While PJM experienced some of its highest peak loads ever during the late January winter storm, it overestimated load, with relatively high load forecasting errors, RTO officials told the Operating Committee.

PJM’s Paul Dajewski told the Operating Committee on Feb. 5 that while operations were strained during the Jan. 24-27 storm, named “Fern” by The Weather Channel, load did not quite reach the forecasted peaks and the RTO maintained reliability.

“We were able to operate through this period reliably; we did have sufficient generation reserves; we were able to serve our loads; we were able to serve our exports,” Dajewski said, adding that PJM provided emergency energy sales to neighboring regions.

PJM saw an instant peak load of 140,049 MW on Jan. 29 at 8:05 a.m. and two new top 10 hourly integrated peaks of 139,046 MW on Jan. 29 and 138,479 MW the following day. It noted that the data are preliminary.

Dajewski said there was a lot of uncertainty with preparing for the storm, owing to the duration of the freezing temperatures, pipeline flexibility, fuel storage, generators running into emission limits, load forecast accuracy, and the interplay between when gas resources are committed and when they purchase fuel from pipelines.

PJM asked that generators cut short maintenance outages between Jan. 25 and Feb. 2, reducing some transmission constraints. The RTO declared a long-duration extreme event, so fuel-limited resources were required to signal when they have 32 hours or less of fuel inventory, rather than the standard 16-hour notice.

The load forecast error was high between Jan. 26 and 29, peaking with an 8% over-forecast on Jan. 27. PJM’s Joseph Mulhern said temperatures were not quite as low as expected and that it’s possible the RTO’s modeling did not properly account for building closures. PJM said that it is difficult to predict the number of buildings that will close because of the weather, as the decisions are based on subjective, location-specific factors.

Stakeholders expressed surprise that building closures would contribute to load falling gigawatts below the forecast. Mulhern said PJM is exploring the issue further.

Transmission constraints and limited ramp capability drove $797.6 million in uplift costs, mostly in balancing operating reserve charges. There were $577.9 million in make-whole costs, $98.2 million in lost opportunity costs and $121.6 million in day-ahead operating reserve charges assigned. PJM is working on a more detailed breakdown of the make-whole costs for stakeholders.

Conservative operations were used to secure advance commitments, which PJM’s Brian Chmielewski said contributed to the make-whole costs. Pre-emergency load management was called in the BGE, Dominion and Pepco zones Jan. 25 for localized transmission constraints, and maximum generation, load management and low-voltage alerts were issued for Jan. 27.

PJM’s Brian Fitzpatrick said gas pipelines performed “very well,” with only one compressor station failing and 1,500 MW of generation interrupted. Winterization efforts on gas production appear to have led to a decrease in reduced output during winter events, with 5% production lost in Appalachia and 9% across the country. Nonetheless, spot prices were some of the highest he has seen, reaching $300/MMBtu on some interfaces.

Even with actual load coming in below forecast, Fitzpatrick said there was a lot of concern in the gas market about the duration of the storm, high loads and potential scarcity.

“That inherent fear in the market drove those prices,” he said.

PJM received Department of Energy waivers under Section 202(c) of the Federal Power Act to operate 39 units totaling 5.2 GW past environmental permit limits for 1,035 hours. The department also invoked a lesser used 202(c) provision to make backup generation available, but those units were not dispatched. (See Wright Ready to Use Emergency Powers to Dispatch Backup Generation During Winter Storm.)

PJM’s Joe Ciabattoni said the day-ahead bid period was extended on Jan. 26 and 27 because of issues running credit checks on market participants. It took longer for staff to accept bids because of the number of offers exceeding $1,000, triggering the automatic offer verification process.

A severe cold snap Jan. 16-21 preceded the storm, but it was much easier for the RTO to manage, with no emergency actions taken. The generation fleet performed well, and no emergency procedures beyond cold weather advisories or alerts were required. Load peaked at 135,121 MW on Jan. 21 at 7:40 a.m. with no load management deployed.

While all pipelines enforced the restrictions in their tariffs, there was no drop-off in production, and fuel remained available and relatively affordable for dispatched units. No advance commitments were made in preparation.

An offshore wind group has urged the California Public Utilities Commission to reject an internal proposal to use a forecast six-year delay to a Humboldt County offshore wind project to inform the state’s grid planning.

Representatives of Offshore Wind California (OWC) said the Humboldt offshore wind project’s online date in the forecast should be revised from 2041 to 2036, according to a Feb. 6 filing with the CPUC.

The projected six-year delay should be eliminated because offshore wind projects are moving ahead on the East Coast, despite Trump administration actions to attempt to hinder them, OWC said.

“Offshore wind is demonstrating its legal as well as business-case durability, even while under attack by the current administration,” OWC said in the filing. “Planning assumptions that doubt offshore wind’s ability to succeed do not reflect the prevailing legal reality. Nor do they capture the realities of steel in the water, which show eight projects are proceeding towards completion on the U.S. East Coast that will deliver more than 6 GW of clean power by 2027.”

Transmission planning often occurs over decades: The CPUC should not delay making important infrastructure decisions to react to what are likely to be short-term federal policy headwinds, OWC added.

California’s offshore wind projects will not need federal permitting for several years, so the Humboldt project could be online in 2036, the same time as the Morro Bay offshore wind project along the state’s central coast, OWC said.

The CPUC should eliminate the limited wind sensitivity case in the commission’s Jan. 14 proposed decision on the matter, OCW said. The group said the portfolio is “unreasonably conservative and unnecessary and directly conflicts” with California AB 525, which shows 25 GW of offshore wind generation by 2045, CAISO’s $4.6 billion in transmission investments to support offshore wind and the $475 million approved to upgrade port infrastructure for offshore wind.

The CPUC included the limited wind case portfolio due to recent increased difficulty of permitting wind projects and federal policy changes toward the projects, the commission said in the proposed decision.

Something strange is happening in American energy policy. U.S. Sen. Elizabeth Warren (D-Mass.) and Florida Gov. Ron DeSantis (R) are worried about the same thing: energy-guzzling data centers. Likewise, Sens. Bernie Sanders (I-Vt.) and Josh Hawley (R-Mo.) both seem to want an abrupt pause on new artificial intelligence.

