IESO officials have broadened the eligibility for hydropower projects in the ISO’s upcoming Long Lead-Time (LLT) procurement, agreeing to accept separately metered expansions as “new build” projects.

Such expansions will be eligible to participate in both the energy and capacity streams of the LLT procurement, which the ISO created for resources that require at least a five-year lead time.

ISO officials had said previously that such expansions would not be eligible for the LLT procurement. But IESO’s Danielle D’Souza told stakeholders Feb. 26 that it changed its position in response to stakeholder feedback that such expansions may require longer design and construction cycles and would be unable to compete against wind and solar projects in its long-term procurements. (See IESO Holds Firm on Hydro Exclusion, Reserve Price in Long Lead-time RFP.)

“What that means is that hydroelectric expansions that are separately metered will be eligible to participate, and this is consistent with the treatment of separately metered expansions under” the pending Long-Term 2 (LT2) procurement, D’Souza said. While the LT2 procurement is limited to resources that can go into operation within four years, the LLT resources will have up to eight years to go into operation.

Pending a final directive from the Ministry of Energy and Mines, IESO expects to offer “rated criteria” incentives to developers by reducing their “submitted” price to an “evaluated” price for comparison against competing offers.

Developers who commit to sourcing 75% of materials and construction services from Canadian suppliers would receive a 2% reduction in their “evaluated” price. The ISO requested feedback on whether the incentive would impact supply chain decisions and whether a 75% threshold is achievable.

Developers making energy proposals will receive up to a 5% reduction for Indigenous economic participation and up to an additional 5% for projects located on tribal lands.

In addition to those incentives, capacity projects will be eligible for up to an additional 5% reduction for facilities that can offer more than the minimum eight hours of continuous energy.

“All of that is pending the final [ministry] directive, but we have a good sense of where that’s going to land now,” IESO’s Ben Weir said.

Prime Agricultural Areas

Weir said IESO expects the ministry to eliminate rated criteria incentives for projects locating outside of Prime Agricultural Areas.

“I think part of the reason why government has been more comfortable in the LLT context to [remove rated criteria] is because of the technologies that are at play,” he said. “Hydroelectric — unless you can prove me wrong — isn’t going to be built on ag land. … And when we’re talking about the [long-duration energy storage] technologies, by and large, the acres taken per megawatt of capacity is a lot smaller … than when we’re talking about wind [or] solar projects.

“I don’t expect government to change tack on that for the LLT,” he added. “But for full transparency, we have not had that discussion with them.”

Assuming the ISO receives a final directive from the ministry in March, Weir said it should complete the request for proposals and contract documents by mid-April. That would enable an Oct. 1 deadline for proposal submissions, with contract awards targeted for March 30, 2027.

Feedback on the supply chain disclosure provisions is due March 5, and comments on the rest of the materials are due March 12 to engagement@ieso.ca.

NEW ORLEANS — The Gulf Coast Power Association’s MISO–SPP Regional Conference showcased the rush to add resources, and panelists mused on which new trends could take hold in resource expansion.

David Mindham, a senior director at EDP Renewables North America, said today’s characterization that a sudden, steep demand for electricity emerged from nowhere is intellectually dishonest. He said more generation than what has been developed was essential for years.

“We have systematically built the shortage into the system today … by poor planning decisions,” Mindham said during the Feb. 23-24 conference. RTO planning relies on the “most conservative set of assumptions you could ever make” and keeps the system chronically underbuilt, he argued.

Far from its intended cost effectiveness, the lack of proactive planning is squeezing customers financially, he said. “We’ve actually needed the generation for decades.”

Wisconsin Public Service Commissioner Marcus Hawkins mulled whether “speed is a premium product” for which generation developers should expect to pay.

“Speed should be the expectation,” Mindham responded, adding that MISO and SPP contain many inefficiencies. He said developers flock to ERCOT not merely to site projects in Texas but because the grid operator offers speedy interconnections.

“If you want two-day shipping, you have to sign up for Amazon Prime,” Hawkins retorted jokingly.

Travis Kavulla, head of policy at the Texas-based Base Power, which installs whole-home batteries for a subscription, suggested that RTOs try out holding interconnection rights auctions. He said developers could bid on incremental capacity in auctions, similar to the Federal Communication Commission using competitive bidding to assign spectrum licenses. He said auctions would weed out any unserious large load developers.

“That solution is so obvious, but no one has pursued it with dynamism,” Kavulla said.

Beth Garza, a senior fellow at R Street Institute, said she is still waiting on the “too cheap to meter” nuclear generation that was promised in the 1950s. She said the industry might be at a tipping point where it is ready to embrace new technology and that small modular reactors could be the answer.

Energize Strategies’ Ted Thomas said he worries that the industry has become too natural gas-heavy and that he plays scenarios in his head before going to bed in which gas costs spike. Resource planners adding copious amounts of gas-fired generation are doing so based on assumed capacity factors, he argued. He predicted that gas capacity factors will “flatten out” and expose which gas plants were ultimately necessary.

Thomas cited President John F. Kennedy’s famous saying, “A rising tide lifts all boats,” before noting Warren Buffett’s retort on economic vulnerabilities: “It’s only when the tide goes out that you learn who has been swimming naked.” He predicted that some new gas plants will in time “show that we’ve been swimming naked.”

Southern Renewable Energy Association Executive Director Simon Mahan said that adding more generation, particularly battery storage, and interregional transmission is crucial.

“If these extreme weather events are going to keep happening, we need to be better prepared. … People are going to get hosed when they get their bills next month,” Mahan predicted of the late January 2026 winter storm. Gas prices that shot to $7 to $8/MMBtu during the winter storm are a “straight pass-through” on bills, he said.

