The Trump administration is moving to close the door on U.S. offshore wind development by remanding approvals for all projects not already under construction.

Federal attorneys filed a motion in the U.S. District Court for D.C. on Sept. 3 saying the U.S. Bureau of Ocean Energy Management plans to vacate the permit it issued to New England Wind during the Biden administration.

In late August, federal attorneys made similar comments about the SouthCoast Wind project off the New England coast, as well as about US Wind’s plans off the Maryland coast. And in March, EPA put a hold on an air permit for Atlantic Shores, at least temporarily blocking the New Jersey project from any start of construction.

Those four projects were the late movers among the 11 approved during the Biden administration. One of the 11 is completed; one was canceled by the developer; and five are in some stage of construction.

Numerous plans at earlier stages of development are on indefinite hold amid the clampdown President Donald Trump has ordered on the offshore wind sector, because of the restrictions themselves or from investors being driven away by the heightened risk and uncertainty that has resulted.

The recent motions were filed in three cases where wind power opponents had sued various federal agencies challenging regulatory approvals that allowed the three projects to move forward. In separate motions, Department of Justice attorneys asked the courts to delay the cases because the federal government is going to do essentially what the plaintiffs were seeking.

Federal attorneys said the government is planning to remand and vacate BOEM’s approval of the construction and operations plan for the Maryland offshore wind projects no later than Sept. 12 (24-cv-03111); move for voluntary remand of the SouthCoast approval by Sept. 18 (1:25-cv-00906); and remand and vacate New England Wind’s approval (1:25-cv-01678) no later than Oct. 10. The EPA action against Atlantic Shores on March 14 was a voluntary remand. (See EPA Puts Hold on Atlantic Shores OSW Permit.)

With Trump’s flat rejection of wind power, it is questionable when or if the approvals would be reinstated once remanded.

In the most recent New England offshore wind solicitation, SouthCoast and New England Wind were selected to feed 1,868 MW to Massachusetts and 200 MW to Rhode Island. (See New England OSW Contracts Delayed Again.)

Coupled with the BOEM’s stop-work order on Revolution Wind — an 80% complete project that would send 704 MW to Connecticut and Rhode Island — the pending actions represent a clear threat to New England’s clean energy ambitions.

“New England needs this energy,” Gov. Maura Healey (D) said Sept. 3. “Having already undergone years of expert review, these projects are primed to lower costs and improve reliability. There is absolutely no need for the Trump administration to reopen permitting processes and deny jobs, investment and energy to the states.”

ISO-NE had warned Aug. 25 that delaying Revolution Wind would increase reliability risks for the New England grid. (See ISO-NE Warns Halting Revolution Wind Boosts Reliability Risk.) On Sept. 3, it pointed to remarks by CEO Gordon van Welie about the importance the offshore wind sector holds for the region.

“The region is counting on the entry of resources in the form of large quantities of offshore wind to maintain resource adequacy,” van Welie commented to FERC in May (AD25-7). Solar panels and short-duration battery storage, he added, would not be an adequate replacement for the giant marine turbines.

Nick Krakoff, a senior attorney with the Conservation Law Foundation, told NetZero Insider that remanding and vacating the construction and operations plans for SouthCoast and New England Wind is a move that can be challenged in court by the developers and or the states involved, but the concept of victory is not clear-cut.

“There’s certainly legal avenues,” he said. “I think the bigger question is, what happens to industry? The Trump administration is just actually sabotaging an entire industry.”

Trump’s strategy has proved quite viable so far: Multiple offshore wind development efforts have been placed on hold since his election, Atlantic Shores among them. (See Developer Shelves Atlantic Shores, Seeks to Cancel ORECs.)

Those that remain face a regulatory limbo as the administration floods the zone with new hurdles and limitations. Projects that are under active construction can incur huge cost overruns because of delays.

All of this creates an untenable business environment.

“The longer this drags out, the more difficult it becomes for the developers financially,” Krakoff said. “I think it’s just another example of this administration’s disdain for the rule of law.”

The systematic attempt to kill an entire industry is unprecedented, he added. “You kind of expect this in other countries, but not this country.”

Trade group Oceantic Network criticized the administration’s stated intention to remand and vacate permits that were issued after years of review. “The unlawful and escalating actions by the Trump administration against fully permitted offshore wind projects up and down the East Coast represent one of the largest, economically devastating assaults on U.S. workers, businesses and energy in generations,” it said.

“Halting construction and revoking permits on approved projects after years of thorough agency review will raise electricity prices for millions across the country, jeopardize billions of dollars in private investment, threaten our national shipbuilding, steel and manufacturing supply chains, and undermine our nation’s energy security.”

Developers installed more than 11 GW of new utility scale solar, storage and wind worth $15.2 billion in the second quarter, but signs point to abrupt decline in renewable development, the American Clean Power Association said Sept. 3.

While those overall numbers were in line with last year, the clean power pipeline showed virtually no growth (adding less than 100 MW to an existing pipeline of 184.5 GW), solar installations declined 23% during the first half of 2025 and power purchase agreements plummeted, which are early indicators of federal policy attacks and fluctuating trade policies, according to ACP’s Clean Power Quarterly Market Report.

“America’s clean energy industry continues to add much needed power to the grid. Unfortunately, federal policy obstacles and restrictive mandates are threatening hundreds of billions in planned energy investment,” ACP CEO Jason Grumet said in a statement.

“The uncertainty created by new bureaucratic delays and unclear demands is having a chilling effect on the pipeline for future energy projects, stalling growth precisely when our nation needs more energy to power a growing economy,” he said.

