Power prices were higher in most states in 2025 compared to a year earlier. A study from Lawrence Berkeley National Laboratory found that was due to multiple factors, which varied by state.

The study is an update of an earlier iteration and adds prices from 2025 to the initial study’s dataset from 2019 to 2024, Brattle Group Principal and study co-author Ryan Hledik said in an interview. (See LBNL Study Examines Drivers Behind Higher Power Prices in Some States.)

“The drivers of changes in electricity prices are nuanced,” Hledik said. “There is often, I think, a tendency to want to point to one single factor that is leading to increasing electricity prices. And this analysis supported the work that we did previously and showed that it’s more complicated than that. There are a number of factors that can push rates either up or down depending on which market you’re in and where you’re located.”

The report will be updated regularly, as this release and the initial version from October 2025 have proven valuable to those interested in the electric industry, he added.

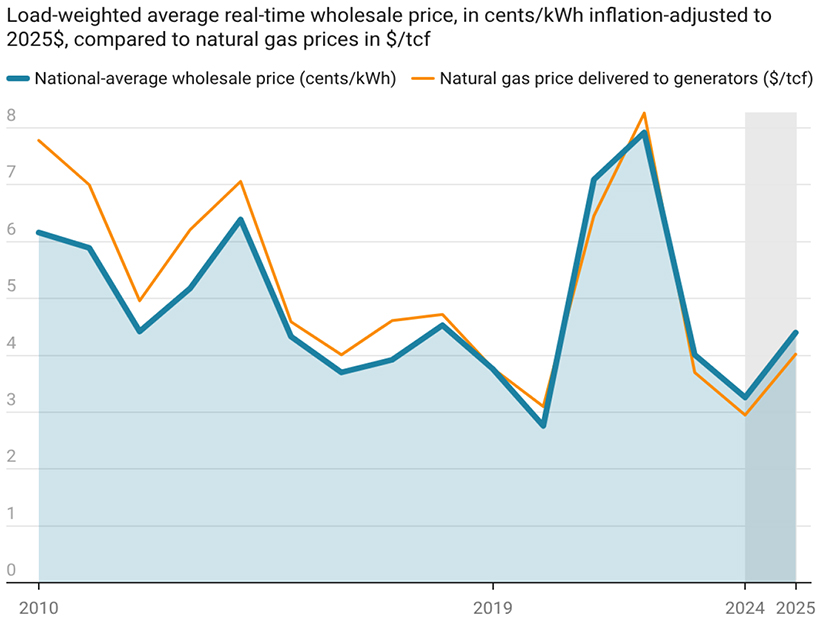

Electricity prices rose, on average, about 3% in 2025 from a year earlier, which is a departure from 2019 to 2024.

“It’s only one year, but it does give you the sense that we could be observing the beginning of this inflection point where rates go from declining at a modest rate in inflation-adjusted terms to increasing in inflation-adjusted terms,” Hledik said.

Data centers often are blamed by the public as a primary culprit for rising prices. So far, new supply in PJM, for example, hasn’t kept up with the demand driven by data centers. That has led to higher capacity prices, which in turn contribute to higher retail prices.

“That’s not the only driver of rate changes in PJM states,” Hledik said. “And then, you know, PJM is not the only market in the United States. There’s a lot happening that looks different than that in other parts of the country.”

Natural gas prices increased between 2024 and 2025, and that was a significant driver of higher electricity prices.

“Load growth can be a contributor. We saw that in PJM, but if natural gas prices swing upward during that period, those are going to drive an increase in electricity prices as well, and that was observed pretty broadly, given the country’s dependence on natural gas as a fuel source for generation,” Hledik said.

The LBNL study did not look into secondary effects of data centers like whether their demand has influenced the cost of components. Wood Mackenzie released a report April 1 finding the cost of gas turbines was expected to hit $600/kW by the end of 2027 — a 195% increase from 2019 — due to higher demand, “especially” from data centers.

The reasons for rising equipment costs in recent years are broader than just data centers, Hledik said.

“The cost of equipment on the distribution system has increased significantly over the last six years, and data centers are not typically distribution-connected loads. They’re plugging directly into the transmission system,” Hledik said. “The reason we’ve seen equipment costs increasing at the distribution level is because of post-pandemic supply chain constraints that still haven’t been resolved.”

State policies play a role, Hledik said. They are one of the top three or four drivers for power prices, with renewable portfolio standards that require utilities to buy generation at above-market rates as one example, he said.

“In a market like Texas that has great access to wind and solar generation, you don’t see rates going up because the market has concluded that those are economically competitive resource types,” Hledik said. “Where we’ve seen there potentially being some upward pressure is if you have a state that has clean energy goals and is asking their utility to go out and buy stuff out of market that is more expensive than they would procure otherwise.”

The policy calculation there is that climate change will lead to costs through extreme weather, wildfires and other issues. So, some states have opted to address that by investing in renewables now, he added.

Situations beyond the control of state policymakers have a big influence on prices, such as the availability of cheap power or the kind of geography on which utilities need to build the grid.

“If it’s a utility that has physical topography that is easier to build power lines across, than one that is harder to develop, that can drive up costs as well,” Hledik said. “If you’re in the West and dealing with drought conditions that can increase the risk of wildfires, and then you’re recovering the cost of wildfire risk mitigation through your retail electricity rates — that can drive up costs.”

Another issue with retail power prices is how they are spread around to different customer classes. Residential customers pay higher rates at a national average in 2025 of 17.3 cents/kWh in 2025, which compares to 13.4 cents/kWh for commercial customers and 8.6 cents/kWh for industrial customers, the paper said.

Residential prices from 2019 to 2025 rose 33%, while commercial and industrial customers saw increases of 26% and 27%, respectively. However, between 2024 and 2025, residential customers saw prices rise 5%, compared to 5.2% for commercial customers and 6% for industrial customers, the paper said.

“Residential customers are located all the way at the end of the distribution system, whereas larger industrial customers or data centers might not be using the distribution system at all,” Hledik said. “They might be plugging directly into the transmission system. And, so, when rates are being set for each of these customer classes, they’re being set roughly based on the costs that each of those classes are contributing to the overall cost.”

That leads to some of the disparity, but policy and politics can get involved as larger customers can intervene in legislative or regulatory proceedings to get lower rates for themselves, he added.

The data center industry, utilities, regulators and politicians all talk about ensuring the new class of hyperscale customers pay for the costs of serving their new load. But given the realities of the retail setting, getting that 100% perfect will not be possible, Hledik said.

“If we conclude that ultimately the best we can do from an accounting standpoint is ensure that about 90% of the costs that are being introduced by very large customers are being recovered from those customers, you might also see accompanying policies,” he added.

Regulators could make up the difference by having data centers pay into funds to offset costs for low-income consumers, or low-income weatherization programs. Low-income customers have a higher energy burden than others.

“If you look back over the last couple of decades, on average, the cost of electricity as a percent of total household expenditures has actually decreased,” Hledik said. “But if you look specifically at certain vulnerable customer segments, like lower-income customers, their energy affordability challenges have actually increased over the last five to six years.”