One of the first items the yet-to-be-seated board of the Regional Organization for Western Energy could decide on is whether to administer a resource adequacy program, as backers seek to have a proposal in place later in 2026.

Members of ROWE’s temporary Formation Board discussed the potential of a new RA program at a March 19 meeting.

The discussion comes after non-CAISO participants in the ISO’s Extended Day-Ahead Market announced they are designing a new RA program, with the hope that the ROWE — the independent body established by the West-Wide Governance Pathways to oversee CAISO’s EDAM and Western Energy Imbalance Market — would govern it. (See EDAM Utilities Moving to Develop RA Program.)

Jim Shetler, ROWE Formation Board member and general manager of the Balancing Authority of Northern California (BANC), said the EDAM entities — of which BANC is one — are working on the details of the RA program and aim to have draft proposal by the end of April.

“The concept here is that we would be requesting [ROWE] to administer this service on behalf of the participants,” Shetler said.

He noted the RA program would “in no way” impact the California Public Utilities Commission’s separate RA program.

ROWE has yet to seat a permanent board and is slated to do so later in 2026, at which point that body would decide whether to administer the RA program.

Because ROWE does not yet have a formal stakeholder process, the EDAM entities are proposing to continue developing the RA program through the summer, according to Shetler.

The goal is to have the revised proposal in front of the seated ROWE board later in the year, he added.

“We recognize right up front that the ROWE board will have to make the decision as to whether it, number one: wants to take on this service or not,” Shetler said. “And we also recognize that, and expect that, the ROWE board, if they decide to do so, would want to conduct additional stakeholder processes as appropriate.”

However, because of the time constraints EDAM entities are facing, “we do need to get to at least an initial decision on whether this is a viable outfit or not by this fall,” Shetler said.

Participants in the RA project are PacifiCorp, Portland General Electric, Public Service Company of New Mexico, Los Angeles Department of Water and Power, NV Energy, the Turlock Irrigation District and BANC. (See Alternative Western RA Program Starts to Take Shape.)

The new resource adequacy program is seen as an alternative to Western Power Pool’s Western Resource Adequacy Program (WRAP).

Participants in the day-ahead market competing with EDAM — SPP’s Markets+ — will be required to join WRAP. EDAM members also may join WRAP, but some expected EDAM participants expressed concerns about the program and decided to withdraw. (See PacifiCorp Next to Leave WRAP After Raising Concerns.)

Shetler said the EDAM entities are looking to take advantage of existing ROWE and Pathways contracts to facilitate stakeholder processes and “try to leverage and take advantage of that expertise.”

“With respect to funding, we are not asking that the ROWE make use of any of your existing funds that have been contributed for the development of the ROWE,” Shetler said. “The EDAM sector is prepared to contribute separately for the support of the facilitator in helping us with this effort.”

Kathleen Staks, ROWE interim president, said while ROWE itself is still in its nascent stages, “it is exciting that we’re in a position where we’re already seeing an interest in developing those additional market services under an independent governance.”

Brian Turner, senior director at Advanced Energy United, said he was “excited” about the proposal.

“I recognize and understand the significant need that it’s serving within non-CAISO Western EDAM entities to have a unified resource adequacy accounting and perhaps trading sharing mechanism,” Turner said, adding the program would add “substantial resources to those non-CAISO entities.”

MISO announced it will reassign multimillion-dollar substation work in Wisconsin to American Transmission Co. in order to meet a sped-up construction timeline for data center load.

The grid operator decided to pull Chicago-based developer Viridon Midcontinent from a portion of the Wisconsin Southeast (WISE) project, which consists of 106 miles of 345-kV lines and four 345-kV substations valued at $350 million.

The WISE project is a subset of the South Fond du Lac-Rockdale-Big Bend-Sugar Creek-Kitty Hawk Long-Range Transmission Project in southeastern Wisconsin, one of the projects approved as part of MISO’s $22 billion long-range portfolio at the end of 2024.

MISO opened a variance analysis on the project at the end of February because it said its selected developer, Viridon, “is unlikely to attain the regulatory requirements in Wisconsin” in time to build three of the substations on an accelerated timeline. The substations are needed by the end of 2027 for new data center load that ATC is handling. The RTO originally expected the project to be in service in mid-2033. (See MISO Opens 3rd Tx Project Review as Data Center Plans Conflict with Long-range Tx Timeline.)

Enter ATC’s Ozaukee County Distribution Project, which is at the heart of the controversy. ATC proposed the project — which involves rebuilding and upgrading existing 345-kV lines and constructing up to five new substations at a cost of $1.36 billion to $1.64 billion — in September 2025 on an expedited basis to meet anticipated data center load. The Ozaukee project relies on three of the substations in the WISE project.

MISO conducts variance analyses on regionally cost-shared transmission projects when they encounter schedule delays, permitting challenges or substantial design changes or experience at least a 25% cost increase from original estimates. The studies also are triggered when developers find themselves unable to complete the project or if they default on the terms of their selected developer agreement.

After an analysis, MISO can either let projects stand, develop a mitigation plan for them, cancel them or assign them to different developers, if possible. A committee of RTO employees selected by leadership determines projects’ fates.

