The Management Committee on Wednesday voted for NYISO to not conduct a new cost-of-service study to modify the Rate Schedule 1 cost allocations between units withdrawing and injecting.

The divided vote was previewed last month when NYISO announced stakeholders would have the opportunity to potentially change RS1 allocations, which have been set at 72% for withdrawals and 28% for injections since 2011. (See “Vote Set on Rate Schedule 1,” NYISO Management Committee Briefs: June 13, 2023.)

Some stakeholders opposed the motion and voted in favor of conducting the study, arguing that the allocations had not been updated in a long time and keeping things up to date was important because new technologies are entering the grid.

David Clarke, director of wholesale market policy at LIPA, argued in favor of conducting the study, saying, “we have put this off for a long time. … It is probably important to do this at least once a decade.”

On the other hand, Scott Leuthauser of Hydro-Quebec Energy Services argued against the study, saying, “it seems to me that nobody’s really opposed to the current values.”

“We have so many really high-priority projects that we’re not doing because resources are not available, so let’s just keep it for another year,” he added.

Howard Fromer, who represents Bayonne Energy Center, asked how distributed energy resources aggregations fit into these RS1 mechanisms.

Chris Russell, senior manager at NYISO, responded: “DER aggregations will be charged as a generator essentially,” adding, “these resources would be charged the injection rate similar to how we charge special resources cases today.”

Russell also said storage resources in an aggregation would be charged the prevailing injection rate whether it was injecting or withdrawing.

Erin Hogan of the state’s Utility Intervention Unit argued that these resource-related issues highlight the need to update the RS1 cost allocations.

The motion passed with 91.22% of the vote in favor of not conducting the RS1 study.

Board Selection Subcommittee

NYISO CEO Rich Dewey announced the ISO is forming a new board selection subcommittee to seek a replacement for Ave M. Bie, whose term ends in April.

Dewey said Julia Popova, chair of the MC and NRG Energy’s manager of regulatory affairs, will lead the subcommittee.

Bie is a former chair of the Wisconsin Public Service Commission and joined NYISO’s board in April 2009.

The Mountain Valley Pipeline’s Southgate extension asked FERC for a three-year extension to build the project after Congress passed a law pushing through the mainline of the project, which ran into protests in comments filed Monday.

The Southgate extension would run 75 miles from the end of the MVP Mainline in southern Virginia to central North Carolina, bringing natural gas from the Marcellus and Utica shale to Dominion Energy subsidiary’s Public Service North Carolina Energy’s distribution system. Equitrans Midstream Corporation owns 47% of the project, NextEra Energy 32.16% and AltaGas 10%.

Both pipelines were initially supposed to be done by now, but the Mainline has been tied up in litigation and that contributed to delays of the Southgate extension, which needs Mainline to be built so it can actually ship natural gas.

“The circumstances have changed,” the pipeline told FERC on June 15. “President Biden signed legislation that will expedite the completion of the Mainline System, which the United States Congress found and declared to be in the national interest.”

That filing came into FERC a few weeks before the pipeline’s opponents got the Fourth Circuit Court of Appeals to issue a stay on construction of the project as the court considers challenges to that legislation. The pipeline has asked Supreme Court Chief Justice John Roberts to overturn that stay, asking for a ruling by July 26.

The projects continued legal woes came up repeatedly in comments on Southgate’s extension request, with North Carolina Gov. Roy Cooper (D) telling FERC that the argument that more time is warranted because Mainline will be completed quickly is “clearly erroneous.” North Carolina has a law requiring a 70% cut in carbon emissions from the power sector by 2030 and carbon neutrality by 2050.

“Proponents of MVP Southgate have argued that the pipeline is needed for new electricity generation units,” Cooper said. “However, due to the requirements of Session Law 2021-165, any newly constructed natural gas fueled electricity generation units will be forced to retire before the end of their useful lives, leading to sunk costs that will be charged to North Carolina’s ratepayers.”

Cooper also argued that the pipeline is not needed for heating after the federal Inflation Reduction Act gave incentives for customers to move away from natural gas.

A group of several dozen legislators from North Carolina also urged FERC to reject the application, saying that the pipeline is not needed.

“There is no need for the gas MVPS is proposing to transport,” the legislators said. “Years’ worth of evidence points to how the developers overstated the demand for gas, and upgrades to existing infrastructure show increased available capacity substantiates the lack of market need for the MVP.”

Dominion Energy’s PSNC asked FERC to grant the extension, saying that it has added 100,000 customers in the past decade without any new supply. It signed a contract with MVP Southgate for a 20-year term of 300,000 dekatherms per day and a related 250,000 dekatherms per day from the Mainline Project.

“The project will provide geographic diversity of supply through access to Marcellus and Utica shale gas and will alleviate price swings that PSNC has experienced in the past,” the utility said. “MVP Southgate will improve reliability and add resiliency to the interstate pipeline services that PSNC receives and enable PSNC to gain optionality in selecting best-cost supply sources,”

Duke Energy urged FERC to grant the extension request, given that the litigation around the MVP project has been outside of its backers’ control and the commission issued similar extensions for the Mainline Project. Duke said the pipeline would help it secure fuel for natural gas power plants.

“The companies have experienced significant growth in natural gas demand for power generation and expect that trend to continue as the company retires its coal units,” Duke said. “Today, the Carolinas and the companies face a potential fuel security challenge that will be difficult to improve without completion of Southgate, which would allow increased physical gas deliverability into the Carolinas.”

New natural gas will help balance new renewables and is the least cost replacement for aging coal fired power plants, but they will require more pipeline infrastructure because the main pipeline serving Duke’s territory, Transcontinental Pipeline, is fully subscribed and constrained during periods of high use, especially during the winter.

“Increased pipe infrastructure allowing Appalachian Gas to flow into the Carolinas can play a key role in enabling the companies’ generation transition while supporting the communities and businesses that rely upon us for their energy needs today and in the future,” Duke said.

