CAISO released its first mandatory report under the California assembly bill that paves the way for an independent regional organization to assume responsibility over the ISO’s energy markets.

Under AB 825, CAISO must submit an annual report to the California governor and Legislature about the ISO’s various initiatives and decisions. Gov. Gavin Newsom signed the law in September 2025, and CAISO submitted the first report to the Legislature on Feb. 1, according to a news release.

“The ISO appreciates the commitment by Gov. Newsom and the Legislature to support independent governance of the real-time and day-ahead regional electricity markets that benefit consumers across the West,” CAISO CEO Elliot Mainzer said in a statement. “We look forward to continuing to work with the state and stakeholders throughout the region to help make that new governance framework a reality.”

AB 825 allows for the creation of an independent organization to oversee CAISO’s Western Energy Imbalance Market and soon-to-be-launched Extended Day-Ahead Market. The bill authorizes CAISO and California’s investor-owned utilities to join the organization.

In the AB 825 report, CAISO listed activities from the past year, including federal tariff proceedings, policy initiatives, decisions, market activity and transmission planning.

The report lists suggested enhancements to congestion revenue rights, initiatives to address reliability needs and uncertainties between the day-ahead and real-time market, new resource adequacy rules, storage enhancements and greenhouse gas coordination, among other initiatives.

CAISO also is working to “extend participation in the day-ahead market to the [WEIM] entities in a framework similar to the existing WEIM approach for the real-time market. EDAM will improve market efficiency by integrating renewable resources using day-ahead unit commitment and scheduling across a larger geographic area,” according to the report.

The report notes that CAISO intends to seek approval from its Board of Governors for its 2025/26 transmission plan in May 2026.

Under the 2024/25 transmission plan, CAISO received approval for 31 projects valued at $4.8 billion, 28 of which are for reliability purposes for $4.6 billion. The ISO estimated it needs 76 GW of additional capacity to meet increasing building electrification and electric vehicle loads. (See CAISO Approves $4.8B Transmission Plan to Support 76 GW of New Capacity.)

NYISO began what is expected to be a yearlong effort of revising its Reliability Planning Process at a Transmission Planning Advisory Subcommittee meeting Jan. 20.

“This is the best opportunity, if you have more concrete feedback, especially any specific suggestions so that we can consider those as we consider revisions before we roll them out,” said Ross Altman, NYISO’s senior manager of reliability planning.

The existing process uses a single base case to determine whether the transmission system meets all reliability criteria. Base case assumptions are identified in May, finalized over the summer and voted on in fall. The final reliability need assessment is issued in late fall. This goes hand-in-hand with the Comprehensive Reliability Plan (CRP), which considers system conditions a decade into the future.

“The only specific feedback we’ve received so far to process revisions is to consider a longer horizon,” Altman said. “There was a suggestion of 15 years. We welcome folks’ thoughts on that.”

Altman said the use of base case means the ISO needs to use the most conservative assumptions to account for growing uncertainty across all elements of grid planning. (See NYISO’s 2026 to be Dominated by Reliability Concerns.) The use of a single base case when reliability margins are tight can mean “flip flopping” between having and not having a reliability need.

Several stakeholders said they were concerned with moving away from a single base case to multiple base cases or scenarios that might trigger a reliability need. Representing Multiple Intervenors, Mike Meager asked Altman to clarify how the ISO would weigh different scenarios or circumstances probabilistically.

Altman said it was difficult this early in the process for the ISO to come up with a “true stochastic” look at probabilities.

“Not declaring needs on outliers is something we’re thinking about how to accomplish,” Altman said.

He said the process must maintain that reliability needs be based on criteria, and he added that multiple combinations of system conditions could more accurately reflect the changing grid. He stressed that the ISO was committed to “open and transparent” stakeholder involvement in revising the process.

The ISO is planning to review key study assumptions for the 2026 reliability needs assessment study with a particular focus on load uncertainty, aging generation, emergency assistance and generator outage rates.

Howard Fromer of Bayonne Energy Center asked how the ISO planned to stick to a 10-year planning horizon for the CRP, given that it was planning on folding multiple forecasts into the reliability process.

“How do we prevent that flexibility you’re looking for from swamping the competitive market, which is what we designed to achieve whatever our reliability requirements are?” Fromer asked.

Altman said that was always a risk when using a decadelong planning horizon for a one-year market. He suggested that the issue be separated from short-term reliability needs planning.

Fromer replied that it deserved consideration because the ISO could force a lot of unnecessary infrastructure investment.

Another stakeholder asked whether NYISO would consider changing some of its base case inclusion rules to be more realistic rather than conservative. Meager said he agreed and wanted the ISO to seriously consider how realistic its assumptions are.

“It’s not difficult to show some reliability criteria will be violated … if there’s no bounds or restrictions or constraints on what assumptions the NYISO can pick and choose to use each year,” Meager said.

Altman replied that the ISO is indeed considering the issue.

Alex Novicki, representing Avangrid, requested that extreme weather events be accounted for in the base case because, he said, NERC was going to try to account for them in upcoming resource adequacy standards.

Meager also questioned the ISO’s timeline for potential changes.

“What you are contemplating are some of the most significant changes to the Reliability Planning Process we have ever considered, with huge impacts moving forward,” Meager said. “There’s not a lot of meat on the bones before us right now. The idea that we’d be voting on tariff changes in a couple months is incredibly ambitious, if not highly unlikely.”