In this case, MISO’s Competitive Transmission Executive Committee (CTEC) investigated the situation brought on by the accelerated in-service date and “determined that Viridon is unlikely to satisfy the Wisconsin regulatory requirements in order” to finish the substations by Dec. 1, 2027. The committee said ATC was a better fit for the project in light of the expedited data center needs.

According to MISO’s tariff, the committee has “exclusive and final authority” over variance analysis outcomes.

“CTEC determined that incumbent transmission owner and authorized Wisconsin public utility ATC is better positioned to attain the necessary regulatory approvals in Wisconsin and achieve the accelerated in-service date,” MISO said in its public determination. “As such, CTEC has determined that the most suitable outcome to meet the accelerated-service date is to reassign these facilities to ATC as reassignment will most likely result in the successful completion of, or increase the ability to complete, the facilities and will alleviate the ground for variance analysis.”

MISO said the remainder of the WISE project — a substation and the 345-kV line work — will “continue to be constructed, implemented, owned and operated by Viridon.”

Viridon was founded in 2023 and is owned by Blackstone Energy Transition Partners, one of Blackstone’s private equity funds.

MISO said it considered other outcomes beyond reassignment of the trio of substations. It said it eliminated a “no action” outcome because of the urgency of the new data center load and that a mitigation plan was impractical because it’s unrealistic to expect Viridon to clear the necessary regulatory approvals on an expedited or prioritized basis from the Wisconsin Public Service Commission.

The RTO also said project cancellation was out of the question because of the footprint’s dependency on the long-range transmission portfolio, in addition to the anticipated data center load relying on the construction.

MISO said it will coordinate and execute the necessary documents with Viridon and ATC “in due time” to reassign the substation portion of the project.

Viridon said it accepted MISO’s decision.

“We are confident in our ability to have executed successfully on the accelerated timeline for the substations. That said, we respect MISO’s decision. We look forward to completing the remainder of the WISE project on time and on budget, including the Big Bend substation and the 345-kV transmission lines,” Viridon said in a statement to RTO Insider.

MISO has completed 11 variance analyses to date. Until now, it has never reassigned a project developer, despite having the authority to do so. The RTO historically has chosen either to create mitigation plans with the existing developer or to allow the project to stand. In one instance, MISO canceled a 500-kV project because of a new right-of-first-refusal law in Texas. (See FERC Rejects Last-ditch Effort to Save Tx Project.)

ATC said it is “pleased with the outcome of MISO’s variance analysis.”

“Our focus remains on maintaining a safe, reliable grid, and meeting our customers’ needs,” ATC said in a statement. ATC said it would roll the substations into its application for a certificate of public convenience and necessity for the Ozaukee County project. The company said it plans to have the substations “in service by the date needed to serve the load.”

ATC did not answer RTO Insider’s question on whether it was involved in the variance analysis process.

ATC is among a group of Midwestern utilities rumored to be asking FERC and the Trump administration to suspend competitive bidding so the grid can be built out faster to accommodate the data center explosion. The company, along with Xcel Energy, ITC Holdings and Ameren, have reportedly taken their request to the White House’s National Energy Dominance Council.

MISO Issues Mitigation Plan for Other Long-term Tx Project

Relatedly, MISO rounded out a second variance analysis it conducted on the 345-kV Morrison Ditch-Reynolds-Burr Oak-Leesburg-Hiple line in Illinois and Indiana, which jumped from an estimated $261 million to a $675 million cost estimate in 2024. The project was approved in 2022 under MISO’s first long-range transmission plan portfolio.

MISO said it was able to work with developer Northern Indiana Public Service Co. on a mitigation plan that should reduce the cost of the long-range transmission project to $477.8 million.

After its variance analysis investigation, MISO said it “observed higher estimated costs for construction matting, technical services and contingency, as well as additional costs associated with securing and permitting the transmission line right of way.”

NIPSCO leadership and MISO were able to identify “cost savings and efficiencies” that would lower estimated project cost through adjustments to the scope of work, reductions in construction costs “as discrete contracts are executed and reductions in contingency costs as the project was further developed with fewer unknowns,” according to the RTO.

Again, MISO said it considered all possible outcomes under the variance analysis. It deemed no action unacceptable because of the sheer size of the cost increase. It said it could not reassign the project because of Indiana’s ROFR law, which rendered the facilities ineligible for competitive bidding.

Finally, MISO once again said cancellation was not a realistic option because of the interconnectedness of the Morrison Ditch project with the rest of the long-range transmission portfolio.

MISO said once it and NIPSCO sign the mitigation plan, it will reflect the new estimated cost in its database of transmission project status reports.

Challenges are piling up to Trump administration orders to keep retiring coal plants online, as the Colorado attorney general and environmental groups have filed petitions to overturn an extension of Craig Station Unit 1.

The petitions for review were filed March 18 in the D.C. Circuit Court of Appeals: one by Colorado Attorney General Phil Weiser and a second by Sierra Club, Environmental Defense Fund and Earthjustice on behalf of Vote Solar.

Craig Station Unit 1, in Moffat County, Colo., had been scheduled to retire on Dec. 31, 2025. On Dec. 30, the U.S. Department of Energy issued an order to keep the unit available for operation for 90 days, saying the extension was needed “to prevent blackouts.” (See DOE Blocks Retirement of Another Coal-fired Plant.)

