House Passes Bill Requiring Open PSC Rate Hearings

The House of Representatives voted 104-0 to pass a bill that would require the Public Service Commission to hold rate case hearings every three years.

Supporters said the legislation is aimed at increasing accountability and public participation in how rates are set. The hearings would be formal and under oath, with subpoena power to gather evidence.

The bill also would prohibit a return on equity greater than the regional average.

The Transportation, Energy and Utilities Committee voted unanimously to approve closure and abandonment of three rights-of-way to allow the development of a solar array facility.

The land will become one of three solar farms that will sell power to JEA. JEA, which owns the land, will buy power from Florida Renewable Partners, which will build, own and operate the facility.

The House of Representatives voted to pass the Utility RELIEF Act.

The legislation would reduce a surcharge on monthly bills that supports the EmPOWER program, which gives customers free or reduced-price smart thermostats and efficient appliances. The bill also changes the way utilities request rate increases by discontinuing the use of spending forecasts, encourages transmission upgrades instead of new lines and regulates data centers. The governor’s office estimated it would save ratepayers an average of $150/year.

Order Mandates 15-month Permitting Deadline for Renewables

Gov. Maura Healey signed an executive order mandating a 15-month limit for state and local permitting decisions on large-scale renewable infrastructure.

The mandate also will create an Energy Infrastructure Siting and Permitting Council that will oversee the regulatory framework and coordinate agencies to prevent the slowing of the state’s renewable transition. Smaller projects would face a one-year approval window.

The Healey administration aims to create 4 GW of new solar capacity by 2030.

Google announced it has reached a 20-year agreement with DTE Energy to power a 1-GW data center.

Google, which is evaluating a 280-acre site near the Detroit Wayne International Airport, said DTE will supply it with 2.7 GW of storage, renewables and grid-sourced power.

Power Siting Board Blocks Morrow County Solar Farm

The Power Siting Board denied construction of the Crossroads Solar project in Morrow County.

The decision referenced “consistent and substantial opposition to the project by the local population.” However, reporting has found that public comments claiming to be from residents do not align with voter registration records and that false email addresses were provided. The board said those comments were not considered in their decision.

PUC Fines UGI $2.6M for Chocolate Factory Explosion

The Public Utility Commission requested $2.6 million in fines from UGI in relation to a gas leak and explosion at a chocolate factory in Berks County.

The complaint filed by the Bureau of Investigation and Enforcement alleges 27 safety violations related to UGI’s natural gas system.

The explosion, which occurred on March 24, 2023, caused $42 million in property damage and killed seven people. Investigators determined natural gas leaked from a retired plastic service tee connected to a vintage plastic pipeline beneath a street near the factory. The gas migrated underground and entered the building, where it was ignited by an unknown source.

Texas installed more solar power than any other state in 2025, according to a Solar Energy Industries Association report.

The Lone Star State installed more than 11 GW of solar, more than twice as much as second-place California (4.6 GW). It is at least the third straight year the state has led the nation in solar installations.

The U.S. solar industry installed 43.2 GW overall in 2025, a 14% decrease from 2024.

The Fluvanna County Board of Supervisors approved a conditional use permit for Tenaska’s second natural gas plant in the county.

The board approved the permit of the 1,540-MW Expedition Generating Station despite a 3-1 vote from the county’s planning commission opposing the plant.

The project still needs State Corporation Commission and Department of Environmental Quality approval and to receive other permits before construction can begin.

The Public Service Commission approved We Energies’ purchase of two solar projects for $360 million.

The Good Oak and Gristmill facilities in Columbia County will generate 165 MW and will help supply data centers.

We Energies will own 80% of both facilities. The remaining power will be split between Madison Gas & Electric and the Wisconsin Public Service Corporation.

HOUSTON — U.S. Energy Secretary Chris Wright opened the CERAWeek conference with a plenary session during which he praised fossil fuels and bashed clean energy.

He patted himself on the back for delaying the retirement of 17 GW of coal-fired power plants: “We stopped energy subtraction policies.”

“The truth is simple. Energy is life, and the world needs massively more of it,” he said, taking the stage as a cheering section led by Secretary of the Interior Doug Burgum in the front row urged him on.

“President Trump’s goal from Day 1 was to get rid of the nonsense and restore common sense,” Wright said. “That means turbo-charging American energy production, including electricity that’s been relatively stagnant for a few decades. Surging energy production will drive down costs for Americans, drive reshoring of manufacturing back to our country, and that in turn will drive up wages. Lower costs, higher wages. In short, that’s the economic agenda.”

To meet the administration’s goal of leading the world in artificial intelligence, he said the U.S. will have to build more electricity generation, preferably baseload, and do so at a rapid pace.

“We haven’t done that in a while,” Wright said, laying the blame at the feet of Democratic administrations. “No one really wanted to build a new gas or coal generation plant when some time in the near future you were going to have to capture the CO2 emissions from it, use a third of the power from the power plant to capture emissions, and then dispose them in quantity underground, which has never been done at scale. Do you really want to spend $100 for something that might give a $1 benefit? That’s not a businesslike attitude.”

He said that by “clearing out a lot of the morass that disincentivizes people from building things,” the marketplace will sort out winners and losers.

As an example, Wright said the Department of Energy is offering the national laboratories’ more than 1 million acres to companies interested in developing small nuclear reactors. The White House issued an executive order in 2025 that set a DOE goal to have three SMRs reach criticality by July 4, 2026.

“Why this year? Because it’s our 250th anniversary,” he said, acknowledging that the deadline is “an aggressive time frame.”

“As I stand here today, we look to be on track to have three next generation nuclear reactors running. They won’t be selling electricity into the grid, but all the nuclear systems will be running and generating the heat that would be used to produce electricity by July 4,” Wright said.

He said 11 SMR technologies are in the queue. At the same time, DOE is reforming permitting for nuclear reactors and trying to ramp up domestic uranium enrichment, fuel fabrication and reprocessing, and permanent waste disposal sites with a “competitive state-level opt-in process.”

