The Trump administration has sued California over its electric vehicle law, claiming it amounts to an illegal, state-specific mileage requirement for carmakers.

The U.S. Department of Justice filed the lawsuit on behalf of the National Highway Traffic Safety Administration (NHTSA), which under the Energy Policy and Conservation Act is supposed to establish “uniform, nationwide vehicle fuel economy standards.”

“Oppressive, expensive electric vehicle mandates drive up costs for American consumers and violate federal law,” Attorney General Pamela Bondi said in a statement March 12. “California is using unlawful policies from the last administration to create exorbitant costs for our citizens.”

The lawsuit names the California Air Resources Board (CARB) as a respondent, arguing that its carbon and zero-emissions vehicle mandates are related to fuel economy standards because they effectively increase fuel economy, which is determined by how much carbon is emitted from a vehicle’s tailpipe.

“CARB’s standards and mandates also undermine and conflict with NHTSA’s congressionally assigned role in establishing nationwide, uniform vehicle fuel economy standards,” the lawsuit said. “CARB’s CO2 standards and ZEV mandates create a patchwork of inconsistent regulation for vehicle and engine manufacturers in an area where Congress imposed a uniform, national approach.”

The Environmental Defense Fund called the lawsuit “reckless,” saying the ZEV standard protects Californians from health-harming and climate-destabilizing pollution.

“California’s standards are firmly anchored in our nation’s clean air laws,” EDF Associate Vice President Peter Zalzal said in a statement. “For more than half a century, and across both Republican and Democratic presidential administrations, California has adopted standards that cut pollution and result in enormous health benefits for people across the state.”

DOE Announces Funding for ATTs

The U.S. Department of Energy announced a $1.9 billion funding opportunity to accelerate upgrades to the nation’s power grid, saying the investments will meet rising electricity demand and resource needs while lowering costs for consumers.

DOE said the “Speed to Power through Accelerated Reconductoring and Other Key Advanced Transmission Technology Upgrades” opportunity builds on the Grid Resilience and Innovation Partnerships program, which offered up to $10.5 billion in funding over five years to states, tribes, utilities and others to strengthen grid resilience and innovation. (See DOE Announces $2.2B in Grid Resilience, Innovation Awards.)

“Thanks to President Trump, we are doing the important work of modernizing our grid so electricity costs will be lowered for American families and businesses,” U.S. Secretary of Energy Chris Wright said in a statement March 12.

DOE wants concept papers by April 2, and full applications are due May 20. The agency expects to make selections in August.

The funding was welcomed by the WATT Coalition, with its Executive Director Julia Selker saying ATTs can help address affordability.

“American utilities have demonstrated that ATTs could unlock gigawatts of grid capacity and save billions in electricity costs if scaled across the country,” Selker said. “This funding will help utilities scale up their ambitions and timelines for transmission grid modernization.”

A new MIT study posits that while retail electric rates are higher in states that have renewable portfolio standards, the standards are not to blame. Instead, utility-scale wind and solar generation show a weak correlation with lower prices, the authors say.

More likely drivers of rate increases include cost-recovery mechanisms for rooftop solar embedded in certain tariffs, grid-hardening necessitated by climate change and the proliferation of data centers.

The correlation between renewable energy policies and electricity prices is relatively straightforward, but correlation famously does not imply causation, and as the title suggests, much of the study is devoted to separating and explaining the factors and causes at play.

Professor Christopher Knittel, MIT Sloan’s associate dean for climate and sustainability, and Fischer Argosino, a graduate researcher at the MIT Center for Energy and Environmental Policy Research, analyzed U.S. electricity and utility spending data from 1998 to 2023, including residential prices, power generation mixes, utility spending and state renewable portfolio standards (RPS).

They said the opposite rate impacts they found for utility-scale and distributed renewables are due partly to the fundamental differences in their design.

“Energy generated by large-scale solar plants, for example, comes with lower transmission, distribution and maintenance costs for utilities, and these efficiencies can be passed on to the consumer,” Knittel said in the news release.

But rooftop solar creates a two-way system out of distribution networks that were designed for a one-way flow from central generation plants to consumers, the authors said. They found this bi-directional flow was strongly correlated with higher operations and maintenance costs, as utilities managed the complex harmonization of thousands of decentralized generators across an aging grid.

“Our antiquated distribution networks are struggling to manage these flows,” Argosino said. “When we defer essential grid upgrades while simultaneously incentivizing rooftop exports, we create an operational strain that inevitably shows up as higher costs on everyone’s utility bills.”

But not uniformly higher. State financial incentives for rooftop solar can shift some of the costs of maintaining the grid onto ratepayers who do not have solar panels, even though solar owners derive full benefit of the grid to power their homes and export their solar panels’ output.

This exacerbates existing inequities, the authors said — those who put solar panels on the roofs of their homes are likely to be wealthier than those who do not.

Knittel and Argosino say decarbonization need not be at odds with electric rate affordability, if policies can be updated to match the changes in technology.

