Stakeholders Approve 2 Key Resource Adequacy Policies

TULSA, Okla. — SPP’s Markets and Operations Policy Committee endorsed recommended revision requests from two stakeholder groups as part of the RTO’s effort to strengthen resource adequacy.

A fuel assurance policy (RR621) that further emphasizes conventional resources’ performance during a season’s most critical hours and reduces the socialization of the planning reserve margin’s capacity allocation passed easily with 92% approval during the July 16-17 meeting.

However, a second revision request (RR622) that establishes base planning reserve margins (PRMs) for summer 2026 summer and winter 2026-27 passed with three-fourths approval, but only after MOPC rejected an amendment to the motion that would have set the winter PRM at 36% instead of 33 (ironically, with only 33% approval). The summer PRM would be raised to 16% from 15.

During its June meeting, the Resource Energy and Adequacy Leadership (REAL) Team approved a 36% PRM over stakeholders’ concerns that the requirement was too soon and unrealistic to meet. (See SPP’s REAL Team Approves Base PRMs, Sufficiency Value Curve.)

SPP staff pointed out that the 33% PRM brought forward by the Supply Adequacy Working Group (SAWG) technically meets a 1-in-10 reliability standard; they intend to bring both PRMs to state regulators and the RTO’s board during their August meetings.

Omaha Public Power District’s Colton Kennedy, the SAWG’s chair, said the PRM’s requirement is intended to ensure that load-responsible entities are appropriately planning for capacity in both seasons. SPP’s 2023 loss-of-load study was the first in which staff directly analyzed seasonal risk beyond summer; it found a 15% PRM would not meet a 1-in-10 LOLE in either season.

“The complexity, the scope and the extent of questions by SAWG members by far surpassed all previous studies,” Kennedy said. “We didn’t previously have that in the historical [record] with an [LOLE] model. The inclusion of correlated outages, the inclusion of winter peak variability are the driving factors and are very reasonably supported. Very demonstrable, very objective in the work that we’re doing.”

He said SPP staff was very consistent with the 36% winter PRM recommendation, which created debate and discussion within SAWG related to the transition to a higher PRM by entities without sufficient capacity.

“They’re concerned about the generation interconnection process and being able to study resources and get them through this process [quickly],” Kennedy said.

Regardless of the final number, individual entities will have to step up, said Bill Grant, formerly with Southwestern Public Service and back on MOPC as a representative for XO Energy.

“The resources are out there. That doesn’t mean that there’s not some entities that have to scramble to meet this requirement,” Grant said. “Remember, if you approve these numbers, you are impacting utilities’ ability to get generation connected before any individual changes. There is an impact, and it’s kind of hidden.”

“For a regulated investor-owned utility, there’s not enough time to get new generation in,” Oklahoma Gas & Electric’s Brad Cochran said.

The fuel assurance policy stems from the 2021 winter storm, when SPP was forced to shed load for the first time in its 83-year history. Casey Cathey, the grid operator’s engineering vice president, said several heavily vetted approaches to fuel assurance failed before stakeholders coalesced around what he said is effectively “somewhat of a weight towards conventional resources during capacity critical hours in the winter season, in particular.”

Under the policy, an “after-the-fact” weighting will be applied to performance-based accreditation resources, based on critical system periods. The mechanism is designed to encourage increased performance by those conventional, or thermal, resources by quantifying their contributions to system reliability.

Noting that there can be a 100-degree differential between the northern and southern states in SPP’s footprint, Cathey said one thought holds that nonperforming resources should be targeted for their failures rather than raising the PRM.

“This revision request and this policy [help] directly address that socialization of planning reserve margin,” he said. “So rather than kind of go down this path of potentially having separate zonal planning reserve margins … this particular revision request and policy [help] to address that in a different way such that the northern resources that may already have winterization during extreme conditions and perform during those types of extreme conditions do not necessarily have to carry additional planning reserve margin accredited capacity beyond where the regional risk is.”

DISIS Waivers Endorsed

The committee endorsed staff’s proposal to file waiver requests with FERC that delay the start of the 2024 generator interconnection (GI) study’s first phase and pause the opening of the 2025 study cluster, easing conflicts with the RTO’s effort to clear the GI queue’s backlog and transition to a new planning process.