Policy actions from nearly every federal department and an unstable regime of tariffs have led to a drop in clean power purchasing, despite skyrocketing demand across the country. PPA contracting fell 32% in the first half of 2025 compared to 2024, battery storage PPA announcements fell 88% from the first quarter to the second, and wind announcements were down 93% on the quarter.

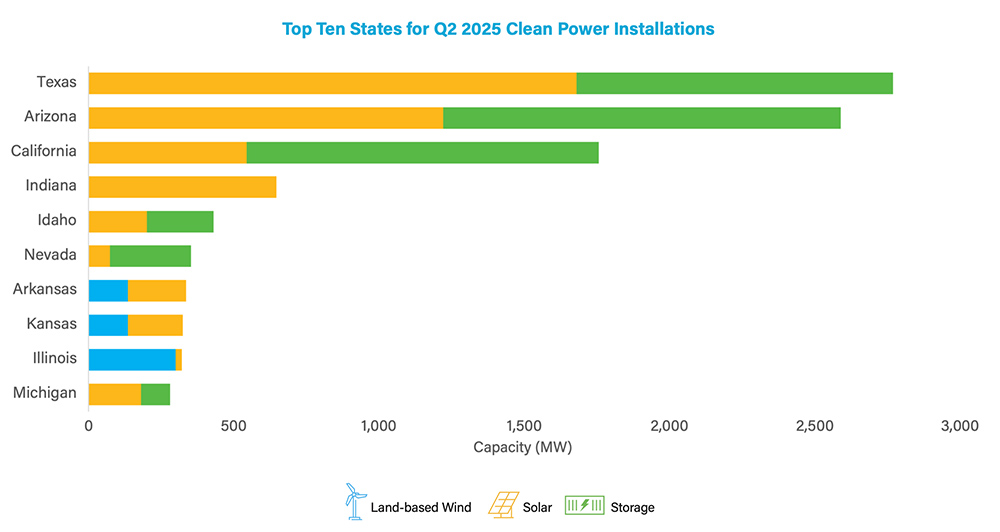

A graph from the report showing the leading states by clean energy capacity additions for the second quarter of 2025. | ACP

Corporate wind and solar PPA prices were up 6% quarter-over-quarter, and 8% on the year, which reflects instability in the purchasing environment. The pace of procurements slowed in the second quarter as developers and buyers waited for clarity on tax credits and attempted to budget with shifting trade agreements.

While solar installations were down 23%, overall numbers of deployed projects were fairly level with 2024 installations, as storage deployments were up 63% to 6,510 MW and wind deployments were up slightly by 12%.

Arizona became the third state to reach 10 GW of nameplate clean energy, as it added 1,220 MW of new solar and 1,369 MW of new storage.

Texas has the most installed capacity and largest pipeline, and it edged out Arizona for additions in the quarter, while California took third place for quarterly additions. Eight of the top 10 states for deployments in the second quarter voted for President Donald Trump in last year’s election.

Overall, the country has installed more than 330 GW of clean power as of June 30, 2025, which is enough to power more than 81 million homes.

Developers reported that 83,403 MW of renewable capacity was under construction as of midyear, which includes 580 projects. Construction activity was highest in Texas at 21 GW, followed by Arizona at 7.8 GW, California at 7.2 GW, New Mexico at 4.8 GW and Wyoming at 4.1 GW.

Solar makes up just over half the national project pipeline, with 96 GW under construction or in advanced development. Storage took second place from land-based wind during the first quarter of 2023 and, along with solar, it has driven the growing pipeline of projects, with the backlogs growing by 32 GW and 22 GW, respectively, since the second quarter of 2022.

“Clean energy is the fastest-to-deploy energy resource. With demand for electricity at historic highs, Americans cannot afford policies that limit power production and raise household electricity bills,” Grumet said. “The U.S. must support all forms of energy.”

Washington’s Ecology Department has clarified that state cap-and-invest rules that apply to CAISO’s Western Energy Imbalance Market also will cover the ISO’s Extended Day-Ahead Market (EDAM) when it begins operations in 2026.

An agency guidance document released Sept. 3 explains how the cap-and-invest program attributes an appropriate volume of greenhouse gas emissions to energy imported into Washington via a centralized electricity market (CEM). The WEIM is the only centralized market operating in the West, with SPP’s Markets+ expected to go live in 2027.

The GHG attribution process is complicated by the difficulty of pinpointing exactly what resource in a centralized market produced the energy imported into the state to meet a market participant’s demand.

Under existing rules, energy transferred into Washington via the WEIM is classified as an “unspecified import” and assigned a default emissions factor of 0.428 MT CO2e/MWh. The rules require that the Washington-based load-serving entity or market participant receiving the import be responsible for reporting the emissions to the Ecology Department.

But a 2024 law (SB 6058) prompted Ecology last December to adopt a new framework that will allow the agency to trace the origin and emissions factor of CEM energy transfers into Washington — transfers that will be categorized as “specified imports” with specific associated emissions rates.

To do that, the new framework calls for centralized market operators such as CAISO and SPP to establish a system for identifying a “deemed market importer” for transfers into Washington, defined as “the market participant that successfully offers electricity from a resource or system into a CEM, which then is “attributed to Washington by the methods put in place by the market operator of that CEM.” The deemed market importer also will be the entity responsible for reporting emissions to the agency.

The Sept. 3 guidance notes that existing reporting rules will remain in place through 2026, but it advises market operators to put a “specified imports” system in place by Jan. 1, 2027.

It also clarifies that although the rules were written with the real-time WEIM in mind, they also apply to EDAM.

“Ecology notes that all optimization of electricity supply from market resources and attribution of imported electricity to Washington through the day-ahead market, EDAM, ultimately occurs in real-time, within the WEIM,” the agency wrote. “For this reason, Ecology clarifies that provisions applicable to the ‘energy imbalance market’ within WAC 173-441-124(3)(v), apply equally to entities participating in WEIM and EDAM.”