The DOE order was issued under Section 202(c) of the Federal Power Act, saying emergency conditions existed due to increasing demand and shortages from the accelerated retirement of generating facilities.

Weiser disputed the DOE’s assertion that there was an energy emergency.

“The long-anticipated retirement of Craig Unit 1 and replacing it with cleaner and more affordable energy resources was the result of a carefully planned process that was driven by economics,” Weiser said in a statement.

Craig Unit 1 wasn’t operational at the time of the DOE order due to a failed valve. Tri-State Generation and Transmission Association, which is the operator and a co-owner of the unit, made the needed repairs. The unit was available to operate by Jan. 20. While complying with the order, Tri-State has said it’s worried about the costs to its members.

A Tri-State spokesperson said March 19 that Craig Unit 1 had not been called upon to run since the DOE order was issued.

“Tri-State continues to evaluate our options moving forward,” the spokesperson said.

On Jan. 29, Tri-State and Unit 1 co-owner Platte River Power Authority petitioned the DOE for a rehearing on the order. Weiser’s office and environmental groups filed their own petitions for rehearing. (See Fight Heats up over Colorado’s Craig Coal Plant Extension.)

The requests for rehearing were denied, opening the door for the parties to file petitions with the federal appeals court.

Ted Kelly, director and lead counsel for U.S. clean energy at the Environmental Defense Fund, called the Craig unit “extremely costly, highly polluting and unreliable.”

“Forcing this coal unit to stay online needlessly jacks up electricity bills and toxic pollution,” Kelly said in a statement.

Other Coal Plant Petitions

The DOE has issued similar orders to extend the life of retiring coal plants in Michigan, Indiana, Washington and Pennsylvania. Those orders in most cases have led to petitions for review in federal appeals courts.

Earlier in March, the Washington state attorney general and environmental groups filed separate lawsuits in the 9th U.S. Circuit Court of Appeals to overturn a DOE order requiring TransAlta to keep running the Centralia coal-fired plant past its scheduled retirement. (See Wash. AG, PIOs Sue to Overturn DOE Order to Keep Centralia Plant Running.)

On March 16, environmental groups filed a petition at the D.C. Circuit to overturn DOE emergency orders to force two coal-fired power plants in Indiana to continue operating past their scheduled retirement dates. In December 2025, the DOE halted the planned retirement of the last coal units at the R.M. Schahfer power plant and one of the coal units at the F.B. Culley generating station. (See Groups Contest Indiana Coal Plants’ Emergency Extensions at D.C. Circuit.)

The challenge came from the Sierra Club, the Environmental Law and Policy Center, and Earthjustice, representing Citizens Action Coalition of Indiana, Just Transition Northwest Indiana and Hoosier Environmental Council.

On Dec. 19, 2025, environmental groups led by the Sierra Club and Earthjustice filed a brief at the D.C. Circuit to overturn DOE orders extending the life of the J.H. Campbell coal plant in Michigan. The order was issued in May 2025 and has been extended every three months since then.

In its first substantive brief in the case, filed March 17, the DOE defended its Campbell order, saying its use of Section 202(c) is well within its authority in response to an ongoing emergency on the grid. (See DOE Defends Use of Emergency Orders in Court Filing.)

Alpha Generation, owner and operator of the Gowanus and Narrows floating power plants in New York City, has proposed replacing the six peaking units with three lower-emitting ones in response to Consolidated Edison’s solicitation for solutions to the city’s reliability need.

The Gowanus and Narrows plants in Brooklyn have been slated for retirement since the state instituted an emissions standard for peaking plants, but the dates have been repeatedly pushed back, as NYISO has said they are needed for reliability. The plants are currently slated for retirement May 1, 2027, but AlphaGen said it expects the ISO to once again determine they are needed for reliability and extend their operation for an additional two years.

“Given tightening resource adequacy margins and uncertainty around the timing of replacement resources capable of delivering equivalent reliability services, AlphaGen anticipates these units will likely be needed even longer,” the company said in a news release. The proposed new units would each deliver 273 MW of fast-start, dispatchable power and produce 50% fewer emissions compared to the existing units.

“Repowering recognizes the realities of current power technology and the need to balance reliability with sustainability,” AlphaGen CEO Curt Morgan said in a statement. “It is not intended to be an affront to the [state’s emission-reductions goals] or the commission-initiated RFI process, which seeks non-emitting solutions, but to start a conversation about supporting cleaner technology as a bridge to a zero-emissions future.”

The proposal also includes the development of a 150-MW/600-MWh battery storage facility at Gowanus, as well as two batteries at the Astoria plant in Queens totaling 126 MW/504 MWh.

“Battery energy storage systems are a critical complement to the repowering projects,” the company said. “While the repowered barges provide fast-start, dual-fuel, dispatchable capacity for extended-duration events, batteries offer near-instantaneous response to short-term fluctuations in demand and frequency.”

But Elizabeth Yeampierre, executive director of Brooklyn-based environmental justice group UPROSE, told RTO Insider that AlphaGen’s proposal was to “justify the continued toxic exposure of Sunset Park under the language of reliability.”

“There is nothing ‘forward-looking’ about doubling down on false solutions,” Yeampierre said. “This is not a bridge — it is a misleading dilatory tactic that undermines the health of our children and elders.”