SPP staff said delaying the 2024 definitive interconnection system impact study (DISIS) cluster’s first phase will save customers up to $3 million by avoiding additional studies and will allow more accurate information for customer decisions. The 2024 DISIS first phase would begin after the 2023 DISIS second phase’s restudy is completed and posted in August 2025; without the waiver, it would start before the second phase of the 2022 and 2023 clusters and likely lead to unplanned restudies, staff said.

Natasha Henderson, senior director of grid asset use for SPP, said that if the 2024 DISIS Phase 1 began on schedule, it would assume $35 billion of transmission upgrades would be built from previous studies. “We know that’s not likely,” she said.

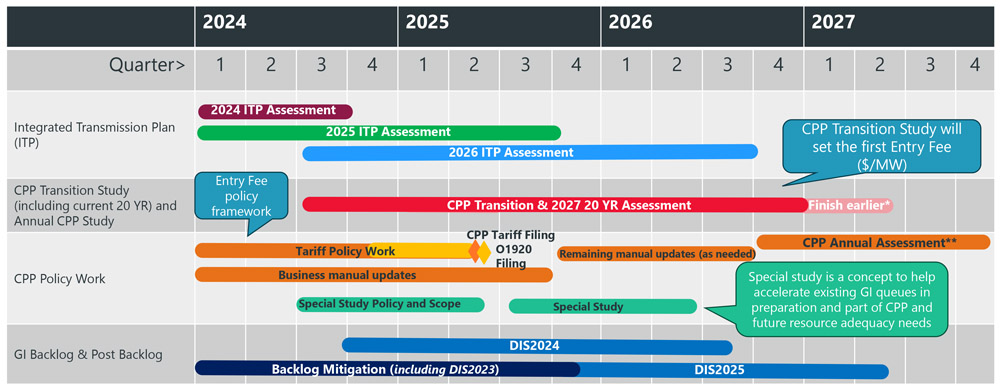

Pausing the 2025 DISIS’ open window will allow “additional optionality” for the grid operator’s transition to the consolidated planning process (CPP), scheduled to begin in late 2026 after a transition period. SPP said opening the 2025 DISIS would mean the cluster’s generation would “significantly” overlap with the CPP’s transition study and first annual assessment.

Golden Spread Electric Cooperative’s Mike Wise, who arrived for the MOPC meeting from the NARUC Summer Policy Summit, said FERC Chair Willie Phillips’ comments made it apparent he favors quickly connecting generation and building out transmission to support the new resources. Wise said words such as “delay” and “waiver” send the wrong message and could make commission approval difficult.

Staff said they believe they have agreed on messaging that should gain FERC’s signoff if the waivers are submitted as a package. They are also planning to schedule a meeting with commission staff.

“I think it’s going to be important that we convey the fact that this is not a pause,” Cathey said. “The message here is we can do things a little bit more efficiently. We’re not asking to pause the DISIS … it’s to try to accelerate and actually reduce the churn of the restudies.”

MOPC Chair Alan Myers struggled to get a second for the waiver requests from members who had previously expressed concerns about not having enough time to consider the proposal. Eventually, Evergy’s Derek Brown bravely raised his name tent to second the motion. It passed with 80.6% approval.

FERC’s approval of the waivers would enable the timely completion of backlog studies and allow time to further develop CPP. SPP in June posted its second study of the DISIS 2017-002 cluster, clearing the way for the 2018 DISIS’ second restudy.

The grid operator has 416 requests in the GI queue totaling about 84 GW in proposed capacity. That’s down from the original backlog of 1,139 requests for 221 GW of capacity. The backlog will be cleared when the 2023 cluster’s second restudy is posted in September 2025.

SPP staff and stakeholders have been working on the CPP and its associated cost-sharing mechanism since 2021. (See SPP’s Consolidated Tx Planning Just Beginning.)

MOPC in April approved a task force’s recommended policy for the CPP’s entry fee. A transition study to the new process, comprised of SPP’s current 20-year assessment and the first annual CPP analysis, is slated to begin this year and will set the first $/MW entry fee. The study is intended to align technical assumptions and scopes, yielding a “more robust” cost-sharing model that sets a specific frequency to avoid late charges.