With the Nuclear Regulatory Commission “at our side,” Wright said the agency is asking states to compete to host nuclear innovation campuses that will prove the worth of SMRs.

“These are small SMRs that can be built and constructed quickly. Fortunately, in America’s free market society, there’s a few dozen small modular reactor companies pursuing different technologies [and] different sizes,” he said. “We welcome it all. This will really speed up the development … nuclear has just been slow and hasn’t moved for decades. We want to get it moving quickly so it could win economically.”

Although there have been significant signs of progress for new nuclear power, nuclear analysts say it also faces a long timeline and plenty of potential obstacles. The analysts add that meaningful capacity increases are still years in the future. (See Nuclear Power Retains Great Potential in 2026.)

The return of demand growth is something new in the electricity industry, especially as it is being driven by individual consumers whose load can exceed the peak demand of a small state, and it is giving new life to an old argument in state legislatures: restructuring the industry.

The states that went forward with restructuring in the 1990s and those that opted against it are not necessarily going to switch sides completely, but longstanding rules are being challenged in both.

Utilities in PJM have been lobbying for long-restructured states like Pennsylvania and Maryland to allow them to build generation into rate base, while independent power producers with retail businesses are asking vertically integrated states to open part of their demand to the market so they can build generation to serve those new customers, as well as commercial and industrial customers generally.

Data centers are definitely driving the conversation, said Abby Foster, senior vice president of policy at the Retail Energy Advancement League (REAL), which is trying to open vertically integrated states and maintain restructured markets in others.

“But this would have been happening either way, especially in the vertically integrated states, because we’re hitting this point where you look at especially the states in MISO, there’s a ton of coal assets, and most of those are scheduled for retirement in the next 10 years,” she said in an interview with RTO Insider.

Without data centers accelerating resource adequacy concerns, it would have been more of a slow burn as utilities kept on applying for new rate cases to replace retiring power plants, with consumers facing higher prices for the first time in 20 years in states like Missouri, Indiana or Kentucky, Foster said. That buildout is coming when the costs of new generation have risen sharply in recent years.

“It’s almost like things have come full circle from the late 90s, when states were in the position that they were in, and they chose to restructure,” Foster said. “So, you have load growth; you have a ton of retirements; you have a ton of generation that needs to be built and costs that are just unsustainable and untenable for customers to pay over the long-term.”

REAL met with some West Virginia legislators on their state’s recent trend in average power prices, Foster said.

Price trends in PJM’s capacity market | Charles River Associates

“They’re still middle of the pack today, but they were like 47th two or three years ago, [and] they didn’t love the idea that West Virginia rates are increasing, second only to California,” she added.

REAL’s model legislation would open 20% of overall load to competition, and consumers would need demand of 1 MW to participate, though C&I facilities with smaller loads could use aggregation of multiple sites to get into the market, Foster said.

“That 20% makes it so that there’s still enough that needs to be built by the utilities; it’s just removing the amount that they have to build that’s new rather than placing costs on the customers who aren’t shopping,” Foster said. “And of course, the customers who are shopping still pay all of the other costs — so transmission, distribution, energy efficiency and low-income programs.” Only the generation part of their bill would go to whatever third-party company they sign up with.

Some states already have a capped level of shopping, and while their experiences varied, often they started to restructure but stopped short. Michigan put a cap of 10% on its market, and it quickly filled up, which meant the market took on the burden of supplying that demand.

“They never had to build what’s the equivalent of seven or eight natural gas plants,” Foster said. “They never had to bill the rest of the ratepayers to build those gas plants to serve those customers, plus their guaranteed rate of return.”

Michigan-headquartered General Motors would like to see a version of that state’s system extended into Missouri, where it employs 4,500 workers, via House Bill 417, the Electric Choice and Competition Law.

“We have invested more than $1.5 billion in our facilities and generated thousands of jobs for related suppliers, contributing to significant baseload demand,” GM Global Energy Strategy Director Rob Threlkeld wrote legislators in a letter in March 2025. “As electricity costs continue to rise, GM supports legislation that ensures reliable and affordable electricity for our operations. HB 417 will assist industrial customers in managing their anticipated rising energy costs.”

Utilities in PJM Want Back in Generation Game

While REAL has been pushing to crack open retail power markets in states that have never opened up, some utilities in PJM have been asking states like Maryland and Pennsylvania to let them rate-base new power plants to help close the widening gap on resource adequacy there.

Exelon hired Charles River Associates to produce a report that argues allowing it and other utilities in PJM to build generation could save consumers $9.6 billion to $20 billion in the 2028/29 delivery year.

“Customers are understandably frustrated about high energy costs, and public utility companies are ready to help bring them under control with utility-generated power such as battery storage or community solar,” Exelon Chief Legal Officer Colette Honorable said in a statement. “Utility-generated power will ensure we have enough electricity to meet skyrocketing demand, address affordability and make sure customers come first.”

Exelon said its report is especially relevant for states like Maryland, where rapid load growth and constrained supply are intensifying affordability and reliability challenges.

While the restructured states in PJM have banned their utilities from building generation in rate base since those laws went into effect in the 1990s, Exelon does not want the change to spark the unwinding of the markets, arguing that any generation it builds can work alongside them. Only some of the states in PJM have fully restructured; West Virginia is fully regulated; and Virginia has a hybrid system with utility-owned generation. Units from those states have operated in the RTO’s markets for years, competing with IPPs.

Advocates of competition argue that letting utilities into the generation business could risk an overbuild of generation, as putting the facilities in rate base guarantees cost recovery regardless, while the IPP model places such risks on the generation firm’s shareholders.

“In restructured states, IPP developers do not have an obligation to build,” Exelon Director of Federal Regulatory Affairs Jordan Kwok said. “And, because they may elect not to build for whatever reason, customers may be left with inadequate generation supply and the ensuing reduction in reliability. Put another way, in a competitive framework, IPPs bear the risk of their actions, but customers bear the risk of IPP inaction. Utility-generated power solves for this risk by fostering certainty and providing a tool for our regulators to fall back on if the market is underdelivering.”

