New Mexico is the best place in the U.S. for getting distributed energy resources (DERs) hooked up to the local distribution system, according to a new interconnection scorecard from the Interstate Renewable Energy Council (IREC) and Vote Solar.

The state is the only one that earned an “A” on the recently released Freeing the Grid scorecard, which is based on states’ adoption of key policies and best practices that can streamline approvals, increase efficiency and reduce costs for the interconnection of DERs.

“One of the great things about New Mexico is they had a very robust stakeholder engagement process … and they really overhauled the rules,” incorporating many of IREC’s recommended best practices, said Mari Hernandez, assistant director of regulatory programs at the nonprofit. New Mexico is also the only state to include provisions aimed at incentivizing and streamlining interconnection for projects that will benefit disadvantaged or underserved households, she said.

“That is something we wanted to signal is really important,” Hernandez said. “Our hope is to figure out more ways to think about equitable access and interconnection, and how to make sure we’re considering that within interconnection rules.”

Whether on transmission or distribution systems, interconnection ― the process for allowing new energy projects to connect to the grid ― has become a major bottleneck for solar, wind and storage projects. Freeing the Grid (FTG) grades all 50 states, D.C. and Puerto Rico on whether they have adopted jurisdictionwide interconnection policies and procedures that apply to all regulated utilities.

“Interconnection is fundamental to the clean energy transition,” Hernandez said. “So, we really believe that what’s included in interconnection procedures is a good indication of whether a state is set up to support clean energy growth.”

But according to the FTG scorecard, a majority of states aren’t adopting the necessary policies and best practices. Following New Mexico, only six states received a B ― Arizona, California, the District of Columbia, Illinois, Michigan and New York ― while 15 squeaked by with a C. A total of 30 were given Ds or Fs.

Those results indicate “real disarray across the country,” said Sachu Constantine, executive director of Vote Solar. “A lack of consistency, a lack of transparency, a lack of best practices across the whole country, and this comes at a critical moment when you look at what the [Inflation Reduction Act] is doing, what it’s signaling about the direction we want to go.”

The landmark legislation, signed into law last August, provides billions in tax credits for solar, wind and energy storage, both grid-scale and distributed, as well as manufacturing tax credits to support the build-out of domestic supply chains. The IRA also ensures many of these credits will be available through 2032, to provide certainty for the industry.

But, Constantine said, the impact of those dollars could be undercut “if we don’t have clear, transparent, useable interconnection standards.”

Freeing the Grid outlines 10 best practices, ranging from “rule applicability” — meaning that interconnection rules cover all distributed generation, including energy storage — to “dispute resolution” — that is, having a process in place to resolve disputes over the upgrades a utility may require a developer to make or pay for.

States are almost evenly split on the storage issue: 24 include storage in their interconnection rules, while 26 don’t. A similar gap appears on dispute resolution, where 28 states have a process for resolving disputes but only 13 require their public utility commissions or other entities to provide ombuds services to track and facilitate the dispute resolution process.

Uneven DER Landscape

Long and costly interconnection processes can delay or sink a DER project, particularly if a utility asks a developer to pay for millions of dollars in system upgrades. A recent study of storage interconnection processes found that in Massachusetts alone, more than 1,600 storage or solar and storage projects had either incomplete or withdrawn interconnection applications in 2022, versus fewer than 400 complete or approved. (See Report: Storage Projects Stymied at Distribution System Interconnection.)

The state received a C from FTG, partly because it does not include storage in its general interconnection rules.

Developing best practices to streamline interconnection of distribution-level solar, wind and storage is another point of resistance, especially from utilities, Constantine said.

“Historically, utilities have had to keep the lights on,” he said. “That’s all they really thought about, and modern technology, like these distributed technologies, kind of upset that paradigm a little bit because now other generators and different kinds of end users are trying to connect into this grid. There are some quality and inertia [issues], but they are operating to older standards and older practices.”

For example, only five states have adopted interconnection regulations that specify a date by which DERs must comply with IEEE 1547-2018, the industry standard for ensuring the safe interconnection and interoperability between DERs and utilities’ electric power systems.

The figures on other key streamlining measures also reflect the uneven DER landscape developers face across the country. Rooftop installations under 10 kW are eligible for a simplified review in only 17 states. FTG found only two states where projects can receive streamlined processing based on their export capacity, as opposed to their nameplate capacity.

Basing interconnection on export capacity can be critical for storage projects because some utilities base their evaluations of such projects on worst-case scenarios rather than on how they actually operate. While most storage projects charge during off-peak hours, a utility might require studies assuming they will only charge during high-demand peaks.

Constantine said he believes part of the problem is the gap between the speed at which technology is advancing and utilities’ traditional aversion to risk and change.

“Part of what we’re seeing in these grades is simply the time it takes for a utility to turn itself around,” he said. “Technology has caught up, and utilities are still trying to … understand that they can operate safely, that they can operate efficiently based on the technical capabilities of the technology that we’re deploying. …

“We’re 10 years on from the major ramp-up in the solar market, and we’re already several years into the battery era. We can’t really say with a straight face that we don’t know how these things are going to operate. We know how they are going to operate, and the standards ought to reflect that.”

A Higher Grade for Hawaii?

While state regulations provide an important benchmark, both Hernandez and Constantine acknowledge that FTG does not always capture the interconnection policies and practices of individual utilities, Hawaii being a major case in point.

FTG gave the state a C but noted that its “updated interconnection practices … have not been reflected in the state’s interconnection tariffs.”

Hawaii was among the first states to adopt a 100% renewable energy target — 2045 — and with its self-contained island grids and high levels of rooftop solar, the state has been a pioneer in DER planning and integration. According to Hawaiian Electric, the state’s main utility, rooftop solar now provides just under 15% of the state’s power, or close to half of all renewable power across the islands.

But rooftop also represents more than 90% of all solar installations in the state, and Hawaiian Electric has periodically come under fire for interconnection delays, such as in 2015, when it was faced with a backlog of 3,000 projects.

“We didn’t have a lot of the tools we have in place now,” said Blaine Hironaga, a supervisor for the utility’s distribution planning. “Hosting capacity was somewhat getting off the ground, and we were concerned about the amount of penetration that was hitting the grid. … So, it was taking some time to do those reviews. … We didn’t have a good process in place to conduct the reviews at the volume we were receiving.”

Fast forward and Hawaii has adopted performance-based ratemaking, under which Hawaiian Electric receives incentives for meeting specific interconnection goals. The state also has a range of rate plans for solar owners, in some cases limiting how much power they can export to the grid.

Ken Aramaki, director of transmission, distribution and interconnection planning, said interconnection reviews can be processed in 15-20 days, relying on “more advanced modeling” of the distribution system and “hosting capacity analysis.”

“We do sort of annual hosting capacity analyses of all the circuits, so we know how much can be added to the distribution system,” Aramaki said. The utility also uses a range of databases to cross-check its technical reviews, he said.

To further streamline interconnection, Hawaiian Electric also performs group or cluster studies, with “a model checkout process ahead of time” to ensure all the members of a group have all the information and system modeling needed before the utility begins the group study, Aramaki said.

The FTG score “doesn’t recognize the level of sophistication required and the technical complexities to get these high renewable numbers,” he said. “We do really complex modeling ahead of the rest of the industry because we have to.”

FARMINGTON, Pa. — The Mid-Atlantic Conference of Regulatory Utilities Commissioners’ (MACRUC) 28th Annual Education Conference last week at the Nemacolin Woodlands Resort focused on interregional transmission planning, resource adequacy and the risks posed by extreme weather.

PJM Vice President of State Policy Asim Haque said the analysis found concerns around the balance between generator deactivations and new entries. As it considers how to address those challenges, he said PJM must balance the interests of member states and regions with diverse priorities.

“I do think that this is overarchingly an engineering problem that we all need to try to collectively solve together,” he said.

