MISO has concluded that Pearl Street’s SUGAR automation software is an effective alternative to the power flow simulations it used to conduct to identify network upgrades for generation projects in the queue.

MISO released an analysis comparing the software’s ability to pinpoint upgrade needs for new generation entering the system with MISO’s previous analyses on the 2021 cycle of generation proposals. The RTO said SUGAR performed at a 99.23% match rate with “minimal deviations” when searching for thermal constraints, a 100% match rate with some extra identified constraints when looking for flowgate limits and a 99.03% match rate when spotting voltage issues with “justified” minor violations.

Ahead of the analysis, MISO said SUGAR would have to identify at least 98% of constraints uncovered through its legacy analyses to be considered a success. MISO said across all three comparisons — thermal, flowgate and voltage — SUGAR results aligned with MISO studies 99.2% of the time.

MISO is using Pearl Street’s SUGAR (Suite of Unified Grid Analyses with Renewables) software to screen generation projects and perform the first phase of studies in the queue. It’s betting the tech startup’s assistance with conducting studies can dramatically accelerate its yearslong queue processing. Austin, Texas-based software company Enverus acquired Pearl Street in March.

The RTO plans to start the first phase of studies on the 2023 batch of project proposals in July. It won’t begin analyzing 2025 entrants until the end of the year. MISO hopes to have all projects in those cycles striking interconnection agreements over 2026, with the still-in-progress 2022 cycle proceeding in the second quarter, 2023 in the third quarter and 2025 by the end of 2026. (See MISO Unveils Later Timeline for Queue Processing Restart.)

MISO skipped acceptance of a 2024 queue class altogether. Throughout 2024, it delayed kickoff of studies on the 123 GW of projects that entered the queue in 2023 while Pearl Street assisted with modeling.

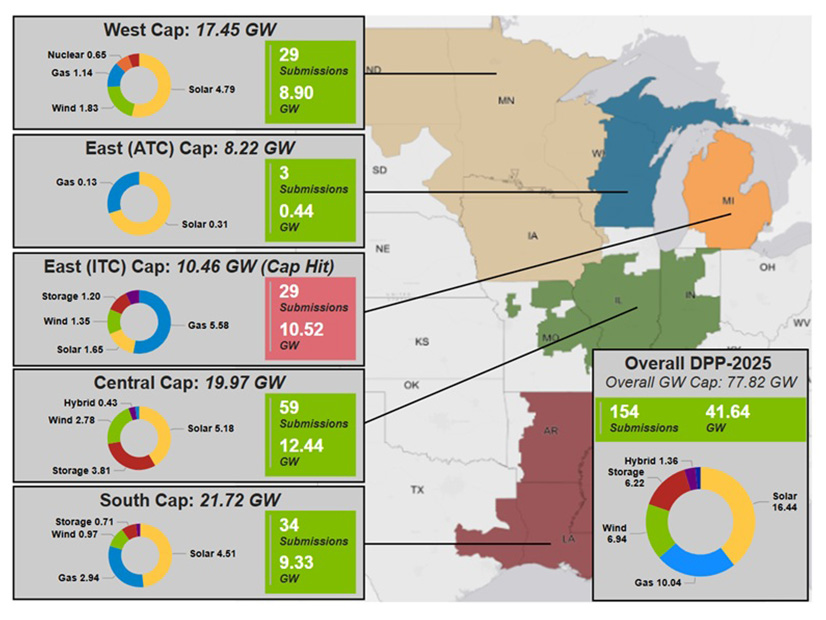

MISO study region queue caps and project submittals as of April 2025. The East ITC study region has exceeded its queue cap. | MISO

MISO found that SUGAR completed the first phase of interconnection studies faster while estimating similar costs for network upgrades. MISO said while it spent 686 days to ultimately estimate $13.36 billion in upgrades for the 2021 queue cycle of projects, SUGAR estimated $13.25 billion for the same batch of projects within 10 days.

MISO staff at an April 22 Interconnection Process Working Group said SUGAR provided a good match for the RTO’s longer-form interconnection studies.

“These results confirm that SUGAR can be utilized in MISO’s [first definitive planning phase (DPP)] studies with minimal impact to stakeholders while also providing significantly increased speed in conducting MISO DPP Phase 1 studies,” MISO wrote in its analysis.

MISO said SUGAR results are in “excellent agreement” with MISO’s previous study process regarding flowgate project assignments. When hunting voltage constraints, MISO said SUGAR landed on 102 of the 103 constraints it previously identified while reporting six more that didn’t turn up in MISO studies. MISO said the additional constraints SUGAR called out are “deemed acceptable within the bounds of engineering judgment.”

MISO also said SUGAR noted 259 of the 261 thermal constraints MISO previously reported. The RTO said it expected small deviations in the output of different powerflow tools.

The East ITC study region, which contains Michigan’s Zone 7, exceeded the cap at 29 submittals at 10.52 GW. Any other projects that hoped to enter under the 2025 cycle now must queue up for the 2026 cycle.

MISO has been allowing projects to line up for 2025 queue processing since last year. Its cap for the 2025 queue cycle is nearly 78 GW. So far, MISO has recorded 154 project submissions at 41.64 GW.

At the April 22 meeting, John Liskey, of the Citizens Utility Board of Michigan, said the resources that entered before the East region’s cap was exceeded contain a large amount of gas capacity, which could violate Michigan’s renewable energy standard of 50% by 2030 and 60% by 2035.

DENVER — FERC, in two separate orders, approved SPP’s $150 million funding agreement for Markets+ and the funding mechanisms under which the RTO will finance the implementation phase of the market’s development.