Industry Experts Split on the Issue

Mark Christie, director of William & Mary Law School’s Center for Energy Law and Policy, said in a recent interview that there are no perfect regulatory structures, but the ultimate goal of any has to be delivering reliable power at the least cost to the consumer.

“Whether new generation is financed through rate-basing by load-serving utilities, or through capacity payments to bidders in the PJM capacity market, consumers will still be paying the bill for the new generation,” the former FERC chair said. “So, the line we have heard for 30 years that using the capacity market alone puts the burden on investors to pay for new generation, not consumers, is misleading at best. Consumers pay for capacity payments in their power bills, just as they pay for rate-based generation.”

Christie said that Virginia has a good regulatory model, with its hybrid system where utilities can rate-base power plants and IPPs can build competitive power plants. It is also one of the states that serves a model for REAL’s preferred policy with a cap on shopping that lets some C&I customers pick their supplier.

“When I was a Virginia regulator, we approved at least five combined-cycle gas generators for our utilities,” Christie said. “All were rate-based, all were built, and none of them would have been built without rate-based financing. And we approved continued rate-based financing, including life extensions, for Dominion’s nuclear units. All of these dispatchable generators have been critically important to keeping the lights on in Virginia and PJM, and without rate-based financing, we would not have gotten them built.”

The debates around which way states should go are coming back up now in PJM because its capacity market has seen prices shoot up, and in its most recent auction, it cleared short of the RTO’s reliability target.

“I think the big picture is that the PJM capacity market is simply not obtaining enough generation,” Christie said. “We know that for an absolute fact.”

Former Pennsylvania Public Utility Commissioner John Hanger served when the state passed its restructuring law. Since then he has written reports as a consultant arguing the policy is best for customers, pointing to offers in PECO Energy’s Philadelphia area territory and Duquesne Light Co.’s Pittsburgh territory that are cheaper in nominal dollars than the utility rates in 1996, when the restructuring law passed.

“It is truly stunning,” Hanger said in an interview. “That is a testament to how bad rate-based, rate-of-return regulation worked in Pennsylvania, especially in the Duquesne Light and PECO service territories, and also the success of competitive generation markets.”

While other restructured states, like Maryland and New York, have restricted the market for residential customers, Hanger said that retail competition works well for large customers, in every jurisdiction.

“If legislators in Missouri want to drive down their costs for their commercial/industrial customers, they should allow these customers to shop for electricity and introduce generation competition,” he added. “And they should do it with a sensible transition plan, but they should do it as soon as possible.”

Letting utilities back into the generation business now, even with the resource adequacy issues in PJM, would not be good, he argued.

“It’s an invitation to waste, fraud and abuse,” Hanger said. “It’s an invitation to boondoggles that the captive ratepayers would have to pay for. I cannot think of an approach to the current concerns that is more likely to blow up in the face of any legislator or any governor who supported that.”

Affordability concerns drove the initial wave of restructuring in the 1990s, Hanger recalled. Those same concerns have given the utilities an opportunity to push legislation to let them build generation again, he said.

“They use the lack of information amongst the general public on these questions and, frankly, the fact that legislators are generalists who do not specialize in electricity markets or utility regulation to try to pull the wool over the eyes of those legislators,” Hanger said. “They come in with simple stories that are simply wrong.”

The fastest rising part of the end-use customer’s bill in recent years has been what is still regulated: the payments for transmission and distribution infrastructure, Hanger said.

“We are supposed to believe that the two companies that have been shooting up transmission and distribution rates somehow or another are going to produce lower generation rates,” Hanger said. “Give me a break.”

Puget Sound Energy and Avista told the Washington Utilities and Transportation Commission that they have taken steps to build clean energy resources quickly to qualify for expiring federal tax credits, while voicing concern that limited transmission capacity and the state’s greenhouse gas targets pose challenges.

PSE and Avista provided comments as part of the Washington UTC’s investigation into how federal tax law changes impact clean energy projects in the state. The deadline to submit comments in the docket was March 20.

The UTC’s investigation follows new rules imposed by the Trump administration in summer 2025 that changed eligibility requirements for tax credits on new wind and solar construction.

Under the rules, solar and wind projects face a July 4 construction-start deadline to claim the tax credits. A project must begin significant physical construction before July 5, proceed continuously and be completed within four calendar years to be eligible. (See IRS Guidance on Wind and Solar Credits Not as Bad as Feared.)

For PSE, the new laws have prompted the utility to invest in projects “earlier than it otherwise would have absent the tax law changes presented in [One Big Beautiful Bill Act],” Wendy Gerlitz, PSE’s director of regulatory policy, wrote in the utility’s comments.

PSE prioritizes projects with a construction-start date before July 4 and requires involved parties to comply with the law’s sunset deadlines, Gerlitz wrote.

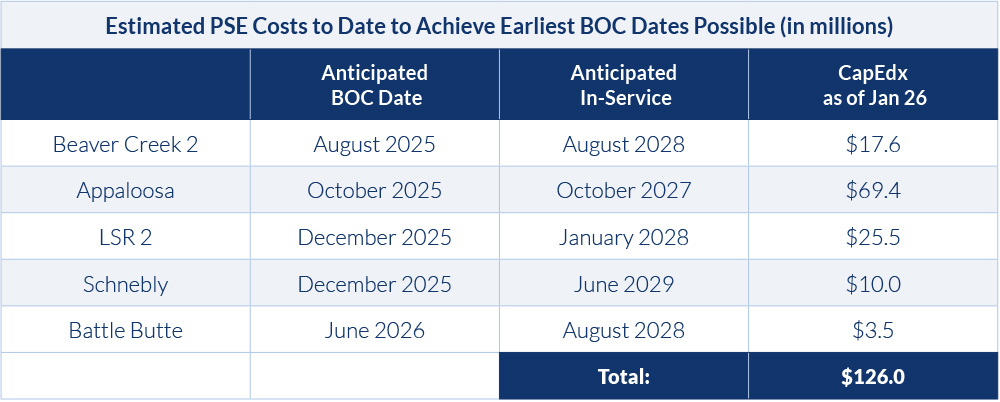

At least five projects are slated to begin construction before the July 4 deadline, including Beaver Creek, a 248-MW utility-scale wind project in Montana; the Appaloosa solar project, a 142-MW project in Washington; and a 130-MW solar project in Montana called Battle Butte, according to PSE’s filing.

