California’s two large offshore wind projects could be delayed by up to six years due to recent federal policy actions, a California Public Utilities Commission administrative law judge said Jan. 14.

The Morro Bay offshore wind project is now forecast to come online by 2036 rather than 2032, CPUC ALJ Julie Fitch said in a proposed decision on electric integrated resource planning and procurement. A second project, in Humboldt County, is projected to come online by 2041 rather than by 2035.

The delays are “reasonable and should be adopted as the recommendation for CAISO’s 2026-2027 Transmission Planning Process,” Fitch said in the proposed decision.

The forecasted delays are part of the CPUC’s latest electricity and sensitivity resource portfolios, which the commission sends to CAISO for inclusion in the TPP. The ISO uses each TPP to determine whether additional transmission projects are needed in its region.

Although federal policy will affect California’s offshore wind projects, regardless of these policy changes, “it is important to note that offshore wind is not optimally selected in least-cost modeling,” the proposed decision says.

Numerous parties cautioned against delaying transmission planning that would support offshore wind in Humboldt County beyond 2036.

Environmental Defense Fund told the CPUC that the offshore wind industry is “at an inflection point” and that delaying the planned projects’ online dates could cause a “significant chilling effect that would not be in the interest of ratepayers,” the proposed decision says.

CalCCA recommended the CPUC maintain the amount of in-state and offshore wind in previous TPP portfolios and limit out-of-state wind. And Humboldt County representatives questioned why the North Coast offshore wind project is delayed by six years while Central Coast is delayed by only four years, the proposed decision says.

Many other stakeholders expressed concern that the state is planning to rely heavily on new out-of-state solar development when in-state resources, such as offshore wind, would be preferable, the proposed decision says.

The current TPP base case for 2025-2026 includes 4.5 GW of new offshore wind capacity.

Additional RA Procurement Proposed

Under the proposed decision, load-serving entities would need to procure an additional 2,000 MW of net qualifying capacity (NQC) by 2030 and 4,000 MW more by 2032.

This additional procurement is the result of the CEC’s 2024 Integrated Energy Policy Report demand forecast, which showed an increase in demand due to data center growth and vehicle and building electrification, and a decrease in the number of people who plan to install behind-the-meter solar and storage units.

In the CPUC’s analysis, Diablo Canyon Power Plant (DCPP) was modeled as offline in all years, and all combined heat and power plants were kept online. While it is “likely that DCPP will be online through 2030 in reality,” the proposed decision says the CPUC’s model follows the requirements of California’s Senate Bill 846, which extended the operating life of the nuclear plant.

Energy storage resources can account for only up to 50% of the additional NQC amounts under the proposed decision.

The “real winner” of the procurement order is geothermal energy, Farhad Billimoria, representative of Aurora Energy Research, told RTO Insider. With offshore wind development in the state facing continued delays, community choice aggregators will again be forced to scramble for clean firm capacity, leaving geothermal as the only realistic, if still costly, option, Billimoria said.

Eversource Energy and National Grid introduced asset condition projects totaling about $110 million at the ISO-NE Planning Advisory Committee meeting Jan. 27.

The proposals coincide with ISO-NE’s ongoing efforts to establish an internal asset condition reviewer. This role is intended to increase transparency into the transmission owners’ asset condition spending, which has cost the region billions of dollars in recent years. (See ISO-NE Responds to Feedback on Asset Condition Reviewer Role.)

Eversource presented a group of asset condition projects that would replace structures on six transmission lines in New Hampshire. The combined estimated costs total $101.6 million, while the expected in-service dates range from the fourth quarter of 2026 to the third quarter of 2027.

In southern New Hampshire, Eversource proposes a $32 million project on Line 367. The company would replace 97 345-kV wood structures with an average age of 55 years, along with a seven-year-old steel structure with damage from bullet holes. The estimated per-structure cost is $330,000.

Eversource’s Steve Allen noted that the company estimates the typical useful life of 115- and 345-kV natural wood structures to be 40 to 60 years.

