Some Americans still think of “energy prices” as a single rising tide. When oil prices top $100/barrel, it feels like everything else follows: heating, groceries and electricity.

For Boomers who filled their cars’ voluminous tank during the 1970s energy crisis, that intuition is grounded in experience: They lived through a time when oil shocks rippled across the entire energy system, driving inflation and straining household budgets.

Today, for Americans in the Lower 48, correlation is not causation. Yes, electricity prices are painfully high. No, they’re not related to oil prices, at least for customers of the RTOs.

Oil prices can surge, and most of the U.S. power system barely notices. Yet that doesn’t mean oil no longer matters. It means the places where it still does — from Hawaii and Alaska to island grids around the world — tell us something important about how electricity prices work and why so many Americans still feel like they’re losing control of their energy bills.

The Persistence of the ‘Energy Bucket’

For many households, energy is experienced as a single category.

Consumers are feeling squeezed by rising costs: April 10 inflation data showed a threefold spike in prices driven by oil. Although U.S. retail electricity prices largely are unrelated to the oil price, they have been rising faster than inflation in recent years and are expected to continue increasing. Just two months ago, I wrote about the political risk inherent in households’ rising electric bills.

Gasoline prices are posted on street corners and updated daily. Electricity and gas bills arrive monthly. Heating oil tanks are filled periodically. And since the U.S. and Israel attacked Iran at the end of February, there’s been increased upward pressure. When all rise — even for different reasons — the result is a powerful perception: Energy is getting more expensive, everywhere, all at once.

Fortunately for the industry, many consumers have mentally decoupled oil prices in the news from their electricity bill. Unfortunately, they largely blame utility profits, infrastructure upgrades and, in third place, data centers’ impact on demand, according to a recent Consumer Reports survey.

How the U.S. Grid Broke its Link to Oil

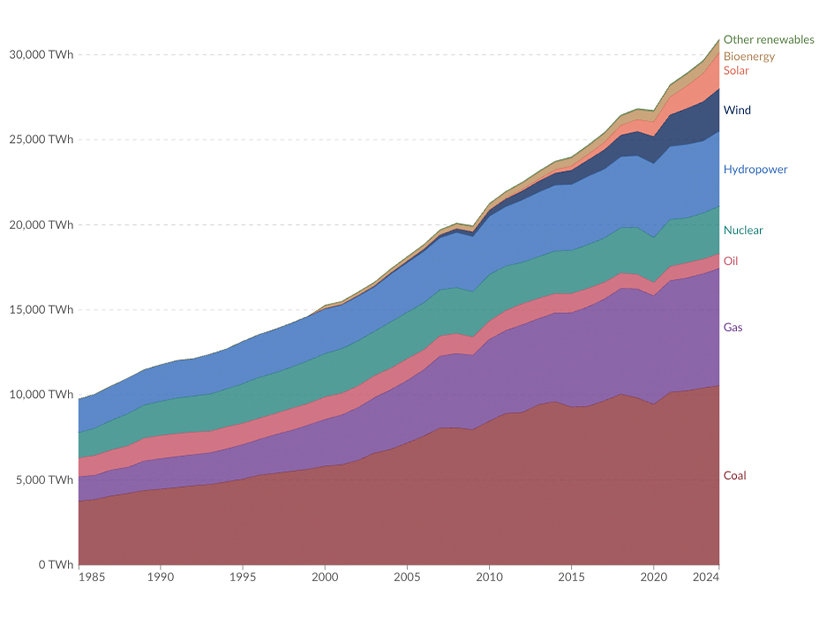

Oil played a meaningful role in U.S. electricity generation 50 years ago. Between 1963 and 1973, oil’s share of electricity generation almost tripled, rising from 5.73% to 17.09%. More importantly, it played a central role in the broader energy economy. When oil prices moved, everything else tended to move with them.

That is no longer the case. The 1973/74 energy crisis was a wakeup call, and though oil use touched a little higher in 1977, the hunt was on for alternatives. By 1984, it was back below 1963 levels and has since sunk to a negligible amount: less than 1.0% since 2011.