Although the Trump administration favors artificial intelligence and data centers, many of the industry’s biggest detractors are sure to run for president in two years. And some states, including New York, are considering statewide bans on new data centers. Local opposition has long been a thorn in the side of data center development and is growing.

A clear political threat to the industry is brewing within both major parties and at all levels of government. What the industry needs is a hedge against bipartisan political risk.

Major tech companies, including Microsoft, Google and Amazon, have announced huge investments in generation assets. Meta announced in January that it would expand its nuclear power purchases by 6.6 GW. For reference, that’s more than three times the output of Hoover Dam.

These tech companies’ thirst for “juice” is apparent. But what if policymakers don’t want them on the grid?

Travis Fisher

In Warren’s recent announcement of an investigation, she and fellow lawmakers alleged that “American families bankroll the electricity costs of trillion-dollar tech companies.” In Florida, DeSantis and state lawmakers are proposing a new suite of regulations on data centers.

More than 230 groups — including environmental and consumer organizations — have called for a national moratorium on new data center construction. Dramatic headlines such as “AI Is Making Your Life More Expensive” are common.

It matters little that the political alarm over data centers is misguided. In fact, Warren’s assertions may be the opposite of the truth. As Nick Myers of the Arizona Corporation Commission recently explained in RTO Insider, data centers “provide long-term, stable demand that may reduce the financial risk of utilities and lower their borrowing costs to the benefit of all customers.”

Researchers have found the “effect of sales growth on rates is highly situation-specific” and largely depends on how new costs are allocated among customer classes. At best, it’s a murky policy area that lends itself to political scapegoating.

So, what can the industry do to protect itself from a populist uprising? One alternative is to allow new industrial customers to develop or join a private, fully off-grid energy system. My colleague Glen Lyons and I call this idea Consumer-Regulated Electricity, or CRE.

Going one step further than typical “behind-the-meter” arrangements with generators, CRE would enable a new, islanded system with no physical connection to the regulated grid. A data center could join many others on an industrial campus powered by whatever resources make sense — solar, batteries, gas turbines, nuclear reactors, you name it — and operate without connection to the utility grid.

Importantly, the lack of a grid connection also means freedom from political meddling. A new proposal by Sen. Tom Cotton (R-Ark.), titled the DATA Act, would exempt large users from regulation by FERC. Operating on a separate electric grid means no risk of causing blackouts for American families and businesses. Hence, the onerous regulations that apply to the “bulk power system” need not apply to independent facilities.

Like the Trump administration, today’s FERC is supportive of data centers and their hunger for electricity. However, the industry should be prepared for a one-two punch of reduced independence at FERC and a new president who wants to cut off electricity supplies to data centers.

For example, DeSantis recently said, “We have a limited grid. You do not have enough grid capacity in the United States to do what they’re trying to do.” If efforts to expand the grid fail or move too slowly — which seems likely — then the pitchfork mob might come for data centers.

States also can help enable the CRE option and insulate households from rising costs or uncertainty created by data centers. New Hampshire has taken the leap, and Ohio and Utah have enabled private electricity systems.

More states are likely to follow suit now that the American Legislative Exchange Council has approved model legislation that would create a path for CRE in any state.

A common critique of CRE is this: “We need AI data centers to help pay for the grid.” Yes, the blackboard economics view of grid supply tells us that retail rates should fall for everyone as the total watt-hours on the grid increase and grid utilization improves. But in the real world, risks abound, and no one can guarantee the AI bubble will never burst.

Indeed, the highly uncertain risk to American families of a sharp increase in their utility bills to pay for infrastructure intended for a collapsed data center industry may be unacceptable to some policymakers.

Far from a “libertarian fantasy,” private grids already are being built, and the data center industry should view policy reforms like CRE as a practical way to hedge political risk. Even if the value seems far-fetched today, why not establish CRE reforms now in case of a future political emergency? Data centers are not the villain, but it may be impossible for them to win the debate in a hostile environment, and the industry would be wise to protect itself against political warfare.

Travis Fisher is director of Energy and Environmental Policy Studies at the Cato Institute.

In Massachusetts, a state with some of the most ambitious decarbonization policies in the country, fundamental disagreements between utilities and consumer advocates threaten to derail the transition from natural gas before it even gets off the ground.

While technical in nature, these disagreements ultimately boil down to different visions of the role of the gas system — and the role of its utilities — in a decarbonized Massachusetts. With affordability already dominating energy politics throughout New England, the direction and effectiveness of the state’s transition could have major implications on consumer costs for years to come.

The arguments over the future of the state’s gas system are not new; many of the underlying disagreements date back to the Department of Public Utilities’ multiyear and at-times-controversial investigation into whether to maintain the system while decarbonizing the fuel, or transition completely away from it altogether.

Initiated in 2020 under Gov. Charlie Baker (R) at the request of then-Attorney General Maura Healey (D), the investigation highlighted the major differences in the strategies proposed by the investor-owned gas utilities and climate and consumer advocates.

Throughout the proceeding, the utilities promoted a strategy reliant on alternative fuels and hybrid electrification. This proposed approach would keep much of the state’s gas network in place to back up electrified heating while blending hydrogen and “renewable” natural gas (RNG) into the system to lower the carbon intensity of the fuel.

By contrast, climate advocates pushed for a full-electrification strategy. They argued that alternative fuels like RNG and hydrogen are expensive, scarce and ultimately non-viable for residential heating at a large scale, and that a hybrid electrification strategy would lead to excessive costs associated with building out the electric system while continuing to invest in the existing gas network.