News of the decision met with an enthusiastic response at a meeting of the Markets+ Participants Executive Committee (MPEC) in Denver.

“I have some lovely breaking news. FERC has approved the funding agreement, the funding mechanism today,” Carrie Simpson, SPP vice president of markets, said at the meeting, prompting applause among committe members.

“These achievements represent meaningful steps in the progress towards launching Markets+ and bringing the West closer to realizing the substantial value of a robust regional market,” SPP COO Antoine Lucas said in an April 22 press release. “SPP is proud to see the hard work of the Markets+ stakeholders pay off in this series of approvals that clear the path toward market launch in 2027.”

Specifically, FERC approved the SPP Phase 2 funding agreement, which lays out how SPP will finance Markets+’s $150 million in implementation costs (ER25-1372).

Eight Western entities have signed the agreement as of April 16: Arizona Public Service, Bonneville Power Administration, Chelan County Public Utility District (PUD), City of Tacoma, Grant County PUD, Powerex, Salt River Project and Tucson Electric Power.

The agreement requires the entities to provide collateral to SPP’s lender to support the financing the RTO will use to develop Markets+ during the implementation phase. The collateral is equal to the amount of the entities’ Phase 2 obligations.

The recovery of the costs to repay the implementation financing “will be incorporated into the rates charged in the Markets+,” according to a frequently asked questions document posted on SPP’s website.

“This eliminates the need for the funding participants that participate in Markets+ to provide lump sums of money to directly fund Phase 2 outside of the specific circumstances outlined in the funding agreement (i.e., withdrawal, termination, default),” according to the FAQ.

A significant detail in the funding agreement order: FERC’s rejection of concerns raised by a group of public interest organizations (PIOs) around the Bonneville Power Administration’s connection to the agreement.

The PIOs protested that the agreement would effectively obligate BPA to participating in Markets+ even ahead of issuing its formal record of decision (ROD) on its day-ahead market participation because the agency would be on the hook for providing up to $40 million in implementation costs to SPP even before releasing the ROD. They contended that either SPP’s filing had mischaracterized BPA’s commitment to Markets+ or that the agency had been engaging in a “sham” process regarding its day-ahead market decision.

“We disagree with PIOs that the funding agreement requires Bonneville (or any other funding participants) to participate in Markets+,” FERC wrote. “As PIOs acknowledge, the funding agreement requires a funding participant to pay its Phase 2 obligations in the event it decides to withdraw from the funding agreement; however, the funding agreement does not obligate any funding participant to proceed with Markets+ participation.”

The commission also dismissed the PIOs’ concerns around how a funding participant such as BPA would cover its costs if it decided to withdraw from the market, saying the issue was out of scope for the order.

“In addition, because the funding agreement does not govern whether or how a withdrawing funding participant will recover its Phase 2 obligations after a withdrawal, we find PIOs’ arguments about Bonneville’s plan to recover such potential costs are outside the scope of this filing.

“We also find that PIOs’ arguments concerning Bonneville’s decision-making process related to Markets+ participation, including any associated communications with stakeholders, are outside the scope of the filing,” the commission wrote.

Funding Mechanism

The second order concerned SPP’s funding mechanism, which details how the RTO “will finance the implementation phase of the market’s development,” according to SPP’s news release (ES25-33).

The mechanism will entail SPP taking out a $150 million loan collateralized by the full funding obligation of each Markets+ participant, except BPA.

The commission approved the mechanism despite its failure to meet FERC’s interest ratio coverage screen, a measure of how readily an entity can cover its debt.

“SPP has cited other factors that provide the commission with a sufficient alternative basis upon which to conclude that SPP has reasonable prospects for being able to service the proposed new debt securities for which authorization is sought in the application, and to continue to be able to provide service as a public utility,” the commission wrote.

FERC has approved a PJM proposal to limit capacity prices to between $175 and $325/MW-day for the next two Base Residual Auctions (BRAs), resolving a complaint from Pennsylvania Gov. Josh Shapiro alleging there was potential for prices to soar above what is necessary to maintain resource adequacy (ER25-1357).

The commission found that PJM’s capacity market is facing conditions outside the bounds considered in the 2022 Quadrennial Review, noting the RTO’s filings highlighted a confluence of a tightened auction schedule, load growth, generation deactivations, a backlogged interconnection queue and external constraints to resource entry such as permitting and supply chain challenges.

FERC said in the April 21 order that PJM and the Shapiro administration proposed a temporary measure to add a “collar” to the clearing prices for the 2026/27 and 2027/28 capacity auctions while the RTO drafts long-term market changes in the current Quadrennial Review and implements a cluster-based approach to studying projects in its interconnection queue. (See PJM, Shapiro Reach Agreement on Capacity Price Cap and Floor.)

While the price band initially would be set at $175 to $325/MW-day, those values would be readjusted annually based on the accreditation of the reference resource — a dual-fuel combustion turbine generator — and therefore could change.

“We agree with PJM that the price cap and price floor will operate together to narrow the range of potential capacity price outcomes, which will reduce the price volatility under the existing” variable resource requirement curve, FERC said. “In accepting PJM’s proposal, we recognize that several commenters representing both suppliers and consumers support the proposal as a balanced, time-limited approach, and that several additional commenters do not oppose PJM’s proposal.”

The proposal was supported by the New Jersey Board of Public Utilities and Pennsylvania Public Utility Commission, as well as generation owners and utilities including Talen Energy, Constellation Energy, Calpine and Dominion Energy, who commented that it represents a temporary measure to keep costs reasonable while new market rules are developed through the Quadrennial Review.

