The surge in large load growth across the Midwest presents MISO with both an enormous opportunity and a critical test. As energy demand accelerates, the region’s ability to attract and support these facilities will depend on whether MISO can modernize its interconnection processes to match the speed and scale of business need while maintaining the reliability the region requires.

The region’s energy needs demand that MISO include clean energy technologies to support rapid load growth. The fact is that clean energy offers the lowest-cost, fastest-to-market solution to meet rapidly increasing energy demand while reducing consumer costs and driving economic growth.

MISO’s initial zero-injection generator interconnection agreement (ZGIA) represents a workable clarification of existing practice that formalizes arrangements, as already applied to three facilities in MISO South. Limiting large load solutions only to zero-injection scenarios misses the mark and can create a myriad of challenges now and in the future.

CGA emphasized the need for better information sharing between processes that currently operate in isolation despite significantly impacting each other in planning models. Generator interconnection nominally aligns with MISO’s 18-month MTEP process but recently has been taking up to five years, a misalignment that creates inefficiencies preventing project development and driving up costs unnecessarily.

Beyond Zero-injection: Leveraging Clean Energy Solutions

MISO should expand its initial ZGIA concept to leverage a larger toolkit of clean energy technologies that can facilitate rapid large load integration while maintaining grid reliability. Three technologies are of significant importance: battery storage, renewable energy paired with storage (hybrid projects) and high-voltage direct current (HVDC) transmission.

Battery Storage as Reliability Solution

Four-hour battery storage is ready to enter MISO markets. Storage responds instantaneously to variations in large loads, including sudden trips offline. This rapid response capability could prevent cascading blackouts in the event a large load suddenly disconnects, offering a reliability benefit that will become increasingly important as large load projects proliferate. Meanwhile, CGA and its members are working on market entry paths for longer-duration storage to complement and extend the benefits of four-hour batteries.

Yet MISO uniquely assesses storage for transmission service during charging, a barrier that no other RTO imposes and that directly delays the deployment needed for large load reliability. MISO should align its rules with its peers and accelerate integration of storage resources already queued in substantial quantities by more realistically modeling the reliability attributes of batteries.

By treating storage as an asset instead of a liability, MISO’s interconnection queue could unleash utility-scale batteries and their grid benefits within approximately 18 months or faster with other improvements to provide flexible capacity while longer-term transmission infrastructure comes online. (See MISO Members Push for Modernized Storage Rules.)

Renewable Energy with Storage Co-location

Co-locating storage with renewable energy maximizes use of existing transmission capacity and improves reliability. Providing grid support with this configuration will allow MISO to integrate even more unprecedented amounts of new demand in a short period of time.

Additionally, MISO should prioritize efforts to refine interconnection rules that allow renewables, storage and HVDC to enter the market with limited operations rather than waiting years for upgrades to allow full operations. This enables needed resources to come online faster while maintaining reliability. MISO must do this in a way that ensures expedited interconnection rules don’t inadvertently favor any one technology or hinder the traditional interconnection queue. Open access policies foster resource expansion and competition that keeps lights on and costs down for all consumers.

HVDC Transmission for Interregional Solutions

While HVDC represents a longer-term solution than storage or hybrid deployment, it offers critical strategic benefits that will expand siting opportunities for data centers for better fiber connectivity, cooling infrastructure or other business reasons by delivering available generation when and where it’s needed.

This matters because a single HVDC line delivers gigawatts of capacity equivalent to multiple large power plants without requiring new local thermal generation, fuel supply chains or emissions, all while allowing the grid to be “bigger than the weather” for better reliability and affordability.

The Path Forward

MISO’s zero-injection clarification represents a constructive first step, and we appreciate MISO’s commitment to expanding the current rules to address today’s complex challenges. After all, the alternative is a patchwork of narrow solutions that fail to capture the full economic and reliability value these technologies offer.

The scale and diversity of load growth projected in MISO demands more ambitious solutions and innovation. By expanding interconnection options to fully leverage battery storage, hybrid renewable energy and HVDC transmission, MISO can turn the large load challenge into an opportunity for grid modernization that benefits all customers now and for generations to come. MISO has a historic opportunity to lead in integrating large loads reliably and cost-effectively. The region’s economic growth depends on seizing it.

MISO has the tools and the moment to lead. Clean Grid Alliance stands ready to work with MISO and all stakeholders to turn today’s large load challenge into tomorrow’s competitive advantage. The Midwest’s energy and economic futures depend on getting this right.

David Sapper, vice president of transmission and markets for the Clean Grid Alliance, has been involved in the wholesale electricity industry for nearly 30 years.

NERC officials appeared before an Organization of MISO States board meeting in an attempt to quell regulators’ discontent with MISO’s “high-risk” label in the 2025 Long-Term Reliability Assessment.

“I think we understand your concerns,” said NERC CEO James Robb, who referred to “anxiety” around the exclusion of MISO’s interconnection queue fast track in the LTRA. He said the LTRA “is not a prediction in any way.”

“It’s a risk assessment,” he told regulatory staff members at a Feb. 9 Organization of MISO States board meeting.

NERC found that by winter 2028/29, MISO would struggle with reliability under normal conditions. Some state regulators bristled at the designation and criticized the assessment for not including MISO’s expedited generator interconnection process and the projects in it.

Regulators also said NERC’s conclusion essentially ignores that most MISO states must plan resources in accordance with state law and that MISO measures its reserve margins differently from in NERC assumptions. (See MISO States Dispute ‘High Risk’ Designation from NERC.)

Robb said this year’s findings in the LTRA are a product of load growing faster than resources can be added or steadily dropping resource inventories. He said NERC is seeing “more and more” regions move into elevated reliability risk. “It’s been growing and growing in severity,” Robb said.

But over the years, he said, areas designated as “normal” in the LTRA have experienced emergency shortages while areas labeled “high risk” have pulled through difficult episodes.

Robb said the emergence of winter-peaking circumstances in the LTRA is due to an increasing deployment of solar generation suppressing the summer peak.

“Solar’s a hell of a resource. It doesn’t do a lot for you in winter,” he said.

He also said NERC has in recent years found more limits overall with generators and resources that have become especially susceptible in winter.

John Moura, NERC director of reliability assessment and system analysis, explained the data collection deadline that left off generation proposals in MISO’s interconnection queue fast lane. He said NERC must cut data collection off in summer to release the assessment. The deadline helps NERC understand which resources are firm and deliverable by transmission, Moura said.

Moura said time and again, NERC sees the most certain, “Tier 1” generation projects fail to meet stated in-service dates.

“So, expecting 20 GW and getting 10 GW. We really are seeing half the resources come in on time,” Moura said. “It’s not an indictment; it’s not a prediction. We are trying to showcase the risk … to stimulate the action needed.”