The case is a microcosm of the fight over energy priorities in New York. Gov. Kathy Hochul has signaled she is open to amending the state’s climate law but hasn’t explained what that would entail, according to New York Focus. In December 2025, the Hochul administration approved a new State Energy Plan embracing an “all of the above” approach to energy policy. (See N.Y. Embraces All of the Above in Energy Strategy Update.)

Hochul’s office declined to comment. Con Ed did not reply to requests for comment.

FERC approved changes to its rules regarding filing “electric quarterly reports” (EQRs) at its regular meeting with the issuance of Order 917.

The changes include updates to how EQRs must be formatted, clarifications of reporting requirements, and a new requirement for ISO/RTOs to produce reports containing market participant transaction data, according to the order issued March 19.

“The commission adopted the EQR as the reporting mechanism for public utilities to fulfill their responsibility under FPA Section 205(c) to have information relating to their rates, terms and conditions of service available for public inspection in a convenient form and place,” FERC said in the order. “The commission established the EQR in 2002 with the issuance of Order No. 2001.”

The changes are meant to update and streamline data collection, improve data quality and increase market transparency. They are expected to cut costs of preparing the needed data and complying with future changes to EQR requirements.

The new rules adopt a single method for EQR reports based on the “XBRL-CSV standard,” which would preserve the efficiency and simplicity of the existing CSV model while adding the flexibility of the XBRL standard. XBRL is a business information standards group. CSV refers to “comma separated values,” a text file used to store tabular data. FERC said adopting the standard would make the process more efficient.

The due date for EQRs was extended to four months after the relevant quarter ends, rather than requiring them to come in after a month.

ISO/RTOs have a new requirement to prepare and make available transaction data reports to their market participants based on the settlement data generated by the organized markets for sales made by market participants within them. The requirement will help sellers prepare to submit transaction data in the EQR and will cut the amount of manual data manipulation prior to submission.

Market sellers in ISO/RTOs still will have to submit their own EQRs and will be responsible for ensuring the accuracy of its EQR data.

The ISO/RTO reports will reflect sellers’ transactions within the relevant market in which the operator is a counterparty. Those ISO/RTO reports will be due by the end of the following quarter.

The data in the ISO/RTO reports should correspond with the markets’ clearing, dispatch and settlements, which generally is in 5-minute increments. One party suggested combining that 5-minute data into hourly data, but FERC said that might hinder its ability to protect customers from unjust and unreasonable rates and reduce transparency into market pricing.

Leading data companies met with the Trump administration recently and signed a Ratepayer Protection Pledge, in which “companies agree to protect American consumers from price hikes due to data center energy and infrastructure requirements, and lower electricity costs for consumers in the long term.”

The White House website declared that “President Trump is calling on the leading United States hyperscalers and AI companies to build, bring, or buy all of the energy needed for building and operating data centers, paying the full cost of their energy and infrastructure, no matter what” to protect other ratepayers.

The five elements of the non-binding pledge committed the companies to:

Pay the full cost of associated supply resources.

Pay for all new required power delivery infrastructure upgrades.

Pay for power assets and supply infrastructure whether or not they consume power.

Invest in the local communities hosting data centers.

Coordinate with grid operators to contribute to a more reliable grid and, when possible, deploy backup generation to shore up the grid during scarcities.

That Horse Got Out of the Barn Some Time Ago

The meeting and associated pledge were perhaps good theater but would have been more valuable a year or two ago. That’s when interconnection requests already were flooding the energy landscape and utilities were negotiating the first tariffs addressing large loads. AEP Ohio started that parade in May 2024, when it requested the Public Utilities Commission of Ohio to bless a proposal that would “enhance financial obligations that data centers must undertake to support infrastructure that serves them.”

Peter Kelly-Detwiler

Perhaps unsurprisingly, the data center crowd strongly opposed the proposed tariff approach, with data companies and some generators offeringa counterproposalthat largely was rejected. Ultimately, a tariff was approved that required new large data loads to pay for 85% of forecast capacity in a take-or-pay approach meant to cover the cost of associated infrastructure.

The tariff included a four-year ramp construction period and eight years of full service, as well as exit fees and a requirement for proof of financial viability. The data centers ultimately acceded to the terms, and as of February, AEP reported 5,642 MW of contracts had been signed under the Data Center Tariff.

Once that regulatory model was approved, utilities elsewhere recognized they had leverage. The construct spread to other markets and later contracts showed even more teeth. AEP, for example, recently highlighted approved tariffs in four of its U.S. service territories, with some including 20-year contract periods and take-or-pay provisions as high as 90% of total demand. It has another four such tariffs awaiting regulatory approval.

Other utilities pushed similar approaches. For example, in Michigan, DTE Energyinstituted a 19-year contract for a 1,383-MW data center that includes an 80% take-or-pay provision and a termination period of up to 10 years, and Consumers Energy received approval in December for a large load tariff that includes a minimum length of 15 years and a take-or-pay provision at 80% of forecasted demand.

Evergy and Ameren in Missouri recently received approval for a 17-year large load contract with collateral requirements, 80% take-or-pay requirements, and exit fees meant “to ensure large load customers contribute their fair share of costs and minimize risk to other customers.”