Those who can afford it are increasingly turning to home battery purchases. “Everyone is getting nervous that the system, today’s system, is inadequate,” Mahan said.

America’s Power CEO Michelle Bloodworth argued that the industry’s saving grace, as shown in NERC’s Long-Term Reliability Assessment, are the delays in planned coal plant retirements across 19 states. She said the postponements kept regions from going even redder in NERC’s assessment.

Bloodworth argued that coal plants can be modernized and cleaned up to run for another 30 years, with the help of the Department of Energy’s more than $500 million in funding. She said it’s going to take “time and sustained investment” to bring in new baseload power to replace coal.

Mahan said subsidizing coal plants should take place at state-level proceedings, not federally. He also said NERC’s LTRA has “significant deviations from reality,” noting that it ignored MISO’s expedited interconnection queue.

“There’s a disconnect between the visuals and the narrative that’s going on in that report,” Mahan said. He said coal lobbyists and environmental advocates can agree on the destination — a reliable, decarbonized grid — just not the timelines they envision to get there.

The Queues

Natasha Henderson, SPP’s senior director of grid asset utilization, said the 108 GW of nameplate capacity in her RTO’s queue is about twice its current load.

SPP also has 40 GW of signed interconnection agreements under its belt, the bulk which are slated to be online by 2030. But Henderson said the RTO forecasts its demand will be 93 to 100 GW by 2035. She likened the queue to “a bit like a bubblegum machine,” where it can be shaken and just a few gumballs pop out.

Of SPP’s 40 GW in generator interconnection agreements, only 7% represent thermal resources, Henderson said. Meanwhile, she said, SPP’s fast-track interconnection queue comprises 70% thermal generation. In its regular queue, SPP is seeing fewer standalone solar or storage projects and more hybrid formats.

Henderson said it’s not a controversial statement that the current transmission infrastructure won’t be able to handle the demand that’s being planned. “The longer we wait to build, the less load we’re going to connect.”

MISO’s queue, on the other hand, contains 190 GW, down from a peak of more than 300 GW in 2025.

“The interconnection queue has been one of the most visible challenges for MISO,” said Robert Kuzman, executive director of external affairs.

Kuzman said MISO remains challenged by 70 GW of generation projects that have signed interconnection agreements but remain unbuilt or unfinished. He said developers behind those projects should answer hard questions as to whether their projects are viable and withdraw them if not. That way, he said, transmission capacity might be freed up for other generation proposals.

The queue has shrunk rapidly on the Trump administration’s announcement that it would phase out renewable generation tax incentives, Kuzman said. He added that although MISO’s expedited queue comprises mostly gas generation, proposed battery storage is also taking up a small chunk.

Kuzman said MISO likely could have benefited from four-hour battery storage during Winter Storm Fern in late January. The RTO might not have had to call up load-modifying resources if it had a larger storage fleet, he said.

“It’s something that’s coming in MISO. There’s definitely a place for it as we continue to add as much solar as we are,” he said.

Henderson agreed that storage would be useful at SPP, though its market ruleset isn’t fleshed out. She said the resource type could help with ramping needs and likely could bridge a gap in intermediate planning needs.

The challenges of meeting accelerating load growth pervaded discussions at EMPOWER 26, Yes Energy’s annual summit, where speakers discussed the changing federal regulatory paradigm, long-term market trends, demand flexibility and how to responsibly interconnect hyperscale data centers.

Data center development is the largest driver of forecast load growth across much of the country, though electrification and manufacturing growth also contribute to the rising demand, multiple speakers noted. More than 400 industry professionals attended the conference Feb. 25-27 in Boulder, Colo.

Building adequate supply to meet this demand is “one of the big challenges that we face,” said Jesse Jenkins, associate professor of energy systems engineering and policy at Princeton University. In his keynote address, he cited Grid Strategies’ forecast for 5.7% annual growth in U.S. power demand over the next five years.

Significant uncertainty remains regarding which sources of supply will arise to meet this demand and whether these sources will align with decarbonization efforts.

To date, much of the focus from data center developers has centered around fossil resources, with 49 GW of gas-fired generation added to interconnection queues across the country in 2025, Jenkins said. With gas turbine supply chains constrained, developers have turned to dirtier, less efficient gas-fired technologies, including converted jet engines. Coal also saw a resurgence in 2025, in part because of load growth from data centers.

“Gas will continue to play an important role in meeting incremental demand growth,” said Eric Brooks, manager of Americas gas pricing at S&P Global Energy. He said he expects new gas demand from new LNG exports and data centers to cause “slightly more elevated” gas prices over the next five years.

Dan Spangler, senior director of analytics at Natural Gas Intelligence, said the trajectory of data center development could have a significant impact on the need for gas generation in the longer term.

“If we get a lot of demand coming on and renewables and batteries can’t meet it, then gas is a natural place to step in to meet that,” he said. “But similarly, if data centers turn out to be a bust and demand is way lower than what people are expecting, then I would expect renewables and batteries to potentially significantly eat into gas’s share, possibly sooner rather than later.”

Beyond the direct climate and health impacts, reliance on polluting resources to meet load growth could undermine data centers’ social license, Jenkins said.

“Growing public opposition is becoming a key impediment to development,” he noted, citing an analysis that found 25 U.S. data centers totaling at least 4.7 GW were canceled in 2025 following local opposition.

But while renewables and energy storage make up the bulk of new capacity coming online, elimination of the federal tax credits has created uncertainty for the renewable projects unable to access the expiring incentives. The Trump administration’s assault on domestic offshore wind also has created major long-term questions about the future of this industry in the U.S.

