Missouri Attorney General Andrew Bailey says he has opened an investigation into Invenergy’s Grain Belt Express transmission project, an 800-mile, HVDC line spanning four states that has been under development since 2010.

Bailey told Invenergy in a June 27 filing that he “has reason to believe” Grain Belt’s developers have “used deception, fraud, false promise, misrepresentation, unfair practice or the concealment, suppression or omission of material fact in connection with its statements and actions” related to the project.

He sent a letter to the Public Service Commission on July 1 urging it to re-evaluate the project’s certificate of convenience and necessity by using its authority to “demand” updated long-term planning and revoke project approvals that are no longer in the public interest.

A PSC spokesperson told RTO Insider that the commission is reviewing the attorney general’s request and declined further comment.

Bailey said the Grain Belt application “relied on speculative and possibly fraudulent assumptions.” He said the developers’ calculations relied “significantly” on a carbon tax, pointing out that neither Missouri nor the U.S. government have carbon-reduction policies.

Andrew Bailey | Missouri Attorney General’s Office

“Grain Belt’s speculative and faulty calculations based on anticipated carbon tax has more than likely inflated demand for this project and dramatically overstated any resulting benefit to Missourians, directly undermining any claims of demonstrated need, economic feasibility and public interest,” Bailey said in the letter to the PSC.

“We’ve been absolutely transparent with everybody involved,” Michael Polsky, Invenergy’s founder and CEO, told The New York Times. “Whatever investigation they want, we will fully cooperate. We have nothing to hide. We’ve done everything above board.”

A Grain Belt spokesperson called the investigation a “last-ditch and obviously politically driven attempt to delay construction” of the project when “our country is facing a national energy emergency,” as declared by President Donald Trump. (See What is and isn’t in Trump’s National Energy Emergency Order.)

“We should be building energy infrastructure in America, but the Missouri attorney general is instead playing politics with U.S. power,” the spokesperson said in an email. “Electricity demand is rising across the country, and we urgently need transmission infrastructure to deliver power. Projects like Grain Belt Express are the answer to providing all forms of affordable and reliable electricity to U.S. consumers.”

U.S. Sen. Josh Hawley (R-Mo.) has also weighed in with a letter to the Department of Energy in June asking Secretary Chris Wright to terminate a $4.9 billion loan guarantee issued by the Loan Programs Office in 2024.

Hawley, who has called Grain Belt Express a “boondoggle,” noted the department is moving forward with the draft environmental impact statement, “a key step in approving the loan.”

Invenergy says the $11 billion project will provide $52 billion in energy cost savings over 15 years, create 5,500 American jobs and power up to 50 data centers. A 2022 economic analysis conducted for Invenergy found that the project would result in $20 billion in total investment and create more than 20,000 temporary jobs and more than 400 permanent jobs in Illinois, Kansas and Missouri.

Invenergy says Grain Belt, a merchant open-access line, will move about 5,000 MW of a “diverse mix of energy” from Kansas across Missouri and Illinois to Indiana. The project will deliver cost savings and strengthen reliability for 29 states and D.C. and more than 40% of Americans, it said.

The project would create links between the SPP, MISO, Associated Electric Cooperative Inc. and PJM grids.

Kansas, Missouri, Illinois and Indiana have all approved the project. The Missouri PSC found the project would save the state’s customers as much as $18 billion, Invenergy said, and noted municipal utilities in 39 communities have contracts with it for power delivery and contractually guaranteed cost savings.

The project has faced pushback from Missouri landowners, who are opposed to a for-profit private entity using eminent domain. Bailey has criticized Grain Belt for filing nearly 50 eminent domain lawsuits against Missouri landowners.

In a blog post, Invenergy said “responsible transmission developers respect private property rights and make every effort to negotiate with landowners.” It said it has “among the strongest set of landowner protections and compensation packages, including a code of conduct and agricultural impact mitigation protocol.”

Invenergy says it has completed over 95% of land acquisition for Phase 1, the segment connecting Missouri and Kansas. The phase’s construction is scheduled to start in 2026.

Grain Belt’s developers received some good news July 1 when the D.C. Circuit Court of Appeals denied a rehearing request from a group of Illinois landowners. The court dismissed the lawsuit in April, finding the group had failed to demonstrate that they will suffer a “certainly impending” injury-in-fact (24-1213).

Grain Belt has been under development since 2010, when the now-defunct Clean Line Energy first proposed the transmission line. After years of regulatory, legal and political hurdles, Clean Line sold the project to Invenergy. (See Invenergy Renewing Push for Grain Belt Express.)

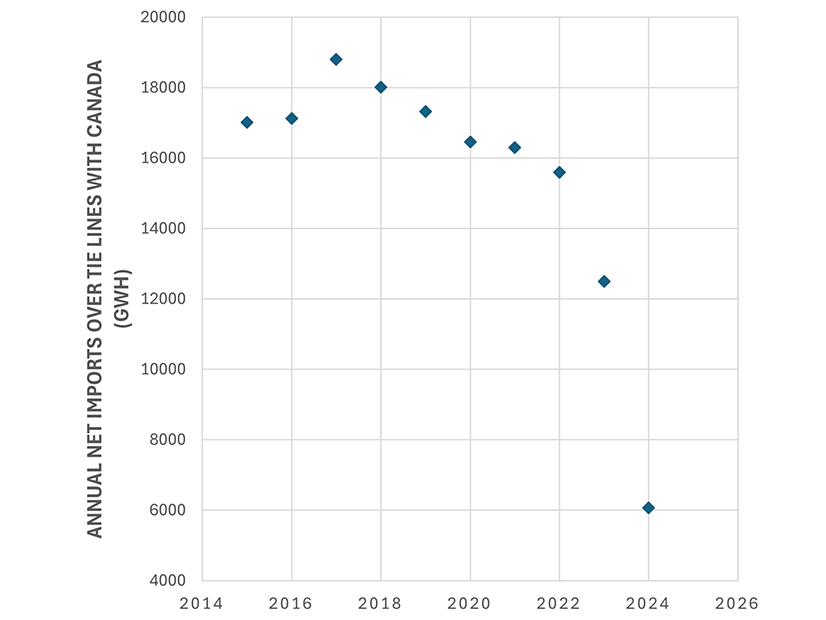

In the spring, as questions swirled about potential Trump administration tariffs on electricity from Canada, power flows from Québec to New England declined substantially, causing some concerns that the tariff threat was causing Québec to limit power exports to the U.S.

While these concerns appear unfounded — the drop in imports likely was driven largely by low power prices in New England — the low import levels illustrate a series of growing challenges on both sides of the border.

