement. It also says that any entity receiving a deficiency payment cannot subsequently sell any of the excess capacity during the applicable calendar year.

“I think we’re getting closer. Today is too soon, given the language was only provided last night,” Evergy’s Mo Awad said. “I would like to take some time and review the language.”

Staff drew up a number of issues for stakeholder consideration, including clarifying that the waiver process is only in effect when the PRM increases; the timing of when generation must be committed to SPP, based on a deficiency megawatt amount; how the cost of new entry is broken into seasonal components; and simplifying megawatt allocation for the MMU’s CONE process.

The Supply Adequacy and Regional Tariff working groups will take up the revision requests on Tuesday and Thursday, respectively. The CAWG met Friday but did not vote on them; it has scheduled a special meeting for Wednesday.

December Storm Raises Same Issues

Staff told the committee that the December winter storm, while less severe than the February 2021 storm that forced the grid operator to shed load for the first time, still highlighted some of the same issues from two years ago.

C.J. Brown, director of system operations, said constricted fuel supplies and extreme cold weather-related outages led to some generation unavailability as surface temperatures in the SPP footprint were up to 25 degrees Celsius below historical averages.

Staff began receiving notifications on Dec. 20 from natural gas suppliers that non-firm usage of pipelines would be limited through Dec. 28. Ice floes on the Missouri River threatened several gigawatts of hydro generation, and the RTO’s main control room operated on backup power during the event after the facility’s transformer malfunctioned.

Empire Electric District and City Utilities of Springfield, Mo., near the Missouri-Arkansas border, experienced extremely low voltages on Dec. 23 caused by resource trips, lack of deliverability and parallel system flows. Empire had to shed about 25 MW of load for 15 minutes on Dec. 22.

Still, SPP was able to meet a peak demand of 47.2 GW on Dec. 22, a winter record.

Brown said that if the worst weather conditions had shifted to Dec. 23 or Dec. 24, SPP would have had 2 to 5 GW of capacity at risk.

“It doesn’t mean we would have had load shed,” he said, noting that the RTO could have reached energy emergency alert levels. “None of us want to be in a headline that says we shed load over Christmas. We need to get better information” from gas suppliers.

Midwest Energy’s Bill Dowling cautioned SPP about taking comfort in the amount of gas generation it committed before the cold front blew in.

“It’s one thing to know that [a gas unit] is committed a couple or three days in advance; … it’s something else to get the gas,” he said. “If the gas producers aren’t producing and it doesn’t show up in interstate pipeline, you’re not going to get it, I don’t care how much you paid for it.”

Josh Phillips, who represents SPP at the North American Energy Standards Board, said the board’s Gas-Electric Harmonization Forum is preparing a report on three main areas of concern during extreme weather events: fuel delivery assurance, communication practices and gas reliability.

Power generators and load-serving entities are underrepresented on the forum, Phillips said. He urged more industry participation as the final report delves into whether there’s a need to require every gas generator to have firm gas supply and transportation contracts.

Dowling said that whenever he listens to discussions between the electric and gas sectors, “it ends up, ‘This is your problem, electricity, so you have to change to meet our requirements.’”

“If [gas suppliers] declare force majeure, you just don’t get your gas,” said long-time MOPC member Bill Grant, now consulting for XO Energy. “The NAESB agreement needs teeth if they don’t perform, that’s the answer.”

Brown said staff will complete its post-event review and gather lessons learned, while also participating in the FERC-NERC joint inquiry on the storm. They will continue to support resource adequacy efforts through the RSC and other stakeholder groups.

Members Endorse ITP Scope, STEP

The committee endorsed two stakeholder groups’ recommendation to approve the 2024 Integrated Transmission Plan’s scope, which includes assumptions not standardized by the ITP manual.

The assessment will study two futures — a reference case and an emerging technologies case — that assume between 49.9 and 54.9 GW of wind resources and between 14 and 22 GW of solar resources by Year 10. SPP currently has 32.5 GW of installed wind capacity and 14,000 turbines on its system, but only about 250 MW of solar, Cathey said.

The scope also includes peak and energy increases in both futures to account for electric vehicle growth and an approved methodology for retirements based on participants’ resource plans. Staff used those plans to also determine wind, solar and storage capacity amounts. The study scenarios will assume all companies meet the PRM.

“We believe the two futures capture the necessary scenarios for building out the transmission system,” Cathey said.

The committee also endorsed the SPP Transmission Expansion Plan (STEP), a comprehensive list of all transmission projects over a 20-year planning horizon. The report indicates that SPP members completed eight upgrade projects costing more than $40 million from last April to year-end. SPP issued 76 notifications to construct (NTCs) for $822 million during the same period; 12 NTCs were withdrawn.

Cathey reminded the committee that the 2022 ITP assessment was a reliability-only study, thus resulting in a smaller portfolio.

RAS Scheme Passes

The committee unanimously approved a consent agenda that included eight revision requests; an extension of the Transmission Owner Selection Process Task Force’s sunset to Jan. 31, 2024; a waiver request to include the 2023 ITP needs assessment’s market powerflow models (MPMs) and consider the 2023 ITP MPM violations in the 2024 ITP; and a sponsored upgrade study of NextEra Energy’s proposal to add a 345/138-kV transformer at Oklahoma Gas & Electric’s Cimarron substation.

Nebraska Public Power District had RR505 pulled off the agenda for a separate vote, over concerns that the remedial action scheme (RAS) criteria would lead to unintended consequences. The change would supplant the need for approval conditions and clarifies RASes’ appropriate uses. Members approved the revision request with a 95% vote.

Five other RRs, if approved by the Board of Directors next week, would:

RR519: formalize the SPP operating criteria’s requirement to perform an annual resource real-time availability evaluation and report findings and recommendations to appropriate stakeholder groups.

RR522: clarify the use of the word “separately” (“Each facility must be registered separately with SPP…”) to direct parties in the agreement to register each facility separately when they have multiple resources involved with the pseudo-tie agreement.

RR523: modify existing pro forma generator interconnection agreements and language to provide a clearer indemnification standard with clearer language. The changes are modeled on PJM’s interconnection service agreement.

RR526: specify that a resource or an aggregation must be able to maintain a response of at least 0.1 MW for at least an hour to participate in the Integrated Marketplace; if the anticipated response drops below 0.1 MW, the resource must set its commitment status to “outage,” consistent with recent FERC orders and SPP’s current process.

RR528: clean up Business Practice 7060 by using “evaluation” rather than “study” for projects that have been issued an NTC, aligning the term with how it is used when an NTC is re-evaluated through the ITP.

The consent agenda also included two other RRs that don’t require board approval and go into effect immediately:

RR525: deletes Business Practices 7100 (Designated Transmission Owner Qualification Process) and 7150 (Transmission Owner Selection when a Designated Transmission Owner Rejects a Notification to Construct), which became obsolete with the implementation of SPP’s competitive transmission selection process.

RR529: the annual cleanup to correct grammar, punctuation and acronyms in the production and/or forward looking protocols.