New York generators had to rely on oil as gas was scarce throughout the Eastern Interconnection during the Jan. 25-27 winter storm, NYISOsaid in a preliminary analysis that was a last-minute addition to the Installed Capacity Working Group’s agenda Feb. 2.

“We wanted to be timely and at least talk about some high-level stuff about what happened last week for folks so we could at least level-set some of the conversation,” said Shaun Johnson, NYISO vice president of market structures.

While the storm, dubbed “Fern” by the Weather Channel, caused few disruptions in the Northeast, it had such a large footprint that it affected demand and prices across the East.

“For those of you who are upstate New York natives, last week’s weather was cold, but it wasn’t extreme New York cold,” Johnson said. “The really important part of this is that it was cold in Atlanta.”

The weather created high demand for natural gas, causing price spikes that rippled through the market. Downstate generators had difficulty obtaining natural gas at all. Index prices during the winter storm were in the $50 to $200/MMBtu range, with some spot quotes in excess of $300. Average prices typically are much lower, with Johnson citing October 2025’s average of $2.17/MMBtu as an example.

Dual-fuel units shifted to trucked-in oil, which is less efficient than piped gas. Simultaneously, snow on solar panels and overcast conditions prevented solar resources from shaving down the peak load.

“During the first two days of Fern, we went through 20% of our oil inventory in New York,” Johnson said. He said the ISO ran its fuel survey multiple times over the week and heard stories of oil-fired generators being continuously served by caravans of tanker trucks “running out the gate” the entire week.

Johnson opened a map of the U.S. from the National Oceanic and Atmospheric Administration that showed the entirety of New England, New York and most of the PJM footprint under an extreme cold advisory. Cold weather extended southward into Tennessee Valley Authority and SPP territory. Effectively, the entire eastern half of the U.S. was in a state of elevated natural gas and electricity demand.

Johnson cited the NYISO 2025 Gold Book forecast of 24,200 MW of peak load in winter. He said the ISO had come close to that several days the previous week. He displayed a graph of day-ahead peak load forecasts during Fern that plateaued just under the Gold Book forecast for several days.

Additionally, several emergency actions were taken to reduce demand. The Special Case Resource program was activated multiple hours daily Jan. 25 to Jan. 30.

External prices also were extremely high, making it impossible to stabilize prices with cheap imports, Johnson said.

For most of the electrical industry’s history, weather was a constraint we designed around. Climate, by contrast, now is a system we operate inside of: a wild, unstable system.

That distinction matters more than many grid leaders, regulators and policymakers have absorbed. Extreme heat, wildfires, intense rain, drought and sea level rise often are approached as separate hazards — each deserving its own planning docket, modeling exercise or capital program. And while this column just completed a series on the impact of each hazard on the grid, they are not a collection of independent risks; they are a tightly coupled system of climate-driven stresses that interact, compound and persist in ways the grid never was built to handle.

Climate risk no longer is an environmental problem. It’s a governance, planning and management problem. And it sits squarely on the desks of utility executives, system operators and policymakers.

From Discrete Events to Systemic Risk

The industry knows how to deal with events. We respond to heat waves, storms, fires and floods when they occur individually. Mutual assistance is activated, crews are staged, emergency declarations are issued and restoration begins.

Climate change has turned those events into conditions.

Dej Knuckey

Heat no longer is a single-day peak but a multiday, multinight stress that simultaneously drives record demand, reduces generation efficiency and lowers transmission capacity. Drought is not just a hydroelectric issue; it constrains thermal cooling, increases wildfire risk and exposes weaknesses in the water-energy nexus. Wildfires are not seasonal hazards but year-round threats with cascading impacts on air quality, solar output, worker safety and liability exposure. Extreme rainfall doesn’t merely knock down lines; it floods substations, undermines foundations and complicates recovery logistics. Sea level rise isn’t a future storm-surge problem; it’s a slow, permanent redrawing of where infrastructure can safely exist.

Taken together, these risks do not stack neatly. They collide.

A heat dome can arrive during a drought, elevating fire risk. Fires strip vegetation, increasing the likelihood of debris flows and flash flooding when rain eventually comes. Flooded substations disrupt power to water systems just when pumping capacity is needed most. Smoke degrades solar output and limits air operations for line inspections. Each stress amplifies the next.

We can’t plan for each hazard in isolation.

Polycrisis, Meet Multisolving

Two terms I keep coming back to as I consider how the industry will manage in a future in which uncertainty is the norm are polycrisis and multisolving.

The term “polycrisis” was coined by French complexity theorists in the early 1990s and popularized in the early 2020s as the planet struggled with a pandemic, climate change, wars and economic instability. Climate change interacts with energy sources, generation, transmission and distribution infrastructure and the safety, well-being and economic stability of residential and commercial customers. It interacts with other critical infrastructure systems that both depend on and support the grid. And this is happening against a backdrop of income inequality, declining health outcomes, population migration and unstable federal emergency management support. Climate is not a single crisis for the grid.

“Multisolving” was coined by Dr. Elizabeth Sawin and focuses on the positive flipside of the coin: solving for one problem can solve for others. Think of it as the BOGO of the solutions crowd. For the grid, building resilience against one extreme challenge comes with the bonus of creating resilience against others, with a further ripple effect of improving reliability and lowering corporate exposure. Similarly, decarbonizing the grid with renewables and energy storage comes with the bonus of lowering exposure to fuel prices, increasing grid stability and improving the health of communities near power generation.