Judd Rogers, vice president of new project development at Scout Clean Energy, said rising demand coupled with the shift in federal energy policy has created a complex mix of headwinds and tailwinds for clean energy developers.

While the “demand for our product is incredible,” he said, “the current administration is calling out our industry as being stupid or dumb or causing cancer. It’s obviously incredibly challenging, and the roadblocks that they’ve been able to put up have been incredibly challenging to navigate.”

Demand Flexibility

Several presenters stressed the importance of demand response and flexibility for limiting infrastructure costs and peaking needs.

While data centers tend to have flat load profiles, Jenkins expressed optimism about technological advancements enabling demand flexibility within the facilities. He highlighted a study recently published in Nature Energy which found the potential for 25% demand flexibility for an AI data center in Arizona using software that enables the designation of computing tasks by priority.

Coupled with on-site battery storage, this represents a “truly scalable solution” to minimize the need for major transmission upgrades, he said.

Former FERC Chair Jon Wellinghoff, now the chief regulatory officer at Voltus, said demand response participating in the wholesale markets can play an important role in meeting near-term supply challenges.

“You need load flexibility if you’re going to get these data centers in place quickly,” he said.

PJM’s initial proposal for the backstop auction would not allow load management to participate. But Wellinghoff said it is not clear that the governors and the White House intended to exclude demand response resources.

“From a regulatory standpoint, FERC in orders 719 and 745 clearly said that demand response and load flexibility should be comparable to generation [and] should be included in the auctions,” he said.

Referencing a recently announced deal between the U.S. and Japan over a 9.2-GW gas facility in Ohio, he said the auction should not prioritize foreign-owned generation plants over demand response capabilities that can be provided by American businesses.

Transmission Expansion

Speakers also emphasized the role of transmission expansion in meeting supply needs.

“We’re trying to figure out how we’re going to serve all of this load we’re seeing,” said Gordon Drake, director of market design and analysis at ERCOT. “One way we can do that is we can approve a bunch of transmission projects that will make it to where the effective load carrying capacity of all this generation is high. We can do that now with generation that’s already in the ground rather than waiting and hoping that a new combined cycle gets built in that load pocket.”

ERCOT is betting big on transmission expansion, pursuing the development of a series of 765-kV lines throughout the state to help meet demand growth. Its Strategic Transmission Expansion Plan includes 2,468 miles of new 765-kV lines and has a total estimated cost of about $33 billion.

Jack Farley, chief commercial officer at Grid United, laid out an even broader vision for expanded interregional transmission connectivity across regions throughout the U.S.

He highlighted the potential economic benefits of the company’s Three Corners Connector transmission project to connect Pueblo, Colo., and the SPP system in Oklahoma.

The line should be in service by late 2030, he said. Without transmission connection, Colorado tends to be “sitting on 30% of its reserves … when SPP needs it most,” he said. “When SPP is in its top 3% of net load hours over the last five years … there are about 3 to 4 GW of stranded reserve capacity in Colorado.”

When connected, “this creates capacity, and this can be accredited just like wind and solar with the standard models,” he said.

Projects like the Three Corners Connector “are gigawatt-plus capacity additions that are ideal for data centers and large flat loads because it’s cheaper than natural gas turbines,” he said.

RTO Insider is a wholly owned subsidiary of Yes Energy.

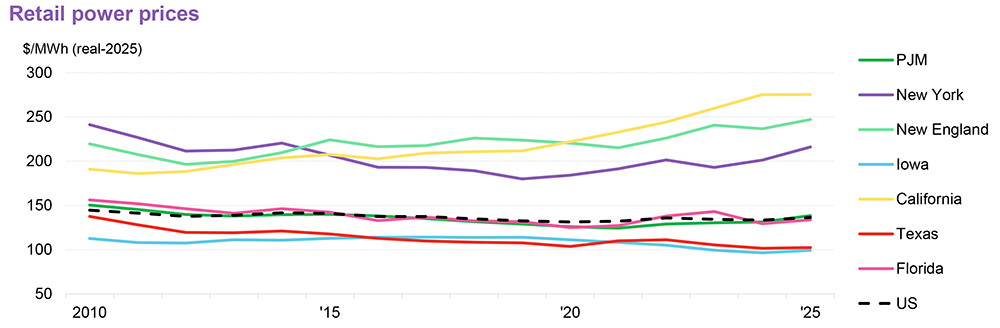

According to the Business Council for Sustainable Energy’s 2026 Factbook, U.S. consumers spent “slightly less” on electricity in 2025 than they did in 2024.

The extent of that “slightly less” is not calibrated in dollars and cents, but you can see in the charts above ─ from BloombergNEF, which compiles the annual report ─ that total energy costs, which include gasoline, and electricity costs are wiggling down, though not by much.

Other charts in the factbook show that while wholesale and retail electricity prices have gone up and down over the past 15 years, they are not appreciably higher today than they were in 2010 ─ with some notable exceptions. After 2021’s dramatic winter storm spike, wholesale prices dropped in Texas, while retail prices are up in New England and California (though BNEF sees a 2025 rate plateau in California).

Retail power prices: How high or low can they go? | BloombergNEF

The factbook and its charts provide the kind of widely quoted data points often used to try to persuade consumers the U.S. electric power industry is working hard to keep their utility bills affordable.

But when I first saw these charts at an advance press briefing for the factbook Feb. 17, what quickly came to mind were the panel discussions I had heard on affordability and transparency at the National Association of Regulatory Utility Commissioners’ Winter Policy Summit in D.C. the week before.