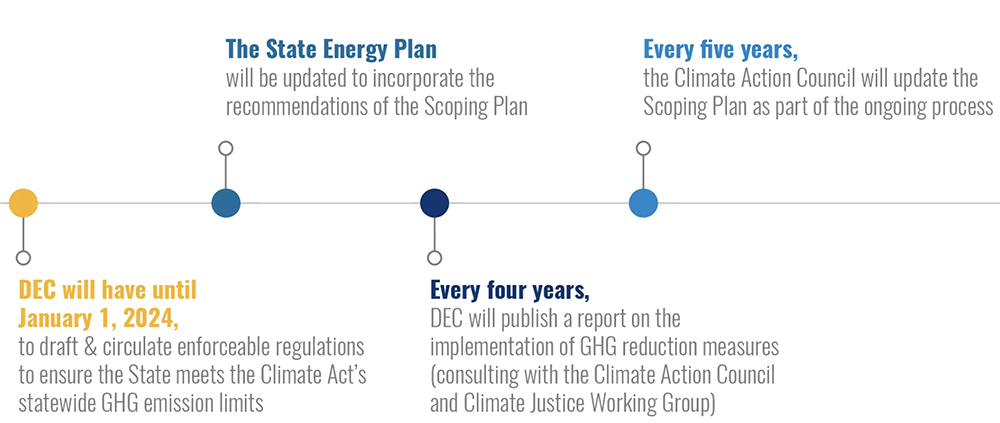

Members of the New York Climate Action Council continued their debate over the future of natural gas at a New York Senate hearing last week on legislative and budgetary actions needed to implement the CAC’s final scoping plan.

More than two dozen witnesses testified at the Jan. 19 joint hearing of the committees on Finance, Energy and Telecommunications, and Environmental Conservation. Sen. Liz Krueger, chair of the Finance Committee, helmed the joint session, saying “this is the most important issue that New York State must get its arms around.”

CAC Member Testimony

CAC members shared their thoughts on protecting ratepayers and revising tax codes in addition to defining the role of natural gas.

Donna L. DeCarolis, president of National Fuel, said mandatory dates that “effectively mandate electrification of homes and businesses without the assurance of identified reliability milestones should be rejected.”

New York “should unlock consumer benefits of alternative fuels, particularly RNG in the near term for immediate emissions reductions and hydrogen in the longer term,” as well as conduct a “quantitative analysis of all costs associated with the various emissions reduction initiatives identified in the scoping plan,” DeCarolis said.

Raya Salter, executive director of Energy Justice Law and Policy Center, told lawmakers “we must, leading with justice and equity, act on climate now, and that means closing the state’s fossil fuel plants and moving away from the combustion of fossil fuels.”

Bob Howarth, a professor at Cornell University, argued New York should restore earlier deadlines from the draft scoping plan and repeal laws that subsidize natural gas utilities.

Gavin J. Donohue, CEO of the Independent Power Producers of New York, cautioned “against legislative action that would increase consumer costs, jeopardize the benefits they are receiving from competitive wholesale electricity markets, and harm the reliability of power supplies.”

Donohue told lawmakers to also heed NYISO’s reliability warnings and conduct a “comprehensive ratepayer cost impact analysis.”

Preserving “existing renewable energy facilities and retaining and expanding other non-emitting facilities” is as important as attracting new resources, he said.

Anne Reynolds, executive director of the Alliance for Clean Energy New York, shared recommendations aligned with the group’s recently released legislative priorities, including tax breaks for renewable developers, policies supporting a cap-and-invest program, and expanding transmission capacity. (See ‘Environmental Expectations,’ 2023 Preview of NY Legislature on Energy and Environment.)

Additional Testimony

Other stakeholders provided suggestions, including passing new decarbonization legislation, adjusting the tax code, and increasing the availability of clean energy development programs.

Brian Schultz, CEO of Central New York Regional Transportation Authority, advised legislators to “allow flexibility to consider renewable natural gas and hydrogen energy sources as alternative means for further decarbonizing” and asked that legislators “avoid overly prescriptive legislation with unfunded mandates and unrealistic timelines.”

The Real Estate Board of New York (REBNY) said policymakers should “prioritize creating a set of achievable, predictable, and efficient standards for the building sector.” Failing to do so, it said, would “add unnecessary compliance costs and make it less likely that the state’s goals are achieved.”

Next Steps for New York’s Scoping Plan | Climate Action Council

REBNY suggested the legislature “create a tax abatement and incentive program for investments in building greenhouse gas emissions reduction” to encourage greater investment in decarbonizing the building sector.

Consolidated Edison (NYSE:ED) said legislators should allow utilities to own and operate renewable generation assets, and “increase clean heat and energy efficiency programs and allow for accelerated depreciation of gas assets.”

The company also called for property tax changes, saying the current system is regressive and discourages electrification of heating and transportation.

Raziq Seabrook, government relations manager at National Grid (NYSE:NGG), said the utility identified four policies to help with implementing the scoping plan: accelerate electric system modernization; expand energy efficiency programs; decarbonize buildings and industry through innovative clean energy options; and promote energy affordability.

Avrielle Miller, policy coordinator at NY Renews told the committee members they need to pass the Climate, Jobs & Justice Package to ensure “40% of the state’s clean energy benefits go to disadvantaged communities, create unionized jobs, lower utility bills, and protect our air and water.”

Betta Broad, director at the Association for Energy Affordability, testified that implementation would be assisted by passing the New York Home Energy Affordable Transition (HEAT) Act — formerly known as the Gas Transition and Affordable Energy Act — and creating programs that expand clean energy career pathways.

Next Steps

The committees will now break into their respective sessions, using recommendations from the joint session to draft bills that will implement the scoping plan.

In October, CAISO, ISO-NE, MISO, NYISO, PJM and SPP filed reports with FERC on how their system needs are changing in response to decarbonization and their shifting resource mixes (AD21-10). Last week, 19 groups and companies filed comments responding to the RTO/ISO reports.

Below is a summary of how the grid operators say they are working to ensure reliability and what the commenters think of their plans.

CAISO

CAISO told FERC its system needs are changing in response to the state’s 100% clean energy by 2045 mandate under Senate Bill 100.

“CAISO is actively engaged in addressing the evolving resource mix, an evolving market, and a growing recognition that regional coordination is necessary to enhance efficiency and reliability,” it said, adding that “weather patterns affected by climate change have created extreme conditions beyond those anticipated by current planning standards.”

One way CAISO is addressing its needs is with large amounts of battery storage to provide power during hot summer evenings after solar goes offline but air conditioning demand remains high. The ISO ordered rolling blackouts in August 2020, and had near misses in the summers of 2021 and 2022, under such conditions.

“The addition of lithium-ion storage capacity has been an extremely positive development,” CAISO said. As of October 2022, the ISO had about 4,300 MW of storage capacity available for dispatch; the California Public Utilities Commission, which is in charge of ordering procurement by the state’s three large investor-owned utilities, has called for 10,000 MW of additional storage by 2024.

Another way CAISO plans to deal with changes in the resource mix and load variability is through its proposed extended day-ahead market (EDAM) for its real-time Western Energy Imbalance Market.

“The EDAM will build upon the proven ability of the WEIM to increase regional coordination, support states’ policy goals and meet demand cost-effectively by supporting the rapidly evolving Western resource adequacy landscape,” CAISO said.

Managing its “unprecedented transition requires us to look very carefully at both the short and the long term,” CAISO said: “short term because we must maintain reliability during the transition to a carbon-free grid, and long term because we must make sound decisions now to help us reach that destination in the most reliable and cost-effective way.”

In February 2022, CAISO published its first 20-Year Transmission Outlook, “a long-term conceptual plan” of the transmission grid based on input from the CPUC and the California Energy Commission.

Its new 5-Year Strategic Plan focuses on what the organization must do in the short term to strengthen reliability during the transition.

To ensure resource adequacy, CAISO said it would rely on the Western Power Pool’s Western Resource Adequacy Program and California’s efforts to evolve its resource adequacy program through advanced computer modeling. “Together with its partners, the CAISO is actively working to develop a multiple-year roadmap that relies on its markets to provide reliable system operations in light of the changing nature of resources and load patterns throughout the West,” it said.