At least five PSE projects are slated to begin construction before the July 4 deadline to claim federal clean energy tax credits. | Puget Sound Energy

One of the major challenges to securing the tax credits is “the slow pace of the Bonneville Power Administration interconnection studies and commencement of upgrades,” Gerlitz stated.

BPA paused certain planning processes in 2025 to consider how to address nearly 61 GW of transmission service requests. The agency has presented several proposals to reduce the queue, but the efforts have been criticized as moving too slowly for utilities in Oregon and Washington to meet strict greenhouse gas standards and secure the federal tax credits. (See Northwest Lawmakers Explore Building Transmission Without BPA’s Help.)

“BPA is undergoing a significant reformation of our queue processes,” agency spokesperson Kevin Wingert told RTO Insider in an email. “This reform will ultimately drive major transmission construction and integration timelines from what is seen typically across the nation of 15 or more years down to a four-to-six-year average.”

Wingert noted that BPA launched the $6 billion Grid Expansion & Reinforcement Portfolio, which includes 23 projects that are being brought online between now and 2035.

Although PSE is collaborating with BPA on the interconnection studies, “in general, actual progress has been too slow to facilitate timely [commercial operation dates] for projects that otherwise have a high probability of meeting the year-end 2029 and 2030 tax credit deadlines,” according to Gerlitz.

Washington’s Clean Energy Transformation Act (CETA) requires all electric utilities in the state to become greenhouse gas-neutral by 2030 (allowing for use of offsets and other programs) on the way to generating all power from emissions-free resources by 2045. It also prohibits utilities from serving their Washington customers with any coal-fired generation after 2025. (See Washington Agencies Adopt New Rules to Implement CETA.)

BPA’s transmission planning pause coupled with Trump’s new tax laws “will certainly increase the cost of compliance with CETA and negatively impact PSE’s financial health, making it more challenging to accelerate important renewable projects,” Gerlitz contended.

Gerlitz urged the UTC to mitigate the impact of the federal tax changes, saying the utility is speeding up investments in projects that “will not be placed in service for many years.”

“This acceleration places additional pressure on PSE’s credit metrics, which is a critical measure of PSE’s financial health and a key set of metrics for credit rating agencies and fixed-income investors,” Gerlitz added.

Avista made similar requests, proposing the UTC accelerate permitting, support procurement processes and provide incentives to developers to acquire equipment to show that “significant physical work” has begun as required under the bill, according to Shawn Bonfield, senior manager of regulatory policy and strategy at Avista.

Bonfield wrote that the company initiated a request for proposals process in 2025 for renewable projects with the uncertainty around the tax credits in mind.

For example, the utility sped up the RFP release schedule to benefit tax-advantaged projects and requested proposals for additional renewable energy before tax credit deadlines.

“Avista is working towards agreements with selected developers based on proposals that meet identified needs, and as applicable, have a planned path towards achieving tax credits,” Bonfield wrote.

“The accelerated expiration of federal tax credits for wind and solar resources is concerning to Avista, particularly as customer growth calls for additional resources into the future,” he stated. “Avista’s top priority is to keep power safe, reliable and affordable for its customers, and the loss of federal tax credits has a significant impact on those goals.”

FERC has denied a complaint from RWE Clean Energy arguing PJM incorrectly identified network upgrades for a 125-MW solar and storage project, increasing the cost allocation over 50-fold during the third phase (EL26-7).

The company canceled its Maryland Blue Crab Solar and Storage project — which would have paired 100 MW of solar and 25 MW of storage — after PJM’s Phase III system impact studies determined the interconnection would require rebuilding eight miles of the Edge Moor-Linwood 230-kV line, increasing RWE’s cost allocation from $1.25 million to $71.6 million. The study found a 0.07% overload under one contingency. RWE argued PJM erred in using DC loading instead of AC, a difference that would have removed the line rebuild from the cost assignment.

In concurrences on the March 19 order and comments made during the same-day open meeting, commissioners stated the complaint underscores the uncertainty developers face when submitting interconnection requests.

“While I and my colleagues agree with the outcome of denying the complaint, the facts of the proceeding raise big-picture concerns for how we will develop much needed generation to meet historic load growth,” Chair Laura Swett said during the open meeting. “The developer in this case spent significant time and capital to advance a project through several rounds of interconnection studies, only to discover significant unexpected network upgrade costs of $71 million.

“This caused the company to withdraw its service request entirely. We hope that PJM and the other RTOs will make reforms to reduce interconnection-cost uncertainty to facilitate the connection of much needed generation. There are many ways that RTOs can address these issues, but SPP’s [Consolidated Planning Process] that I just noted really stands out as a manner of solving them.”

RWE wrote that Manual 14B: PJM Region Transmission Planning Process requires planning staff to use AC loading in the six-step test used to determine whether a flowgate is overloaded. But the manual is silent on whether DC or AC should be used for the common mode outage procedure final determination. Without that specification, the company argued PJM should be required to use AC loading. The complaint asked FERC to reinstate the project’s queue position without the cost allocation for the Edge Moor-Linwood line.

PJM responded that RWE misunderstood how DC loading is used in the generation deliverability tests, specifically the common mode outage procedure. While the manual language detailing the common mode outage test does not specify if AC or DC should be used, PJM wrote it always used the DC, as it tends to be more stable, with fewer swings in infrastructure overloads between studies.

The response said RWE had not shown there was any misapplication of the generation deliverability procedures and its requested relief would harm other developers by shifting costs to other projects. That would violate the filed rate doctrine by requiring a waiver of the deadline for posting the security of the network upgrade costs the project was assigned.

