A bill in the Colorado legislature seeks to reduce the environmental impact of federal orders delaying the retirement of coal-fired power plants.

House Bill 26-1226, introduced Feb. 18, would require utilities to report quarterly on the costs of running coal plants beyond their retirement dates. It would limit nitrogen dioxide and sulfur dioxide emissions from coal plants that are still operating in 2031.

The bill also would direct the Colorado Public Utilities Commission to approve new resources to help the state meet its 2030 climate goals.

HB26-1226 follows a U.S. Department of Energy order under Section 202 (c) of the Federal Power Act to keep Unit 1 of the coal-fired Craig Generating Station operational for 90 days, which the department said was needed to prevent blackouts. The order was issued Dec. 30, a day before the unit was set to retire, as had been planned since 2016. (See DOE Blocks Retirement of Another Coal-fired Plant.)

State Sen. Mike Weissman (D) said the Trump administration was using the order “to turn years of careful planning on its head.”

“This will result in increased air pollution, higher energy costs and a delay in achieving our renewable energy goals,” Weissman said in a statement. HB26-1226 “gives the state tools to address these impacts.”

In addition to Weissman, the bill’s major sponsors are Rep. Jenny Willford, Rep. Meg Froelich and Sen. Lisa Cutter, all Democrats. The bill has been referred to the House Energy and Environment Committee.

The Sierra Club supports the bill, pointing to the costs of keeping aging coal plants running. A Grid Strategies report, commissioned by the Sierra Club and other environmental groups, found that the cost to ratepayers of keeping Craig running past its retirement date would be about $80 million/year.

“We urgently need laws like this to protect our state against the high price — both financial and environmental — the federal government is trying to foist on us,” Sierra Club Colorado Director Margaret Kran-Annexstein said in a statement.

Tri-State Generation and Transmission Association, co-owner and operator of Craig Unit 1, announced in January that it had completed repairs to return Unit 1 to operational condition. Tri-State declined to disclose the cost.

HB26-1226 would require investor-owned utilities and wholesale electric cooperatives to file a report every 90 days after a federal order to keep one of their coal-fired units running past its retirement date. The report must include capital costs and maintenance and operations expenses to keep the unit online. It also must state the number of hours the unit ran over the past 90 days, the amount of electricity generated, and the resulting amount of resource curtailment and its cost.

An IOU that owns but does not operate the coal-fired unit would report its share of the costs. The bill would allow an IOU to apply for a financing order to recover the costs of complying with an order.

DOE’s order to Craig said there is an energy emergency in the WECC-Northwest assessment area. The order pointed to projected load growth in the area paired with planned retirements of baseload generation.

Although the order expires March 30, some are concerned it will be extended.

On Jan. 29, Tri-State and Craig Unit 1 co-owner Platte River Power Authority filed a request for rehearing of the order, arguing it disrupts their “carefully considered reliability planning.” (See Fight Heats up over Colorado’s Craig Coal Plant Extension.)

Challenges to the order were also filed separately by the Colorado attorney general and a coalition of environmental groups. DOE has 30 days to respond; if it does not, the request is automatically deemed denied.

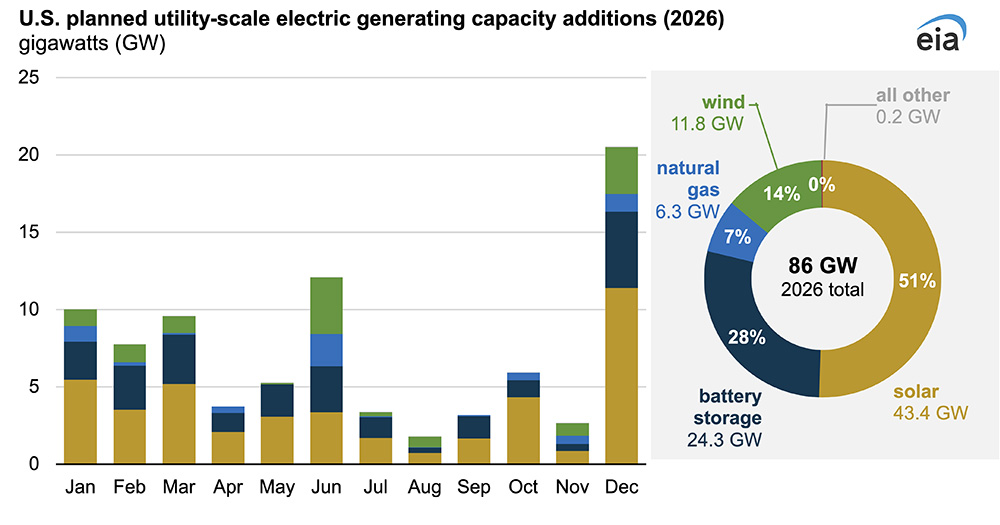

A record 86 GW of utility-scale generation capacity is projected to be added to the U.S. power grid in 2026.

The Energy Information Administration (EIA) said Feb. 20 that if the plans reported by power plant developers and operators come together as expected, they would far outpace the 53 GW of capacity added to the grid in 2025, which was the most since 2002.