They are both linked to unintended consequences: polycrisis in a negative sense where one challenge results in multiple, compounding challenges; multisolving in a positive sense where one solution solves more than one challenge.

Grid Resilience in the Time of Climate Change

Most grid planning frameworks still assume three things that no longer hold: historical climate baselines, independent hazards and short disruption durations.

Reserve margins, resource adequacy models and integrated resource plans often are still calibrated to yesterday’s weather. Reliability metrics reward fast restoration after discrete outages, not the ability to avoid catastrophic system failure during prolonged, overlapping stresses. Yesterday’s n-1 contingency planning won’t work when climate delivers n-many failures simultaneously.

The problem isn’t a lack of data. Climate science has advanced rapidly, and hazard modeling is more sophisticated than ever, assuming inputs and assumptions are adjusted for today’s reality. The problem is institutional inertia: Planning processes and regulatory structures have not evolved at the same pace as the risk landscape.

The industry needs to focus on correlation risk. Heat waves reduce solar efficiency at the same time demand peaks. Wildfire smoke causes “wiggling” in photovoltaic output while also limiting crew deployment. Flooding disrupts electricity, communications and transportation at once. These interactions are predictable and need to be built into planning assumptions.

This planning needs to be done against a backdrop of rapidly accelerating risk. The creators of the First Street Correlated Risk Model found, “the frequency of losses resulting from major climate disasters in the U.S. has increased over fivefold in the past four decades, with climate change and increased development in vulnerable areas being the primary drivers.”

And there’s no one-solution-fits-all. Existing adaptation approaches typically assume rather simplified models, an IEEE study found. “The reality, however, is that climate change patterns and the uncertainties they introduce can differ regionally, complicating the formulation of effective countermeasures.”

As climate hazards become more frequent, more extreme and more varied, the industry can’t afford to rely on plans that appear robust on paper but are brittle in practice. The industry must invest in comprehensive planning and prioritize infrastructure upgrades that address multiple risks.

Climate Risk Has Become a Balance-Sheet Issue

The most underappreciated shift may be financial rather than technical.

Climate exposure is reshaping utility balance sheets. Wildfire liability has driven bankruptcies and forced restructuring, insurance providers are retreating from high-risk regions or sharply raising premiums, and credit rating agencies are flagging climate exposure as a material risk. Capital costs are rising fastest for utilities with the greatest climate vulnerability, often the same utilities facing the largest infrastructure reinvestment needs.

In effect, climate risk is becoming a de facto regulator, often acting faster and more bluntly than public utility commissions.

This matters because resilience investments too often are framed as discretionary or extraordinary: nice to have if regulators approve, deferrable if rates are politically sensitive. But in reality, failing to invest in resilience now simply shifts costs forward, where they reappear as higher borrowing costs, insurance gaps, emergency repairs and, ultimately, customer harm.

Swiss-Re Institute, which studies the risk landscape closely — because reinsurance companies are the ones pricing the growing risk — said, “Ongoing risk assessment is necessary to ascertain how resilient infrastructure is. Assets that are poorly maintained are more vulnerable.”

Conversely, today’s resilience investments can pay dividends beyond repairing and preparing for the same risk. Think about the $1 billion, four-year Con Edison storm fortification initiative following Superstorm Sandy: It was triggered by outages following a storm surge, but is paying dividends as the utility faces ice storms, heat waves and more.

Executives who treat climate adaptation as an environmental compliance issue are misreading how quickly financial markets are moving.

No Utility is an Island

Another lesson emerging across climate hazards is that grid resilience cannot be built in isolation. Power outages cascade. They shut down water pumping and wastewater treatment. They cripple communications networks. They undermine emergency response and health care delivery. During fires and floods alike, loss of electricity turns manageable crises into life-threatening ones.

Yet in many states, energy planning remains siloed from water utilities, emergency management agencies, transportation departments and telecom providers.

Cross-infrastructure coordination can’t be ad hoc or occur only after a disaster. Integrated planning and response reduce both risk and cost. If infrastructure needs to be protected from rising sea levels, for example, it’ll be more cost effective if all affected agencies coordinate resilience investments, hardening power, water, wastewater treatment and roads simultaneously.

At the same time, a region may be more of an island than ever before: If multiple states face an event at the same time, like the winter storm that recently shut down a solid slice of the lower 48, mutual aid agreements break down as crews are needed locally and flying in distant crews becomes impossible. Mutual aid is ideal, but some disasters will be more Lord of the Flies than Swiss Family Robinson.

Resilience is not something the power sector can buy on its own. It is an interdependent system, and governance structures have to reflect that reality.

What a Climate-adjusted Grid Strategy Actually Looks Like

If climate risk is now a core management challenge, what follows is not a checklist of projects but a shift in mindset.

First, resilience must move beyond asset hardening toward system flexibility. Hardening substations and elevating or undergrounding equipment remain necessary, but they are insufficient on their own. Islandable microgrids, distributed energy storage and modular recovery strategies allow systems to absorb shocks rather than simply resist them. Flexibility — not brute strength — is what enables systems to function under compound stress.