In comments filed last week, the American Petroleum Institute cited CAISO’s experience during strained conditions as a reason natural gas generators’ fast-ramping capability are needed. California continues to rely heavily on gas generation, especially at times when solar is unavailable.

“CAISO, which has the highest share of solar generation of the six ISO/RTOs, has already observed an increase in uncertainty around its net load forecasts,” API said.

“As the share of non-dispatchable resources grows, it can become difficult to guarantee that generation will be available when needed — particularly when resources with flexible attributes are either forced into retirement or not developed in the first place due to market, regulatory or legislative headwinds,” it said. “California faced such an issue in August 2020, when insufficient fast-ramping resources were available to compensate for the evening decline in solar generation and CAISO was forced to shed load on consecutive days. As former FERC Commissioner Tony Clark concluded in a recent opinion piece, ‘On-demand resources may not run as often in a renewables-heavy future, but the value of their ability to run when called upon will be critical.’”

CAISO monthly trend of historical day-ahead imbalances, which can exceed 6,000 MW, requiring large amounts of reserved capacity | CAISO

Advanced Energy United (formerly Advanced Energy Economy) offered its thoughts last week on several parts of CAISO’s submission.

“CAISO predicts that ‘artificial intelligence and machine learning will play an increasingly important role as the energy industry continues its trend towards more complex and distributed systems,’” the group said. “Given the foundational role of software in supporting critical RTO/ISO functions, the commission should work to track RTO/ISO software needs and upgrades and look for ways to support expedited software upgrades and use of new and emerging tools and practices.”

Advanced Energy endorsed CAISO’s recommendation that the commission “continue to facilitate industry dialogue regarding the coordination between the transmission and distribution interface.”

“This is especially critical in light of the trend mentioned by multiple RTOs/ISOs toward increased electrification of transportation and heating; ensuring that these end uses can be leveraged as a grid resource rather than simply adding a new source of load for grid operators to balance will be essential to maintain affordability and reliability in light of shifting system needs.”

ISO-NE

ISO-NE said it recognizes its energy systems are in the “early stages of a significant shift” caused by electrification and decarbonization goals in the six states of New England.

Among the changes that ISO-NE is preparing for are increasing winter peaks in the next five years, and the potential for a full-blown shift to a winter-peaking system in the next 10.

The grid operator said it expects to need “additional resource physical capabilities, ISO informational capabilities and markets’ capabilities to incent the former,” over those time frames.

ISO-NE cited what CEO Gordon van Welie has called the “four pillars” of New England’s energy future: clean energy, balancing resources, energy adequacy and transmission investment. It stopped short of making any specific asks of FERC, but called on the commission to remain flexible in its approach to overseeing RTOs.

New England’s emission reduction goals | ISO-NE

“We look forward to continued efforts by the commission to remain responsive to the evolving resource mix and load profiles of individual RTO/ISO regions, and any related future market reforms that the evolving energy system may motivate,” the RTO said.

Four public power systems from Massachusetts, Connecticut, New Hampshire and Vermont called on FERC and ISO-NE to continue to focus on reliability, saying, “New England today is facing profound winter reliability issues that require swift action.”

Specifically, the groups wrote that FERC should mandate the use of competitive processes in transmission development, take a closer look at New England’s rules for fuel procurement and consider creating a regional energy reserve. They also urged a major revamp of ISO-NE’s capacity market, calling for a seasonal auction to replace the existing annual one.

They also said ISO-NE should look at new market products to incentivize building balancing resources and commit to undertaking cost-benefit analyses as it evaluates changes to market rules.

MISO

MISO said adapting its markets to reliably meet future system needs has been “core to MISO’s mission and vision” since it introduced its energy market in 2005.

The grid operator cited its plan to use a seasonal accreditation of capacity, the opening of its markets to electric storage and the 2021 rollout of its short-term reserve product. It also said its long-range transmission portfolios and its ongoing market platform replacement are meant to keep the system nimble.

MISO also cited analyses such as its “Markets of the Future” report and annual regional resource assessment as ways to keep close tabs on its evolving resource mix and anticipate what new market products might be needed.

Policy drivers are accelerating the fleet transition and associated risks, MISO says. | MISO

The RTO said it considers market pricing “a powerful signal” to attracting resources. In its “ideal state,” it said, it would remove the requirement that it must declare an emergency to access its load-modifying and other “emergency only” resources and be able to commit and dispatch them “through more regular market operations.”

MISO has begun discussions with stakeholders on how to appropriately value and maintain resources that supply beneficial system attributes. It has defined six system reliability attributes as necessary, including resource availability, the ability to deliver long-duration energy at a high output, rapid start-up times, providing voltage stability, ramp-up capability and fuel certainty. (See MISO Considers Resource Attributes as Thermal Output Falls.)

NYISO

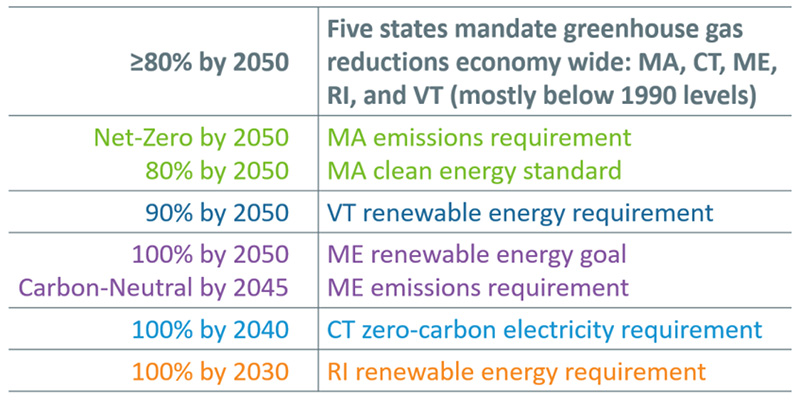

NYISO said it is simultaneously responding to more frequent extreme weather and higher temperatures caused by climate change and the renewable requirements of the Climate Leadership and Community Protection Act (CLCPA). Reaching the CLCPA’s targets — 70% renewable electricity by 2030; 100% emissions-free electricity by 2040 — “will require unprecedented levels of investment in both new supply and transmission resources.”

The ISO’s 2020 Climate Change Impact and Resilience Study said it could be facing one-hour ramp requirements of more than 10,000 MW and a six-hour ramp of more than 25,000 MW by winter 2040. In 2021, in contrast, the ISO’s maximum one-hour ramp was 1,800 MW, and the largest ramp was 8,800 MW.

NYISO said it faces uncertainties including “weather, net load forecasts, actual available energy from intermittent wind and solar resources, available energy from limited-energy resources, reduced availability of traditional flexible generation resources and higher probabilities that weather, or other factors, lead to correlated supply and transmission issues.” In July 2019, it experienced a 36-hour period when the state’s wind resources produced only 4% of their maximum output.

The ISO identified six time frames in which it must balance the variance in intermittent resources, ranging from six seconds (for regulation service) to decades — the time horizon over which investments in resources able to provide balancing will be made.

Progress toward New York’s “70 x 30” mandate | NYISO

NYISO told FERC its energy and ancillary services markets are “working efficiently,” citing its operating reserve demand curves, which were changed in 2021, and stakeholders’ recent approval of its constraint-specific transmission shortage pricing project. The latter project is intended to help its market software redispatch suppliers to alleviate transmission constraints and identify locations where new resources could provide the greatest benefits.

“The upcoming balancing intermittency project and the initiative to review real-time market features to enhance incentives to follow NYISO instructions directly respond to expected ramping and flexibility needs,” it said. The real-time project will consider lengthening the look-ahead capabilities of the ISO’s real-time commitment and real-time dispatch software.

