Local elected officials in Colorado are speaking out against the Trump administration’s order to keep the coal-fired Craig Generating Station Unit 1 available to operate past its planned retirement date.

The officials addressed the Colorado Public Utilities Commission during the public comment portion of the Jan. 14 meeting.

“It is painfully clear that the federal government currently has not only abandoned climate-sensitive policies and fuel choices, but that it is actively seeking to destroy a durable climate and to return to the damaging fuel sources that got us into this pickle in the first place,” said Glenwood Springs City Council member Steve Smith.

The U.S. Department of Energy issued an emergency order Dec. 30 to Tri-State Generation and Transmission Association and other co-owners of Craig Station Unit 1 to keep the unit available to operate. Unit 1 was slated to retire Dec. 31; Tri-State said it had planned for adequate resources to maintain reliability after the unit retired. (See DOE Blocks Retirement of Another Coal-fired Plant.)

A DOE news release said the order was to ensure access to “affordable, reliable” electricity through the winter. The order is in effect through March 30.

Tri-State said in a release that Unit 1 was hit by an outage Dec. 19 due to a valve failure. But Tri-State has a “100% compliance” policy, CEO Duane Highley said, and planned to take needed steps to repair the valve.

Local officials said their communities are ready for the coal plant to close.

“[The] heavy-handed order to Tri-State to keep the Craig Unit 1 coal plant open flies in the face of Colorado law, Tri-State’s bottom line and what people in Craig and Moffat County want,” Ridgway Mayor John Clark told the PUC.

Speakers pointed to the impact that climate change is already having on their communities.

Broomfield City Council member Sean McKenzie said a grass fire that broke out in the community Jan. 5 was quickly contained, but sparked memories of the devastating Marshall Fire in December 2021 that destroyed 1,084 homes.

“The conditions that were once reserved for July are now visiting us in January,” McKenzie said. He urged commissioners to “uphold the policies you’ve worked so hard to put in place.”

Basalt City Council member Hannah Berman called climate change an “existential threat” to the area’s economy, which relies on outdoor recreation. She asked the PUC to “take any and all action they can to ensure that Colorado continues to transition off of coal power as mandated by Colorado law.”

Adams County Commissioner Emma Pinter warned the commission that now is not the time to backslide on climate goals.

“In Colorado, our climate emission goals still stand and must be achieved,” Pinter said. “This commission needs to work to ensure that we meet all of our climate goals in spite of any federal efforts to the contrary.”

Over the past year, “capacity” — the assurance that electricity will be there when one flips the switch — increasingly has dominated the electricity conversation. PJM has been the epicenter of that conversation.

That market has seen its previous three capacity auction revenues skyrocket by tens of billions of dollars, driven largely by unexpected and rapid load growth from data centers as well as the adoption of a more rigorous method for accrediting the capacity of various resources.

Seeking to avoid a similar problem, ISO-NE is reforming its approach to acquiring sufficient capacity, submitting a proposal to FERC on Dec. 30. The filing is ISO-NE’s biggest change in this area since such markets first were established 18 years ago, evolving from its traditional three-year lead time model to a “prompt” approach, beginning in 2028.

Closing the 3-Year Gap

With the new proposal, ISO-NE will shake things up considerably. Citing growing uncertainty in load forecasting — a result of hard-to-predict end uses such as “the construction of data centers, and changes in public policy that could impact the pace of electrification,” as well as increasingly volatile weather and the variability of renewables output — the grid operator proposes to reduce the three-year lead time to only a single month.

The three-year schedule originally was intended to provide economic signals that provided sufficient time for developers to build new resources. But given the evolution of markets and technologies, that logic has unraveled.

Peter Kelly-Detwiler

When I oversaw Constellation Energy’s demand response group back when the formal DR markets were created around 2005, we found that prices whipsawed significantly from one year to the next. Consequently, it was nearly impossible to assess the long-term value of planned investments. A single annual price signal — even three years in advance — was not very valuable. It was bad enough for existing DR end-use assets that could be enrolled within a year; for multibillion-dollar generation units with lifespans of 30-40 years, such annual price indicators were next to useless.

Furthermore, the reality of today’s generation asset development — characterized by sclerotic interconnection queues, lengthy and complex state and local permitting processes, and a brutally slow supply chain — means that nothing gets built within a three-year time frame even in the most optimistic scenario. To take one example, one cannot even get a new gas turbine from GE until 2028/29 at present.

The result of the old three-year forward system was an abundance of “phantom assets” haunting the resource mix — projects that cleared the auction but never were developed. Those shortfalls in capacity subsequently had to be addressed through intermediary reconfiguration auctions. The new prompt auction, taking place just a month ahead of delivery, helps ensure that ISO-NE will secure capacity from actual resources capable of delivering, rather than empty promises from developers who may never see steel in the ground.