Second, planning must explicitly account for duration. Multiday heat waves, weeks of wildfire smoke, yearslong droughts and permanent sea-level rise pose fundamentally different challenges than short, sharp events. Planning processes that focus on peak hours or single-day extremes underestimate both operational strain and human fatigue.

Third, we must align incentives with future conditions. Regulators play a critical role here: Cost-recovery frameworks still favor post-event rebuilding over preemptive adaptation, even though avoided outages and avoided disasters deliver far greater public value. Utilities, for their part, need to treat resilience as a core dimension of service quality — not a regulatory add-on.

Planning for grid resilience requires a comprehensive framework such as the one developed by NARUC | NARUC

Fourth, reliability metrics need updating. Measures that prioritize restoration speed after outages do little to encourage investments that prevent catastrophic failure in the first place. In a climate-altered grid, success increasingly looks like outages that never happen, liabilities that never materialize and emergencies that never escalate.

Leadership in a Non-Stationary World

The grid already is operating inside a climate-stressed environment. The question facing leaders and policymakers is not whether the lights can be kept on during the next storm, it is whether governance structures, planning tools and investment frameworks can evolve fast enough to manage permanent instability.

That evolution will be uneven. Some utilities and system operators are already internalizing climate risk as a core design constraint. Others remain trapped in a compliance mindset, waiting for clearer regulatory signals or the next disaster, legal action or insolvency to force action.

The future of our industry will not be defined by how cheaply it delivers electrons, but by how well it absorbs shock, and that can happen only if leaders treat climate risk as the multidimensional management challenge it has become.

With natural gas being the dominant fuel for electricity generation in New York, rising electricity prices are driven by the increased cost of gas because of the ongoing Russia-Ukraine War and increased LNG exports, according to a recent policy paper by NYISO.

The paper, released Jan. 29, comes after a week of winter weather and elevated off-peak prices. It relied on the Short-Term Energy Outlooks (STEOs) by the Energy Information Administration and an analysis of electricity prices by Lawrence Berkley National Laboratory.

Prior to the surge in LNG exports, prices remained low because of the shale gas fracking boom of the late 2000s, just as President Barack Obama entered office. Around the same time, Russia began antagonizing Ukraine, culminating in the invasion and annexation of the Crimean Peninsula in 2014. Russia, which also controlled most of Europe’s supply of natural gas, cut off supply to Ukraine the same year.

To counter Russia’s aggression and lessen Europe’s dependency, the Department of Energy under Obama began in 2012 to issue approvals of LNG facilities for exports to countries with which the U.S. did not have free-trade agreements, a policy that continued under Presidents Donald Trump and Joe Biden — though Biden would unsuccessfully attempt to pause such exports in early 2024.

The U.S. became a net exporter of LNG in 2017 and the world’s leading exporter in 2023, according to a 2024 study at Harvard University. In its STEO for January 2026, EIA noted that LNG exports in 2025 increased by roughly 26% compared to 2024 exports, growing to an estimated 15 Bcfd.

“For context, U.S. residential gas customers consume approximately 12 billion cubic feet of gas per day,” the NYISO paper says. “In other words, the U.S. is forecast to export more natural gas than residential customers are expected to consume.”

The result has been a strong correlation between gas and electricity prices across the U.S., including in New York. The Transco Zone 6 pricing hub is the primary procurement site for the state’s gas fleet. In 2020, amid the COVID-19 pandemic, the price at the hub was $1.64/MMBtu. In 2022, Russia began its full-scale invasion of Ukraine, and exports to Europe — sent over pipelines that run through Ukraine — dwindled. The Transco 6 price shot up to $7.01/MMBtu.

The price for electricity followed the spike, from the record low of $25.70/MWh in 2020 to $89.23/MWh in 2022, according to the paper.

While prices for both electricity and gas fell in the short term, they gradually rose again over the next three years as LNG exports continued to grow. In 2024, gas traded on average at $2.10/MMBtu; by 2025 prices were hovering around $4.64/MMBtu. “The result was significantly higher wholesale prices for electricity as well — with an average price of $74.40/MWh throughout 2025, compared to $41.81/MWh for 2024,” the paper says.

The paper was published just after a Jan. 28 meeting of the Budget & Priorities Working Group in which stakeholders asked NYISO staff why energy prices were trading high when load was not near peak.

“We’re noticing right now that while the load isn’t great, the marginal cost of energy is very high,” said Kevin Lang, a lawyer representing the New York City and Multiple Intervenors.

Many stakeholders asked for specifics on hourly pricing, and what facilities on which pipelines were involved in setting daily natural gas prices.

“It’s not just as simple as ‘Transco 6 day-ahead cleared at X,’” said Doreen Saia, chair of natural resources law at Greenberg Traurig. “There’s a lot of factors going on.”

In an email, Lang told RTO Insider that the policy paper did not answer his questions about why energy prices had been surging during periods of low demand, particularly in recent days. According to Yes Energy data, off-peak prices have been on average higher than on-peak prices over the previous 10 days.

Barbara Kates-Garnick, a professor of the practice of energy policy at Tufts University and former Massachusetts Department of Public Utilities commissioner, said rising price trends could be broadly attributed to natural gas prices, Trump’s energy export policy and demand.

“Exporting LNG does subject all burns over time to world markets,” Kates-Garnick said. “Global natural gas prices were something that we had to become more sensitive to” during her time on the DPU and as undersecretary of energy.