It acknowledged that the low marginal costs of renewables will require changes to the markets to balance intermittency and improve price formation.

“Determining the quantity and location of operating reserves more dynamically will be instrumental in preparing the markets for the new grid risks as the resource mix evolves.”

Simultaneously co-optimizing energy and ancillary services requirements will increase revenues in those markets, the ISO said. “Absent ancillary services market changes or other wholesale energy market changes to improve incentives for flexible resource availability, market signals to retain and invest in flexible, controllable resources may not be sufficient.”

Another source of uncertainty is behind-the-meter solar PV. The ISO forecasts that 6,000 MW of BTM solar nameplate capacity will be installed by 2024, rising to 10,000 MW by 2030.

The ISO and its stakeholders are considering additional changes, including the implementation of reserve requirements within constrained load pockets; additional availability incentives for suppliers on Long Island; five-minute transaction scheduling; and separating up and down regulation service.

In response to Commissioner Mark Christie’s question on whether LMPs remain the best way to run energy and capacity markets, the ISO attached to its filing a report by economists Scott Harvey, of FTI Consulting, and William Hogan, of the Harvard Kennedy School.

Harvey and Hogan rejected those who question whether LMPs still make sense in a world of low-marginal-cost variable resources. “The critical role for LMP was true in the past, is true today, and will be true and more important with the anticipated changing resources mix,” they wrote.

PJM

PJM aims to meet the challenges presented by growing renewable penetration and electrification by expanding its energy and ancillary services market to include pricing of flexibility attributes. In its report to the commission, the RTO said many of the characteristics of dispatchable generation will be crucial through the clean energy transition — such as the ability to ramp, cycling capability, quick start times and low minimum run times.

“A significant challenge PJM faces over the next five to 10 years is the disorderly retirement of resources that provide needed ancillary services,” the RTO said. “The limitations in how these resources are priced today could well add to the premature and disorderly retirement of these needed resources that are not priced accurately in today’s markets.”

While the RTO believes it has adequate flexibility in the near term, it said it must create defined values for attributes as quickly as possible to incentivize generation owners to keep their facilities online.

“The value in addressing this issue now is that prices for this additional flexibility will rise slowly as the fleet transitions and send early price signals on the increasing value of flexibility. This is critical to avoiding the disorderly retirement of resources,” PJM wrote.

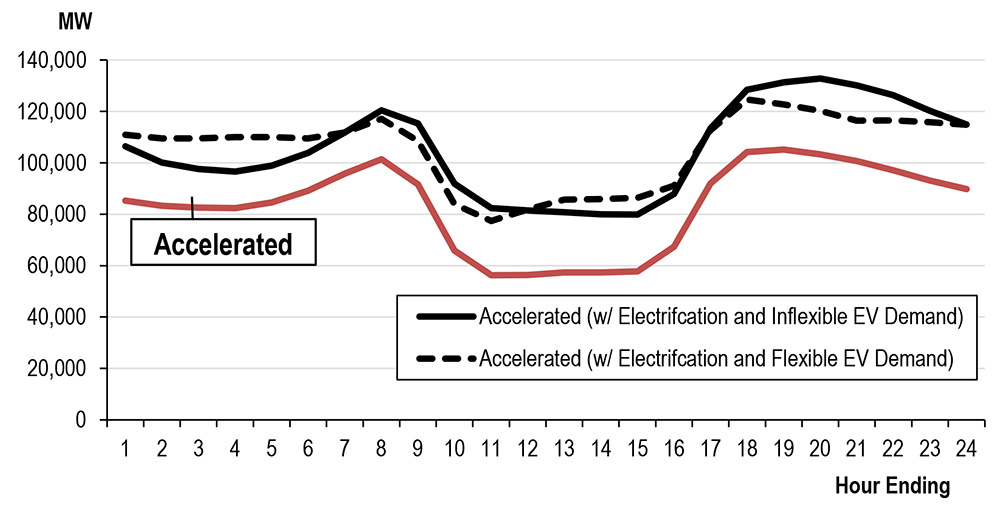

Winter load shape with electrification | PJM

The RTO urged the commission not to take a “passive stance.”

“A policy statement outlining the commission’s expectations would help to focus RTOs and their stakeholders on these issues at a time when there are countless issues that could distract from their development,” it said. “Moreover, such a policy statement, if adopted on a bipartisan basis, could ensure a level of continuity in the commission’s direction that would further incent the industry to move proactively.”

PJM’s Independent Market Monitor argued that the RTO’s core market design elements already provide the flexibility it will need going into the future. It said the focus should be on removing existing barriers rather than creating new market products.

“Creating new ancillary services products and repeatedly revising the existing ones is a distraction from identifying opportunities to improve dispatch tools and enhancing basic market rules to unlock existing resource flexibility,” the Monitor wrote in response to PJM’s filing.

Current market rules often allow resources to avoid defining their flexible operating parameters outside of instances where they fail the market power test, or during weather alerts and emergencies, the Monitor said. For example, combined cycle units have the physical capability to be dispatched on and off for morning and afternoon peaks, and typically do not offer their start and down time parameters on their price schedules.

The IMM also said “inferior capacity resources” that are exempted from must-offer rules — namely intermittent generation, storage and demand response — are undermining the reliability offered by PJM’s capacity market.

The PJM Industrial Customer Coalition said that the RTO must ensure that load is not responsible for resources that cannot meet their obligations.

“Currently, load is fully responsible for the payments associated with the reserve products in PJM. If certain resources are not able to meet their reserve obligations due to the intermittency of those resources or for other reasons, those resources should bear an appropriate cost; the full risk and costs should not be borne directly by consumers,” the coalition wrote.

The ICC also argued that all generation types carry some physical flexibility and that they should be required to offer that capability to grid operators. Those resources that cannot provide a range for its flexibility or fail to follow dispatch instructions should be obligated to purchase flexibility from other resources or their respective RTO, it said.

“Resources that cannot provide desired flexibility and dispatchability attributes should appear more costly and less desirable than resources that can provide the desired attributes. As a result, the mantra of ‘reliability through markets’ would continue to be fostered through proper investment signals,” it wrote.

The PJM Power Providers Group (P3) noted that the RTO is forecasting strong load growth as thermal resources are scheduled to retire. It argued that the renewable resources expected to go online are not a “megawatt-for-megawatt” replacement for those going offline, particularly as risk moves to the evening hours.

To address the reliability challenges expected in the future, P3 said that an overhaul of the capacity market is necessary to undo “myopic regulatory decisions from the commission, illogical proposals from the RTO” and delays in running auctions. P3 said the current market is unsustainable, with resources exposed to nonperformance charges during extreme weather, no ability to independently evaluate risk and no protection from buyer market power.

SPP

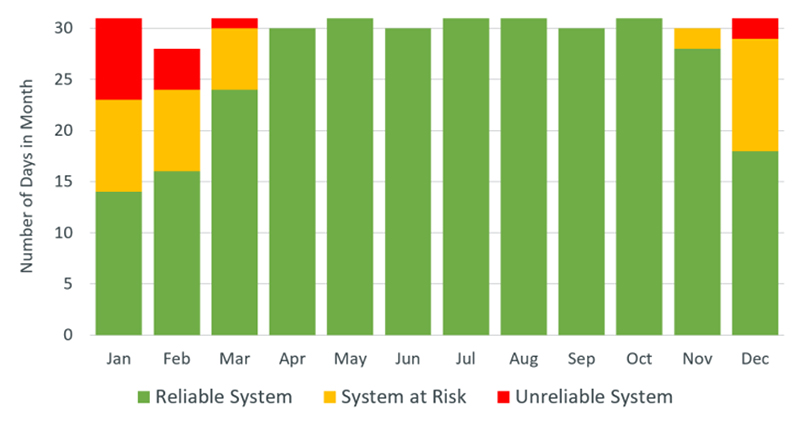

SPP’s report documented the RTO’s response to the rapid growth in wind energy and its increasing peak demand.