A new analysis of the One Big Beautiful Bill Act from Aurora Energy Research found that the bill likelywill increase wholesale power prices in NYISO and PJM by up to $8/MWh, driven by reductions in renewable energy development and increases in fossil fuel plant operation.

“When you cut off some of the capacity that was going to come through as a result of faster buildout of things like offshore wind, you get a lot of baseload gas moving in to fill in the gap, and that has a significant longer-term impact on prices,” said John Kidenda, a researcher for Aurora.

Kidenda estimates PJM will experience a $6 to $8/MWh price increase by 2035. NYISO is estimated to increase by $5 to $7/MWh in the same time frame.

The end of tax credits coupled with deployment hurdles and tariffs likely will cause PJM and NYISO to have 10% fewer renewable resources by 2040 compared to Aurora’s base case. Roughly 10 to 15 GW of renewables are at risk of missing the new in-service deadline for tax credits across both grid operators. This will force them to rely on thermal plants more often, resulting in 5 to 7% more runtime.

A separate analysis of the clean energy and transportation sectors under the OBBBA by Rhodium Group and MIT illustrated the challenges that renewable energy development faces nationwide. New utility-scale clean energy projects declined 51% between the first and second quarters of this year. New industrial decarbonization developments declined 17% in the same period and 38% year-to-year.

The Rhodium/MIT group also examined the outstanding projects receiving Inflation Reduction Act credits. Roughly $517 billion of outstanding investment remains to be spent on construction and installation; $406 billion of that is tied to electricity and industrial investment, and 42% is tied to wind and solar generation projects.

The findings of both reports point to large nationwide pressures on renewables to get to market and qualify for tax credits, a far cry from Aurora’s stance late in 2024, when it said the projected impact of a second Donald Trump presidency on New York’s grid were “minimal.” The assumption was that, despite Trump’s promise of ending the IRA’s tax credits, congressional Republicans would be unwilling to pass legislation repealing them because they benefited their districts. (See NY Well Positioned to Push Forward on Climate Goals Under Trump.)

That assumption — like that of President Joe Biden and congressional Democrats when the IRA was enacted in 2022 — turned out to be very wrong.

Kidenda said that despite Trump’s desire to keep natural gas prices down and increase gas generation, the long waits for new turbines coupled with increased demand mean there is significant upward pressure on gas prices.

“As that tightness comes through and you get demand from heating, then you get price increases,” Kidenda said. “Not because baseline gas prices are increasing but because people are bidding up the right to access the pipeline.”

Kidenda said it was critical for New York to ensure that renewable projects like Sunrise Wind are finished. The state runs the risk of blackouts and loss of load without added capacity, particularly in New York City and Long Island, he said.

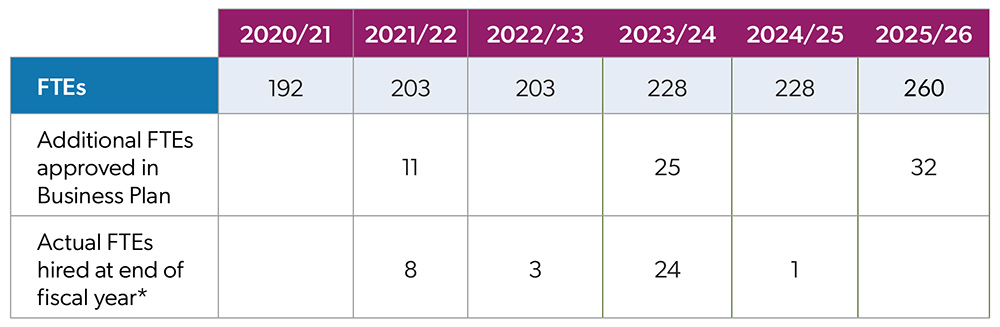

The Ontario Energy Board (OEB) plans a 22% increase in its 2025/26 budget with the addition of 32 employees, its biggest hiring surge in at least five years.

The board cited “the increased volume and complexity” of its job in announcing the hirings, which would increase OEB’s staff by 14% to 260 full-time equivalents.

“We are building an organization that can enable government policy and be the regulator Ontario needs during the energy transition,” OEB said in its Business Plan for 2025/26 through 2027/28, which outlines $70.3 million in spending for the current fiscal year (beginning April 1) and preliminary budgets for the following two years.

The board said the $12.5 million budget increase was needed to respond to the Ministry of Energy and Mines’ 2024 vision statement and the ministry’s Dec. 19, 2024, Letter of Direction, which outlined the province’s strategy for responding to an expected 75% increase in electric demand by 2050.

“These additional resources will enable the OEB to deliver on its mandate, which, when coupled with the minister’s letter, requires taking on additional deliverables at a time when the organization is at full capacity with existing commitments and adjudicative work,” the board said.

“Resources will be applied across the organization to meet the highest-priority needs at any point in time, balancing adjudicative support and policy development, and matrixing resources depending on expertise, topic and timeline,” it added.

Three initiatives each will receive six new FTEs:

Advancing the Energy Transition: ensuring regulated entities plan across fuel types; considering how to apply the “beneficiary pays” principle; and streamlining approvals for electric connections and “priority” pipeline projects.

Driving System Modernization: developing local market opportunities for distributed energy resources, such as distribution system operators; implementing performance-based rate regulation for electric distribution companies; supporting Indigenous participation; and ensuring cost-effective integration of innovative business models.

Sustaining Resources: adding legal, public affairs, finance and human resources staff to support OEB’s expanded operational requirements and strategic priorities. OEB said those functions “have not kept pace with recent growth across the organization.”