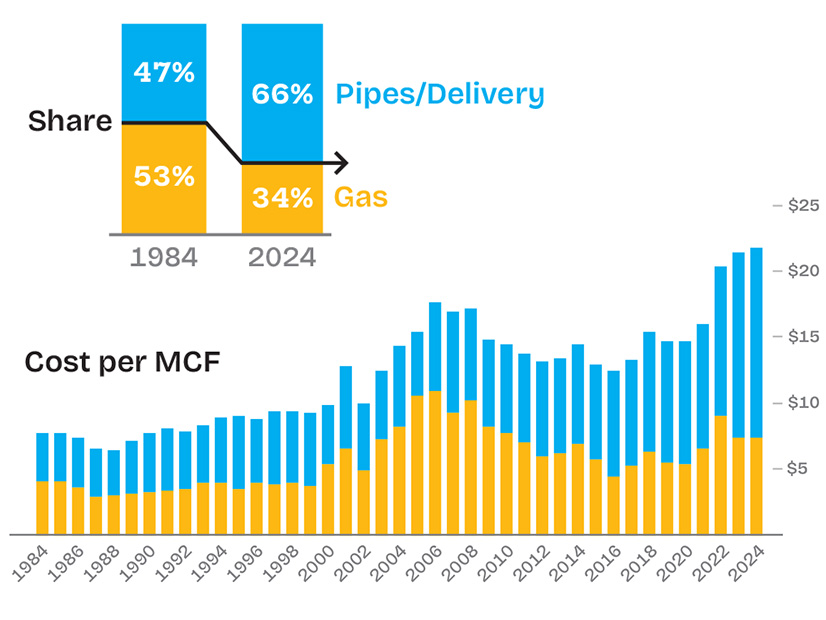

Residential gas delivery charges and supply costs in Massachusetts, 1984-2024 | Future of Heat Initiative

The DPU concluded the investigation in late 2023 under new leadership appointed by Gov. Healey, who took office at the start of that year. While climate advocates had criticized the DPU under Baker for relying on utility-hired consultants to conduct the technical analysis for the investigation, the department ultimately agreed with the advocates on the core issues.

With the order, the department established a regulatory framework “to move the commonwealth beyond gas and toward its climate objectives.” It expressed skepticism about the cost effectiveness of a “broad hybrid heating strategy” that maintained the bulk of the state’s gas distribution system. The DPU also declined to allow utilities to recover costs associated with procuring alternative fuels, citing concerns about “costs, availability and the treatment of renewable fuels as carbon neutral.”

The order required the utilities to file “climate compliance plans” plans every five years, evaluate non-pipeline alternatives when making gas system investments, cease promoting gas expansion with ratepayer funds and pursue targeted electrification pilot projects (D.P.U. 20-80-B). (See Massachusetts Moves to Limit New Gas Infrastructure.)

But in the two years following the landmark order, the conflicts that defined the DPU’s investigation have continued in the regulatory proceedings that have branched out from the ruling.

Across proceedings related to gas demand forecasting, pipe leaks, the climate compliance plans and the future of the region’s only LNG import terminal, the utilities have butted heads with proponents of the transition.

The utilities have been slow to embrace gas alternatives and pipe decommissioning at scale, which their critics attribute to the companies’ profit motive and reluctance to give up their traditional business model.

In contrast, the utilities have dug in on the language of customer choice, and they argue they lack the legal authority to decommission pipes without obtaining the consent of all affected customers. They argue that if a single customer on a pipeline segment is not willing to give up gas service, they cannot decommission the pipeline, even if electrified alternatives are available.

While advocates dispute this reading of state law, the question about the utilities’ authority to retire parts of the gas system remains unsettled, as does the underlying question of whether the state will ever be able to get its investor-owned utilities to embrace a transition away from gas.

The Obligation to Serve

According to the state’s gas distribution companies, their obligation to provide gas to existing customers stems from their franchise rights as regulated utilities.

“In exchange for a monopoly franchise, LDCs [local distribution companies] must actually provide natural gas service to customers absent the legislature rescinding their franchise charter or other clear legislative action alleviating the obligation to serve customers residing in a franchise territory,” the companies wrote in a joint filing in October in response to an inquiry by the department (D.P.U. 25-40, et al.).

In contrast, climate and consumer advocates argue the utilities’ obligation to serve does not prohibit the companies from substituting gas service for alternatives — such as networked geothermal or other electrified heating technologies — when viable alternatives are available. They point to a 2024 change in state law, which, according to its the lead senator in the negotiations, amended the obligation to serve to prevent issues related to holdout customers. (See Mass. Clean Energy Permitting, Gas Reform Bill Back on Track.)

The 2024 law directed the DPU to consider the public interest and the availability of non-gas alternatives for heating and cooking when ruling on petitions for gas service. It also explicitly authorized the department to “order actions that may vary the uniformity of the availability of natural gas service.”

The utilities argue that this change in law changed neither the “the legal foundation for the obligation to serve existing customers” nor the “obligations of the LDCs to existing customers.”

The Massachusetts Attorney General’s Office, the official ratepayer advocate in the state, disagrees. It argued in response that the DPU is well within its authority to authorize the disconnection of gas customers to advance the public interest.

With the 2024 changes to state law, “the legislature aligned the obligation to serve with the commonwealth’s climate goals by expanding the power of the department and articulating a balancing test to weigh the interests of the commonwealth with the interests of the individual customer,” the AGO wrote.

“It is illogical to suggest that the LDCs and department lack the authority to deny or discontinue gas service to promote the public interest in cost-effective decarbonization,” it added.

The DPU has yet to rule on the question of the utilities’ obligation to serve, and its interpretation of state law could face legal challenges from the utilities if the department ultimately sides with the consumer advocates. The potential impacts are substantial.

“It’s a very important issue,” said Jamie Van Nostrand, who led the DPU from 2023 through fall 2025 and oversaw the department’s order on the gas decarbonization investigation. He is now policy director for the Future of Heat Initiative. (See Outgoing Mass. DPU Chair Van Nostrand Discusses Gas Transition.)

Under the utility interpretation of the statute, “it’s all about customer choice, and if the customer wants to keep their gas, end of discussion — no decommissioning,” he said. “That is a bad outcome, because we need to have a managed transition.”

Stranded Assets

A managed transition, Van Nostrand said, is essential for long-term energy affordability in the state. Since leaving the DPU in the fall, he has been vocal in the ongoing affordability debates in the state, raising the alarm about the trend of increased spending on gas infrastructure.