Seasonality: Addressing the Worst Days of Winter

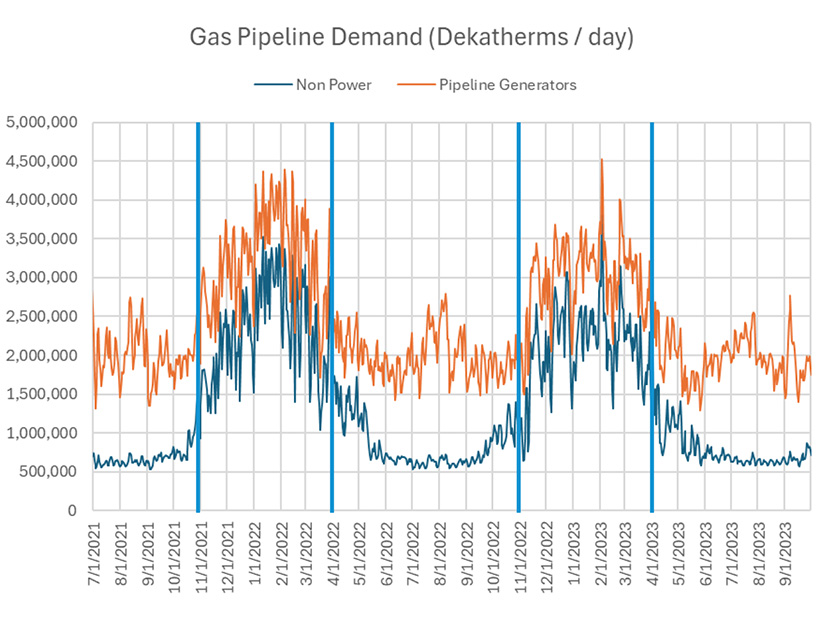

The New England grid operator also changed its approach to seasonality, an approach that is long overdue. While summer heat may challenge the grid, New England’s lengthy winter cold snaps are where the greatest risk lies. With only two pipelines feeding the region, on the coldest days there is simply insufficient gas to generate power and keep people warm and safe. In that equation, power generation loses. At that point, the region resorts to its store of fuel oil, which is not limitless.

During the extended cold weather of 2017/18, for example, New England’s generators burned through nearly 3 million gallons of fuel oil reserves, with 2 million gallons consumed over just eight days. As can be seen in the graphic, oil reserves plummeted from 34% to 19% availability during the coldest 24-hour period, meaning the region was perhaps a single day away from rolling blackouts.

ISO-NE’s revised approach to capacity planning will address that seasonal challenge by establishing a bifurcated system with summer (June 1 to Oct. 31) and winter (Nov. 1 to May 31) periods. This scheme will differentiate resources based on performance during each season. So, for example, solar may fare well during the summer, while assets with on-site fuel would have an advantage in the winter.

Resource Capacity Accreditation: Who Shows Up When the Party Starts?

ISO-NE’s greatest proposed technical change is the way in which capacity resources are “counted.” The existing summer performance-based accreditation process will give way to an approach intended to “accurately capture the marginal reliability contribution of resources during the periods that will be of highest risk to reliability.” In other words, resources will be rated based on their effectiveness at staving off a blackout when the system is under maximum stress.

The grid operator will evaluate characteristics such as forced outages, output variability and access to fuel. For the reasons discussed above, gas-fired generation may be significantly impacted, with ISO-NE reflecting the effect of “pipeline constraints that can limit the ability of the region’s gas-fired resource fleet to obtain fuel during the winter.”

Gas units without firm supply contracts are likely to be penalized by this approach, and they should be. They rarely show up to the party when needed, on those days when power generation and other demands are both clamoring for the same gas molecule. As illustrated in ISO-NE’s planning document, those two demand peaks are highly coincident.

| ISO-NE

ISO-NE is not the only grid operator seeing this dynamic. 2021’s Winter Storm Uri in Texas and 2022’s Winter Storm Elliott in the Mid-Atlantic aptly demonstrated the fact that a megawatt of gas-fired capacity is useless if gas is frozen in at the wellhead or if pipeline pressures fall and generating turbines are starved of fuel.

After Elliott, PJM significantly reduced the accredited capacity off gas plants, with combined cycle plants falling from 96% to 79% over one year as a result. ISO-NE’s new rules may have a similar effect, so that a 1,000-MW gas plant might be credited for only 700 MW or 800 MW of “reliable” capacity.

A Better Way of Saying Goodbye

ISO-NE is reforming its resource retirement process. Currently, a power plant must signal its retirement four years in advance. With the new approach, plant owners can submit a retirement notification one year in advance. This approach gives owners far better knowledge as to the remaining life of their equipment and the near-term market conditions, allowing them to remain in the market if conditions are favorable.

The Inflationary Bottom Line for the New England Power Market

ISO-NE has asked FERC to approve these revisions by March 31, 2026, with the first affected auction occurring in May 2028 for delivery starting in June. The new approach is more realistic, but it may well have a significant inflationary effect for two reasons.

First, if the experience of PJM holds true, ISO-NE could find itself short of accredited capacity because of its revised accreditation approach. With 42% of 2025’s capacity supplied by gas generators, a significant de-rating could cut supply and drive prices up, especially if the demand side heats up.

Second, the seasonal approach may further affect future available capacity figures, especially with the winter re-rating of gas-fired generation, creating additional shortfalls.

And finally, with the capacity auction only a month prior to delivery, there’s zero time for the supply side to react to higher prices.

It’s probable we’re entering an era in which our “friendly little electron” demands a much higher price for the privilege of being there exactly when we need it. So, customers must be prepared to focus more intently than ever before on managing their demand — on a seasonal basis — even as they reluctantly reach for their checkbooks.

Around the Corner columnist Peter Kelly-Detwiler of NorthBridge Energy Partners is an industry expert in the complex interaction between power markets and evolving technologies on both sides of the meter.

The California Public Utility Commission approved a set of transmission infrastructure projects to support a 90-MW data center owned by Microsoft, but questions remain about whether the upgrades will increase or decrease ratepayer costs.

The transmission projects present “unique considerations” not fully addressed by certain existing electric rules, the CPUC said in a resolution approved at its Jan. 15 voting meeting. The resolution is based on advice letter 7635-E, which was submitted by Pacific Gas and Electric (PG&E) in July 2025.

The electric rules in question normally apply to distribution energization projects, but Microsoft’s data center is expected to have a 90-MW load — a “significant” amount that will require a new 115-kV transmission line and substation upgrades, the resolution says.