The board plans five new staffers to boost DERs, including providing incentives for implementing non-wires solutions, publishing capacity maps for distribution and transmission systems, and reducing barriers for new energy efficiency programs.

The Ontario Energy Board plans to hire 32 new employees in 2025/26, the biggest contributor to a 22% budget increase for the year. | Ontario Energy Board

In total, the salaries and benefits budget is increasing by 19% to $50.4 million.

Because they will have staggered start dates, the 32 new hires will cost $4.15 million in 2025/26 and $6.2 million annually thereafter.

The budget also includes $1.8 million for salary increases for existing staff and $1.2 million for short-term contract staff needed to “backfill” for subject-matter experts shifted under the Business Operations Optimization and Systems Transformation (BOOST), a new platform for data and workflow management across OEB processes.

The plan pointedly reiterates the board’s belief that “diversity, equity and inclusion (DEI) is not just an ideal but also our competitive business advantage, a defining characteristic of our culture and an essential organizational strategy.”

The new hires will allow OEB to “provide strategic and prudent oversight of Ontario’s energy sector through initiatives that support broader government priorities such as planning for growth, keeping costs down, enabling energy system modernization and streamlining solutions that will make Ontario an energy superpower,” the board said.

“How the OEB’s planned key projects presented in the plan have changed and will be prioritized post-IEP (and directive) remain to be seen,” he added.

The big spending increase caught the attention of Martin Benum, former director of regulatory affairs for London Hydro.

“The OEB is supposed to regulate industry costs, not grow into another bloated cost-recovery machine itself,” Benum said in response to Hrab’s posting. “Is the OEB still focused on consumer protection and efficiency, or are we watching another cost monster take shape here in Ontario?”

Capital Spending Trending Down

While the board is increasing spending on personnel, it expects capital spending (business systems, infrastructure and end-user computing) to drop slightly, from $474,000 in 2025/26 to $451,000 in 2027/28.

“With more resources available as services, the OEB’s IT capital budget is expected to be stable in the coming period with some spending moving to the IT operating budget,” it explained.

Priorities

The board’s priorities for the coming year include simplifying the connection processes for DERs, incentivizing electric distribution companies to use third-party DERs as non-wires alternatives and a benefit-cost analysis framework for addressing system needs.

OEB also is considering changes to its rate design to accommodate electric vehicles and battery storage, following up on its analysis of the impact of delivery costs on EV charging facilities. “The OEB is also planning to consider reforms to rate design for resources providing grid services and other emerging technologies,” it added.

Also on the schedule for the board is a ruling on Enbridge’s 2026-2030 electric demand-side management application, which includes a residential program that would be delivered through a “one-window” approach in conjunction with IESO. OEB said it expects to rule on the case this fall.

ERCOT’s board selection committee has chosen two new independent directors, restoring the Board of Directors’ full complement of seats after several departures earlier in 2025.

The grid operator said Houston’s Christopher Krummel and Austin’s Kathleen McAllister will fill the remaining vacancies on the 12-person board. The selections were announced and became effective Sept. 3.

Christopher Krummel | Centuri Holdings

Krummel has more than 30 years of financial executive experience in the energy and construction industries. He is a founding partner of Krummel, Ellis & Weekley Advisory, which provides sell-side transaction advisory services to energy focused clients, and previously served as McDermott International’s CFO.

He has a bachelor’s degree in business administration from Creighton University and a master’s in business administration from The Wharton School of the University of Pennsylvania.

McAllister has more than 15 years of experience in corporate governance as a CEO, CFO and board director. She currently serves on the boards for Black Hills Corp. and Höegh LNG Partners after spending years in executive roles with offshore driller contractor Transocean Partners.

Kathleen McAllister | NACD

McAllister holds a bachelor’s degree in accounting from the University of Houston and is a certified public accountant.

Board Chair Bill Flores welcomed the newest members to the board, saying in a press release, “Their background, knowledge and expertise will continue to support ERCOT’s strategic objectives of maintaining a dynamic, reliable and resilient electric grid.”

Two independent directors resigned from the board earlier in 2025 to pursue “new opportunities” in the ERCOT market. That left the 12-person board three short of full membership. Industry insider Bill Mohl was selected in July to fill one of the vacancies. (See ERCOT Adds Industry Vet to Board of Directors.)

The ERCOT board is subject to oversight by the Public Utility Commission and the Texas Legislature. By law, all board members must be Texas residents.

The board’s selection committee was created by state law in 2021. It is composed of three appointed members, with the governor, lieutenant governor and the speaker of the Texas House of Representatives each selecting a representative.

The California Public Utilities Commission (CPUC) has approved guidelines for utilities to use to design dynamic electricity rates, with one commissioner asking for more research on whether implementing such rates will leave some customers further behind financially.

The decision applies to Pacific Gas and Electric, Southern California Edison and San Diego Gas & Electric, which must propose dynamic rates in their general rate cases for approval by the CPUC.

And it comes just weeks after publicly owned utilities Sacramento Municipal Utility District and the Los Angeles Department of Water and Power outlined their challenges with implementing the practice in reports submitted with the California Energy Commission. (See Calif. Utilities Move Cautiously on Dynamic Pricing.) The dynamic rate design idea comes from the CEC’s load-management standards.

“This is an exciting proposed decision and it really marks another step … to support California’s long-term goals: grid reliability, electrification and affordability,” CPUC President Alice Reynolds said at the commission’s Aug. 28 voting meeting, during which the decision was approved.

Reynolds said the decision addresses key demand flexibility — or dynamic rate — design elements: marginal energy costs based on CAISO’s hourly load; day-ahead prices at default load aggregation points; marginal generation capacity costs; marginal distribution capacity costs; marginal transmission costs; non-marginal costs; and line-loss factors.