Rising demand expected from new data centers and other larger loads has touched off a scramble to add power generation.

But details of the EIA analysis suggest the surge projected in 2026 is rooted at least in part in the clean energy push of the Biden administration, rather than the fossil-heavy energy dominance push of the Trump administration.

EIA calculated 43.4 GW of solar, 24.3 GW of battery storage and 11.8 GW of wind coming online in 2026, or 93% of the 86 GW total.

Just 6.3 GW of new utility-scale natural gas capacity is expected.

The U.S. Energy Information Administration breaks down by technology the expected utility-scale capacity additions to the U.S. grid in 2026. | EIA

Given the time frames involved in development, permitting and interconnection, the Biden-era surge of renewables development still is in process in the second year of the Trump administration and the Trump 2.0 push for fossil generation has not yet resulted in extensive construction.

President Donald Trump engineered an accelerated phaseout of the lucrative federal tax credits President Joe Biden engineered for solar and wind development, so there is additional impetus for renewables developers to accelerate construction of their projects.

EIA broke the numbers down by geography and technology:

The 43.4 GW of new solar would be a 60% increase over 2025.

Texas is the site of 40% of the planned solar construction; rounding out the top three states are Arizona and California, at 6% each.

The 24.3 GW of new battery capacity expected in 2026 would continue the technology’s five-year streak of exponential growth in the U.S. and would far surpass the record 15 GW installed in 2025.

Three states account for most of the new batteries expected to come online in 2026: Texas (53%), California (14%) and Arizona (13%).

Annual wind power additions have slumped since exceeding 14 GW in both 2020 and 2021; the 11.8 GW projected in 2026 would not be a complete rebound but would be more than double the amount that came online in 2025.

Four states account for nearly 60% of the wind total: New Mexico, Texas, Illinois and Wyoming.

The largest onshore wind project in the nation, New Mexico’s 3,650-MW SunZia, is expected to start commercial operation in 2026, as are the nation’s first two large offshore wind projects, the 710-MW Revolution Wind and the 800-MW Vineyard Wind 1 along the New England coast.

Combined-cycle generation accounts for 3.3 GW of the 6.3 GW of natural gas capacity expected to be added in 2026; the planned combustion turbine units total 2.8 GW.

Florida, Ohio, Oklahoma, Tennessee and Texas together would host more than 80% of the gas-fired capacity additions.

The 1,158-MW Orange County Advanced Power Station in Texas is the largest single gas addition expected in 2026.

Generation additions for all other technologies are expected to total approximately 0.2 GW.

EIA has not released full data for electrical generation in 2025.

But the most recent electric power monthly update indicates that through the first 11 months of 2025, significant changes in utility-scale generation were seen with solar (34.5% higher than the first 11 months of 2024), coal (13.8% higher) and natural gas (3.7% lower).

Also in the first 11 months of 2025, U.S. electricity consumption was 2% higher, the average price was 5.3% higher and revenue from sales was 7.4% higher.

MISO is confident that meeting spring demand should be a breeze. The grid operator said it will be able to deliver on both its coincident and non-coincident peak forecasts through May.

During a Feb. 19 Market Subcommittee meeting, MISO’s Jason Howard told stakeholders that the RTO is in “good standing” for spring.

MISO predicts a 100.2-GW load over spring under a 50-50 coincident peak forecast, while its non-coincident peak forecast calls for a 95.8-GW peak in March, an 89.5-GW peak in April and a more dramatic 107.3-GW peak in May.

MISO’s coincident peak forecast draws on load-serving entities’ load forecasts and attunes them to the entire RTO’s simultaneous, seasonal peak. The non-coincident peak forecast, on the other hand, is the peak load submitted by each load-serving entity per month considered in isolation.

The RTO indicated it should have plenty of non-emergency electricity supply under either scenario.

The grid operator’s spring capacity auction cleared 118.3 GW of offers and attracted 123.4 GW in offered capacity.

On top of that, MISO has about 15 GW in load-modifying resources available for grid emergencies. At this point, the RTO doesn’t foresee a need to use them.

Ramping Demand Curve Increase Imminent

The MSC is set to explore upping the pricing of its ramping product through changes to its associated demand curve.

The RTO hopes to stimulate much-needed up-ramping movement to accommodate a growing solar fleet that signs off in the evenings.

Senior Market Engineer Chuck Hansen said MISO hasn’t updated its reserve demand curves, including the one governing its up-ramping capability, since it increased its value of lost load. He said MISO similarly should adjust the up-ramping demand curve to better reflect how high MISO is willing to increase prices to satisfy reserve requirements.

MISO’s existing up-ramp demand curve is priced at just $5/MWh until MISO experiences a 50% ramping deficit. Then, the curve uses eight steps to top out at $31/MWh.

In MISO, it’s become cheaper for the market to “violate the up-ramp constraint than to procure and price the full requirement,” Hansen said.

MISO leadership has frequently discussed its more intense need for ramping, the thrust behind more frequent reserve shortages.

Hansen said over the past three years, MISO has experienced more instances of reserve shortages in the real-time markets. He said they most notably include real-time operating reserve shortages and day-ahead up-ramp shortages.