Moura said the industry is learning that the “individual, isolated planning that got us a long way is breaking down a bit.” He said neighboring regions need to understand one another’s systems more. NERC strives to provide a “bedrock,” he said, by using consistent assumptions.

Wisconsin Public Service Commissioner Marcus Hawkins cautioned NERC officials about assuming all new load at speed is gospel. He pointed out that the utilities reporting load additions stand to benefit from the boosted demand. He told NERC to be careful “if all upstream assumptions are from people with vested interests.”

Michigan Public Service Commission Chair Dan Scripps said it feels like states in an RTO get “picked on” because even though most states in MISO are vertically integrated and have the same state-level mandates to maintain resource adequacy, they nevertheless are coded red.

South Dakota Public Utilities Commissioner Chris Nelson asked NERC officials if they think the LTRA is read as a prediction by the public.

Robb said it “certainly seems” the LTRA is construed that way “despite our best efforts.” He added NERC hopes to “raise the flag” about getting more infrastructure built, and “not the old-fashioned way.” He said grid expansion is going to take changes to permitting and siting processes.

MISO Senior Manager of Market Design Neil Shah said at a Feb. 10 Entergy Regional State Committee meeting that MISO is in contact with NERC to try to improve assumptions used in the LTRA.

Shah said including the generator interconnection express lane likely would “close the gap” in the NERC report. However, he said uncertainty remains due to the potential for more large loads claiming spots on the grid.

MISO expects the first projects from its expedited generator queue to come online in 2028, Shah said. Beyond that, Shah said “MISO is projecting higher rate of new resource additions in 2026” than have historically come online annually from 2022 to 2025.

“It incorporates a lot of things that we don’t necessarily agree with,” Bill Booth, a consultant to the Mississippi Public Service Commission, said of the assessment. He added that in addition to the expedited queue omission, NERC didn’t factor in the trio of coal plants in MISO kept online via the U.S. Department of Energy’s emergency orders under the Federal Power Act’s Section 202(c).

MISO Promotes Stakeholder Involvement in Reworking NERC RA Standard

Meanwhile, MISO has encouraged its stakeholders to participate in NERC’s development of a new energy assurance draft standard after it scrapped the first draft.

MISO’s Zhaoxia Xie said at the January Reliability Subcommittee meeting that stakeholders should get involved. The reliability corporation’s first draft of a proposed planning energy assurance standard failed to get enough votes in support to advance. NERC’s standard drafting team is assessing next steps and is planning a technical workshop Feb. 17 and meetups Feb. 18 and 19 to start revisions.

NERC’s original design would have had planning coordinators conducting their own Long-Term Energy Reliability Assessments using an unserved energy basis and reporting the results to NERC. Resource planners and transmission planners then would have to prove they developed corrective action plans — enforced by the ERO — to address “unacceptable” levels of reliability risks in long-term assessments.

“MISO is being open-minded and working with NERC to move along this effort,” Xie said.

Minnesota Power’s Tom Butz said it seems the NERC effort is entering “uncharted territory” and that a draft standard could be an opportunity to view system reliability in a new way. Butz asked that the RASC plan for “hands-on interplay” with the NERC docket as it’s drafted.

Xie said MISO doesn’t plan to schedule stakeholder discussion on the standard “because the project is not moving as fast” as originally thought.

MISO staff also said the RTO already covers or exceeds what the standard originally intended to include; they said even the draft standard wouldn’t push its modeling into unfamiliar ground.

PJM’s Market Implementation Committee passed by acclamation a PJM issue charge seeking to more thoroughly define how storage resources participate in the energy and ancillary service markets.

Much of the focus was on PJM’s obligation under FERC Order 841 to implement storage state of charge in its energy storage resource rules, as well as how lost opportunity costs (LOCs) are determined. The issue charge was revised after January’s first read spelling out that the LOC discussion should consider how the timing of PJM dispatch interacts with changing prices, emergency conditions and supply/demand balance.

The list of additional items for consideration was expanded to include cost-based energy offers, calculation of uplift, LOC rules for storage participating in energy and ancillary service markets, and whether pumped storage hydro resources should be part of the conversation. It also includes must-offer rules for storage resources with capacity commitments, intraday offers, cost-based offers and resource parameters.

The out-of-scope section includes changes to resource adequacy, performance assessment interval and effective load-carrying capability modeling for storage; surplus interconnection service; storage as a transmission asset; the pumped hydro optimizer; and peak shaving adjustments. A sixth key work activity was added for a possible second phase to explore out-of-scope topics.

The issue charge envisions governing document and manual revisions being drafted within six to nine months, which stakeholders said is an appropriate timeline given the numerous other market redesigns being considered.

Carl Johnson, representing the PJM Public Power Coalition, said it’s important that PJM’s planning and markets departments both be involved in the stakeholder discussion and remain aware of the changes being made. In particular, planning models should account for any changes to how storage resources offer into the energy market.

Constellation Proposes Dual-fuel Quick Fix

Constellation presented a quick fix proposal to revise the must-offer requirement for dual-fuel capacity resources to recognize that dual-fuel gas resources have a downtime when switching fuels. The quick fix process allows an issue charge and problem statement to be brought concurrent with a proposed solution. The proposal is set to be voted on by the MIC at its March 11 meeting.

The proposal would specify that a dual-fuel resource met its must-offer requirement so long as it submits offers including the primary and alternate fuels within “limitations or restrictions resulting from fuel switching time modeling within PJM’s software platforms.” The language would be added to the capacity resource offer rules in Manual 11: Energy & Ancillary Services Market Operations.

Stakeholders said there may be differences in how units switch fuels or in the details of that switching period. They said a broad change that applies to all dual-fuel resources could help avoid the must-offer requirement.

ARR and FTR Timeline

PJM laid out the schedule for the 2026/27 auction revenue rights (ARRs) and financial transmission rights (FTRs) markets. Stage 1A of the annual allocation begins on March 4 before moving on to stage 1B on March 10. Stage 2 begins on March 18.

Trading for ARRs begins on April 2, while the annual FTR auction starts April 8.

PJM Presents Quick Fix Proposal on Battery Dispatch Modeling

PJM’s Julia Spatafore presented a quick-fix proposal to model battery storage dispatch in Regional Transmission Expansion Plan base cases. The quick-fix process allows an issue charge and problem statement to be brought alongside a solution.

Battery units are modeled as offline under Manual 14B: PJM Region Transmission Planning Process, which would be revised to allow them to be dispatched in the block dispatch methodology. The resources are already modeled as online in generation deliverability studies, a misalignment Spatafore said would be closed by the proposal. The change would also increase the generation available when planning transmission and support state policies promoting storage.