“Because the Microsoft project will be interconnected at the transmission level, Microsoft will pay lower electric rates than an equivalent large load customer that is connected at the distribution level and normally covered by the Rule 15 process, while at the same time potentially contributing to the need for broader transmission network upgrades in the region,” the commission said in the resolution.

Providing electricity to the new data center requires “significant costs but comes with the opportunity for significant revenue received by PG&E,” the resolution says.

If these revenues are large and consistent, other customers might need to pay less of PG&E’s overall revenue requirement, which could lower rates for PG&E customers, the resolution says. But if the revenues are small or are not received consistently, PG&E customer rates could increase, it says.

PG&E will complete the following work for Microsoft’s data center:

transmission upgrades at PG&E’s Los Esteros substation

a new 115-kV transmission line from PG&E’s Los Esteros substation to Microsoft’s Kaku substation

a design review of Microsoft’s Kaku 115-kV substation

an additional 115-kV transmission line from PG&E’s Los Esteros substation to Microsoft’s Kaku substation

PG&E could not determine which transmission facilities CAISO will control, according to the resolution.

The data center will operate at a continuous 90-MW load for 24 hours a day, 365 days a year, the resolution says.

Microsoft has also requested a second 115-kV line to provide redundant service; however, this project falls under a special facilities agreement and will not be paid by PG&E ratepayers at any point, the resolution says.

Microsoft also plans to install two natural gas-fired generators for critical load and emergency backup, the advice letter says.

At the meeting, the CPUC approved also a 225-MW lithium-ion battery storage project for PG&E. The storage facility will provide resource adequacy capacity and has a planned online date of May 20, 2028, with a 15-year energy delivery commitment.

The storage facility’s capacity will replace Diablo Canyon Power Plant’s capacity when, and if, the nuclear plant is retired. The facility, called the Dirac Battery Energy Storage System, will be built by Aypa Power Development using the company’s subsidiary, Balsam Project.

Earthjustice accused Meta of deliberately executing an unsanctioned financial arrangement to underwrite its planned, multibillion-dollar data center in northern Louisiana and asked the Louisiana Public Service Commission to investigate.

Representing the Alliance for Affordable Energy and the Union of Concerned Scientists, Earthjustice said it appeared Meta had ulterior motives for the financial risk it was willing to undertake for the data center.

Meta did not reply to a request for comment on the allegations.

In a Jan. 14 motion for investigation to the Louisiana PSC, the environmental law center said “immediately after” the commission approved Entergy Louisiana’s application for three new gas plants to power the data center in August 2025, Meta “fundamentally altered” the financing structure of the project.

Enter asset management firm Blue Owl Capital. In late summer, it and Meta created the joint venture Beignet Investor, which now reportedly owns an 80% stake in the data center. Meta owns the remaining 20%. Beignet acquired Meta company Laidley to secure the majority ownership. (Stay with us here.)

When the Louisiana PSC approved Entergy’s power supply proposal for the data center, Meta used Laidley, its development affiliate, to represent itself. Laidley is the sole signatory to the data center’s energy service agreement with Entergy Louisiana for the three natural gas plants. Earthjustice noted that Beignet Investor registered as a limited liability company in Delaware on Aug. 20, 2025, the same day the Louisiana PSC voted 4-1 to approve Entergy’s supply contracts (U-37425). (See Louisiana PSC Approves 3 Controversial Gas Plants Ahead of Schedule for Meta Data Center.)

Now, Meta would pay rent to Beignet to use the Meta Hyperion data center, with the option to exit the lease every four years. Should Meta decide to depart, Beignet would sell the center to pay outstanding bonds and then pay itself, Earthjustice told the Louisiana PSC. If sale proceeds fall short of what’s owed to bondholders combined with Blue Owl’s investment, then Meta would pay the difference. Meta would guarantee its rent and payment obligations via parent guaranty to Blue Owl.

Earthjustice said because Meta already has significant debt load, Blue Owl invested $3 billion for an 80% stake in the Hyperion data center. Meta’s existing $1.3 billion investment earned it the remaining 20%.

Beignet then borrowed $27 billion for the project. The new LLC has no assets beyond the data center; Earthjustice said that makes it a “riskier partner as the guarantor” of the supply arrangement with Entergy.

Meta’s rent payments would go to bond interest and principal payments, as well as dividends for Blue Owl.

The joint venture between Meta and Blue Owl is the largest private credit transaction ever and allowed Meta to receive a $3 billion cash distribution from the venture upon closing.

The convoluted arrangement was referred to as “Frankenstein financing” by The Wall Street Journal, which published a Nov. 11 investigative piece on the labyrinthine financing Big Tech uses to break ground on data centers.

‘A Secret’

Earthjustice said the “remarkable,” same-day creation of Beignet “illustrates that Meta and Blue Owl were working behind the scenes to significantly alter the financial structure of the data center project while the proceeding to examine the now irrelevant data center financial structure was ongoing.”

“Meta kept this significant change a secret, just like Meta kept how they developed their load forecast and how they determined their job numbers a secret,” Earthjustice claimed, adding that the PSC needs to know the facts behind the funding of the data center.

Earthjustice said if the AI boom were to dry up, Meta could walk away from the deal as soon as 2033. It said by then, the data center could lose prospects for another buyer and depreciate.

Meta, Entergy and the Louisiana PSC expect construction on the data center campus to continue through 2030.