The Natural Resources Defense Council noted that the federal debt deal might have eased the federal permitting process for MVP, but it failed to reckon with market conditions that have changed since the pipeline was first proposed.

“Given national, state and regional commitments to move away from natural gas as an energy source in the coming years, combined with continued uncertainty around the fate of the Mainline system, the commission must reject Mountain Valley’s plea and deny the extension request,” NRDC said. “Denying this extension provides the commission with a logical imperative opportunity to demonstrate its commitment to a sensible energy future by refusing to saddle the public with another stranded asset inconsistent with statewide, regional, and federal energy needs, and ultimately the public interest.”

The firm effectively has stopped trying to get permits for the Southgate project, waiting for the litigation around Mainline to play out. It has failed to resubmit for a water permit in North Carolina, an air permit in Virginia, and it has halted all eminent domain proceedings.

“Mountain Valley has sat on its hands during the certificate period–abandoning efforts to secure crucial permits for the project, time and time again,” NRDC said. “These pending litigation- and permitting-related delays are entirely within Mountain Valley’s control.”

FERC requires that developers continue to work on their projects when it grants extensions, but in this case that has amounted to focusing on the Mainline Project, NRDC said.

Utility regulators from Oregon and California discussed their proposal for a new independent RTO covering the entire West for the first time publicly during Tuesday’s summer meeting of the Committee on Regional Electric Power Cooperation (CREPC).

The proposal was first described in a July 14 letter signed by regulators from Arizona, California, New Mexico, Oregon and Washington and sent to the chairs of the Western Interstate Energy Board (WIEB) and CREPC, which has become a forum for discussing Western market development. (See Regulators Propose New Independent Western RTO.)

Mark Thompson, a member of the Oregon Public Utility Commission and a signer of the letter, told CREPC Tuesday that the proposal originated from a desire to pursue the benefits of a full Western market and not see the West “fractured” by competing market proposals by SPP, CAISO and possibly others.

SPP and CAISO have offered competing day-ahead market proposals, and SPP is developing a Western version of its Eastern RTO, called RTO West, to compete with CAISO, which lacks independent governance. (See Western Day-Ahead Markets Debated at CREPC-WIRAB.)

“The idea was that perhaps we can form an entity in the West that would have independent governance shared across all states, and that the entity could eventually become the delivery arm for some of the programs that we already have through the CAISO, including the [Western] Energy Imbalance Market, perhaps the EDAM as well,” Thompson said, referring to CAISO’s proposal for an extended day-ahead market for the WEIM.

“Ultimately, that entity could create an independently governed full market opportunity for the West that all states could join, including California,” he said. “The vision would be that rather than fracture the market, let’s stand up another entity to at least be a vessel that can deliver a full market opportunity and that can have independent governance that all Western states could join in.”

Alice Reynolds, president of the California Public Utilities Commission, also signed the letter and helped develop the proposal, which she called an initial “invitation for all states that are interested to discuss and consider this concept.”

“I really do share the view that the fundamental driver of this working group idea and consideration of the concept is the recognition that customers across the West will benefit significantly from a West-wide market,” Reynolds said at the CREPC meeting. “As regulators, this is a common goal that we share — affordable rates, and increased Western cooperation can help us advance that.”

A June 2021 study found an RTO covering the entire U.S. portion of the Western Interconnection could save the region $2 billion in annual electricity costs by 2030 and cut carbon dioxide emissions by 191 million metric tons. Utah Gov. Spencer Cox’s Office of Energy Development led the study along with energy offices in Colorado, Idaho and Montana. (See Study Shows RTO Could Save West $2B Yearly by 2030.)

The WEIM has produced nearly $4 billion in cumulative benefits for participants since its founding in 2014, she noted.

“The discussion of a new concept, a West-wide entity with independent governance, really gives us an opportunity to build on this and to ensure that customers are getting the benefit of the full range of possible services and benefits that can be achieved through West-wide cooperation,” she said.

Others who signed the letter included Washington Utilities and Transportation Commission members David Danner, Milt Doumit and Ann Rendahl; Oregon Public Utility Commissioner Letha Tawney; Arizona Corporation Commission member Kevin Thompson; Pat O’Connell, chair of the New Mexico Public Regulation Commission; and Siva Gunda, vice chair of the California Energy Commission.

“We have identified a common commitment in seeking the benefits shown in multiple studies that demonstrate the most favorable electricity market for consumers is one that includes a West-wide market footprint,” the letter said. “Such a market would avoid the issue of ‘seams’ from separate markets across major portions in the West and result in optimized use of resources to meet loads across the entire interconnection.”

The new entity could contract with CAISO as a regional transmission operator and assume control of the WEIM and EDAM, it said.

‘Larger Conversation’

CREPC allotted 20 minutes for the presentation by Reynolds and Thompson and a brief question-and-answer session.

One question was whether the Canadian provinces in the Western Interconnection could join the RTO.

“I don’t see any reason to limit it to states,” Reynolds said. “We need a collective term that’s broader” than a Western RTO.

Utah Public Service Commissioner John Harvey asked about the potential costs of establishing a new entity.

“I’m an economist by training, and I’m curious and worried about the idea that if a whole new entity is created, you’re adding a tremendous amount of transaction costs,” Harvey said. “Just looking at CAISO or SPP, there’s a huge infrastructure there to try and settle these markets and determine the pricing and settle the accounts. Duplicating that again could burn up a lot of those benefits.”

He also said states with lower energy costs might not want to join an RTO.

“They would tend to say that the EIM and the day-ahead market give them the opportunities they need, and they don’t really see much benefit to moving beyond that,” he said.

Reynolds replied, “I think that’s part of the conversation that we want to have around this concept. If states are feeling like, ‘Well, wait a minute, we’re good with EIM and EDAM,’ then that’s certainly relevant to next steps.”