All Phase III studies would have to be rerun after the completion of Transition Cycle 1, possibly requiring amendments to signed generation interconnection agreements. Granting planning staff the authority to apply the DC or AC loading case by case would undermine the consistency between studies and the assigning of network upgrades. Shifting the project to Transition Cycle 2 would result in cost-sharing between queues, which is prohibited by PJM’s tariff, the PJM response continued.

The commission found RWE had not demonstrated PJM failed to follow its governing documents and manual language, as none specify whether AC or DC loading should be used. Absent concrete manual or tariff language, the order deferred to PJM’s engineering judgment on which loading should be employed. It encouraged PJM to consider changes to reduce the uncertainty around interconnection costs and timelines as stakeholders on a review of whether the RTO’s markets are providing the incentives needed for new resources to serve forecast demand growth.

“Given the breadth of PJM’s review, we encourage PJM to consider whether there are regionally appropriate reforms that could reduce interconnection cost uncertainty and expedite the interconnection process in PJM,” the order states.

Rosner and Chang Concur, Recommend Changes to Interconnection Process

Commissioners David Rosner and Judy Chang wrote a concurrence stating that PJM had reasonably conducted its studies using a DC power flow rather than AC. But the complaint shows that developers are required “to take shots in the dark in pursuit of low-cost points of interconnection that fail to materialize.” They pointed to the “but for” approach to determining when projects are responsible for network upgrades as being responsible for “unmanageable risk”: The standard considers a project responsible for a network upgrade if the underlying violation would not be present “but for” the interconnection request.

“Although the band AC/DC once sang ‘a shot in the dark, makes you feel alright,’ reading the facts of this complaint felt more like being ‘on the highway to hell.’ This complaint is the latest example among many that shows how strict adherence to ‘but for’ cost allocation has made building a new generator too costly and too slow, making energy more expensive and less reliable for customers,” they wrote.

Rosner and Chang wrote that SPP’s Consolidated Planning Process shows how transmission planning and generation interconnection can be aligned. Approved on March 13, the process expands SPP’s long-term transmission assessment to include a generation expansion plan that aims to upgrade the system to be prepared for forecast growth, including specifying pre-planned locations where it would be most efficient to construct new resources.

Developers siting at those locations would enter into a generalized rate for interconnection development-contribution (GRID-C), providing interconnection costs up front before commitments are made. (See SPP’s Consolidated Planning Process a ‘Bold Step,’ FERC Says.)

“Needless to say, this level of unpredictability and variability could not be what the commission envisioned when it required grid operators to implement ‘but for’ cost allocation for generator interconnection over two decades ago,” they wrote.

HOUSTON — The U.S. Department of the Interior and TotalEnergies have announced an agreement under which the French global energy giant will give up leases for two offshore wind projects in return for nearly $1 billion that will be invested in American fossil fuel production.

As part of the agreement, Interior will terminate the leases for TotalEnergies’ Attentive Energy and Carolina Long Bay projects off the New York and North Carolina shorelines. Interior will reimburse TotalEnergies $928 million for the original lease expense after the company invests in developing U.S. natural gas exports, shale gas production and offshore oil drilling in the Gulf of Mexico.

Interior Secretary Doug Burgum and TotalEnergies CEO Patrick Pouyanné signed the agreement March 23 on the sidelines of CERAWeek by S&P Global.

“The era of taxpayers subsidizing unreliable, unaffordable and unsecured energy is officially over and the era of affordable, reliable and secure energy is here to stay,” Burgum told reporters during a press conference.

The secretary framed the agreement as “unleashing” nearly $1 billion tied up in a lease deposit made during the Biden administration and criticized subsidies “pushing expensive weather-dependent offshore wind.”

“Those subsidies were directed toward picking winners and those winners were forms of energy that were not only expensive, but they were intermittent,” Burgum said, adding the previous administration “lured” companies into “inefficient developments” with “massive” tax subsidies that created “artificial demand.”

“This administration believes in energy reality. We are not driven by climate fantasy,” he said.

In response, the offshore wind trade group Oceantic Network released a statement from Sam Salustro, senior vice president of policy and market affairs, that accused the Trump administration of political theater.

“After failing to shut down offshore wind through strong-arm tactics and litigation losses, the administration is now spending $1 billion in taxpayer dollars to force developers out of the market — wrapped in a false narrative about affordability, reliability and national security,” Salustro said.

Abandoning OSW in the U.S.

Pouyanné, who has said offshore wind is a pillar of the energy transition, said the company is not renouncing offshore wind but it is abandoning the technology in the U.S. “in exchange for the reimbursement of the lease fees.”

“These investments will contribute to supplying Europe with much-needed LNG from the U.S. and provide gas for U.S. data center development,” he said. “It’s important that our investments fit with the policies developed by the countries, and that’s what we will do here in the U.S.”

Pouyanné said it’s a matter of “ranking” technologies. Offshore projects are massive projects costing billions of dollars and take a long time to develop, he said, and still make sense in Europe where open land is scarce. TotalEnergies announced an agreement with Google in February to provide 1 GW of solar capacity for the tech company’s Texas data centers.

“At the end of the day in terms of allocation of capital, even if you target reliable and low-carbon energy, it’s better not to invest in [offshore] but to continue to invest in other technologies,” Pouyanné said. “Offshore wind is too expensive from my standpoint. We believe this is a more efficient use of capital in the United States.”

Interior said in its press release that TotalEnergies has pledged not to develop any new offshore wind projects in the U.S.

The agency stopped all offshore development in 2025, citing security concerns that Burgum again brought up during the press conference. TotalEnergies paused its wind farms’ development after the 2024 election, promising to reassess the situation in four years, and quickly came to the conclusion that offshore wind is not the most affordable way to produce electricity in the U.S., Pouyanné said.

He said the company met with Interior in 2025 and proposed to Burgum what he called an “innovated solution” to TotalEnergies’ situation.

“It was a win-win dialogue, and I welcome the fact that Burgum was very pragmatic as well, and why not?” Pouyanné said. “It’s original, a European company proposing to not litigate but to make pragmatic solution.”

Salustro was dismissive of the administration’s concerns.