According to an analysis by the Future of Heat Initiative, gas utilities in the state more than doubled their assets between 2014 and 2024, significantly increasing customer costs despite a 22% decline in per-customer gas demand.

“If you can’t shrink the system as the throughput goes down, delivery charges go through the roof; it’s simple math,” Van Nostrand said.

A large portion of this spending has occurred under a state program that gives the gas companies expedited cost recovery for replacements of leak-prone pipes. The costs of the Gas System Enhancement Plan (GSEP) program have risen rapidly in recent years, totaling $814.4 million in 2024. In total, the utilities spent more than $4.7 billion through the program between 2015 and 2024.

In an attempt to rein in the spending, the state has made several amendments to the GSEP statute in recent years to increase emphasis on pipe relining and repair, along with non-pipe alternatives, including networked geothermal.

But despite the efforts to curb spending and prevent stranded assets, costs have continued to rise, and traditional pipe replacements continue to constitute essentially all GSEP projects.

According to the utilities, the rise in GSEP costs is the result of the effects of inflation and supply chain constraints on the prices of materials and labor. In a written response to questions, Eversource Energy, one of the two major gas utility companies in the state, wrote that it already has replaced the bulk of the most accessible pipes and that its remaining portions of leak-prone pipes tend to require more complicated and expensive construction.

The company said an increased focus on pipeline repair would not help limit costs, writing that “there is no viable method for ‘repairing’ leak-prone infrastructure in a manner that obviates the need for replacement or that achieves the level of public safety that is achieved through replacement.”

“Prioritizing repairs over replacement can lead to higher longer-term costs, as sections of leak-prone pipes will likely require multiple future repairs and ultimately be replaced anyway, at which point the cost of replacement will have likely increased,” it added.

Van Nostrand did not dispute the underlying economic conditions, but he did highlight the attractive financial proposition to the utilities of expedited cost recovery, as well as the regulatory incentive structure that enables the utilities to earn more money from capital investments than from operating expenditures.

“Utilities are going to respond to whatever mechanism the regulators put in front of them,” he said. “They have a fiduciary obligation to shareholders to maximize profits, and that’s what they’re going to do.

“It’s great for shareholders to replace [pipes]; it’s bad for ratepayers. If your state has an aggressive greenhouse gas target like Massachusetts does — net zero by 2050 — putting a pipe in the ground that’s going to last 50, 60 [or] 70 years does not make any sense.”

He said expedited cost recovery on the GSEP investments has removed the important check on utility spending that regulatory lag provides in traditional ratemaking. This lag between when utilities increase their spending and when rates go up “provides a strong incentive for the utility to control costs,” he said.

In April, the DPU lowered the cap on GSEP spending from 3 to 2.5% of total firm service revenues and indicated it will likely cut the cap to 2% in 2026 and 1.5% in 2027. The cap reduction, coupled with a ban on carrying charges, is intended to limit the amount of spending for which the utilities can receive expedited cost recovery. (See Mass. DPU Aims to Align Gas Leak Program with Climate Strategy.)

While questions about the obligation to serve could inhibit the use of non-pipe alternatives instead of traditional pipe replacements, “the vast majority of these projects aren’t even getting to that point of having conversations beyond just the internal utility screening,” said Jeremy Koo, assistant director of clean energy at the Metropolitan Area Planning Council, a regional planning agency representing municipalities in the Boston area.

He said there is “definitely a lack of transparency” around why utilities have ruled out repairs and non-pipe alternatives for GSEP projects.

“We’re really concerned about it from the perspective of stranded assets,” he said, noting that the utilities’ approach appears to entail increasing levels of investment in both the gas and electric systems, with ratepayers left with the costs.

He added that he is similarly concerned that lower-income customers who lack the means to exit the gas system will become saddled with an increasing share of the gas system’s growing fixed costs.

Separate but Related

The utilities’ increasing investments in pipe replacement bears more than a few similarities to growth of asset condition costs on New England’s electric transmission system.

Asset condition spending, which is aimed at upgrading deteriorating transmission infrastructure, has cost the region $4.67 billion for projects placed in service since the start of 2020, according to an October update from the region’s transmission owners.

Eversource and National Grid, which own the largest gas utility businesses in Massachusetts and two of the three largest electric transmission footprints in the region, are responsible for the vast majority — $4.2 billion — of asset condition spending since 2020. Asset condition investments are subject to limited regulatory scrutiny, passing to ratepayers through FERC formula rates.

Concerns about the spending have caused the New England states to make a big push for increased oversight and transparency into the projects over the past several years, and ISO-NE is establishing internal asset condition review capabilities that could provide information for potential challenges of the spending with FERC.

But at a recent event held by the Northeast Energy and Commerce Association, Rhode Island Public Utilities Commission Chair Ron Gerwatowski said this might not be enough. He said the states may need to consider changing how transmission costs are recovered through electric rates.

To reduce the TOs’ appetite for spending, he said, the states could introduce regulatory lag by requiring them to recover costs through the full base rate case process, instead of as pass-through costs.

Echoing Van Nostrand’s comments on gas pipe replacement spending, Gerwatowski said subjecting asset condition spending to regulatory lag “could give the financial folks an incentive to push back” on the investments. (See Facing Rising Demand, New England has Limited Options for New Supply.)

‘A Very Expensive Insurance Policy’

As regulators eye a managed transition away from gas, the future of the Everett Marine Terminal (EMT), an LNG import facility just north of Boston, remains a multimillion-dollar question mark. Similar to the GSEP program, questions about the gas utilities’ obligation to serve could have a major bearing on the terminal’s future.

The LNG facility is on the site of the Mystic Generating Station, a retired gas-fired power plant that was once its primary customer. The plant retired in 2024 at the end of a two-year reliability-must-run agreement with ISO-NE.

To keep the EMT in operation following the closure of Mystic, the Massachusetts gas utilities signed contracts with Constellation Energy, the owner of the facility, to keep the terminal open into 2030. (See Massachusetts DPU Approves Everett LNG Contracts.)

In the DPU’s approval of the contracts, it acknowledged the importance of the facility to ensure the reliability of the region’s gas system during peak days, but it directed the gas distribution companies to take action to reduce their reliance on the facility.