To Harvey’s first question, she said, “the idea of this is not to add costs, but to take advantage of investments that have already been made and then build on those.”

There was not time to answer questions from other participants.

CREPC Co-Chair Megan Decker, who is also chair of the Oregon PUC, said the committee would convene a follow-up meeting.

“It seems to me this is something where CREPC could convene a larger conversation to answer some of the questions that we didn’t have time for in 20 minutes today,” Decker said.

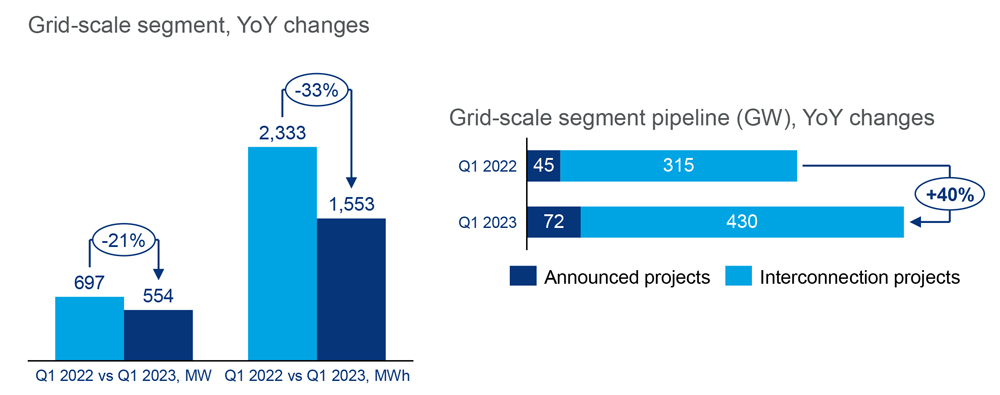

New solar power surged to record heights in the U.S. in the first quarter of 2023, while energy storage slumped because of a major jump in the already-high number of megawatts sitting in interconnection queues across the country, according to recent reports from industry analyst Wood Mackenzie.

Solar had its best first quarter in the industry’s history, with installations of 6.1 GWdc, up 47% from a year ago, according to Wood Mackenzie’s latest Solar Market Insight report for the Solar Energy Industries Association. Further, solar accounted for 54% of all new generation on the grid in the first quarter.

Drivers for the year-over-year growth include a loosening of supply chain constraints, with a wave of formerly delayed projects being completed, and a rush of first-quarter residential installations in California ahead of the state’s new, lower solar compensation plan, called NEM 3.0, which went into effect April 15, the report says.

At the same time, the full impact of the solar tax credits in the Inflation Reduction Act has yet to really affect the market as installers continue to work through the Internal Revenue Service guidelines that have been issued to date. For example, project developers can get add-on credits for locating projects in “energy communities” — such as areas that have lost employment because of coal plant closures.

The IRS guidelines for the add-on credits are complex and still being issued, the report says.

Storage, on the other hand, added a modest 778 MW/2,145 MWh in the first quarter, down 26% from the fourth quarter of 2022, as reported in Wood Mackenzie’s Energy Storage Monitor for the American Clean Power Association.

The amount of storage sitting in interconnection queues soared 40% year over year in Q1, as installations fell 21%. | Wood Mackenzie

Year-over-year figures in the report are divided by sector, with grid-scale storage taking the biggest hit, declining 21% from Q1 2022, installing 554 MW this year versus 697 MW a year ago. The culprit here is the 40% increase in the new storage capacity added to interconnection queues, the report says, growing from 315 MW in Q1 2022 to 430 MW this year.

The report also notes that more than 1.8 GW of storage projects scheduled to come online in the first quarter have been delayed to later in the year.

Additions came from a 119% increase in the commercial and industrial sector, from 31.6 MW last year to 69.1 MW, and a smaller 7% gain in residential storage, from 145.1 MW to 155.4 MW.

The storage tax credits in the IRA are proving a mixed blessing, the report notes. While lithium-ion prices are down, to get the law’s full 30% tax credit, developers have to meet its requirements for prevailing wages and apprenticeship programs, which are raising labor and other costs.

Big Growth Ahead

Growth in solar and storage markets is seen as critical for President Joe Biden’s goal of decarbonizing the U.S. electric grid by 2035. While the uneven first-quarter results may cause some uncertainty, Wood Mackenzie still expects exponential growth for both sectors.

Solar capacity is expected to nearly triple over the next five years, from 142 MW to 378 MW. In addition, the IRA’s domestic content provisions — which link tax credits to panels with U.S.-made components — have spurred a growing list of announcements of new panel manufacturing in the U.S.

By the end of the first quarter, Wood Mackenzie was tracking 52 GW of new facilities that had been announced, with at least 16 GW under construction. The challenge for the sector is that even if assembled in the U.S., solar panels may not meet the IRA’s domestic content provisions, as manufacturing for other key components will likely lag, the report says.

“There is currently no silicon solar cell manufacturing located in the U.S., and these facilities take at least two to three years to build and ramp up production,” the report says. Only 20 GW of new cell manufacturing facilities have been announced since passage of the IRA, significantly less than the new solar panel capacity already announced, the report says.

Wood Mackenzie is also anticipating a drop in the California residential solar market — with a knock-on effect on national growth — because of NEM 3.0, which slashes the amount of compensation rooftop solar owners will get for the excess power they put on the grid.

While a backlog of installations in California will keep figures up in 2023, Wood Mackenzie expects residential installations in the state will drop 38% in 2024, reducing the national residential market 4%. Boosted by IRA tax credits, solar across other states is expected to grow 12%.

For storage, Wood Mackenzie predicts 75 GW of new capacity will be installed by 2027, up from the current figure of just under 11 GW. More than 80% of the new capacity will be utility-scale storage, the report says.

The growth may start slowly, with supply chain and interconnection roadblocks affecting the market this year and next, but will accelerate to make up for such delays in the following years, the report says.