In his complaint, filed Dec. 30, 2024, Shapiro argued that between a backlogged interconnection queue and an auction schedule that has been delayed repeatedly to the point the 2026/27 BRA is set to be conducted within a year of the start of the corresponding delivery year, developers would have no opportunity to respond to high prices by bringing new resources to market.

In line with PJM’s proposal and statements to stakeholders when it was presented to the Members Committee in February, the commission’s acceptance of the filing included the dismissal of Shapiro’s complaint as moot. (See PJM Presents Capacity Price Cap and Floor to Members Committee.)

A maximum price point has been a part of the Reliability Pricing Model (RPM) since its inception, but the proposal represents the first instance of a price floor being included in auction rules. The Independent Market Monitor and North Carolina Utilities Commission protested against the minimum price, arguing it could require consumers to procure unneeded capacity.

The Monitor also argued that curtailment service providers may seek to take advantage of the price floor by offering a large amount of demand response resources, which the commission found out-of-scope as PJM proposed no changes to DR rules.

PJM said the floor would counterbalance the diminished maximum price by providing revenue certainty to market sellers, which would support near-term investments in capacity. It also wrote it would be unlikely the marginal resource would clear at $175/MW-day or less given the tight market conditions and that the 2025/26 BRA cleared at nearly $270/MW-day.

Shapiro also supported the price floor, arguing it would address the market uncertainty sellers are likely to face over the next two auctions.

The commission wrote that PJM demonstrated the capacity shortage seen in the 2025/26 auction — when just 20.7 MW of offered capacity did not clear — is likely to continue for at least the next two years. It noted that PJM anticipates 4 GW of load growth in the 2026/27 delivery year and 6 GW the following year.

“Given the facts and circumstances presented in this record, we find that the benefits of PJM’s proposed temporary price floor outweigh the potential risk of over-procurement, and therefore find PJM’s proposal for a temporary collar is just and reasonable,” FERC said.

The commission rejected a protest from coal trade association America’s Power that the proposed maximum price would prompt planned resources to drop out of the queue and cause existing generation to deactivate or seek to offer capacity to other regions. It cited analysis of resources that have deactivated in the past after operating on reliability-must-run (RMR) agreements with cost-of-service compensation, finding that a $500/MW-day clearing price would make half of those resources economic, while a $325 clearing price would make them all uneconomic.

The commission wrote that cost-of-service is not comparable to the revenues a resource receives from PJM’s capacity, energy and ancillary service markets.

FERC’s order follows several others approving PJM proposals to rework elements of its capacity market, including requiring intermittent and storage resources to submit capacity offers, including the output of units operating on RMR agreements in the supply stack and reworking how gas resources are modeled in the winter.

Stakeholders and advocates are sounding off for and against expedited review of the $5 billion-plus Clean Path transmission proposal that would feed power into New York City.

Efforts to build the 175-mile underground HVDC line suffered a setback in late 2024 due to cancellation of a larger project in which it was packaged with 23 new wind and solar facilities in rural New York. (See $11B Transmission + Generation Plan Canceled in NY.)

NYPA is asking the state Public Service Commission (PSC) to designate Clean Path a priority transmission project (PTP) (Case 20-E-0197) in hopes of accelerating its development and speeding up the benefits it would provide to the environment and to grid reliability. (See NYPA Argues Clean Path Potential Benefits Outweigh Cost.)

NYPA estimates the cost of Clean Path at $5.2 billion. It proposes allocating 60% of the cost to NYISO Zone J (New York City), which could reduce its reliance on fossil fuel generation and enjoy cleaner air thanks to Clean Path, and 40% to rest of the state on a load-share basis.

The PSC solicited comments on NYPA’s request in February, and the window closed April 21; a spokesperson said April 22 the comments will be reviewed but there is no timetable yet for further action.

In the comments, advocates for environmental quality and for organized labor generally argued in favor of priority status for the proposal while many in the energy sector raised objections.

These objections often focused on the need or lack of need for Clean Path, and the fact that the proposal differs substantially from the one first submitted.

The original project, called CPNY or Clean Path New York, was a public-private generation-transmission proposal by NYPA and Forward Energy that won a state contract for Tier 4 renewable energy certificates. The contract was terminated in November, the partnership was dissolved, and Clean Path now is transmission-only.

Among the comments:

National Grid Ventures said without the 3.8-GW suite of renewable generation projects originally envisioned for CPNY, Clean Path should not be granted priority status. It further said the project itself should not proceed without independent verification of its need. It concluded: “If the commission determines the project is required and that it should be granted PTP status, then NYPA should be ordered to competitively solicit proposals and reserve the right for the commission to approve who NYPA ultimately teams with for the project.”

PSEG Long Island supports designation as a priority transmission project on the belief that, because NYPA’s cost of debt is lower and it is tax-exempt, development costs and costs to customers would be lower than if a private developer did the work.

Independent Power Producers of New York noted that CPNY won its state contract through a competitive solicitation and argued the PSC should consider new competitive solicitations to avoid burdening ratepayers with unnecessary costs. It added that renewable energy development is behind schedule in New York. “Thus, any ‘urgency’ to complete the Clean Path project is an overreach at best and should not outweigh the commission’s long-established precedent that competitive solicitations ensure the lowest cost for consumers.”

Alliance for Clean Energy New York supports priority designation as a way of addressing future reliability and transmission security deficiencies; reducing the need for more expensive local generation to meet the locational minimum installed capacity requirement in Zone J; and facilitating development of renewable resources upstate, where the HVDC line would originate.