Imports from Québec historically have played a significant role in the ISO-NE system, accounting for an average of about 11% of net energy for load in New England between 2015 and 2022. But net imports over tie lines with Québec have dropped drastically over the past two years, making up just over 5% of net energy for load in New England in 2024 and sitting at a similar level through the first four months of 2025, according to ISO-NE data.

The largest factor driving Québec’s multi-year reduction of exports appears to be an extended drought, which began in early 2023 and has caused declining water levels in Hydro‑Québec’s major reservoirs.

“It’s the third year of a deep drought,” said Robert McCullough, principal of McCullough Research. Data collected by the firm indicate water levels of Hydro-Québec’s largest reservoir systems have declined significantly since the start of 2023.

Hydro-Québec’s exports also have been affected by a pair of looming, long-term power contracts the company signed with U.S. states: the 1,200-MW New England Clean Energy Connect (NECEC) project, anticipated to come online at the end of 2025, and the 1,250-MW Champlain Hudson Power Express transmission project, expected to come online in mid-2026. Both projects are intended to procure over 1,000 MW of baseload power on an annual basis from Hydro-Québec.

“When we talk about exports, an important firm energy commitment we have to take into account is the two new contracts that we will have with New York and Massachusetts,” said Maxime Nadeau, senior director of system control and grid operations at Hydro-Québec.

Over the past two years, the company has reduced its allowed amount of non-firm exports to ensure it has enough water to meet all its long-term firm power commitments, Nadeau said.

Québec, like much of North America, faces its own load growth; Hydro‑Québec’s most recent electricity supply plan forecasts power demand to grow by 14% between 2022 and 2032. While the company has announced plans for major long-term investments in new generation, the impending addition of new export commitments could pose a challenge over the next few years if drought conditions persist.

Declining Water Levels

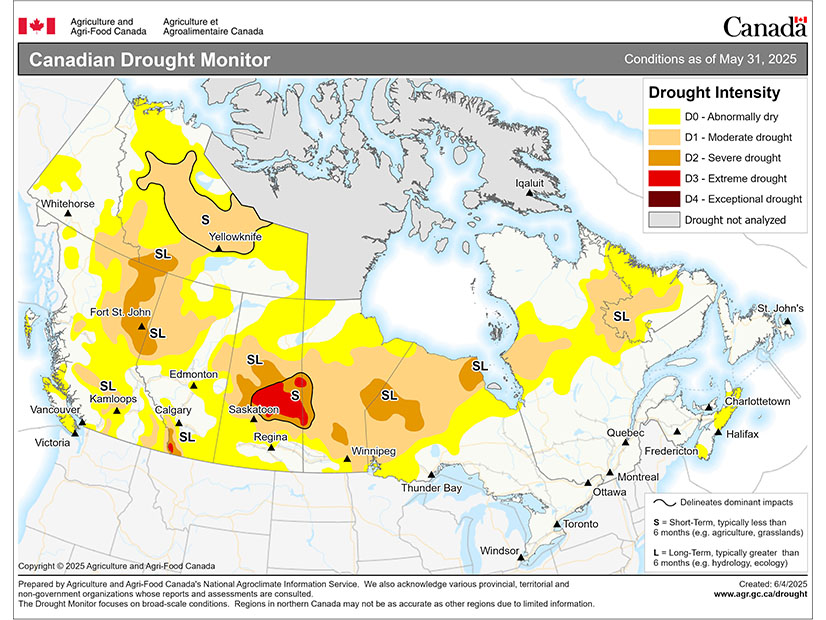

On the La Grande watershed in northern Québec, home to more than 17,000 MW of installed hydroelectric capacity, 2025 inflows are tracking between 2023 and 2024 levels, according to data from McCullough Research. Meanwhile, the Canadian Drought Monitor indicates that a significant portion of northern Québec is facing moderate drought or abnormally dry conditions, according to the May 31 update.

“We’re having even lower inflows than we had last year,” McCullough said. “If they go into a fourth year of drought, [Hydro‑Québec] may be forced to reduce their external commitments.”

Canadian Drought Monitor, May 31 | Agriculture and Agri-Food Canada

Despite low water levels, representatives of Hydro‑Québec expressed optimism that inflows will return to typical levels this year, bringing the region’s reservoirs back to historical norms. The company has maintained it will have enough energy to meet all its firm commitments in the coming years.

“The very low inflows observed in 2023 and 2024 have had a lasting impact on 2025 overall levels,” said Lynn St-Laurent, spokesperson for Hydro‑Québec. “However, the combination of a revised production strategy and normal inflows should help restore water levels to more typical values.”

St-Laurent said it is normal for the region to experience fluctuating water levels and that the company has faced multiyear droughts on a similar scale in the past.

She stressed that “inflows remain around normal levels for 2025” and said it can be misleading to compare inflows at an isolated point in time, noting that “the low water availability of the last two years at La Grande was not due to weak spring runoff, but rather to low precipitation during the summer and fall of previous years.”

Climate Impacts and Uncertainty

While it is difficult to pinpoint exactly how climate has affected the current drought and water levels, scientists expect precipitation variability — both over multiyear stretches and intra-year periods — to increase in Québec as the planet warms.

“We expect droughts to be more frequent and more persistent in the future, related to climate change,” said Christopher McCray, climatologist at Ouranos, a climate research organization funded by the Québec government.

Although most studies indicate northern Québec will see increasing average annual precipitation, multiyear drought periods could create increasing challenges for water management, McCray said.

While Québec always has seen a fluctuation between dry and wet years driven by large-scale weather patterns, warming temperatures are “accentuating the effects of those patterns,” McCray said.

“The same weather pattern that caused a drought 50 years ago, now it’s a little bit warmer … and there’s a greater capacity for evaporation than in the past,” McCray said. “And so, the soil dries out, and that can cause a feedback loop that leads to a persistent period of dry conditions.”

Hydro‑Québec expects to see “more overall water supply in the northern part of the province,” Nadeau said. “That’s good news, because that’s where we have all of our major main reservoirs.”

He added that the company recently began working with experts on studies to better understand how climate change will affect inter-annual variability.

Researchers also anticipate climate change will cause seasonal shifts in precipitation. Ouranos predicts average winter precipitation to increase and more frequently fall as rain. This likely would increase stream flows in the winter and move the spring high-runoff period earlier in the year.

McCray said there is more uncertainty around how climate change will affect overall summer precipitation but that there could be an increased “whiplash” between dry periods and extreme rainfall events within summer seasons.

While long-term scientific studies consistently forecast increased precipitation for the province, McCullough said the impact of climate change on the jet stream has created significant new challenges for forecasting precipitation and water levels.

“We’ve been doing this for about 40 years,” McCullough said. “I would’ve sounded a lot more confident 20 years ago.”