Glen Thomas, president of the PJM Power Providers (P3) Group, said that when the Reliability Pricing Model (RPM) was adopted, there was an expectation that the value of capacity would clear at the cost of new entry (CONE), which is currently about $300/MWh. Recent auctions, however, have been clearing much lower, which he said sends a signal for generation to retire.

That has resulted in few new resources being built and generators deactivating, including the 2.2-GW Homer City coal generator in Pennsylvania shuttering this month, Thomas said. He argued that the dynamic has contributed to a decline in reserve margins over the past several years, from above 20% to falling into the single digits.

“You should not be sending a retirement signal knowing what we know now,” he said.

Thomas said improving the outlook for reliability will require revising how PJM accredits resources to ensure the amount of capacity they are able to offer is accurate to their reliability contribution and reworking the market seller offer cap (MSOC) to allow generators to represent their full risk as a capacity resource.

Haque said there has been agreement that the current clearing price is not sending appropriate price signals. PJM’s Board of Managers initiated the Critical Issue Fast Path (CIFP) process to solicit stakeholder proposals to overhaul the capacity market, with the goal of submitting a proposal to FERC in October. (See PJM Continues CIFP Discussion of Seasonal Capacity Market Proposal.)

“The goal should not be to increase prices; that should not be the goal of any market construct. The goal as we see it should be to continue to provide resource adequacy” while keeping costs effective for consumers, Haque said.

Ohio Public Utilities Commissioner Dan Conway said decarbonization is an important focus of his job, but maintaining reliability is his “first and last.” As thermal resources, especially coal-fired, have retired, he said the new resources coming online lack the same reliability attributes and present a looming risk of more regular curtailments and shortfalls.

He said he believes the competitive model formed by PJM offers the best path forward, saying that neighboring MISO is largely vertically integrated and is closer to the edge than PJM.

Vistra CEO Jim Burke said the thinking around renewable resources has shifted from a technology supplementing existing thermal resources to displacing them. As that transition continues, he said far more nameplate generation will need to be developed to replace the same amount of capacity, owing to renewables’ lower accreditation.

“The scale of this is one of the biggest things that I’d just like to emphasize. We’re nowhere near a one-to-one trade,” he said.

While much of the discussion in PJM has been on the pace of new development, Burke said ERCOT has seen a large amount of investment over the past 20 years but continues to have reliability concerns during peak loads, noting that Texas was experiencing a heat wave straining the grid as the conference was ongoing.

“We’re $100 billion in, and we’re still checking the app everyday,” he said, referring to ERCOT’s mobile dashboard.

Interregional Transmission Spotlighted

During a June 26 panel on interregional transmission planning, discussion centered on how new transmission buildout — especially between RTOs — could address growing risks from extreme weather.

The Brattle Group’s Joe DeLosa III said the company’s analysis has found that additional transmission could have provided about $1 billion in value during the December 2022 winter storm — also known as Winter Storm Elliott — paying itself in just the four days of the storm. Despite the benefits, he said new lines largely aren’t being built in part because the multidriver approach doesn’t capture independent transmission needs, and the sequencing of how needs are considered creates a patchwork of regional projects.

Resolving cost allocation disputes poses a challenge to transmission development, but DeLosa pointed to MISO’s planning process as a success in realizing benefits that are greater than the costs. For it to work in the Mid-Atlantic, he said close collaboration will be needed between states, RTOs and FERC.

Jeff Dennis, deputy director for transmission at the U.S. Department of Energy’s Grid Deployment Office (GDO), said his staff are focused on exploring improvements that can be made beyond the RTO-level, such as siting, permitting and other processes that can be streamlined to get transmission built without compromising on environmental justice communities.

In a study the GDO plans to release this fall, investment trends and wholesale price differentials were used to identify constraints, with preliminary results suggesting that new transmission would provide significant value when storms are stressing the grid.

Looking at scenarios with high clean energy penetration and high load growth, the study’s preliminary results find that there is significant need for interregional capacity transfer capability, particularly between the Midwest and Mid-Atlantic. As much as double the current transfer capability could be needed, as well as additional interchange between the Mid-Atlantic and Southeast.

Barbara Tyran, of the American Council on Renewable Energy, said much of the U.S.’ solar and wind potential lies between the Mississippi River and the Rocky Mountains, but only a fraction of it could currently be connected with load centers on the coasts with existing transmission.

FERC’s Jessica Cockrell said cost allocation has to balance planning and the needs of merchant generation to avoid eroding the value of projects. When considering how capacity transfer can be mandated between regions, she said that operational agreements can be reached to determine the share of capability on each line that can be used to flow power from one RTO to another.

David Townley, director of public policy for CTC Global, said grid-enhancing technologies such as reconductoring, dynamic line ratings, fast power flow controllers and energy storage can be used to get more out of existing infrastructure without needing to get new developments through the siting and permitting processes. One of the challenges with installing those technologies is a lack of understanding among utilities in how they can be used, he said.

Executives from some of the largest utilities in the Mid-Atlantic discussed how extreme weather could impact their operations, as well as how differing policies across the states in which they operate interact together and with federal law.

Dominion CEO Robert Blue said the company was able to maintain service throughout its PJM footprint during Elliott, but it implemented load shedding in other regions. That experience has led it to consider adding LNG storage to some of its large gas-fired generators to address some of the fuel security issues seen during the storm.

Exelon CEO Calvin Butler Jr. said the number of severe weather events has tripled in its region, especially microbursts that come in with minimal warning and put tens of thousands of customers without power. He said improvements in communications have reduced response times, and drones are now being used to detect obstacles that could prevent crews from using a route to access a repair site, aiding in sending the right equipment to where it’s needed.

“What we are finding is the storm forecasts are less and less predictable,” he said.

John Crockett III, president of LG&E and KU Energy, said wind storms are also posing an increasing challenge. High winds during Elliott contributed to three hours of load shedding, along with issues with an interstate pipeline causing some gas generation to be unavailable. A storm in early March brought wind speeds exceeding 60 mph and left around 400,000 customers without power.

Butler said Exelon’s decision to shift to multiyear planning in some states has allowed greater transparency and collaboration, with more detail than annual rate cases. The intervenor process is also changed with multiyear plans, allowing discussion of how rates interact with the policy goals of a state or intervenor.

While the federal government has made billions available to promote its climate and reliability goals, Butler said its actions haven’t always matched its ambitions. Both there and at the state level, legislation is interacting with decades-old regulatory frameworks, which he said can sometimes impede policy goals.

Lightning Round Discussions on Key Issues

During a series of lightning round discussions, several speakers shared their thoughts on the potential of green hydrogen, congressional bills addressing permitting authority, how investors view the state of the energy markets, and an upcoming report on coordination between the gas and energy industries being written by the North American Energy Standards Board (NAESB).

Bank of America’s Julien Dumoulin-Smith said investors are expecting costs for wholesale energy, interconnection and new generation — particularly offshore wind — to generally rise in the PJM region over the coming years.

He predicted that there will continue to be ample capital available for new developments, but the cost of capital is likely to rise with interest rates. Offshore wind installation costs, for example, could double because of interest rates, while concerns linger about whether the ships and logistics required to put the turbines in place are sufficient for looming projects.

“There’s clearly capital available in both debt and equity capital markets, and I think you’re going to see a lot of traditional equity getting raised in lieu of debt in this environment,” he said.

With rising interconnection costs and a growing gap in the valuation between clean and thermal assets, he said some resources are now worth just the value of their interconnection, reducing their prospects for continued operations.

“In this day and age, I don’t think you’re going to see a lot of tolerance if there are operational issues. If you see other issues on gas plants today, you’re going to see people favoring to take them out,” he said.