WASHINGTON — Leah Ellis is not worried about building demand for the low-carbon process she has developed for making cement. The CEO of Massachusetts-based Sublime Systems says she has a healthy pipeline of prospective customers waiting to buy the company’s product, made with an electrolyzer powered by wind and solar, rather than the traditional, high-heat, high-emission kiln.

“The demand for low-carbon cement is phenomenal,” Ellis said during an interview at Wednesday’s Clean Industrial Summit, sponsored by the Clean Air Task Force and ClearPath Foundation, both nonprofits focused on reducing greenhouse gas emissions. Sublime has a pilot plant up and running in Somerville, Mass., and potential customers are often more interested in how much of the company’s high-performance cement they can get than the price.

“They do ask about price, but I think it’s just not one of the first questions that people ask me,” she said. “Understand, you’re not just buying a ton of cement; you’re also buying the carbon avoidance.”

Ellis was just one of the startup executives at the summit, talking about the potentially game-changing technologies they are bringing to market, all aimed at upending conventional wisdom about heavy industry and its notoriously hard-to-abate greenhouse gas emissions.

Antora Energy, a California based startup, has developed a thermal storage technology that allows wind and solar energy to be stored at high temperatures — as high as 1,500 degrees Celsius — to provide heat for industrial processes. The company is targeting steel and cement as early markets, said CEO Andrew Ponec.

“This product has the potential to strike right in the heart of industrial emissions,” Ponec said. “It can serve almost every industry at any temperature range that’s used widely [and] any geography that has wind and solar at scale.”

The company’s investors include the Bill Gates-funded Breakthrough Energy Ventures, Lowercarbon Capital and Shell Ventures.

Historically dependent on carbon-intensive processes, heavy industry — including cement, iron and steel, and petrochemicals — accounts for 23% of U.S. greenhouse gas emissions, according to EPA. While transportation (28%) and electric power (25%) are the country’s top emitters today, industrial emissions are projected to jump into the No. 1 spot by 2035, according to the Rhodium Group.

The Department of Energy has made industrial decarbonization a priority, with a series of reports and funding opportunities, such as the Industrial Heat Shot, which is supporting research into new technologies that can cut industrial heat emissions by 85% by 2035.

Early research-and-development funds from DOE’s Advanced Research Projects Agency-Energy (ARPA-E) were essential for both Sublime and Antora, their CEOs said.

But, while promising, these new technologies may not be able to scale fast enough to meet the decarbonization goals of industrial giants such as Cemex, a multinational cement company with plants in seven states in the U.S., said Jerae Carlson, the company’s senior vice president for sustainability, communications and public affairs.

What’s technically feasible may not be economically feasible for “each and every one of our operations,” she said. And the new technologies like Sublime’s and Antora’s may take a long time to scale.

Many companies in the industrial sector have committed to cutting emissions and reaching net zero by 2050, but David Crane, DOE’s under secretary for infrastructure, says that’s not fast enough.

Crane said most of these businesses are approaching decarbonization with a four-step strategy. Efficiency and electrification are first and second, respectively, both over the next decade, followed by efforts to tackle industrial process heat in the mid-2030s and 2040s and some form of carbon sequestration for any residual emissions.

Crane is also focused on industrial process heat. “Our goal is to break that third step, which is where government can play a role because it’s the hardest step to change the mentality of both producers and buyers,” he said. “If you think you have to wait around till 2035, you won’t be a leader in your industry.

“The federal government is going to use every power at its disposal” to push industrial decarbonization forward, he said, from DOE programs, such as its $7 billion initiative to stand up regional green hydrogen hubs, to procurement.

“The government directly or indirectly pays for 50% of the cement used in the United States,” Crane said. “Now, how do you translate that into sending a market signal that we want green cement? That’s something we’re still working on.”

Melissa Carey, head of climate policy and government affairs for Holcim, a building materials multinational, acknowledged her company’s decarbonization strategy hews closely to Crane’s description.

“We do efficiency. We do carbon capture. We plant trees,” Carey said. “It’s unfortunate but true, in a sense, because we know what we need to do. We need to be able to do it faster.”

The key roadblocks to Holcim’s decarbonization plans are what Carey called “enabling conditions.” The company has ordered 200 of Ford’s F-150 Lightning electric pickup trucks but so far has received only one.

Reviewing plans for carbon capture at the company’s largest cement plant, Carey recalled asking, “How much does the timeline depends on funding and technology availability? And the answer was ‘completely.’

“If we can’t get more transmission built, then we can’t get more renewable energy,” she said. “We have 13 cement plants and zero pipelines right now to connect any captured CO2 to storage. … Where we’re really focused now is having later plans on trying to spur some of these enabling conditions so that we can do what we want to do as fast as possible.”

Cemex is looking to alternative fuels — such as bioenergy and renewable natural gas — to power its high-temperature kilns, Carlson said. With plants that operate 24/7 at high temperatures, the company would like to tap into waste streams as a source for bioenergy that can meet its need for tightly scheduled operation.

But, Carlson said, “the regulations around waste management here in the U.S. are not nearly as cohesive at a rural level, and then you also have to deal with state and local issues.”

While “focusing heavily” on carbon capture, Cemex’s “goals for 2050 … do not rely on known, proven, viable strategies right now,” she said. “We know we’re going to have to rely on innovations that we haven’t even conceived of yet.”

The steel industry has already cut its emissions, with a heavy reliance on the use of recycled steel as feedstock for steel production. “About 70% of the steel made in the United States is actually made through a recycling process,” said Kevin Dempsey, CEO of the American Iron and Steel Institute, an industry trade group.

Companies also are shifting from coal to natural gas to produce the high heat needed for purifying iron ore, a key step in making steel, and looking forward to possibly moving to clean hydrogen, when it becomes available, he said.

At the same time, Dempsey cautioned, “there’s not going to be a single way to get to [net] zero. All our companies are significantly committed to get to zero … but they’re pursuing a variety of paths, because our industry is very competitive.