They suggest prioritizing utility-scale wind and solar to maximize economy of scale, modernizing distribution networks and adjusting fee structures so that all who benefit from grid infrastructure contribute to the cost of its maintenance.

The research is built on data from the U.S. Energy Information Administration, FERC and the Lawrence Berkeley National Laboratory. The years studied span a period before, during and after the widespread adoption of state RPS.

Although large loads are not new to California or the West, CAISO is now formulating technical standards that address their potential boom over the coming years.

Developing the standards is a critical step to ensure artificial intelligence data center and electric vehicle large loads will reliably and safely interconnect to CAISO’s grid. The ISO established a working group on the issue last year and opened a new large loads initiative Feb. 27.

“Large loads are a topic of extreme urgency and interest lately, especially with the emergence of artificial intelligence,” Danielle Mills, CAISO principal of infrastructure policy development, said at a March 10 workshop. “But we also consider large loads to be more than just data centers and AI. While data centers do present the largest use case, we are also looking at things like electric vehicle charging, electrification of buildings, and industrial processes and agricultural processes and the like.”

CAISO’s 2025/26 transmission plan shows 4.5 GW of data center capacity online currently, with an additional 1.8 GW added by 2030 and 4.9 GW more by 2040.

“We do proactively plan for these types of large loads through the integrated planning process with the California Energy Commission,” Mills said. “We are always trying to stay ahead of any new demand for large loads, but we are aware that this is really dynamic space right now and that we are seeing increasing numbers of large load interconnection service applications at the utilities.”

CAISO is developing a definition of what constitutes a large load and new requirements for voltage and frequency ride-throughs, along with setting limits on rapid ramping and pulsating load levels. (See CAISO Examines ‘Pulsating’ Data Center Loads.)

One topic of concern is how large loads consume power or reduce load during grid disturbances, such as during a post-fault active power recovery (PFAPR) moment.

“Our mission is to ensure large loads continue to draw power from the grid during and following grid disturbances,” Ebrahim Rahimi, CAISO senior adviser for transmission planning, said at the workshop.

During a PFAPR, large loads will be allowed to reduce their power consumption during and immediately after severe faults, Rahimi said. However, after the fault is cleared and voltage returns to normal, the power consumption from the grid should be required to recover to — or close to — pre-disturbance levels within a given time, Rahimi said.

Another concern is persistent small load fluctuations. Even modest but continuous fluctuations in load can produce voltage flicker or unacceptable variations in local power quality, CAISO staff said in a large loads issue paper.

Over time, these load fluctuations might increase mechanical fatigue in equipment, such as in rotating machines and transformers. Requirements will need to ensure that persistent small-signal load variations remain within acceptable limits, staff said.

CAISO is also following NERC’s formulation of national standards for large loads, such as for computation loads from AI training centers. Rahimi said those standards will be ready for approval at the end of 2026, and NERC is planning a large load level 3 alert in May or June.

CAISO has not yet decided where large load technical requirements will ultimately be documented and enforced, he said.

“Although we are coming up with these technical requirements … how these requirements will be documented has not been decided at this point,” Rahimi said. “The whole idea is to come up with these requirements and ensure reliability, and then at a later stage a decision will be made about where to document them.”

CAISO plans to publish a straw proposal in April that includes technical requirements, transmission service offerings and cost-allocation methods for large loads.

Forecasting is like driving a car blindfolded while following directions given by someone who is looking out of the back window. — Anonymous

Utility regulators beware: Not all forecasts are objective. Some are normative or biased, while others are based on science. When making important decisions, regulators must frequently choose between competing forecasts submitted by parties with varying agendas.

With potentially billions of dollars at stake, regulators need to reconcile the “forecast” discrepancies. Just as important but often overlooked, regulators also need to know the range of plausible forecasts and the risks associated with accepting one forecast over others. The risks triggered by uncertainty can play an important role in regulatory decisions.

Much of the push for a particular decision, whether for long-term planning purposes, merger proposals, determining future utility rates or other matters, comes from interest groups.

Regulators should receive their forecasts, which are critical for decision-making, with a grain of salt. They should ask if the forecasts are self-serving or are they legitimate and reflect objective analysis? Gaming by different stakeholders can present regulators with biased forecasts, which would require special regulatory-staff expertise to uncover.

Hedging Under Uncertainty

Often ignored, regulators should hedge their decisions to account for the inherent uncertainty associated with forecasting the future. A rational decision-maker would tend to respond to future unknowns by exercising caution in committing to a major action today.

Ken Costello |

Regulators therefore should require utilities and other parties to submit a reasonable range of forecasts to justify their positions. Basing a large investment or other major decision solely on the “best guess” forecast, or the future deemed most likely to occur, can result in substantially higher costs relative to the best action determined ex post facto with actual outcomes. In other words, an avoidable risky decision is more likely when based only on information provided by a “best guess” forecast without considering other possible futures and their implications for the right decision.