Constellation Discusses Hydrogen Development

Constellation Energy Executive Vice President Kathleen Barron said hydrogen offers a potential solution to several areas of the economy that have proved challenging to decarbonize, but remains uneconomical for the time being.

“We have proven technology; we know how to do this; companies are actually already doing this at one of our sites in New York, using nuclear energy to make hydrogen using electrolysis,” she said. (See related story, Constellation Gives Details on First-in-nation Pink Hydrogen Production.) “The problem is the cost of doing that is about three to four times what a customer is going to be willing to pay to use hydrogen as a substitute for natural gas.”

Barron said the Infrastructure Investment and Jobs Act provides funding for hydrogen hubs to jumpstart the production and transportation infrastructure necessary for mass industrial use of hydrogen, but the “additionality” clause in the law could pose a roadblock. The clause requires that only new clean energy can be used to power the electrolyzers, but she said it would require a doubling of the amount of renewable power currently available and to use that energy only to produce hydrogen.

“We’d need to double the size of today’s renewable grid and use it only to make hydrogen — not use it satisfy state [renewable portfolio standard] programs or to satisfy the EPA rules that are coming. … If we really want to try to tackle emissions in other sectors, and we want to use hydrogen, we’re going to need to use” existing generation, she said.

Nuclear makes hydrogen cost-effective because of its steady supply of power and the existing transportation infrastructure that tends to be in place at those facilities,” Barron said. Nuclear plants also tend to be further from population centers and have land available around them, raising the possibility of placing electrolyzers behind generators’ interconnection meters, a configuration the company has been proposing through the PJM stakeholder process. (See “Discussion Continues on Capacity Offers for Generators with Co-located Load,” PJM MIC Briefs: June 7, 2023.)

NextEra Evaluating Hydrogen Uses

NextEra Energy Resources Vice President of Development Ross Groffman also spoke about how green hydrogen could be used for industrial decarbonization. Some of the initial uses the company is developing projects for are green ammonia production to create agricultural fertilizer and liquid hydrogen as fuel for long-haul trucks and buses.

Hydrogen could also be used in steel and chemical production or blended into the fuel for natural gas generators, he said.

Intermittent resources sited alongside hydrogen could also be used for energy production when generation exceeds the amount of power the electrolyzers consume. Using hydrogen to fuel combustion turbines will play a central role in the future of decarbonizing the grid, Groffman predicted, and the NextEra is already investing in projects to explore technologies.

“It’s an important part of the long-term view of how some of these plants will run. It’s not going to happen in the next year or two; this is longer term, but it will be a key part of how the long-term green grid will perform,” he said.

Congress Considering Siting and Permitting Legislation

Christina Hayes, executive director of Americans for a Clean Energy Grid, shared her views on a slate of bills being considered by Congress that would address how the federal government interacts with siting and permitting of energy infrastructure. Some of the proposed legislation would offer transmission tax credits “as a kind of hook to getting siting and permitting handled more broadly.”

Hayes said there’s also a growing recognition of the need to incorporate community benefits and other impacts on where projects would be developed, both for pipelines and transmission.

With renewable standards now widespread not only among states, but also utilities and corporations, she said many are coming around to the need for more transmission to be built.

When considering the impact to their ratepayers, she said regulators could be more thoughtful when considering approval of transmission projects that would benefit other states, saying those could be viewed as an “insurance policy” for their future reliability.

NAESB Drafting Recommendations on Gas-Electric Coordination

Robert Gee, co-chair of NAESB’s Gas-Electric Harmonization Forum, gave an update on the recommendations being drafted with the aim of improving the coordination between the two industries. He encouraged all interested parties to either submit written comments or participate in the meetings, of which there have already been a dozen.

There are both operational and structural issues that impact the ability for gas generators to procure fuel during emergency conditions, Gee said, leading NAESB to consider creating a commercial standard or emergency protocols.

“Generators are not able to access gas during critical peak periods for a number of reasons. One is that they don’t have firm contracts, generally for economic reasons. Second, there’s inadequate information regarding available pipeline capacity and little to no transparency on certain parts of the system,” he said.

Gee reviewed a handful of the 17 recommendations that the forum is currently considering, which include increasing the transparency and communication around the status of interstate pipelines, ensuring that gas markets are fully functioning around the clock to allow generators to prepare for peak demand during emergency periods, and synchronizing the gas and electric markets to align the electric industry’s day-ahead procurement schedule with how generators procure fuel.

The forum is also considering recommending re-evaluation of whether out-of-market solutions are needed.

“We rely on competitive markets to basically give us the ability and tools to address this issue of trying to access gas during critical peak periods. We think it’s time to reconsider out-of-market solutions; weigh them carefully; see whether they work; see what they offer solutions to,” he said.

Gee said thought also is being given to recommending that two studies be commissioned by FERC and NERC to look at whether markets currently offer proper incentives for generators to procure firm fuel contracts during emergency conditions and to develop more gas storage infrastructure.

FARMINGTON, Pa. — Several sitting and former FERC commissioners shared their views on the future of RTOs and the relationship between state and federal regulators during the Mid-Atlantic Conference of Regulatory Utilities Commissioners (MACRUC) annual educational conference last week.

Speaking during the opening sessions of the conference June 26, acting FERC Chair Willie Phillips said cyber and physical security, the changing resource mix, extreme weather risk and the challenge of building the transmission necessary for the clean energy transition are some of the most critical issues the states and commission are likely to face in coming years.

Former Commissioners Suedeen Kelly, Philip Moeller, Robert Powelson and Richard Glick, the last of whom served as chair until January, sat on a June 28 panel discussing how communication between state and federal regulators can be improved. That forum was moderated by Maryland Public Service Commission Chair Jason Stanek, a former FERC senior staffer.

Both panels were asked how FERC should respond if it concludes that state policies are jeopardizing reliability by causing resources to retire without adequate replacement capacity. Glen Thomas, president of the PJM Power Providers group, asked Wednesday’s panel if the commission would take action in such a scenario.

“In this situation where you have a state policy that is causing pretty significant impacts in other states, is there a role for FERC here? Is this a situation where FERC just shrugs its shoulders and says, ‘Well it’s a state; it gets to do what it wants to?’ Or is this a situation where FERC recognizes the interstate impacts of a state’s action and can do some things to balance the equity?” he asked.

Kelly said the grid requires resources that are dispatchable, a characteristic that renewables largely lack. Until enough utility-scale storage can be developed, she said, thermal resources will have to be retained to maintain reliability.

“If you aren’t at the point where we can dispatch all of our renewables, we need our tried-and-true dispatchable generators, including gas-fired. As much as the community may not want carbon emissions, I think it’s important to educate the community that you can’t have 100% green without storage and in the meantime, we need other ways to ensure our renewables are dispatchable,” she said.

Glick said FERC’s ability to delay retirements is limited and the industry may need to find out-of-market solutions to ensure enough capacity remains available.

“You do have to have market reform, but I also think you have to engage — and I think you’re seeing it more increasingly frequently — you have to have out-of-market solutions to keep plants around, to take other actions to keep the lights on while the [development of] transmission’s underway, [and] while battery storage technology comes into play,” he said.

Powelson said shutting down units could have a cascading effect that impacts other states and requires increased use of reliability-must-run (RMR) contracts.

“We’re all in this together, and my concern is we move too fast and we start having these out-of-market RMR contracts, and that’s not good for consumers; that’s not good for the long-term future of grid reliability,” he said.

When asked about the future of coal plants, Phillips said they will likely continue to play a role for at least the next five years. Gas-fired resources will likely continue operating years past that, while coal units will see economic pressure to deactivate.

Speaking on Monday, Phillips said streamlining the path for building new transmission could provide the “biggest bang for the buck” in getting new generation on the grid. Much of the nation’s infrastructure is over 50 years old and will soon need replacement. He said it may be necessary for RTOs and regulators to begin using a 20-year planning horizon and to explore regional planning. The commission may also explore interregional transfers, he said, pointing to the benefits the capability provided during the February 2021 winter storm.