The EMT is located at a strategic location at the heart of the state’s gas system, has access to both the Tennessee and Algonquin pipeline systems, and can feed directly into National Grid’s distribution network.

“That was a tough decision,” Van Nostrand said. “Basically, it’s a very expensive insurance policy.”

Gas customers in the state could face significant additional costs once the contracts expire if the utilities can’t eliminate their reliance on the facility.

Despite the regulatory requirements and a state-led working group focused on eliminating the state’s reliance on the facility, “another round of contracts seems incredibly likely,” said Carrie Katan, policy advocate at the Green Energy Consumers Alliance.

Katan, a member of the state’s Everett working group, said, “At this point, it does not look like either NSTAR [one of Eversource’s two gas distribution service territories] or National Grid are going to be able to basically function without EMT post-2030.”

A proposed expansion of the Algonquin pipeline system may cut some of Eversource’s reliance on Everett. The company’s recently approved firm transportation agreements associated with the expansion project would eliminate the need to extend the Everett contract for one of its service territories and partly eliminate the reliance on the terminal for its other service territory, Eversource wrote (DPU 25-133, 25-134).

But eliminating reliance on the terminal in one service territory could result in shifting the facility’s significant fixed costs onto gas customers in other areas still reliant on it.

It is also unclear what Constellation might charge to keep it open past 2030.

“Constellation is not operating on any kind of cost-of-service agreement: They can charge whatever price they want, and if they wanted to shut down EMT whenever they decided to, they could do that,” Katan said.

Van Nostrand concurred: “The LDCs put themselves in a position where they’re pretty much at Constellation’s mercy.”

Katan said National Grid appears to be in the “weakest negotiating position,” adding that “it really does seem to me that [Constellation] could decide to squeeze National Grid as hard as possible, and I don’t know of anything National Grid can do.”

National Grid declined to comment on whether it expects to seek additional contracts with Constellation. It said in a statement that its “responsibility is to operate a safe, reliable gas system for the customers who count on us, which requires making the investments necessary to keep aging infrastructure secure.”

Eliminating reliance on the Everett facility would require “a number of interventions, which would take a large amount of time,” such as strategic electrification or a moratorium on new gas hookups in EMT-constrained areas, Katan said.

But the utilities’ insistence that they cannot decommission lines without the consent of all customers complicates the picture.

While neighborhood-wide networked geothermal heating systems had drawn significant attention in the state in recent years, including pilot projects run by Eversource and National Grid, “if you want to deploy networked geothermal on a large scale outside of the pilots, you’re going to have to decommission the gas lines,” Katan said.

If the state cannot decommission pipes, “I don’t think we have anything when it comes to controlling gas costs,” she said. “I think at that point you would just need to accept that the situation is bad, it will get worse, and there is absolutely nothing that can be done about it.”

The PJM Operating Committee endorsed a set of manual revisions to implement ambient-adjusted line ratings (AARs) in compliance with FERC Order 881. (See “Manual Language to Implement AARs Endorsed,” PJM OC Briefs: Jan. 8, 2026.)

The changes to Manual 3: Transmission Operations, and Manual 3A: Energy Management System Model Updates and Quality Assurance, will create a system where temperature-adjusted line ratings are produced 248 hours out, including a buffer of eight hours to ensure compliance with Order 881. Monthly ratings also will be produced, which PJM’s Ryan Nice noted goes beyond the order’s seasonal requirement.

The changes are set to take effect March 4. Nice said any transmission owners with concerns about being prepared for the launch date should reach out to him.

Grid Security Drill

PJM’s Ed Figuli announced plans to hold the annual grid security drill Nov. 17, with invitations planned to go out in March. The drill focuses on cyber and physical security and is open to state and government agencies, in addition to PJM members.

MISO state regulators are considering asking the RTO to keep tabs on resource adequacy risk indicators as they contemplate crafting a replacement standard in the footprint.

During a Feb. 6 meeting dedicated to the topic, members of the Organization of MISO States (OMS) were clear they should preside over development of a possible new resource adequacy standard in the RTO. They proposed that MISO’s ongoing RA analysis could become a regular occurrence and help regulators decide when to substitute other benchmarks for the one-day-in-10-years loss-of-load standard.

MISO toyed with the idea of replacing or modifying the one-in-10 standard that its loss-of-load expectation study relies on. The grid operator suggested using conditional value at risk, loss-of-load hours or expected unserved energy as possible new measures of risk but has said it is not attached to any approach and is open to other ideas. (See MISO Dips Toes into Potential New Resource Adequacy Standard; States Demand Key Role.)

The RTO paused its formal work on a revised metric in 2025. Wisconsin Public Service Commissioner Marcus Hawkins said OMS expressed a desire for MISO to “tap the brakes and understand the topic more” before drawing up hypotheticals on different standards. He told fellow regulators that MISO is “waiting on us to steer the ship on this one.”

Hawkins said it is time to communicate to MISO what regulators might want to explore and “establish guardrails” that respect state jurisdiction over resource planning.

“There’s a potential if you change the resource adequacy metrics, that you change the requirements,” Hawkins said. “Because we encouraged MISO to pump the brakes … it’s now the time to collect our thoughts in a coherent way.”

MISO is working on gap analysis, which seeks to capture risks that the existing loss-of-load metric might be missing. OMS expects to review the RTO’s analysis later in 2026.

Over time, MISO expects risk to dwindle until it barely registers in the summer months, while winter mornings present challenges.

Werner Roth, economist with the Public Utility Commission of Texas, said OMS members need to examine what the gap analysis shows “five [to] 10 years from now.”

“Do we start to see a deviation as the resource mix changes?” he asked rhetorically.

He said state regulators must have the last word on which resource adequacy standard MISO pursues. “We need to have the ultimate say in that. Anything less would be unacceptable.”

Hawkins said OMS could direct MISO to continue tracking resource adequacy metrics from its footprint-wide vantage point so regulators know when they should change course on standards. The RTO would need to “produce a predictable source of information” that could potentially help regulators see risks that have not previously been obvious. He added that MISO would be creating probabilistic, forward-looking studies and said inputs into those studies should be well understood among regulators so there is no distrust and “we can have faith in the results.”