New York Transco — which is collaborating with NYPA on another major downstate transmission project, Propel NY Energy — said NYPA has not demonstrated that Clean Path meets the criteria for priority designation. It also questioned whether Clean Path could unbottle existing renewable capacity in the region and said NYPA has failed to support the cost recovery mechanism it proposed.

Consolidated Edison Co. and four other utilities said the PSC should deny NYPA’s request because NYPA had not shown a need for urgency and its petition lacks sufficient analytical support.

The president of a residents’ association at a public housing project near Clean Path’s planned southern terminus said her neighborhood long has been plagued by poor air quality from nearby fossil-burning plants and the new line would provide relief. “I respectfully ask the commission to approve this project and move it forward. Our community can’t wait any longer.”

U.S. Sen. Charles Schumer and U.S. Rep. Dan Goldman, both New York Democrats, recited a list of benefits Clean Path is expected to offer and said priority status should be granted.

Con Edison Transmission recited a list of deficiencies it said exist in the Clean Path petition and said priority status should not be granted.

New York State AFL-CIO President Mario Cilento said: “We support designating this project as a priority transmission project because it will create good union jobs and help achieve the state’s emissions reduction goals.”

Multiple Intervenors, a collection of 55 large energy consumers statewide, faulted the 60-40 cost allocation split on several levels and urged a 75-25 split instead, placing most of the cost where most of the benefit would be realized: Zone J. And they said the 25% share should be spread across the entire state — not the rest of the state excluding New York City.

New York City urged priority designation for Clean Path for all the benefits it would provide but urged transparency on the cost of the project. It said it does not object “for now” to footing 60% of the cost, but said the split should be revisited if power begins to flow from downstate to upstate. (New York’s vision is that offshore wind farms someday may accomplish this feat.)

The city also wants clear indication that the 40% is to be spread across the rest of the state — not across the entire state including New York City.

The Census Bureau estimates New York City is home to 42% of the state’s residents.

NYISO estimates the generation mix on the New York City grid is almost 90% fossil-powered, while parts of the upstate grid are almost 90% emissions-free.

A California state Senate committee voted unanimously in favor of the Pathways bill, bringing the Golden State closer to allowing CAISO to cede oversight of its energy markets to an independent regional organization (RO).

Members of the state Senate Energy, Utilities and Communications Committee on April 21 voted 17-0 in favor of Senate Bill 540, dubbed “Pathways,” sending the proposed legislation to the Senate Judiciary Committee for a hearing April 29.

The bill is the product of the work of the West-Wide Governance Pathways Initiative, the nearly two-year effort to support the expansion of CAISO’s Western Energy Imbalance Market (WEIM) and soon-to-be-implemented Extended Day-Ahead Market (EDAM) to entities outside California by shifting governance of the markets from the ISO to a proposed independent RO.

Democratic Sens. Henry Stern and Josh Becker introduced the bill in February. During the April 21 hearing, Becker noted the legislation comes as SPP prepares to launch its own day-ahead market, Markets+, which already has attracted participants. (See Pathways ‘Step 2’ Bill Introduced in Calif. Legislature.)

“Why do we need to do this now? The urgency is that if we don’t act quickly, we risk having less ability to trade with other regions and impact the clean energy resources available across the West,” Becker said. “Regions are getting tired of waiting for us and are considering joining Southwest Power Pool’s Markets+. If they do, they will stop trading with California and also in this WEIM I mentioned earlier, and have less need to make other bilateral trades with California.”

Becker said participation in the RO is voluntary, adding that California retains its right to set its own energy policy goals and doesn’t have to join unless “specific, stringent guardrails are met.”

Reached for comment about Becker’s statement, SPP spokesperson Derek Wingfield told RTO Insider: “Markets+ creates additional opportunities for Western entities and will not inhibit trade among them, including entities in California.”

Stern, meanwhile, contended Pathways would allow California to tap into a wider market of clean energy resources, saying “if we don’t reach beyond our borders and allow for other cleaner renewables to be able to come in and balance our grid depending on the time of day, we’re gonna have to find that power somewhere. And right now, we are literally paying for it, and we’re not just paying for it with taxpayer dollars, but it’s in our lungs, it’s in environmental injustices everywhere.”

Representatives from the International Brotherhood of Electrical Workers, Natural Resources Defense Council, Environmental Defense Fund and others supported the bill during the hearing.

Opposition, Concerns

However, lawmakers also heard from opponents, including the Center for Biological Diversity, the California Solar & Storage Association and Californians for Green Nuclear Power.

Bill Julian, former legislative director of the California Public Utilities Commission, opposed the bill on behalf of himself and former CPUC President, Loretta Lynch.

Lynch, in a previous meeting, contended many of the arguments favoring Pathways rely on hypothetical scenarios in which EDAM would consist of participants from all Western states. This is unlikely, Lynch said, noting that several entities already have decided not to join EDAM. (See Pathways Initiative Receives Praise, Skepticism at Calif. Hearing.)

Though the committee voted unanimously to pass the legislation, some lawmakers voiced concern about the lack of certain provisions in the bill.

For example, Democratic Sens. Benjamin Allen and Aisha Wahab expressed concern about California’s ability to withdraw from the RO under the legislation.

Allen pointed to comments by groups like The Utility Reform Network (TURN) that have argued the bill’s language is not strong enough to protect from the risk of penalties against the state or utilities if California withdraws.

Committee member Susan Rubio urged Becker to explore further consumer protections.

Becker noted that the groups behind the bill are looking at amendments and plan to move forward with some suggestions, even some from opposing parties like Lynch.

