The U.S. Energy Information Administration is forecasting the highest power demand growth in a quarter century in 2026 and 2027, largely due to the proliferation of data centers.

The predicted 1 and 3% growth in 2026 and 2027 would be the first time since 2007 that power demand has increased four years in a row and would be the largest four-year increase since 2000, EIA said Jan. 13.

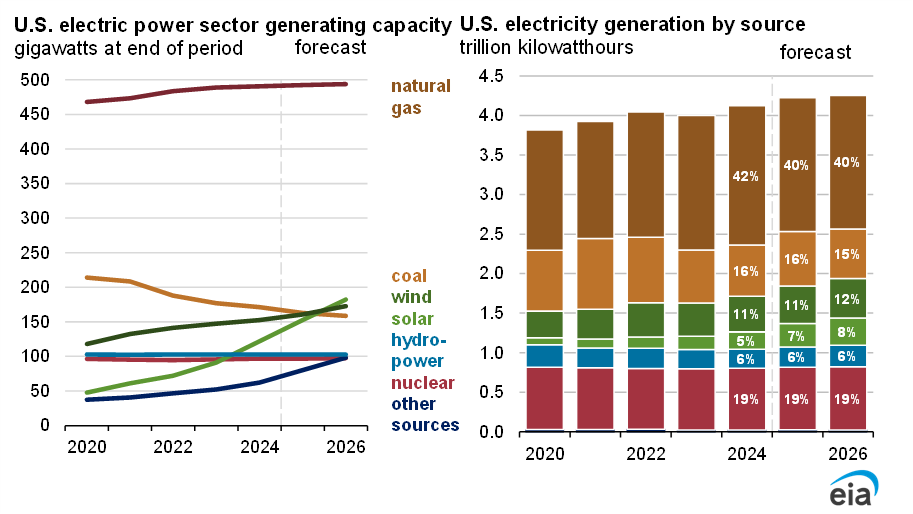

EIA’s January 2026 Short-Term Energy Outlook also projects that solar power output will continue its sharp growth, natural gas will provide a slightly smaller percentage of U.S. electricity and coal will resume its decline.

EIA predicts:

-

- Solar generation will increase by more than 20% in both 2026 and 2027, giving it 10% of U.S. power generation by the end of 2027, up from just 5% in 2024.

- Natural gas generation will be unchanged in 2026 and increase 1% in 2027; this gives it a 39% share of the power supply in both years, down from 40% in 2025 and 42% in 2024.

- Coal will provide 15% of U.S. power in 2026 and 2027, down from 17% in 2025 and 16% in 2024.

- Wind power will tick up from 11% to 12% of the power supply.

- Nuclear and conventional hydropower will hold steady from 2024 to 2027, with nuclear providing 18 or 19% of the nation’s power and hydro 6%.

- The benchmark Henry Hub price for natural gas will start to increase in 2027 on higher natural gas consumption in the electric power sector and growing demand for LNG exports, with three new export facilities coming online.

“U.S. energy production remains strong, and natural gas output is expected to grow to nearly 109 billion cubic feet per day this year,” EIA Administrator Tristan Abbey said in the news release. “Natural gas supply is critical as we forecast that U.S. liquefied natural gas exports expand and electricity demand rises through 2027, driven largely by increasing demand from large computing facilities, including data centers.”

The increases are a marked change from the early part of this century — EIA reports that U.S. electricity consumption increased by an average of only 0.1% per year from 2005 to 2020.

Other projections from EIA’s January outlook include:

-

- Power demand growth is being driven in part by data centers and other commercial users; as a group, they bought 2.4% more electricity in 2025 and are projected to buy 2.4 and 4.3% more in 2026 and 2027.

- The industrial sector, by contrast, is expected to see 1.6 and 3.4% growth in 2026 and 2027 after 1.7% growth in 2025.

- Total generation by the electric power sector increased 2.5% in 2025 to nearly 4,300 BkWh; it is expected to increase 1% in 2026 and 3% in 2027.

- The 4% decrease in natural gas generation and the 13% increase in coal generation seen in 2025 were both due largely to higher natural gas prices.

- Coal generation will decline 9% in 2026 and be nearly unchanged in 2027; even with deferred coal plant retirements, coal generating capacity is expected to decline by 13 GW — nearly 8% — over the two years.

- Nuclear power generation will increase 2% in 2026, largely due to the anticipated Palisades nuclear plant restart, but no change is expected in 2027.

- Wind power generation will increase 6% in both 2026 and 2027, even factoring in the uncertainty facing the offshore wind sector.

- Solar will hit 171.3 GW of installed capacity in the fourth quarter of 2026, finally surpassing wind (170.7 GW) as the leading U.S. renewable by nameplate capacity and becoming second only to natural gas (495.1 GW) among all forms of power generation.

- However, solar’s low capacity factor will leave it fifth among the six major types of power generation sources in 2026, providing 8% of U.S. power; only hydropower — 6% — will be lower.

{kind=link}