Bill Booth, a consultant to the Mississippi Public Service Commission, asked if OMS should secure a third-party consultant to serve as a check on MISO’s analysis results.

Hawkins said OMS could entertain the idea and that it has been in consultation with and gathering expertise from the National Laboratories. Representatives from some of the labs will appear at the organization’s Resource Adequacy Summit in May, he said.

“We sort of got a line of sight on some of those experts,” Hawkins said.

Hawkins also said OMS will be privy to other expert views because a new RA standard would be vetted through MISO’s Resource Adequacy Subcommittee. He said OMS members would benefit from the larger stakeholder community’s views.

WASHINGTON — The challenges and opportunities of meeting demand from new large loads like data centers took center stage at the National Association of State Energy Officials’ recent Energy Policy Conference.

“I think there’s an opportunity right now to think about how the transmission system can be enhanced while we’re going through this growth,” FERC Commissioner Judy Chang said Feb. 4. “So, there is an opportunity where when large loads come in, it can actually keep rates steady while we enhance the grid.”

Regulators could get it wrong and miss that opportunity, leading to higher rates for all consumers, she added. When large loads, potentially paired with their own generation, come online, they will trigger the need to upgrade the transmission system, and it is important that regulators get it right, she said.

Data center developers are flush with cash and have said they are willing to pay their fair share of incremental costs to serve their demand, which in FERC lingo is “beneficiaries pay,” Chang said. “So, beneficiaries should pay for the incremental cost of generation and transmission, but if they also are willing to support the system enhancement overall, it could put downward pressure, or at least leveling pressure, on the rates for all.”

The biggest item in front of FERC is the Advance Notice of Proposed Rulemaking from the Department of Energy, which asked the commission to assert jurisdiction over large loads to the transmission system.

Historically, states have always overseen the process of connecting new customers to the grid, and they might be putting in new processes, as the number of large loads and their speed-to-market concerns are new phenomena for the industry, Chang said.

“I’m still trying to understand that current practice and how this ANOPR will respect — I think that’s the best way to think about this — how to respect the current practices,” Chang said.

Maryland Energy Administration Director Kelly Speakes-Backman recalled that just a few days after she started her job, she received directions from Gov. Wes Moore (D) on working toward ensuring reliability and affordability in the state. (See Maryland Governor Issues Executive Order on Affordability and Reliability.)

“As a member of PJM … 40% of our power is imported from states like West Virginia, and so you can imagine that transmission is a very important issue for us that we are facing right now,” Speakes-Backman said. “Also, as a member of PJM, we’ve seen electricity prices just skyrocket.”

The executive order Moore signed in 2025 seeks immediate relief to the high prices in the short term, while connecting distributed energy resources in the medium term and building transmission in the long term.

West Virginia wants to be one of the sources of electricity being shipped over the transmission serving Maryland and other importing states in PJM, said Nicholas Preservati, director of the state’s Office of Energy. The state already has 40% more generation than it needs, which is exported to the rest of PJM, but load growth forecasts there mean it needs to build many more generators.

“You look at PJM, and they need 100 GW by 2050 to meet peak load,” Preservati said. Along with “58 GW coming offline by 2035, there’s a real problem that we see.”

West Virginia is home to 15 GW of generation, but its 25-year energy plan calls for it to get to 50 GW by 2050.

“People told us we lost our minds,” Preservati said. “But when you look at the need and PJM, someone has to do it, and we can’t do it all, but we’re going to try to step up.”

Federal Government’s Use of Emergency Powers

DOE has signaled it wants to stop all coal plant retirements and has used its authority under Federal Power Act Section 202(c) to effectuate that, said Melissa Birchard, director of the Georgetown Climate Center’s Mitigation Program.

“Imagine a state that is planning to replace an old, unreliable power plant with a new generator, perhaps as part of the utility’s integrated resource plan, perhaps consistent with the large load tariff,” Birchard said. “But if there is a 202(c) order in place that is repeatedly renewed, the state can’t transition the physical use of the site. The state can’t reduce costs for ratepayers by substituting a cheaper plant. They can’t free up interconnection capacity [and] grid capacity, which are extremely valuable right now, in order to put something more efficient and more reliable on the system.”

DOE has issued six such orders so far, but 23 more plants are scheduled for retirement in 2026, with pending retirements in May and others in August, October or December. Those retirements could lead DOE to issue more 202(c) orders to keep the plants open.

After the orders pausing coal plants retirements in Michigan and Pennsylvania, Indiana decided to work with DOE and explain which of its retiring plants made the most sense to keep open given load growth, said Jon Ford, executive director of the state’s Office of Energy Development.

“We had really gone through and analyzed all of our coal-fired plants and then provided DOE with a list that — if they were going to do this, here are our rankings of the units,” Ford said. “Schahfer was at the top of the list, [but Culley] was at the bottom of the list, so we’re not quite sure how they ended up picking” them.

Indiana also asked its utilities to seek grants and work with DOE, which is why Duke Energy decided to keep an existing coal plant running while it builds a natural gas unit, set for completion in 2031, at the same site, instead of at the older facility, he added.

The 202(c) orders came after President Donald Trump issued a Day 1 executive order declaring a national energy emergency, which has been renewed this year. Despite working for the administration briefly, Cato Institute Energy and Environmental Policy Studies Director Travis Fisher said he disagrees with the policy-by-executive-order approach.

“I don’t think governing by emergency is a good idea in general,” Fisher said. “I will happily eat my hat, though: This past 10 days or so have shown that sometimes that emergency authority is very helpful.”

Energy Secretary Chris Wright issued more traditional 202(c) orders during the recent winter storm, while also using the authority to let large customers offer their backup generation be available to meet elevated demand.

“There’s all sorts of novel applications that we can do, and some of them are scary. Some of them are terrifying,” Fisher said. “I’ve heard people talk about using 202(c) in a blanket nationwide fashion, to put a moratorium on coal plant closures. That’s obviously a terrible idea.”