A range of forecasts or scenarios can help regulators quantify and evaluate the risks associated with individual decisions, related to electric-generation planning, energy efficiency initiatives or other actions, then judge whether the risks are intolerable. Uncertainty requires regulators and utilities to ask if the possible maximum losses from a particular decision are large enough to disqualify that decision from further consideration?

I use the term “forecast” to encompass both 1.) the future outcome that is most likely to occur (i.e., the “best guess” or single-point forecast) and 2.) a future outcome that is less likely to occur based on an alternative set of assumptions like economic conditions, the price of electricity, the price of substitutes for utility electricity, and the economics of renewable energy.

Some analysts refer to “best guess” forecasts as reference forecasts when they reflect the future with the highest probability of occurrence. The forecast is based on a set of events the forecaster expects will occur or considers more likely to occur than other events. If one has to choose a single forecast with a bet of $100 on the line, what would it be? It would presumably be the “best guess” forecast since the payoff would go to the person whose forecast lies closest to the actual outcome.

The regulator makes choices by using forecasts provided by utility stakeholders. First, it could approve the utility action based on the single-point price forecast; for example, the “best guess” demand growth of electricity 4% per annum, so the decision is contingent only on this forecast. This is a valid decision, however, only when 1.) the regulator places a high degree of confidence in single-point forecasts, and 2.) the consequences of incorrectly forecasting demand within a large range are minimal. For example, the preferred decision does not depend on whether demand growth is 2% or 4%. Otherwise, the regulator lacks access to valuable information to decide.

This situation is analogous to a person choosing a financial asset with the highest expected return, say, stock in a high-tech company, without considering its risk relative to other assets.

Most people would decide not to allocate all their investments to this high-return, high-risk asset. They would tend to diversify their investment portfolios to balance the tradeoff between return and risk. For financial assets, diversification implies an objective other than maximizing expected return or minimizing risk. Diversification reflects managing risk at a cost acceptable to the decision-maker given the degree and nature of their risk adversity.

Modern portfolio theory considers the inherent risk in various financial and physical assets and develops methods for aggregating investments to maximize the tradeoff between risk and return. In a different context, selecting a specific generation technology, or group of technologies, may stem from its lower risks relative to other technologies, even if the other technologies have lower expected levelized costs.

Using Different Forecasts

In our above example, as an alternative, the regulator could approve the utility action based on a range of demand-growth forecasts. It could, for example, review several forecasts from credible sources to select high, medium and low forecasts that represent reasonable demand-growth possibilities.

The evidence might show that demand-growth forecasts within a certain range result in the same preferred decision (e.g., expand generating capacity by a certain level by the year 2035). This sensitivity analysis makes the regulator more confident that the action taken will carry little risk unless it assigns a non-trivial probability to demand growth beyond the selected range. (The risk would be the opportunity cost of making a particular decision when another decision would have produced a better outcome after the fact.) Analysts consider such actions to be robust under a wide range of conditions. Robustness means that regulators would require less precision from a “best guess” forecast.

The regulator could approve the utility action after considering the cost of making the wrong decision based on erroneous demand forecasts (i.e., the loss function). The building of a generating facility based on demand growth of 5%, for example, could cost the utility an additional $100 million a year, compared with building the facility when the actual demand growth turns out to be 3%.

The regulator might want the utility to “hedge” its plan to moderate the cost (i.e., loss) from mis-forecasting demand growth. One idea is for the regulator to instruct the utility to take a wait-and-see approach as it accumulates more information to improve its forecasting accuracy before committing to a decision. To the extent that waiting reduces demand-growth uncertainty, the utility may reap an “option value” from an investment delay stemming from this uncertainty.

Loss Function

Rational risk-averse decision makers, implicitly if not explicitly, apply what is called a “loss function.” This function calculates the cost of a decision conditioned on a single forecast or range of forecasts that turn out to be wrong. Assume the decision to build a new gas-fired generating plant is contingent on the natural gas price being in the range of $3 to $5.

If the actual price is $7, the utility’s revenue requirements would be $500 million lower if it chose to build a solar facility instead. The $500 million represents a loss from relying on the wrong forecasts, which is inevitable when dealing with something as dynamic and unpredictable as demand growth, natural gas prices and other factors affecting the optimal decision.

The above example has a parallel to the current climate-change debate. Studies have shown that catastrophic consequences can follow if we do not take actions today to reduce greenhouse gases, but these consequences are highly uncertain, so much so that scientists cannot assign probabilities to their likelihood.

We may, therefore, spend money today to avoid an outcome that may never occur. The question is: What should we do today? The same question applies when an event is unlikely to occur but will cause a catastrophic outcome if it does. A society, group or individual that is risk-averse would tend to spend something today, for example buying insurance, to mitigate possible financial consequences in the future.

Distorted Incentives?

Although less guilty than in the past, utilities, in my observation, place excessive reliance on “best guess” forecasts to justify major decisions and fail to include a loss function in their forecasting exercise. One question still lingers: Does this problem reflect flawed decision-making, or do utilities and regulators deliberately produce and approve forecasts with overblown sureness and absent information on the negative consequences of erroneous forecasts?