“Demand flexibility is one of the most important things we are doing as a state and will help provide additional resources that we can use,” Commissioner Darcie Houck said at the meeting. “I know a lot of time, effort and thought has gone into this decision.”

The goal of dynamic rates is to “motivate customers to shift electricity consumption away from high-demand periods, when polluting, peaking plants run and electricity is most expensive,” Commissioner John Reynolds added at the meeting. “Dynamic rates promise to achieve this by providing accurate price signals that reflect actual grid consumptions.”

However, as California moves from the approved guidelines to implementing these new rates, it is important to evaluate their effect on different types of customers, he said.

It may prove true that factors like income, whether a customer owns their home, or a customer’s climate zone could “substantially impact their ability to shift energy usage to lower-cost hours,” he said.

“We should evaluate these rate design changes to understand these consequences,” he said. “This is an equity concern that I think we need to attend to.”

In the decision, the commission said community choice aggregators (CCAs) should be able to either design their own dynamic rate or use their associated IOU’s dynamic rate. IOUs should describe how they will collaborate with CCAs on dynamic rates and programs, the commission said.

Marginal vs. Fixed Costs

In the decision, the commission said IOUs’ dynamic rates must include a marginal generation capacity cost (MGCC), which is the cost to procure and maintain sufficient generation capacity to reliably serve an incremental unit of electric demand at all times, including during peak demand and ramping periods.

The MGCC price “must account for costs associated with both peak and flexible capacity needs during periods of grid stress,” the commission wrote. An IOU’s proposal must include a price component that recovers an IOU’s MGCC revenues “to ensure that generation capacity costs are appropriately reflected in DF rates.”

“I expect the marginal costs on our grid to be much lower than our current electric retail rates,” John Reynolds said at the meeting.

The reason for that is that California’s electric system has many fixed costs, he said.

“For example, using more electricity does not really change the amount of money needed to trim vegetation to reduce wildfire risk,” he said.

Historically, the state recovers these fixed costs in the electricity rate, making that rate higher than the marginal costs of energy.

However, the modest fixed charge that the state already adopted still “does not fully cover our fixed costs of the system,” John Reynolds said.

“There will be debate about which costs are actually marginal and which are fixed, and that’s healthy, and we will need policy decisions resolving that debate,” he said.

“As we make policy decisions evaluating the nature of marginal costs, I expect that truly reflecting marginal costs in hourly prices will be lower rates and higher fixed charges,” he added. “These will be revenue neutral … and should actually lead to a lower overall cost grid.”

But fully moving to hourly marginal pricing will mean customers who can shift their usage will “have greater opportunities for bill savings than customers with inefficient appliances and leaking homes that don’t stay cool on hot days,” he said.

The large IOUs should use CAISO’s locational marginal prices at default load aggregation points in CAISO’s day-ahead market, CPUC staff said in the decision. This approach provides customers with a degree of rate certainty because electricity prices in the day-ahead market at default load aggregation point prices represent a majority of load-serving entities’ actual energy purchase costs, staff said.

Another offshore wind project is facing a potentially crippling threat from the Trump administration.

In an Aug. 29 filing in federal court in Washington, D.C., the Department of the Interior said it intends to reconsider its approval of the construction and operations plan for SouthCoast Wind off the New England coast (1:25-cv-00906).

Interior said the same thing in an Aug. 22 filing in federal court in Delaware about the US Wind projects off the Maryland coast (1:25-cv-00152).

Both cases involve attempts by wind power opponents to overturn Interior’s approval of the projects. Interior argued in its motions that since it plans to reconsider its approval, the cases should be paused, as they might soon become moot.

On Sept. 1, SouthCoast replied with a motion opposing Interior’s request:

“Federal defendants’ failure to show good cause is further exemplified by their lack of diligence in moving this litigation forward, which is indicative of a pattern of unreasonable delays designed to further the political agenda of the current administration,” SouthCoast’s attorneys wrote.

“This delay and the forthcoming request for remand are simply pretext for the unabashed desire of the president to eliminate all offshore wind projects from existence regardless of their impacts.”

Eleven offshore wind projects have been approved in U.S. waters:

South Fork Wind (completed);

Ocean Wind (canceled by developer);

Coastal Virginia, Empire, Revolution, Sunrise and Vineyard 1 (under construction); and

Atlantic Shores, New England Wind, South Coast and US Wind (advanced development.)

While many projects date back to the first Trump administration, all the records of decision came during the Biden administration. There were no rejections.

Interior’s Bureau of Ocean Energy Management announced SouthCoast’s record of decision Dec. 20 and approved its construction and approval plan Jan. 17 — the last business day before President Donald Trump returned to office.

On the campaign trail, Trump had vowed to halt construction of offshore wind generation, and he and his administration have taken extensive steps to accomplish that since he returned to office Jan. 20.

Along with many actions to block future development, a few moves have targeted existing projects:

EPA revoked an air permit for Atlantic Shores, blocking whatever chance it had of starting construction.

Revolution, which is 80% complete, is sidelined by a recent stop-work order.

Empire was the target of a stop-work order that lasted several weeks this spring.

And now SouthCoast and US Wind’s MarWin and Momentum are facing potential reversals of their construction and operations permits.

Numerous other projects at earlier stages of development are on indefinite pause, due either to hostile federal policies or spooked investors.

AUSTIN, Texas — The dust has settled in Texas after another biennial legislative session that installed guardrails for data centers and other large loads and avoided stiff penalties on the clean energy sector. At the same time, ERCOT stakeholders still are digesting the massive federal budget reconciliation bill signed into law in July.