“This novel financial arrangement lets Meta add computing power quickly and then wait to see how demand for AI shapes up before fully committing to projects that can last for decades. Thus, Meta is off-loading its own risk by placing that financial risk on others, including ratepayers who will be on the hook for all the infrastructure built solely for this data center should Meta exercise its option to walk away,” Earthjustice argued. The law organization said all the ratepayer protections the Louisiana PSC hammered out in its approval are “at best, called into question” because Meta no longer is Laidley’s parent company.

Throughout the PSC’s consideration of the gas plants to power the data center, the Alliance for Affordable Energy and the Union of Concerned Scientists voiced concern of the risk of after-the-fact changes to the electric service agreement with Entergy, the risk of stranded costs or capital cost overruns on the gas plants and an “inappropriately short” 15-year contract term on the power supplied by Entergy.

“This new, novel financial arrangement, which very likely was withheld from the commission prior to its action on [Entergy Louisiana’s] application, calls into question the meager ratepayer protections included in the application and contested settlement agreement and undermines the assumptions made by the commission when it voted to approve the application,” Earthjustice wrote.

The Louisiana PSC approved consumer protections including a provision that Meta’s minimum bill payments would cover 100% of the costs of the trio of generating units, including cost overruns. Meta also agreed to fund development of 1.5 GW of solar generation under the state’s Geaux Zero program and to provide up to $1 million per year for Entergy’s Power to Care, which is a bill assistance program for low-income, elderly and disabled Entergy Louisiana customers.

Entergy has entered the first of three gas plants into MISO’s expedited interconnection queue and submitted the 500-kV facilities needed to connect the data center into MISO’s expedited transmission approval process.

At publication time, Meta did not respond to RTO Insider’s questions on whether the new financing arrangement would transfer more risk to Entergy’s ratepayers; who would be responsible for termination fees should Meta take Beignet up on one of the four-year exit options; and whether Meta is prepared to honor its end of the deal as spelled out in the Louisiana PSC’s original approval order even with the additional investors involved.

Investigation Request

Earthjustice asked the PSC to launch an investigation to decide whether it was deliberately misled and establish the new financial setup’s effect on ratepayer protections. It also said the commission should open a prudence review to figure out whether Entergy Louisiana was aware of the financial reformatting and to decide whether it’s wise to allow Entergy to continue with the trio of gas plants.

Finally, Earthjustice said the PSC should direct Entergy Louisiana to file a copy of the “parent guaranty that is executed by Laidley’s current parent that does not include a cap on the parent’s cumulative liability;” and order Entergy to file a legal opinion clarifying that the parent is bound by the parent guaranty and confirming that termination payments to Entergy must be paid out before investors are compensated.

Meanwhile, Entergy is seeking a 10-year property tax exemption worth an estimated $237 million to build the first 1.5-GW natural gas plant for the Meta data center campus. Entergy submitted the application under Louisiana’s Industrial Tax Exemption Program, which waives local property taxes on some industrial projects.

Entergy plans to build the more than $2.3 billion Titanium Power Station first, which would consist of two combined-cycle combustion turbines.

Entergy has pledged that Meta will foot the bill for the power station — at least for the contract length of the first 15 years of the generating unit’s life — and that it should save ratepayers about $650 million in the long run.

Washington’s attorney general and a coalition of environmental groups have mounted separate challenges to the U.S. Department of Energy’s December decision to order TransAlta to continue operating the state’s last coal-fired plant for three months beyond its scheduled retirement at the end of 2025.

Attorney General Nick Brown and the coalition — which includes Earthjustice, NW Energy Coalition, Washington Conservation Action, Climate Solutions, Sierra Club and the Environmental Defense Fund — have separately filed requests to rehear DOE’s Dec. 16, 2025, order to keep the Centralia Power Plant’s 670-MW Unit 2 running until March 16, 2026, due to an energy “emergency” in the Pacific Northwest this winter. (See DOE Orders Retiring Wash. Coal Plant to Stay Online for Winter.)

The order was one in a series of such moves the Trump administration’s DOE has taken over the past year to extend the life of aging fossil fuel-fired plants slated for closure, including in Michigan, Pennsylvania and Colorado.

“The Trump administration is once again ignoring both the law and the facts,” Gov. Bob Ferguson said in a Jan. 13 statement accompanying announcement of the state’s request, which asks DOE to “immediately withdraw” the order. “DOE needs to reverse course on this harmful and misinformed order.”

“DOE is misusing its narrow authority reserved for imminent emergencies to force a dirty, inefficient coal plant to keep operating,” Earthjustice attorney Patti Goldman said in a Jan. 14 statement by the coalition. “Our region has moved beyond reliance on coal and this plant. We are meeting our region’s energy needs, now and into the future, with cleaner sources.”

In their statements, the AG’s office and the coalition questioned DOE’s authority to keep the Centralia plant open under Section 202(c) of the Federal Power Act — and the department’s reason for doing so, arguing that the law is intended to address only “real” emergencies.

The coalition contended that the order “exceeds that authority and instead tries to impose the administration’s preference for coal-fired power over a 2011 agreement between the state of Washington and TransAlta, the owner of the plant, to shut down the plant by the end of this year.” (Unit 1 at Centralia was shut down in 2020 under the first phase of that agreement, and TransAlta plans to convert the facility to natural gas.)

The AG said the order “is a clear attempt by DOE to bypass the limits imposed on it by Congress.”

In its rehearing request, the AG said the department failed “to properly identify or clarify the appropriate entities that have any authority to direct” Centralia’s operation. The Dec. 16 order called on TransAlta to “take all measures necessary” to ensure the plant is available operated at the direction of either the Bonneville Power Administration as a balancing authority or CAISO’s RC West as the regions reliability coordinator, but it was apparent neither of those entities was consulted before the order was issued.