The jet stream — a strong west-to-east flow of air typically located five to nine miles over the U.S.-Canada border — causes droughts when larger-than-normal north-south waves in its flow push precipitation away from a region for an extended period, said Jennifer Francis, a senior scientist at the Woodwell Climate Research Center.

“A growing body of research is finding that wavy jet-stream patterns are occurring more often, in part because the Arctic is warming three to four times faster than the globe as a whole, which reduces the north-south temperature difference that fuels the jet stream,” Francis said. “A weaker jet stream is more easily deflected from its west-to-east path by things like mountain ranges and abnormal temperature patterns, which causes larger north-south excursions and increased waviness.”

Increasing disturbances to the jet stream will cause more temperature and precipitation extremes in the northern hemisphere, Francis explained.

“When it comes to Québec’s reliance on rainfall to fill rivers and reservoirs to generate electricity, this aspect of human-caused climate change is indeed a concern,” Francis said. “Some years will bring extended droughts. Others will bring prolonged rains. Both extremes are expected to occur more often as we continue to add heat-trapping gases to the atmosphere.”

As increased temperatures and decreased snow cover dry out soil, wildfire risks also are increasing in Québec, creating additional reliability risks on the power system, which can have knock-on effects on reliability in the U.S. In 2023, a forest fire caused the shutdown of a transmission line in Québec during New England’s evening peak, triggering an ISO-NE capacity deficiency. (See Canadian Wildfires Trigger ISO-NE Capacity Deficiency.)

According to an analysis by World Weather Attribution, an academic research group, “climate change made the cumulative severity of Québec’s 2023 fire season to the end of July around 50% more intense, and seasons of this severity at least seven times more likely to occur.”

‘More Dynamic Changes in Flow’

In the coming decades, with the anticipated growth of intermittent renewables across the Northeast, Hydro-Québec expects its reservoirs to be used less as a baseload power resource and more as a massive balancing resource, allowing the company to conserve water during periods of high renewable production. (See Québec, New England See Shifting Role for Canadian Hydropower.)

The economic justification for a large-scale two-way exchange of power between regions likely will not occur until a significant number of offshore wind projects come online, which may not be until the mid-2030s or later. However, Vineyard Wind and Revolution Wind appear on track to eventually deliver about 1,500 MW of capacity to the New England grid, which could drive more frequent power exchanges between regions during periods of high production.

“With all that renewable energy that is being integrated in the electrical grid, we will see more dynamic changes in flows on the interties,” Nadeau said, adding that it is harder to forecast changes to the overall balance of imports and exports.

This phenomenon could help the region address a major need for clean firm energy to help meet state climate targets in the coming decades. (See ISO-NE Study Lays Out Challenges of Deep Decarbonization.) A 2021 study found that increased transmission capacity between regions would significantly reduce the overall costs of decarbonization by 2050 and limit the need to overbuild intermittent renewables.

However, if Canadian hydropower ultimately is to help displace fossil units in New England, the region must be able to rely on the power when it is needed.

While imports from Québec have performed during capacity deficiencies in the region in recent years (aside from the 2023 wildfire-induced line outage), the decrease in overall import levels since 2023 has given fuel to arguments that imports from Québec are not as reliable as in-region generation.

In NEPOOL debates over the development of a new capacity accreditation framework for ISO-NE, representatives of generation companies have argued the RTO overestimates the benefits of its interregional transmission lines during emergency events, noting that these tie benefits are not backed up by capacity supply obligations. (See ISO-NE Discusses Details of New Prompt Capacity Market.)

Generation companies in New England also have expressed concern about the overall annual level of imports the region can expect to receive from Québec.

While the NECEC transmission project is intended to provide firm supply from Hydro-Québec, skepticism about how much incremental power the project will provide the region dates back to state regulatory proceedings for the power procurement. Multiple groups voiced concern in the proceedings that the contracts do little to guarantee net imports above the historical levels to New England.

In its approval of the contracts in 2018, the Massachusetts Department of Public Utilities wrote that the NECEC power purchase agreements would guarantee firm power deliveries incremental to what Hydro‑Québec “would otherwise be expected to deliver to New England through its ongoing, largely non-firm commercial trading activities (D.P.U. 18-64).”

Ultimately, when NECEC comes online, flows from Québec to New England are poised to increase; the NECEC contract requires the company to send 9.55 TWh of power annually, compared to the 6.3 TWh of power imported to New England in 2024.

The export commitments, coupled with the addition of Vineyard Wind and Revolution Wind, may correspond with an increase in Québec’s spot market imports from New England, potentially mitigating the change to the overall balance of power exchanges. Beyond its export commitments, the total amount of power Québec sends back to New England may depend in large part on how long the drought conditions persist.

“At the moment, given the forecasts of a significant deficit at Hydro-Québec, I don’t think [NECEC] will change the balance at all,” McCullough said. “There’s nothing in the contract to prevent them from buying cheaply in New England, storing it and sending it back to New England.”

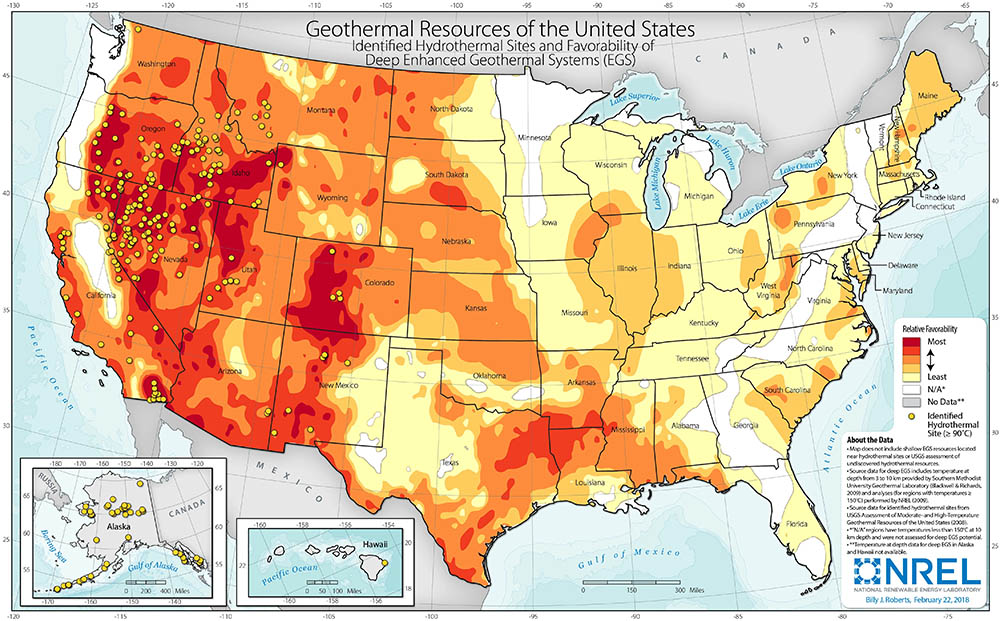

Until now, a carbon-free, load-following electric supply resource has been elusive. That may be about to change because of a resource that sits literally right below our feet — even if it is a mile or more down. That supply resource is the earth’s heat, which radiates continuously from the earth’s core, and entrepreneurs are quickly figuring out how to tap it.