Both pieces of legislation weighed heavily on the minds of panelists during Infocast’s annual Texas Clean Energy Summit Aug. 26-28.

The summit’s opening panel took on Texas’ Senate Bill 6, which governs the planning, interconnection and operation of large loads and generation resources in ERCOT. The bill directs the state’s Public Utility Commission to set rules that address cost-sharing and interconnection standards for new large load customers (defined as any load 75 MW or greater). These loads will be required to contribute to utilities’ costs to connect them to the grid.

The legislation also requires electric cooperatives and municipally owned utilities that have not adopted retail choice to pass through reasonable interconnection costs for large loads.

Ned Bonskowski, vice president of Texas regulatory affairs for Vistra, pointed out that SB 6 didn’t occur in a vacuum.

“It wasn’t like on the first day, the Legislature said, ‘Let there be Senate Bill 6,’ and then that was the first energy policy that we had in the state,” he said. “There’s a long continuum of statutory and regulatory policies that it has to fit in, and that goes way back beyond Senate Bill 6. I honestly think that about 75 to 85% of what you see in Senate Bill 6 was already happening or was going to happen anyway, so it’s really codifying in statute, putting some guardrails that the Legislature said they learned how they wanted to be implemented.”

“Load growth, triggered largely by data centers, is creating a lot of anxiety in different markets and we’re seeing different approaches to how to manage that pending issue,” Samantha Robertson, director of global strategy at cryptocurrency miner Bitdeer, said. “In Texas, it’s codified in statute, but we’ve seen it in other jurisdictions where [transmission and distribution providers] are dealing with it differently in their specific service territory or it’s happening at the RTO level. Not only do we have a lot of tools, but we’re in a market where finding innovative approaches and looking at problems in a completely new way is possible based on how the market is designed.”

Caitlin Smith, policy lead for storage developer Jupiter Power, called for load forecasts that are accurate and believable. Load forecasts help transmission planning, she said, but the market also needs to know what is coming in order to serve resource adequacy.

“We’ve had what we all recognize as these kind of very bloated load forecasts. I think we will see that what comes out of this law is hopefully a more accurate load forecast,” Smith said. “Load being the signal that you need more generation, but my understanding what may be different about the data center loads and the AI loads is they’re not price responsive. That creates a tricky situation when you’re thinking about these things, too, right?”

PUC Reviewing 4CP Program

High on the PUC’s priority list is a review of ERCOT’s 4CP program, which assesses transmission charges for the following year based on the grid’s overall — or coincident — peak demand during four 15-minute intervals, one from each summer month. The Texas grid’s increased reliance on solar power has shifted tight conditions from the load peak to the net load peak at the same time as more flexible crypto miners and data centers are connected to the system.

That has caught the attention of lawmakers, who directed the PUC to review 4CP within the context of SB6. The review must be completed by the end of 2026.

“[4CP] has long been a subject of discussion and debate. It certainly will have an impact on incentives for loads and for the market,” Bonskowski said.

Michael Macias, vice president of operations for Electric Transmission Texas, a joint venture between American Electric Power and Berkshire Hathaway Energy subsidiaries, urged his panel’s listeners to engage themselves in the stakeholder process.

“I think it’s clear that 4CP is on the table for a revision. What’s not clear is how that’s going to be implemented,” Macias said. “What’s also clear is that we know that in order to support the substantial growth that we’re seeing in our time, we’re going to have to spend tens of billions of dollars. If we’re going to build the system up to bring the new load in, then we need to make sure that we’re putting protections in place for everybody, for the folks that are investing in that infrastructure, folks that are using that infrastructure, and then for everybody else that wasn’t planning on having to pay for 760 pipelines around the state.”

Robertson said the conversation needs to include how costs are allocated to large loads.

“I think it’s largely the expectation that AI or high-performance computing data centers wouldn’t necessarily participate in 4CP, so their demand would be whatever their load contribution is during the coincident peaks,” she said. “I think another question that SB6 is asking is how transmission costs are allocated. … That’s something that is going to go back to addressing utility business models. And again, I think it also goes back to the fact that if you want to be interconnected to the grid very quickly and you’re willing to pay for it, maybe you can shoulder 100% of the cost. So, I think that’s a bigger question that isn’t necessarily addressed by 4CP or 8CP or 12CP or whatever it ends up being.”

Managing Large Load Forecasts

Kristi Hobbs, ERCOT’s vice president of system planning and weatherization, keynoted the summit’s second day with a discussion of — what else? — large loads and their effect on the market.

She said ERCOT’s regional transmission planning studies look six years into the future because “we know it takes time to build transmission on the system.”

As part of ERCOT’s latest regional plan, staff asked transmission service providers how much load they were expecting to hook up to their systems. They told staff they expected more than 218 GW of demand.

“Anyone in this room believe that we’re going to hit 218 GW of demand in six years?” Hobbs asked.

A few hands shot up.

“Anybody believe we won’t?” she asked.

More hands were raised.

“Yeah, we were a little bit uncertain about that as well,” she said. “If we would have taken the entire forecast that we received from the transmission service providers, it would have been 85,000 MW of demand from data center loads. That’s more than the entire United States.”

ERCOT is currently tracking about 188 GW of large loads seeking interconnection, compared with 63 GW in December 2024. The grid operator has reviewed and approved planning studies for more than 19 GW of large loads over the past two years. Almost 7 GW have been approved to energize.

A report released in August by Enverus Intelligence Research said load projections from ERCOT and PJM widely differ from the company’s models.

“ERCOT’s and PJM’s estimates imply that each of the next five years, their regions alone would absorb more than 100% of U.S. annual data center capital spending, an assumption we believe is unrealistic,” according to Enverus senior analyst Kevin Kang.