The latter reason could be to buttress a particular, politically palatable action or, in some other way, advantageous to a utility or the regulator. One has to wonder.

Kenneth W. Costello is a regulatory economist and independent consultant who resides in Santa Fe, N.M.

New York energy storage and solar trade groups are seeking an immediate end to what they say is an effective freeze on interconnection of distributed storage facilities by the state’s largest investor-owned utility.

The New York Battery and Energy Storage Technology Consortium (NY-BEST) and New York Solar Energy Industries Association (NYSEIA) filed a petition for emergency rulemaking March 11 asking the Public Service Commission to restrict Consolidated Edison from applying an “unlawful and arbitrary” review standard for New York City storage projects.

They charge that Con Edison’s review process was implemented without legal justification, is causing irreparable harm to the storage industry and is exacerbating grid reliability concerns in the region. There was no need to change the way storage is studied under the state’s Standardized Interconnection Requirements, they argue, but if such a need did exist, there are much better ways to address it.

The utility stood by its actions.

“Con Edison supports battery storage as a critical part of New York’s clean energy transition, and the rapid growth in applications reflects strong market momentum,” Vice President for Distributed Resource Integration Raghu Sudhakara told RTO Insider via email March 11. He added, however, that the sector’s expansion must be carried out in a way that does not shift new infrastructure costs onto the utility’s ratepayers.

The disagreement has been fermenting for months, and it spans PSC cases on energy storage (18-E-0130), distributed generation and storage (24-E-0621) and New York City reliability needs (25-E-0764).

Battery energy storage systems (BESS), with their dispatchable output and lack of on-site emissions, are one of the potential solutions in the densely populated region; over 2,000 MW of capacity have been proposed.

On Aug. 15, 2025, Con Edison notified developers that it had placed on hold all BESS proposals seeking interconnection at seven constrained substations. It added 21 more substations to the list Sept. 16.

NY-BEST on Jan. 13 petitioned the PSC for “urgent action” on the utility’s move. It supported its call for immediate relief from Con Edison’s new restrictions on BESS interconnection with a white paper outlining suggested changes in interconnection and market rules to better enable storage to provide maximum value to the grid.

The infrastructure upgrade requirements resulting from Con Edison’s changes to the Coordinated Electric System Interconnection Review rendered most of the energy storage projects proposed in New York City economically unviable, NY-BEST said.

The organization also flagged the “fundamental misalignment between utility financial incentives and New York’s energy affordability goals”: A utility earns a regulated rate of return on capital expenses such as infrastructure upgrades, but not for facilitating third-party BESS interconnections.

The PSC on Feb. 20 solicited public comment on the petition but took no action to change or limit Con Edison’s practice.

On Jan. 14, Con Edison told the PSC there were 115 MW of operational BESS and 865 MW with executed interconnection agreements in the utility’s service area as of Dec. 31. But the interconnection queue for BESS proposals with 5 MW or less capacity had reached 2,500 MW, up 300% in two years.

That is a quarter of its 10-GW peak load in 2024, Con Edison wrote.

A problem, it said, was that the BESS proposals were being concentrated in areas with less expensive land and more favorable zoning — 65% of the storage megawatts in the queue would be supplied by just 10 of the company’s 63 substations. More than 20 substations were at or near hosting limits.

Because BESS typically would seek to recharge overnight, full buildout would make night peaks exceed daytime peaks and require new infrastructure that otherwise would not have to be built. Con Edison sought to put the developers on the hook for the resulting costs, which it said could run in the $100 million to $1 billion-plus range.

“As the market scales, storage must deliver real benefits to customers — not drive new infrastructure costs that show up on bills — which is why we are working with regulators and stakeholders to align growth with real-world grid conditions preserving grid reliability while also protecting affordability,” Sudhakara explained. “Without reforms, current policies risk shifting significant new costs to customers, undermining both affordability and the long-term success of storage.”

NY-BEST and NYSEIA in their petition attempt over the course of 26 pages to punch holes in the legality, accuracy and necessity of Con Edison’s steps to carry out the priorities Sudhakara cited.

They ask the PSC for an emergency rule to immediately block Con Edison from using the restrictive requirements for distributed storage applications and keep the ruling in place while it considers NY-BEST’s Jan. 13 petition.

As Nevada regulators consider NV Energy’s request to join CAISO’s Extended Day-Ahead Market, the debate over the independence of EDAM’s governance has reached a critical point.

EDAM proponents and opponents shared their views during a Public Utilities Commission of Nevada hearing March 10. The parties also sounded off in written testimony and rebuttal comments filed with the PUCN in February. The commission is expected to vote April 3 on NV Energy’s EDAM request.

“I recommend that the commission prioritize the independence of the market’s governance over most other factors,” David Patton, president of Potomac Economics, an independent market monitor for four RTOs/ISOs, said in written testimony filed on behalf of Powerex and Wynn Las Vegas, a luxury resort and NV Energy customer. Powerex has committed to joining SPP’s Markets+, a competing day-ahead market.