Getting the Story Straight

The coalition in its rehearing request argued that DOE failed to provide evidence of an energy emergency or electricity shortage that warranted continued operation of the plant. It notes that two third-party studies cited by DOE to support its order “demonstrate the absence of an emergency.”

The coalition points out that the first study, NERC’s assessment of reliability for this winter, “expressly states that ‘operating reserve margins are expected to be met after imports in all winter scenarios.’ … This means that the study on which the department relies anticipates that the region will be able to meet peak demand and maintain the full added buffer of reserves on top.”

The second study, by Energy and Environmental Economics (E3), has not yet been released, the coalition noted. Instead, DOE based its finding on a September 2025 presentation on the pending study, whose author has said shows the Northwest’s resource adequacy risk is “slightly elevated above the target risk,” which “was calculated to achieve a loss of load expectation of one event-day per decade.”

“E3 also confirms that it calculated this ‘slightly elevated’ risk without examining the actual conditions this winter; as a planning document, the presentation is based on a historical model and does not reflect actual weather and hydrological conditions presently existing for this winter,” the coalition wrote in the rehearing request.

The coalition contends that recent actions by DOE undercut the department’s claim of an emergency, including an October 2025 order by the Grid Deployment Office that allowed the Northwest to export electricity to Canada based on a finding (in DOE’s own words) “that the wholesale energy markets are sufficiently robust to make supplies available to exporters and other market participants serving United States regions along the Canadian and Mexican borders.”

In that order, DOE itself pointed to the “comprehensive” reliability processes in the region that ensure “bulk-power system owners, operators and users have a strong incentive both to maintain system resources and to prevent reliability problems that could result from movement of electric supplies through export,” the coalition noted.

“The Trump administration can’t get its story straight,” Tyson Slocum, Public Citizen’s Energy Program director, said in the coalition’s statement. “While it claims the West Coast is in a state of emergency requiring families to bail out an expensive coal plant, Trump’s Department of Energy is simultaneously concluding the region has energy abundance to authorize electricity exports to Canada. Which is it, Donald?”

The coalition contends that complying with the DOE order will “be expensive, as Centralia does not have the coal, customers or workforce to keep the coal plant running. Other coal plants forced to keep operating are experiencing extremely high costs, which [FERC] can require ratepayers to pay.”

The groups point to the pollution impact of the order, and how it violates Washington’s Clean Energy Transformation Act, which required the state’s utilities to stop using electricity from coal-fired plants by the end of 2025.

“So many of us — from state leaders and utilities to elected officials and public interest groups — have worked for decades to plan for and build cleaner, more efficient generation and transmission that will ensure Washington state’s transition to clean energy while keeping energy affordable and reliable,” said Lauren McCloy of the NW Energy Coalition. “That work is ongoing, and burning more coal at Centralia is not the answer to meeting growing energy demand in the Northwest.”

Asked to comment on the challenge, a DOE spokesperson responded: “Under the disastrous energy subtraction policies of the previous administration, the U.S. was on track to lose 100 GW of reliable generation capacity by 2030. Much of the U.S. is now at ‘elevated risk’ of blackouts under extreme conditions, which NERC declared a ‘five-alarm fire’ for grid reliability.

“At the same time, the U.S. may need to build 100 GW of new reliable capacity to win the AI race and onshore manufacturing. The Trump administration is committed to preventing the premature retirement of baseload power plants and building as much reliable, dispatchable generation as possible to achieve energy dominance.”

NYISO kicked off the demand curve reset reform process with a discussion of how to improve the overall process and what could be done to strengthen the definition of the proxy unit. The ISO seeks to stabilize the installed capacity market by reducing volatility and making the DCR less complex and burdensome.

“I think, uncontroversially, we can consider this process quite burdensome for both NYISO and stakeholders, and we want to address those issues now as part of a project,” said Michael Ferrari, a market design specialist for NYISO.

No specifics, tariff changes, definitions or formulas were discussed. The discussion at the Jan. 12 Installed Capacity Working Group Meeting was centered on possible avenues to improve the DCR and what the ISO might explore with stakeholders.

The DCR anchors capacity prices on a curve by picking a “proxy unit” to represent the cost of a hypothetical new generator entering the market every four years. The most recent DCR set a two-hour battery energy storage system as the proxy unit for the 2025/29 period. (See FERC Accepts NYISO Demand Curve Reset.)

The current process involves considerable debate, outside consultation and stakeholder meeting time to pick a type of generator to serve as the proxy unit and determine a reasonable hypothetical capital cost estimate for it. Debating the engineering cost assessments to estimate capital costs for potential technology takes much of the 18-month DCR process. These findings are subject to an annual adjustment to try to keep the curve in line with market conditions.

“We want to address the issues now as part of a project before the status quo process of the demand curve reset begins in earnest,” said Ferrari.

Ferrari outlined some of ISO’s preliminary ideas for smoothing the DCR. The ISO is considering a periodic review that would use the existing annual update framework to apply systemic, formulaic adjustments to reduce the need for a total reset every four years. This would involve using cost-trend publications, inflation-based indexes and various annual financial parameters such as interest rates to adjust prices periodically. This would, in theory, reduce the administrative burden by getting away from detailed engineering studies.

NYISO also is considering redefining the proxy unit. It would no longer be a unit based on specific technology; instead, the proxy unit would merely be a hypothetical unit that meets a minimum operating criterium.

Stakeholders seemed skeptical of NYISO’s proposal. Some pointed out that national price indexes were extremely bad at predicting costs in New York City. Others pointed out that the annual adjustment mechanism already doesn’t work very well.

Adam Evans, a representative of the New York Department of Public Service, pointed out that the status quo was not tenable.