Developers have been accessing traditional geothermal energy resources for decades in those limited areas of the world where hydrothermal resources exist in the form of hot springs, geysers, volcanoes and fumaroles. These areas typically are near tectonic plate boundaries. In this country, 93% of the 3,700 MW of installed capacity is located in these more geologically active areas of California and Nevada. In recent years, though, development of domestic hydrothermal resources has stagnated.

Fortunately, a much larger geothermal resource exists that is more geographically widespread, and it doesn’t require the presence of existing underground water. Developers are tapping into this unconventional geothermal asset by using specialized equipment to drill holes miles deep into hot, hard rock — often granite.

Using techniques developed in the hydrocarbon fracking industry, specialized technicians drill at depth, then rotate the drills 90 degrees and guide them laterally to develop horizontal boreholes in the hot zones that often exceed 300 degrees Fahrenheit. Instead of relying on existing underground water resources, developers bring their own working fluids, typically water but also high-pressure supercritical carbon dioxide (neither a gas nor a liquid). These working fluids are circulated deep underground to harvest the rock’s ambient heat and bring it back to the surface, where it creates steam to spin turbines and generate power.

This new geothermal industry already is branching off into multiple approaches, some of which may work better than others based upon local conditions. Today, the two main approaches are called enhanced and advanced geothermal.

Enhanced geothermal: The enhanced geothermal companies typically drill parallel wells and then frack the rock between the wells using high-pressure water. This creates fissures in the rock and establishes permeability and connectivity between two wells. An injection well introduces water into the system, which heats up when it contacts the broad surface areas in the broken rock. The second withdrawal well draws the heated water back to the surface for electricity generation.

Just as with hydrocarbon fracking, developers can punch multiple wells into the earth from a single pad, minimizing drilling time and surface area impacts. Fiber optic cables collect data relating to temperatures and the flow of the working fluids that capture and “mine” the heat from the rock. The trick is to optimize the flow of fluids to capture the maximum amount of heat extracted to the surface.

Advanced geothermal: With advanced geothermal development, some operators drill vertically and then horizontally, but rather than fracking the rock, they install a lining in the hole to create closed-loop circuits, essentially developing underground inverse radiators. Others use a pipe-within-a-pipe system, sending water down in one pipe and withdrawing it through the other. In either case, a finite quantity of working fluid — either water or supercritical CO2 — is injected into the closed system, heated by the surrounding rock, and then brought back to the surface. The use of supercritical carbon dioxide requires special turbines, but because it boils and creates high-pressure steam at lower temperatures, it can further enhance output.

The first commercial contracts point the way: Within the past year, leaders in this nascent industry have inked the first meaningful deals. Pathbreaker Fervo Energy signed its first 3-MW proof-of-concept contract with Google in late 2023. It then turned its attention to developing a far larger effort in Cape Station, Utah, and has signed contracts with Shell Energy, Clean Power Alliance and Southern California Edison, with initial deliveries from its 500-MW facility beginning next year.

Technological advancements: Just as the fracking industry saw rapid technological development and improvements resulting in lower costs, the new geothermal players also are pushing the envelope as they drill deeper into challenging heat and hard rock environments. They use tools and practices adopted from conventional drilling and fracking and adapt those to their specific industry. These include specialized polycrystalline diamond drill-bits, specialized lubricants and additions to the drilling mud that keep the well cool enough for the equipment to operate.

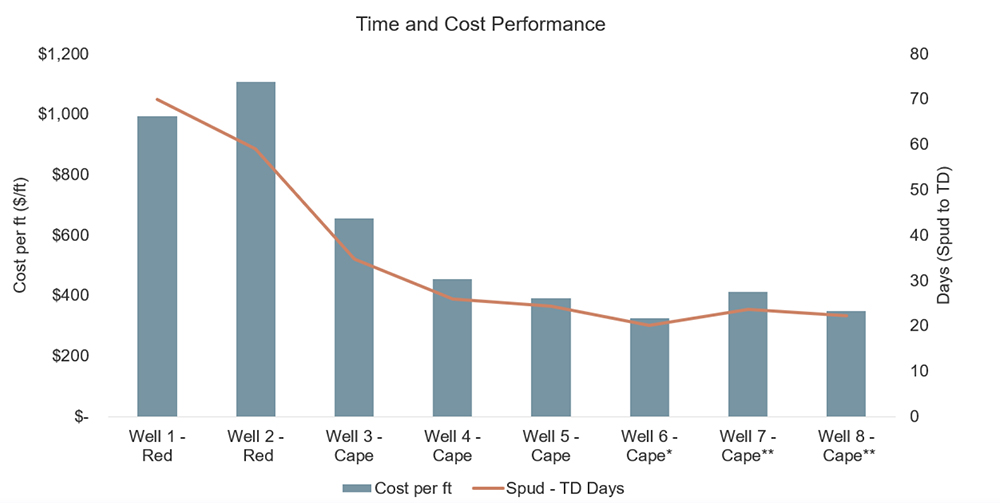

A recent paper evaluating drilling speeds and costs demonstrated significant progress — in terms of speed, required number of drill bits and related costs — with each new well drilled. In the example cited, Fervo was able to demonstrate a 60% improvement in drilling speeds over just eight wells.

Fervo horizontal well cost per ft and spud to TD trends | Stanford University

Multiple players, with a growing pot of money: There are more than a dozen geothermal startups in the U.S., with Texas seeing the greatest concentration. Together, they have been funded with more than $2 billion (Fervo just raised an additional $206 million for project financing in June).

Many companies are far enough along in their efforts that 11 of them have been pre-qualified by the U.S. Department of Defense for projects on military bases (and seven pilots reportedly are in the works). Most are adapting existing oil and gas technology, but startup Quaise is using a different approach. It emulates others by drilling to initial depths using conventional technology. However, it then plans to go far deeper than its competitors — as far as 12.5 miles down to access heat over 900 F — and to achieve this goal, it is testing high-powered millimeter waves that vaporize holes in the rock.