Transmission Expansion Advisory Committee

Transmission Projects for Large Loads

Dayton Power and Light presented a $246 million transmission project to supply an 800-MW service request of load near the Darby substation in Marysville, Ohio. A 765/345-kV substation, named Patina, would be cut into the existing 765-kV Marysville-Flatlick line. Two new 5-mile 345-kV lines would connect Patina to a new 345-kV substation, named Weaver, serving the customer. The project has an in-service date of May 1, 2031, and is in the conceptual phase.

Exelon presented a $263.5 million project in the BGE zone to serve an 880-MW customer near the Calvert Cliffs nuclear plant in Maryland. A 500-kV substation, named Camp Canoy, would be constructed with a 175-MVAR, 500-kV capacitor bank. It would be cut into the 500-kV Calvert Cliffs-Waugh Chapel and Calvert Cliffs-Chalk Point lines. The customer is seeking to come online in 2028 with 190 MW before reaching full capacity in 2030. The project is in the engineering phase, with a projected in-service date of March 1, 2028.

Exelon also presented a $245 million project in the ComEd zone to serve a customer seeking to bring 504 MW to the DeKalb, Ill., area. Two 345-kV substations, Charter Grove and Gurler, would be constructed to link the customer to the 345-kV Bryon-Wayne line. Charter Grove would cut into Bryon-Wayne, and a 16-mile 345-kV line would connect it to Gurler. A 1.5-mile 345-kV line would connect Gurler to the Keslinger substation, and two 345-kV lines would link it to the customer. The load is expected to come online in 2029 at 12 MW and ramp to 504 MW in 2033.

A $269 million project in ComEd would serve a 1.8-GW customer near Joliet, Ill., by constructing a new 345-kV substation, named Rowell, featuring two 150-MVAR, 345-kV capacitor banks. It would cut into the 345-kV Elwood-Goodings Grove line and link to four customer-owned substations. The customer is expected to come online in June 2029 with 225 MW and ramp to its full consumption in 2033. The project is in the conceptual phase, with an estimated in-service date of July 1, 2028.

A $145 million ComEd project is planned for a 1,296-MW customer near Coal City, Ill., involving the construction of a 345-kV substation, named after the village, with two 150-MVAR, 345-kV capacitor banks. It would cut into the 345-kV Dresden-Pontiac Midpoint and Lasalle-Braidwood lines. The customer is seeking to bring 216 MW online in June 2029 and grow to its full load in 2034. The project is in the conceptual phase with an estimated in-service date of July 1, 2028.

A $99 million project in ComEd would serve a 1-GW customer near Joliet by constructing a new 345-kV substation, named Hiawatha, with one 150-MVAR, 345-kV capacitor bank. It would cut into the 345-kV Kendall County E.C.-Collins line and feed two customer-owned substations with two 0.7-mile radial lines. The customer is seeking to come online with 30 MW in June 2028 and reach its full load in 2032. The project is in the conceptual phase with an estimated in-service date of June 1, 2028.

PPL presented a $220 million project to serve a customer seeking to service 1 GW of load in Archibald, Pa. A new 500/230-kV Archbald Mountain Switchyard would be constructed, cutting into the 230-kV Callender Gap-Paupack and the 500-kV Lackawanna-Hopatcong lines. Archbald Mountain would be connected to Callender Gap with a new 4.6-mile double-circuit 230-kV line and to the customer substation with a 4-mile single-circuit 230-kV line. The customer is expected to come online with an initial load of 166 MW in 2027 and reach 900 MW by 2030, before reaching 1 GW the following year. The project is in the development phase, with a projected in-service date of May 30, 2028.

Dominion Energy presented three projects to serve data centers in Caroline and Spotsylvania counties and Petersburg, Va. They total $106 million and would serve at least 912 MW.

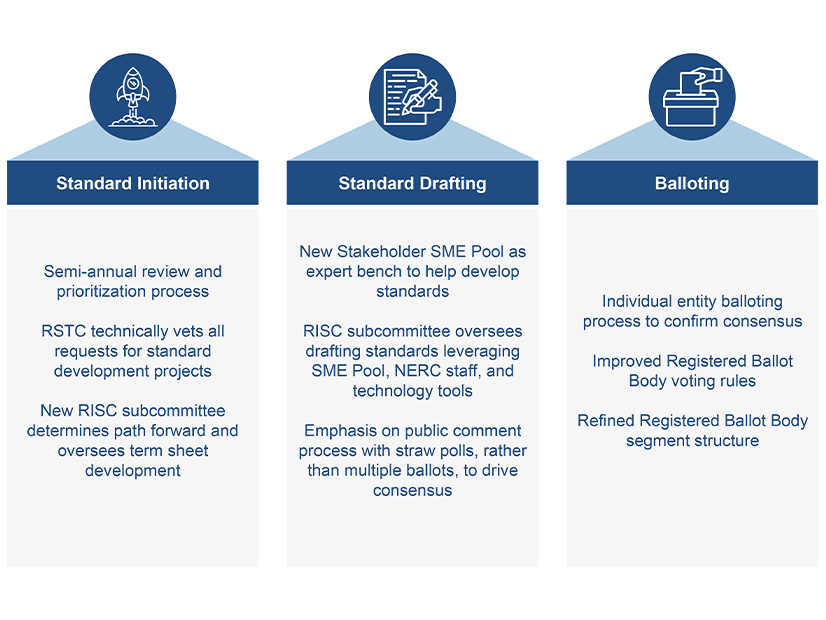

Stakeholder comments on NERC’s proposed changes to its reliability standards development process revealed widespread support for the ideas in principle, with suggested revisions to specific aspects of the plan.

The MSPPTF’s recommendations include initiating standards projects through a biannual review and prioritization process conducted by the Reliability and Security Technical Committee and creating a new subcommittee of the Reliability Issues Steering Committee to determine a plan of development. A “fast track” process that skips certain steps would be permitted for urgent projects.

Updates to the drafting process — covering the writing of proposed standards — would have NERC staff and a pool of subject matter experts create an initial draft of a new standard that can be refined through industry feedback. Stakeholders could submit comments during the process and vote on the final product. The voting process would also be streamlined by restructuring the ballot body and updating the voting rules.

Stakeholder comments were accepted through Feb. 5 and drew feedback from 18 utilities, trade associations and regulators. NERC published the responses Feb. 9 ahead of the board meeting.

Most commenters expressed appreciation for the MSPPTF’s work as a starting point while suggesting further changes. American Electric Power asked that NERC ensure the task force is not “a one-time effort” by establishing a team, selected by industry, to “continuously review and enhance the standards development process.” AEP expressed concern that the MSPPTF’s original goal “was narrowly focused on accelerating the process, rather than both accelerating it and improving the quality of the resulting standards.”