The White House pledge requiring coordination with grid operators also is being independently addressed in multiple jurisdictions, including Texas, with Senate Bill 6 including a so-called “kill switch” to ensure ERCOT can cut data loads during grid emergencies.

Meanwhile, PJM is exploring a parallel capacity auction (with administration support), while its board has proposed a series of decisions related to connecting new data center load. Utilities, state regulators and grid operators across the country are keenly focused on these issues. Pledge or no pledge, they eventually will get these issues sorted out because they must.

Too Much Demand Chasing Too Few Goods

That fact does not mean ratepayers are not at risk from this massive wave of data center development. There’s the simple inflationary dynamic resulting from demand for infrastructure (and related labor) outstripping supply.

Even non-grid-connected data centers will affect ratepayers, just indirectly. One cannot have tens of gigawatts of new demand for turbines, transformers, switchgear and natural gas mushroom up out of nowhere and expect prices to remain flat. They won’t, so it’s best to forget that fiction.

Time Frame Mismatches, Consolidation, and Technological Risks

There are other risks as well, including the stranded asset risk. Even if data companies pay their way for the length of an initial contract, cost recovery for many utility assets exceeds 30 years, so there is considerable risk down the road in the out-years if long-term demand does not stabilize or grow.

More immediately, there also is the risk that business models will change, or that the industry will see considerable consolidation among all of the players fighting for supremacy in the large language model (LLM) AI landscape. Each LLM developer is playing to win in a very high-stakes game, and it’s likely not all will succeed.

Bankruptcies or buyouts could lead to billions of dollars in stranded assets. If the “dark fiber debacle” of the 1990s — where tens of billions of dollars were spent on an overbuild of the fiber optic network that took more than a decade to eventually grow into — taught us anything, then we should know to be cautious.

We also saw a similar dynamic play out in the search engine space over two decades ago, with few winners and numerous losers. And if you are skeptical of that assertion, you would do well to go Ask Jeeves.

There’s also the uncertainty of a constantly evolving technology. Chips continue to change, cooling systems evolve and approaches change. AI has only been around since ChatGPT 3.5 popped out of the box in November 2022, kicking off an AI arms race that has accelerated so quickly nobody knows where it’s going.

Leading chipmaker Nvidia’s GTC conference in March is an indicator of just how fast this is evolving. CEO Jensen Huang’s keynote indicated the company’s hardware and software are being developed specifically with energy efficiency in mind. Depending on the task, new hardware could yield efficiency improvements of between two and 35 times per watt. Advanced software further accelerates some of these gains.

The approach to developing the AI models also may be changing. In this country, the approach to training LLMs that “learn to think” like humans typically involves throwing a combination of chips, raw data and massive amounts of power into the mix in a “brute force scaling” approach. But that ultimately may not prove to be the best avenue in the future.

Other approaches may be worthy of consideration, as DeepSeek (out of China) demonstrated, relying on better algorithms to achieve its outcomes. Baidu’s ERNIE X1 (also China) built further on this approach to reasoning and claims to offer similar performance at a more attractive cost.

U.S. labs appear to be adapting to take advantage of some of the lessons learned, adopting open-source algorithms used originally by Chinese competitors (though brute force still matters today — especially for processing huge amounts of video and data).

Dark Horses

Then there are other uncertainties that may either become historical footnotes or significantly change the industry’s trajectory. To take one example, Yann LeCun, the high-profile AI researcher who once was Meta’s chief AI scientist, recently raised $1.03 billion for his Advanced Machine Intelligence Labs.

The company is predicated on a bet that LLMs ultimately won’t prove to be the winning approach to creating intelligent systems. Rather than relying on text-based models to achieve human-type reasoning, LeCun’s team will develop models trained in visual and spatial data. If they are proven right, a lot of capital may have been allocated in the wrong direction, with investments in supporting energy systems at risk.

There is also the emerging use of photonics — the use of light, rather than electrons, to process and transmit data. Light dramatically reduces the heat produced by chips because one no longer is driving electrons through tiny copper wires or silicon transistors.

Photonics can eliminate the need to constantly turn transistors on and off, an action which requires energy with each cycle. Finally, photonics can beat today’s approach of using copper wire to send signals, one at a time. Using light, one can send multiple signals using the various inherent wavelengths and reduce the energy required.

Photonics is not fully developed or commercialized yet, but leading chipmaker Nvidia already is using “co-packaged optics,” in which optical transceivers are located next to electronic switching chips in AI data centers. This use of light cuts networking power consumption by up to five time.

There is a great deal of optimism around the technology, with significant investment pouring into the field. In July 2025, German researchers demonstrated the world’s first photonic processor for high-performance and AI computing. It’s too early to tell whether the technology will hit the mainstream anytime soon. The point here is simply that computing technology — aided by advances made within AI itself — will continue to evolve.

A Pledge Offers Only Limited Protection

Looking across the landscape at this very early stage of a rapidly developing AI industry, uncertainty exists on multiple levels. As a consequence, White House pledges and data company commitments to protect other ratepayers may be of some limited benefit. But they protect us rate-paying pawns only for the first few limited moves in a vast multitrillion-dollar global game of high-stakes chess whose outcome is uncertain, bringing both potential promise and peril to the grid of tomorrow.