The RTO’s 33 GW of installed and registered wind power capacity represents 29% of its total capacity and 38% of its total energy. It also has seen a continued drop in coal generation, although rising natural gas prices allowed its usage to rebound in 2021.

Because of rising high temperatures, the RTO said, its coincident instantaneous peak demand has risen more than 7% in two years, from 49,569 MW in 2020 to 53,243 MW in July 2022.

Share of SPP’s real-time, annual generation by technology type | SPP

It also reported increasing uncertainty in load forecasting because of demand response and behind-the-meter generation. “SPP receives load forecasts from its members that inform SPP’s own load forecasts, and these load forecasts may be performed differently,” it said.

It has also seen increased generation variability, which it manages through reliability unit commitment studies and manual operator commitments and its new ramp capability product.

“SPP’s primary source of uncertainty comes from generation, not from load,” it said. “With the balance between available flexibility and system variability expected to tighten in the future, efficient methods to assist in providing the needed flexibility with the available generation fleet will become increasingly important to economical and reliable operations.”

The RTO said its requirement is for resources that are “visible, forecastable and responsively dispatchable.”

It recently revised its balancing authority emergency operating plan to incorporate information on generators’ on-site fuel and the ability of the BA to allow resources to take actions to conserve fuel. The RTO is also tracking plant retirements based on owners’ plans instead of making assumptions based on plants’ age.

SPP said it will need more information from its 550 distribution utilities as additional resources interconnect on distribution lines.

Another concern is the increasing complexity of the system, which is making it more difficult for software to clear, solve and post the results of SPP’s market in a timely fashion.

“The SPP market clearing engine has to optimize an extensive mathematical model (greater than 1,000 resources, large amounts of transmission constraints over a large footprint, granular modeling),” it said. “The potential addition of thousands of distributed energy resources, storage, greenhouse gas logic and continued variable energy resource growth could require adjustments to how SPP clears the market.”

SPP said it has an increased need for visibility of resources. “This means knowing where resources are on the system and forecasting their output. Visibility concerns arise with increasing numbers of distributed energy resources and behind-the-meter generation. This generation may not be registered in SPP’s markets and may be accounted for differently in the load forecasts of distribution utilities connected to the transmission system operated by SPP,” it said.

“Another potential problem with resource visibility is the potential for mobile storage resources (both plug-in vehicle and commercial-size truck bed storage) within SPP’s footprint. This possibility may be more likely as new electric charging stations along interstate highways come online.”

“Renewables have not caused any new problems but have only highlighted the shortcoming of the market,” SPP’s Market Monitoring Unit said in its comments last week.

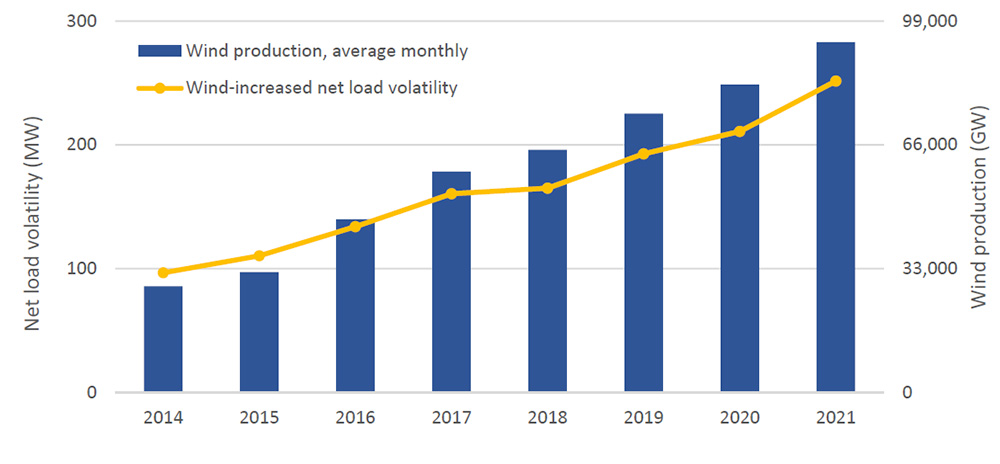

Net load volatility increases with wind production. | SPP

The MMU said the RTO needs to construct its rules with an eye to “flexibility, dependability, availability, resiliency and quality.”

“These attributes must be defined and incentivized, or they may not be provided in the future,” the MMU said.

The MMU noted that wind’s market share has nearly tripled from 2014 to 2021 to about 35% of total annual generation. Compounding the challenges, in about half of all real-time intervals, wind production moves in the opposite direction of load, it said.

“Although almost all weather-dependent renewables are dispatchable in the down direction, they were expected to follow dispatch instructions in less than 7% of resource intervals, compared to about 80% for non-renewables.

“When not following a dispatch instruction, weather-dependent renewable output varies irrespective of price, causing a need for rampable capacity separate from load.”

Almost 36% of capacity in SPP is more than 40 years old, most of it gas and coal.

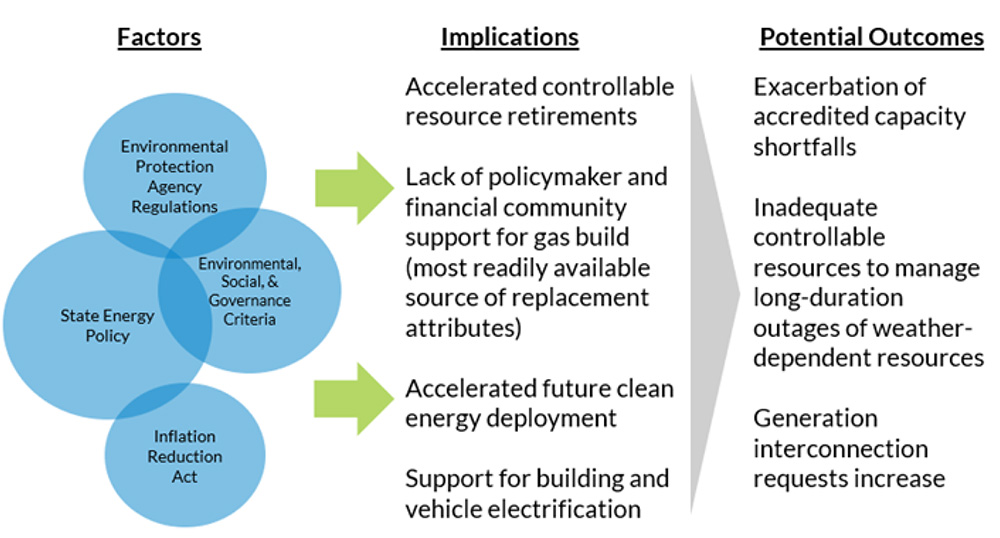

RTO stakeholders last week presented FERC with a cornucopia of suggestions for dealing with electrification and the increasing penetration of variable resources, some supportive of grid operators’ actions, others calling them discriminatory.

On Thursday, 19 groups and companies filed comments responding to the RTOs’ reports, which were filed in October (AD21-10).

Most of last week’s responses supported FERC’s position that it would not propose a “generic solution” across the RTOs/ISOs because of the diversity of the regions’ generation mixes. But several commenters said the commission should provide guidance to RTO efforts to develop new products and market rules.