“In the last reset, we saw a potential $2.5 billion increase in demand curve cost based on what some folks were arguing for the proxy unit, which is frankly untenable,” said Evans. “I think this type of proposed solution to limit volatility … I think it makes sense.”

Other stakeholders pointed out that the current DCR process was not responsive or flexible in the face of state policy shifts. One stakeholder pointed out that state incentives for procuring carbon-free energy were not incorporated into the cost of new entry models. Another said the state climate law could be altered or removed by the legislature if the political winds shifted and any new process would have to account for that.

“I would be very concerned about trying to have a demand curve process that is super responsive to every policy shift that comes at us. That undermines the idea of certainty,” said Mike DeSocio, a consultant with Luminary Energy. He disagreed with the idea of a flexible process and asked NYISO to instead focus on market certainty.

Stu Caplan, representing New York Transmission Owners, said the market should not be designed for high price increases without reliability gains.

Equinor has won a temporary injunction against the Trump administration’s stop-work order on U.S. offshore wind projects, allowing it to resume work on Empire Wind.

The Department of the Interior on Dec. 22 shut down work on all five projects under construction in U.S. waters, citing national security concerns.

Empire, which incurred millions of dollars in added costs from a monthlong stop-work order in April and May 2025, filed a challenge to the new stop-work order Jan. 2 and a motion for preliminary injunction Jan. 6 in U.S. District Court for the District of Columbia (1:26-cv-00004).

After a Jan. 14 hearing, District Judge Carl Nichols — appointed to the federal bench by President Donald Trump in 2019 — granted the motion Jan. 15.

Equinor, which holds an offtake contract with New York for the 810-MW Empire Wind project, had told the court it likely would need to abandon the project if it could not resume work by Jan. 16. With any further delay, it said, crews would not be able to finish a key component before the specialized installation vessels had to depart for the next contracted work.

Later Jan. 15, Equinor said: “Empire Wind will now focus on safely restarting construction activities that were halted during the suspension period. In addition, the project will continue to engage with the U.S. government to ensure the safe, secure and responsible execution of its operations.”

It was the second court victory this week for the beleaguered U.S. offshore wind sector.

On Jan. 12, another Republican-appointed federal judge lifted the stop-work order on Revolution Wind, a 704-MW project nearing completion off the New England coast. (See Judge Again Lifts Revolution Wind Stop-work Order.) The same judge also lifted the Trump administration’s August stop-work order against Revolution.

Meanwhile, Dominion Energy is contesting the stop-work order on Coastal Virginia Offshore Wind, a 2.6-GW wind farm near completion, and Ørsted is fighting to restart work on the 924-MW Sunrise Wind, an earlier-stage New York project. (See Offshore Wind Developers Fight to get Back in the Water.)

Vineyard Wind was the last project to join the legal fray. On Jan. 15, it filed a complaint in U.S. District Court in Massachusetts (1:26-cv-10156) asking the court to declare the stop-work order unlawful and allow work to resume.

The Avangrid-Copenhagen Infrastructure Partners joint venture is 95% complete and already able to send 572 MW of its planned 800-MW capacity to the New England grid, according to the court filing. Construction began in 2021 and was on track to be completed by March 31.

In a statement, the developers said they will continue to work with federal regulators to understand the matters raised in the stop-work order but believe the order was unlawful and said if it is not promptly enjoined, it will cause immediate and irreparable harm to the project and the communities that will benefit from it.

Despite the setbacks it has sustained in court, the Trump administration has succeeded to a significant degree in its bid to thwart offshore wind development: The level of risk it has created has scared away further investment.

The five offshore wind projects hit with the Dec. 22 stop-work order constitute the entire large-scale U.S. offshore wind sector, and they appear unlikely to be followed by others anytime soon. To cite the obvious example, Empire Wind 2 has been shelved indefinitely.

Oceantic Network welcomed the Jan. 15 ruling: “Empire Wind is critical to securing New York’s electric grid, stabilizing rising energy costs for local communities, creating jobs and achieving energy independence, underscoring the importance of building out America’s energy infrastructure to meet rising electricity demand.”

Regional Plan Association hailed the win but warned it is not a final victory: “Despite the good news of these decisions, they still do not ensure that these projects will be completed. The court rulings are temporary injunctions that allow the companies to continue to build while the lawsuits against the administration’s efforts to stop them make their way through the courts. Even an ultimate victory against the administration’s freeze — based on supposed national security concerns — does not prevent them from taking additional steps to disrupt, delay or cease the projects.”

Advanced Energy United said: “Restarting Empire Wind is a major win. This project will deliver clean power and local jobs exactly when we need them the most. Today’s ruling shows that smart energy planning beats political games every time — and that delaying critical projects only drives up costs for consumers.”

PJM‘s 2026 load forecast has decreased the amount of growth expected for the following six years owing to a more pessimistic view of the volume of large loads, economic growth and electric vehicles.

The forecast continues to expect that load growth will accelerate over the 20-year scope, with load reaching 253 GW in 2046.

Load growth still is expected in the near term, just slower — particularly in the winter. For the summer of 2028, the total load expected is 2.6%, or 4.4 GW, lower than the 2025 forecast; for the following winter, the estimates are 3.8%, or 5.8 GW lower. Between 2027 and 2031, the summer peak is expected to grow to 191 GW, up 30 GW. By 2046, the peak is expected to reach 253 GW for the summer and 237 GW in the winter.

PJM said the forecast was likely to cut into the 6.6-GW shortfall in the 2028/29 Base Residual Auction (BRA). While the haircut is not enough to make up the difference, the RTO said it also expects some resources scheduled to deactivate and winter-only resources without an annual commitment to be available. (See PJM Capacity Auction Clears at Max Price, Falls Short of Reliability Requirement.)