Through the West-Wide Governance Pathways Initiative and California Assembly Bill 825 of 2025, governance of EDAM and CAISO’s Western Energy Imbalance Market is being shifted to a Regional Organization for Western Energy (ROWE). Some see the ROWE as a means to alleviate concerns among potential market participants that CAISO, whose governing board is appointed by the California governor, plays too large a role in the markets’ governance.

Patton said the ROWE is “a very positive step” in the governance of EDAM and WEIM. But he said the entity is proposed to have minimal staff and that “critical roles,” including market operation, would remain with CAISO.

During the March 10 hearing, NV Energy representatives and intervenors in the case presented witnesses for questioning by the other parties in attendance. PUCN Chair Hayley Williamson presided over the session.

Attorney Curt Ledford with Davison Van Cleve grilled Stacey Crowley, CAISO’s vice president of external affairs, about EDAM governance. Ledford represents Powerex and Wynn Las Vegas.

Ledford asked Crowley to read aloud Section 345.5(a) of the California Public Utilities Code, which directs CAISO to “conduct its operations … consistent with the interests of the people of the state.”

“When you read ‘the state,’ do you understand [that to mean] the state of California, not the state of Nevada?” Ledford said.

“Correct,” Crowley responded.

Ledford asked Crowley about the steps needed to establish the ROWE. While the ROWE has an interim board, it doesn’t yet have staff. A consumer advocate office must be established, and a service agreement needs to be drawn up between the ROWE and CAISO. That agreement must be reviewed by the California Public Utilities Commission for conformance with AB 825 and likely will need FERC approval.

CAISO wants to wait until the permanent ROWE board is in place before negotiating the service contract, Crowley said.

“Would it be fair to say that this entire ROWE exercise could be for naught if CAISO doesn’t pursue it?” Ledford asked.

Crowley disagreed.

“The [ROWE] could exist without California participation,” she said, later clarifying that the ROWE “could take on other Western services if they so choose.”

In response to Ledford’s questioning, NV Energy attorney Roman Borisov asked Crowley whether the Pathways Launch Committee has the most control over the Pathways Initiative at this time. Crowley said yes, noting that the committee has broad representation from across the West and industry sectors.

Until the ROWE takes over governance, EDAM and WEIM are being overseen by the Western Energy Markets Governing Body, which has shared authority with the CAISO Board of Governors.

Without NV Energy, EDAM would lose a large and central piece of its footprint.

David Rubin, NV Energy’s federal energy policy director, said Section 345.5 of the California Public Utilities Code was adopted before CAISO was running a regional market. He noted that AB 825 added Section 345.6, which allows California utilities to participate in a CAISO market that has independent governance if the FERC tariff for the market includes a requirement to respect the authority of each participating state. That authority includes setting procurement, resource adequacy, environmental, reliability “and other public interest policies.”

The language “reflects a clear recognition that the regional markets — including the EDAM — must accord equal respect to the policy interests of all participating states,” Rubin said in written rebuttal testimony.

Rubin said market participants and regulators must have confidence in the overall fairness of a market’s governance.

He said other key reasons why NV Energy chose EDAM are the company’s positive experience in the WEIM; expected costs of day-ahead market implementation; EDAM’s expected market footprint and interconnectivity of participants; and transmission work within the footprint that will enhance interconnectivity and supply diversity.

Additional reasons are EDAM’s market design and projected financial, reliability and environmental benefits.

“These factors favor the EDAM over Markets+,” he said.

Oregon and Washington lawmakers are exploring ways to build new transmission independent of the Bonneville Power Administration as electric sector stakeholders in the Pacific Northwest worry about the agency’s struggle to build transmission fast enough to keep up with aggressive clean energy laws and increased load.

BPA paused certain planning processes in 2025 to consider how to address nearly 61 GW of transmission service requests. The agency presented several proposals to reduce the queue, but concerns have been raised that many of the efforts would go into effect after the 2030 deadline for utilities in Oregon and Washington to meet strict greenhouse gas standards.

Former BPA Administrator Randy Hardy has argued the issue lies with the states’ respective clean energy laws, which he said set off a “gold rush” among developers, leaving BPA to solve the issue of building enough transmission to keep up. His comments received support from utilities and other organizations during BPA meetings. (See BPA Tx Planning Overhaul Prompts Concern for Northwest Clean Energy Compliance.)

For Gamba, the issue is not the law’s requirements but rather that BPA, which controls approximately 75% of the region’s high-voltage transmission, has failed to build enough transmission.

“I’m less concerned with HB 2021 and the law as I am with the fact that we are still burning fossil fuels in the state of Oregon to supply energy to a rapidly growing load. That needs to come to a screeching halt,” he said. “But the only way that’s going to happen is if we build more transmission.”

As a federal entity, BPA does not have to follow mandates imposed by the Oregon legislature. The agency has focused on its preference customers — publicly owned utilities that rely on it for generation — and failed to realize “they are the backbone of the transmission system in the whole Pacific Northwest,” Gamba contended.