She said the question facing local policymakers is whether to invest in infrastructure or “cobble” solutions together to deal with emergent price spikes.

“We keep pushing this can down the road. Every time it emerges, we address it as if it’s a new problem,” she said. “It’s very frustrating.”

IESO is reconsidering how it deploys hourly demand response (HDR) following complaints over partial activations and an increase in standby notices.

In a meeting Jan. 29, stakeholders expressed frustration over IESO’s issuance of standby notices and said partial DR activations were harming performance. The ISO also heard concern about its announcement that the capacity targets set in the Annual Planning Outlook will no longer be binding and may be adjusted upward or downward before the yearly auction.

IESO said HDR resources are “critical” to reliability during tight supply conditions but that they have historically underperformed, making it difficult for control room operators to maintain supply-demand balance during emergencies. In summer 2025, IESO activated 16,775 MW of HDR, but only 12,153 MW (72%) was delivered.

IESO previously triggered HDR activations manually during a Conservative Operating State or NERC Energy Emergency Alert 1. More recently, activations have been triggered by pre-dispatch scheduling run prices exceeding $2,000/MWh.

HDRs were activated 10 times in summer 2025 and seven times so far this winter, an increase from the historical rate of two to three activations in summer and none in winter.

The ISO acknowledged that more frequent HDR activations could lead to “resource fatigue” and participants dropping out. In addition, “all-or-nothing” HDRs lack the ability to follow dispatch instructions for partial activations.

As a result, IESO said it will hold an engagement over the next three capacity auctions on potential changes to HDR rules and improvements to non-HDR rules that have been identified in previous engagements.

The engagement, scheduled to begin in Q1 2026, will initially focus on “achievable ‘quick wins’” due to the limited time available before the 2026 auction, the ISO said.

Standby Notices

IESO issues standby notices to provide HDR resources time to prepare for potential activations.

Gilon Hershkowitz, of steelmaker ArcelorMittal, asked for guidance to help DR providers understand when standby notices will translate to activations.

“We want to be able to respond to the activations with our full capacity. [With] the short notice it’s very challenging for us to do so,” he said. “If we receive [fewer] standby notices and [have] a higher level of confidence that when we do receive a standby notice — maybe there’s some other data that [will indicate] this notice will actually translate to an activation — teams can be prepared.”

Laura Zubyck, IESO’s capacity auction supervisor, said the ISO will review its procedures to “make sure the standby is working in the way that that we want it to.”

Ted Leonard, of EnPowered, said the Market Renewal Program, which introduced LMPs and a financially binding day-ahead market in May 2025, has resulted in a “new normal” with unintended consequences.

“HDR [is] a reliability product; it wasn’t constructed to have partial activations,” said Leonard, IESO’s former chief financial officer. “It’s not meant to be there to help suppress prices during high demand events. It’s meant to keep the lights on.

“Maybe we need to look back and say, ‘Was this the intended consequence?’” he added. “Was this what HDR is all about, or HDR is meant to be? Because it feels like we’re losing our way a little bit.”

Zubyck said higher-than-normal temperatures during summer 2025 caused an increase in HDR activations and — for the first time — partial deployments.

“Now that we are seeing a partial activation of an HDR, we need to look at it, and we need to understand if there’s perhaps some changes we need to make,” she said.

Inefficient Decisions?

Roman Grod, of Rodan Energy, said his company has been challenged by partial activations that differ hour to hour. “Let’s call it 10 MW in the first hour, 15 in the second and 20 in the third. … That’s when I think it gets a little more challenging, because then you’re forced to do this kind of cascading effect where you’re activating folks for … three hours, then a different … side of your portfolio for two hours, and then another one for three hours,” he said.

Aaron Lampe, of Workbench Energy, said the ISO’s optimization engine is making inefficient decisions in picking HDR resources because “unlike for other resources, where the tools the ISO has built respect the operating characteristics of those resources — things like minimum loading point, ramp rates, minimum runtime, daily energy limits, etc. — none of those are reflected for the DR resource.

“And so, the optimization engine is picking the DR resource in situations to fill these short gaps, assuming this is an essentially infinitely flexible resource and then activating them. But it’s actually a very expensive resource [because of] market payments outside of that optimization that are occurring.”

Zubyck said the ISO is reviewing its rules “from a holistic level.”

“It’s not as simple as … we need to just fix partial activations, or we need to do this item. We do have to kind of look at everything that happened and consider … those bigger questions.

“This is the feedback we want to hear: that it’s a challenge to go up and down for some resources, and that we may need to consider … solutions to deal with that,” she added.

Other Priorities

Lampe said that stakeholders have been waiting for several years for action on items that were “shelved,” in part because the ISO was consumed by developing the Market Renewal Program.

In late 2023, Lampe said stakeholders had a meeting with the ISO to discuss issues regarding DR data submission and metering requirements. “It’s been two-and-a-half years or so [and] we haven’t heard anything following up,” he said. “I just want to ask: Are those still being tracked? … And how do those fit in the relative prioritization?”

Zubyck said the issues will be included in the new engagement. “We will bring those items back out and start to speak with stakeholders again about reprioritizing them and … allotting them into the next few auctions,” she said. “They have not been shelved.”

Changing Capacity Targets

Rodan Energy’s Grod also expressed concern about the ISO’s announcement that the capacity auction targets published in the Annual Planning Outlook (APO) each spring will now be preliminary, with the binding target published in the Pre-Auction Report in summer.