Also, many projects are designed with a single purpose and don’t consider additional benefits that could be realized.

“We do have projects that sit in silos. They’re siloed because of reliability, they’re siloed because of economics or jobs; what I would like to see are more multivalue projects,” he said.

Fixing Cost Allocation

One of the challenges Phillips anticipates is how to address cost allocation, which he said the commission will likely be addressing in the near future.

On Wednesday, Glick said interstate transmission projects can be difficult to plan when the cost allocations and benefits for each state do not match. While Congress is discussing providing FERC with preemptive siting authority on some lines, he said buy-in from the states will lead to a better outcome.

“The current approach to siting — obviously it can be problematic because there are some cases where some states may not have as much of an incentive to site a line if they feel it’s going to benefit another state, but they’re going to have to pay a significant share of the cost. So fixing the cost allocation problem is a big part of it,” he said.

Kelly said the commission has seen growing opposition to projects, including a convergence across the political spectrum as conservative landowners and liberal environmentalists turn to FERC to push against developments. She said developers of projects such as the West of Devers line in California or Western Spirit in New Mexico were able to build transmission to clean energy by engaging in dialogue with local communities.

“Both of those have been characterized by intense working with the community to try and understand what the communities’ opposition or problem with it is and accommodate it,” Kelly said. “Oftentimes that accommodation comes not just in changing the siting, which is oftentimes what we did at FERC when we were talking about natural gas pipelines, but in spending the money necessary to take care of some of the concerns in communities that were going to be impacted.”

“One thing that we should think about as regulators — state and federal regulators — is can we be a force to further the discussions of transmission developers with the communities and maybe be part of that and facilitate that,” she said.

FERC and EJ

Following the commission’s roundtable on environmental justice last month, Phillips and Glick both spoke about the importance of listening to communities’ concerns and ensuring that the benefits of the clean energy transition are felt by all.

Phillips said it’s a personal priority of his, being from Alabama where he grew up in the shadow of heavy industry. He said FERC has streamlined the permitting process to create a legal obligation for communities to be given a voice. Not enough of the public is participating in hearings, he said, but the commission’s Office of External Affairs is working on improving its consultation process.

Glick recounted visits he made to Port Arthur, Texas, and Lake Charles, La., to view the impact polluting industry has had on residents there. While those aren’t FERC-regulated industries, he said it showed the potential consequences when environmental justice isn’t considered.

Hearing from residents and putting conditions on FERC orders to address communities’ concerns during the FERC process can also avoid legal challenges to its decisions and help get projects built easier, Glick said.

Beacon Wind submitted its construction and operations plan (COP) to the U.S. Bureau of Ocean Energy Management (BOEM) on June 5.

BOEM on June 29 announced it would initiate a review of the plan, inviting public comments through July 31 as it prepares an environmental impact statement for the project.

It’s the 11th offshore wind COP review BOEM has started since President Biden took office, with a goal of 30 GW of offshore capacity by 2030. But that burst of regulatory enthusiasm has not yet translated to a burst of construction activity.

Two small-scale projects totaling 42 MW are in operation and two utility-scale projects are under construction, both neighbors of Beacon.

Beacon itself has been in the pipeline for more than four years, and developers do not expect it to produce power until 2028. Nor do they expect to be able to build the first phase under the financial terms of the contract they signed with the state of New York in January 2021.

The development team of Equinor and bp petitioned in June 2023 for inflation adjustments for their Beacon Wind 1, Empire Wind 1 and Empire Wind 2 projects, saying the world had changed drastically and costs had risen dramatically.

Also, developers are trying to back out of power purchase agreements for two large Massachusetts OSW projects for the same reasons, and there are signs of financial strain in some other states’ OSW development portfolios.

Beacon occupies Lease Area OCS-A520 — 128,811 acres on the Outer Continental Shelf south of Massachusetts and east of New York. Equinor won a December 2018 BOEM auction with a $135 million bid, and the lease was executed in March 2019.

The developers in January submitted a proposal for Beacon Wind 2 in New York’s 2022 offshore wind solicitation, which has yet to result in contract awards. In this round, bidders had the option of including an inflation adjustment mechanism to address any cost increases.

BOEM says the Beacon Wind lease area holds the potential for at least 2,430 MW of nameplate generation. Beacon Wind 1 is proposed at 1,260 MW.

“BOEM is advancing the administration’s ambitious energy goals while remaining diligent in our efforts to avoid, minimize and mitigate impacts to ocean users and the marine environment,” BOEM Director Elizabeth Klein said in a news release. “As part of our environmental review process, we seek input from tribes, our government partners, the fishing community and other ocean users to inform our next steps.”

In-person public meetings for the environmental review are scheduled for July 18 and 20 in Dartmouth, Mass., and Queens, N.Y., respectively. Virtual meetings are scheduled for July 13 and 26. Details on the meetings and on submitting comment electronically are posted on the Beacon Wind page of BOEM’s website.

The Northeast Atlantic Coast is the early focus of the offshore wind industry, with clusters of multiple wind farms proposed east of Long Island/south of Massachusetts, as well as south of Long Island/east of New Jersey.

BOEM’s previously completed environmental impact statements for other wind projects in the region have predicted a potentially significant impact on marine life, and on area fisheries. But much remains unknown, due to the lack of operational data about offshore wind power projects individually and collectively.

The Northeast Fisheries Science Center of the National Ocean and Atmospheric Administration on June 15 announced a five-year partnership with the University of Rhode Island to explore the impacts of offshore wind on marine ecosystems and the people who live near or work on the ocean.

MISO and CAISO received above-average marks while other regions got middling to failing grades in a “report card” on transmission planning and development published last week by Americans for a Clean Energy Grid.

“Overall the grades leave a lot of room for improvement,” ACEG said in its report, which it intends to spur discussion about how the FERC Order 1000 transmission planning regions can improve their efforts.

“We hope parties in each region can see positive examples in other ones from which they might learn,” ACEG said. “Our intent is not to criticize. Instead, we aim to show that good performance is possible and achievable, and all regions can improve to reach an ‘A’ grade in the coming years.”

The Southeast region has the most room for improvement, “while the West (minus California), Mid-Atlantic (PJM), New England (ISO-NE) and Texas are also lagging in their planning and development efforts,” ACEG said.

ACEG represents a broad coalition of clean energy and conservation groups and companies such as Berkshire Hathaway Energy, Google and NextEra Energy, all “focused on the need to expand, integrate, and modernize the North American high-voltage grid.”

In its report, the group said FERC Order 1000 and the commission’s other efforts to promote regional planning have produced “lackluster” results.

In response, FERC issued a Notice of Proposed Rulemaking in April 2022 to require long-term regional transmission planning and increased state involvement in transmission cost allocation, among many other changes (RM21-17). (See Battle Lines Drawn on FERC Tx Planning NOPR.)

“The NOPR acknowledges that regional planning under Order No. 1000 failed to adequately plan for and meet transmission needs, driven largely by the changing resource mix and increasing load,” ACEG said.

ACEG is pleased to see growing recognition of the need for proactive transmission planning, Executive Director Christina Hayes said in a statement accompanying the report. “Without continued improvement, the U.S. grid will remain a barrier to reaching our climate goals, and result in more dangerous power outages that threaten lives and livelihoods.”

Assessing Transmission Capacity

The “Transmission Planning and Development Regional Report Card” was written by Grid Strategies Research and Policy Manager Zach Zimmerman. Hayes and Grid Strategies President Rob Gramlich helped develop its methodologies and analysis.

The report evaluates the performance of Order 1000 planning regions, not specific entities such as RTOs, because “many parties, besides the planning entities, bear responsibility for performance, including utilities, states, and other stakeholders,” it said.