The situation worsened in 2025 after approximately 200 employees accepted a “deferred resignation” buyout offer under President Donald Trump’s effort to slim down the federal government, according to Gamba.

BPA declined to comment for this story, but the agency has noted its efforts to build out transmission and generation.

For example, when BPA paused its transmission planning processes to deal with the 61 GW of generation in its current interconnection study, it identified 16 GW of late-stage projects that are being integrated at a rate of roughly 1 to 1.5 GW per year, with the goal of integrating the full 16 GW by 2035, according to the agency.

As for transmission, the agency secured $773.8 million in transmission capital for 2025 with the goal of doubling transmission capital execution by 2028. It plans to issue awards to contractors in March 2026 that will cover a 10-year period with a maximum value of $25 billion to build and modify lines.

BPA also launched its $5 billion Grid Expansion and Reinforcement Portfolio initiative in 2023 with the aim of building 23 new transmission lines and substation projects.

However, Gamba said BPA was “pretty nonresponsive” even before staffing cuts, adding that he doubts the agency will “start building significant new lines anytime soon.”

Instead, the Democratic lawmaker thinks Oregon should take matters into its own hands. Gamba presented a bill in 2025 aimed at creating a transmission authority (TA) and intends to revive that effort in 2026.

“We just need some entity to act like an adult in the room and actually start developing the transmission that we need,” Gamba said.

A map over BPA’s transmission assets within the Pacific Northwest | BPA

The TA would explore where transmission is needed and begin the siting and permitting process. It then would work with utilities or third parties to get lines built. The approach has found success in New Mexico and Colorado, according to Gamba.

When asked about Gamba’s initiative, Oregon Gov. Tina Kotek’s office noted that the governor issued an executive order in November 2025 aimed at streamlining transmission siting and permitting approvals.

The order recognized that “a coordinated, statewide approach to planning and designating transmission corridors is essential to long-term infrastructure development that will support economic growth and ensure clean energy can be delivered efficiently and reliably to consumers.”

The governor’s office is working with the state’s Department of Energy on developing the framework, which is expected to be completed in Fall 2026 to support policy discussions next year, according to a spokesperson.

In an email to RTO Insider, JD Podlesnik, Portland General Electric’s senior director of transmission delivery, said the utility is ready to work with BPA and other regional entities to expand transmission.

Podlesnik noted that PGE has added more than 3,000 MW of clean energy and storage to the grid and recently finalized agreements for an additional 1,000 MW of clean energy resources, “making steady progress toward customer-driven clean energy targets.”

“At the same time, transmission capacity remains a key challenge across the region, both for reliability and clean energy targets,” Podlesnik said in the email. “BPA plays an important role in expanding the transmission network and accelerating the interconnection of new generation resources. Continuing to execute on BPA’s Grid Expansion and Reinforcement Portfolio is one of the critical steps in addressing those constraints.”

Washington Issues

Oregon entities are not alone in grappling with transmission constraints and compliance with clean energy laws. Washington utilities face a similar situation.

A study by Energy and Environmental Economics predicts that accelerated load growth and aging power plant retirements will create a resource gap in the Northwest starting at about 1.3 GW in 2026 and expanding to almost 9 GW by 2030. That is approximately the load of the state of Oregon.

For context, BPA’s White Book released in May 2025 projected the Northwest would have about 27.9 aMW of total (not just federal) generation available in 2026.

As is the case nationwide, data centers and electric vehicles are the primary drivers behind the expected load growth.

And just as in Oregon, Washington’s Clean Energy Transformation Act (CETA) requires all electric utilities in the state to become greenhouse gas-neutral by 2030 (allowing for use of offsets and other programs) on the way to generating all power from emissions-free resources by 2045. It also prohibits utilities from serving their Washington customers with any coal-fired generation after 2025. (See Washington Agencies Adopt New Rules to Implement CETA.)

But again, lack of transmission poses challenges for utilities to meet the law’s requirements.

There is collaboration across state lines to build more transmission independent of BPA, according to Washington Rep. Alex Ramel (D).

Washington lawmakers also seek to create a transmission authority under Senate Bill 6355.

“There is this sort of federal government monopoly in the space,” Ramel said.

Relying too much on the federal government as BPA struggles with staffing shortages “is a real concern,” according to Ramel.

“That, to me, is part of the reason why we need to be more expeditious about how we think about putting together these kinds of projects,” Ramel said in referring to a potential Washington TA. “Because if [BPA] is losing staff, that can only … impact negatively our need to be able to increase clean energy transmission opportunities.”

As for CETA, Ramel said he is not ready to “pull the plug on it.” He acknowledged the law was passed when the region did not have the same electricity use that comes with the development of AI and electric vehicles.

“I could be persuaded to have reasonable extensions or extenuating circumstances for utilities that really can’t meet those goals,” Ramel said. “But right now, I haven’t seen anything that persuades me that those goals can’t be met. We could revisit that in the future if we need to. Right now, I think we should stay full steam and let’s build out clean energy and let’s accelerate transmission.”