“The MSPPTF’s recommendations rest on an implicit assumption that increased engagement results in better outcomes; however, early engagement alone does not equate to higher-quality standards,” AEP continued. The company also suggested that NERC conduct a pilot using two standard initiation requests — the proposed term for the documents that would start the development process — to allow practical examination of the new process.

The MSPPTF summarized its recommendations in an informational session ahead of NERC’s Member Representatives Committee meeting. | NERC

The ISO/RTO Council (IRC) also supported a pilot project while encouraging NERC’s board to ensure sufficient resources are available to support implementation of the recommendations. The IRC further reminded the board of “the potential need for region-specific variances,” especially in Canada, and explicitly encouraged the expansion of existing procedures for developing variances on standards to allow Canadian entities to pursue variances in their territories.

Both Electricity Canada and IESO joined the IRC in urging that NERC ensure Canadian participation in the process is protected. Electricity Canada approved of the MSPPTF’s recommendation for “sufficient Canadian representation in the membership of the RISC subcommittee” and echoed IESO and the IRC in requesting additional provisions to allow both Canada-wide and “more granular provincial variances” to standards.

IESO also suggested that the proposed SME pool be solely responsible for creating initial standard drafts, rather than a combination of SMEs and NERC staff. The move “would reduce the risk of over-reliance on NERC staff, who may not always have the specific expertise required for certain standards,” IESO wrote.

Several commenters shared reservations about the proposed revisions to the registered ballot body, particularly the idea of consolidating and eliminating segments. For example, large and small end-use customers would be merged into a single group, electricity end users; electric generators would be combined with brokers, aggregators and marketers; and regional reliability organizations and regional entities would be combined with federal, state and provincial regulatory or other government entities.

Michigan Assistant Attorney General Michael Moody and Pennsylvania Consumer Advocate Darryl Lawrence — who represent small end-use customers on the Member Representatives Committee — criticized the proposal to eliminate the sector. The task force justified this move by the “lack of participation” of the sector in the existing standards process, but Moody and Lawrence wrote that this argument “elevates participation metrics over equitable and meaningful representation.”

“While industry frequently raises concerns about regulatory burden, in practice, many standards create predictable cost recovery pathways that are often welcomed rather than resisted,” Moody and Lawrence wrote. “NERC has a responsibility to ensure that the public interest has appropriate weight in a forum that is already dominated by well-resourced, profit-motivated industry interests.”

The American Clean Power Association disagreed with combining brokers, aggregators and marketers with generators, writing that the merger would “water down the existing representation spots for” independent power producers; ACP instead suggested that IPPs be given their own category “to ensure that [they] are sufficiently represented.”

Invenergy also objected to eliminating the brokers, aggregators and marketers segment, arguing that it “represents a unique function and business model among stakeholders.” The utility observed that 71% of entities represented in the load-serving entities segment are also represented in the transmission owners segment, but neither of these has been proposed for elimination.

“We urge NERC not to eliminate this stakeholder pool from its balloting process (which would also eliminate some entities’ balloting rights entirely),” Invenergy wrote. “Retaining [the brokers segment] is in keeping with NERC’s laudable goal to maximize stakeholder engagement to foster and accelerate reliability standards … by virtue of an inclusive stakeholder consensus-building process.”

PJM, Voltus and the RTO’s Independent Market Monitor presented proposals to establish penalties for demand response and price-responsive demand (PRD) resources that fail to perform during a pre-emergency load management event.

Penalties are being considered after a summer of poor performance in 2025, when six pre-emergency load management events totaling 30 hours had a weighted average performance of 67%. PJM has no penalties in place for poor performance outside a performance assessment interval (PAI). (See “PJM Proposes Performance Penalties for Non-emergency Load Management,” PJM MIC Briefs: Jan. 7, 2026.)

The PJM proposal would penalize resources with poor performance at half the rate for PAI events, which is around $2,300/MWh for the 2027/28 delivery year. That would be accomplished by mirroring the PAI penalty formula but doubling the number of expected deployments for pre-emergency events to 60.

PJM’s Pete Langbein suggested the modeled number of deployments might be worth considering further, noting there have already nearly been 60 events this delivery year. He presented the PJM solution to the Market Implementation Committee on Feb. 4.

The allocation of revenue collected through the penalties was revised since the January MIC meeting so bonuses would be evenly split between load-serving entities (LSEs) and curtailment service providers (CSPs) if overall performance were deficient. If the fleet overperformed during an event, the bonuses would be entirely allocated to CSPs.

Monitor Proposal Seeks to Withhold Market Revenues

The Independent Market Monitor proposal would withhold daily capacity payments from underperforming resources going back to the last event or test where they met their obligations to their next successful deployment. The payments would be pro-rated to scale with the shortfall.

The Monitor argued that PJM’s proposal undermines the incentive to improve performance by allowing lagging resources to continue collecting significant revenues. It gave an example of a 100-MW resource that does not curtail at all during a 12-hour deployment; it would be assessed a $1.4 million penalty under the PJM proposal, which is 12.2% of its annual capacity revenues.

For proposals including a penalty, the Monitor wrote that the associated revenues should be allocated entirely to LSEs.

The proposal would adjust the effective load-carrying capability (ELCC) rating for individual resources based on their historic performance, and PRD accreditation would be set at the lesser of a unit’s summer or winter nominated installed capacity.

Voltus Reworks Proposal

The Voltus proposal would set the penalty rate at 8.3 to 25% of the PAI rate, depending on the number of non-emergency load management hours modeled and the share of net cost of new entry (CONE) it was designed to recover. Net CONE would be reduced by a quarter to half to account for the reduced reliability risks with a pre-emergency event, and the number of events would be assumed to be two to three times greater than 30 PAI hours.

The penalty revenues would be allocated to overperforming resources with a cap 1.2 times the penalty rate; any remaining funds would go to LSEs.

Voltus proposed reducing the penalty and increasing the bonus cap should the number of non-emergency events exceed the amount modeled to reduce dispatch fatigue. The prospect of deployments becoming increasingly common as the capacity market tightens has led to alarm bells from CSPs who have argued that many participants will drop off if the financial impact of curtailments exceed their capacity market revenues.

While PJM experienced some of its highest peak loads ever during the late January winter storm, it overestimated load, with relatively high load forecasting errors, RTO officials told the Operating Committee.

PJM’s Paul Dajewski told the Operating Committee on Feb. 5 that while operations were strained during the Jan. 24-27 storm, named “Fern” by The Weather Channel, load did not quite reach the forecasted peaks and the RTO maintained reliability.