“This change provides additional flexibility for the IESO to adjust the target in response to issues/uncertainties that may emerge after the APO is published,” said the ISO, adding that the changes “will have limited impacts on stakeholders.”

“The ability to decrease the target concerns us significantly,” Grod said. “Customers often commit to this program based off historic clearing prices and where they … see the market going. [The] target in the APO really provides some level of confidence that … pricing is going to stay somewhat stable.

“If the ISO has the ability to lower the target — say, by 500 MW — that’s going to have a significant negative impact on pricing,” he added. “And I frankly think that that’s the wrong signal we want to be sending, especially as we’re seeing this resource be … activated more and more often.”

Bryan Timm, senior adviser on IESO’s capacity auction team, said the ISO would raise or lower the target only in response to an “unusual or significant event.”

“If [a] procurement delivered fewer megawatts than we anticipated, that might cause us to consider raising the target to meet system needs,” he said. “So, these would be significant events, not … one-off, minor changes.”

Feedback

Feedback on the Jan. 29 engagement is due Feb. 12 via the feedback form on the Capacity Auction Enhancements webpage.

A judge has granted developers of Sunrise Wind a preliminary injunction against one of the federal stop-work orders slapped on U.S. offshore wind construction.

The Feb. 2 ruling in the U.S. District Court for the District of Columbia (1:26-cv-00028) completes the judicial pushback against the Trump administration: One by one, in the space of three weeks, four judges have granted the five projects under construction in U.S. waters permission to resume construction.

Sunrise Developer Ørsted said it would resume construction of the 924-MW project as soon as possible and said: “Sunrise Wind will determine how it may be possible to work with the U.S. administration to achieve an expeditious and durable resolution.”

Durable is an important caveat.

President Donald Trump has attacked offshore wind relentlessly, starting with an executive order hours after his second term started. His administration has moved on multiple fronts to hinder construction of projects underway and block future construction from starting.

This culminated in the five stop-work orders issued Dec. 22 on grounds of national security that now have been set aside.

Revolution Wind got its injunction Jan. 12, Empire Wind Jan. 15, Coastal Virginia Offshore Wind Jan. 16 and Vineyard Wind Jan. 27.

Counting an August 2025 stop-work order against Revolution that a judge lifted and an April 2025 stop-work order against Empire the Trump administration removed after discussions, the administration’s record is 0-1-6.

But the fight is not over, and the administration has secured an important achievement: Investors likely have been scared away from U.S. waters. Further, the offshore wind industry has been thwarted in its attempts to develop infrastructure, create an industrial ecosystem and build project momentum in the U.S.

There also is considerable financial impact on the developers.

Empire placed the cost of the April 2025 stop-work order at $200 million. Court papers estimated the costs at “millions per week” for Revolution and $2 million a day for Vineyard.

In a Jan. 30 regulatory filing, Dominion tallied the full cost of the December shutdown at $228 million.

Sunrise, which is at an earlier stage of construction than the other four projects, said in its Jan. 6 complaint that the shutdown was costing it more than $1 million a day.

“Sunrise Wind represents a vital investment in strengthening both Long Island’s power system and the broader regional grid that millions of residents rely on — particularly during the harsh winter months. Offshore wind is uniquely suited for these conditions and stands ready to deliver steady, abundant power, easing the burden on families who have long relied on costly peaker plants to keep the lights on. Oceantic applauds this decision, which moves us closer to providing reliable, affordable clean energy and creating high‑quality jobs for the communities that stand to benefit the most.”

New York’s senior U.S. senator, Charles Schumer (D), posted on X: “Trump just received his 5th straight loss in the courts in his crusade to stop offshore wind and kill thousands of jobs. Trump is losing his war against offshore wind. I will keep fighting to make sure these projects and the thousands of good-paying jobs they create move forward to help reduce energy costs for the country.”

Some of the many opponents of offshore wind wasted no time replying.

“SHAME ON YOU! SHAME! SHAME! SHAME!” was among the milder comments.

Replacement resources would qualify for replacement generation interconnection studies in lieu of the full slate of network impact studies new resources must undergo. The replacement resource cannot exceed the maximum output of the retiring unit, and it must interconnect at the same substation bus and voltage. The studies are expected to take 180 days to complete.

Since the CIRs for the deactivating resource already have been studied and the unit included in PJM’s system modeling, the commission wrote it is not necessary for a replacement to undergo the full suite of studies to ensure deliverability. The creation of a parallel queue would not constitute queue jumping because the CIRs already have been studied and determined to be deliverable, while the network impacts of a greenfield project are unknown.

The filing is PJM’s second crack at creating a fast track for replacement resources after the commission rejected its first proposal in August 2025 because of two carveouts from the proposed requirement that projects be capable of entering service within three years. Those provisions would have created a one-time extension of the in-service date requirement and an exception for resources with long development timelines, which the commission wrote would undermine the purpose of PJM’s proposal: bringing replacement resources online faster (ER25-1128).

“PJM’s proposal permits milestone extensions only in certain circumstances, and only for up to a specific amount of time, which will help ensure that the replacement generation interconnection process results in the timely and efficient replacement of generating facilities. Unlike the prior proposal that allowed replacement generation project developers to unilaterally extend the commercial operation date for their project without restriction, the instant proposal allows PJM to ‘reasonably extend’ the in-service date or other milestones under specified conditions,” the order states, adding that if a developer requires a longer extension, a waiver can be requested from the commission.