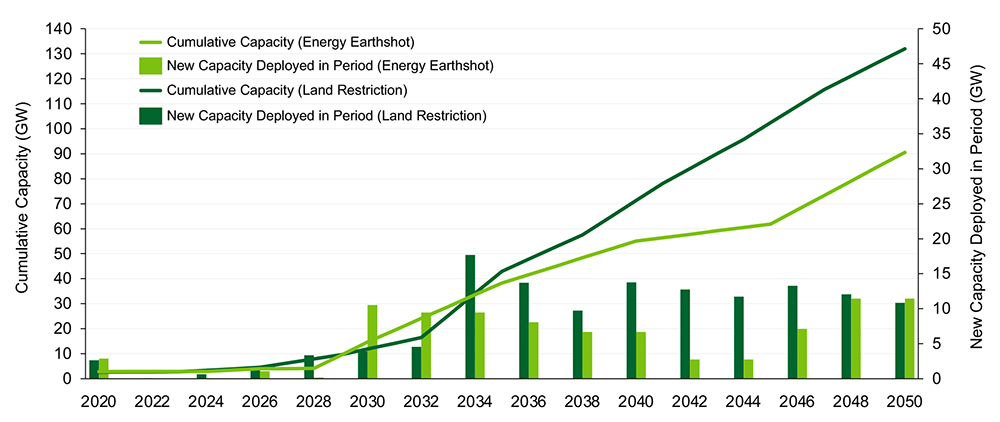

Size of potential resource: Studies suggest the geothermal resource is enormous. A June 2025 study looking at New Mexico estimates as much as 163 GW of potential geothermal production, 15 times the state’s installed capacity. At the national level, a 2024 Department of Energy Lift-off study suggested a potential 90 to 130 GW of installed capacity over the next 25 years.

Estimated next-generation geothermal deployment potential | DOE

That number would represent a fraction of the 7,000 GW of national potential at three miles deep, and 70,000 GW accessible at all depths. There’s one inherent challenge here, though: The geology of the U.S. clearly favors the West, where drillers can access heat at far shallower depths. Because going deeper has been prohibitively expensive and time consuming until now, the Eastern U.S. has been largely excluded from consideration.

That may be changing, though, as evidence is beginning to suggest that perhaps these deeper depths are more easily attainable. Fervo announced in June that it had drilled a new well to a depth of 15,765 feet (75 feet shy of three miles!) in only 16 days, accessing temperatures in the range of 520 F. Furthermore, it was able to drill laterally through the hard rock at that depth at an impressive rate of over 300 feet per hour.

Hype or real reason for hope? While it’s still too early to tell, and early capital certainly will be deployed where drilling is easier and more cost-effective, we may see an industry expansion to the east in the visible future. For the emerging unconventional geothermal industry, the theoretical potential is there and the first facts on (and in) the ground are promising.

The industry already has viable and tested technology, successes, financing and the first commercial contracts in hand. It also may have continued government support in the form of continued tax credits and a relatively easy permitting process for projects on federal lands. We will know a lot more about just how real this industry is in just a few short years.

Around the Corner columnist Peter Kelly-Detwiler of NorthBridge Energy Partners is an industry expert in the complex interaction between power markets and evolving technologies on both sides of the meter.

A yearslong dispute over who gets to own a 345-kV network upgrade in Michigan had the D.C. Circuit Court of Appeals meditating on the definitions of “system” versus “facility.”

Ultimately, the D.C. Circuit decided that Michigan Electric Transmission Co. (METC) does not have exclusive ownership rights to an almost $12.4 million upgrade to support EDP Renewables’ in-progress 120-MW Eagle Creek Solar Park (24-1039).

The court’s July 1 order means that Michigan Public Power Agency (MPPA) and Wolverine Power Supply Cooperative, as fellow co-owners of the existing Styx-Murphy 345-kV line, also should have a stake in the line’s extension and new substation construction.

The D.C. Circuit examined the semantics of MISO’s Transmission Owners Agreement to reach its conclusion. METC argued it should be the sole owner of the upgrades because they will be located within its larger transmission system. It also said that 33-year-old agreements bestowing partial line ownership to MPPA and Wolverine don’t extend to network upgrades on the line.

Wolverine owns 64% of the Styx-Murphy line, while MPPA owns 35% and METC owns 1%. MPPA and Wolverine acquired their ownership in 1992 through an antitrust settlement agreement to limit Consumer Energy’s market power in the Lower Peninsula. METC, meanwhile, purchased its stake from Consumers in 2020.

METC argued that the circumstances behind MPPA and Wolverine’s ownership made them ineligible for network upgrade ownership interest. It argued the two have “limited grants of ownership” on the line that permit them to transmit certain megawatt flows over METC’s larger system and nothing more.

METC also said per the MISO Transmission Owners Agreement, the line qualifies only as a “facility” and not a “system.” METC said the distinction between the phrases means it, as the owner of the larger system, is entitled to the network upgrade, not MPPA and Wolverine, which merely own a facility on its system.

The D.C. Circuit agreed that the context of Wolverine and MPPA’s rights to the line didn’t make them less worthy of owning generator interconnection-related network upgrades. The court also said a dictionary reading of “system” versus “facility” does not “demarcate as sharp a distinction … as METC would like.” It said previous FERC orders METC cited as proof “merely refer to METC’s ‘transmission system’ and the Styx-Murphy line as a ‘facility’ without reference” to specific sections of the MISO Transmission Owners Agreement.

The court said METC’s rigid interpretation would mean that MISO Transmission Owners who own a single facility would be barred from ever constructing or owning a network upgrade for a generation interconnection, which is not the case.

“It would make no sense for the other TO signatories or for MISO itself to discriminate in this manner against the owner of only one facility,” the court reasoned.

The D.C. Circuit said it agreed with the commission that METC couldn’t claim ownership of an upgrade to a line it doesn’t completely own “simply because that existing facility was located within its ‘system.’”

“That result ‘would ignore the ownership, and responsibilities, of the actual owner(s) of the existing transmission facilit(ies),’” the court said, quoting FERC. It also said it would render a portion of MISO’s Transmission Owners Agreement “meaningless.”

The court seconded FERC’s conclusion that the history behind MPPA and Wolverine’s ownership provisions wouldn’t exclude them from owning network upgrades on the line. It said the antitrust agreements conferred “unrestricted pro rata ownership in the Styx-Murphy line” which enables them “to compete on an equal footing with other TOs.”

“Limiting the agreements as METC requests … could only help entrench rather than restrain METC, an effect at odds with the pro-competitive purpose of the agreements,” the court said. It added that it could not tack on a “new prohibition” to the decades-old agreements.

METC, meanwhile, has been building the network upgrades to support Eagle Creek.

Although one aim of Western day-ahead markets in the West is to fix a fragmented transmission landscape, some islanded entities will have a tough time navigating seams issues likely to arise as markets take shape, analysts at Aurora Energy Research said during a July 1 webinar.