“Certainly, you have my commitment to work with you and make sure that by the end of this process there’s a bill that we’re all comfortable with,” Becker said. “And then, as just a reminder, we’ll have at least two years with the legislature able to weigh in before we join.”

The Pathways bill states that CAISO can decide whether to join the RO-governed market on or after Jan. 1, 2027.

FERC has approved most of NYISO’s proposed plan to comply with Order 2023, denying several of its proposed variations to the commission’s pro forma rules and directing the ISO to submit an additional compliance filing in 60 days (ER24-1915, ER24-342).

Issued in July 2023, the order directed grid operators to revise their generator interconnection procedures to a “first-ready, first-served” cluster study process. It revised the commission’s pro forma procedures while allowing for independent entity variations to account for regional differences.

For NYISO, this meant altering several of the order’s time frames to align with its current Class Year study process, which already used a clustered approach, with queue position playing a limited role. For example, the ISO asked for 596 days to complete the overall study process, slightly more than the order’s maximum of 585, and proposed that its customer engagement window be 70 calendar days, instead of the order’s prescribed 60.

FERC accepted most of these in its April 17 order because it found they “accomplish the purposes” of Order 2023 and would give both NYISO and its interconnection customers flexibility.

While several parties protested the proposed 596-day time frame, the commission said “NYISO’s cluster study process has a unique study structure and requirements due to its proposed single, two-phase study process, which already incorporates restudies and does not have a separate facilities study. Thus, the timeline of the proposed NYISO cluster study process is appropriately compared to the timeline of pro forma study process including the pro forma LGIP facilities study timing, contrary to the contentions of” the protesters.

The commission, however, denied the ISO’s proposal to not allow interconnection customers to use third-party consultants to perform study work. While it argued “that study elements need to be sequenced and managed in a particular order, NYISO does not explain why a third-party consultant could not perform its study within that time frame,” the commission ruled. The variation would not “accomplish the purposes of the cluster study to increase efficiency and provide greater certainty to interconnection customers,” it said.

FERC also denied NYISO’s proposal to apply penalties only at the end of the process, and not at the end of Phase 1. The commission said this did not provide a sufficient incentive for NYISO to complete Phase 1 in a timely manner.

And FERC denied NYISO’s proposal to use a 300-day affected-system study timeline, saying it would bring the ISO out of step with neighboring regions that adhere more closely to the pro forma 150-day timeline. FERC told it to either revise the timeline to 150 days in its compliance filing or justify its proposal.

Finally, FERC rejected NYISO’s method for allocating the costs of several studies as outside the scope of Order 2023, but without prejudice, giving the ISO the opportunity to file it as a separate proposal.

MISO and PJM will not take on customary interregional planning studies this year, deciding they have enough on their plates with a new and in-progress joint transfer study.

The grid operators announced they would devote their attention throughout 2025 to their interregional transfer capability study (ITCS), a new type of study that might yield projects that allow for a greater volume of transfers. (See Smaller Projects Expected from Maiden MISO-PJM Joint Tx Study and OMS, OPSI Pen 2nd Letter to MISO and PJM to Compel Meaningful Interregional Planning.) The two decided against undertaking a more traditional coordinated system plan, which could result in more expensive interregional market efficiency projects, or their established, smaller targeted market efficiency project study.

MISO and PJM arrived at the conclusion after conducting an annual issues review designed to look for transmission opportunities. The process is required under their joint operating agreement.

The RTOs said there’s a possibility their ITCS changes the way the two manage future interregional studies. They said their transfer study could lay the “foundation for assessing future coordinated planning needs.” MISO and PJM are working from a blended, long-term model that combines the RTOs’ assumptions to identify system needs in the transfer study, a first for two major North American RTOs.

“By focusing our efforts on the ITCS, we aim to gain a clearer understanding of emerging transfer limitations and deliverability issues across the seam. The insights gained through this study will help guide future planning activities and determine whether additional interregional analysis or project development is appropriate in subsequent years,” MISO and PJM said in an April 18 emailed statement to their stakeholders.

The two said they would update stakeholders as the transfer study progresses and if “planning needs arise that warrant further coordination.”

MISO and PJM so far have identified more than 30 shared reliability, transfer and economic issues that could form the basis for upgrades under the ITCS.

In an emailed statement to RTO Insider, MISO said the goal remains to develop a draft portfolio by the end of 2025. MISO said it and PJM plan to open a monthlong stakeholder comment period at the end of April to solicit solutions.

MISO and PJM previously said they would focus on equipment upgrades and projects that can use existing rights-of-way in the first transfer study. They said the study, combined with FERC Order 1920, could open the door for longer-term interregional planning and greenfield projects.

MISO and PJM historically have approved one interregional market efficiency project in 2020 and four sets of the smaller targeted market efficiency projects aimed at relieving congestion since 2017. They haven’t completed an interregional transmission planning study since 2022.

FERC Commissioner Willie Phillips, who chaired the agency for two years, announced April 22 that he was leaving the agency just over a year before his term was set to expire, after pressure to resign from the White House.

In news first reported by POLITICO, the White House asked Phillips to step down. The move gives President Donald Trump the power to nominate a new commissioner, shifting its partisan balance to three Republican appointees and two Democrats, the standard makeup of a fully staffed FERC that gives the party in the White House a majority.

FERC Chair Mark Christie released a statement, noting the two had known each other for years before becoming federal regulators as they both were on state utility commissions that were active in the Organization of PJM States Inc. (OPSI) and at the National Association of Regulatory Utility Commissioners.