Those milestone extensions would be permitted only for “delays not caused by the project developer and that could not have been remedied through the exercise of due diligence,” PJM wrote in its transmittal letter. Milestone extensions would be capped at three years past the original commercial operation date.

PJM wrote the proposal is one of several changes to PJM’s planning and interconnection processes intended to allow resources to come online more quickly as the RTO seeks to ward off a looming resource adequacy shortfall. Other efforts include the Reliability Resource Initiative, which allowed 51 resources that could quickly add capacity to be inserted into Transition Cycle 2, and expanded eligibility for surplus interconnection service. (See FERC Approves PJM’s One-time Fast-track Interconnection Process.)

“At a time when PJM needs additional capacity resources in the near term to meet serious resource adequacy challenges, the expedited processing of replacement generation interconnection service requests claiming a deactivating facility’s CIRs can yield significant reliability benefits by facilitating the timely addition of new capacity while promoting the efficient use of existing infrastructure,” PJM wrote.

The Independent Market Monitor protested the filing, arguing it would divert planned resources from the cluster-based interconnection queue to a less efficient serial study process and further slow development by creating an incentive for resource owners to withhold CIRs until they can be sold to a developer.

During the stakeholder process that led to PJM’s filing, the Monitor proposed a model under which the CIRs associated with a deactivating resource would be made available to all resources on the grid as transmission headroom. It reiterated the argument that CIRs should not be for sale in its protest. (See “Voting on CIR Transfer Proposals Deferred to October,” PJM PC/TEAC Briefs: Sept. 12-13, 2024.)

“The basic purpose of the process is to permit existing generators to sell their CIRs to the highest bidder rather than to identify the best replacement resource. The proposal is inconsistent with open access and the purpose of CIRs. A proposal to truly reform CIRs would terminate CIRs immediately at the time a resource deactivates, and thereby avoid undue discrimination, promote competition and facilitate the rapid entry of needed new generation,” the Monitor wrote.

The commission wrote the proposal would not implicate market power as the ability to transfer CIRs already is codified in the tariff.

“This filing simply establishes an expedited review process for replacement generation resources interconnecting at the same location as a deactivating generating facility that would not change the voltage or maximum generation output at that location. Nothing in the instant filing would modify the existing rights to transfer CIRs or the transfer process,” the order states.

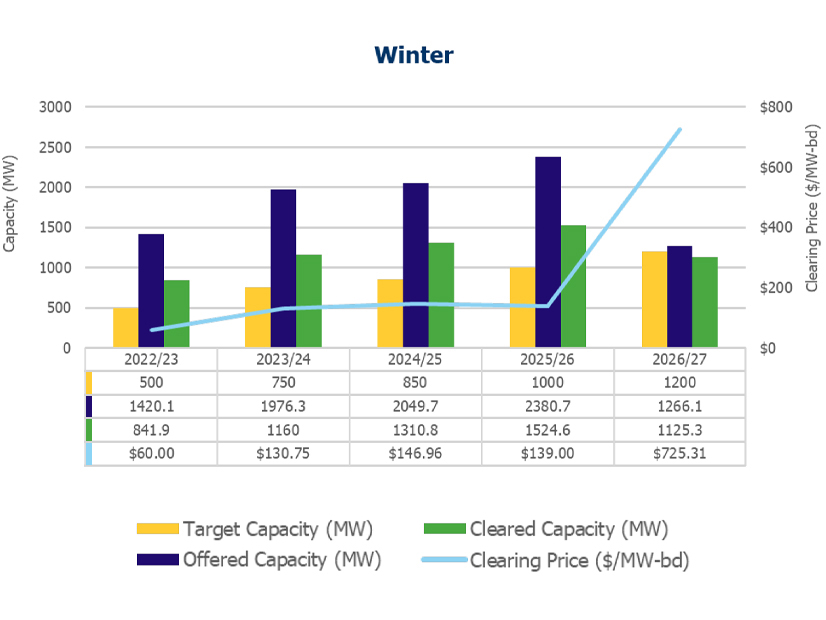

IESO downgraded less than 100 MW of capacity for November’s auction in the first application of its Performance Adjustment Factor (PAF) in both the winter and summer seasons.

The PAF ensures the ISO procures only capacity that has been confirmed by testing.

“It really was a small number of megawatts that ended up being derated because of the [PAF] … less than 100; probably less than 50 megawatts. But it was a very small amount,” Laura Zubyck, IESO’s capacity auction supervisor, said during a Jan. 29 engagement. “We’ve seen good performance in our capacity tests, and so we rarely derate.”

IESO year-over-year capacity auction comparisons for winter. | IESO

IESO’s Paulo Antunes said the results reflected short-term changes in supply combined with a 200-MW increase in the target capacity. The auction cleared 1,832.8 MW for summer 2026 and 1,125.3 MW for winter 2026/27.

IESO cleared no imports from New York, a loss of 200 to 300 MW compared with previous years. Antunes said. In addition, about 200 MW of Ontario-based generation that previously participated in the auction instead signed contracts with the ISO under its second medium-term procurement.

“The remaining available supply in the market was not enough to offset the combined impact of these two factors,” said Antunes, who also noted the impact of increasing electricity demand and ongoing nuclear refurbishments.