One of the issues discussed was the market seams likely to arise as entities enter either SPP’s Markets+ or CAISO’s Extended Day-Ahead Market (EDAM). Seams arise from the differing policies and separate dispatch between neighboring markets, resulting in additional costs for transferring energy across the boundary.

The Western Interconnection contains 38 balancing authorities serving about 82 million customers across 14 states, Canada and Mexico. Though BAs operate under an Open Access Transmission Tariff, transferring power through the footprints in the West still can be “incredibly complex given the vast geographic spread and sheer fragmentation of this transmission landscape,” said Gaurav Sen, market lead at Aurora.

“That legacy fragmentation is part of that impetus driving BAs toward Western regionalization,” Sen said.

Despite those efforts, seams will remain as BAs have signed with different day-ahead markets, creating non-contiguous footprints. Seams and wheeling costs will have a particular impact on the cost of energy in the Pacific Northwest, according to Susanna Lofvander, data analyst at Aurora.

With the Bonneville Power Administration sitting on about 22 GW of hydro resources and having the second-largest transmission mileage of any BA in the West, BPA is a crucial resource for its neighboring BAs, Lofvander noted.

“BPA has signed an implementation agreement with Markets+, and in doing so, they have islanded a couple of their neighboring balancing authorities, which have previously committed to EDAM, namely Seattle City Light and Portland General Electric,” Lofvander said. (While Seattle City Light has expressed that it heavily favors EDAM, it has not yet formally committed to the market.)

Seattle City Light and PGE are surrounded by territories that have committed to Markets+, and if the two utilities want to continue to import from BPA, they will have to pay seams costs or wheeling costs from EDAM territories, which will have an upward pressure on energy costs, according to Lofvander.

“This is particularly impactful for these two regions, as they sit on two large load centers, namely Seattle and Portland, that are expected to have significant population growth and electrification that will continue to drive load,” Lofvander said.

‘Comprehensive and Inclusive’

BPA staff has argued the agency is not solely responsible for creating seams and consistently has expressed confidence in SPP and the agency’s ability to manage energy transfers across seams based on its own history of doing so within the Northwest. This point most recently was reiterated by BPA Administrator John Hairston during a keynote at the Western Conference of Public Service Commissioners on June 2. (See Day-ahead Issues Could Take Years to Resolve, BPA Staff Says and BPA Chief to Regulators: Industry Needs ‘New Planning Paradigm’.)

“BPA completed one of the most comprehensive and inclusive public processes in the West regarding its policy direction toward Markets+,” agency spokesperson Nick Quinata told RTO Insider in an email. “BPA stands by its analysis and does not agree with the assertion that any utility is ‘islanded’ because of BPA’s policy direction. BPA will work collaboratively with all neighboring utilities to proactively address and manage any seams.”

However, the Pacific Northwest is not the only region where potential seams could cause headaches. A similar situation is expected in the Desert Southwest, specifically in Arizona and New Mexico, “where some of these territories are surrounded by other balancing authorities that are committed to the opposing day-ahead market and therefore are exposing themselves to those wheeling costs and seams costs,” Lofvander said.

City Light asked for more details about the webinar before responding to a request for comment. PGE did not respond in time for publication of this article.

Public Service Company of New Mexico has made it official: The utility signed an implementation agreement to begin participating in CAISO’s Extended Day-Ahead Market in fall 2027.

The move, which PNM announced July 1, also triggers Step 1 of the West-Wide Governance Pathways Initiative, an effort to create greater independence in the governance of CAISO’s regional markets.

Under that change, the Western Energy Markets (WEM) Governing Body now has primary decision-making authority over market rules for the Western Energy Imbalance Market (WEIM) and EDAM, rather than joint authority with CAISO’s Board of Governors.

PNM announced in November its intention to join EDAM rather than SPP’s competing day-ahead market, Markets+. One factor in the utility’s decision was its participation since 2021 in the WEIM, a real-time market that has provided PNM with nearly $170 million in benefits.

“The EDAM will integrate our state’s renewable energy potential while helping us continue to serve our customers with clean and reliable service at the lowest cost,” PNM CEO Don Tarry said in a statement.

PNM is the seventh entity to formally commit to joining EDAM. The others include PacifiCorp and Portland General Electric, which will begin participating in the market in 2026. The Los Angeles Department of Water and Power and the Balancing Authority of Northern California, which includes the Sacramento Municipal Utility District, signed agreements to join in 2027.

While PNM’s commitment to join EDAM is no surprise, it gives the CAISO market a solid foothold in a region rich with wind resources California seeks to tap to meet its ambitious clean energy goals.

“PNM’s participation strengthens the foundation of a more interconnected, reliable and cost-effective regional electricity market,” CAISO CEO Elliot Mainzer said in a statement.

BHE Montana, NV Energy, Idaho Power and Arizona G&T Cooperatives have indicated they’re leaning toward EDAM.

Step 1 Triggered

The CAISO Board of Governors and the WEM Governing Body last August approved a proposal in which Step 1 of the Pathways Initiative would be triggered when entities meeting certain size and geographic diversity criteria signed EDAM implementation agreements. (See CAISO, WEM Boards Approve Pathways ‘Step 1’ Plan.)

With PNM’s commitment to EDAM, utilities outside the CAISO balancing authority area that have signed EDAM implementation agreements represent a load equivalent to 75% of load in the CAISO balancing authority area — exceeding the 70% threshold to trigger Step 1.

And the EDAM commitments have enough geographic diversity because they include non-California entities from the Northwest and the Southwest, CAISO management said in a July 1 certification notice.

The Step 1 provisions also include a dispute resolution process. If the CAISO board and WEM Governing Body can’t agree on a particular proposal, they may file two proposals with FERC as “co-equal” options in a single document.

Another change enhances language in the WEIM and EDAM governance charter about considering the public interest.

“Independent governance of the Western Energy Markets is crucial for establishing a strong day-ahead energy market that will maximize consumer benefits,” Stacey Crowley, CAISO’s vice president of external affairs, wrote in a July 1 blog post.

Step 1 is seen as a temporary measure until Step 2 of the Pathways Initiative can be implemented.

Step 2 calls for transferring market governance to an independent “regional organization,” a move requiring changes to California law. Senate Bill 540, which would implement Step 2, was passed by the state Senate on June 4 and is now being considered in the Assembly. (See ‘Pathways’ Bill Passes California Senate on 36-0 Vote.)

‘Substantial Benefits’

PNM’s announcement of its intention to join EDAM followed the New Mexico Public Regulation Commission’s release of a set of “guiding principles” for utilities to use in selecting a day-ahead market. (See PNM Picks CAISO’s EDAM.)