Affordability can be defined in many ways, depending on context. Affordability in the abstract ─ what a utility or regulator thinks of as affordable ─ may have little if any relationship to affordability as experienced day to day by consumers looking at electric bills that keep going up.

David Springe, executive director of the National Association of State Utility Consumer Advocates, talked about his 86-year-old mother, who had upgraded her HVAC system to improve efficiency at the home she has lived in for decades but was still seeing higher electric bills.

“There’s a level of frustration going on out there right now with customers not feeling like they can control their budget and control their usage, and no matter what it is that they do, their bill keeps going up,” Springe said during the panel on affordability that closed the conference. “This is a conversation we seem to have every year at NARUC. … This interaction with customers and giving customers tools and power and ownership is something we always struggle with.”

The pressing issue of demand growth ─ primarily from data centers ─ has only heightened consumers’ and consumer advocates’ anxieties, he said.

“The scary part to me [is that] the answer seems to be that … we’re going to build our way out — spend a lot of money building our way out of this problem — and I’ll tell you that does not give the consumer advocate community the warm and fuzzies.”

Springe pointed to the October 2025 forecast from the Edison Electric Institute, the trade association for investor-owned utilities, that its members will spend $1.1 trillion in capital investments over the next five years ─ a figure that could already be out of date.

For example, in its most recent earnings call Feb. 10, Duke Energy raised its projected five-year capital expense plan 18.4%, from $87 billion for 2025-2029 to $103 billion for 2026-2030.

“Those costs are going to end up in rates,” he said.

‘Growth Must Pay for Growth’

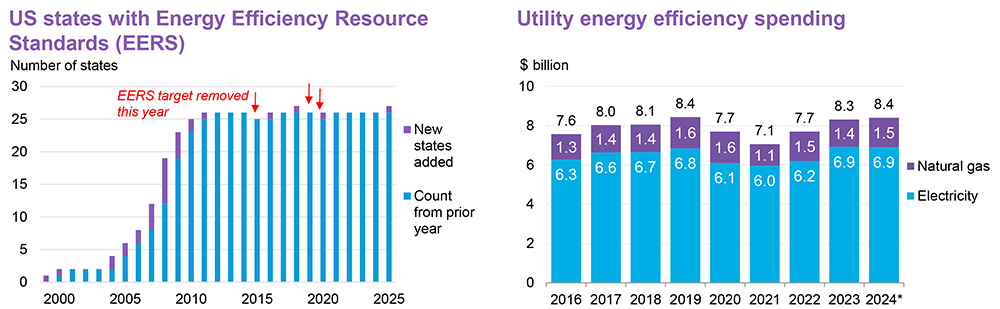

Energy efficiency and better customer communication are the perennial low-hanging fruit ─ and as Springe noted, ongoing pain points ─ of the industry’s efforts to bridge the gap between different definitions and experiences of affordability.

According to the BCSE factbook, utility spending on efficiency programs ─ for electric and natural gas companies ─ has never exceeded $8.4 billion per year over the past decade, or less than 1% of the $1.1 trillion or more the IOUs will invest in new generation and the grid over the next five years.

Efficiency: The low-hanging but underfunded fruit of affordability. | BloombergNEF

Policy signals also are mixed. Currently, 27 states and D.C. have some kind of energy efficiency standard, setting targets for utilities to reduce electricity consumption with efficiency measures. Arizona is expected to repeal and revise its efficiency rules, despite broad public opposition.

Springe cautioned that communication promoting efficiency must be ongoing but balanced. If bombarded with messages about energy conservation, customers could tune out and not react to cut consumption in real emergencies, he said.

Matthew Ketschke, president of Con Edison of New York, agreed that while “it’s very important to constantly [engage] our customers on the value of energy efficiency, I do have concerns about going out right before either a high-load day for heat or cold and sending [an appeal to conserve]. … It gives the impression that we, collectively as the people responsible for their energy delivery systems, did not do our jobs in making sure that we have enough capacity for safe, reliable delivery of energy. … You kind of want to save that messaging for when … there’s no room for failure.”

If efficiency can be a hard sell, the challenge is even greater for convincing consumers of the potential benefits of building new generation and power lines to meet demand growth from data centers, calling for levels of transparency that are not exactly utilities’ or regulators’ strong suit.

The new mantra at the state and federal level is that “growth needs to pay for growth,” according to speakers at a separate panel on demand growth and large loads.

“Whether it’s a regulated or a deregulated area, you need to be trying to develop policies where new large loads are accompanied by new large generation, and you grow the system in a balanced way,” said Nick Elliot, senior policy adviser for the White House’s National Energy Dominance Council.

Several reports have provided case studies in which adding new generation for large loads has helped mitigate rate increases by spreading the fixed system costs of utility bills to a larger customer base. The caveat is that “there are obviously a lot of different models for connecting these loads … [which] may not be replicable and scalable in every scenario,” said Lakin Garth, director of emerging technologies for the Smart Electric Power Alliance.

Trump’s Election Year Ploy

How these ideas play out at the state level is very much a moving target. A map and database compiled by SEPA and the NC Clean Energy Technology Center show that individual states, their regulators, utilities and high-tech customers are trying out different approaches.

According to Christopher Ayers, executive director of public staff and consumer advocate for the North Carolina Utilities Commission, it is too early to say if the various rate structures or contracts being proposed will consistently or substantially lower rates.

Transparency is critical, so the public can understand any proposed rate structures or other regulations on large loads, Ayers said.