After four technical conferences in 2021 and dozens of comments, the commission has built a large record in the wide-ranging docket, which included discussions of resource adequacy, interregional planning, NERC reliability standards and distributed energy resources.

The only commission actions to come out of the fact-finding thus far have been orders to essentially eliminate the minimum offer price rule in PJM and ISO-NE. Those votes came with a 3-2 Democrat-controlled commission. With the Jan. 3 departure of Chair Richard Glick, Acting Chair Willie Phillips and Democrat Allison Clements will be unable to approve any rule changes without winning over Republican James Danly or — more likely — Mark Christie.

Deference vs. Standardization

The Edison Electric Institute said FERC should defer to the RTOs. “It is critical that RTOs and ISOs be allowed to identify issues and propose solutions to changing system needs through their stakeholder processes,” EEI said. “It is especially important that the commission allow the existing reform efforts described in the RTO/ISO reports to play out.” EEI also urged the commission not to consider action on interregional transfer capability in the docket, saying docket AD23-3, the subject of a FERC workshop in December, was a more “appropriate” venue. (See FERC Considers Interregional Transfer Requirements.)

In contrast, the American Clean Power Association, American Council on Renewable Energy and the Solar Energy Industries Association — filing jointly as “Clean Energy Associations” — called for standardization across RTOs. “Competition in the markets will be improved if the RTOs/ISOs adopt common terms, products, protocols, and review measures,” they said.

Constellation Energy (NASDAQ: CEG) said ISO-NE could use FERC guidance in designing operating reserves and related products, citing the RTO’s statement that it is difficult for RTOs and their stakeholders “to make progress … in the absence of proactive guidance from the commission.”

Shell (NYSE:SHEL) — which owns Shell New Energies U.S., developers of the Atlantic Shores and Mayflower Wind offshore wind projects, and Savion, a utility-scale solar and energy storage developer — said FERC “must provide an overall framework to both ground and discipline RTO/lSO efforts to ensure reliability is maintained” in light of state actions to address climate change.

Revenue stack comparison: Most of solar resources’ revenues comes from environmental attribute markets and energy markets. | Shell

“Addressing one-off questions on a stand-alone basis — such as whether locational-based marginal pricing for energy markets can continue; whether co-optimized ancillary service markets with opportunity cost pricing will deliver the right resources; or even whether capacity markets serve as the right platform for providing the ‘missing money’ needed to meet resource adequacy challenges — will be woefully insufficient,” it said. “Issuing a policy statement that defines general principles without prescribing set solutions will provide cohesion but permit the necessary flexibility for each RTO/ISO to efficiently and effectively meet its respective regional needs.”

Advanced Energy United, formerly Advanced Energy Economy, said FERC should “engage critically” on the issue of capacity accreditation and “proactively engage on flexibility” through new energy and ancillary service products and evaluation of existing market rules.

The group also called for the commission to finalize its rulemakings on transmission planning, cost allocation and generator interconnection; complete rulings in Order No. 2222 dockets on removing barriers to DERs and look for ways to increase the roles of DERs and flexible demand; and improve wholesale-retail coordination.

Generation Dispatch

Constellation said RTOs should be more transparent about their out-of-market actions.

“There is little understanding — by the market participants who are most affected — of RTO out-of-market actions such as manual unit commitments, posturing and load biasing; the frequency or magnitude of these activities; the circumstances that necessitate them; or, importantly, how these ‘practice[s] … affect … rates,’” it said. “Most of these out-of-market actions are taken in control rooms and are hidden from market participants.”

The Clean Energy Associations called for increased use of probabilistic unit commitment, saying it would produce more efficient, lower-risk operations. “For example, if forecasts indicate a significant chance of both very high load and very low renewable output, operators will likely want to commit more resources. However, because those risks are not reflected in the median value for either forecast, current deterministic methods do not automatically incorporate them into commitment decisions, forcing operators to attempt to subjectively incorporate them.”

Capacity Markets, Ancillary Services

R Street Institute called for less reliance on capacity markets and more demand-side participation, which it said is “chronically underutilized.”

“The most efficient and accurate price signals come from energy and ancillary service markets, where the reflection of actual conditions occur on a granular basis, unlike the more administrative constraints at broader estimation of transmission constraints in capacity markets,” it said.

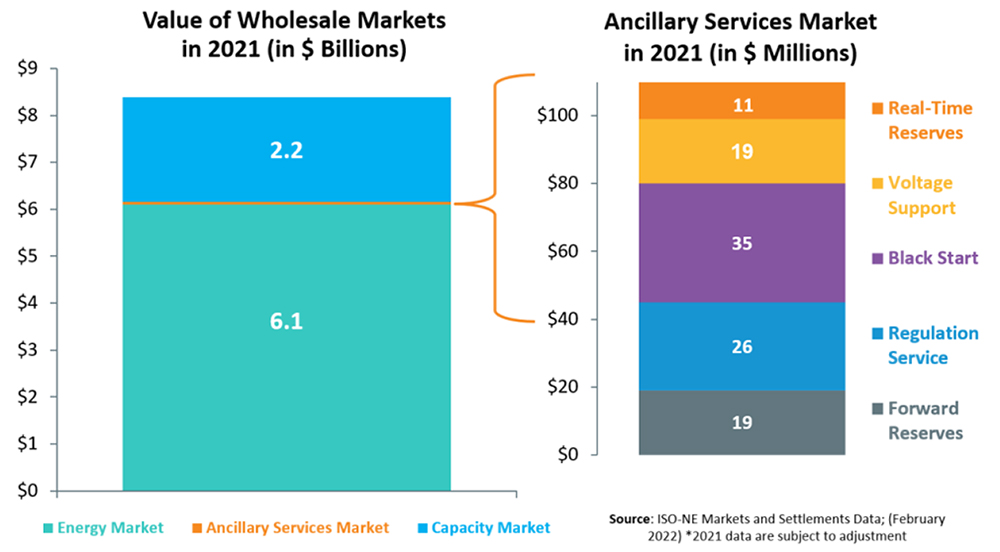

ISO-NE’s markets for ancillary services represent only $110 million in 2021, compared to $8.4 billion of overall wholesale electricity market costs that year. | ISO-NE

Environmental groups, including Earthjustice, Natural Resources Defense Council, Sierra Club, Sustainable FERC Project and the Environmental Defense Fund, also called for more demand-side solutions. “Resources such as demand response, electric storage and distributed energy resources can go a long way to ameliorate the resource adequacy shortfalls that some of the RTOs/ISOs complain of in their reports.”

The Clean Energy Associations cited PJM in calling for “reducing over-procurement of capacity,” and urged the commission hold a dedicated technical conference on capacity accreditation.

Groups filing as the “Clean Energy Associations” complained PJM’s capacity market has resulted in over-procurement caused by overestimates of load growth, unduly conservative assumptions about imports during peak demand periods and an assumed net cost of new entry that is too high. | PJM

They also said energy market price caps should be increased to reflect the true value of lost load. “CAISO, MISO and PJM all have relatively low price caps in their energy markets, which can mute the incentive for performance during periods of extreme scarcity and result in under-investment in flexible generation that contributes to resource adequacy,” they said. “Low price caps can also cause unintended consequences in energy markets. For example, energy market price caps in CAISO caused many storage resources to prematurely discharge during early afternoon periods in the September 2022 heat wave because once prices hit the $2000/MWh cap, storage resources had no incentive to retain their state of charge even though it was known that net load would be even higher later in the afternoon and evening.”

They said FERC should also consider making planned generator and transmission outages transparent “so they are priced in the market.”