“PNM continues to believe joining EDAM will offer substantial economic and operational benefits to New Mexico customers,” Kelsey Martinez, PNM’s director of regional market and transmission strategy, wrote in a June 30 filing with the PRC.

“This decision reflects a careful review of commission principles, including analysis of customer benefits, efficient resource dispatch and effective stakeholder engagement,” she added.

Martinez also noted in the filing that CAISO imposes no exit fees if an entity decides to leave EDAM. The entity may then return to WEIM-only participation or leave both the WEIM and EDAM.

Martinez said PNM would provide regular updates to the commission on its EDAM integration.

California’s first offshore wind project got a boost June 30 when FERC granted CalGrid an abandoned plant incentive for a set of OSW-related transmission projects in the Humboldt County area.

The incentive provides some financial protection to CalGrid should its proposed projects be cancelled (ER25-563).

Both are reliability projects and were approved by CAISO in May 2024 as part of CAISO’s 2023/24 transmission planning process. In May 2025, CAISO selected CalGrid’s parent company Viridon to finance, construct, own, operate and maintain both lines. (See CAISO Chooses Viridon to Develop Humboldt OSW Transmission Projects.)

Viridon California is a subsidiary of Viridon Holdings, a portfolio company of Blackstone.

The first project, the NH-C project, includes about 200 miles of new 500-kV transmission line, which will connect a new substation in Humboldt to a new substation in Collinsville. The second, the NH-F project, includes about 100 miles of new 500-kV transmission line from the new substation in Humboldt to a substation on Fern Road in Shasta County.

“The projects face risks beyond CalGrid’s control that could lead to the projects’ abandonment,” the commission wrote in the order. “We find that CalGrid has demonstrated a nexus between its requested incentive and its planned investment, and that CalGrid has tailored its incentive rate request to its identification of risks and challenges associated with the projects.”

The abandoned plant incentive would be available to CalGrid for 100% of prudently incurred costs expended on and after the date of the order if the projects were abandoned for reasons beyond CalGrid’s control, FERC wrote.

The projects face significant risks that “could result in their cancellation,” CalGrid said in its filing. Those include regulatory approval uncertainties and CalGrid’s lack of building experience — i.e., the projects will be the first transmission lines that CalGrid has built.

The abandoned plant incentive will help CalGrid attract financing “by removing the risk that lenders and investors may have to bear prudently incurred costs if the projects are canceled for reasons outside of CalGrid’s control,” the order says.

The projects will cost up to $4.1 billion and are expected to be completed by 2034.

In 2006, FERC issued Order No. 679, which allows applicants to request incentive rate treatment for transmission infrastructure investments that ensure reliability or reduce the cost of delivered power by reducing transmission congestion. CalGrid said the Humboldt projects meet this requirement because they were approved as part of CAISO’s regional planning process. CalGrid also said the projects are beneficial to ratepayers and promote FERC’s pro-competitive policies.

In the order, FERC Chair Mark Christie dissented “for reasons consistent with my previous statements on the subject.” In a May 13 order, Christie said, “As I have said repeatedly over the past four years, it is long past time for this commission to do its job of protecting consumers by cutting back on its unfair practice of handing out ‘FERC candy’ without any serious consideration of the impact on consumers already struggling to pay monthly power bills.”

FERC on June 30 changed its regulations implementing the National Environmental Policy Act (NEPA) in compliance with President Donald Trump’s Executive Order 14154, “Unleashing American Energy” (RM25-11).

Trump ordered the Council on Environmental Quality to rescind its regulations implementing NEPA; FERC’s action eliminates references in its own rules to those now-defunct regulations.

“We will continue to ensure our environmental reviews are legally durable so projects stand up in court and get built,” FERC Chair Mark Christie said in a statement. “Thanks to the leadership of President Trump, our new staff guidance on NEPA will inform all interested parties on our process and should be a useful tool in making the permitting process more efficient and transparent.”

Enacted in 1970, NEPA established the CEQ and required all federal agencies, including FERC, to craft environmental assessments (EA) and environmental impact statements (EIS) that evaluate their actions’ effects on the environment. Trump’s Day 1 executive order repealed one issued by President Jimmy Carter in 1977, Executive Order 11991, which made CEQ the lead agency to develop the process agencies should follow to comply with NEPA and to manage conflicts between agencies over their responsibilities.

The CEQ’s authority to write regulations was rescinded in November 2024 by the D.C. Circuit Court of Appeals, which found NEPA did not provide it. In his order, Trump directed the CEQ to instead provide guidance on how each agency should update their environmental review processes.

The details on how FERC’s process will change are laid out in a manual prepared by its staff. The manual includes details on how staff will determine what actions are subject to NEPA’s requirements and the level of review required by the law. It describes how staff will “ensure that relevant environmental information is identified and considered early in the process in order to support informed decision-making” and “conduct coordinated, consistent, predictable and timely environmental reviews while cutting unneeded burdens and delays.”

The manual spends several pages describing exclusions from the NEPA process and then explains that if a project is found to have a foreseeable effect on the quality of the human environment, staff will craft an EA. The text of the assessments is not to exceed 75 pages (not including citations or appendices with data such as scientific tables or statistical calculations).

Staff will have a year to prepare the assessment, with the deadline starting when hydropower projects are issued a Notice of Intent to Prepare an Environmental Assessment, or when natural gas projects get issued a Notice of Schedule. The assessment will determine whether an EIS, which is required when a project’s environmental impacts cannot be mitigated, is needed.

The EIS process will include the chance for other interested parties to make comments on the proposed infrastructure and any NEPA mitigations required. Each EIS is to be limited to 150 pages of main text, with actions of “extraordinary complexity” getting up to 300 pages.

The deadline for an EIS will be two years, but staff can get extensions if that schedule is not possible to meet.

New England’s offshore wind ambitions were dealt a further setback as contract negotiations under way for most of the past year were extended again, potentially into 2026.

The reason is not difficult to guess: A June 30 filing (Massachusetts DPU 23-42) cites uncertainty created by substantial changes in federal energy policy since President Trump was inaugurated.

The parties now are targeting completion of negotiations on or before Dec. 31, 2025, and filing of contracts with state regulators on or before Feb. 25, 2026.

The joint offshore wind solicitation by Connecticut, Massachusetts and Rhode Island was an ambitious attempt to rebound from setbacks and frustrations each state had experienced individually as the industry ran into headwinds in its efforts to establish itself in the United States.

Vineyard Offshore then withdrew its bid for the 1,200-MW Vineyard Wind 2 proposal because Massachusetts would take only 800 MW of output and Connecticut would not take the other 400 MW. (See Connecticut Closes the Door on 2024 OSW Procurement.)