Jose Esparza, senior vice president for public policy at Arizona Public Service, pitched for his company’s model, which uses a formula to allocate costs to large load customers so they pay 45% of the utility’s requested rate increase, compared to 14% for residential customers. APS is also providing “special contracts” for data centers looking for fast-track interconnection and service.

“What we’re offering is what we’re calling a subscription rate, where you’ll take a portfolio of resources,” he said. “The customer will have to put up a certain amount of collateral, agree to pay a 20-year or 15-year agreement, to pay down and appreciate those costs as much as possible.”

APS is facing opposition to its special contracts from Arizona Attorney General Kris Mayes, a former utility commissioner who argues they lack transparency and public oversight. APS customers might also not see a 14% rate increase as particularly affordable, she notes.

The call for transparency could be opening a new front in industry and regulatory debates, where definitions are again varied and subjective.

“We can say growth pays for growth, [but consumers] are not really understanding that because there is a national narrative going around on both sides of the aisle that’s convincing folks that that’s not really happening,” Esparza said. “Utilities and large load customers have to do a better job of partnering with their regulators and our customers to ensure them that we are taking this seriously.”

Briana Kobor, head of energy market innovation for Google, agreed that “transparency is key. We are screaming from the rooftops that we are here to pay our fair share of costs. Help us to show that to the public and to the regulatory ecosystem. … The math is different in every single jurisdiction. Maybe [the data center share] is 70%; maybe it’s 80%. Maybe it’s 12 years; maybe it’s 15 years. Behind that minimum revenue guarantee is a math problem, and it should be compared with what your rate is and what your marginal costs are, what you are going to be investing in, and it’s a conversation that we’re going to be having for years and years to come.”

All of which makes President Donald Trump’s State of the Union announcement of a “Ratepayer Protection Pledge,” committing the AI giants to providing their own data center power, little more than an election-year ploy aimed at co-opting and taking credit for the hard, innovative work being done on the ground.

Electricity Value vs. Cost

And, as the consumer advocates are saying, it is too early to gauge the impact of the state-level initiatives, let alone a vague federal effort.

“Once there is a large load tariff in place, the load projections kind of drop,” North Carolina’s Ayers said. “It’s because now you’re able to quantify impact; now you’re going to have to start putting money where your proposal is … and that has an inherent heightening effect in terms of our need to sharpen our pencils and get to that number. … There’s also a perception amongst the consumer advocate community that large load is still running around from jurisdiction to jurisdiction, trying to find the best deal.”

The bottom line is that, at least for the near term, electric bills are going up, and definitions and perceptions of affordability will have to evolve.

U.S. LCOEs: Again, what’s high and what’s low? | BloombergNEF

Morgan Scott, vice president of global partnerships and outreach at the Electric Power Research Institute, said that as the cost of electricity goes up, so does its value, which should be a key theme in industry messaging to customers.

The bring-your-own-power imperative for hyperscalers may be a first step, but it raises some tricky questions.

Ayers has a major concern about long-term risk and costs shifting back to consumers. If we’re building 40-year assets ─ like natural gas or nuclear plants ─ what happens after a data center’s 15- or 20-year contract runs out, he asked. Will consumers be left to pick up the tab for the remaining 20-plus years?

That’s a rabbit hole the industry has yet to go down, he said.

Look who’s buying clean energy | BloombergNEF

The way forward for both affordability and transparency will involve figuring out what combination of technologies ─ generation, transmission and flexible demand response ─ are going to deliver the highest value and reliability for consumers, while raising rates the least.

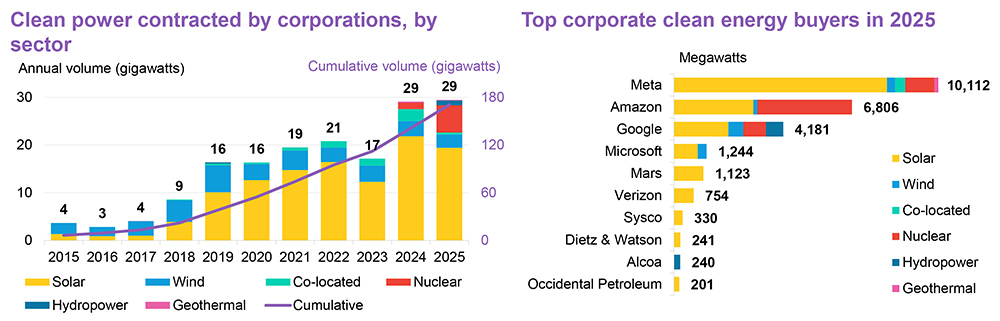

While it is by no means the only or most reliable measure of affordability, the levelized cost of electricity remains a useful marker. On that basis, the BCSE factbook shows that renewables remain the most affordable, which is likely at least one consideration for the corporations and investors still betting heavily on them.

Not surprisingly, Meta, Amazon, Google and Microsoft are leading the pack. Corporations are all about affordability.

WASHINGTON — Congress needs to disallow states from vetoing Clean Water Act permits for interstate natural gas pipelines, FERC Chair Laura Swett said Feb. 24.

With natural gas production expected to shatter records this year, Swett joined oil and gas executives at the annual Energy Aspects Conference to urge Congress to advance permitting reform legislation that would ease the construction of natural gas pipelines.

“We can do everything to speed up the process,” Swett said. “But the court will overturn that pipeline if any state in the right of way of that pipeline does not grant the [Clean Water Act] permit.”

An attorney with Vinson & Elkins representing energy companies prior to her nomination, Swett said much of the regulatory expense and uncertainty stems from prolonged litigation over permits. “Congress has to not allow states to effectively veto federal projects.”