“Winter Storm Fern showed how offshore wind helps keep the lights on and rates down for millions in the Northeast,” he said. “And while security claims have been reviewed and dismissed by multiple federal judges, the Department of the Interior and Department of Defense have repeatedly signed off on projects well before construction began.”

The “political theater” is “meant to obscure the fact that offshore wind capacity is being pulled out of the pipeline when energy prices are skyrocketing, even as other offshore wind projects continue delivering reliable and affordable power to the grid. Paying to remove affordable, homegrown energy out of the equation leaves American consumers struggling to pay their electricity bills,” Salustro said.

The labor and environmental group BlueGreen Alliance also released a statement from Vice President of Federal Affairs Katie Harris.

“Donald Trump truly can’t leave a good thing alone. His never-ending vendetta against offshore wind shows that he either doesn’t understand the affordable energy crisis or that he just doesn’t care,” she said. “Either way, it’s clear he’s never paid his own electricity bill, and he’s determined to raise bills for working people. He’s failed at every other attempt to halt offshore wind development, so now he’s doing what he always does: squandering taxpayer funds to force his own agenda.”

CAISO is moving toward approval of an $8.5 million financing plan for the Regional Organization for Western Energy’s start-up costs, saying the proposal has “widespread support” from stakeholders.

Under the West-Wide Governance Pathways Initiative, CAISO plans to transfer governance of its Western Energy Imbalance Market and soon-to-launch Extended Day-Ahead Market to the ROWE in 2028.

Now the ROWE is seeking a commercial loan or line of credit of up to $8.5 million starting in mid-2026 to cover start-up costs. In a Feb. 3 letter to CAISO, Pathways co-chairs Pam Sporborg and Kathleen Staks asked the ISO to develop a funding mechanism for the ROWE’s debt-financed start-up costs that would be repaid by market participants. (See Pathways Asks CAISO to Kickstart ROWE Funding Discussions.)

Sporborg and Staks said start-up costs for the ROWE would be about $8 million. Stakeholder donations and grants are expected to raise about $1.2 million.

CAISO released a straw proposal for the financing plan Feb. 5 and then posted a draft final proposal March 12 addressing stakeholder comments. The ISO held a meeting March 19 to gather additional feedback.

“The ROWE would be responsible for making payments on the loan, with the ISO serving as guarantor,” CAISO said in the draft final proposal. “This is necessary because the ROWE at that point [mid-2026] would not be able to obtain credit.”

Once the loan is in place, the ROWE would access funds periodically for start-up costs such as paying the initial board, hiring staff and consultants, and covering costs for equipment, insurance, travel and office expenses.

The loan would be structured so that the ROWE’s repayment wouldn’t start until 2028. Shortly before then, CAISO would start collecting money from market participants that would be sent to ROWE to repay the loan. The start-up costs would be allocated “in proportion to market participants’ benefits,” CAISO said.

“Although this rate would be allocated in fundamentally the same way the ISO recovers its own market-related costs, the rate would be separate from what the ISO charges to recover its own costs,” CAISO said in the draft final proposal.

Allocation Concerns

Stakeholders expressed support for providing credit backing to ROWE for a commercial loan or line of credit of up to $8.5 million, although some had questions about the specifics.

The California Municipal Utilities Association said it “supports continued progress toward independent regional governance and recognizes that a successful launch of ROWE could enhance regional coordination and market efficiency if designed and funded prudently.”

The Environmental Defense Fund said the ROWE should work to minimize its spending to reduce charges to market participants.

“This approach will allow ROWE to maintain a competitive edge as it seeks to maximize its market footprint while reducing ratepayer impacts,” EDF said.

CAISO responded that the ROWE board would provide “appropriate oversight of spending” and stakeholders can raise concerns about spending with the ROWE.

Several California utilities and the California Public Utilities Commission’s Energy Division voiced concerns about the cost-allocation method. The utilities — including Pacific Gas and Electric, San Diego Gas & Electric, Southern California Edison and a group of six California cities — said ROWE costs should be allocated based on real-time market participation only.

Because day-ahead volumes are much larger than volumes used for real-time balancing transactions, EDAM participants would be paying a larger share of ROWE start-up costs than WEIM-only participants, creating an unfair situation, they said.

But CAISO said real-time-only participation is “a lighter use of the market.”

“Allocating costs based on real-time participation only would ignore the significant day-ahead benefits and result in day-ahead users free riding on them,” the ISO said.

Next Steps

Although terms of the loan haven’t been finalized, CAISO said it expects it to be a variable-rate loan with repayment occurring during 2028. The ISO acknowledged that if the ROWE failed during 2027, the repayment schedule could be earlier.

Any additional comments on the draft final proposal are due April 2. The Western Energy Markets Governing Body and CAISO Board of Governors are expected to vote April 28-29 on the proposal. A tariff revision then would be sent to FERC for approval in early May.

CAISO noted that its proposed financing plan covers only ROWE’s start-up period.

“Issues related to ROWE cost recovery for ongoing post-start-up costs will be addressed in a later stakeholder proceeding,” the draft final plan said.

RENSSELAER, N.Y. — NYISO presented a detailed breakdown of systemwide issues in response to multiple calls from stakeholders for more granular information about conditions during the late January winter storm.

The weather encompassed most of the East Coast for a sustained period that lasted into early February. The already-gas-constrained Northeast was pressured even more, leading to near-record electricity costs and a reliance on oil for fuel. (See: NYISO: Gas Demand Soared Across Eastern U.S. During Fern.)

During the chill, liquid fuel provided roughly 2 million MWh of energy, while wind and solar collectively supplied roughly 500,000 MWh, according to NYISO. Only three other winters since 2013/14 have burned anywhere near that much fuel, with most only burning about half as much, Aaron Markham, NYISO vice president of operations, told the Operating Committee on March 19.

“Because of the constraints on the gas system, we had to make [dispatch] decisions early after the day-ahead when there was going to be more certainty about what was going to be unavailable,” Markham said. “If we don’t make those scheduling decisions and get the units working to get gas pretty timely in the gas nomination cycle, there [would be] no gas available.”