Fifty-seven of the structures on the line require immediate replacement, while Eversource also proposes to replace the 41 other original wood structures. Replacing all original wood structures would prevent the need for an additional project “in the near future,” Allen said.

On Line A126, a 115-kV line in western New Hampshire, Eversource proposes a $7.4 million project to replace 20 wood structures with an average age of 72 years. The estimated per-structure cost is $370,000.

In southeastern New Hampshire, the company proposes to spend $38.1 million to replace 96 structures on the 115-kV A152 line. Twenty-eight of the structures need immediate replacement, while 41 structures have engineering concerns, Allen said. The average age of the wood structures is 57 years, and the estimated per-structure cost is $397,000.

Eversource proposes a $5.6 million project on the 115-kV B143 line in southern New Hampshire. The project would replace 16 wood structures at an estimated per-structure cost of $351,000. The structure ages range from 48 to 59 years.

In eastern New Hampshire, Eversource proposes a $5.5 million project on the 115-kV K174 line to replace 15 wood structures with an average age of 58 years. The company considers four of the structures to be immediate replacement needs. The estimated per-structure replacement cost is $370,000.

In central New Hampshire, the company proposes a $12.5 million project on the 115-kV M127 line. The project would replace 39 wood structures, which have an average age of 58 years, at an estimated per-structure cost of $321,000.

Allen noted that the ISO-NE 2050 Transmission Study forecasts overloads on the A152 and K174 lines, though Eversource did not identify any project modifications to address these needs. ISO-NE plans to begin stakeholder discussions about right-sizing asset condition projects in the third quarter of this year.

Eversource also presented an update on asset condition projects at two river crossings affecting several lines in Connecticut. The modifications to the design have reduced the total estimated cost by about $5.5 million. The updated combined cost estimate now totals $101.3 million.

Rafael Panos of National Grid presented a $7.3 million asset condition project to replace a pair of 61-year-old circuit breakers at a substation in Brockton, Mass. The existing breakers are deteriorating and difficult to find parts for, Panos said. The project’s estimated in-service date is May 2027.

Asset Condition Interim Review

Also at the PAC meeting, Brent Oberlin, executive director of transmission planning at ISO-NE, discussed the RTO’s interim asset condition review process. ISO-NE is working to stand up the permanent reviewer at the beginning of 2027 and is relying on an external consultant to review nine selected projects during the interim period.

The list of nine projects in the interim review is mostly unchanged from the initial list ISO-NE presented in October, though the RTO has replaced National Grid’s proposed rebuild of Line 323 in eastern Massachusetts with a different project by the company in western Massachusetts expected to cost more than $200 million. ISO-NE made the change after an outage opportunity arose for National Grid to pursue the 323 project on an earlier timeline, Oberlin said. (See ISO-NE Gives Update on Asset Condition Reviewer Role.)

ISO-NE has initiated the interim review for several projects and expects about a three-month review process for most projects on the list, he said, adding that the RTO plans to eventually present results to the PAC and “will be looking to take lessons learned and feedback on the interim process to inform the development of the permanent [asset condition] reviewer role.”

Oberlin said additional asset condition projects that are proposed in 2026 but not on the interim list will not be subject to review. Jeff Iafrati, a consultant for Customized Energy Solutions, expressed concern that this could result in TOs advancing projects for the rest of the year to avoid review.

Alex Lawton of Advanced Energy United echoed this concern, saying, “It would be more assuring if there was a bit more review for upcoming projects.”

“While it’s a possibility, I really think it’s a limited risk,” Oberlin responded.

Since 2019, the Bonneville Power Administration, Pacific Northwest utilities, independent power producers and other interested parties have struggled with politically required, but operationally difficult, development of renewable/storage resources in the region.

While much of this struggle involved slower than expected generation interconnection and transmission access/construction by BPA, the dynamics behind such clean energy development are considerably more complicated. As a former BPA CEO with over 40 years of dealing with PNW energy issues, I thought a more comprehensive analysis of this situation might be helpful.