“Willie has been a good friend for whom I have tremendous respect and affection,” Christie said. “He is a dedicated and selfless public servant. As I have said many times, he did an outstanding job as chairman of FERC. He and I worked together on many contentious issues to find common ground and get things done to serve the public interest. We will miss him here at FERC.”

Christie wished Phillips continued success on “whatever career path he chooses” after leaving the commission.

Phillips posted his own statement on LinkedIn, saying it was time for to move on after being a regulator for 12 years, which includes his tenure at the D.C. Public Service Commission.

“As my time at FERC comes to a close, I’m proud of all we’ve accomplished to advance a more reliable and affordable energy future for all Americans,” Phillips said. “Our grid faces growing challenges — from surging demand driven by data centers, to resource adequacy, capacity markets and the urgent need for transmission reform. These complex issues demand bold, innovative solutions, and I look forward to continuing to work on them in the next chapter of my journey.”

The other three FERC commissioners all released statements praising Phillips for his work on the commission, but his departure was criticized by longtime agency watcher and Public Citizen Energy Director Tyson Slocum.

“Commissioner Phillips’ decision to voluntarily leave his seat a year early hands control of FERC to the White House, where Trump’s radical plans to abuse national security and emergency powers will now likely no longer feature meaningful FERC opposition,” Slocum said. “Phillips had an opportunity to ensure an independent check on Trump’s abuses, but he apparently decided he has better things to do than ensure the public interest is protected.”

While the president can name the chair at FERC, current legal precedent holds that commissioners can be fired only for cause.

The chairs of other regulatory agencies that fall under that precedent, including the Securities and Exchange Commission, the Federal Communications Commission and the Federal Trade Commission, all stepped down when Trump took office this January. The chair stepping down if the opposite party won the presidential election used to be the norm at FERC, but it started breaking down before Trump took office in 2017.

A spat between President Obama and the Senate Energy and Natural Resources Committee left FERC with only three Democratic members when Trump took office and without a quorum when he demoted Norman Bay from chair, who resigned in response. Then after President Joe Biden took office, two of Trump’s former chairs — Neil Chatterjee and James Danly — both served out their full terms.

Chatterjee posted on X when the news broke that Phillips’ departure was disappointing, and he noted that the differences between commissioners at FERC usually are not partisan. Phillips pushed through new LNG export facilities when the Biden White House issued a pause on approvals from the Department of Energy, and he was the lone dissenter on a data center co-location deal last year when Republican colleagues voted to deny it. (See FERC Rejects Expansion of Co-located Data Center at Susquehanna Nuclear Plant.)

FTC Chair Lina Khan stepped down in January, but last month, Trump fired two other Democratic appointees to the agency who are challenging that in court.

Speaking at the Colorado Legislature in March shortly after Trump fired him, FTC Commissioner Alvaro Bedoya said he was not focused on the status of the law, or respect for Supreme Court precedents.

“I think we need to be focused on the billionaires over President Trump’s shoulder at his inauguration, and what this attempt will do for them,” Bedoya said. “Because I think above all else, we need to be asking ourselves, who will win from this attempt to illegally remove us?”

Those included big tech executives like Tesla and X’s Elon Musk, Meta’s Mark Zuckerberg and Amazon’s Jeff Bezos, all of whom were subject to court orders or litigation from FTC cases, he added.

Trump has not made any moves on the two Democrats left on FERC, and doing so now would leave the agency without a quorum and unable to move on key policy priorities like ensuring data centers can reliably connect to the power grid or expanding LNG exports.

“What could happen is that if the president has the authority to remove members of the FTC, I would think there is nothing that would constrain the president from moving members of FERC if the president so desired,” former Chair Bay said at the WIRES Group Spring Meeting on April 3.

Bay also made the point that when he was on the agency, the split votes were more likely to happen between Democrats than across party lines.

“That was the world I came from, but I think that was really important for FERC authority, for its legitimacy, for the regulatory stability and certainty provided to industry,” Bay said. “And, so, what I hope does not happen at FERC is that you get a revolving door of commissioners based upon changes in presidential administrations.”

HOUSTON — SPP’s Markets and Operations Policy Committee has endorsed the last of 21 recommendations made by a task force that reviewed the RTO’s transmission and market operations in the last decade.

The proposed tariff change (RR665) would establish “subregions” for the cost allocation of future byway (between 100 and 300 kV) upgrades.

“It’s been a long time coming,” Evergy’s Derek Brown, a supporter of the revision request, said during MOPC’s April meeting. “We just need to know the size of the subregions, which we now have.”

SPP said the tariff change could be implemented next year, once it receives approval from the Board of Directors, state regulators and FERC.

“I’ll just share Evergy’s opinion that we should try and move faster than that, if possible,” Brown said. “The policy has been approved for a long time now. We have some of the largest portfolios we’ve ever seen that we just went through the last few years, and we have another large one, potentially, in the 2025 [Integrated Transmission Planning assessment]. Cost allocation has a big impact on those discussions.”

The change, as developed by the Cost Allocation Working Group’s state regulatory staff, would decouple SPP’s Schedule 9 (zonal rates) and Schedule 11 (highway/byway) transmission pricing zones and create larger Schedule 11 subregions of existing zones. Two-thirds of the cost of byway upgrades would be allocated to the subregion where they are connected, with the remaining 33% allocated to the SPP footprint.

Similar to 300-kV and above highway projects, new base plan upgrades larger than 300 kV would be allocated RTO-wide.

The change must be approved by the board and Regional State Committee when they meet May 5.

MOPC approved the proposed tariff change with 75.99% approval. Six of 17 transmission owners and seven of 55 transmission users voted against it.