FERC Chair Laura Swett | Jason Dixon Photography

The Clean Water Act’s Section 401 authorizes states to certify that a proposed activity, be it construction of a pipeline or a hydroelectric dam, won’t harm water quality. States and environmental groups have used this provision and other laws to block pipeline construction, such as the 303-mile-long Mountain Valley Pipeline, which now transports natural gas from the shale production areas of northern West Virginia to Virginia. Its construction was allowed only after President Joe Biden signed the Fiscal Responsibility Act of 2023 into law.

FERC is once again considering Williams Companies’ 124-mile Constitution Pipeline, for which New York state declined to issue a water permit. On the day of the conference, the state argued in a filing that the commission must dismiss the petition and not force its Department of Environmental Conservation to “engage in yet another round of wasteful administrative review.”

Joining Swett on the panel was Toby Rice, CEO of EQT, the largest natural gas producer in the Appalachian Basin. He agreed that supply is not the problem; infrastructure is.

“Our biggest challenge in natural gas is the infrastructure that it takes to move this to market,” Rice said. “While we spend maybe 50 cents getting it out of the ground, I’ll spend $1 [to] $1.50 getting it to market.” It costs two to four times as much to ship natural gas to Boston as to extract it from the ground, he said.

Despite concerns about fracking, the shale boom has achieved record production. However, Rice said, “the pipeline cancellation movement is the only time environmentalists have been successful in shutting down development.”

Approximately 65% of total pipeline capacity built in 2025 consists of intrastate pipelines, continuing the trend of intrastate pipeline builds outpacing interstate capacity additions, the U.S. Energy Information Administration reported Feb. 25.

Congress has been debating permitting reform for years without success, but Mike Sommers, CEO of the American Petroleum Institute, is optimistic about its prospects under a Republican-controlled Congress.

“I am more optimistic today than I was three months ago that we actually could get something done this year with this Congress, because it is becoming a political imperative for politicians to do this because of affordability,” Sommers said.

Meeting Power Demand

While much of the conference was focused on the oil and gas production and celebrating the 10th anniversary of the first LNG cargo shipment from the Sabine Pass Terminal, panels also discussed rising power demand from data centers and potential solutions.

Speaking prior to Swett and Rice in an earlier panel on policy perspectives, Deputy Energy Secretary James Danly acknowledged that rising electricity demand is “undeniable.”

He said the Department of Energy is taking steps to ensure reliability while making sure rates remain affordable.

“We are doing everything we can to reconductor as many of the strategically important transmission lines to reduce congestion costs and to improve reliability,” Danly said.

Deputy Energy Secretary James Danly speaks to M2M Advisors CEO Majida Mourad. | Jason Dixon Photography

FERC is working its way through the voluminous comments on DOE’s proposal, with the department asking for action by April 30 (RM26-4).

President Donald Trump alluded to data centers bringing their own generation in his State of the Union address to Congress the same day as the conference, saying he had reached a “a new ratepayer protection pledge” with major tech companies to build their own power plants.

Calling it a “unique strategy never used in this country before,” Trump said this approach will ensure that “no one’s prices will go up, and in many cases, prices will go down for the community, substantially down.”

Trump did not disclose the names of the firms involved in the pledge, and it is still unclear what exactly it will involve. The president is planning to host officials from Amazon, Google, Meta, Microsoft, xAI, Oracle and OpenAI at the White House to sign the pledge March 4.

In the conference’s final panel, Invenergy CEO Michael Polsky said the U.S. grid must be improved before new generation sources are added.

“You build roads, and then you build houses,” Polsky said. “The same goes with electricity; you build up a grid first.”

PSEG is working to meet the energy needs expressed by New Jersey Gov. Mikie Sherrill (D) and is gearing up to help with the potential expansion of the state’s nuclear and gas generation fleet, the utility’s CEO said in its fourth-quarter earnings call.

CEO Ralph Larossa, after presenting the company’s expectation of 6 to 8% compound annual growth through 2030, said it could be even higher given some of the initiatives drafted by the state to increase its energy generation capacity and curb rate increases.

“We have been cooperatively working with policymakers since last November,” Larossa said on the Feb. 26 call. He also cited a bill introduced in recent days that would establish a new natural gas power plant procurement program at the Board of Public Utilities “and incentivize the development of new natural gas power plants in the state.”

“This gas bill pairs with an earlier bill that establishes a new nuclear procurement program, also within the BPU, that was introduced at the start of this legislative session,” he said. He added that the utility would “support legislation that would increase competition for generation supply, should New Jersey decide to pursue new in-state generation.”

The utility is “well positioned to help meet that need,” he said. “We have sites with grid connection capability and pipeline supplies, as well as the in-house expertise to build new supply here in New Jersey with prevailing wage labor.”

Sherrill, who took office Jan. 20, has prioritized tackling the energy problem. She released two executive orders on her first day that sought to freeze electricity rates and implement a range of policies designed to improve energy efficiency and stimulate the development of new generation. (See New N.J. Governor Rapidly Confronts Electricity Crisis.)

As part of that effort, the BPU issued a request for information to the state’s four utilities probing their response to issues such as how to speed up connection and how they are complying with new rules instituted in 2025 to modernize the grid. (See N.J. Looks to Utilities for Solar Expansion Answers.)

Asked about specific issues that may concern PSEG as it works with the governor’s administration, Larossa said, “the way we’ve been thinking about it is trying to help policymakers think through and then enable the opportunities for gas or for new nuclear.”