Hansen said 80% of intervals with real-time operating reserve shortages occurred in an hour that contained a day-ahead up-ramp shortage.

He said while there has been a more than threefold increase in day-ahead up-ramping capability shortage hours, market clearing prices have increased only 21% over the same time.

In many cases, prices don’t reflect the “reserve shortages that are imminent,” Hansen said. He said MISO should formulate prices that are high enough to incent units to be flexible and be fairly compensated.

MISO also hopes to include a deliverability component to its reserves to make sure they’re helpful.

MISO said that as congestion patterns become more active, it will need to ensure reserves can be delivered where needed.

MISO clears its ramp product on a system-wide or zonal basis to cover for load variation. But MISO’s Congcong Wang said the RTO can over-clear ramping capability in MISO South, some of which runs headlong into the 2,500 to 3,000-MW transfer limit between the South and Midwest.

MISO said it needs to manage deliverability in its ramping products so they can meet needs in a subregion. Wang said MISO should devise a way to clear ramping help behind constraints to avoid manual operator interventions such as derates or generator disqualification.

Wang said MISO will review past reserve deliverability to propose a solution.

MISO Makes DER Task Force More Permanent Group

Finally, MISO stakeholders officially disbanded the Distributed Energy Resources Task Force and reformed it into a more permanent working group.

The MSC voted by consent at the Feb. 19 meeting to form the new DER Working Group, issuing it a charter and management plan. Prior to that, the DERTF had been operating on multiple annual stakeholder votes to extend.

Stakeholders also voted in early January to give the DERTF a more stable foundation. In MISO, task forces are temporary stakeholder groups that must be renewed every year to avoid a mandatory sunset date. Working groups, on the other hand, are permanent fixtures that have a charter.

Stakeholders at the time reasoned that a longer-form committee would be best suited to discuss perennial DER topics.

Chair Zachary Callen, an economic analyst at the Illinois Commerce Commission, has said the DERTF is “outgrowing” the definition of a task force, considering the permanence of DER topics in MISO. He said while renewal doesn’t take much, MISO and stakeholders spend hours preparing documents and procedures to re-up the group year after year.

“Importantly, I think the working group is a standing entity that won’t require a renewal process,” Callen said at the DERTF November meeting.

EPA Administrator Lee Zeldin traveled to the Mill Creek coal plant in Kentucky to announce the agency is reversing 2024 amendments that expanded the scope of the Mercury and Air Toxics Standards (MATS), saying the change is expected to save $670 million.

“The Biden-Harris administration’s anti-coal regulations sought to regulate out of existence this vital sector of our energy economy,” Zeldin said in a statement accompanying the Feb. 20 announcement. “If implemented, these actions would have destroyed reliable American energy. The Trump EPA knows that we can grow the economy, enhance baseload power, and protect human health and the environment all at the same time. It is not a binary choice and never should have been.”

The reversal restores as the law of the land the 2012 MATS rule, a regulation that pushed many plants to retire, along with cheap shale gas that made older coal-fired plants less competitive in the markets.

“The Obama administration’s 2012 MATS rule was one of the biggest blows against West Virginia in the war on coal, putting an indescribable strain on our dedicated coal miners, their families and communities and our entire state,” Sen. Shelley Moore Capito (R-W.Va.) said in a statement. “The Biden administration only made matters worse when it included an even more stringent MATS rule in its package of regulations aimed at eliminating coal from our nation’s energy mix.”

The 2024 revisions to MATS established more stringent standards for non-mercury emissions from coal generators and mercury emissions from lignite-fired generators and required all generators to install continuous emissions monitoring systems for particulate emissions.

EPA said that by 2021, the 2012 MATS rule had cut mercury emissions by 90%, acid gas pollutants by more than 96% and emissions of non-mercury metals such as arsenic and lead by 81%.

“EPA has re-evaluated the 2024 final rule and, after considering public comments, finds that the revisions to the emissions standards were not ‘necessary’ because they impose unwarranted compliance costs or raise potential technical feasibility concerns,” the agency said in its repeal.

Reactions to EPA’s announcement varied, with environmental organizations lamenting that the repeal will allow coal- and oil-fired power plants to emit more brain-damaging mercury, other harmful metals and soot. That pollution puts the public at greater risk of cancer, premature deaths, and heart and lung disease, according to a joint statement from the Clean Air Task Force, Earthjustice, Environmental Defense Fund, Environmental Law & Policy Center, Natural Resources Defense Council and Sierra Club.

The eliminated requirement to install monitoring systems on power plants deprives communities of a powerful tool ensuring that the facilities comply with emissions standards, they added.

“This repeal is an unprecedented, unlawful and unjustified reversal that flies in the face of congressionally mandated efforts to reduce hazardous air pollution from industrial facilities,” Clean Air Task Force attorney Hayden Hashimoto said in a statement. “EPA’s repeal puts polluters’ interests over public health by loosening the limits on emissions of air toxics from power plants, which the agency has previously recognized as the largest domestic emitter of mercury and other hazardous air pollutants. Allowing more emissions of air toxics puts Americans at greater risk for the benefit of a small number of particularly dirty coal plants.”