Markham also provided new insight into how and when NYISO called supplemental resource evaluations, a process by which the ISO can commit additional resources outside of the normal day-ahead scheduling process. They are activated only when day-ahead reliability criteria violations are forecast after the normal scheduling process has begun or when the ISO detects a reliability violation within the next 75 minutes. NYISO called SREs every day from Jan. 24 to Feb. 9.

January also set a record for the largest weekly natural gas withdrawals from storage. By Feb. 9, oil reserves were the lowest they had been since NYISO began tracking fuel inventories in 2016.

“During that cold snap, not only was it cold in New York, but [so was] the eastern part of the continent,” Markham said. “That drove gas prices to pretty high levels,” between $50 and $250/MMBtu. Heavy strain on the gas system caused pipeline operators to issue operational flow orders. That, combined with limited supply, forced some generators offline or to switch to oil.

Albany spent Jan. 23 through Feb. 10 at below-freezing temperatures, making the 19-day cold snap the longest seen since 2011. New York City spent nine days between Jan. 24 and Feb. 1 below freezing, the longest stretch for the city since the 2017-18 season.

During the worst of the cold Feb. 7, a Saturday, the fuel mix was 28% oil, 26% natural gas, 16% hydro, 14% nuclear, 10% imports and 6% wind. This coincided with the winter peak of 24,317 MW. Without demand response, the peak would have been 24,717 MW, according to NYISO. Three daily peaks in the cold snap exceeded 22,000 MW.

“We do estimate that if those similar weather conditions had occurred on a weekday, the load would have been in excess of 25,000 MW,” Markham said. That is “pretty close to the 90/10 load forecast for the winter.”

Most of the generator outages were concentrated in Zones F to K, an area encompassing the Capital District, the Hudson River Valley, New York City and Long Island. Most of the generators in the zones are natural gas- or oil-burning.

Stakeholders once again tried to get even more specific information on the outage locations, but Markham rebuffed them, saying it could identify individual facilities. He was able to say there were strong correlations between interruptions on the gas system and forced outages.

Report after report confirms that energy demand in the United States is growing fast, with AI data centers driving massive increases in the energy needed to keep the lights on. There’s no question we’re going to need more sources of energy if we’re going to keep up with demand, from more renewables to nuclear plants, and some companies and states are planning to restart or build from scratch.

There remains a sizable partisan gulf when it comes to energy generation, but officials on both sides of the aisle can agree that no matter how the energy is produced, it’s critical we have the modernized infrastructure to deliver it safely, reliably and affordably.

Right now, Congress could take major steps to speed up the process of building new transmission infrastructure. Two critical pieces of legislation —the SPEED Act and PERMIT Act — passed the House in late December with the potential to remove meaningful barriers to the development of new infrastructure and alleviate the demand crunch we face. But after a sudden move by the administration to halt offshore wind projects, the bipartisan coalition backing permitting reform legislation is now fracturing.

It is vital our lawmakers and regulators hold fast to their focus on realistic solutions that will break through the debate over how we get our energy and make sure it’s possible for energy users to access it when needed.

Much of the country’s transmission lines date back 70 years or more — leading to major bottlenecks that constrict our ability to deliver energy from these large-scale projects, even when we do have the power available. As the demand for reliable, affordable energy grows, the need for modernized infrastructure has never been more urgent.

Will Hazelip

Why does this matter so much? Because transmission is the enabler. It unlocks the potential of every other energy investment. Whether we’re talking about new renewables like solar or a refired nuclear plant in Pennsylvania, that energy means nothing if electrons can’t reach users. Today, projects are delayed for years, sometimes decades, because of permitting hurdles and outdated planning processes.

Right now, to build a major transmission project that crosses state lines, developers must abide by a patchwork of laws, regulations and requirements that trace their origins to different decades, legislatures and purposes. That makes it painfully difficult, if not impossible, to get steel in the ground and cable run from one pylon to another.

To fix this, Congress needs to empower FERC to play a leading role in siting interstate projects. As one of the most critical agencies in the federal permitting process, FERC needs the authority to mandate interregional planning — with projects measured against a clearly delineated set of desired benefits — and to site projects that cross state lines.

This will allow federal regulators to solicit, review and site projects with the potential to truly transform our electric system, evaluated against benefits such as improved reliability, reduced congestion, greater carrying capacity, reduced operating reserve requirements, and improved access to generation that reduces the cost of power.

Clearing the Backlog

The goal is simple: empower FERC to unlock the full potential of the grid without tying its hands and put the benefits for local communities front and center in the process. By accompanying this reform with adequate funding for our federal and state permitting agencies, we can clear out the longstanding backlog of projects yet to be reviewed and equip regulators with the tools to meet this incredible rise in demand. (See MISO Pushes Interconnection Queue Timelines Back Again.)

Transmission can and must be a bipartisan, realistic part of the solution to the demand challenge we face. The benefits reach beyond increasing available power for data centers and other large load users. A modernized electric system is far more resilient in the face of severe weather. And an interconnected system unlocks access to lower-cost energy sources over longer distances, keeping customers’ utility bills lower at a time when affordability is top of mind for every American.

Stronger transmission also equates to a stronger economy. Without enough power, local economies can’t take advantage of opportunities or host new large-load facilities, from data centers to major shopping and tourism attractions. By increasing the power flowing into our communities, we’re enabling and encouraging much-needed economic growth.

The Cost of Inaction

Critics argue that transmission projects are expensive or disruptive. But the cost of inaction is far greater. Every year we delay, we waste opportunities to develop large-scale projects that avoid the higher costs of scattered, piecemeal upgrades that saddle energy users with higher bills without nearly as many benefits.

This is an opportunity for leadership that reaches beyond party lines and focuses on something we broadly agree needs our attention, and which will deliver a tangible result for thousands of communities across the country.

Transmission isn’t a luxury. It’s the backbone of our energy system and it’s been too long since it was a national priority. The debate over how and where we produce our energy undoubtedly will continue. But as it does, we should acknowledge the common ground in front of us and seize the chance to improve how our system is built and maintained.