Big Nuclear, Not SMR

Introduced on Feb. 24, bill A4491 would direct the BPU to launch a request for expressions of interest in developing new natural gas power plants that could generate at least 1,100 MW. The legislation sets out the conditions that would need to be met for the BPU to approve the plant and gives the agency authority to grant financial support in the form of a Natural Gas Development Charge and Natural Gas Energy Certificates (NGECs).

PSEG neither owns nor operates gas plants, having announced plans in July 2020 to sell all its fossil plants, a task the company completed in February 2022, said spokesperson Marijke Shugrue. The utility owns and operates three nuclear plants in South Jersey.

Larossa did not specify what role the utility might play in the development of new gas or nuclear plants. Asked for clarification, the company referred RTO Insider to an article Larossa released after the election. It outlined the state’s problems — including the predicted generation shortfall — and called for the state to “immediately open a process to procure in-state generation.” Larossa added that “PSEG is ready to deliver new generation quickly and affordably.”

At present, however, New Jersey law prohibits regulated electric utilities from building or owning generation plants.

Asked on the earnings call about the company’s interest in hosting small nuclear reactors (SMRs) on its South Jersey site, Larossa said “if we were advocating, we’re advocating for — on a nuclear front — big nuclear. We think that that makes the most sense based upon our property and our footprint.

“We have a site that makes a ton of sense, where we have pipes, wires running to it already. SMRs, from our standpoint, would not be the highest and best use of our property, but one that would be open to people if that was really what folks wanted us to enable. Remember, our early site permit is technology agnostic, so we could go in any direction on that.” The U.S. Nuclear Regulatory Commission in 2010 issued an Early Site Permit for the site in 2010.

Q4 Results

PSEG reported 2025 net income of $2.11 billion ($4.22/share), compared to $1.77 billion ($3.54/share) for 2024. Net income for the fourth quarter was $315 million ($0.63/share), compared to $286 million ($0.57/share) a year earlier.

Black Hills Energy and PowerWatch are to join CAISO’s Western Energy Imbalance Market, extending the market’s geographical reach into South Dakota, the ISO announced.

Black Hills and PowerWatch, formerly known as BHE Montana, are to join the WEIM on May 6, five days after the scheduled launch of CAISO’s Extended Day-Ahead Market with PacifiCorp as the first participant, CAISO announced Feb. 25.

“We are honored to welcome Black Hills Energy and PowerWatch into the WEIM,” CAISO CEO Elliot Mainzer said in a statement. “The continued growth of our markets delivers real economic benefits to market participants and their customers and is a proven strategy for improved reliability and affordability throughout the region.”

Black Hills and PowerWatch are working with CAISO to complete readiness criteria by March. FERC must approve the readiness certification before they can join, according to the release.

With Black Hills joining the fold, the market’s footprint extends into South Dakota as WEIM’s twelfth Western state, CAISO wrote in a news release.

Black Hills serves 1.35 million natural gas and electricity customers in eight states. In January, the utility announced it had completed construction on a 260-mile, $350 million transmission expansion project to interconnect electric systems in Wyoming and South Dakota. (See Black Hills Completes $350M Tx Project.)

Under the WEIM implementation agreement signed by Black Hills Power and Cheyenne Light, the utilities agreed to register a new balancing authority to facilitate participation in the market by 2026.

The newly energized 260-mile line is part of Cheyenne Light’s FERC tariff and will be within the WEIM when the utility begins participation in May, according to Black Hills.

PowerWatch is a subsidiary of Berkshire Hathaway Energy. It is the second generation-only balancing authority committed to participate in the WEIM, CAISO stated, with Avangrid in the Northwest being the first.

WASHINGTON — Bill Gates-backed nuclear power startup TerraPower expects to break ground on its planned Natrium power plant in Wyoming within weeks, the company’s top executive said Feb. 24.

“We’re probably just a few weeks from the [Nuclear Regulatory Commission] awarding the construction license for our plant,” TerraPower CEO Chris Levesque told the annual Energy Aspects Conference at the Waldorf Astoria hotel in D.C.

Once the permit is in hand, TerraPower can begin building its 345-MW sodium-cooled, small modular reactor, which would be the first commercial venture of this nature to reach this stage. The company hopes to complete construction by 2031, after which it will seek a permit to begin operations.

“This will be really huge for us as a nation,” Levesque said, calling the project a key step forward in deploying the next generation of grid-scale nuclear reactors.

The U.S. needs these next-generation reactors to achieve parity with Russia and China, he argued.

At least eight commercial reactors featuring state-of-the art smart modular technologies are at various stages of licensing with the NRC, according to a tracker developed by the Nuclear Innovation Alliance.

Among them is an 80-MW small modular reactor being jointly developed by Dow Chemical and X-energy at Dow’s UCC Seadrift Operations along the Texas Gulf Coast. X-energy submitted a construction permit for it in March 2025.

The Trump administration has prioritized nuclear power to meet rising demand from data centers to power artificial intelligence applications and replace aging baseload generation. Just the day after the conference, the Department of Energy announced a $26.5 billion loan package for Southern Co. subsidiaries Alabama Power and Georgia Power that includes licensing and upgrades for about 6 GW of nuclear generation. (See related story, DOE Loans $26.5B to Southern Co. for Infrastructure Upgrades.)

Federal regulators also are moving to streamline licensing and regulations. DOE recently created a new categorical exclusion under the National Environmental Policy Act for certain advanced reactor projects, while the NRC is developing a new regulatory framework for advanced reactors under Parts 53 and 57. Those rules are expected to be finalized by the end of the year, NRC Commissioner David Wright said at the conference.

Still, challenges remain. “To say that nuclear power is not without its challenges would be ingenuous,” Deputy Energy Secretary James Danly said in an earlier panel.