Coal trade group America’s Power welcomed the reversal, saying it will help power plants stay online at a time when they are needed for reliability. More than 55 GW of coal generators are currently scheduled to retire in the next five years as demand continues to rise, CEO Michelle Bloodworth said.

“In combination with other EPA rules, the 2024 MATS rule would have helped accelerate coal plant retirements, ignoring the critical role these facilities play in providing dependable, baseload power,” she added. “Utilities have already invested more than $2.5 billion to comply with the original 2012 MATS rule, and the 2024 update would have required roughly $1 billion in additional costs that ultimately would have been borne by ratepayers.”

FERC has approved three reliability standards setting model validation and data sharing requirements for inverter-based resources, fulfilling the second tranche set in the commission’s Order 901 from October 2023.

Commissioners approved the standard at their monthly open meeting Feb. 19 (RD26-1 et al.), with Chair Laura Swett calling the task of ensuring IBR performance “more important than ever.”

FERC’s acceptance of the standards leaves one more set of standards to satisfy Order 901, covering operational and planning studies, due Nov. 4. NERC’s Standards Committee assigned development of those standards to separate drafting teams in August 2025. (See NERC Standards Committee Tackles Final Order 901 Tranche.)

NERC submitted the second set of IBR requirements to the commission in November 2025, comprising five standards:

MOD-032-2 (Data for power system modeling and analysis)

IRO-010-6 (Reliability coordinator data and information specification and collection)

TOP-003-8 (Transmission operator and balancing authority data and information specification and collection)

MOD-026-2 (Verification and validation of dynamic models and data)

MOD-033-3 (Steady-state and dynamic system model validation)

MOD-032-2 will require planning coordinators and transmission planners to specify the data needed to model IBRs for planning purposes and identify entities responsible for providing the data, along with requiring similar data on aggregated distributed energy resources. IRO-010-6 and TOP-003-8 will “reinforce” requirements for reliability coordinators, transmission operators and balancing authorities to request IBR-specific data and parameters in their data specifications.

MOD-026-2 requires generator owners and transmission owners to perform model validation and model verification of positive sequence dynamic and electromagnetic transient models provided to their TPs. MOD-033-3 includes requirements for PCs to have a documented process for validating models applying to their portions of the electric system, which must include performance comparison between actual system behavior and the steady-state and dynamic models of the system.

In its order, FERC acknowledged that ERCOT, ISO-NE, MISO, NYISO, PJM and SPP had submitted comments supporting MOD-026-2 but disagreed with a provision that excluded “generator owners or transmission owners of legacy facilities with no original equipment manufacturer support for EMT models from the requirement to provide EMT models to their transmission planners.”

The RTOs wrote that NERC’s definition of legacy facilities — covering any facility with a commercial operation date earlier than the effective date of MOD-026-2 — includes IBRs that currently are going through the interconnection process, along with those already in service. They claimed the exclusion would unfairly shift the burden of obtaining EMT models from GOs and TOs to transmission planners, despite their lack of knowledge and access to the facilities, and requested the relevant language be removed from the standard.

NERC replied in the same docket that the team behind the standard “adopted a limited and narrowly tailored exclusion” for legacy facilities after concluding that requiring owners of such facilities to develop their own models would require “costly [and] extensive testing” that would stress the facilities, potentially creating reliability risks. The ERO also observed the exclusion would apply only in cases where the OEM no longer supports the equipment; NERC predicted the number of such cases would fall as new resources were brought online.

Commissioners declined the RTOs’ request to remove the exclusion language, stating they were “persuaded by NERC that the impact of the exclusion will be limited.” FERC approved all the proposed standards “as just, reasonable, not unduly discriminatory or preferential … in the public interest [and] responsive to the relevant directives in Order 901.”

AUSTIN, Texas — Speaking at a recent industry conference, Thomas Gleeson, who chairs Texas’ Public Utility Commission, pointed to a slide on the screen behind him.

“So, this is my job right now,” he said.

Above him, under the title “Batch Study,” were four bullet points that detailed how the state’s regulatory body plans to grapple with the 232 GW of interconnection requests in ERCOT’s large load queue:

“Evaluate multiple projects in the same region

Identify shared transmissions upgrades

Coordinated timelines

Eliminates restudy loop.”

The weight of the task that lies ahead hit Gleeson during the PUC’s open meeting Feb. 6. He said at least half of those in attendance were lobbyists or representatives for data centers, a result of Texas’ open-door policy for all kinds of large loads. Under Gov. Greg Abbott’s direction, the state is expected to overtake Virginia as the world’s largest data center market by 2030.

“It’s really quickly changing, [with] an interest from a diverse group of folks in the work that we do. [It] has really made my job a lot more interesting. A little more difficult, but definitely a lot more interesting,” Gleeson said.

Drawn to the state’s wide-open spaces, energy access and transmission infrastructure, developers filed 225 interconnection requests for large loads through mid-November. ERCOT received only 152 interconnection requests from 2022 to 2024.