“We were able to operate through this period reliably; we did have sufficient generation reserves; we were able to serve our loads; we were able to serve our exports,” Dajewski said, adding that PJM provided emergency energy sales to neighboring regions.

PJM saw an instant peak load of 140,049 MW on Jan. 29 at 8:05 a.m. and two new top 10 hourly integrated peaks of 139,046 MW on Jan. 29 and 138,479 MW the following day. It noted that the data are preliminary.

Dajewski said there was a lot of uncertainty with preparing for the storm, owing to the duration of the freezing temperatures, pipeline flexibility, fuel storage, generators running into emission limits, load forecast accuracy, and the interplay between when gas resources are committed and when they purchase fuel from pipelines.

PJM asked that generators cut short maintenance outages between Jan. 25 and Feb. 2, reducing some transmission constraints. The RTO declared a long-duration extreme event, so fuel-limited resources were required to signal when they have 32 hours or less of fuel inventory, rather than the standard 16-hour notice.

The load forecast error was high between Jan. 26 and 29, peaking with an 8% over-forecast on Jan. 27. PJM’s Joseph Mulhern said temperatures were not quite as low as expected and that it’s possible the RTO’s modeling did not properly account for building closures. PJM said that it is difficult to predict the number of buildings that will close because of the weather, as the decisions are based on subjective, location-specific factors.

Stakeholders expressed surprise that building closures would contribute to load falling gigawatts below the forecast. Mulhern said PJM is exploring the issue further.

Transmission constraints and limited ramp capability drove $797.6 million in uplift costs, mostly in balancing operating reserve charges. There were $577.9 million in make-whole costs, $98.2 million in lost opportunity costs and $121.6 million in day-ahead operating reserve charges assigned. PJM is working on a more detailed breakdown of the make-whole costs for stakeholders.

Conservative operations were used to secure advance commitments, which PJM’s Brian Chmielewski said contributed to the make-whole costs. Pre-emergency load management was called in the BGE, Dominion and Pepco zones Jan. 25 for localized transmission constraints, and maximum generation, load management and low-voltage alerts were issued for Jan. 27.

PJM’s Brian Fitzpatrick said gas pipelines performed “very well,” with only one compressor station failing and 1,500 MW of generation interrupted. Winterization efforts on gas production appear to have led to a decrease in reduced output during winter events, with 5% production lost in Appalachia and 9% across the country. Nonetheless, spot prices were some of the highest he has seen, reaching $300/MMBtu on some interfaces.

Even with actual load coming in below forecast, Fitzpatrick said there was a lot of concern in the gas market about the duration of the storm, high loads and potential scarcity.

“That inherent fear in the market drove those prices,” he said.

PJM received Department of Energy waivers under Section 202(c) of the Federal Power Act to operate 39 units totaling 5.2 GW past environmental permit limits for 1,035 hours. The department also invoked a lesser used 202(c) provision to make backup generation available, but those units were not dispatched. (See Wright Ready to Use Emergency Powers to Dispatch Backup Generation During Winter Storm.)

PJM’s Joe Ciabattoni said the day-ahead bid period was extended on Jan. 26 and 27 because of issues running credit checks on market participants. It took longer for staff to accept bids because of the number of offers exceeding $1,000, triggering the automatic offer verification process.

A severe cold snap Jan. 16-21 preceded the storm, but it was much easier for the RTO to manage, with no emergency actions taken. The generation fleet performed well, and no emergency procedures beyond cold weather advisories or alerts were required. Load peaked at 135,121 MW on Jan. 21 at 7:40 a.m. with no load management deployed.

While all pipelines enforced the restrictions in their tariffs, there was no drop-off in production, and fuel remained available and relatively affordable for dispatched units. No advance commitments were made in preparation.

An offshore wind group has urged the California Public Utilities Commission to reject an internal proposal to use a forecast six-year delay to a Humboldt County offshore wind project to inform the state’s grid planning.

Representatives of Offshore Wind California (OWC) said the Humboldt offshore wind project’s online date in the forecast should be revised from 2041 to 2036, according to a Feb. 6 filing with the CPUC.

The projected six-year delay should be eliminated because offshore wind projects are moving ahead on the East Coast, despite Trump administration actions to attempt to hinder them, OWC said.

“Offshore wind is demonstrating its legal as well as business-case durability, even while under attack by the current administration,” OWC said in the filing. “Planning assumptions that doubt offshore wind’s ability to succeed do not reflect the prevailing legal reality. Nor do they capture the realities of steel in the water, which show eight projects are proceeding towards completion on the U.S. East Coast that will deliver more than 6 GW of clean power by 2027.”

Transmission planning often occurs over decades: The CPUC should not delay making important infrastructure decisions to react to what are likely to be short-term federal policy headwinds, OWC added.

California’s offshore wind projects will not need federal permitting for several years, so the Humboldt project could be online in 2036, the same time as the Morro Bay offshore wind project along the state’s central coast, OWC said.

The CPUC should eliminate the limited wind sensitivity case in the commission’s Jan. 14 proposed decision on the matter, OCW said. The group said the portfolio is “unreasonably conservative and unnecessary and directly conflicts” with California AB 525, which shows 25 GW of offshore wind generation by 2045, CAISO’s $4.6 billion in transmission investments to support offshore wind and the $475 million approved to upgrade port infrastructure for offshore wind.

The CPUC included the limited wind case portfolio due to recent increased difficulty of permitting wind projects and federal policy changes toward the projects, the commission said in the proposed decision.

Something strange is happening in American energy policy. U.S. Sen. Elizabeth Warren (D-Mass.) and Florida Gov. Ron DeSantis (R) are worried about the same thing: energy-guzzling data centers. Likewise, Sens. Bernie Sanders (I-Vt.) and Josh Hawley (R-Mo.) both seem to want an abrupt pause on new artificial intelligence.

Although the Trump administration favors artificial intelligence and data centers, many of the industry’s biggest detractors are sure to run for president in two years. And some states, including New York, are considering statewide bans on new data centers. Local opposition has long been a thorn in the side of data center development and is growing.

A clear political threat to the industry is brewing within both major parties and at all levels of government. What the industry needs is a hedge against bipartisan political risk.

Major tech companies, including Microsoft, Google and Amazon, have announced huge investments in generation assets. Meta announced in January that it would expand its nuclear power purchases by 6.6 GW. For reference, that’s more than three times the output of Hoover Dam.

These tech companies’ thirst for “juice” is apparent. But what if policymakers don’t want them on the grid?

Travis Fisher

In Warren’s recent announcement of an investigation, she and fellow lawmakers alleged that “American families bankroll the electricity costs of trillion-dollar tech companies.” In Florida, DeSantis and state lawmakers are proposing a new suite of regulations on data centers.