It employs four metrics to grade the regions: planning methods and best practices; miles of transmission built and future transmission plans (i.e., plans that go beyond reliability upgrades); transmission capacity available for new resources; and congestion ($/MWh).

Transmission capacity available for new resources combined three metrics — cost to interconnect, time in queue, and project completion rate — “all of which indicate whether a region’s system has sufficient transmission capacity to connect new generation,” it said.

“No single metric is entirely dispositive, but in combination, they provide an accurate assessment of transmission capacity,” ACEG said.

Based on the criteria, Midwest/MISO and California/CAISO each earned a “B.” New York/NYISO and Plains/SPP received grades of “C+.” The report card gave “D’s” to Mid-Atlantic/PJM, New England/ISO-NE, Texas/ERCOT, Northwest/Northern Grid and Southwest/West Connect.

The Southeast region — composed of Southeast Regional Transmission Planning (SERTP), South Carolina Regional Transmission Planning (SCRTP) and Florida Reliability Coordinating Council (FRCC) — got an “F.”

Midwest/MISO

Transmission planning efforts earned MISO and CAISO their relatively high marks.

ACEG said MISO’s “B” grade — and its 86% score, the study’s highest — resulted largely from the ISO’s work on its 2011 Multi-Value Projects initiative and its first, $10-billion long-range transmission plan (LRTP) portfolio. The ISO would have received an even higher score if not for MISO South, “where relatively little transmission planning activity occurs,” the report said.

MISO said it plans to address system needs in MISO South and to establish stronger connections between its South and Midwest areas in future iterations of its LTRP effort. The grid operator also pointed out that its first LRTP portfolio is “one of the largest transmission portfolios in U.S. history.”

“Although we have not had the opportunity to fully review the report, MISO’s ranking highlights our continued focus on planning a reliable grid of the future,” MISO spokesperson Brandon Morris said in an emailed statement. “This is why transmission evolution is a key pillar of our ‘Response to the Reliability Imperative’ efforts.”

MISO refers to its joint responsibility with its members to ensure that the clean energy transition occurs in a reliable and orderly manner as its “reliability imperative.” It issued its latest report on those efforts in January.

California/CAISO

CAISO’s “proactive, scenario-based, multivalue” transmission planning over the past two years accounted for its high score, which at 85.8% nearly matched MISO’s.

The report highlights the ISO’s work with the California Public Utilities Commission and California Energy Commission to plan collaboratively for the state’s clean energy future and coordinate resource procurement and transmission development.

It commended CAISO’s inaugural 20-year transmission outlook, approved last year, which examined in-state needs and transmission lines required to import large quantities of wind energy from Wyoming and New Mexico. And it cited the ISO’s most recent transmission plan, which broke with CAISO’s traditional planning process to bring needed resources online faster while dealing with an interconnection queue that has grown too large and unworkable.

ACEG awarded CAISO an “A-” for its planning efforts but only a “C” for lines planned and built, giving it an overall grade of “B.”

“Although it received one of the highest grades with a ‘B,’ there is still room for improvement,” the report said. “California needs to develop the lines it is planning, which could create a congestion-specific metric and provide better public access to good interconnection cost data.”

In addition, “California receives a higher grade than most regions for taking a relatively successful and innovative approach to interregional planning,” it said.

CAISO’s 2021-22 transmission plan noted that the “interregional coordination process [with NorthernGrid and WestConnect] has not met expectations.”

As an alternative, “CAISO has implemented programs to enable import transmission from other regions, such as making the TransWest Transmission line a part of its balancing authority even though it is not in California, and the cost of the line will be paid for by off-takers,” the report said.

TransWest Express, which recently broke ground, will link Wyoming wind to markets in California and the desert Southwest.

“We are pleased that ACEG highlighted the value of this complex effort to develop a vision for what the transmission system will look like in 2040, and appreciative of close cooperation from the California Energy Commission and the California Public Utilities Commission,” CAISO Vice President Neil Millar said in a statement to RTO Insider.

New York/NYISO

After MISO and CAISO, New York/NYISO was the next highest scoring region with a 78.6% total, earning it a “C+,” “based on their transmission planning methods and recently developed plans for new transmission,” the report card said.

The grade reflected NYISO’s public-policy transmission planning processes, which identify high-voltage transmission projects necessary for New York’s transition to clean energy. It also gave NYISO good marks for building projects.

NYISO has a “proactive, scenario-based planning process … [that] incorporates multiple cases and scenarios over a 20-year evaluation time horizon and uses reliability, economic, and public policy metrics to evaluate projects and select a transmission solution,” ACEG said. “For example, New York, in its 2019 public policy transmission plan, studied transmission lines using three scenarios, including a base case, Clean Energy Standard and Retirement Scenario.”

“This planning process is why New York is graded relatively well,” it said.

New York has also succeeded in getting important transmission projects built, it said. “After many years of little planning, persistent congestion and little transmission, New York has improved dramatically in the last few years,” it said. “Significant lines connecting Quebec, upstate, and downstate areas reduced congestion, improved reliability, and achieved public policy goals.”

ACEG said that while “NYISO does very little proactive interregional transmission planning,” the recent lines, such as those connecting it to Quebec, might signal a more proactive approach.

NYISO’s cumulative grade might have been higher except for the “F” ACEG gave it for transmission capacity available for new resources. NYISO deserved the failing grade because New York had by far the slowest completion score (0% compared with 65% for SPP, the next lowest scorer) for getting new resources out of its interconnection queue studies and onto the grid, the report said.

In an email, NYISO responded that “New York has recently seen the most significant investment in new transmission in decades through the NYISO’s Public Policy Transmission Planning Process. While the process has been a great success, the NYISO has called for significant additional transmission investment through its Public Policy Transmission Planning Process to support the achievement of public policy requirements.”

“The NYISO’s System Resource Outlook report from 2022 found that extensive transmission investments will be necessary to deliver renewable energy to consumers and address new constraints from the future addition of new resources,” it said.

Plains/SPP

The report card gave SPP a “C+” while saying it has the potential to achieve an “A” if it continues with its planning upgrades.

The report points to SPP’s developing consolidated planning process (CPP), which integrates its transmission planning and generator interconnection processes. The CPP’s intent is to determine the transmission needed to interconnect new generation, provide transmission service, maintain reliability and resiliency and relieve congestion.

SPP also overhauled its generator interconnection process, instituting a three-phase approach that FERC approved last year, and says it is “aggressively” clearing the queue.

The grid operator currently has 556 projects in its queue, representing 111 GW of capacity; 43% of the proposed projects are solar resources.

According to the report, the Plains region has one of the lower completion rates for new projects, with a capacity-weighted rate of 2% for those entering the queue in 2017 and reaching commercial operation. In 2022, ACEG said SPP received almost triple the interconnection requests compared to their next-highest queue year in 2021.

“This historic queue will likely lead to problems going forward,” the report said.

Congestion is increasing in the Plains, thanks to significant curtailment of wind generation in recent years. The RTO’s Market Monitoring Unit reported in the 2022 State of the Market that average hourly curtailments increased “substantially” from 244 MW in 2020 to 1,260 MW in 2022.

ACEG credited SPP for its Joint Targeted Interconnection Queue (JTIQ) work with MISO but noted the process is “not necessarily reflective of all planning best practices … and primarily focused on generator interconnection requests.”

SPP could also “better incorporate” merchant developers into its planning, ACEG said.

The JTIQ process has identified 400 miles of projects on the seams valued at over $1 billion in investments, but their cost allocation has yet to be approved. SPP also has almost 700 miles of new lines planned or in development within its near-term and long-range transmission plans, representing a roughly $2 billion investment.

Texas/ERCOT

ERCOT, which delivers about 90% of the state’s electricity to 26 million Texas customers, was given one of the report’s lower scores, a “D+.”