The tariff change was hung up for several years by work on another HITT recommendation to adopt a policy creating an appropriate balance between cost assessed and value attained from energy and network resource interconnection service products and generating resources with long-term firm transmission service.

“Not everybody got what they wanted on this, but this really is bringing about what was intended; what HITT wanted to do,” said Golden Spread Electric Cooperative’s Mike Wise, who was a HITT member. “I remember how long it took to get through [the other recommendations], and finally when we did, we breathed a sigh of relief. And then we started working immediately on [RR665].”

2025 ITP: Waiting on Study Request

SPP’s manager of transmission planning, Kirk Hall, told MOPC that the 2025 Integrated Transmission Planning assessment will be the most complex study to date.

He based his comments on a potential 9-GW generation shortfall; exponential load growth that has resulted in 57,000 non-converged contingencies (too many needs for one Microsoft Excel workbook); large loads interconnected with substations that have substandard transmission; and other factors.

“People have asked me, ‘What do you think the portfolio is going to look like this year?’ And I don’t really know, but I think it’s going to be somewhere between diddly-squat and a gazillion,” he said to laughter. “Somewhere in the middle. We’re just not quite there yet.”

Hall said staff were “smack dab” into the 2025 window for detailed project proposals (DPPs), which closed April 20.

“The transmission planning team is going to come in Monday morning, bright-eyed and bushy-tailed, and ready to start validating,” he said. “We’re anxiously awaiting those DPPs coming in.”

The 2025 study has completed its needs assessment but is in yellow status because the DPP submission window was extended. Hall said mitigation steps are being taken and staff are planning on-time approvals in the October MOPC cycle.

The 2026 ITP, which begins the transition into SPP’s Consolidated Planning Process (CPP) assessments, is also underway and developing its models. The 2027 ITP’s scope efforts should begin by late summer, Hall said.

Following the quarterly ITP update, MOPC endorsed a pair of motions recommended by the Transmission and Economic Studies working groups: scope changes that update the resilience language, and staging resilience projects. Those projects that also have economic, reliability, policy or operational needs will be staged based on the earliest need date identified; resilience-only projects will be staged as determined by model extrapolation and interpolation methodologies.

In other transmission-related issues, MOPC also:

endorsed a tariff change (RR673) that would eliminate a requirement to have met definitive interconnection system impact study (DISIS) requirements before submitting an interim service request. Instead, transmission customers can make that request when a DISIS open season is delayed.

accepted the Project Cost Working Group’s recommendation that 12 upgrade projects exceeding their estimated in-service date thresholds by more than 90 days be deemed reasonable and acceptable. Members also endorsed the baseline used to evaluate future in-service delays.

GI Queue Backlog on Track

SPP’s effort to relieve the generator interconnection queue backlog is on track, with four study clusters expected to reach the GI agreement stage in 2025, Natasha Henderson, senior director of grid asset utilization, told the committee.

Henderson said that while the 2017 and 2018 clusters are in the GIA stage, transmission customers in the 2022 cluster will receive their GIAs within three years of submission.

The key cluster is the 2026 DISIS, which SPP hopes will be the first of its CPP. The new study process is expected to be brought before MOPC in July and the board in August. Assuming timely FERC approval, it could be active in 2026.

“The timing actually aligns so that we can either open the 2026 DISIS, or those same generators could go into the CPP,” Henderson said. “Either way, this is the time frame in which we would anticipate opening the 2026 DISIS window [for study requests].”

She said the timing could also benefit members of SPP’s RTO expansion into the Western Interconnection, set to go live in April 2026.

Excluding the record 2024 DISIS (102 GW), SPP staff are currently studying 325 projects representing 65.8 GW. Solar, wind and batteries account for all but 10% of the queue. Henderson said 24 GW have GIAs but have not reached their commercial operations date; another 5 GW have CODs in 2025, she said.

More than 150 projects have already withdrawn from the 2021, 2022 and 2023 clusters, taking with them 33 GW of capacity. Those withdrawals can shift upgrades and associated costs. They will be reassessed in the next planned study.

SPP Waiting for FERC’s Response on Z2

SPP says a FERC response is imminent for its plans to resettle invoices for transmission upgrades under tariff Attachment Z2, a process that has bedeviled the RTO since 2016. (See “Grid Operator Waiting for FERC Order to Resettle Z2 Funds,” SPP Markets & Operations Policy Committee Briefs: Oct. 15-16, 2024.)

“We, as well as many parties, have asked for an order soon, sooner rather than later, because of the significant interest that is accruing on those Z2 refunds,” General Counsel Paul Suskie told MOPC. “We continue to work hard to be proactive and addressing issues, answering questions and providing information in a transparent way.”

Under Z2, transmission upgrade sponsors receive credits from any upgrade users whose service could not be provided “but for” the upgrade. The attachment also requires the RTO to invoice the charges monthly and to make any adjustments within one year.

However, software problems delayed the attachment’s final implementation for eight years before 2016, during which the RTO did not invoice for the upgrade charges. FERC approved a waiver request to settle more than 365 days in arrears, but in 2019, the commission reversed course and said SPP should have settled Z2 from only September 2015 forward. (See FERC Reverses Waiver on SPP’s Z2 Obligations.)

In January 2022, the grid operator filed with FERC an update to its proposed refund plan, submitted in 2019. SPP made an informational update to the commission in September 2024. FERC has made it clear SPP can’t process refunds without an order, Suskie said.