A new study quantifies some of the benefits that could come from more fully using the existing capacity of the grid before expanding it to meet demand growth from data centers and other large loads.

The report released March 19 is based on a central characteristic of the U.S. grid and some converging factors surrounding it:

It is sized to handle peak loads, so only about half its capacity is used on average through the year. Significant new load is anticipated at a time when electricity rates already are soaring and there are concerns that expanding and modernizing the grid to serve the new load will be painfully expensive.

But some of the demand can be met with grid management or peak shifting — and the technology that would enable this has begun to mature and scale.

“We’ve heard a lot about affordability of electricity in the last year,” Utilize Executive Director Ian Magruder said during a March 18 presentation on the Brattle study. “There are a lot of solutions being proposed. But our view is that this solution of grid utilization is one of the only near-term solutions that can meaningfully reduce the cost of electricity at scale in short order.”

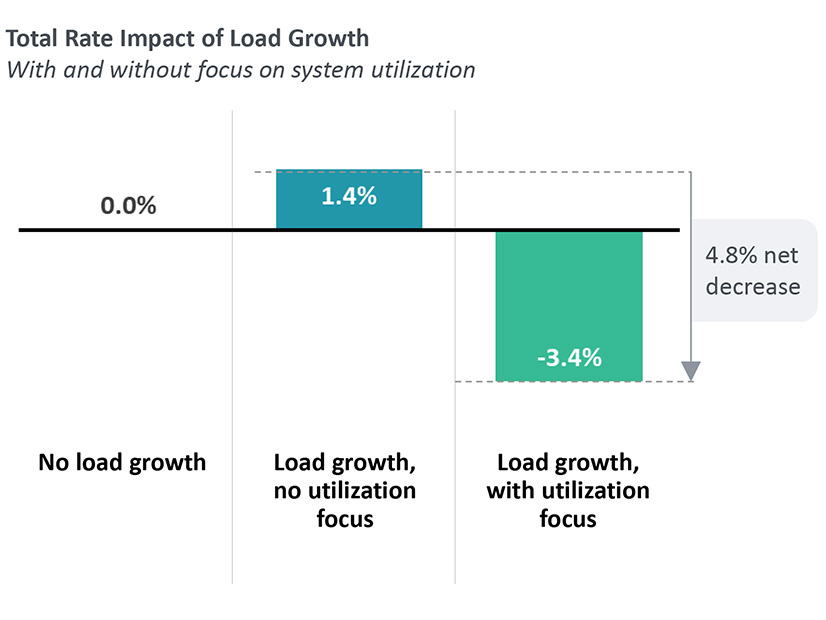

“The Untapped Grid” models a mid-sized utility with a 3,000-MW peak demand experiencing 1,000 MW of load growth — 500 MW of it transmission-connected (such as a data center) and 500 MW of it distribution-connected (such as electric vehicles and heat pumps).

The Brattle Group modeled the rate impact of load growth with and without a focus on fuller utilization of the existing grid. | The Brattle Group

Status quo grid management would result in a calculated 1.4% all-in average rate increase. A 10% increase in annual system utilization would result in a 3.4% rate decrease.

The authors caution that not every circumstance in every utility or market is factored into the calculation, nor other cost-influencing factors, such as aging infrastructure that needs to be replaced or fuel price fluctuations.

GridLab Executive Director Ric O’Connell said some grids are better used than others, but the opportunities to do better are expanding.

“We actually can shape demand and get higher utilization of our existing grid and really use that asset — that very expensive asset — better,” he said. “And so I think that’s going to be incredibly important for affordability going forward.”

Lead author Ryan Hledik said the first step of any effort is to determine the spare capacity on the existing system.

“Studies that Brattle and others have done in the past have shown that nationally, there’s a lot of potential to do this,” he said. “We’ve estimated that with demand flexibility alone, there’s over 200 GW of untapped potential to create capacity across the power system.”

The analysis does not propose specific policies or programs to make better use of that 200-plus GW.

Aligning Incentives, Opportunity

A question was posed during the presentation: Are there factors or circumstances that stand out as obstacles?

Hledik said a fear of the unknown and the financial structure of the utility industry have been problems.

“Current regulatory models typically don’t do a great job of aligning utilities’ incentives with this opportunity. Utilities are financially incentivized to go out and make capital investments in traditional infrastructure,” he said. “They’re not incentivized to go out and pay their customers to use less.”

Hledik added: “There is sometimes a tendency, a perceived risk associated with doing something new, relying on grid flexibility or distributed energy resources to provide the same types of grid services that traditional infrastructure has provided historically. So we need to continue to demonstrate to the industry that this is a reliable option.”

But other things are working in favor of grid flexibility and demand response, particularly the proliferation of battery energy storage systems, which allow energy supply to be moved chronologically to meet demand, rather than demand being moved to match supply.

“The coincidence of batteries getting cheap and load growth coming back make this inevitable, even in the current regulatory model,” said Pier LaFarge, CEO of Sparkfund, which is part of the Utilize coalition.

“There are a lot of tools that are available to do this — batteries, air conditioning, load control, EV charging control, smart panels, time-varying rates, energy efficiency, grid-enhancing technologies,” Hledik said. “There are a lot of options that have really just emerged at scale over the last five years or so … to create the type of capacity that we need for this all to pencil out.”