More than 230 groups — including environmental and consumer organizations — have called for a national moratorium on new data center construction. Dramatic headlines such as “AI Is Making Your Life More Expensive” are common.

It matters little that the political alarm over data centers is misguided. In fact, Warren’s assertions may be the opposite of the truth. As Nick Myers of the Arizona Corporation Commission recently explained in RTO Insider, data centers “provide long-term, stable demand that may reduce the financial risk of utilities and lower their borrowing costs to the benefit of all customers.”

Researchers have found the “effect of sales growth on rates is highly situation-specific” and largely depends on how new costs are allocated among customer classes. At best, it’s a murky policy area that lends itself to political scapegoating.

So, what can the industry do to protect itself from a populist uprising? One alternative is to allow new industrial customers to develop or join a private, fully off-grid energy system. My colleague Glen Lyons and I call this idea Consumer-Regulated Electricity, or CRE.

Going one step further than typical “behind-the-meter” arrangements with generators, CRE would enable a new, islanded system with no physical connection to the regulated grid. A data center could join many others on an industrial campus powered by whatever resources make sense — solar, batteries, gas turbines, nuclear reactors, you name it — and operate without connection to the utility grid.

Importantly, the lack of a grid connection also means freedom from political meddling. A new proposal by Sen. Tom Cotton (R-Ark.), titled the DATA Act, would exempt large users from regulation by FERC. Operating on a separate electric grid means no risk of causing blackouts for American families and businesses. Hence, the onerous regulations that apply to the “bulk power system” need not apply to independent facilities.

Like the Trump administration, today’s FERC is supportive of data centers and their hunger for electricity. However, the industry should be prepared for a one-two punch of reduced independence at FERC and a new president who wants to cut off electricity supplies to data centers.

For example, DeSantis recently said, “We have a limited grid. You do not have enough grid capacity in the United States to do what they’re trying to do.” If efforts to expand the grid fail or move too slowly — which seems likely — then the pitchfork mob might come for data centers.

States also can help enable the CRE option and insulate households from rising costs or uncertainty created by data centers. New Hampshire has taken the leap, and Ohio and Utah have enabled private electricity systems.

More states are likely to follow suit now that the American Legislative Exchange Council has approved model legislation that would create a path for CRE in any state.

A common critique of CRE is this: “We need AI data centers to help pay for the grid.” Yes, the blackboard economics view of grid supply tells us that retail rates should fall for everyone as the total watt-hours on the grid increase and grid utilization improves. But in the real world, risks abound, and no one can guarantee the AI bubble will never burst.

Indeed, the highly uncertain risk to American families of a sharp increase in their utility bills to pay for infrastructure intended for a collapsed data center industry may be unacceptable to some policymakers.

Far from a “libertarian fantasy,” private grids already are being built, and the data center industry should view policy reforms like CRE as a practical way to hedge political risk. Even if the value seems far-fetched today, why not establish CRE reforms now in case of a future political emergency? Data centers are not the villain, but it may be impossible for them to win the debate in a hostile environment, and the industry would be wise to protect itself against political warfare.

Travis Fisher is director of Energy and Environmental Policy Studies at the Cato Institute.

In Massachusetts, a state with some of the most ambitious decarbonization policies in the country, fundamental disagreements between utilities and consumer advocates threaten to derail the transition from natural gas before it even gets off the ground.

While technical in nature, these disagreements ultimately boil down to different visions of the role of the gas system — and the role of its utilities — in a decarbonized Massachusetts. With affordability already dominating energy politics throughout New England, the direction and effectiveness of the state’s transition could have major implications on consumer costs for years to come.

The arguments over the future of the state’s gas system are not new; many of the underlying disagreements date back to the Department of Public Utilities’ multiyear and at-times-controversial investigation into whether to maintain the system while decarbonizing the fuel, or transition completely away from it altogether.

Initiated in 2020 under Gov. Charlie Baker (R) at the request of then-Attorney General Maura Healey (D), the investigation highlighted the major differences in the strategies proposed by the investor-owned gas utilities and climate and consumer advocates.

Throughout the proceeding, the utilities promoted a strategy reliant on alternative fuels and hybrid electrification. This proposed approach would keep much of the state’s gas network in place to back up electrified heating while blending hydrogen and “renewable” natural gas (RNG) into the system to lower the carbon intensity of the fuel.

By contrast, climate advocates pushed for a full-electrification strategy. They argued that alternative fuels like RNG and hydrogen are expensive, scarce and ultimately non-viable for residential heating at a large scale, and that a hybrid electrification strategy would lead to excessive costs associated with building out the electric system while continuing to invest in the existing gas network.

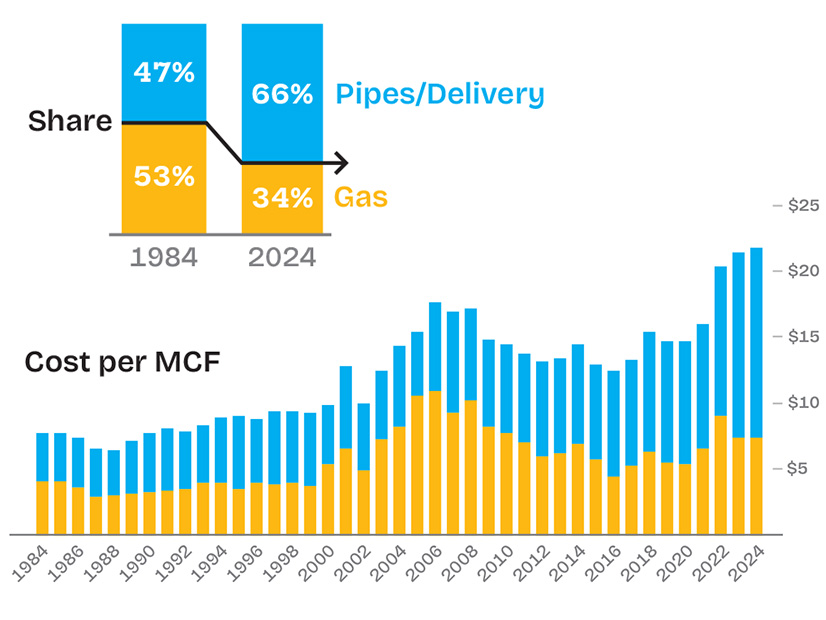

Residential gas delivery charges and supply costs in Massachusetts, 1984-2024 | Future of Heat Initiative

The DPU concluded the investigation in late 2023 under new leadership appointed by Gov. Healey, who took office at the start of that year. While climate advocates had criticized the DPU under Baker for relying on utility-hired consultants to conduct the technical analysis for the investigation, the department ultimately agreed with the advocates on the core issues.