RTOs could also play a greater role in coordinating transmission and generation outages to reduce congestion costs, they said. MISO’s Independent Market Monitor has recommended such a change, noting that: “ISO-New England does have the authority to examine economic costs in evaluating and approving transmission outages, which has been found to have been very effective at avoiding unnecessary congestion costs.”

Broaden the Inquiry?

The Electricity Consumers Resource Council (ELCON), which represents large industrial energy users, was among commenters that called for FERC to broaden its inquiry.

“This proceeding is a perfect opportunity to explore whether — and if so, how — the policy goals outlined by the Commission 23 years ago in Order No. 2000 have been achieved,” ELCON said. “At this point, the track record with existing institutions is nothing if not sufficiently long. FERC has employees on staff who were born, raised and earned graduate degrees in the time since Order No. 2000 was issued.”

The Clean Energy Buyers Association, which represents 89 Fortune 500 companies, said it agreed with Commissioner Christie that the commission should expand the scope of its inquiry beyond E&AS markets, “including requiring RTOs/ISOs to address whether intermittent and hybrid resources are compensated appropriately to ensure reliability.”

Advanced Energy United said the commission should require the RTOs to update their reports on modernizing electricity market design annually. “Having year-over-year data and insights from the RTOs/ISOs will give the commission insight into emerging grid and market changes and a deeper understanding of long-term trends.”

R Street Institute challenged the presumption that RTOs will continue in their existing form, reiterating its request, with ELCON and others, for a congressional study of the electric power industry and its regulation. “The benefits of wholesale competition have not always been clear for retail consumers, sometimes because of unmitigated market power but more often because of faulty retail regulation,” R Street said.

Gas-electric Coordination

The Electric Power Supply Association asked FERC to redouble efforts to improve gas-electric coordination, warning “we are approaching a precipice in terms of system reliability which must be acknowledged.

“The need to reform power markets to address planning parameters, operational issues and flexibility needs is no longer a theoretical exercise but an imminent concern that must be addressed. Additionally, the lessons of Winter Storms Uri in 2021 and Elliott just a few weeks ago shine a bright and unavoidable light on ongoing coordination problems between the electricity and natural gas systems, which are likely to intensify as the system becomes increasingly dependent on dispatchable resources including natural gas-fired generation,” EPSA said.

Electric-gas coordination has been an issue in PJM since at least the 2014 polar vortex, when the RTO saw more than 20% of its gas-fired generation unavailable. The high outage rate was supposed to be solved by PJM’s Capacity Performance rules, yet the RTO saw similar rates of natural gas plant outages over the Christmas holiday. (See PJM Gas Generator Failures Eyed in Elliott Storm Review.)

“The issues raised by the challenges of gas-electric coordination are complex and implicate long-held practices in both industries, contributing to the reluctance to change or reform from either side. There are reforms that can be undertaken in electricity markets to address natural gas supply issues and availability. Notably, however, those power market reforms likely need to be matched in some manner by either reforms or adjustments on the natural gas side.”

Days per month of natural gas supply risk under deep decarbonization in New England | ISO-NE

EPSA said the discussions should go beyond weather to also ensure sufficient gas-fired capacity to respond to ramping needs. “The broader discussion must evaluate the need for additional supply and transportation capacity to ensure units can run when called and not be restricted by a system that is not expanding with the increase in demand,” it said.

EPSA said solutions could require “reimbursement for the cost of fuel in a manner not provided for today.”

EEI suggested the commission convene a technical conference to discuss the issue.

Barriers to Entry

Environmental groups including Earthjustice, Natural Resources Defense Council, Sierra Club, Sustainable FERC Project and the Environmental Defense Fund said the RTO/ISO reports “fail to address barriers to entry that resources face in attempting to gain access to markets.”

“The commission should require that each RTO/ISO focus on improving existing ancillary services prior to identifying new services or expanding the scope of market,” they said. Among the improvements the groups would like: shortening the durational requirements for eligibility to provide ancillary services and identifying stacking techniques for battery storage and hybrid resources. They also called for development of new ancillary services such as market-based fast frequency response and primary frequency response products and for splitting regulation services into upward and downward ramping products.

They said FERC should open proceedings under Section 206 of the Federal Power Act over MISO’s refusal to let dispatchable intermittent resources (DIRs), such as wind and solar, sell ancillary grid services in the operating reserves markets. They said MISO’s report “understates the ancillary services contributions of inverter-based resources while overstating the contributions of legacy resources.”

“It is well-accepted that DIRs and hybrid resources are technically capable of providing these services, and often more quickly and accurately than traditional thermal resources. However, MISO’s blanket prohibition is locking these resources out of the market, unnecessarily removing tools at MISO’s disposal to lower ancillary services costs while simultaneously increasing reliability,” they said. (See MISO Plans to Bar Intermittent Resources from Ramp Capability.)

The Clean Energy Associations said RTOs/ISOs should not interfere with market participants’ use of their commitment and dispatch preferences, including giving battery storage operators the option of managing their state-of-charge at all times.

“Today wind and solar may or may not be the most cost-effective resources to provide certain services given the opportunity cost of curtailing renewable generation,” they acknowledged. “However, as the renewable penetration increases, curtailment will increase, and the opportunity cost of foregone energy production will decline so that renewables may increasingly become cost-effective sources of ancillary services and flexibility in the upward as well as downward direction.”

Saving Coal

Coal industry group America’s Power asked the commission to require RTOs pay coal generators to keep operating to reflect the reliability benefit of their dispatchability and on-site fuel storage. “We respectfully urge the commission to require RTOs to value the needed attributes to mitigate the impacts of further retirements until global reforms can be developed and implemented,” it said.

Tom Stacy and George Taylor, who have consulted with America’s Power, filed comments calling themselves “Independent Ratepayer Advocates,” in which they said variable energy resources should not be granted interconnection rights unless their sites also include a dispatchable resource or storage. “The commission should resist the desire of VER investors — or anyone else — to continue to expand their market share while avoiding costs their resources create,” they said.

Below is a summary of the agenda items scheduled to be brought to a vote at the PJM Markets and Reliability Committee and Members Committee meetings Wednesday. Each item is listed by agenda number, description and projected time of discussion, followed by a summary of the issue and links to prior coverage in RTO Insider.

RTO Insider will be covering the discussions and votes. See next week’s newsletter for a full report.

Markets and Reliability Committee

Consent Agenda (9:05-9:10)

The committee will be asked to endorse:

B. proposed revisions to Manual 2: Transmission Service Request, to clarify changes made to the internal network integration transmission service process, as well as administrative cleanup. (See “Streamlining Internal NITS Process Under Consideration,” PJM MRC/MC Briefs: Sept. 21, 2022.)

C. proposed revisions to Manual 14A: New Services Request Process and Manual 14B: PJM Regional Transmission Planning Process, addressing the generator deliverability test. (See Stakeholders Endorse Changes to Generator Deliverability Test,” PJM PC/TEAC Briefs: Jan. 10, 2023.)

D. proposed revisions to Manual 28: Operating Agreement Accounting, addressing conforming clarifications and corrections to support the implementation of reserve price formation expanding on the revisions endorsed by the MRC in September 2022.

E. proposed revisions to Manual 38: Operations Planning, resulting from its periodic review.

PJM’s Brian Chmielewski will review a proposal addressing capacity interconnection rights for effective load-carrying capability resources, endorsed by the Planning Committee during its Jan. 10 meeting. (See PJM Planning Committee Endorses Capacity Accreditation for Renewables.) The committee will be asked to endorse a solution and corresponding manual, tariff and Reliability Assurance Agreement revisions.

PJM’s Scott Baker will review proposed revisions to the Emerging Technology Forum charter. The committee will be asked to endorse the charter revisions.