The generation mix has been fundamentally reshaped since the mid-1970s, and more than once. After the energy crisis, nuclear and coal output rose. Nuclear — slow and expensive to build and facing community acceptance headwinds following the 1979 Three Mile Island accident — stalled at about 20% of electricity generation. Coal kept climbing, with half of all electricity produced by coal-burning plants in 2005.

Then the shale revolution challenged coal’s dominance, and coal’s use declined sharply as natural gas surged. The rise of renewables reshaped the market again in the past decade or so, with wind, solar and hydro now supplying more than 20% of U.S. electricity.

What Actually Drives Electricity Prices Now

If oil no longer drives electricity prices, what does?

Today, more than 40% of U.S. electricity comes from gas, which frequently sets the marginal price in wholesale markets. Renewables continue to grow if you look at trends longer than a political administration, adding capacity but not displacing gas as the price-setting resource in most regions — though a sunny day in California or a windy night in Texas can push the wholesale price of electricity negative.

But retail electricity prices are shaped by far more than fuel. It’s no longer what we burn (or capture, when it comes to renewables) but what we build — and rebuild after disasters — that drives the retail cost of delivered electricity. In 2023, the U.S. Energy Information Administration said transmission accounted for 12% and distribution accounted for 26% of the cost of retail electricity.

This shift helps explain a paradox that frustrates consumers: Electricity prices can rise steadily even when fuel prices are stable or falling.

Oil Still Matters, Just Not Everywhere

In some parts of the world, oil still plays a significant role in electricity generation — particularly in island grids, remote systems and regions with limited access to natural gas infrastructure. Diesel and fuel oil remain common fuels for power generation in parts of the Caribbean, Africa and South Asia.

Even where oil is not the primary fuel, it often plays a critical backup role. In systems with unreliable grids or constrained infrastructure, diesel generators provide essential capacity, tying electricity costs more directly to oil prices.

And oil still matters indirectly everywhere. As the Brookings Institution has noted, oil shocks continue to ripple through the global economy, affecting inflation, supply chains and household budgets.

The key distinction is not between oil and non-oil systems, it is between grids that are structurally insulated from fuel volatility, and those that are not.

No Person is an Island … but Some U.S. Grids are

That distinction exists within the United States as well. Not all U.S. grids look like PJM or ERCOT. Some look a lot more like the Caribbean.

Oil makes up a significant part of the electricity generation mix in two states — Hawaii (65%) and Alaska (15%) — and most territories, such as American Samoa (97%) and Puerto Rico (62%).

Hawaii has consistently had some of the highest retail electricity prices among the 50 states, and its utilities know their customers will feel the pain of rising oil prices. Hawaiian Electric has warned customers that higher bills are on their way, forecasting residential bills may rise 20% to 30% over the next several months.

The sensitivity to global oil prices is just one more reason for the islands to continue their push for resilience by expanding the use of renewables. “Hawaiian Electric has reduced its use of oil by 55 million gallons annually since 2008 and is bringing more than a dozen fixed-price renewable energy projects online in the coming years,” the recent announcement said.

Alaska presents a different version of the same challenge. Many remote communities rely on diesel-powered microgrids, where fuel costs are a primary driver of electricity prices. These systems behave less like the interconnected grids of the Lower 48 and more like the island and remote systems found elsewhere in the world.

New Headlines, Same Conclusion

Oil no longer sets the price of electricity in most of the United States, but oil shocks shape how much end users think about the cost of all their energy. Because of that, it’s critical that policymakers keep electricity prices and the perceived value of the services customers receive top of mind.

While those inside the industry recognize electricity prices are the outcome of infrastructure, investment and system design as much as fuel costs, customers care less about the why and more about the how much. And just because the price of oil isn’t driving most customers’ bills higher, it is making them increasingly price sensitive.

It’s self-referential to quote my conclusion from a couple of months ago, but the conclusion of this column is the same as the last one on prices, only now bolded and underlined thanks to oil prices: Utilities, grid operators and regulators have to focus on affordability. This means balancing necessary long-term capital investments with measures that keep electricity costs manageable.

Oil price shocks may settle soon or may continue if global oil supply can’t reach markets, but there’s no sign that customer concerns about the price of energy will settle any time soon.