“We know a lot is coming in Texas, but we need to be careful that we’re balancing the cost to consumers with the transmission build for those that will actually be here,” Hobbs said. “They’re very motivated, they’ve got contracts … and they’re wanting to move forward. They come motivated.

“We also have some that come, and I feel like they’re just fishing,” she added. “They put in a request over here, they put a request over there, and they see which utility bites. Whichever one bites first, they’re going to go with that, and then they let the other one just fade off.”

Clean Energy Still Faces Uncertainty

With the federal budget reconciliation bill hamstringing the development of clean energy, the only resource that can quickly and cheaply be brought to market, the sector is grappling with an uncertain future. The bill took away tax credits from wind and solar projects unless they were able to begin construction by July 4, 2026 — or be in service by Dec. 31, 2027, if they did not meet the July 4 deadline.

Clean energy advocacy group E2 said companies have canceled or scaled back more than $22 billion in projects since the start of 2025, including $6.7 billion in investments in June alone.

“It is going to be impactful long-term and in the immediate, too,” said Doug Pietrucha, senior principal with Advanced Energy United. “Realistically, those resources needed to have steel in the ground in the next 10 months to have any ability to take advantage of the remaining tax opportunities that exist for them. So really, the quickest turnaround for those resources is creating a huge decision-point bottleneck for those developers at the moment. There are a lot of projects that are on the bubble.”

Pietrucha noted that batteries are eligible for credits into the 2030s, as long as they maintain Foreign Entity of Concern compliance.

“Certainly, storage has the capacity to do procurement in a way that will permit them to qualify into the future, but the reality of navigating how to do it and actually getting your hands on components that are going to keep you compliant is a whole ballgame in itself,” he said.

“We’re on pause right now, there’s so many moving pieces,” energy storage consultant Katherine Meik said. “It’s not just about the tariffs. Sometimes, it’s about equipment availability. I think a lot needs to be defined. We’ll start seeing some of those answers, but we need to get through the tariff wars first and then we have to figure out who can manufacture and where it’s coming from.”

Asked how ERCOT is dealing with the uncertainty, Hobbs said SB6’s directive to standardize the information required to be included in load forecasts will help. Large load customers must disclose whether they are pursuing similar interconnection requests elsewhere in Texas that could affect the planning and timing of their requests.

“We’re working with the utilities who have the relationships with the customers making the load request to better understand the level of certainty,” she told RTO Insider. “I think we have more certainty on those developments in the shorter term and then it’s getting the best information on the longer-term [loads].”

Developers: Chaos is Good

That uncertainty is not necessarily a problem, agreed a panel discussing the future of the Texas grid, which leads all other states in clean energy installations.

Former ERCOT staffer Nemica Kadel, now with Lightsource BP, advocated for a hybrid solution where everyone contributes to the cost of building out the grid because “we’re all working towards a stable grid.”

“[Cost allocation] has always been a heated topic, especially in Texas, where it’s a socialized cost. There’s questions of who gets to hold the bag right now,” Kadel said. “The way it is, all the ratepayers are paying for it. There’s also a lot of demand, and I know that the policymakers are working on trying to come up with the optimal solution.”

“I’ve always been told that power development is no place for the faint of heart,” moderator Dino Barajas, with the Baker Botts law firm, said. “If you have a weak stomach, you’re probably in the wrong industry, because everything changes on the dime.”

“Every chaos is an opportunity, right?” Kadel responded.

“I love the chaos, just simply because we do have chaos and people have to be talking about it. People talking about it is a good way to get improvements,” said Alex Shattuck, director of grid transformation for Energy Systems Integration Group.

As an example, he used the technical aspects of recent regulatory changes for clean energy being critical facts for eight years.

“We’re just now getting there and putting them into place because people are finally talking,” Shattuck said. “The conversations they’re having give [the regulatory space] momentum to actually get improvements and enhancements to regulatory procedures done.”

“The chaos is 100% a good thing,” OTC Global Holdings’ Campbell Faulkner said. “We finally went from the power industry being rather boring to being interesting again.”

After more than a year of preliminary proceedings, parties filed their first briefs Aug. 30 in Appalachian Voices v. FERC, in which the 4th U.S. Circuit Court of Appeals is reviewing the commission’s Order 1920 (24-1650).

Parties from all sides of the argument weighed in. Environmentalists and developers argued the transmission order did not go far enough. States and utilities argued FERC exceeded its authority. And one brief seeks to avoid the reimposition of a federal right of first refusal (ROFR). A response from FERC is not due until early 2026. The court will take other briefs later in February.

A group of more than 30 utilities that includes American Electric Power, Dominion Energy, Duke Energy, Exelon and Xcel Energy Services argued FERC exceeded its authority by forcing them to file cost-allocation proposals they might disagree with.

“FERC compels public utilities to include and promote state-designed utility tariff provisions, including those with which utilities disagree, which FERC would then be free to adopt even though the utility’s proposal was just and reasonable (the ‘inclusion requirement’),” the utilities said. “FERC also requires public utilities to consult with states before exercising their statutory right to amend their long-term transmission cost-allocation, and to explain why they reject contrary state proposals (the ‘consultation requirement’). This violates both the FPA [Federal Power Act] and the First Amendment.”

In the initial version of Order 1920, FERC declined to make utilities file state agreement approaches against utilities’ wishes, but in Order 1920-A, it reversed course and allowed “state entities to infringe on transmission providers’ filing rights.”

The filings come under Section 205 of the FPA, which is supposed to be reserved for utilities that cannot be forced to include proposals from states or other third parties. FERC said it would consider state agreement approaches on par with utilities’ own cost-allocation proposals, even though it is supposed to accept utilities’ Section 205 filings if they are in a broad zone of just and reasonable rates.