ACEG awarded ERCOT high marks on interconnection but said it needs to address congestion soon.

ERCOT’s Independent Market Monitor’s 2022 State of the Market report said real-time congestion costs in ERCOT rose 37% last year to $2.8 billion.

Texas’ interconnection process uses a “connect and manage” approach to integrated interconnection and transmission planning, the report said. New generators only pay for their connection to the grid, as opposed to the “broader systems or affected interregional system costs that generators in other regions have to pay.” The generators don’t receive firm transmission rights and grid operators curtail them more quickly, ACEG said.

“However, easy interconnection without proactive planning can lead to congestion and curtailment as significant amounts of generation are added, filling up existing transmission capacity,” the report said.

Lawrence Berkeley National Laboratory’s 2022 Interconnection Queue report found Texas has the highest project completion rate of any region — 28% of capacity-weighted projects were commercialized — and one of the lowest wait times at 18 months. ERCOT’s queue has 902 projects and 250 GW under study, according to the ACEG report.

The report calls for ERCOT to adopt more “proactive, scenario-based, multivalue transmission planning.”

ERCOT’s latest regional transmission plan only identified new lines required for reliability upgrades over a six-year horizon, ACEG said. While Texas did build 2,400 miles of new transmission as part of the 2010-13 competitive renewable energy zones project, those projects are fully subscribed, the report said.

ACEG also said there is a “major need” for interregional transmission in Texas, as was made clear during the deadly 2021 winter storm. In dire need for energy to save a grid that couldn’t meet demand, the state was limited in what it could import from its neighbors.

As an islanded interconnection, Texas maintains its jurisdictional freedom from FERC by not mixing its electrons with those of its neighbors.

Legislation following the deadly 2021 winter storm has strengthened the Texas Public Utility Commission’s oversight of ERCOT’s transmission process. The PUC can direct ERCOT to build certain transmission facilities and a new law has cut the time to approve transmission certifications from 360 days to 180.

New England/ISO-NE

ISO-NE’s lack of proactive planning methods led to a low overall score, ACEG said, but the RTO received an “A” on the congestion metric.

ACEG found that transmission planning in New England “has traditionally focused on reliability and been reactive, rather than proactive,” noting that a significant buildout of transmission in the early 2000s cut down on congestion, but new resources in remote areas remain constrained. The report also said that ISO-NE would benefit from increased interregional planning.

“New England has done very little to coordinate with New York despite a rapidly growing amount of offshore wind hoping to interconnect close to the seam of both regions,” the report said.

In response, an ISO-NE representative highlighted the region’s history of making significant transmission investments, including almost $12 billion in grid upgrades since 2002.

“We have and will continue to work collaboratively with the New England states and energy stakeholders to determine how the region can build upon past success as the states look to meet their aggressive climate goals,” ISO-NE said.

In June, the New England states, New York and New Jersey, sent a letter to the US Department of Energy asking for federal assistance to establish a Northeast States Collaborative on Interregional Transmission, while ISO-NE, NYISO, and PJM supported the proposal in a separate letter.

The Collaborative would enable the states to “work in partnership to explore opportunities for increased interconnectivity, including for offshore wind, between our regions.”

Mid-Atlantic/PJM

PJM scored poorly in the report, which gave it low rankings for all categories except on its stakeholder process and governance. Its total planning grade was 65%, a letter grade of “D.”

ACEG faulted PJM for not considering if transmission proposals could be better addressed through regional projects, not conducting proactive generation and load forecasting and not modeling expected retirements in its 15-year planning period.

While there has been some use of the MISO-PJM Targeted Market Efficiency Process (TMEP), ACEG said interregional planning remains minimal, despite potential benefits related to offshore wind development coordination with the New York and New England regions. Coordination with MISO remains largely limited to operational reliability or short lead-time projects.

The report states that merchant developer proposals are studied through PJM’s backlogged interconnection process, which has resulted in FERC complaints about delays.

PJM spokesperson Jeff Shields responded to the report by pointing to the Summer Reliability Assessment released by NERC in May, which found much of the country outside of PJM is at an elevated reliability risk. He said work is already underway on expanding its planning methods as outlined in its Grid of the Future Paper released last year.

He said PJM’s queue overhaul, approved by the commission in December, will go into effect this month.

“The reforms will speed up and streamline generation interconnection requests, improve project cost certainty, and significantly improve the process by which new and upgraded generation resources are introduced onto the electrical grid,” he said.

Though he argued that PJM has made strides in improving the turnaround for interconnection requests, Shields said many projects that the RTO has completed studies on have yet to be built due to factors beyond its control.

“Today there are 44,000 MW of mostly renewable generation resources that have cleared the PJM study process but have yet to be built. The developers of these projects have everything they need from PJM to move forward with construction, but they are not building. We continue to hear that there are a number of factors unrelated to PJM that are causing delays, including supply chain, siting, regulatory issues or financing,” he said.

Northwest/Southwest

In the non-CAISO West, the Northwest/NorthernGrid planning region received a “D” grade, and the Southwest/WestConnect region earned a “D-.” Both are Order 1000 regional planning entities ostensibly responsible for grid planning across most of the Western Interconnection.

“NorthernGrid and WestConnect have not conducted proactive planning,” ACEG said. “The work of individual utilities or states in the region is much of why the regions managed a ‘D’ grade.”

Both regions received an “F” for planning methods and a “D” for congestion but significantly better grades for transmission capacity for new resources (B-minuses) and transmission lines planned and miles built (“B-” for Southwest/“C” for Northwest.)

“In the Northwest, individual utilities advance much of the significant high-voltage transmission buildout,” it said. “PacifiCorp and NV Energy are leading this effort. PacifiCorp’s planned transmission lines, known as the Gateway Projects … are an $8 billion investment and over 2,300 miles of new transmission lines.”

“NV Energy also has almost 600 miles of new transmission lines known as the Greenlink projects, which are just over $2 billion in investments,” it said. “However, NorthernGrid’s 2020-2021 transmission plan did not include any interregional or nonincumbent transmission lines.”

In the Southwest, WestConnect “did not identify any regional needs in its previous transmission plan,” the report said. “States, utilities, and merchant developers are driving most of the transmission planning and development in the region.

“For example, in Colorado, Xcel has planned the Colorado Power Pathway projects, an approximately $2 billion investment in almost 600 miles of high voltage lines that will help Colorado meet its goals by interconnecting 5.5 GW of resources.”

“In New Mexico, the [Renewable Energy Transmission Authority] has approximately 1,200 miles of new high voltage transmission under development that will interconnect almost 9 GW of new generation and represents over $5 billion in investments,” it said.

Southeast

The Southeast/SERTP, SCRTP and FRCC region came in last with an “F.”

“The region makes little information available to the public, has limited opportunities for stakeholders to engage meaningfully and has built and planned minimal regional transmission,” the report said.

The region failed under both the planning methods/best practices and transmission lines planned and built criteria. It got a “D” for congestion but came in second in the rankings with an “A-“ for transmission capacity available for new resources after scoring 100% for the time that projects spend in its interconnection queue.

In 2021, it took only 18 months from the time an interconnection request was made to the signing of an interconnection agreement in the Southeast. That compared to 51 months in SPP, the longest wait time in the nation.

Lawrence Berkeley’s Interconnection Queue report “showed that the Southeast had a queue size similar to NYISO or SPP, with over 800 project requests and around 100 GW of capacity,” ACEG said. “For our metrics, the Southeast scored well on completion rates for projects with 16% of projects reaching commercial operation.

“In addition, the Southeast scored well on time projects spent in the interconnection queue,” it said. “However, regions without an RTO rely on individual utilities to interconnect resources, and very little aggregated data or transparency exists on those project costs.”

‘Grades Can Change’

Even the lowest scorers can move up in the rankings, ACEG said in its concluding remarks.