Data center load growth has been the primary cause of the growing capacity shortfall and billions of dollars in transmission projects. The Board of Managers is considering a slate of proposals to rework the capacity market to address large loads, as well as an $11 billion Regional Transmission Expansion Plan to increase transfer capability into growing load clusters in Virginia, Pennsylvania and Ohio.

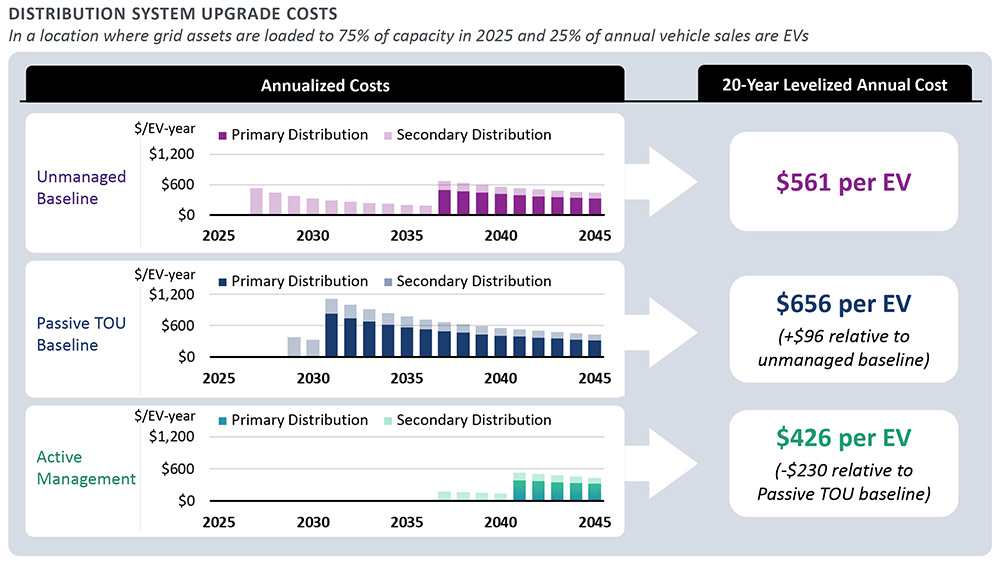

EnergyHub and Brattle Group released a report showing that utilities can achieve significant savings if they actively manage electric vehicle charging.

“Demonstrating the Full Value of Managed Electric Vehicle Charging” includes the results of a real trial of 58 EV drivers in Washington state who got $100 upfront and $10 per month when they limited opt-outs to three or fewer in a month. They were tested for four weeks with time-of-use rates. Energy Hub actively managed their charging using an unmanaged baseline on flat, volumetric rates.

“We found that with the solution, it enabled distribution utilities to host over twice the number of EVs on the same system as if they were unmanaged,” Energy Hub CEO Seth Thompson said in an interview. “So, it kind of doubles the distribution grid’s EV hosting capacity just by managing the EV charging load and in terms of cost impacts. We found that in the long term, it could bring the cost of hosting EVs from about $800 per year per EV if they were unmanaged, to about half of that if they were managed.”

EnergyHub’s main business is to contract with utilities to manage EVs and distributed energy resources (DERs) on their systems.

In the past, a lot of that work was focused on replicating a peaker plant with distributed resources. But as EVs become more common, the industry needs a way to manage their impact on distribution circuits.

“EVs clearly were starting to apply a degree of pressure to the distribution grid where the sort of traditional idea of a one-time or occasional, discrete activation of a VPP [virtual power plant] was not what the grid needed,” Thompson said. “The grid needed a system that sits there running all the time, protecting the system from overloads and essentially just moving load around to raise your utilization factor. That’s the future of VPPs, to be able to do both of those things.”

Active managing of EV charging delivers 95% of that load to off-peak hours, which helps cut customer bills. A more passive approach using time-of-use (TOU) rates (with lower off-peak charges) can deliver similar benefits when EV penetration is low, but it can exacerbate peaks when too many EVs are on one distribution circuit, Brattle managing associate and report co-author Akhilesh Ramakrishnan said in an interview.

“It’s not a generalized finding about TOU, but it’s specific to the type of load that EVs are, where they’re basically this kind of huge load that’s coming from one source,” he added. “EVs can be double the peak load of a typical house, and so you really don’t want all of these things charging and discharging at the same time.”

A chart from the report showing the costs in system upgrades per EV by different charge management styles. | Brattle

With passive TOU rates, customers would set their EVs to start charging once the cheaper power kicks in and everyone on the block would start pulling power at the same time, leading to a larger peak than even flat rates. Energy Hub’s management system can spread those charges over the entirety of the off-peak hours, flattening the peak.

“Every EV will let you set a charging schedule, and essentially, if you were trying to do this through behavior change, the more successful you are at getting everybody to pay attention to that black-and-white pricing signal, the greater the peak,” Thompson said. “And so, the ideal combination is a mix of the TOU signal and a piece of software that kind of randomizes and distributes that strategically over time.”

The study looked only at TOU rates, which offer discounts in off-peak hours. Thompson argued that more complex rates, like passing through wholesale costs, do not attract customers.

“If you go around Europe, if you go to Australia, in major other markets, the per capita participation with flexible loads is lower than it is in the U.S.,” Thompson said.

EnergyHub’s and other distributed energy resource management systems can link up EVs, solar panels, smart thermostats and other resources to those wholesale signals and optimize their performance for the grid, Thompson said.