Ruling on a series of complaints dating back to 2011, FERC ordered a reduction in the return on equity for New England transmission owners, from 10.57 to 9.57% (EL11-66, et al.).

The commission set an Oct. 16, 2014, effective date for the rate and directed the TOs and ISO-NE to refund with interest all excess funds collected since this date. FERC also required refunds for a 15-month period beginning in October 2011.

The ruling appears to be a win for consumer advocates at a time of elevated concern about energy affordability in New England, though the 330-page order appears likely to face additional challenges and clarification requests.

The ruling comes “three presidents and 11 chairmen” after the initial complaint, FERC Chair Laura Swett noted.

“This ping-ponging of judicial review and agency action that has gone for 15 years is a great example of how our regulatory processes combined with unending ability to seek judicial review can cost ratepayers a huge amount of money,” she said at FERC’s open meeting March 19.

The order follows a convoluted series of petitions, rulings and court challenges.

The initial 2011 petition was filed by a group of utility regulators, consumer advocates and end users, who argued that the 11.14% base ROE in place at the time was unjust and unreasonable.

In rulings following the original complaint, FERC updated its methodology for setting ROE to include longer-term growth projections and alternative financial models. It set the base ROE at 10.57%, with an effective date of Oct. 16, 2014 (Opinion 531, et seq.).

Both the TOs and the complainants challenged this determination in court. The TOs argued FERC had not adequately justified its findings invalidating the original ROE rate, while the complainants argued the commission failed to justify the new 10.57% rate. The D.C. Circuit Court of Appeals agreed with both arguments and sent the case back to FERC.

As the TOs and consumers battled over the first complaint, transmission customers filed two additional complaints about the 11.14% base ROE in 2012 and 2014, along with a complaint in 2016 about the 10.57% base ROE established by FERC in 2014.

To address the issues identified by the D.C. Circuit over the first challenge, FERC in 2018 proposed a new methodology for calculating ROE, which it refined in a 2019 order regarding complaints about the ROE for TOs in MISO (Opinion 569).

The order set a new methodology, based on two financial models, for determining whether a ROE rate is just and reasonable and setting a new rate if needed. FERC amended this determination in follow-up orders in 2020, adjusting the modeling methodology and adding an additional risk premium model (RPM).

But the D.C. Circuit vacated the order and sent it back to FERC, finding that the commission failed to justify the inclusion of the RPM after originally finding this model defective.

FERC responded with an order in 2024 omitting the RPM from its ROE methodology, citing a lack of evidence to support its use. It set a new 9.98% rate for MISO TOs and required refunds for a 15-month period following the initial MISO complaint in 2013 and for the period from the 2016 effective date through 2024 (EL14-12-016, EL15-45-015).

Amid the court challenges, the New England TOs have continued to collect a 10.57% base ROE, though FERC has maintained its authority to set a different rate with an October 2014 effective date.

Determinations

In its ruling March 19, the commission set a 9.57% base ROE for the New England TOs, relying on the same methodology it ultimately used in the MISO proceeding. It found the TOs to have an average risk profile and set the “applicable range of presumptively just and reasonable ROEs” in the first complaint proceeding at 8.72 to 10.41%.

“In light of this and the other circumstances of the case, we find that [the TOs’] 11.14% base ROE is unjust and unreasonable,” FERC ruled.

The 9.57% replacement rate represents the midpoint of the applicable range identified by the commission.

It also set a refund period of October 2011 to December 2012 for the first complaint. Meanwhile, it dismissed the second, third and fourth complaints and did not issue refunds for these proceedings. It found the 9.57% ROE to be within the zone of reasonableness for these complaints.

The refund periods for the second complaint and part of the third complaint would have occurred in between the refund period for the first complaint and the 2014 effective date of the new 9.57% rate. The 11.14% base rate was in place at the time of these complaints.

While consumer advocates argued for refunds for this in-between period, FERC ruled that Section 206 of the Federal Power Act limits its ability to order refunds when not ordering a new rate. It noted that the FPA “explicitly limits the length of time that public utilities may be subject to potential refunds as a result of a commission determination in a proceeding to 15 months after the refund effective date.”

It wrote that issuing refunds for the second complaint and the pre-Oct. 16, 2014, portion of the third complaint “would exceed our statutory authority under FPA Section 206 because it would effectively extend the refund period in the first complaint proceeding beyond the statutory 15-month limit.”

While the TOs argued that the FPA also limits FERC’s ability to require refunds after the 2014 effective date, FERC disagreed.

“In this order, we establish a different replacement base ROE under Section 206 than was set previously,” it wrote, referencing the previous 10.57% rate invalidated by the D.C. Circuit. “In making the 9.57% rate effective prospectively from Oct. 16, 2014, and requiring refunds to reflect that rate, the commission is only requiring [the TOs] to reconcile this difference.”

Chair Swett said FERC is “doing everything we can within the limitations of our jurisdiction” to refund customers.

“Given the statutory limitations on FERC’s ability to issue refunds, unfortunately, we could only give relief to ratepayers on the first of the four complaints … because the Federal Power Act limits our authority to revise rates to a 15-month period,” she said.

Implications

The order sets the stage for significant refunds to New England transmission customers amid broad concerns about energy affordability in the region.

According to ISO-NE’s External Market Monitor, transmission rates in New England are more than twice the average rates of other RTOs, largely because of investments made over the past two decades to improve reliability and reduce congestion.

In recent years, consumer advocates have pushed for increased scrutiny around upgrades of existing transmission lines. These asset condition projects account for the vast majority of new transmission investment in the region.

According to some consumer advocates, a lower ROE should reduce the profit incentive for aggressive spending, potentially saving customers money directly by cutting the rate and indirectly by reducing overall spending.

Meanwhile, TOs argue higher ROEs are necessary to attract the level of investment needed to maintain a reliable grid.

“We are pleased that FERC has finally ruled in this matter; that it has lowered base allowed returns on equity and has established a refund requirement back to 2014,” said Drew Landry, deputy public advocate of Maine. “However, we believe that allowed ROEs remain too high and expect to continue to fight for more reasonable rates in future proceedings.”