That left 791 MW from Avangrid’s New England Wind 1 proposal and 1,087 MW from the EDP Renewables/Engie joint venture SouthCoast Wind. The SouthCoast partners said in February that project could be placed on hold for as long as four years due to its uncertain prospects during the Trump administration. (See SouthCoast Wind to Take $278M Impairment as Delay Appears Likely.)

Rhode Island Energy is warning that it may terminate its conditional selection of 200 MW from SouthCoast if the negotiations are not successful by Oct. 31, 2025.

Meanwhile, two offshore wind projects serving New England are under construction: Vineyard Wind 1, which will feed 800 MW to Massachusetts, and Revolution Wind, which will send 300 MW to Connecticut and 400 MW to Rhode Island.

Both have had problems of their own: Ørsted has reported good progress in Revolution’s offshore construction, albeit at a higher cost than initially expected, but complications on land have pushed back its projected commercial operation date. (See Ørsted Takes $1.7B Impairment on US Offshore Wind.)

Avangrid and Ørsted did not respond to requests for comment for this report.

The three southern New England states have had high hopes for offshore wind as a way of providing clean, affordable electricity while creating a new economic sector. After a series of contract cancellations, they banded together for the solicitation that now has stalled.

Their neighbors down the coast also have struggled with cancellations and failed solicitations.

In February 2025, New Jersey called off its latest solicitation midprocess after two developers withdrew proposals. (See N.J. Abandons 4th OSW Solicitation.)

In April 2024, New York had to cancel its 2022 solicitation after 20 months of work due to turbines not being available. (See N.Y. Offshore Wind Plans Implode Again.)

New York expected to announce contracts in the first quarter of this year for its 2024 solicitation but still has not done so as the third quarter begins. One of the four developers that offered proposals withdrew them a month after submitting them. Another has paused U.S. offshore wind development indefinitely. A third saw the federal review process halt for the project it proposed.

The transition from the strongly pro-renewables President Biden to the strongly pro-fossil and anti-renewables President Trump significantly boosted the risk and uncertainty facing U.S. offshore wind generation development.

As NetZero Insider reported before Trump’s inauguration, the president did not need to deliver a huge knockout punch against offshore wind to fulfill his campaign promise of halting it. All he had to do was magnify the existing levels of uncertainty and risk — the industry could then wither on its own, as investors withheld capital. (See Offshore Wind Industry Girds for 2025, Trump Presidency.)

Trump’s Day One order of a review of wind power permitting — along with his unpredictable leadership style and his tariff threats — has accomplished this. The impact was such that in May, 17 states and the District of Columbia filed a federal complaint (1:25-cv-11221) against Trump and key federal officials challenging the order.

In its motion to intervene in the case, trade organization Alliance for Clean Energy New York said billions of dollars of investments and hundreds of thousands of jobs are at risk through the delaying effect of the Day One memorandum, given the great number of federal approvals needed for projects and their vulnerability to unexpected delays.

“Due to the uncertainty as to when federal permitting will resume, investment in new projects has halted, and developers are not setting new construction timelines or entering into new construction or manufacturing contracts,” ACE NY wrote. “Demand for specialized materials, equipment and labor has plummeted.”

A few bright spots remain in the U.S. offshore sector.

The Department of the Interior removed the stop-work order it had slapped on Empire Wind 1, an 810-MW Equinor project beginning work off the New York coast. (See BOEM Lifts Stop-work Order on Empire Wind.)

A spokesperson said June 30 that 108 of 176 foundations, 59 of 176 transition pieces and the first offshore substation have been installed; nearly 75% of deepwater export cables are in place; and the first turbine components have arrived at Portsmouth Marine Terminal, where they will be assembled later in 2025.

The U.S. Senate met through the weekend and overnight June 30 to work on Republicans’ budget reconciliation bill, passing it 51-50 with Vice President JD Vance casting the tiebreaking vote around noon July 1.

The One Big Beautiful Bill Act includes most of the Trump administration’s legislative priorities, such as earlier phaseouts of clean energy tax credits. The Senate took out some of the most heavily criticized aspects, including a tax on the production of solar and wind power that was introduced over the weekend. (See Renewables Supporters Decry Late Change to Trump’s ‘Big Beautiful Bill’.)

President Donald Trump welcomed the Senate vote in a post on Truth Social, saying it will lower taxes, raise wages, secure the country’s borders and lead to a stronger military.

But American Clean Power Association CEO Jason Grumet said in a statement that “the Senate reconciliation package is a step backward for American energy policy. The intentional effort to undermine the fastest-growing sources of electric power will lead to increased energy bills, decreased grid reliability and the loss of hundreds of thousands of jobs.”

Grumet noted, however, that it could have been worse. The 12-month phaseout of the tax incentives is aggressive, but the final bill did not include the production tax.

“We appreciate the members of Congress who worked to get this legislation to a better place,” Grumet said. “Their efforts reinforce the basic principle that Congress should not bet against progress in any part of our economy.”

The House of Representatives is expected to quickly take up the Senate version of the bill, having already passed another version with different language on energy tax credits. The House Rules Committee met hours after the Senate passed the bill, clearing the way for it to reach the floor and possibly meet Trump’s personal deadline of getting the bill fully passed by July 4.

ClearPath Action, a conservative group that supports addressing climate change, argued that the bill keeps in place enough tools for industry to move forward on the next generation of clean energy technologies.

“The private sector needs all tools available, including tax credits and faster permitting, to meet the goals of increasing reliable electricity and lowering costs in an era of rising demand,” ClearPath CEO Jeremy Harrell said in a statement. “The reconciliation process started with calls from some to fully repeal all energy tax incentives, which would have devastated the ability to build new clean energy. Senate Republicans and House allies rejected that approach and preserved some financial tools to accelerate American innovation and invest in American manufacturing. We encourage House Republicans to swiftly pass this bill with the key energy provisions included.”

The Senate bill keeps incentives for advanced nuclear, geothermal, hydropower and storage through 2032, while wind and solar credits would be phased out in 2027. It preserves the transferability provisions for the life of each energy credit and retains the 45X advanced manufacturing incentive to support domestic production of critical minerals and certain energy components. It also provides new financing authority for the Department of Energy’s Loan Programs Office to support nuclear, geothermal and energy supply chains.

The Natural Resources Defense Council said the bill cuts tax credits for the fastest-growing source of new generation and is expected to lead to higher power bills around the country.

“With spiking power demand and rising bills, we need more clean, affordable American energy, but Senate Republicans just voted to kill jobs and deliver the largest utility bill increase in U.S. history,” NRDC CEO Manish Bapna said in a statement. “This measure props up the dirty and expensive technologies of the past while strangling the clean energy investments that are creating millions of jobs across the country. At a time when we need new energy more than ever, Republicans are punishing the plentiful wind and solar power that can be quickly added to the grid.”

{kind=link}