When the order comes, SPP plans to send out refund invoices with FERC interest for the March 2008-August 2015 operating days, accrued to the current invoice date. Once the resettlement system is deployed in about a year, invoices would be issued for the September 2015-January 2020 operating days. Additional resettlements from February 2020 would be run monthly in the current settlement system, along with normal current day Z2 settlements, until they catch up to the operating month.

“At this point, we’re waiting for a FERC order so that we can quickly issue the refunds and collect the money and issue the refunds, and then begin the process of building the models in the system so that we can start resettling 2015 to present,” Suskie told RTO Insider. “Once FERC gives us an order, we’re thinking it’ll take us about four years to resettle it.”

8 Tariff Changes

MOPC’s consent agenda included eight NPRRs that would:

RR658: prevent the uneconomic dispatch of demand response resources by creating an energy offer curve price floor equal to the net benefits threshold price for DR resources.

RR661: introduce a new “TCR model” definition in the transmission congestion rights (TCR) tariff language by clarifying the congestion-hedging team’s ability to adjust NERC-defined flowgates in the modeling process to match the day-ahead market topology and improve TCR funding.

RR662: remove Form EIA-411 from the Integrated Marketplace protocols.

RR663: develop inverter-based requirements based on reliability needs for SPP governing documents.

RR666: clarify deadlines for market participants submitting project-related data for commercial model changes and provide a commercial changes submission due date column.

RR667: add language clarifying that opportunity costs for hydro resources are excluded when obligations are imposed outside of the Integrated Marketplace. This does not include commitments ordered by a transmission provider or local transmission.

RR669: update the ITP Manual with SPP’s brand standards, correct small typographical errors and add consistent formatting throughout the document.

RR671: remove the annual violation relaxation limits analysis’ date requirement to create a more flexible timeline.

A panel of storage developers, regulators and RTO representatives discussed the roadblocks holding back the growth of battery storage installations in PJM during a meeting of the RTO’s Public Interest and Environmental Organization User Group.

Claire Lang-Ree, an advocate for the Natural Resources Defense Council and moderator of the April 16 panel, said storage presents an opportunity to work toward state environmental goals while also providing capacity at a time when PJM is signaling a possible shortfall in 2030. While batteries share a similar effective load carrying capability rating to gas generation, she said, they aren’t affected by a shortage of turbines and have one of the fastest development timelines of any resource type.

“Really if we need resources to come online and provide capacity quickly, battery storage is uniquely positioned to do that,” she said.

She said storage also could allow generators to deactivate without requiring reliability-must-run (RMR) agreements, which are triggered when reliability violations are identified should a resource go out of service. PJM traditionally has resolved those needs with transmission projects, which consumer advocates and environmentalists have said take years to complete, sharply increasing rates while the RMR agreement is in effect and keeping fossil generation online longer.

Increasing Capacity Prices Create New Market Potential for Storage

Convergent Energy COO Don Jenkins said high capacity prices in PJM’s 2024/25 Base Residual Auction have helped make batteries more economical. But the core challenge continues to be the amount of time it takes to get construction started.

“Where we really run into the biggest roadblocks or delays is that permitting or interconnection process,” he said.

CAISO Storage Sector Manager Sergio Dueñas Melendez said long-term bilateral capacity contracts also can give investors the stability needed to invest in storage development, which has helped fuel the growth of batteries in California. The state directed utilities to develop storage procurement targets and worked with the public utilities commission, CAISO and utilities to resolve roadblocks to getting batteries online.

While the approach in CAISO is simplified by its structure as a one-state grid operator, Melendez said there are several PJM members with their own climate goals, who can develop their own procurement plans or coordinate with each other.

Grant Glazer, MN8 Energy senior manager of regulatory and market affairs, said the uncertainty of future capacity prices can make it difficult to underwrite storage as projects increasingly look to target revenues beyond PJM’s ancillary service markets.

New Market Products Could Capture Unrecognized Storage Capabilities

Much of the panel centered around whether new market designs or products are needed to reflect the capabilities storage has to offer.

PJM Chief Economist Walter Graf said batteries offer valuable flexibility when ramping capability is needed, but the only lever dispatchers often have is out-of-market commitments. When uplift is paid to resources for those services, all other flexible resources — like batteries or demand response — that also provide those services are undercompensated for services they provide.

Glazer said MN8’s top market design priorities are allowing storage resources to include opportunity costs in their energy bids, a seasonal capacity market and new ancillary service products — namely uncertainty and ramping reserves.

When storage resources are mitigated to their cost-based offers, Glazer said they cannot include opportunity costs and therefore lose the ability to manage their state of charge. This can cause a storage resource to discharge once it becomes profitable, even if prices are expected to be higher later in the day. It also can expose them to potential capacity performance (CP) penalties if they discharge before anticipated periods of high-strain conditions begin and a performance assessment interval is initiated. He argued that both forgone energy costs and CP risk should be allowed in energy market opportunity costs.

Jenkins said this was on display in ERCOT on April 7, when batteries were deployed earlier in the day only for there to be a spike in prices later in the day associated with thermal generators going offline. Had there been a mechanism for price signals to storage and dispatchers to recognize there would be a jump in demand in the near future, he said the dispatch of those resources could be better optimized.

Melendez said CAISO has “mitigated the challenges of mitigation” by introducing a default energy bid that includes opportunity costs which considers the highest price of the day-ahead market, the duration of the resource and the potential revenues a battery could miss out on.

The hold exceptional dispatch instruction also allows CAISO to tell a storage resource to reach a certain state of charge and maintain that for future needs, including opportunity costs in the process. It has proved useful, but the growing number of resources is cumbersome for operators to manage, leading staff to explore how it can be streamlined.