Another audience question was about concerns that greater grid utilization would reduce the headroom needed during extreme weather events or other crises.

No one is proposing a reduction of reserve margins or revision of grid structures or changes to NERC standards, O’Connell said — the goal is better utilization with the new tools available.

LaFarge said the investments being advocated would create more dispatchable resources that would boost reliability metrics during peak stress periods. He added: “If anything, we’re very intentionally designing this version of grid utilization to advocate for things that directly align with that concern.”

The authors calculate that scaling the report’s model nationally could save ratepayers $110 billion to $170 billion over 10 years, with additional benefits for those who participate in incentivized peak-reduction programs.

“The Untapped Grid” is the newest of many analyses pointing out the value grid optimization and flexibility.

The American Council for an Energy-Efficient Economy offered strategies for demand-side growth management; EPRI laid out scenarios under which new large loads could reduce costs for other grid users; and an analysis modeled the benefits awaiting hypothetical large loads that agreed to partial curtailment.

As many observers have concluded, efforts to optimize the grid through means such as flexibility have become a recurring theme. (See Why 2026 will be the Year of Flexibility.)

Constellation Energy will sell nearly 4.4 GW of PJM generation assets to LS Power.

The agreement announced March 18 is valued at $5 billion before closing adjustments, or approximately $1,142/kW of capacity. It will satisfy many of the federal regulatory requirements attached to Constellation’s acquisition of Calpine, which owned the power plants LS Power has agreed to buy.

FERC ordered some generation assets divested as a condition of approval, and the U.S. Department of Justice added others in its antitrust review.

The Constellation-Calpine deal was completed Jan. 7, creating the world’s largest private-sector power producer, controlling approximately 55 GW of generating capacity.

FERC’s approval in July 2025 entailed Calpine selling 3,546 MW of generation, all of it in PJM: the 1,134-MW gas-fired combined-cycle Bethlehem Energy Center, the 569-MW dual-fuel combined-cycle York Energy Center Unit 1, the 1,136-MW dual-fuel combined-cycle Hay Road Energy Center and the 707-MW gas-fired simple-cycle Edge Moor Energy Center. (See FERC Approves Constellation Purchase of Calpine with Conditions.)

The DOJ agreement also included the sale of the Jack Fusco Energy Center, a 606-MW gas-fired combined-cycle facility in Texas, and minority ownership in the Gregory Power Plant, a 385-MW gas-fired combined-cycle facility in Texas.

The stake in Gregory was divested earlier in 2026. Constellation CEO Joe Dominguez said in a news release that Fusco will be divested later in the year:

“This transaction is an important step in satisfying the DOJ’s requirements and advancing our path forward. These are well-run facilities that will continue powering consumers and businesses for decades to come. We’re pleased to be moving ahead and expect to complete the remaining DOJ requirements later this year.”

LS Power CEO Paul Segal said his company has been building and operating gas-fired power plants for more than 35 years and expects a seamless integration of these new assets: “PJM is at the epicenter of the surge in electricity demand, and these are exactly the kind of assets the grid needs — efficient, dispatchable gas generation that can deliver reliable power around the clock.”

The Constellation-LS Power transaction will require DOJ, FERC and other regulatory approvals.

A new standards development project is a chance for NERC to pilot some of the recommendations from the ERO’s Modernization of Standards Processes and Procedures Task Force, ERO staff told members of the organization’s Standards Committee at their monthly meeting March 18.

The project will focus on computational large loads such as data centers, artificial intelligence computing clusters and cryptocurrency mining, an issue Howard Gugel, NERC’s senior vice president for regulatory oversight, reminded attendees “is coming at us like a freight train.”

“I just talked with a utility [whose] peak load is about 2,500 MW, and they have 15,000 MW of data center load that wants to connect to their system,” Gugel said. “It’s going to be important for us to get this right [and also] to move quickly on this. The data center folks want consistent, uniform standards across North America, and I think the transmission owners want some guidance as to what should be done … to make sure that everything operates reliably.”

That “need for speed” also made the new standards project a good candidate to test out the efficiency improvements proposed in the MSPPTF recommendations approved by the Board of Trustees in February, NERC Manager of Standards Development Sandhya Madan told SC members. (See NERC Board Accepts MSPPTF Recommendations.)

Among those recommendations were using AI to help NERC staff create a term sheet outlining the goals of the proposed standard, and the creation of a pool of subject matter experts to oversee standard development rather than the current practice of creating a dedicated standard drafting team, whose members must be recruited from industry and approved by the SC. (See NERC Modernization Task Force Leaders Present Final Recommendations.)

NERC is planning to test both proposals with the large loads project, Madan said, emphasizing that any experimentation would be “within the bounds of the current” Standard Processes Manual. She told attendees NERC had identified a group of SMEs that were “appropriately vetted and have already demonstrated some level of commitment to addressing emerging risk,” and recommended that these experts — who were not identified by name during the meeting — be chosen as the drafting team for the project.

Alison Oswald, manager of standards development at NERC, added that the ERO is “working on developing a template for a term sheet,” which the drafting team will use to create “a high-level explanation of who a standard would apply to, what goals it is trying to meet [and] what kind of requirements it might cover.”