Background

In 2019 and 2021, Washington and Oregon set ambitious clean energy goals, requiring their utilities to achieve 80% clean/decarbonized energy portfolios by 2030. At that time, those states’ two main utilities, Puget Sound Energy (PSE) and Portland General Electric (PGE), were roughly 35 to 40% clean/decarbonized. Today they are only 45 to 50%. While such limited progress seems problematic, the nature of the non-ISO/RTO grid in the PNW and our specific transmission difficulties slowed renewable energy development substantially.

Geography

Northwest geography significantly complicates regional transmission development. Nearly all wind and solar sites are east of the Cascade Mountain Range, while loads are mostly in Seattle and Portland. In addition, current high-voltage cross-Cascades transmission lines are fully loaded. So devising methods to provide new transmission to PNW load centers or even upgrading existing 230-kV transmission to 500 kV across this environmentally sensitive barrier is a major challenge. I would estimate the degree of difficulty associated with overcoming this challenge, since it affects nearly all PNW renewables development, probably exceeds such geographic/environmental challenges in any other region.

BPA owns and operates roughly 70% of the region’s high voltage transmission. Despite this transmission position, it operates, not as an RTO/ISO, but under FERC’s Open Access Transmission Tariff (OATT) regime. It currently has 115 GW in its generation interconnection (GI) queue and, like RTOs/ISOs in other regions, is struggling to interconnect these resources as rapidly as possible.

Unlike those entities, however, as an OATT utility it also must operate a separate transmission access process complete with its own first-come, first-served queue for providing transmission capacity to renewable resource developers and others.

Randy Hardy

BPA typically processed this queue via an annual transmission cluster study that analyzed each submitted transmission service request (TSR) and thereby provided a specific plan of service for each such project. That CS queue has increased dramatically since 2020. Specifically: 2020 CS, 4 GW; 2021 CS, 6 GW; 2022 CS, 11 GW; 2023 CS, 17 GW; and 2025 CS, 65 GW.

This recent exponential growth in TSRs has stalled BPA’s ability to analyze the 65 GW in its 2025 CS because of the multiple years required to perform such complicated power flow analyses and because the amount far exceeds any credible projection (even with data centers) of future PNW load. As a result, any project in the 2025 CS probably will not receive any long-term firm (LTF) transmission until well after 2030.

BPA TSRs From 2020-2023

For TSRs submitted to BPA from 2020 to 2023, the situation is better but still challenging. As a result of these TSRs, BPA plans to significantly expand its transmission portfolio, primarily through upgrading cross-Cascade 230-kV transmission lines to 500 kV, plus adding series capacitors and reconductoring existing high-voltage transmission.

This program, labeled its Grid Expansion and Reinforcement Portfolio (GERP), will cost $5 billion according to BPA, although realistically closer to $10 billion given all the environmental and procurement cost escalation factors involved. However, given the permitting realities, BPA staffing shortages and GI/TSR processing challenges, most GERP transmission projects will not be energized until well after Washington/Oregon 2030 80% clean energy deadlines.

The relatively good news: when eventually energized, GERP projects probably will enable PSE and PGE to meet their 80% clean energy goals. In addition, BPA also has enabled 3 to 5 GW of clean energy projects to reach Portland and Seattle by repurposing existing LTF transmission freed up by retirement of Colstrip and other thermal resources.

Complicating Factors

Data Center Load Growth

Similar to electric utilities in other regions, PNW entities have experienced dramatic increases in projected loads driven by data centers and, to a lesser extent, electrification. From 2001 to 2022, annual PNW load growth equaled 1% or less. Loads from 2025 to 2034 now are estimated to grow by 2 to 3% annually.

Recent announcements of potential data center amounts/locations in the PNW total 12 to 15 GW by the mid-2030s mainly in Hillsboro (west of Portland), Salem or east of the Cascades (e.g. northeastern Oregon). Current data center load projections could easily be double or half of the 12- to 15-GW estimate.