“The load forecasts are insane,” Enverus’ Adam Jordan said during a panel discussion at the Infocast ERCOT Market Summit where Gleeson made his presentation.

“We have this explosion,” Cholla Petroleum’s Clayton Greer said during the conference’s obligatory panel on load growth.

During the PUC’s open meeting, Gleeson and his fellow commissioners agreed ERCOT needed to back off its original plan to request a good-cause exception, allowing the grid operator to deviate from its normal study processes and begin the first batch analysis in late February. (See ERCOT Taps the Brakes on Batch Study Process.)

Gleeson said that while he was “very supportive” of ERCOT’s initial direction, after watching the concerns raised in the first workshop on large load interconnections, reading filed comments and talking with different interested parties, he had become “convinced that slowing down a little is the right answer.”

“We have to get this right, and I don’t want to sacrifice the quality of what we’re doing to get it done quickly,” he said. “I know the governor and others want to make sure that we get this right, but they also want to make sure we do it expediently, so that we’re not holding up development. As we’re trying to solve for both speed and quality, I think this gives us the best chance of being successful.”

The plan now is to use ERCOT’s stakeholder process to work out the details of the batch process, using input from market participants rather than a top-down approach driven by the grid operator and PUC. Working with the stakeholder-led Technical Advisory Committee and its Protocol Revision Subcommittee, ERCOT plans to draft nodal protocol revision requests (NPRRs) codifying the process that will be approved by market participants, the Board of Directors and the commission.

“The message was that we need to get it right,” Jeff Billo, ERCOT vice president of interconnection and grid analysis, told stakeholders during a Feb. 12 workshop. “However, [the PUC] also expressed that we need to still move quickly through that revision request process, so this cannot be a revision request that sits in the stakeholder process for half a year or anything like that. We’ve got to move this quickly because those same stakeholders, those developers that have that uncertainty and want to move their projects quickly, that still exists.”

ERCOT staff and stakeholders will begin by writing the protocol change for “Batch Zero,” the transitional study for large loads that face restudies in the current interconnection process. Staff have a mandate, as Gleeson made clear during his conference appearance, to bring the NPRR for the board’s consideration during its June 1-2 meeting. They plan to file the NPRR in early March.

Billo said that would allow Batch Zero studies to begin by late summer. By then, staff and stakeholders should be working on the NPRR for ongoing batch studies, with a September deadline for submission to the board.

The studies would take place every six months, with ERCOT reviewing the projects to evaluate their collective impact on the grid instead of subjecting each project to an individual study. The goal is to integrate the large load requests, adjust the grid as needed, then move on to the next batch.

Anxious to get started, staff limited the Feb. 12 workshop to three and a half hours of discussion. ERCOT’s Matt Mereness, fresh off guiding the successful Real-time Co-optimization plus Batteries project that was deployed in December, noted that “we have a long journey. … That’s why the workshop is short today, because [staff are] going into a room to beat up a whiteboard.” (See ERCOT Successfully Deploys Real-time Co-optimization.)

At the same time, staff also will file revision requests on controllable load resources (CLRs) and large loads proposed concurrently with generation interconnection requests, aligning them with the Batch Zero RRs.

The revisions would allow large loads to declare their intent to register as CLRs and be treated accordingly in the batch process. It would create a binding framework that would require the large load to remain a CLR until it meets defined exit conditions.

For loads proposing to build new generation to meet some or all the requested demand — bring your own generation (BYOG) — ERCOT intends to define the technical requirements needed for a large load “never” to be seen or served by the grid. The protocol change would define the scenarios to be assessed in the batch and other planning studies and would establish rules preventing a large load studied with new co-located generation to be energized until the generation is operational.

Mereness said ERCOT will keep the CLR and BYOG protocol changes “decoupled … but ‘bolt-able’ together, if that’s a good word.”

“When I say ‘bolt-able,’ it would mean, ‘Let’s create the batch study framework,’ and if the CLR concept can be vetted and fit together to where it can be approved at the same time and it all fits together, that would then be the batch process and the CLR.”

Stakeholders generally agreed on the principles outlined, reserving additional discussions on CLR and BYOG topics for future meetings. A third batch study workshop will be held Feb. 26, with as many as five more scheduled.

ERCOT says the critical path for a successful Batch Zero NPRR relies on a series of approval votes in May. That’s when TAC, the PRS and the Reliability and Operations Subcommittee — the latter for accompanying Planning Guide revisions — all will hold votes before the changes go to the board.

“We will brace ourselves for many workshops,” NRG Energy’s Bill Barnes said Feb. 12. It “makes sense that we are supportive of a modified, potentially ad hoc stakeholder approval process where we can accelerate this.”

The interest is there. The Feb. 12 workshop drew more than 150 attendees, according to a head count inscribed on a staffer’s palm. The Feb. 3 workshop had between 800 and 900 people listening in, with 187 in the room.

The PUC has received more than 100 comments from different organizations, while consulting firm McKinsey & Co., supporting ERCOT, has interviewed stakeholders and conducted surveys over the past two months. McKinsey said a strong majority (more than 80%) prefer some form of screening by transmission and distribution service providers to ensure realism and feasibility, with debate on whether it should be optional or mandatory.