The upside is that customer demand has become a major spur for innovation. “Frankly, demonstrating you can produce a clean product that can meet your customers’ needs is really one of the most significant driving forces in the steel market today,” he said.

‘Turn off the Tap’

As with steel, the quest for carbon-free cement is also drawing multiple innovators and new technologies. The industry has long been seen as one of the hardest sectors to decarbonize, with its reliance on a raw material, limestone and a high-heat process. Worldwide cement accounts for about 8% of all CO2 emissions.

At California-based Brimstone, CEO Cody Finke and his team have developed a chemical process for making cement from calcium silicate rock, a carbon-free rock that, Finke said, is 100 times more abundant than the limestone used to make most cement. The process also produces magnesium, which can passively absorb CO2, making Brimstone’s cement potentially carbon negative.

The company’s goal is to manufacture Portland cement, a building industry standard, that is both cost-competitive and carbon-free. Brimstone’s cement was recently certified to meet a key industry standard for Portland cement, ASTM C150.

To earn industry acceptance and scale quickly, “you need to use the [industry] structure that exists out there, existing trade unions and builders who know how to deal with the material,” Finke said. “If I have the option to build that building with the material we trust, the same material that we’ve always been building buildings out of … it’s hard to take the risk to build with a new material, even if the new material may be as good.”

Finke also said Brimstone’s process can be used “across a broad range of energy scenarios” and can be completely electrified. All of the cement the company has produced to date has been powered by electricity, he said.

Sublime is going another route, also using calcium silicate rock but producing cement that meets another ASTM standard, C1157, which is performance-based, CEO Ellis said. The standard is just as rigorous as C150 and has increasing acceptance across the industry, she argued.

When mixed with water, Sublime’s cement “sets and hardens to make the same concrete we’ve be using for millennia, but it’s not made in a kiln,” she said.

The company’s pilot plant has recently expanded its capacity from 100 tons of cement per year to 250, Ellis said. The first shipments of cement are being sent to customers for field testing.

Responding to Carlson’s comments on scalability, Ellis said the next steps will be to “optimize” the demo plant and then scale, to produce tens of thousands of tons of low-carbon cement per year as soon as 2025 and up to 1 million tons by 2027 or early 2028.

The cement’s strongest selling point will be its carbon-avoidance, as opposed to the carbon capture used by Brimstone and the multinationals, she said.

“We have to do everything as fast as possible to bend the curve of CO2 emissions,” she said. “I think of CO2 emissions as a leak from a tap, and you have water spilling out onto the floor. And in my opinion, the first thing you do is turn off the tap … avoiding the source of the emissions.”

As Antora CEO Ponec says, tackling industrial process heat lies at the heart of industrial decarbonization, and multiple solutions will likely be needed. But he and others emphasized that new technologies should not be forced on the market.

Nuclear developer X-energy decided to go small with its 80-MW small modular reactor (SMR), the Xe-100. Benjamin Reinke, director of global business development, said the design provides a flexible solution with both electricity and super high temperatures for process heat.

The company is one of two being funded through DOE’s Advanced Reactor Demonstration Program, with $1.1 billion to stand up its first reactors this decade; the other is the Bill Gates-founded TerraPower.

X-energy had originally partnered with Energy Northwest, a public power provider in Washington state, for its first deployment, but it announced in March it would instead be working with Dow Chemical, providing process heat and electricity to one of the company’s plants on the Texas Gulf Coast.

The Xe-100 is a high-temperature, gas-cooled reactor, which uses small “pebbles” of graphite-covered nuclear fuel and can produce steam for high-heat industrial processes, with temperatures of 750 C, or close to 1,400 degrees Fahrenheit.

Reinke said the Xe-100 can turn its power level up or down, like a natural gas peaker plant, and can be expanded as needed. For Dow, the company is planning to install four of its SMRs. It is also still working with Energy Northwest and recently signed a joint agreement to develop up to 12 reactors for a site near the utility’s Columbia nuclear reactor in central Washington. (See X-energy, Energy Northwest to Develop up to 12 SMR Nukes.)

“Two years ago, we thought for sure that the largest utilities in America would be the first to adopt advanced nuclear at [scale] because they had the most experience operating nuclear reactors,” Reinke said. “Today, what we’re seeing is that investors’ [environmental, social and governance] goals and requirements at various companies and their customers are driving a lot of heavy industry to decarbonize faster than many utilities have in their own projections. …

“We’re opening up a new market,” he said. “It changes the total addressable market for us and for many of our competitors … but we’re also leveraging that for additional learning and the ability to de-risk new technology coming to market.”

Ponec said Antora’s process has also been market driven.

“We were really looking for what would have the biggest impact,” Ponec said. Looking at industrial heat, he said, combining “that need to decarbonize with the incredibly low cost of variable renewable energy is so tantalizing. It was clear that renewables could do the job, if not for the variability.”

Finding a solution to that problem led to the development of the company’s carbon-based thermal storage technology, he said. “The way our system works is you take electricity from wind and solar when it’s available; you run that through resistive heating elements, just like a twister coil, to heat up carbon blocks to a very high temperatures, white hot, about 1,500 degrees; and then you continuously extract that … heat as steam.”

Further, he said, the materials in the storage unit are inexpensive and domestically sourced. “There aren’t a lot of barriers to scaling this up to the massive scale we need for rapid decarbonization,” he said.

The company has completed construction of a pilot plant and hopes to have its first systems online by 2025, he said.

While not naming names, Ponec said potential customers are looking at Antora’s combination of cheap renewables and thermal storage as a lower-cost source of industrial heat than natural gas by 2030. “At the point that you can start saying … you can beat the cost of … natural gas over a 10-year contract, that opens a market that is extraordinarily large,” he said.