“As with many students that grow over time, these grades can change as regions evolve their planning processes and transmission build out,” the report said. “This progress does not strictly depend on compliance with potential new rules from FERC, but on the initiative of the regions and their participants in enhancing their planning processes and building much-needed high-capacity regional transmission.”

“Future report cards will watch closely for improvement and look forward to regions moving to the head of the class,” it said.

Overall grade and summary of grades for each metric | ACEG

The New Jersey Board of Public Utilities (BPU) on Thursday approved an additional $150 million of expenses for the state’s $1.07 billion transmission project to connect offshore wind farms to the grid, saying the extra cost would not undercut the project’s financial benefits for ratepayers.

The 14% increase follows by eight months the board’s approval of the project in what the agency said was the first use in PJM of FERC’s state agreement approach (SAA), which allows a state or group of states to initiate a project to fulfill state policy requirements as long as they foot the bill for associated costs in the RTO’s transmission plan.

The cost rise comes amid growing scrutiny of New Jersey’s ambitious clean energy commitments, especially the plan to develop 11 GW of offshore wind capacity, with some Republicans and business groups demanding an estimate of the cost to ratepayers and questioning whether the investment is worthwhile.

As the BPU acted, state lawmakers in a last-minute vote before the summer recess backed a bill that would enable Danish developer Ørsted to receive federal tax credits to help meet cost increases in its Ocean Wind 1 project, rather than the state receiving the benefits of the credits. (See NJ Lawmakers Back Ørsted’s Tax Credit Plea.)

“We have to keep moving forward,” BPU President Joseph L. Fiordaliso said before the board’s 5-0 approval of the order outlining the increase. “There are unfortunately many unforeseen developments that have occurred over the past couple of years prior to the pandemic and after the pandemic as far as the economy is concerned, where we see increases that were never anticipated.”

The BPU endorsed additional expenses of $40.76 million for several changes — described as “interconnection work” — in the scope of work, or additional elements of construction that were not part of the original bids approved in the solicitation. Part of that expense will pay for the engineering, procurement and construction of cables and connection points that would tie the offshore projects to the grid.

The interconnection cost increases also included Jersey Central Power & Light’s replacement of 115- and 230-kV transmission lines to make way for larger lines, and the replacement of certain equipment.

The board also approved $109.5 million in “scope-related cost estimate adjustments,” cost increases resulting from a closer analysis of the developer’s work and estimates. That included $27.1 million for the “reconductor of a small section” of a 230-kV line as a result of “updated communication between the developer and PJM,” which is a partner to the BPU in the SAA project. An additional $71.9 million stemmed from the “additional refinement” of the developer’s “cost estimates for their awarded scope,” which the BPU expected at the time the offshore wind project was awarded, the order states.

The $109.5 million estimate was reduced from the previously released revised estimate of $127.34 million, which was first reported at a May 9 meeting of the PJM Transmission Expansion Advisory Committee. (See NJ BPU Pulls Offshore Tx Project Mod from Agenda After Complaint.)

Ratepayer Benefits of Offshore Wind

Andrea Hart, BPU’s senior program manager for offshore wind, told the board the changes would not affect the agency’s estimation that the selected SAA solutions would save ratepayers more than $900 million, a figure calculated by looking at the “cost of the transmission facilities that would be necessary to achieve New Jersey’s offshore wind goals in the absence of an SAA solution.”

That’s because, according to The Brattle Group, a consultant working on the project, the cost increases would have been incurred anyway had the agency opted to tie in the offshore projects to the grid using a non-SAA agreement approach.

“Clearly, price increases are not uncommon,” said Commissioner Zenon Christodoulou. “But as a consumer, they’re never welcomed. So although we accept this and we appreciate all the efforts, I think that additional changes might not be as welcome.”

Brian Lipman, director of the New Jersey Division of Rate Counsel, who first raised concerns about the hikes in June, said he was “skeptical that these increases result in no change to the amount of benefit to be seen by ratepayers.”

“We still question whether the scope changes are in fact prudent increases,” he said in an email to NetZero Insider. “It is unclear to Rate Counsel why some of these issues were not identified in the initial bid. While we understand that some changes may be necessary (equipment not available or has been updated) these changes appear to be due to a failure to fully understand the project when bid.

“These increases are not due to changes in economics or increases in materials,” he wrote. “These changes are coming about because as the developers take a closer look at the work they bid to do, they realize that changes need to be made.”

Anticipated Future Hikes

The BPU awarded the main part of the SAA project — costing $504 million — to Mid-Atlantic Offshore Development (MAOD) and JCP&L to build a new substation called the Larrabee Tri-Collector Solution next to an existing JCP&L substation through which offshore wind projects would tie into the grid. The agency also awarded contracts totaling $575 million to seven smaller projects to upgrade existing onshore transmission identified by PJM as necessary.

The agency’s awards focused only on infrastructure on land, leaving the offshore infrastructure to be completed later by offshore project developers. (See NJ BPU OKs $1.07B OSW Transmission Expansion.)

The order approved by the BPU last week said the original project selection anticipated that additional interconnection work would be needed but did not define whether it would be done by the SAA project developer MAOD or an offshore wind developer. Documents for the BPU’s third offshore wind project solicitation, released in March, outlined the winning developer’s responsibility for “prebuild infrastructure” that would build the necessary duct banks and access cable vaults to be used by all offshore wind projects to the new Larrabee substation.

The solicitation documents did not specify whether MAOD or the winner of the third solicitation would build certain parts of the infrastructure, and the BPU and its consultants recently concluded that the work would be best done by MAOD, adding to its costs, the order said. Pursuing that option would allow the work to be completed faster than waiting for the third solicitation process to be completed, would be safer and would yield various technical benefits, the order said.

The work included the engineering, procurement and construction of infrastructure to “accommodate” four HVDC lines and the work needed to design and build the trenches and collector lines for three alternating current lines, the order said.

“As transmission projects develop, it is common, if not expected, for cost estimate adjustments to occur,” the order states. “As such, additional cost estimate adjustments, in addition to the cost estimate adjustments noted herein, may be anticipated in the future.”

MANCHESTER, Vt. — ISO-NE is considering moving to a prompt and seasonal capacity market, the organization told stakeholders at its Participants Committee (PC) summer meeting last week.

The RTO has emphasized the need to address the seasonal variance of resource reliability in its capacity market, especially as it expects to transition from a summer peaking to a winter peaking system. The organization outlined potential options for transitioning to such a market, while also accounting for the implementation of Resource Capacity Accreditation (RCA) updates, which likely would affect the scheduling of future capacity auctions.

The RCA project has been an extended effort by the RTO to better assess the reliability of various resource types, which ISO-NE was hoping to implement for Forward Capacity Auction (FCA) 19, which would procure capacity for the 2028-29 capacity commitment period (CCP).

However, ISO-NE announced in June that it had found an error in the software used in the RCA project, which caused an underestimation of the amount of LNG available to generators when assessing winter risk. The RTO has said this error affected several months’ worth of work on the project and will affect its implementation schedule.

In a memo written prior to the PC meeting, ISO-NE Chief Operating Officer Vamsi Chadalavada asked for stakeholder feedback on the best way to incorporate the RCA project into the forward capacity auctions. ISO-NE also highlighted the potential of moving away from the current forward capacity market structure and holding auctions seasonally and just a few months ahead of the CCP.

ISO-NE wrote in the memo that moving to a prompt capacity market would buy time for the RTO to implement the market changes.

“In transitioning from a three-year forward to a prompt capacity market construct, there will be up to a three-year period between conducting the final forward capacity auction and conducting the first prompt capacity auction,” Chadalavada wrote.

David Patton of Potomac Economics, which serves as ISO-NE’s external market monitor, recommended transitioning to prompt and seasonal market as soon as feasible and said a seasonal market would do a better job accounting for the differences in seasonal reliability between resources.