With the order, the department established a regulatory framework “to move the commonwealth beyond gas and toward its climate objectives.” It expressed skepticism about the cost effectiveness of a “broad hybrid heating strategy” that maintained the bulk of the state’s gas distribution system. The DPU also declined to allow utilities to recover costs associated with procuring alternative fuels, citing concerns about “costs, availability and the treatment of renewable fuels as carbon neutral.”

The order required the utilities to file “climate compliance plans” plans every five years, evaluate non-pipeline alternatives when making gas system investments, cease promoting gas expansion with ratepayer funds and pursue targeted electrification pilot projects (D.P.U. 20-80-B). (See Massachusetts Moves to Limit New Gas Infrastructure.)

But in the two years following the landmark order, the conflicts that defined the DPU’s investigation have continued in the regulatory proceedings that have branched out from the ruling.

Across proceedings related to gas demand forecasting, pipe leaks, the climate compliance plans and the future of the region’s only LNG import terminal, the utilities have butted heads with proponents of the transition.

The utilities have been slow to embrace gas alternatives and pipe decommissioning at scale, which their critics attribute to the companies’ profit motive and reluctance to give up their traditional business model.

In contrast, the utilities have dug in on the language of customer choice, and they argue they lack the legal authority to decommission pipes without obtaining the consent of all affected customers. They argue that if a single customer on a pipeline segment is not willing to give up gas service, they cannot decommission the pipeline, even if electrified alternatives are available.

While advocates dispute this reading of state law, the question about the utilities’ authority to retire parts of the gas system remains unsettled, as does the underlying question of whether the state will ever be able to get its investor-owned utilities to embrace a transition away from gas.

The Obligation to Serve

According to the state’s gas distribution companies, their obligation to provide gas to existing customers stems from their franchise rights as regulated utilities.

“In exchange for a monopoly franchise, LDCs [local distribution companies] must actually provide natural gas service to customers absent the legislature rescinding their franchise charter or other clear legislative action alleviating the obligation to serve customers residing in a franchise territory,” the companies wrote in a joint filing in October in response to an inquiry by the department (D.P.U. 25-40, et al.).

In contrast, climate and consumer advocates argue the utilities’ obligation to serve does not prohibit the companies from substituting gas service for alternatives — such as networked geothermal or other electrified heating technologies — when viable alternatives are available. They point to a 2024 change in state law, which, according to its the lead senator in the negotiations, amended the obligation to serve to prevent issues related to holdout customers. (See Mass. Clean Energy Permitting, Gas Reform Bill Back on Track.)

The 2024 law directed the DPU to consider the public interest and the availability of non-gas alternatives for heating and cooking when ruling on petitions for gas service. It also explicitly authorized the department to “order actions that may vary the uniformity of the availability of natural gas service.”

The utilities argue that this change in law changed neither the “the legal foundation for the obligation to serve existing customers” nor the “obligations of the LDCs to existing customers.”

The Massachusetts Attorney General’s Office, the official ratepayer advocate in the state, disagrees. It argued in response that the DPU is well within its authority to authorize the disconnection of gas customers to advance the public interest.

With the 2024 changes to state law, “the legislature aligned the obligation to serve with the commonwealth’s climate goals by expanding the power of the department and articulating a balancing test to weigh the interests of the commonwealth with the interests of the individual customer,” the AGO wrote.

“It is illogical to suggest that the LDCs and department lack the authority to deny or discontinue gas service to promote the public interest in cost-effective decarbonization,” it added.

The DPU has yet to rule on the question of the utilities’ obligation to serve, and its interpretation of state law could face legal challenges from the utilities if the department ultimately sides with the consumer advocates. The potential impacts are substantial.

“It’s a very important issue,” said Jamie Van Nostrand, who led the DPU from 2023 through fall 2025 and oversaw the department’s order on the gas decarbonization investigation. He is now policy director for the Future of Heat Initiative. (See Outgoing Mass. DPU Chair Van Nostrand Discusses Gas Transition.)

Under the utility interpretation of the statute, “it’s all about customer choice, and if the customer wants to keep their gas, end of discussion — no decommissioning,” he said. “That is a bad outcome, because we need to have a managed transition.”

Stranded Assets

A managed transition, Van Nostrand said, is essential for long-term energy affordability in the state. Since leaving the DPU in the fall, he has been vocal in the ongoing affordability debates in the state, raising the alarm about the trend of increased spending on gas infrastructure.

According to an analysis by the Future of Heat Initiative, gas utilities in the state more than doubled their assets between 2014 and 2024, significantly increasing customer costs despite a 22% decline in per-customer gas demand.

“If you can’t shrink the system as the throughput goes down, delivery charges go through the roof; it’s simple math,” Van Nostrand said.

A large portion of this spending has occurred under a state program that gives the gas companies expedited cost recovery for replacements of leak-prone pipes. The costs of the Gas System Enhancement Plan (GSEP) program have risen rapidly in recent years, totaling $814.4 million in 2024. In total, the utilities spent more than $4.7 billion through the program between 2015 and 2024.

In an attempt to rein in the spending, the state has made several amendments to the GSEP statute in recent years to increase emphasis on pipe relining and repair, along with non-pipe alternatives, including networked geothermal.

But despite the efforts to curb spending and prevent stranded assets, costs have continued to rise, and traditional pipe replacements continue to constitute essentially all GSEP projects.

According to the utilities, the rise in GSEP costs is the result of the effects of inflation and supply chain constraints on the prices of materials and labor. In a written response to questions, Eversource Energy, one of the two major gas utility companies in the state, wrote that it already has replaced the bulk of the most accessible pipes and that its remaining portions of leak-prone pipes tend to require more complicated and expensive construction.

The company said an increased focus on pipeline repair would not help limit costs, writing that “there is no viable method for ‘repairing’ leak-prone infrastructure in a manner that obviates the need for replacement or that achieves the level of public safety that is achieved through replacement.”

“Prioritizing repairs over replacement can lead to higher longer-term costs, as sections of leak-prone pipes will likely require multiple future repairs and ultimately be replaced anyway, at which point the cost of replacement will have likely increased,” it added.

Van Nostrand did not dispute the underlying economic conditions, but he did highlight the attractive financial proposition to the utilities of expedited cost recovery, as well as the regulatory incentive structure that enables the utilities to earn more money from capital investments than from operating expenditures.

“Utilities are going to respond to whatever mechanism the regulators put in front of them,” he said. “They have a fiduciary obligation to shareholders to maximize profits, and that’s what they’re going to do.

“It’s great for shareholders to replace [pipes]; it’s bad for ratepayers. If your state has an aggressive greenhouse gas target like Massachusetts does — net zero by 2050 — putting a pipe in the ground that’s going to last 50, 60 [or] 70 years does not make any sense.”