The need for that management scales up with EVs on the system. Ramakrishnan said a local grid can handle a car or two but that once more start to plug in, their charges need to be managed to avoid the need for distribution upgrades.

“You can assume there’s a random distribution of these things up to a point, and you never know whether you’re already basically at capacity or there’s tons of headroom,” Thompson said. “The other thing that you hear from utilities all the time is that there’s clustering, and so you might have 5 or 10% adoption in the service territory, but you might have 25% in a neighborhood.”

The market changed for EVs in general in 2025 as federal tax incentives expired at the end of the third quarter. That led to a spike in purchases as consumers sought to take advantage of those, Thompson said.

Now the industry is waiting for new quarterly figures to get a sense of how fast EV sales will grow absent federal tax incentives. Even with those incentives, most of the plug-in models were more expensive, which kept their sales numbers low. With technology improving, prices are expected to come down and that could lead to significant growth.

“We now have the ability to tackle this in an orderly way,” Thompson said. “What’s nice about the way we’ve built this solution is that a utility can adopt it very cost effectively at small scale, get comfortable with sort of understanding what does it do? How does it work? How do they integrate it with our other systems?”

Once they begin building consumer awareness, “as they hit these levels of kind of a critical mass, whether that’s locationally or across their whole system, they’re ready for it,” he added.

To help critical infrastructure organizations strengthen their cybersecurity stances, the Department of Homeland Security’s Cybersecurity and Infrastructure Security Agency and several foreign counterparts have provided a set of principles to guide internet connectivity for operational technology environments.

The Secure connectivity principles for operational technology (OT) document was published Jan. 14 with contributions from CISA, the FBI, the Australian Signals Directorate, Germany’s Federal Office for Information Security, the Canadian Centre for Cyber Security and Communications Security Establishment, and the National Cyber Security Centres of the U.K. and New Zealand. The U.K. NCSC hosted the document on its website.

OT assets — which interact with the physical environment or manage devices that do so, according to the National Institute of Standards and Technology — have traditionally been separated from internet-connected systems for security reasons, but in today’s industrial landscape are increasingly integrated with information technology networks to increase business efficiencies.

Such integration can create security risks for reasons including “dependence on legacy technologies that were never designed for modern connectivity or security requirements,” along with the use of third-party tools, remote access and supply chain integrations that “expand the potential attack surface,” the agencies wrote. The risks of cyber intrusion are “elevated” in an OT environment because the consequences can include disruption of essential services, environmental impact and physical harm to employees and customers.

Experts have warned that OT networks are increasingly vulnerable to attack. Cybersecurity firm Dragos identified multiple new adversary groups in its annual Year in Review report, at least one of which demonstrated the capability to meaningfully attack industrial control systems. (See Dragos: Attacks on ICS Increased in 2024.)

In a later case study, the firm reported that the China-connected hacking group Voltzite had infiltrated a U.S. electric utility’s computer system in 2023. (See Dragos Outlines Voltzite Electric Utility Breach.)

8 Principles

The new document organizes its guidance into eight principles, to be used “as a framework to design, implement and manage secure OT connectivity.” Agencies encourage device manufacturers and integrators to make the principles easy to achieve through equipment design and documentation.

The first principle is balancing risks and opportunities when identifying where and how connectivity is permitted within OT systems. Entities should develop a business case that supports decision-making and documents the purpose of the connectivity, potential impacts of a compromise to the connectivity, senior risk owners and any dependencies that may be introduced by the connection. Organizations must also exercise control and oversight of their supply chains; agencies recommended previous publications to help with this, including CISA’s Secure by Demand guidance.

Principle 2 is limiting the exposure of the connectivity; exposure means “where an asset sits within the wider system architecture and how accessible it is to external or adjacent networks,” according to the document. An organization’s attack surface broadens as more assets are exposed at the network edge. An effective exposure management approach involves evaluating an asset’s placement in the network, the type of connectivity it involves and the strength of cybersecurity controls.

Mitigation measures can include reducing the time of exposure and removing inbound port exposure so that connections to the OT environment can only be initiated from within the network. Entities must also manage the risks posed by obsolete technology, by replacing the relevant devices when possible and shoring up defenses around equipment that cannot be replaced yet.

The third principle is centralizing and standardizing network connections, which can be difficult to manage as the presence of third-party equipment on the system grows. This is also a factor in principle 4, which calls on entities to use standardized, secure protocols for communication so that data flows can be readily monitored for trouble signs.

Hardening the OT boundary is principle 5, with network segmentation and segregation providing “a robust first layer of defense [and being] even more effective when combined with native security capabilities within OT systems.”

“Because many OT systems are difficult to update or replace, the boundary becomes the primary defense against external threats,” the agencies wrote. “Organizations should therefore invest in modern, modular and easily replaceable boundary assets. … These assets offer greater flexibility for patching, upgrading and reconfiguring security controls. Importantly, they can be maintained without disrupting core OT operations.”

Principle 6 involves limiting the impact of compromise with “controls that extend beyond the OT boundary.” With effective controls such as network segmentation, organizations can limit the effects of contamination and inhibit intruders’ ability to move laterally within a system, a capability demonstrated recently by the China-linked Volt Typhoon group.

The next principle calls for logging and monitoring all connectivity, which the document called an organization’s “last line of defense.” Monitoring connectivity helps defenders identify abnormal activity that can indicate compromise.

Finally, organizations should create a plan to isolate their OT environments completely from external influences, which comprises principle 8. Strategies can vary based on the nature of the network. Site isolation, which involves removing all external network connections, is applicable for sites built on a flat network or with restricted security measures, while more robust security architectures may allow for specific services and network routes to be isolated with others left unaffected.