“FERC cannot circumvent statutory limitations by creating a rule that trumps the FPA’s plain meaning and confers on state entities filing rights that Congress withheld,” the utilities said.

Even when FERC sets a rate under Section 206 of the FPA, the utility keeps its right to respond and propose its own preferred rate under Section 205, the utilities said.

“Section 206 does not authorize FERC to override utilities’ Section 205 rights,” they added. “When remedying a rate that it finds no longer just and reasonable under Section 206, FERC must stay within the statutory limits of its power, just as in any other remedial context.”

Another brief arguing for rehearing was filed by the American Forest and Paper Association, Industrial Energy Consumers of America, National Rural Electric Cooperative Association, New England States Committee on Electricity, Ohio Consumer’s Counsel and others that faulted FERC for failing to adopt cost-management and customer-protection proposals.

“Order 1920 arbitrarily and capriciously facilitates an escalation in transmission rates without implementing any cost controls and cost-containment mechanisms to ensure rates remain just and reasonable,” the groups said. “FERC’s rejection of its initial proposal to eliminate certain transmission rate incentives for long-term regional projects violated FPA Section 206’s requirement that FERC must remedy unjust and unreasonable rates and practices.”

That includes a financial incentive that allows utilities to charge consumers 100% of prudently incurred costs before projects go into service, or even if they never go into service. FERC also failed to address ideas of an independent transmission monitor to ensure fair plans, leaving that for another docket where it has no requirement to act.

Order 1920 also shifts the costs of interconnecting generators from developers themselves to consumers, who will pay for those lines under the regional transmission planning process, the organizations said.

Their brief also urged the court to find that electric cooperatives can participate in the cost-allocation process with states. In much of the country, cooperative boards establish their consumers’ rates independently of any state regulator.

States including the attorneys general of Texas and Utah, the Arizona Corporation Commission, the Louisiana PSC, the Mississippi PSC, the Ohio PUC’s Federal Energy Advocate and others argued FERC goes too far and is trying to encourage a shift to renewable energy with Order 1920.

“It effectively transforms the transmission planning process into a tool to subsidize transmission facilities that support a specific set of favored generation resources,” they said.

Order 1920 requires transmission providers to use seven categories of factors to develop planning scenarios that lead to the construction of favored technologies. The factors include state or local policy, including decarbonization and renewable energy targets.

“The effect of this process is to socialize costs of transmission,” the state opponents said. “If a city passes an ordinance requiring that all its energy must be solar (without regard to the cost), the transmission provider for the entire region must now account for that policy in its planning and thus build the infrastructure necessary to support the city’s power generation goals. The transmission providers cannot disregard the policy as unreasonable.”

States that favor traditional methods of power generation are required to subsidize the development of the infrastructure required to support states and localities that favor other methods of generation, they added.

Appalachian Voices, Invenergy, Environmental Defense Fund, Natural Resources Defense Council, Sierra Club and others filed a brief that FERC did not go far enough and that Order 1920 will not fix the “broken” transmission grid that has been neglected by is owners and operators for decades.

“The existing regional grid has experienced catastrophic and deadly failures during extreme weather events,” the environmentalists and Invenergy said. “It lacks the infrastructure necessary to adapt to acute changes to electricity supply and demand. And cheaper, cleaner resources wait years to connect to the grid while aging, uneconomic plants are unable to retire, costing consumers billions of dollars every year.”

FERC has passed other transmission reforms over the decades where it was clear what the industry had to do, they argued. But when it paired “a choose-your-own-compliance adventure” with a general set of planning principles then nothing changed.

“This is unsurprising; incumbent transmission owners tasked with transmission planning and development have financial incentives to avoid the most cost-effective projects, since truly efficient regional transmission introduces competition and reduces profits for them and their affiliated generating resources,” the environmentalists and Invenergy said.

They argued that FERC was wrong to let transmission owners ignore benefits like access to cheaper generation, deferred generation investments and increased competition from the planning process. It also failed to consider alternatives such as new transmission technologies and storage, or merchant transmission lines, in the planning process.

The final brief came from industry competition proponents such as Advanced Energy United, Electricity Transmission Competition Coalition, LS Power and others. They argued FERC should not have reimposed a federal ROFR for “right-sized” projects.

Order 1000 had eliminated federal ROFRs, but Order 1920 would reimpose them for projects that come out of local planning processes but would produce more benefits if the need addressed a larger, regionally planned project.

The rule is the first time FERC has imposed a ROFR on its own. The old federal ROFRs were put in place by incumbent transmission owners themselves and filed with FERC under Section 205 of the FPA. It proposed the new one because in earlier rounds of reforms, many incumbent transmission owners were replacing aging infrastructure on their own, avoiding regional planning processes.

FERC reasoned that allowing a ROFR for right-sized projects would subject more transmission to regional planning. Competition proponents argued the lack of planning for such lines was a calculated effort from utilities to counteract Order 1000’s attempt to use competitive market forces.

“Order 1920 takes a drastic step in the opposite direction — creating a ROFR from whole cloth and mandating its use in FERC-jurisdictional tariffs — on the flawed theory that the power to find a practice unlawful under the FPA necessarily entails the power to mandate that practice,” AEU, ETCC and LS Power said.

“Although FERC’s motivation to incentivize regional transmission investment may be well-intentioned, its chosen method is both misguided and unlawful. Giving incumbent transmission owners a monopoly right to build tomorrow’s regional grid free from competition is a Faustian bargain. For the incumbent utilities, that deal is too good to be true. For consumers, it is a financial nightmare.”