Patton said the current process has a “a dubious track record of facilitating entry of new resources,” and that procuring capacity three years ahead “inhibits resources with fast development timeframes from receiving revenues as soon as they are able to support reliability.”

He noted that the existing FCA structure introduces uncertainty into the expected load and resource mix and added that the current market can also lead to premature retirement of older existing resources.

“Retirement of older units is often prompted by unforeseen equipment failure that is not economic to repair,” Patton said. “Such units must accept a capacity obligation that ends more than four years after the FCA, which creates substantial risk for the supplier.”

Presenting a cross-market comparison between ISO-NE and other RTOs, Patton found New England had the highest all-in costs in 2022, largely consistent with previous years. Patton said that higher gas prices in the region drive the higher overall costs but added that New England also has the highest capacity charges, largely due to “over-forecasted demand ahead of the FCAs, which are slow to correct.”

Comparison of RTO all-in prices | Potomac Economics

ISO-NE laid out four potential pathways for implementing the RCA updates as well as a prompt and seasonal capacity auction, including the possibilities of delaying FCA 19, delaying the RCA implementation and/or implementing a prompt and seasonal market along with the RCA changes for either the 19th or 20th auction cycle. The RTO noted that the removal of the Minimum Offer Price Rule will proceed for the 2028-29 CCP as scheduled.

Aleks Mitreski of Brookfield Renewables expressed his opposition to delaying FCA 19 due to the uncertainty this could introduce.

“ISO-NE has a great track record of never delaying an auction, so having FCA 19 run as scheduled will avoid market uncertainty and any regulatory uncertainty if the delay is challenged at FERC,” Mitreski said in a statement to RTO Insider. “By pushing the RCA implementation for FCA 20, this will give the stakeholders time to evaluate the RCA changes, as well as the benefits and tradeoffs for implementing a seasonal and/or prompt capacity market.”

Mitreski added that a move to a prompt and seasonal market would introduce several tradeoffs, and that stakeholders will need time to evaluate the merits of such a change.

“While it will help with the fuel qualification processes for RCA, a prompt market does not enable new entry in the market to address any retirements or transmission issues,” Mitreski said. “The only fix for those reliability issues would be expensive out-of-market reliability-must-run agreements like we have seen in NYISO in the past, something that the New England region wants to avoid.”

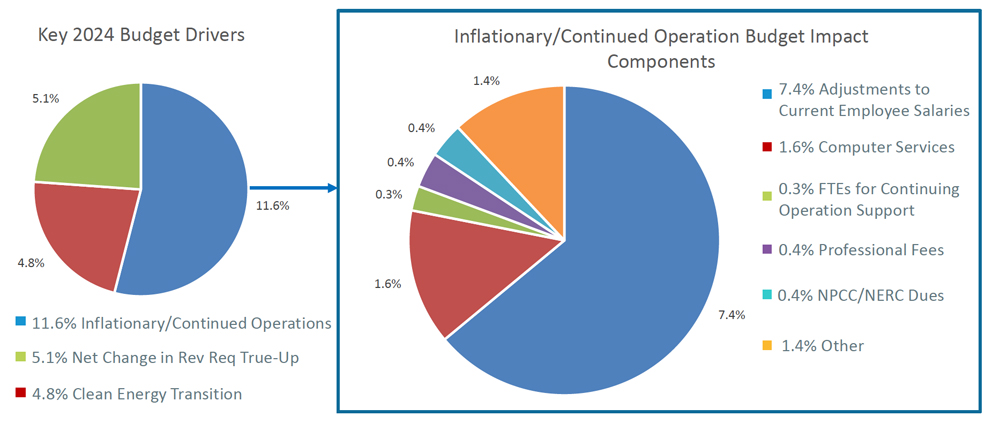

Budget Increase

ISO-NE also told the Participants Committee that it expects a significant year-over-year increase for its 2024 budget in its presentation on its preliminary budget for the coming year, equaling a 21.5% increase in the total revenue requirement for 2024.

This increase is driven by increased costs related to preparing for the clean energy transition, effects of inflation on labor and information technology costs, and the net-change from the annual revenue true-up, the RTO said. The largest single portion of the increase is associated with adjustments to employee salaries.

ISO-NE preliminary 2024 budget | ISO-NE

“The 2024 budget represents a ramping-up of organizational capacity to carry out the organization’s mission of planning the transmission system, administering the region’s wholesale markets, and operating the power system to ensure reliable and competitively priced wholesale electricity; as well as developing new capabilities that will be necessary for supporting the grid of the future,” ISO-NE CFO Robert Ludlow said.

Ludlow said that the RTO needs to increase staffing to meet clean energy planning needs, noting that the changing resource mix and the overall increase in generating assets will increase the organization’s workload. For 2024, the RTO proposed the addition of 40 new full-time employees, 34 of whom would be focused on supporting the clean energy transition.

“In order to keep pace with the needs of the transition to cleaner generating resources, the ISO must begin ramping up its capabilities and operational capacity now,” Ludlow said.

FERC on Friday accepted NYISO’s proposed tariff revisions that it said will prevent generators not using their capacity resource interconnection service (CRIS) rights from retaining them and allow for more efficient transferring (ER23-1824).

The revisions are intended to make it easier for deactivated facilities to adjust their unexpired CRIS rights while also increasing capacity deliverability headroom and potentially lowering the cost of market entry for future facilities by lessening the need for deliverability upgrades.

CRIS is required to participate in NYISO’s capacity market and can only be obtained either through a transfer from a facility with existing rights or from ISO deliverability studies.

“NYISO’s proposal adds greater clarity and flexibility regarding the rules applicable to CRIS transfers and bolsters the existing CRIS retention and termination rules,” FERC said. “We agree with NYISO that these revisions will help facilitate the full and efficient utilization of existing interconnection capacity by mitigating the retention of CRIS by suppliers who are not fully utilizing or who are unable to fully utilize their CRIS, and by enabling the more efficient transfer of CRIS between facilities.”

The Long Island Power Authority and energy storage development company Elevate Renewables F7 did not oppose NYISO’s proposal, but they suggested several changes to address concerns they had with it. As they did not lodge any protests against the filing, FERC did not address their concerns, ruling their suggestions outside the scope of the proceeding.

A group of North Carolina businesses urged the state’s legislature and governor to support studying “wholesale market competition options,” including an RTO, saying they were “concerned over limited access to cost-competitive, clean energy.”

In a letter sent Thursday to the General Assembly and Gov. Roy Cooper (D), the businesses endorsed North Carolina House Bill 503, introduced in March. The bill would direct the North Carolina Collaboratory — a clearinghouse established among the state’s public universities to provide useful research data to state and local governments — to “evaluate reform of the [state’s] regulatory wholesale electricity market.”

Studies undertaken under the bill would have to include an evaluation of designated market structures — an RTO within either North and South Carolina or the entire Southeast U.S.; an energy imbalance market within the same areas; or participation in the Southeast Energy Exchange Market (SEEM) — along with “any other market reforms the Collaboratory [deems] appropriate.”

In May, the South Carolina Legislature received a report that said participating in an RTO could provide the state benefits of up to $362 million per year. (See Brattle Report Sees Benefits for SC RTO Membership.)

Signers of the letter include hotel chain Marriott, food and beverage brands Sierra Nevada and Nestle, solar power developer Carolina Solar Energy, and Unilever, along with advocacy groups such as the Carolina Utilities Customer Association and the Clean Energy Buyers Association (CEBA).

In a statement on CEBA’s website, Reese Rogers, the organization’s Southeastern market and policy innovation manager, said “expanding [the state’s] market options … would help drive innovation and cost savings for all energy customers and improve grid reliability and resilience.”

“House Bill 503 would open a path for North Carolina to move toward greater options for customer choice and grid reliability,” Rogers added.