Deploying first-of-a-kind technology, such as the kind Oklo and TerraPower are pioneering in the U.S., comes with its own challenges, including access to financing, reliable supply chain and a skilled workforce, as well as supportive government policies, NIA CEO Judi Greenwald said during a webinar Feb. 26 on the project tracker.

At a meeting about 260 miles away from its headquarters, the California Public Utilities Commission ordered 6 GW of new capacity to meet forecast data center and electric vehicle loads — among other new demand — in the state.

More than half of the 6 GW will come from Pacific Gas and Electric and Southern California Edison, according to the final decision approved by the CPUC on Feb. 26.

“Over 800 pages of comments on the proposed decision alone is a testament to how seriously stakeholders take this work,” Commissioner John Reynolds said at a voting meeting held in Santa Maria City Hall.

The original proposed decision, issued in January, said no more than half of the 6 GW could come from energy storage resources, but the revised final decision threw the requirement out.

“The imposition of a cap on the amount of storage to be procured would be unwise,” the decision says, “because we have no wish to discourage the development of longer-duration storage beyond four-hour lithium-ion batteries, which imposing a cap could do.”

Instead, the revised proposed decision mandates at least one-quarter of the new capacity must come from long-duration energy storage or clean, firm power.

“This change was partly driven by the fact that these resources have value that may not always be captured by our existing renewable portfolio standard and resource adequacy compliance,” Reynolds said.

However, Commissioner Matt Baker said he is “weary of any kind of carve out for specific technologies. The integrated resource planning process really is designed to say how do we get to zero carbon emissions at the lowest possible costs.”

Most of the stakeholders supported the 6 GW procurement order, except for Protect Our Communities Foundation (PCF), the final decision says.

The CPUC should analyze and report on the expected data center load in the utilities’ service areas before requiring costly utility-scale resources and corresponding transmission expenditures, PCF said in Feb. 6 comments. It also said the commission should determine how much of that load — as well as load from future adoption of EVs and building electrification — can be met by facilitating customer-sited generation instead of requiring ratepayers to foot the bill.

The CPUC acknowledged it lacked sufficient evidence regarding its asserted bases for requiring procurement of an additional 6 GW, PCF added.

“The commission should not burden ratepayers with the costs of additional procurement unless and until the commission has first established with reliable evidence that such a need exists in the first place,” PCF said.

Some stakeholders questioned other assumptions in the decision, such as VoteSolar, which said data centers could be built in lower-cost states such as Oregon and Arizona, thereby lowering the CPUC’s assumed future data center load. Drought conditions could lower the amount of hydropower available to California as well, the organization added.

“I find that, like many stakeholders, there is a lot of uncertainty surrounding the medium-term forecast,” Baker said. “I think it would be pragmatic to reevaluate the medium-term forecast … in the next couple of years to make sure we right-sizing things.”

In Feb. 11 comments, CAISO said if only 2 GW of procurement is required in 2030 and no more until 2032, then the electric system could be vulnerable to reliability risks in 2031.

“Issuing a procurement order well ahead of the identified need will provide LSEs and developers with the necessary lead time to complete procurement processes and navigate potentially long development timelines,” CAISO said. “This proactive approach is critical to avoid capacity shortfalls in 2029 to 2032.”

Commissioner Darcie Houck added it is “critical that we closely scrutinize procurement amounts and that we should all be concerned about any excess procurement that could needlessly add to ratepayer costs.”

SPP has secured two new commitments for its day-ahead Markets+, as Grant County Public Utility District and Tacoma Power in Washington state announced their intent to join.

The utilities are to begin participating in Markets+ and SPP’s real-time market Oct. 1, 2028, joining at least seven other entities that have signed agreements, the RTO announced Feb. 27.

“The addition of Grant County PUD and Tacoma Power reflects the continued growth and momentum of Markets+ across the Pacific Northwest,” said Carrie Simpson, SPP vice president of markets. “These utilities recognize the value of a market built on strong governance, reliability and cost savings for their customers. We look forward to our continued partnerships building a market that works for the entire Western Interconnection.”

The two utilities are both parties to a $150 million funding agreement SPP signed in April 2025 with eight Western entities to develop Markets+. However, neither utility had announced when it would join, according to SPP’s announcement. (See SPP Launches Markets+ Phase 2 With $150M Secured.)

Arizona Public Service, Powerex, Public Service Company of Colorado, Salt River Project and Tucson Electric have said they will begin participating in Markets+ when it goes live in October 2027. Grant County PUD and Tacoma Power, with Puget Sound Energy and Chelan County PUD, are to join in 2028.

The Bonneville Power Administration announced in May 2025 it intends to pursue participation in Markets+ over CAISO’s Extended Day-Ahead Market, but a group of nonprofits has challenged BPA’s decision in the 9th U.S. Circuit Court of Appeals. (See related story, Nonprofits Tell 9th Circuit BPA’s DAM Decision Poses ‘Imminent’ Harm.)

Grant County PUD serves approximately 56,000 customer meters in Central Washington and operates more than 2,100 MW of hydroelectric generation, according to SPP’s announcement.

Tacoma Power, meanwhile, serves 186,975 customers in Pierce County.

“Grant PUD’s mission is to deliver reliable and affordable energy to our growing customer base,” John Mertlich, the utility’s CEO, said in a statement. “Joining SPP’s Markets+ is a strategic step that strengthens our ability to do so. Additionally, joining Markets+ aligns us with a growing coalition of utilities across the West who are working toward a more reliable, interconnected and economically integrated regional power grid.”