One new report flags risks entailed in the massive planned buildout of gas-fired generation, and another predicts a sharp continued rise in gas turbine prices.

The Institute for Energy Economics and Financial Analysis (IEEFA) on April 8 issued “The Misguided Stampede To Build Gas Power Plants,” which centers on the financial risks and long timelines associated with planning new gas power generation in the United States in the mid-2020s.

Wood Mackenzie on April 1 issued “The U.S. Gas Turbine Market: Navigating Manufacturing Scarcity and Demand Growth,” which predicts that gas turbines will command prices in the range of $600/kW by the end of 2027 — up 195% from 2019.

Commodity price spikes and the age-old law of supply and demand are at the heart of the reports.

To submit a commentary on this topic, email forum@rtoinsider.com.

IEEFA cited S&P Global’s January 2026 estimate that 133 GW of new gas-fired capacity has been proposed in the United States.

This newly built generation would be dependent on a fuel that is vulnerable to price spikes from weather or geopolitical events, IEEFA said. The simultaneous expansion of U.S. LNG exports would subject these power plants to further price volatility by linking the U.S. supply of natural gas to the world market.

Wood Mackenzie said the increase in prices for turbines follows an increase in demand for turbines. Global orders totaled 110 GW by the end of 2025, but global production capacity was only 60 to 70 GW per year, resulting in lead times of up to six years.

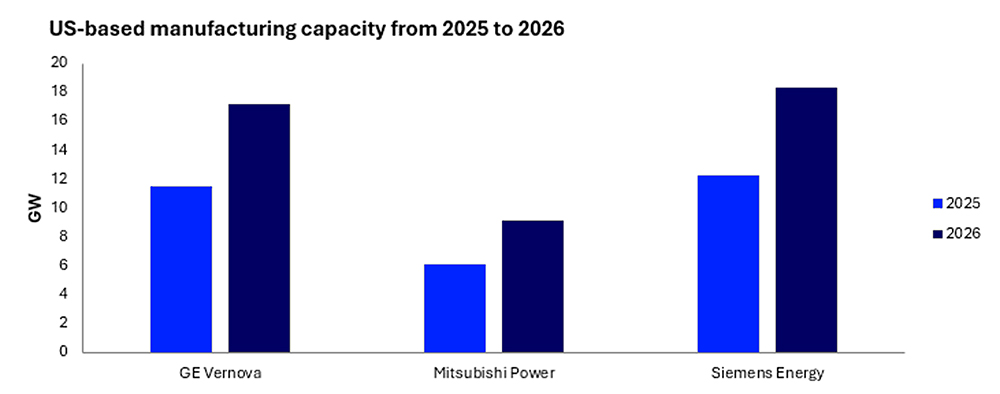

The research consultancy expects turbine orders to peak in 2026, and said the major turbine manufacturers — GE Vernova, Mitsubishi Heavy Industries and Siemens Energy — are investing in U.S. production capacity increases.

Wood Mackenzie pointed out that turbines are the largest single cost driver for a combined-cycle generation project but represent only 20 to 30% of the total cost. IEEFA said total costs for the current crop of proposals are running in the $2,500/kW range, roughly triple the price tag of projects built in the early 2020s.

Importantly, that total cost typically does not include the costs of financing or any necessary pipeline upgrades, nor contingency costs if the project runs too far behind schedule due to supply chain constraints or skilled labor shortages.

All of this inevitably is passed along to the consumer, IEEFA said, whether through regulated utility rates or competitive power market prices.

And the economics of gas generation raise the risk of stranded costs.

The report uses these points to argue for solar, storage and wind power development.

“Wind and solar do not share the shortcomings of gas. Their costs are not tracking its rapid upward climb, and the hardware is readily available,” said IEEFA energy analyst Dennis Wamsted, author of the report. “Renewable projects can be built in 18 to 36 months, and they have no fuel costs — ever. Paired with dispatchable battery storage, which continues to benefit from declining capital costs, renewables offer firm power and fixed costs on short development timelines.”

Wood Mackenzie painted a complex web of factors affecting the economics of gas-fired generation.

“This [turbine] supply constraint, compounded by six-year lead times and order books sold through 2027, has fundamentally shifted the market from fuel-economics-driven decisions to procurement-strategy-driven project viability,” said Aurora Tenorio, senior supply chain analyst at Wood Mackenzie.

“Despite the rush in demand for product, the market is also hampered by specialized labor shortages, component bottlenecks in hot-section manufacturing, and ongoing trade-related cost pressures that will continue to limit production throughput improvements. This has all compounded the issue and will affect U.S. power investments well into the next decade.”

Wood Mackenzie identifies data center expansion as the dominant force shaping the gas turbine market. It expects data centers to be the fastest-growing load on the U.S. grid between 2026 and 2031, increasing its power consumption 96%.

IEEFA notes that the U.S. Energy Information Administration and Wood Mackenzie project higher average natural gas prices in the U.S., due to increased exports and increased domestic consumption.

IEEFA said the economic competitiveness of gas-fired generation has depended on three factors — relatively low and stable costs for new turbines, low-cost fuel and low pipeline construction costs — that all seem to be crumbling now.

And IEEFA flags a possibility others have warned about: The data center industry may not grow as much or may not need as much electricity as some analysts predict.

“The stampede for gas makes no sense for consumers, investors or utilities,” the IEEFA report concludes.