Puget Sound Energy, which is one of BPA’s largest transmission customers, has removed coal from its energy portfolio in accordance with CETA and is focused on providing 80% of its electricity from renewable or non-emitting resources by 2030-2033, according to Matt Steuerwalt, PSE’s vice president of external affairs.

Still, BPA’s ability to expand transmission capacity and allow new resources to come online “will have a major impact on our progress toward Washington clean energy laws,” Steuerwalt told RTO Insider.

“We also have to consider permitting and siting for energy infrastructure development undertaken by entities other than BPA, which is a major challenge to building any project,” he added. “We have been following the current legislation closely to see the extent to which it can address these and other issues.”

‘Morass of People’

But for Scott Simms, executive director of the Public Power Council, there are risks with creating separate TAs.

“I think that once you create an additional apparatus to try to do the exact same thing that other organizations are statutorily obligated to do, it’s going to create a morass of people trying to all do the same things,” Simms said.

Instead of solving the transmission challenges, the risk is that additional TAs would “exacerbate the very problem you’re trying to solve,” he added.

Rather, Oregon and Washington should fix the challenging operating environments they have created for consumer-owned and investor-owned utilities alike, Simms contended.

“There’s a variety of things on both the energy policy side with regards to resources and there are fixes on the transmission side when it comes to permitting and the planning process,” he said. “If the states were just to focus on how to best facilitate and streamline the transmission permitting and siting elements, that would be a huge help.”

Artificial intelligence has been framed by the Trump administration as ushering in a “new golden age of human flourishing, economic competitiveness and national security” for the U.S. should it win the race for computing systems that perform tasks normally requiring human intelligence.

But with the country’s drive to build up its AI ecosystem comes increased risks, both digital and physical.

Faruk Dziho, the business intelligence analyst and data solutions lead for the Texas Reliability Entity, says that while AI can strengthen grid reliability, it also creates risks if it is not managed properly.

“At the end of the day, it’s just a tool, and it’s not a replacement for engineers or operators. It excels at pattern recognition and forecasting when there is clean data,” he said during a Talk with Texas RE webinar March 10. “When it comes to some risk-mitigation strategies, there needs to be a robust data governance in building high-quality data pipelines with clear ownership, extensive validation model transparency and oversight.”

Texas RE added AI integration as a “moderate” risk in its 2024 Reliability Performance and Regional Risk Assessment, released in June 2025, saying the risks are “currently relatively unlikely to manifest themselves.”

“As AI increases in scale and integration, however, associated risks may increase in both likelihood and impact,” the regional entity wrote.

“That assessment itself is not set in stone. As adoption expands across the industry, both the probability and severity of those risks may rise,” Dziho said. “We’ll continue to monitor developments and adjust the assessments as the technology evolves.”

The Texas Interconnection grew faster than any other region in 2025, with demand increasing 5% through September when compared to the same period in 2024, according to the U.S. Energy Information Administration. The agency has said it expects demand to increase by more than 9% in 2026.

Dziho told his online audience that AI carries risks that demand robust mitigation strategies. AI-driven load growth could lead to cybersecurity vulnerabilities that can be exploited faster with AI-powered tools and systems, adaptive malicious code that bypasses security controls, and data poisoning.

“Artificial intelligence basically makes it easier for attackers to generate phishing attacks by generating thousands of personalized emails instantly or scanning for vulnerabilities faster,” he said.

Because AI systems use massive amounts of data collection and typically include confidential and/or sensitive information, data privacy controls must be effective in reducing the risk of breaches, Dziho said.

“We need to secure artificial intelligence workflows,” he said. “The field is changing constantly. There are new threats that we find out daily.”

FERC has initiated a show cause proceeding based on concerns about the lack of provisions in ISO-NE‘s tariff enabling fixes to incorrect payments to or from market participants.

The order, issued March 10, comes following multiple recent requests from participants for waivers to return improperly accrued funds to the RTO.

The commission wrote the ISO-NE tariff “appears to be unjust and unreasonable because it lacks provisions that would enable ISO-NE to return amounts that it erroneously charged to market participants and to accept payments from market participants that were erroneously or improperly received in ISO-NE’s markets.”

FERC established settlement procedures in 2024 for a waiver request by Canal Marketing to return improperly accrued funds from the RTO’s Inventoried Energy Program. The commission approved a settlement between ISO-NE and Canal in early 2025. (See FERC Establishes Settlement Procedures for ISO-NE IEP Exit Request.)

In fall 2025, Brookfield Renewable Trading and Marketing requested a waiver to refund ISO-NE for four months of improperly received capacity market revenues. FERC established settlement proceedings for this waiver request on the same date as its show cause order.

ISO-NE has 60 days to justify its existing tariff rules or explain what changes it would make if FERC requires it to make tariff changes addressing the issue.

“If ISO-NE prefers to propose revisions to the tariff on the subject of this order, then it may do so pursuant to its applicable [Federal Power Act] Section 205 filing rights,” FERC added.