“The biggest frustration for these loads is the lack of uniformity from TDSP to TDSP,” Google Energy’s Chris Matos said during the second workshop.

The discussions will continue through the spring. As Greer said, the “massive” data center load growth is “being kind of hampered by the existing process that we have.”

“Hopefully, the batch process will allow the dam to break a little bit and moves it from a planning blockade to a supply chain blockade,” he said. “We’ll see how it goes after that.”

Colorado regulators have approved 3.2 GW of new resources requested by Public Service Company of Colorado under an expedited approval process designed to take advantage of soon-expiring federal tax credits for solar and wind projects.

The Colorado Public Utilities Commission voted Jan. 28 to approve six projects with a combined capacity of 1,095 MW. Projects totaling an additional 2,100 MW were approved Feb. 18.

The approved resources include 200 MW of gas generation; four wind projects totaling 595 MW; two standalone storage projects totaling 700 MW; 500 MW of standalone solar; 600 MW of hybrid solar; and 600 MW of hybrid storage.

PSCo, an Xcel Energy subsidiary, may return for approval of either a 608-MW wind project or a 450-MW solar-plus-storage project after further analysis to compare them.

Near Term Procurement

The projects were approved under the Near Term Procurement (NTP) process, a standalone, expedited procedure the commission approved in 2025 after the Trump administration moved up the eligibility timeline for federal tax credits.

The commission’s decision on Jan. 28 included a request for PSCo to further analyze several projects in its proposed resource portfolio that had not yet been approved. That included updated modeling and a business-case analysis.

But several parties quickly filed requests for rehearing or reconsideration of the commission’s decision. They said the request for additional analysis would defeat the purpose of the NTP.

The commission’s process causes delays and “creates an unnecessary new process that was not contemplated by the motion to initiate [the] NTP,” said a filing from the Colorado Energy Office, PUC trial staff and the Utility Consumer Advocate.

The Colorado Independent Energy Association questioned why the commission hadn’t asked for additional project analysis earlier and said the commission risked losing safe-harbored projects to other states.

“To the extent the commission deviates from its prior decisions, introduces unanticipated regulatory delay and moves forward with projects based on criteria that were not expressed to all bidders at the outset of the NTP process, Colorado sends the signal that it is not a conducive place for [independent power producers] to do business,” CIEA said in a filing.

The filings convinced commissioners to take another look at projects in the proposed portfolio despite some frustration over proceeding with limited information.

“It’s challenging to balance moving forward quickly with very large investment decisions while waiting for better data and analysis,” Commission Chair Eric Blank said.

Commissioner Megan Gilman said it’s clear that more resources will be needed in the future. And even with changes in federal policy, renewables still seem to be the cheapest option.

“Forgoing resources that are favorably priced, that are right in front of us, that have time to safe harbor and get the tax incentive — I don’t think forgoing those is a good scenario in any of the ways the future plays out,” she said.

Clean Energy Commitment

In August 2025, Colorado Gov. Jared Polis issued a letter that recommitted the state government to prioritizing the development of clean energy projects.

“Getting this right is of critical importance to Colorado ratepayers,” Polis wrote. “By maximizing the utilization of tax credits while they’re available and reducing future tariff uncertainty, the state can avoid billions of dollars in additional energy costs for decades to come.”

Under an IRS notice issued in August 2025, a project must begin significant physical construction before July 5, 2026, proceed continuously and be completed within four calendar years to be eligible for the tax credits.

Under the NTP process, PSCo was asked to seek bids with commercial operation dates no later than the end of 2029. Each bidder was required to show their project would qualify for tax credits. PSCo was directed to evaluate projects based on levelized energy cost and levelized capacity cost but was told additional modeling wouldn’t be needed.

In terms of project location, PSCo was asked to focus on “just transition” communities that will be affected by the planned closure of coal-fired power plants. Three of the approved projects will be in such communities.

Blank argued for more resources in the Denver metro area “to increase the likelihood we can timely retire the coal plants.” He said transmission hasn’t yet been identified for bringing electricity from remote regions into the Denver area.

Colorado PUC Director Rebecca White said stakeholders had demonstrated “an extraordinary effort” to bring projects forward quickly. And the commission “closely reviewed these projects on a very tight timeline to ensure the best mix possible for ratepayers.”

“Today’s action locks in cost savings for Xcel customers as we work to replace aging coal plants and meet growing energy demand,” White said in a Feb. 18 statement.

Southern Co. is “extraordinarily positioned to capture and serve growth” during “a watershed moment for the energy industry and our nation,” CEO Chris Womack said during the company’s fourth-quarter earnings call Feb. 19.

Southern reported net income of $416 million ($0.38/share) for the final quarter of 2025, down from $534 million for the same period in 2024, and full-year net income of $4.3 billion ($3.94/share), down from $4.4 billion for 2024.

The drops came despite a rise in operating revenue from $6.3 billion in the fourth quarter of 2024 to $7 billion for the final quarter of 2025, and growth in full-year operating revenue from $26.7 billion to $29.6 billion.