3. Hybrid Resources Phase II (9:50-10:10)

PJM’s Danielle Croop will review the package detailing the Hybrid Resources Phase II solutions. (See “MIC Endorses Proposal on Hybrid Resources,” PJM MIC Briefs: Nov. 2, 2022.) The committee will be asked to endorse a proposed solution and corresponding tariff and Operating Agreement revisions.

4. Day-ahead Zonal Load Bus Distribution Factors (10:10-10:30)

PJM’s Amanda Martin will review a proposed solution package to revise PJM’s zonal load bus distribution factors methodology to look at all hours of a given day. (See “Manual Revisions for Day-ahead Zonal Load Bus Distribution Factors Endorsed,” PJM MIC Briefs: Dec. 7, 2022.) The committee will be asked to endorse revisions to Manual 11: Energy and Ancillary Services Market Operations, Manual 28: Operating Agreement Accounting and tariff section 31.7.

C. endorse proposed tariff and OA revisions addressing the alignment of PJM’s authority in event of a default. (See “1st Read on Proposal to Allow Flexibility for Market Participation During Defaults,” PJM MRC Briefs: Nov. 16, 2022.)

D. endorse proposed clarifying tariff and OA revisions as endorsed by the Governing Documents Enhancements and Clarifications Subcommittee (GDECS).

Endorsements (1:25-2:00)

1. Manual 34 Revisions (1:25-1:40)

Adrien Ford, of Old Dominion Electric Cooperative, will move — and Jim Benchek of Monongahela Power will second — a main motion for proposed revisions to Manual 34: PJM Stakeholder Process, addressing motions for new issues at the Members Committee. The new language would allow for issues that are best addressed by the MC to be brought as a problem statement and issue charge directly before the committee. The committee will be asked to approve the proposed Manual 34 revisions.

2. CIRs for ELCC Resources (1:40-2:00)

See MRC item 1 above. Following potential same-day endorsement at the MRC, the MC will be asked to endorse the corresponding tariff and RAA revisions.

A financial consulting firm has concluded that MISO’s auction revenue rights and financial transmission rights market needs updating to keep it relevant to the changing grid.

London Economics International (LEI) said during a Market Subcommittee meeting Thursday that the grid operator’s process needs a refresh, saying it is becoming increasingly outdated because its auctions rely on a 2004 benchmark rights allocation in the MISO Midwest region.

“The ARR entitlement process, though valuable, has not kept pace with new entries and resource retirements, limiting transmission customers’ ability to hedge their day-ahead energy market congestion risks,” LEI consultant Victor Chung told stakeholders.

MISO contracted LEI last spring to evaluate its ARR and FTR markets. The grid operator hopes the firm can make recommendations to help it address gaps in its market design and ensure the ARR/FTR market’s health. (See “Concerns Develop over FTR Market,” MISO Market Subcommittee Briefs: Oct. 7, 2021.)

LEI recommended MISO re-evaluate its basis for determining ARR entitlements and “move away from a fixed historical reference year to better track actual usage of the transmission network.”

Chung said ARR megawatts tied to paths with retired generation have increased from about 1% to 3% in recent years.

“Entitlements don’t track network use,” LEI Managing Director Julia Frayer said, noting that entitlements should “better reflect the system today, where load and generation are.”

MISO has become increasingly concerned over the congestion-hedging market’s underfunding. It has said there’s a growing discrepancy between awarded ARRs and the footprint’s actual congestion patterns. As a result, load-serving entities hold a historically smaller share of FTRs, and the ARRs’ congestion value has fallen.

The grid operator issues the financial instruments based on transmission capacity; they are used by load-serving entities and other market participants as financial hedges against congestion charges in the day-ahead market. MISO funds FTRs through day-ahead congestion costs; an ARR is the LSE’s entitlement to a share of revenue from FTR auctions because of its historical use and investment in the transmission system.

LEI noted that there have been “very few” new ARR paths allocated to LSEs and the new paths “appear to be insufficient in providing a hedge” against congestion risk. The firm said MISO should allow its LSEs to nominate more variations of paths.

The firm also recommended staff tailor their FTR products to the RTO’s evolving supply mix and load patterns by offering morning, afternoon, evening and night options that could also account for weekdays or weekends. However, it acknowledged that selling FTR products by time periods would make for more complex monthly auctions.

MISO’s regulated and more risk-averse LSEs have “limited participation” in the monthly FTR auctions, LEI said, so most profits go to financial traders. The firm suggested staff create an entitlement FTR product for LSEs when additional network capacity is available in the monthly auctions.

“This may help motivate LSEs to participate … without necessitating LSEs to take on any additional risk,” LEI said.

The firm urged MISO to also monitor trends among pivotal suppliers and participants with large market shares competing in the FTR market and track the number of LSEs versus financial traders. It also recommended staff keep a more public tally of the amount of congestion revenue lost by transmission customers because of ARR allocation curtailments.

Finally, LEI said the grid operator should consider incentivizing more accurate reporting of transmission outages, so outages modeled in the FTR auctions match planned transmission outages and the actual outages that ultimately impact the day-ahead market.

MISO said increasing wind generation has cut down on the volume of ARRs. Wind-related ARRs tend be about one-third of those associated with retiring baseload generation.

Stakeholders agree that staff must revisit ARRs. Multiple stakeholders said state-regulated utilities cannot participate because of the market’s speculative nature.

MISO’s Independent Market Monitor reported that FTRs were fully funded this fall and that the grid operator collected more than $47 million in surplus. The Monitor said the surplus “indicates that some paths were significantly undersold after both the annual and monthly FTR auctions.”

Monitoring staffer Carrie Milton said the quarterly surplus “would have been higher but for large shortfalls on paths that were over-allocated in MISO’s ARR process.”

Milton said a single transmission owner’s failure to report a known transmission outage before the annual auction caused a $15 million shortfall. MISO’s FTR surplus collections are used to fund shortfalls, so that the costs of over-allocations are subsidized by all other transmission customers.

Monitor David Patton is asking MISO crack down on transmission owners not reporting outages to MISO before AARs/FTRs are issued.

Patton said in a footprint that racks up billions of dollars in congestion, an unreported outage can have “tens of millions of dollars” in ramifications when a TO sells property rights to its lines but doesn’t disclose planned outages.

Washington lawmakers have introduced a bill to require a study on disposing and recycling blades from wind turbines.

Senate Bill 5287, which calls for such a study by the Washington State University Extension Energy Program to be turned in to the legislature by Dec. 1, drew no opponents during a hearing before the Senate Environment, Energy and Technology Committee on Friday.

Three people testified in favor of the bill, while another 29 signed up in favor but did not testify. No one signed up in opposition. The bill has co-sponsors from both parties.

“There is currently not any facility in the United States that recycles wind turbine blades. … We think this will be someday mandatory in the future,” Jeff Gombosky, a lobbyist speaking on behalf of Renewables Northwest, told the committee.

“We need to be concerned with the total life cycle infrastructure,” said Ann Murphy, representing the League of Women Voters.

The average lifespan of a wind turbine blade is 20 years, said a Senate committee memo. The average length of a blade is 170 feet. Washington’s wind turbines produce 3,400 MW of power.

“Landfilling these giants is not green nor sustainable,” said the bill’s sponsor, Sen. Jeff Wilson (R). He added that roughly 8,000 blades have been removed from turbines nationwide.

“We’ve talked about industries being responsible for the life cycles of their projects,” Sen. Lisa Wellman (D) said.

The bill calls for the study to include the costs, feasibility and environmental impacts of disposal methods for the blades. The study would also look how a state-managed disposal program could be managed and at the possibility of recycling blades made of steel, plastic and fiberglass.