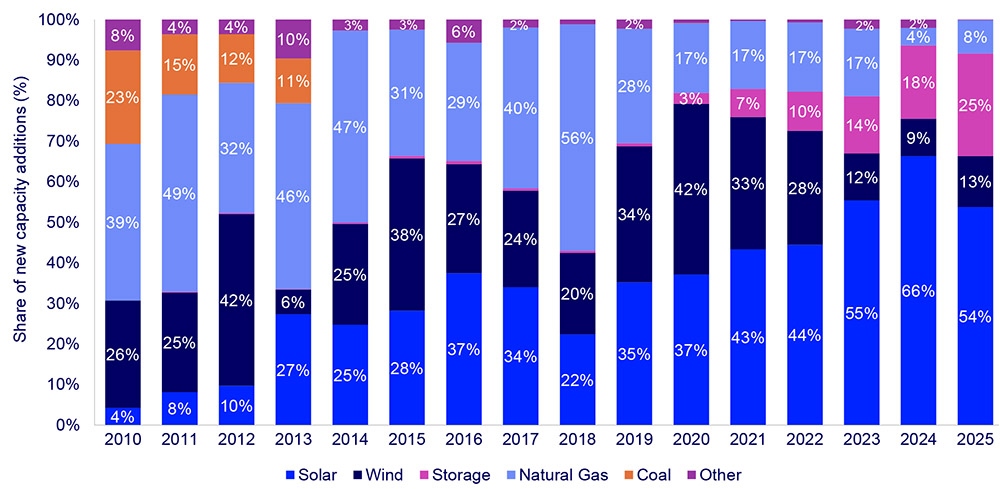

Nearly 40% fewer U.S. solar power projects reached completion in the fourth quarter than in the third quarter as developers pivoted to start new projects in time to qualify for tax credits.

But while the 43.2 GW of solar capacity installed in 2025 was 14% less than in 2024, it nevertheless made up 54% of all new capacity added to the U.S. grid in 2025, the Solar Energy Industries Association (SEIA) and Wood Mackenzie said in a new report March 10.

2025 was the fifth straight year solar was the top source of new U.S. power generation capacity.

Looking ahead, the analysis predicts nearly 500 GW of additional photovoltaic capacity will be installed nationwide through 2036, even with the headwinds created by a president hostile to renewable energy. The costs of alternatives are high enough that solar remains a value proposition even without the lucrative investment and production tax credits that are being sunsetted sooner than originally planned.

“It’s clear that solar will continue to be the dominant source of new power capacity in the United States, even as gas generation continues to grow,” said Michelle Davis, head of solar at Wood Mackenzie and lead author of the report. “Strong demand growth combined with escalating costs of new gas plants will allow solar to remain competitive, even without tax credits.”

The “U.S. Solar Market Insight 2025 Year in Review” acknowledges the many uncertainties facing solar power. The baseline prediction of 490 GW more solar capacity by 2036 could be 11% higher or lower due to a series of factors, but the projected variation for utility-scale solar (6-7%) is much less than for distributed solar (23-28%).

Distributed solar is more sensitive to changes in retail rates and cost-impacting policies such as tariffs and import guidance, the authors state, while utility-scale projects are more likely to be affected by interconnection bottlenecks, supply chain constraints and power demand growth.

Another unknown factor is President Donald Trump.

Trump’s signature on the One Big Beautiful Bill Act in July 2025 moved forward the expiration of tax credits in the Inflation Reduction Act.

Projects now must start construction before July 4, 2026, or be placed into service by Dec. 31, 2027, to qualify for full tax credits. This led to significantly fewer completed projects in 2025 than expected — the value of completing them was outweighed by the imperative of beginning work on the next projects in the pipeline in order to safe harbor their tax credits.

While the president relentlessly boosts fossil fuels over renewables, he does not show the same level of hostility to solar panels as to wind turbines. There even have been a few hints in early 2026 of solar opposition softening among some MAGA influencers.

Solar power’s growth as a U.S. power generation technology is shown. | Wood Mackenzie

Whatever the motive for this turnaround, solar has some effective selling points in 2026: It is faster and less expensive to deploy than gas or nuclear; U.S. solar component manufacturing has expanded greatly; and battery energy storage systems to smooth out its intermittent performance are proliferating in number while decreasing in price.

SEIA interim President Darren Van’t Hof indicated that while the federal uncertainty has not gone unnoticed, it is not insurmountable: “Solar and storage continue to dominate new capacity additions to the grid despite policy headwinds. American households and businesses of all sizes are demanding solar + storage because they deliver fast, affordable power to help meet rapidly rising demand,” he said.

“Washington must deliver policy certainty for the market to work and to keep pace with growing energy demands. Without this certainty, less solar will get built and Americans will pay the price with higher energy bills.”

Even with this churn, all of Wood Mackenzie’s U.S. power projections show solar constituting nearly half of all U.S. capacity additions each year through 2060.

The 2025 outlook calls for an average annual addition of 44 GW through 2036, which is an increase over previous projections based on the increase in the near-term utility-scale pipeline and continued growth in energy demand expectations.