Adjusted earnings per share for 2025 came to $4.30, CFO David Poroch said on the call, up from $4.05 in 2024 and once again at “the very top of our … guidance range,” which the company set at $4.20 to $4.30 in last year’s fourth-quarter earnings report. (See Strong Southeast Economy Bolstered Southern Co. Growth in 2024.) Southern set an adjusted EPS goal for 2026 of $4.50 to $4.60.

“I’m convinced that 2025 will stand out as a transformative year for Southern Co., one in which we achieved milestones that will propel the future of our business and customers for generations to come,” Womack said. “Economic development activity at our utilities is robust and provides a tremendous foundation for sustainable growth.”

As in previous years, Womack and Poroch credited the strong economy in Southern’s territories for the company’s performance, with $0.34 of the EPS growth attributed to its state-regulated electric utilities. Weather-adjusted retail electricity sales grew across all customer classes in 2025: 39,000 new residential customers were added over the previous year, resulting in growth of 0.8%; industrial sales rose 1.4%, with primary metals and lumber leading the growth; and commercial sales grew 2.8%, 1.8% of which was driven by data centers.

Southern expects the strong retail electric sales growth to continue through the coming years thanks to data centers and other large loads, Poroch said, with 10 GW of facilities already under construction for 26 companies, including Google, Meta and Microsoft, an increase of 2 GW from projections in the prior quarter. Another 10 GW is either finalizing or in late-stage discussions, and the company has a pipeline of more than 125 prospective projects totaling over 75 GW.

“The framework and methodology under which we approach contracting with large load customers are, we believe, one of the best in the industry, and are uniquely designed to benefit and protect existing customers and investors,” Poroch said. “Our contracts include a robust set of terms and conditions [such as] minimum terms of at least 15 years for data centers, with some going out even further over the term of the contract.”

Poroch also reviewed the company’s capital expenditure plan, which has increased from $63 billion in investments through 2030 planned last year to $81 billion. The main driver of the expansion is new generation facilities announced in 2025, including five combined cycle plants, three combustion turbines, two combined solar and battery plants and 17 battery energy storage system facilities.

“We are clearly in a phase of execution,” Womack said. “The planned large-scale buildout across our electric system in the Southeast over the next several years is tremendous and Southern Company’s experience, expertise and scale support the necessary execution. … We are experiencing incredible growth, and we are making investments in all parts of our business to recognize the value of the extraordinary opportunities in front of us.”

FERC has rescinded the West-wide wholesale electricity price cap mechanism it implemented in response to widespread price manipulation during the Western energy crisis of 2000-2001, saying development of new markets and expanded authority have led to improved monitoring capabilities.

The policy required sellers to justify the costs behind power prices exceeding the soft cap of $1,000/MWh, or refund any amount earned above the cap. FERC in a Feb. 19 order (EL10-56) cited three reasons for eliminating the price cap: the evolution of Western wholesale markets, FERC’s expanded legal authority to monitor market misconduct and filing burdens associated with the price cap.

The order rescinding the soft cap is effective July 18, 2025. (While the policy is referred to as the “WECC soft price cap,” WECC is not involved with it or any regional market operations.)

Following the court’s decision, FERC proposed eliminating the policy altogether and launched a Section 206 proceeding in July 2025.

When initiating the 206 proceeding, FERC recounted the D.C. Circuit’s findings and noted that, while FERC has over time revised the soft offer cap to reflect increases in CAISO’s caps, it never reassessed whether the framework is necessary to ensure just and reasonable rates in the West as required under the Mobile-Sierra doctrine.

In the Feb. 19 order, FERC reiterated many of its initial findings, saying the policy no longer is justified.

One major reason is the development of new wholesale markets in the West, which provide alternatives to traditional bilateral markets. These newer markets, like CAISO’s Western Energy Imbalance Market and the Extended Day-Ahead Market (EDAM), already include market monitoring tools to address potential abuse, FERC wrote.

“In particular, we note that RTO West and EDAM are scheduled to go live this spring (of 2026) and will meaningfully expand Western market participants’ access to centralized, day-ahead markets as an alternative to existing bilateral trading activities,” the order stated. “While we recognize that Markets+ is not scheduled to go live until next year, and that participation in these new market constructs will expand gradually over time, we nonetheless find that the coming expansion of these market alternatives provides additional support for eliminating the WECC soft price cap at this time.”

‘Important Check’

Another reason to eliminate the cap is FERC’s own ability to tackle misconduct, according to the order.

The Energy Policy Act of 2005 granted the commission “authority to pursue allegations of market manipulation in FERC-jurisdictional wholesale electric markets, which serves as an important check against the types of misconduct that fueled the Western energy crisis and led to the adoption of the currently effective soft price cap,” the order states.

The 2005 act has led to development of new tools, capabilities and enforcement mechanisms, the order notes.

“In total, these various data sources and improved analytical capabilities provide the commission far more comprehensive, timely, and actionable information to identify and address market misconduct than was available to the commission in 2002 when it established the WECC soft price cap,” FERC wrote. “We conclude that these capabilities are also more effective at deterring, identifying and addressing market misconduct than any delayed and indirect oversight via review of individual sellers’ spot market transactions under a Mobile-Sierra framework.”