Virtual hourly demand response resources made up the largest share of cleared capacity, representing almost 41% in summer and 60% in winter. (See related story, IESO, Stakeholders Ponder Changes to Hourly DR.)

The largest increase in cleared summer capacity came from system-backed imports, which accounted for almost one-third of cleared capacity.

The increase largely was enabled by increasing the Hydro-Québec import limit from 400 MW to 600 MW.

Generation-backed imports, in contrast, declined.

The 2025 auction also showed a narrowing gap between offered and cleared capacity. “In previous years, the gap has been much bigger, and this is resulting in an upward pressure on price,” Antunes said.

Julien Wu, of Brookfield Renewable, thanked the ISO for providing more detail on auction results than in past years but asked officials to provide still more, including information on the technology types that experienced derates due to the PAF.

“The more information we have, the easier it is for us to make scheduling and trading decisions,” he said.

NYISO staff presented more of their initial ideas for improving the Demand Curve Reset process, centered on alternative shapes, slopes and points of the curve.

“The demand curve is at the core of aligning system reliability needs to market fundamentals,” Michael Ferrari, market design specialist for NYISO, told the Installed Capacity Working Group on Jan. 21. “Modifying them can enhance the efficiency of market signals to improve capacity market outcomes.”

The DCR shape and slope govern the value of capacity under different market conditions, sending price signals for new resource development and retirement of old units. The more installed capacity that is on the grid, the less any given megawatt is worth, and vice versa.

The curve is drawn from the zero crossing point (ZCP) to a reference point set by the cost of new entry and locational minimum capacity requirement. The ZCP is where the marginal price of an additional megawatt of capacity is equal to zero.

Currently, the curve slopes downward from the maximum clearing price plateau in a straight line to the reference point and the ZCP. Ferrari said NYISO had investigated “kinking” the demand curve into multiple slope segments, increasing the steepness of the curve to change prices more rapidly and increasing the ZCP. The ISO also discussed pinning the loss-of-load expectation reliability criteria to losing the largest generation unit in each location, similar to the N-1 contingency analysis in transmission planning.

“We are not trying to indicate an endorsement of any particular change or option,” Ferrari said, explaining that the presentation reflected “early analysis” of reform options.

Stakeholders said adjusting the ZCP might be difficult. Howard Fromer of Bayonne Energy Center said the first time the ZCP was set was a heavily negotiated process. Doreen Saia, of Greenberg Traurig, agreed.

“All of our locality curves have to work within the [New York state] curve,” she said. “If you extend out some of the curves too far, it eats into the ‘Rest of State’ price. … If you go too tight, then New York City gets problematic very quickly.”

Saia said that she welcomed looking at the demand curve and ZCP “with fresh eyes” because the situation has become much more complex, from both a regulatory and market player standpoint. More entities of more types are in the market trying to sell power.

One stakeholder mentioned that in the current DCR process, there are provisions to revise the shape and slope of the curve, but in practice this does not happen regularly. Ferrari said that the last time he recalled discussing changes to the ZCP was in 2014.

“Mike, I think you’re absolutely right,” Saia said. “We could have always looked at shape and slope, but for the first six or seven reset processes, the only thing that was even slightly considered was moving to a combined cycle gas facility” for the reference point.

Pinning the LOLE to a contingency analysis based on the largest generator also stirred discussion among stakeholders. Some said this would establish an incentive to build “really large generators” by essentially announcing that the demand curve would shift to accommodate them. One said that a contingency in the capacity requirement created uncertainty in developer cost-benefit calculations.

A NYISO staffer argued that using the largest generator had the benefit of greater clarity and transparency for understanding how the market would behave and would not necessarily increase market complexity.

NYISO is also considering alternative ways to divide transmission congestion contracts into more granular products.

Currently, TCCs are a 24-hour product only. NYISO is the sole RTO/ISO to offer only 24-hour financial transmission rights. This has been criticized by stakeholders as limiting the effectiveness of TCCs to serve as hedging mechanisms against congestion because they cannot distinguish between congestion patterns that change during the day or over the course of a week.

NYISO considered time-differentiated TCCs in 2021, proposing products for on-peak workdays, off-peak weekends and holidays, and off-peak “all other hours.” In 2025, Calpine proposed a system that broke TCCs into on-peak and off-peak hours. (See Calpine Sees Support for TCC Auction Proposal.)

The ISO is planning on finalizing a proposal in 2026, building off both its 2021 design and Calpine’s. Tariff language will not be pursued until it passes the annual project prioritization process.

Champlain Hudson Power Express Integration

NYISO provided stakeholders with an update on the Champlain Hudson Power Express integration process.

The capacity market is predicated on annual inputs with limited seasonality, and the capability year starts in May. If CHPE’s integration into the grid is mistimed, it could have major implications for capacity market parameters, such as the transmission security limit for the New York City-area capacity zones.

To accommodate this uncertainty, the ISO created two sets of market parameters, one assuming CHPE is operating and one assuming it is not. This creates two sets of TSLs, locational capacity requirements, capacity accreditation factors, unforced capacity demand curve parameters and load-serving entity minimum capacity requirements.

If CHPE provides notice by March 2 to participate in the ICAP market in May, NYISO will set the market to reflect its participation. The ISO intends to issue a notice by March 9 to market participants as to whether CHPE will be in the market.