NERC sees the project itself — which the ERO has dubbed Project 2026-02 after its approval by the SC — as the first phase of a larger effort, Madan said. This stage will focus on drafting new definitions for NERC’s Glossary of Terms, including for “computational load” and “computational load entity.”

Phase 1 will also initiate development of one or more standards to address “near-term” risks associated with computational large loads. These risks include reduced visibility into large load centers, potential instability during system disturbances and “increasing certainty for both system planning and real-time operations,” Madan said.

Michael Goggin of Grid Strategies pointed out a lack of representation by independent power producers on the proposed team and asked if there was any potential to “add one or two people to bring in that perspective” while still approving the rest of the slate. Gugel observed that the SC “at any point could bring a motion forward to do an augmentation for any standard drafting team.” Goggin agreed that this “may be a viable path” to add the needed expertise.

Final IBR Standards to be Posted

Only two other standards projects came before the committee, both of which address the final milestone of FERC Order 901, covering operational and planning studies for inverter-based resources.

The team for Project 2025-03 (Order No. 901 operational studies) brought a request to authorize posting two proposed standards for a 45-calendar-day formal comment and ballot period: TOP-003-9 (Transmission operator and balancing authority data and information specification and collection) and IRO-010-7 (Reliability coordinator data information specification and collection). (The standards are found on pages 36 and 64 of the committee’s agenda, respectively.)

According to Madan, the proposed standards would address FERC’s directive by including “IBR performance and behavior in operational assessments and real-time monitoring of individual IBR plants,” along with aggregated IBRs across an operator’s footprint.” They would also require distributed energy resources to be included in operational assessments.

At the same time, Project 2025-04 (Order No. 901 planning studies) requested that the SC post TPL-001-6 (Transmission system planning performance requirements) for comment and ballot (page 99 of the agenda). Madan explained that the standard includes new requirements to study registered and unregistered IBRs, including distributed IBRs, in planning assessments.

Both requests were accepted without objection by SC members.

The Western Transmission Expansion Coalition’s 10-year outlook has spurred talks about increased coordination among jurisdictions to upgrade or build 12,600 miles of transmission in the West and fueled calls for states to create a task force to streamline permitting and other issues.

That volume of transmission would cost approximately $60 billion over 10 years to meet the region’s forecast 30% increase in peak demand by 2035, according to WestTEC’s 10-year outlook. (See West Needs $60B in Transmission Ahead of 2035, WestTEC Finds.)

Another key finding is that coordinated action between states, utilities, developers and regional partners can help the West meet this challenge, Sarah Edmonds, CEO of Western Power Pool, told RTO Insider.

“What we’re hoping to see is continued collaboration and engagement among many members of that coalition to use the results of the study to inform planning, catalyze development and advance transmission projects,” Edmonds said. “As stakeholders or regulators weigh these potential projects, they can look at the study to gain a better understanding of why projects are needed and how they fit into the larger, regional picture, perhaps making the process a little easier than it would have been otherwise.”

The WestTEC effort, jointly facilitated by WPP and WECC, addresses long-term interregional transmission needs across the Western Interconnection. The 10-year planning horizon was released in February 2026. A 20-year outlook is slated for release later in 2026.

WestTEC’s main objective is to create an “actionable” transmission study by conducting integrated planning analysis across the Western Interconnection.

But to implement the report’s findings, the region must overcome “development, regulatory and financing challenges,” according to the report.

Coordination among states, utilities, developers and regional partners “can materially improve outcomes” by addressing a host of issues, such as cost allocation, procurement of transmission components, siting and permitting, the report states.

During a March 10 WECC meeting on the report, WECC board member Jacinda Woodward asked how stakeholders can “collectively help build momentum,” noting that without engagement on the report, “we’ll be talking about this in five years from now and then we’ll be in real trouble.”

Trade organizations RTO Insider spoke with similarly called for collaboration across state lines and appeared ready to build momentum.

For example, The Western Transmission Consortium (TWTC), which is referenced in the WestTEC report as a vehicle for collaboration, said it is “excited” to implement the findings and ultimately put “steel in the ground.”

Launched in 2024, TWTC is member-owned organization with a goal of bringing together various entities to build infrastructure across the West, according to its website.

“WestTEC set the table, and we will see whether the states and federal government are serious about building the transmission needed to meet the demands and policy imperatives of the 21st century,” Ray Gifford, TWTC co-founder, told RTO Insider in an email.

That sentiment was echoed by Gridworks Executive Director Matthew Tisdale, who said “one of the biggest barriers to moving these critical transmission projects forward is permitting across multiple jurisdictions.”

“States can lead by working together through a coordinated task force to streamline processes, reduce delays and deliver the transmission our region needs,” Tisdale said. He added that the organization “is actively working with states, developers and other leaders across the West who are willing to stand up such a team.”

Although the WestTEC team is not involved in policymaking, there is still time for stakeholders in the West to get involved, especially in activities related to the upcoming 20-year horizon, Edmonds said during the March 10 WECC meeting.

“We have defined already the scenarios we’re going to look at,” she said about the 20-year study. “But the devil is in the details, and there’s a lot more conversation about those details left to be had. I always leave with the invitation that WestTEC is a very open community and a marketplace of ideas. And we’re open for business.”