He said expedited cost recovery on the GSEP investments has removed the important check on utility spending that regulatory lag provides in traditional ratemaking. This lag between when utilities increase their spending and when rates go up “provides a strong incentive for the utility to control costs,” he said.

In April, the DPU lowered the cap on GSEP spending from 3 to 2.5% of total firm service revenues and indicated it will likely cut the cap to 2% in 2026 and 1.5% in 2027. The cap reduction, coupled with a ban on carrying charges, is intended to limit the amount of spending for which the utilities can receive expedited cost recovery. (See Mass. DPU Aims to Align Gas Leak Program with Climate Strategy.)

While questions about the obligation to serve could inhibit the use of non-pipe alternatives instead of traditional pipe replacements, “the vast majority of these projects aren’t even getting to that point of having conversations beyond just the internal utility screening,” said Jeremy Koo, assistant director of clean energy at the Metropolitan Area Planning Council, a regional planning agency representing municipalities in the Boston area.

He said there is “definitely a lack of transparency” around why utilities have ruled out repairs and non-pipe alternatives for GSEP projects.

“We’re really concerned about it from the perspective of stranded assets,” he said, noting that the utilities’ approach appears to entail increasing levels of investment in both the gas and electric systems, with ratepayers left with the costs.

He added that he is similarly concerned that lower-income customers who lack the means to exit the gas system will become saddled with an increasing share of the gas system’s growing fixed costs.

Separate but Related

The utilities’ increasing investments in pipe replacement bears more than a few similarities to growth of asset condition costs on New England’s electric transmission system.

Asset condition spending, which is aimed at upgrading deteriorating transmission infrastructure, has cost the region $4.67 billion for projects placed in service since the start of 2020, according to an October update from the region’s transmission owners.

Eversource and National Grid, which own the largest gas utility businesses in Massachusetts and two of the three largest electric transmission footprints in the region, are responsible for the vast majority — $4.2 billion — of asset condition spending since 2020. Asset condition investments are subject to limited regulatory scrutiny, passing to ratepayers through FERC formula rates.

Concerns about the spending have caused the New England states to make a big push for increased oversight and transparency into the projects over the past several years, and ISO-NE is establishing internal asset condition review capabilities that could provide information for potential challenges of the spending with FERC.

But at a recent event held by the Northeast Energy and Commerce Association, Rhode Island Public Utilities Commission Chair Ron Gerwatowski said this might not be enough. He said the states may need to consider changing how transmission costs are recovered through electric rates.

To reduce the TOs’ appetite for spending, he said, the states could introduce regulatory lag by requiring them to recover costs through the full base rate case process, instead of as pass-through costs.

Echoing Van Nostrand’s comments on gas pipe replacement spending, Gerwatowski said subjecting asset condition spending to regulatory lag “could give the financial folks an incentive to push back” on the investments. (See Facing Rising Demand, New England has Limited Options for New Supply.)

‘A Very Expensive Insurance Policy’

As regulators eye a managed transition away from gas, the future of the Everett Marine Terminal (EMT), an LNG import facility just north of Boston, remains a multimillion-dollar question mark. Similar to the GSEP program, questions about the gas utilities’ obligation to serve could have a major bearing on the terminal’s future.

The LNG facility is on the site of the Mystic Generating Station, a retired gas-fired power plant that was once its primary customer. The plant retired in 2024 at the end of a two-year reliability-must-run agreement with ISO-NE.

To keep the EMT in operation following the closure of Mystic, the Massachusetts gas utilities signed contracts with Constellation Energy, the owner of the facility, to keep the terminal open into 2030. (See Massachusetts DPU Approves Everett LNG Contracts.)

In the DPU’s approval of the contracts, it acknowledged the importance of the facility to ensure the reliability of the region’s gas system during peak days, but it directed the gas distribution companies to take action to reduce their reliance on the facility.

The EMT is located at a strategic location at the heart of the state’s gas system, has access to both the Tennessee and Algonquin pipeline systems, and can feed directly into National Grid’s distribution network.

“That was a tough decision,” Van Nostrand said. “Basically, it’s a very expensive insurance policy.”

Gas customers in the state could face significant additional costs once the contracts expire if the utilities can’t eliminate their reliance on the facility.

Despite the regulatory requirements and a state-led working group focused on eliminating the state’s reliance on the facility, “another round of contracts seems incredibly likely,” said Carrie Katan, policy advocate at the Green Energy Consumers Alliance.

Katan, a member of the state’s Everett working group, said, “At this point, it does not look like either NSTAR [one of Eversource’s two gas distribution service territories] or National Grid are going to be able to basically function without EMT post-2030.”

A proposed expansion of the Algonquin pipeline system may cut some of Eversource’s reliance on Everett. The company’s recently approved firm transportation agreements associated with the expansion project would eliminate the need to extend the Everett contract for one of its service territories and partly eliminate the reliance on the terminal for its other service territory, Eversource wrote (DPU 25-133, 25-134).

But eliminating reliance on the terminal in one service territory could result in shifting the facility’s significant fixed costs onto gas customers in other areas still reliant on it.

It is also unclear what Constellation might charge to keep it open past 2030.

“Constellation is not operating on any kind of cost-of-service agreement: They can charge whatever price they want, and if they wanted to shut down EMT whenever they decided to, they could do that,” Katan said.

Van Nostrand concurred: “The LDCs put themselves in a position where they’re pretty much at Constellation’s mercy.”

Katan said National Grid appears to be in the “weakest negotiating position,” adding that “it really does seem to me that [Constellation] could decide to squeeze National Grid as hard as possible, and I don’t know of anything National Grid can do.”

National Grid declined to comment on whether it expects to seek additional contracts with Constellation. It said in a statement that its “responsibility is to operate a safe, reliable gas system for the customers who count on us, which requires making the investments necessary to keep aging infrastructure secure.”

Eliminating reliance on the Everett facility would require “a number of interventions, which would take a large amount of time,” such as strategic electrification or a moratorium on new gas hookups in EMT-constrained areas, Katan said.

But the utilities’ insistence that they cannot decommission lines without the consent of all customers complicates the picture.

While neighborhood-wide networked geothermal heating systems had drawn significant attention in the state in recent years, including pilot projects run by Eversource and National Grid, “if you want to deploy networked geothermal on a large scale outside of the pilots, you’re going to have to decommission the gas lines,” Katan said.

If the state cannot decommission pipes, “I don’t think we have anything when it comes to controlling gas costs,” she said. “I think at that point you would just need to accept that the situation is bad, it will get worse, and there is absolutely nothing that can be done about it.”