SPP Adds Context on April Event

SPP told MOPC members that it is recommending several changes to its operational procedures following an April emergency event in Southwestern Public Service’s (SPS) New Mexico region that resulted in a 150-MW load shed lasting about two hours. (See “SPP, SPS Reviewing April Outage,” SPP Board of Directors/MC Briefs: May 7, 2024.)

Staff said they saw contingencies begin to develop April 28 as wind dropped from 16 GW to nearly 5 GW and load began to increase. Derek Hawkins, the RTO’s director of system operations, said that shortly after 7 p.m., an exceedance occurred on an SPP-SPS tie line.

Hawkins said his operators exhausted all available options within the constrained time frame in trying to address potential instability and were forced to shed load because of “immediate circumstances” and “evolving conditions.” SPP directed SPS to drop 150 MW of load at 7:43 p.m. to mitigate the unsolved contingencies. Load was restored by 9:41 p.m.

Hawkins said a post-event analysis revealed the importance of clear communication, robust coordination agreements and improved data integrity practices. He said operators were rebuffed twice when requesting energy from switchable units with ERCOT, which was dealing with its own tight conditions.

The recommendations include emphasizing timely and clear communications, evaluating improvements to operating procedures with ERCOT, and discussing coordination plans with neighboring entities.

SPS’ Jarred Cooley, director of strategic planning, said his own conversations with Hawkins and C.J. Brown, SPP’s senior director of system operations, policy and performance support, were beneficial and useful for the entire RTO footprint.

“We’ve met multiple times, had pointed, real in-depth discussions, and those were really useful for where we are with the recommendations,” Cooley said. “Obviously, it’s up to all of us to help support staff to have the tools that they need in real time so they act appropriately and that we can ensure good reliability for the system.”

Storage Self-charging Change

Members approved a pair of tariff revisions recommended by the Market Working Group related to storage and system dispatch.

RR635 would ensure market storage resources’ self-charging is identified and charged appropriately. The MWG said the change will increase alignment with FERC Order 841’s requirements for identifying and charging equitably for self-charging and will ensure that MSRs are subject to unreserved use when self-charging.

The FERC order found that energy storage resources should not be charged transmission costs when providing a market service. SPP currently dispatches MSRs based on economics and resource parameters; if the MSR is providing a market service, no transmission service is required.

RR628 would dispatch the system based on the system’s true obligation and price by removing load shed and emergency purchases. It would restore the load shed amount’s requested congestion prices from each forecast area to reduce the effects.

The RR635 and RR628 passed with 90 and 95% approval, respectively.

The unanimously approved consent agenda included nine other tariff changes that, if necessitating approval from the Board of Directors, would:

-

- RR595: Allow make-whole payments for instructed real-time incremental energy costs for day-ahead market committed and self-committed resources for offers under FERC Order 831 (adds changes after original MOPC approval in April 2024).

-

- RR602: Add process structure, tracking and improved criteria for evaluating potential transmission reconfigurations.

-

- RR610: Allow third-party cost estimate information and/or engineering judgment when creating a conceptual cost estimate to be used during a project study.

-

- RR615: Changes the RTO’s credit policy to introduce a portfolio-level mark-to-auction mechanism within the transmission congestion rights collateral requirement, thus mitigating default risk by updating collateral requirements to reflect the portfolio’s most recent valuation.

-

- RR619: Add application programming interfaces as an acceptable submittal process.

-

- RR623: Deploy a compensation mechanism to incentivize continued operation of resources whose studied retirements have identified one or more network upgrades as necessary to address reliability impacts that are unable to be completed prior to the projected retirement date. A unique contract will be developed for each retiring resource that details the eligible costs and a new schedule will be created detailing the allocation of the contract costs.

-

- RR627: Clarify that the turnaround ramp rate factor applies to energy and contingency reserve.

-

- RR631: Ensure consistent governing language and address corrections to previously published settlement calculations in RR613, RR556, RR578 and RR596.

-

- RR633: Clarify how SPP recalculates real-time balancing market outages and extends the repricing notifications.

The consent agenda also included the retirement of a remedial action scheme near Rapid City, S.D., upgrades to terminal equipment at one 115-kV and two 345-kV substations, and cost increases for a Western Farmers’ and an Omaha Public Power District’s projects.