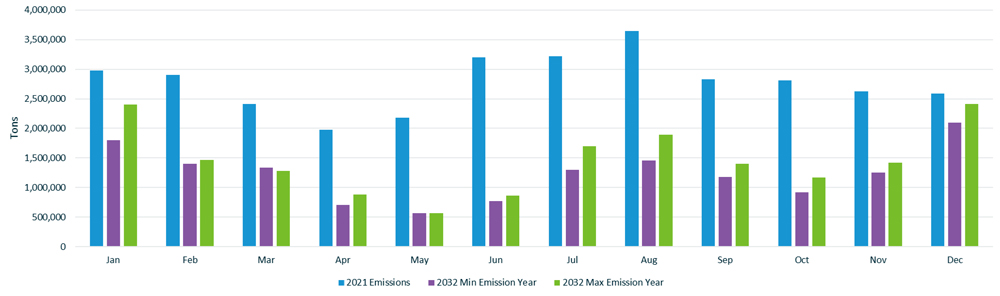

ISO-NE projects an approximate 47% decline in gas generation for the year 2032 compared to current levels but expects coal and oil generation to increase by 45% to meet winter peak loads, the RTO told its Planning Advisory Committee on Tuesday.

Despite the expected winter increase in coal and oil generation, ISO-NE anticipates emissions declining across all months by 2032, with the largest emissions reductions coming in the spring, summer and fall. ISO-NE projects annual emissions being nearly half of 2021 levels, declining from about 30 million tons of carbon per year to 16 million tons.

These findings are part of the RTO’s ongoing Economic Planning for the Clean Energy Transition pilot study. The study takes into account the increase in peak load due to electrification projected by ISO-NE’s 2023 Capacity, Energy, Loads and Transmission report. (See ISO-NE Increases Peak Load Forecasts.)

“Additional PV and wind resources beyond what is already in the model may help alleviate demand for dispatchable generation, but the needed volume of energy is significant,” said Benjamin Wilson of ISO-NE. “Some additional energy storage will likely be needed to shift the energy from when it is produced to when it will be needed.”

Wilson said the results indicate overall lower production costs and locational marginal prices due to the influx of zero-marginal-cost energy resources replacing gas generation.

“The system may experience an increase in reliance on stored fuels (LNG, oil, and coal) in the winter despite the new wind, solar and energy storage resources,” Wilson added.

The results contain limits: The study did not model generator outages and includes generators that did not receive capacity supply obligations in the latest Forward Capacity Auction and may retire prior to 2032. This includes the Merrimack Station, the last coal-fired generator in New England. The study also assumes continued operations of the Everett LNG import terminal for 2032.

Monthly emissions in 2021 compared to 2032 min and max scenarios. | ISO-NE

“A reduced LNG capacity would lead to an increased demand on other stored fuel resources,” Wilson said.

Transmission Planning

Also at the PAC, Dan Schwarting, manager of transmission planning at ISO-NE, presented initial high-level takeaways from the RTO’s 2050 Transmission Study, looking at meeting the transmission needs of the region for 2035, 2040 and 2050. ISO-NE expects a draft of the study to be ready to present to the PAC in November.

Schwarting told the committee early results indicate relatively small reductions in the projected 2050 winter peak load are associated with outsized reductions in transmission costs.

A 10% reduction of ISO-NE’s initial 57-GW winter peak “snapshot” for 2050—which represents the electrification of nearly all the region’s heating using existing technology—would be associated with a roughly one-half to one-third reduction in transmission costs, Schwarting said.

Despite uncertainty in predicting future load concentrations and generator locations, Schwarting said some high-likelihood upgrades could be pursued in the near term, including increasing capability for north-south transfer and Boston imports.

“Investment in addressing these concerns may be prudent regardless of exact generator locations and load distribution,” Schwarting said.

To meet the future needs for north-south transfers and Boston imports, Schwarting laid out four potential pathways: prioritizing rebuilds of existing lines, building new 345-kV overhead transmission, building new HVDC transmission lines or building an offshore grid that would enable power transfer between states and regions.

“In many parts of New England, addressing concerns by rebuilding existing lines for higher capacity is clearly more cost-effective and feasible,” he said, adding that using this approach to address all regional needs could end up being more expensive than the alternatives, and this path could not scale up to meet a 57-GW peak demand.

Schwarting highlighted some potential benefits of an offshore grid, including the ability to move power between interconnection points when capacity is not taken up by wind power.

“For example: In summer daytime peak snapshots, wind is assumed to be at 5% output. The remaining 95% of cable capacity is available to transfer power from one point of interconnection to another,” Schwarting said. “Beyond what is modeled in the 2050 Transmission Study, these grids could be expanded to include wind farms connecting to New York, PJM or other neighboring areas.”

Schwarting emphasized that providing a full cost/benefit analysis of an offshore grid is beyond the scope of the study, which will look only at approximate costs and a limited set of benefits.

“While significant research and development towards offshore transmission has been performed in Europe, meshed offshore HVDC systems are not yet in use commercially,” Schwarting added, noting the National Renewable Energy Laboratory is conducting a two-year study into Atlantic offshore wind transmission that will consider the potential for an offshore grid.

Asset Condition Projects

Eversource, National Grid, and Avangrid presented on several asset condition projects totaling over $100 million:

Eversource expects to spend about $31 million on structure replacements and optical ground wire installations on one 115-kV line and two 345-kV lines in Connecticut, citing age-related issues including woodpecker damage, cracking and splitting, and damaged insulators and deteriorated steel hardware. The expected in-service dates for the projects range from late 2024 to early 2025.

National Grid proposed spending about $6 million to replace five 69-kV and six 115-kV Oil Circuit Breakers at the Northboro Road Substation in Northboro, Mass.

Avangrid increased its cost estimate for its 115-kV Derby Junction to Ansonia Line Rebuild Project, proposing to spend $71 million to rebuild the line, nearly doubling the cost compared to its 2021 estimate of the rebuild. The company said the rebuild would extend the life of the line by at least 50 years.