The Feb. 19 order affirmed the commission’s preliminary finding “that the administrative burdens associated with the soft price cap framework outweigh the negligible benefits associated with retaining the cap merely as a flagging mechanism.”

“We also find that this negligible benefit does not offset the burden imposed on sellers and the commission,” the order states. “We affirm the commission’s preliminary finding in the 206 order that ‘the filing requirement imposes costs on market participants and the commission and creates uncertainty for individual transactions while those filings are pending review at the commission.’”

Thirteen blue states are suing the Trump administration for reversing Biden administration funding commitments worth $7.6 billion for energy and infrastructure projects.

California Attorney General Rob Bonta filed the complaint (26-cv-01417) Feb. 18 in U.S. District Court in the Northern District of California. He was joined by the attorneys general of a dozen other states as plaintiffs.

They name the U.S. Department of Energy, the U.S Office of Management and Budget, Energy Secretary Chris Wright and OMB Director Russell Vought as defendants.

The plaintiffs ask the court to declare the funding cuts unconstitutional on the grounds the president cannot reverse funding appropriated by Congress or target opponents. They seek reversal of the grant terminations and abandonments, and they want an injunction against similar cuts in the future.

Some of the cuts would spill over into Republican-led states or congressional districts, but all were centered in 16 “blue” states won by then-Vice President Kamala Harris in her losing run against President Donald Trump in 2024.

The 32 U.S. senators representing those 16 states all were Democrats and all voted against a bill that would have averted the fall 2025 federal government shutdown.

At the time, DOE framed the cuts as part of a process by the new Trump administration to winnow out wasteful spending. But as it defended a subsequent legal challenge led by the city of St. Paul, Minn., against a handful of the grant terminations, the Trump administration acknowledged that the October grant cancellations were based primarily on their locations in blue states, and asserted that was legitimate justification. Further, the administration acknowledged that the grants terminated in blue states were comparable to red-state grants it did not terminate.

The judge in the St. Paul case (25-cv-03899) ruled Jan. 12 that this approach had violated the plaintiffs’ guarantee to equal protection of laws under the Fifth Amendment to the U.S. Constitution. (See Judge Rules Blue-state Energy Grant Terminations Unlawful.)

But that ruling pertains only to seven grants at the center of that case.

RTO Insider asked DOE at the time whether it considered the ruling applicable to the other 300-plus grants it terminated in October 2025.

DOE did not answer the question, but its Feb. 13 filing in the St. Paul case sheds some light: It told the judge the plaintiffs’ request for a permanent injunction was unwarranted but if any injunctive relief were granted it should pertain only to the seven grants in question.

California filed its lawsuit three business days later.

It is joined by the attorneys general of Colorado, Connecticut, Illinois, Maryland, Massachusetts, New Jersey, New York, Oregon, Rhode Island, Vermont, Washington and Wisconsin.

The California Governor’s Office of Business and Economic Development (GO-Biz) also is a plaintiff, on behalf of ARCHES.

ARCHES — the Alliance for Renewable Clean Hydrogen Energy Systems — is one of seven regional hydrogen hubs created amid a Biden-era push to develop hydrogen as an energy sector; it was focused on building a green hydrogen ecosystem in California.

ARCHES was the biggest loser in the October 2025 tranche of DOE grant terminations, at $1.2 billion.

CEO Angelina Galiteva decried the termination when it went public Oct. 1, but said the initiative would continue to advance in collaboration with state leaders and the private sector. However, a month later, ARCHES said it would pause hydrogen hub activities because of the federal funding cuts and hand administrative oversight to GO-Biz and the University of California.

It has laid off its entire full-time staff, according to California’s lawsuit.

GO-Biz demanded on Jan. 15 that ARCHES file a lawsuit seeking to remedy harms from the grant termination; the ARCHES board of directors replied that pursuing litigation would be in its best interest but it lacked the financial resources to do so because of the DOE grant termination.

All told, the October grant terminations totaled nearly $2 billion in California.

California’s Feb. 18 lawsuit lists much smaller sums for the 12 other states affected by the DOE grant terminations.

Trump and California Gov. Gavin Newsom (D) snipe at each other often and hard, and the lawsuit hints at that relationship.

“In early October, as the administration sought a cudgel to wield in budget negotiations, defendants deployed this unlawful policy as an opportunistic way to hurt the administration’s political enemies and those associated with them,” the introduction to the complaint reads.

The specific complaints in the California lawsuit are similar to those in the St. Paul case: violation of the separation of powers between Congress and the president, violations of the Administrative Procedures Act, ultra vires action by federal officials, violation of the First Amendment by retaliating against free speech and violation of the Fifth Amendment right to equal protection.

The plaintiffs ask that the DOE memo on which the grant terminations were based be declared unlawful; seek a permanent ban on any future action based on the memo; and ask for reversal of the grant terminations.

They also want a declaratory judgment that the defendants may not terminate or abandon awards based on policy preferences or geographical location.

And they ask for an injunction reinstating the cooperative agreement DOE terminated with ARCHES as it terminated the hub’s grant.