Members of the Organization of MISO States have sent a letter to contradict aspects of NERC’s Long-Term Reliability Assessment, disputing the ERO’s label of MISO as being at “high risk.”

State regulators in MISO said NERC should have counted resources in MISO’s fast-track interconnection queue in assessment totals.

Organization of MISO States President Michael Carrigan, of the Illinois Commerce Commission, sent the letter to NERC CEO James Robb on behalf of “several” other OMS member states concerned about MISO’s designation in the LTRA. The letter was not considered a statement from the OMS Board of Directors.

Carrigan wrote that MISO’s generator express lane — “developed collaboratively by state regulators, MISO and stakeholders” — is well underway, “and it is expected to address emerging capacity needs in the near to medium term.”

MISO has more than 11 GW of natural gas generation and battery storage proposals in the first two cycles of its expedited interconnection queue that are set to come online by mid-2028. The grid operator will accept more projects throughout 2026. (See MISO Accepts 6 GW of Mostly Gas Gen in 2nd Queue Fast Lane Class.)

At a Feb. 4 MISO Advisory Committee meeting, OMS Executive Director Tricia DeBleeckere said OMS members aired concerns “most importantly because the report did not include” projects in the queue fast lane. She said the expedited generation should neutralize the 7-GW shortfall NERC expects to materialize in winter 2028.

NERC has acknowledged its model didn’t include MISO’s expedited generation proposals. It said if the projects arrive as promised, a projected reserve margin shortfall “would be eliminated.” MISO expects about 8.6 GW more of winter on-peak capacity to reach operation by 2028/29 through the expedited queue.

Per NERC’s assessment, MISO is due to experience a net loss in natural gas units by 2030. MISO’s queue fast lane is comprised mostly of natural gas-fired additions.

OMS continued to voice dissatisfaction with NERC conclusions at a Feb. 6 meeting dedicated to resource adequacy.

“MISO continues to be red. But we think there’s a lot of work in the region … that’s changing the trajectory,” DeBleeckere said.

She said MISO and members “have concerns over the outputs” and that OMS representatives have been in communication with NERC officials since the release of the assessment.

DeBleeckere said there’s a difference between MISO and members carefully crunching reserve margins and “heading toward a stop sign that we’re not going to stop at.”

She said she understands NERC must impose a cutoff on its data to begin working on the assessment.

“But this was such a big piece for us,” she said of MISO’s formation of the interconnection fast lane.

NERC’s inclusion of a sidebar in the report indicates NERC realizes the generator fast lane will mitigate risk, DeBleeckere added. She said MISO’s largely vertically integrated utility model would not allow “massive amounts of load that is un-resourced.”

OMS is meeting with MISO and NERC representatives to understand “the math that goes into the models that produce these results,” DeBleeckere said. She said NERC’s perceived risk of a shortfall by winter 2028/29 clashes with MISO’s summer-peaking conclusions from loss of load studies and that NERC’s interpretation might be one of an array that could be drawn.

DeBleeckere said there may be a “translation issue” between the way utilities plan their resources and how NERC draws its conclusions.

OMS believes there could be issues with the reference margin levels NERC uses in the LTRA, which assume risk only in summertime. NERC’s winter reference margin levels use a one-event-in-100-years assumption.

MISO uses varying seasonal requirements to account for risks. For the 2026/27 planning year, MISO found a slight loss of load risk in all winter months, leading it to use a 0.014 days/year risk — roughly equivalent to one day in more than 70 years — in its loss of load expectation study.

Interestingly, NERC determined MISO would maintain resource sufficiency in summers through 2029, even with an added 10 GW of load growth and a peak demand drifting upward to 138 GW.

Wisconsin Public Service Commissioner Marcus Hawkins said he wanted MISO, members and regulators to focus on the anticipated summertime performance.

“That is wildly impressive in this assessment, so I don’t want this to get lost among the concerns,” Hawkins said.

Bill Booth, a consultant to the Mississippi Public Service Commission, asked how results would be used and which outcomes they could influence.

DeBleeckere said beyond the report “hitting hard” in the press, the U.S. Department of Energy has used NERC assessments to justify keeping generation online in emergency 202(c) orders.

“It also can certainly work its way into state dockets,” Hawkins added.

Booth predicted reacting to the report would involve “damage control.”

‘Already Proactively Addressed’

Meanwhile, Carrigan noted in his letter that most utilities in MISO and state commissions coordinate to anticipate demand growth, retire generation and plan new generation through integrated planning approvals. He said reliability is handled “holistically” in MISO.

“[S]tate regulators, regulated utilities and MISO are actively engaged in identifying and mitigating evolving risks and have well-established tools to do so, as we have been doing for decades. Many risks highlighted in the assessment have already been proactively addressed in the MISO region, for example, by establishment of winter planning requirements,” Carrigan wrote.

Carrigan added that NERC treats planned retirements and load additions as certainties, while replacement generation is branded uncertain until the projects traverse regulatory, interconnection or market prerequisites.

“Utilities and regulators are aware of evolving system needs and have been, and will continue to be, actively engaged in taking corrective planning and regulatory actions to maintain reliability,” Carrigan wrote.

Carrigan said OMS’ well-established resource adequacy survey in conjunction with MISO often predicts shortfalls years down the road, similar to the LTRA. But he said the OMS-MISO survey’s “out-year uncertainty is a structural feature of planning-based jurisdictions and is routinely managed through coordinated utility planning, regulatory oversight and market and policy actions, well before reliability could be affected.”

Carrigan recommended NERC incorporate MISO’s longstanding planning processes and work from its collection of jurisdictions to moderate LTRA results. He said more balanced results could help dodge “disproportionate economic or policy consequences driven by out-year risk signals.”

“In MISO, the balance of state regulatory oversight, utility obligations and market mechanisms is intentionally designed to moderate risk and ensure timely corrective action,” Carrigan wrote.

Southern Renewable Energy Association Executive Director Simon Mahan said NERC’s “maps of doom” aren’t helpful and that MISO’s results in the assessment are “head-scratching.” Mahan said NERC’s inputs are outdated by the time it publishes the report, evidenced by the missing expedited resource additions.