The U.S. Department of Energy is proposing efficiency standards it says will save Americans billions a year on the operation of their water heaters and eliminate millions of tons of carbon dioxide emissions.

The proposal announced Friday would mandate heat pump technology in the most common-sized electric water heaters and mandate improved condensing and other technology in fossil fuel-burning units.

The department is mandated by Congress to make periodic updates in efficiency requirements; this is the 18th it has issued so far in 2023. The last update of water heater standards was in 2010.

The agency said it followed recommendations from two major water heater manufacturers, the Consumer Federation of America and a variety of stakeholders as it put together this new proposal. If adopted on the timeline DOE proposes, it would take effect in 2029.

Warming up water for household purposes accounts for about 13% of annual residential energy use.

The actual consumer benefit of the new standard would depend on the cost of fuel or electricity and on the speed of replacement of old technology with new. But DOE estimates that over the course of 30 years, the proposed standards could save Americans $200 billion and reduce CO2 emissions by 500 million metric tons.

That breaks down to a savings of $1,868 over the lifespan of an electric heat pump water heater compared with a traditional electric resistance unit, the department said. Further savings accrue with credits, rebates and other incentives offered through the Inflation Reduction Act.

The rule also would boost minimum efficiency ratings for tankless and storage water heaters that burn oil or gas, again by relying on technology improvements.

In total, DOE estimates the proposed rule would reduce energy used by water heaters by 21% and provide a $2.8 billion-a-year health benefit.

ALBANY, N.Y. — NYISO took stakeholder questions on its statement about the predicted reliability shortfall in New York City, during the Electric System Planning Working Group meeting on Tuesday.

“The short-term reliability need is primarily driven by a combination of forecasted increases in peak demand and the assumed unavailability of certain generation in New York City affected by the peaker rule,” read the ISO’s statement.

NYISO Reliability Studies Manager Keith Burrell explained the ISO was required by tariff Section 38.3.6 to explain why it was soliciting “a regulated non-generation short-term reliability solution solely from a responsible transmission owner,” which became necessary after its second quarter short-term assessment of reliably report identified that NYC could have up to a 446 MW marginal reliability deficiency by 2025. (See NYC to Fall 446 MW Short for 2025, NYISO Reports.)

“The reason the need observed in our Q2 STAR wasn’t observed in prior STAR reports was primarily due to the updated demand forecast,” said Burrell, referring to how planned fossil fuel plant retirements were included for the first time.

“We identified in our 2022 RNA [reliability needs assessment] that if demand forecast increased by as little as 60 MW there was the potential for a reliability need,” he added, “looking now at NYC forecasts, the demand went up by 294 MW when considering the baseline statewide coincident peak for estimated needs.”

Howard Fromer, who represents Bayonne Energy Center, asked if NYISO was measuring the need in MWs or MWhs.

Burrell responded, “it’s a little bit of both, when we identify a need it’s going to get the MW deficiency, but we also do some investigation to get an idea of what the hour of the need can be.”

Fromer then asked whether NYISO would entertain solutions that were less than the 446 MWs of identified need, and if some combination of regulated solutions would be considered.

“Ultimately, the solutions selected need to fully address the need but can come from multiple different options,” Burrell said. NYISO staff referred to Section 38.6.1 of the tariff to clarify what constitutes a viable and sufficient solution.

Mark Younger, president of Hudson Energy Economics, asked NYISO to further investigate statewide reliability shortfall scenarios, pointing out that the Q2 STAR also identified that at extreme loads the entire state could see marginal deficiencies. “It would be good to have some of these [scenarios] chased down before we finalize the next round of analysis,” he said.

Doreen Saia, an attorney with Greenberg Traurig, warned NYISO that whatever solution it chooses, “there are certain actions that can’t be undone,” referring to how decisions to decommission Indian Point nuclear power plant, in hindsight, seem regrettable given the state’s current reliability needs.

NYISO asked for any further comments or questions be sent to DeveloperSolution@nyiso.com before July 28. All notes will be posted online.

NYISO plans to post the third quarter STAR by Oct. 13.

NYC PPTN

NYISO also gave a status update to the ESPWG/TPAS on the public policy transmission need for New York City, which was called by the state’s Public Service Commission to deliver at least 4,770 MW of offshore wind from Long Island. (22-E-0633).

The PSC ordered another Zone J-to-K OSW transmission solution to help meet state energy goals like producing 9,000 MW of OSW by 2035, using the momentum that was built after NYISO’s board selected a project to fulfill the Long Island PPTN that called for at least 3,000 MW of export capability. (See New York PSC Calls for More Transmission for Long Island OSW.)

The NYISO has begun conducting baseline assessments for the NY PPTN to determine the actual need and what solutions are needed to meet that need. This process is followed by a 60-day window where developers can propose their own transmission solutions.

NYISO tentatively will start soliciting solutions in the first quarter of next year with the goal of the PPTN being completed by the third quarter of 2025.

NYISO promised it was actively coordinating with state agencies and other relevant parties, such as the Department of Public Service, Con Edison and the New York State Energy Research and Development Authority, in response to questions from stakeholders about the ISO’s engagement with these groups.

NextEra Energy on Tuesday discussed the continued growth of its renewable energy portfolio in a positive second-quarter 2023 earnings report.

Subsidiary Florida Power & Light placed 225 MW of new solar capacity into service in the quarter, bringing its total for the first half of the year to nearly 1,200 MW, while subsidiary NextEra Energy Resources added 1,215 MW of solar, 150 MW of wind and 300 MW of storage.

“As we indicated in our recent 10-year site plan, solar continues to be the lowest-cost alternative for our customers,” NextEra Energy Chief Financial Officer Kirk Crews said in a conference call with financial analysts.

The challenges surrounding solar power development in 2022 appear to have subsided, he added: “After a period of underlying commodity price inflation, supply chain disruption and trade policy risk premiums, we are finally seeing signs of stability.”

CEO John Ketchum said: “All those ’22 projects that got delayed into ’23 are now starting to go into commercial operation. That’s really good news.”

NextEra Energy has announced intentions to decarbonize its operations, and Crews said Tuesday that remains the plan.

“We believe renewables remain economically attractive to alternative forms of generation,” he said. “Today, we have a pipeline of roughly 250 gigawatts of renewables and storage projects in various stages of development. This includes projects in early stage diligence and our current backlog and is supported by roughly 145 gigawatts of interconnection queue positions.”

This last point is important, Ketchum said.

“I would challenge you to find anybody in the industry that has even close to that number of projects with interconnection capacity,” he told an analyst during the Q&A portion of the call. “Given the demand we’re seeing in the market, if you have a site ready to go with interconnection capacity, that’s the hard part. Finding the customer right now is not the hard part.”

NextEra Energy signed its first contract for a standalone battery energy storage facility co-located with a wind farm in the second quarter, Crews said, and expects to use storage to further monetize its 29 GW renewables portfolio.

Ketchum said this strategy change with storage is possible because of financial changes — investment tax credits under the Inflation Reduction Act — and because of market changes.

“We are starting to see an opportunity, particularly in MISO and SPP, in ERCOT, where capacity values and reliability are being priced higher than … we’ve seen them in the past, given some of the shortfalls that they have in those markets and that just happens to coincide with where most of our wind is,” he said.

Ketchum also emphasized that NextEra’s wind portfolio is not exposed to the highly publicized quality control problems afflicting some turbine manufacturers.

“We do almost all of our business with GE,” he said. “We have done a little bit with Siemens, and I know there’s been some press on Siemens recently. We don’t have any of the Siemens Gamesa turbines in our fleet. I just want to make that very clear.”

During Tuesday’s call, the executive team also discussed second-quarter financials for NextEra Energy Partners LP.

The company completed acquisition of 690 MW of wind and solar assets in the second quarter, pushing its renewable portfolio past the 10 GW mark, but it also ran into one of the limits of wind power: varying wind speed.

The second quarter of 2022 saw the strongest wind in 30 years, 112% of the long-term average. The second quarter of 2023 saw the weakest wind in 30 years, just 86% of the long-term average.

Adjusted EBITDA generated by existing projects declined by approximately $99 million, though new projects and other revenue canceled much of that loss.

NextEra Energy Partners’ stock closed down 4.07% in trading Tuesday. NextEra Energy stock dropped 0.19%.

The standards development team (SDT) revising NERC’s cold weather standard has more work ahead of it after industry respondents put the freeze on their latest proposed revisions with a negative segment-weighted vote of more than 56%.

The comment and formal ballot period for EOP-012-2 (Extreme cold weather preparedness and operations) — and its implementation plan — closed Thursday. The revised standard received 101 votes in favor from members of the selected ballot body, while 141 voted against it; 31 abstained, and 28 did not respond.

EOP-012-2 is intended to revise EOP-012-1, which FERC approved in February along with EOP-011-3 (Emergency operations). (See FERC Orders New Reliability Standards in Response to Uri.) Both standards were created by Project 2021-07 in response to the recommendations in FERC and NERC’s joint inquiry into the 2021 winter storm that nearly led to the collapse of the Texas Interconnection. They require generator owners (GOs) to implement several measures to prevent their units from freezing during extreme cold weather events.

In its order, the commission criticized EOP-012-1 for including “undefined terms, broad limitations, exceptions and exemptions, and prolonged compliance periods.” It directed NERC to clarify these issues while adding a deadline for completing corrective action plans and a shorter grace period for GOs’ implementation than the five years originally given. After the SDT for Project 2021-07 revised the standard, NERC’s Standards Committee approved its submission for comment and ballot in a special call last month.

Respondents Call Revisions Unclear

In addition to giving their approval on the overall standard, respondents also addressed the SDT’s questions about specific language and requirements incorporated into EOP-012-2. These included:

whether the proposed definition of generator cold weather constraints — technical, operational or economic limitations that would prevent GOs from implementing freeze protection measures — provided the clarity the FERC order required;

whether the standard meets FERC’s recommendation that GOs account for the cooling effects of precipitation in their temperature data; and

whether the two timeframes proposed in the standard for corrective action plans — 24 months for addressing existing equipment or freeze protection, and 48 months for implementing new equipment or freeze protection — are appropriate.

Responding to the first question, Thomas Foltz of American Electric Power said the proposed definition of “commercial constraint” still lacks clarity. The standard — which states that a commercial constraint exists when implementing freeze protection would result in the unit not being in service at the time of evaluation — leaves open the question of what utilities should do about equipment reaching the end of its life, Foltz said. That could leave utilities that decide not to implement expensive modifications on nearly retired units open to the accusation of “choosing economics over reliability.”

Foltz suggested revising the definition to include measures that “require unreasonably expensive modifications [or] significant expenditures on equipment with minimal remaining life.”

Regarding the requirement to account for precipitation in temperature data, Robert Follini of Avista said the standard would require utilities “simply … to perform a wind chill calculation, with an ambiguous 20-mph wind speed.” Follini pointed out that because “some regions or facilities are more protected from wind effects than others, and there is no direct correlation between extreme cold weather temperatures and wind,” the requested number likely would have little relevance to utilities’ practical winter preparations.

Finally, Donald Lock of Talen Generation objected to the timeframes for corrective action plans, saying “it is impossible to fully understand what it is that a generator owner is being asked to do at this time” because of ambiguity in the other requirements of the standard and the large number of generating facilities and units with which an entity might have to deal.

He said that while some of NERC’s other standards require similar timeframes, those typically refer to a much smaller number of units and a much smaller scope of action. Lock concluded that it isimply is not possible to say with certainty how long a retrofit campaign involving an entire generation fleet might take, and therefore the inclusion of such a requirement would be a mistake.