“These maps are already being teed up in legislative hearings, regulatory filings and media articles as justification for: bypassing competitive procurement; fast-tracking utility self-build projects; locking in long-lived fossil investments; and sidelining lower-cost clean energy resources,” Mahan wrote in a reaction piece, adding that knock-on effects include rising gas prices and less-thought-out reliability.

“People make decisions based on NERC reports, even if NERC attempts to dissuade just that,” Mahan said.

In 2025, the MISO community similarly found itself at odds over NERC’s risk interpretation in its LTRA. In that case, MISO’s Independent Market Monitor criticized NERC’s conclusion and pointed out an error.

NERC had used unforced capacity values for MISO when calculating a margin that it ultimately compared to an installed capacity requirement. After a back and forth between MISO and NERC, the reliability corporation ultimately downgraded MISO from “high risk” to “elevated risk.” (See IMM: NERC Reliability Assessment Still Overstating MISO Risk.)

The New York Public Service Commission has issued new interconnection rules for distributed energy resource developers and utilities aimed at capturing as many expiring Inflation Reduction Act tax credits as possible for wind, solar and storage projects (24-E-0621).

Issued Jan. 22, the rules require utilities to develop schedules and plans for completing the utility-side work to interconnect DERs seeking tax credits.

The One Big Beautiful Bill Act, signed into law on July 4, 2025, terminated the IRA’s tax credits for wind and solar facilities going into service after Dec. 31, 2027. Under orders from President Donald Trump, the IRS established a deadline of July 5, 2026, for projects to have begun construction to qualify for the credits.

The IRS defined having “commenced construction” as developers having begun the physical work (whether on- or off-site) and having a continuous construction schedule. For small solar projects (1.5 MW and below), spending 5% of the cost of the project by the deadline satisfies the requirement. The IRS allowed for a four-year “safe harbor” allowance for construction delays outside the developer’s control, like natural disasters or work stoppages.

The PSC divided DER projects into two groups based on whether the project requires utility-side system upgrades. For those that do, the commission gave utilities some discretion in how they choose to schedule the interconnection work, so long as they meet the IRS deadline. Utilities must offer first-scheduling opportunities for developers who opt in to an accelerated procedure and must supply preliminary work plans for the upgrades by May 1. Developers must pay for their share of the upgrades by June 1. Final work plans must be published no later than July 15.

The PSC also implemented some comments from the utilities, adding deadlines for developer system upgrade payments to utilities. If a project is at risk of not making the deadline, the PSC authorized utilities to consider alternatives.

Taken together, “this approach improves the utilities’ ability to plan and deploy their engineering and construction resources to support tax-credit eligible projects, ahead of others that are not eligible,” the PSC said in a press release. “Today’s action also provides developers flexibility to manage the development of their projects as needed, while providing greater certainty that IRS in-service dates will be met.”

If Ørsted can continue to beat back the Trump administration’s interference, it could start generating electricity with its Revolution Wind project in a matter of weeks.

The 704-MW wind farm off the New England coast is 87% complete, with the export cables, interlink cable and both offshore substations energized, CEO Rasmus Errboe said Feb. 6.

The developer expects the facility to reach commercial operation and full power delivery to Connecticut and Rhode Island in the second half of 2026, barring further setbacks.

Errboe gave the update on Revolution and Ørsted’s other North American project, Sunrise Wind, during a fourth-quarter and full-year earnings presentation to financial analysts.

The Trump administration shut down work on Revolution in August and then shut down work in December on Revolution, Sunrise and the three other wind farms under construction by other developers in U.S. waters on grounds of preserving national security.

Ørsted won injunctions against all three stop work orders, but the shutdowns caused it to lose several weeks of work and take a $90 million impairment. And the injunctions are only temporary protection in the Trump administration’s campaign against offshore wind.

Ørsted began running into problems with its U.S. offshore portfolio in the form of soaring costs and logistical constraints well before Donald Trump was elected to a second term and followed through on his campaign-trail rhetoric against offshore wind.

The Denmark-based offshore wind market leader already has indicated it would undertake no further projects in U.S. waters but an analyst nonetheless asked Errboe during the conference call if he would be “interested in increasing your exposure in the U.S. market at all.”

He replied: “We have no expectations whatsoever to increase our exposure to offshore wind in the U.S.”

Errboe said Ørsted decided shortly after he became CEO in January 2025 to concentrate on wrapping up the two U.S. projects and refocusing its offshore attention on its core European market, plus select Asia/Pacific markets. Value is the priority, not volume.

The company retains its undeveloped wind leases in U.S. waters but has no plans for them, he said.

However, Ørsted still is engaged in onshore U.S. renewables development, which it set up as a separate business unit in October 2025.

“The business is going well, we are moving forward projects, we have right now roughly 500 MW under construction — one wind project, 260 MW, in MISO, and one battery, 250 MW, in ERCOT,” Errboe said.

“And then on top of that, we have 6 to 7 GW of capacity that meet the IRS qualifications through 2029, and we have this development portfolio consisting of mix of solar, wind and storage, slightly weighted more towards solar in the near term. So, moving forward well.”

Errboe said 59 of Revolution’s 65 turbines are installed and work is approximately 87% complete on the project, a joint venture with Skyborn Renewables.

Sunrise Wind, which will send up to 924 MW to New York, is 45% complete with 44 of 84 foundations installed, onshore and near-shore export cables installed, and fabrication completed of most remaining components. First power is expected in the second half of 2026 and commissioning is expected in the second half of 2027.

Ørsted is developing Sunrise alone. After Eversource departed the project, Ørsted sought an equity partner, but the actions of the Trump administration spooked potential investors to the point that the conditions they set for joining the project were untenable, Ørsted has said. (See Ørsted to Raise $9.3B, Self-finance Sunrise Wind.)

It has said Revolution and Sunrise will have a combined cost of approximately $16 billion.

Ørsted reported 2025 revenue of $11.6 billion, up from $11.2 billion in 2024; EBITDA of $3.6 billion, down from $5.1 billion; and net profit of $501 million, up from $2.5 million.