In almost any case, they will increase regional loads substantially. This phenomenon dramatically increases the transmission capacity required to serve them, as well as the time needed to build such transmission and its cost. For example, over 3 GW of data center load is projected for Hillsboro (mostly in PGE’s service territory), but reaching this densely populated area involves multiple 230/500-kV upgrades by BPA and PGE and likely will cost $2 billion or more.

BPA Staffing

BPA experienced substantial staff reductions and associated turmoil resulting from the Trump/Musk actions in early 2025. While regional parties helped BPA avoid the worst of these, they still lost 200 of their 3,100 employees in February 2025 and, despite finally being exempted from the federal hiring freeze in November, have yet to even get back to their start of 2025 staffing levels. Then there’s the additional 400-plus staff they are projected to need (bringing total eventual staffing to roughly 3,500) to timely process all the GI/transmission access requests needed to meet reliability/clean energy requirements.

Both the data center boom and administration staffing restrictions came at the worst possible time, given BPA’s GI/TSR queues and unique transmission processing problems. Better late than never for DOE to exempt them from the federal hiring freeze, but the PNW effectively lost a year or more in its ability to identify and build the high voltage transmission necessary to meet PNW clean energy, reliability and data processing needs.

Conclusions

While well intended, Washington/Oregon goals of 80% clean/decarbonized energy by 2030 were set without consideration of the transmission access and construction realities BPA and other regional transmission providers would face.

Achieving such goals also was handicapped by emerging data center load growth and administration staff reductions on BPA.

Perhaps most significant, besides these transmission realities, the 80% by 2030 mandates set off a virtual gold rush of TSRs, resulting in the 65 GW in BPA’s 2025 CS queue that are not capable of being processed in any reasonable time frame — if at all.

Many of these outcomes could/should have been foreseen and planned for. Others represented unfortunate surprises that were unanticipated under reasonable assumptions.

The probable result: BPA/PNW will simply need to muddle through this mess over the next five to seven years. As mentioned before, GERP projects eventually will enable PNW utilities to reach 80%, but probably not until 2033 to 2035.

Even with these transmission realities now plainly visible, Washington and Oregon legislators have yet to deal with the affordability of these clean energy mandates. This is an emerging problem but no doubt will worsen significantly in the next five years. Given that both PGE and PSE are only at 45 to 50% clean/decarbonized now, reaching 80% (whenever that occurs) will involve substituting 1 GW or more of renewable energy for energy from existing thermal resources. Such substitution involves replacing current coal/natural gas generation, probably costing utility consumers $40 to $50/MWh, with wind/solar which nominally cost $50 to $60/MWh busbar. However, when you include balancing, load following, additional transmission costs and purchasing additional energy to serve load when the wind does not blow or the sun is not shining, increases delivered cost to utility customers by $25 to $30/MWh. Then this $80 to $85/MWh delivered cost energy could well increase by an additional $20 to $30/MWh when federal tax credits expire, raising the overall cost for renewables to reach the 80% goal past $100/MWh. While this problem is belatedly being recognized, it has yet to be dealt with in any meaningful way by either state legislature.

Lesson Learned

Beware of unintended consequences. As this article hopefully illustrates, they already have adversely impacted the timing and (potentially) the cost of achieving 80% by 2030, and, if further action is not taken, they will further frustrate achieving such goals in the next four to five years.

Industry watcher Randy Hardy was CEO of the Bonneville Power Administration from 1991 to 1997. Prior to that, he held a similar title at Seattle City Light.

AUSTIN, Texas — ERCOT stakeholders used their first Technical Advisory Committee meeting of 2026 to mark the committee’s 30 years of existence and achievements, sharing memories of their work together and recognizing members past and present.

“It has been an honor and privilege to serve on this committee and contribute to the greatest competitive retail and wholesale power market in the world,” Reliant Energy Retail Services’ Bill Barnes said during TAC’s Jan. 21 meeting.

The committee, composed of several subcommittees and working groups, recommends policies and procedures to ERCOT’s Board of Directors and is responsible for prioritizing projects through protocol revision requests, system change requests and guide revisions.

SPP staff went through their files and found the names of 64 members who have served at least five years on the committee. Mark Dreyfus, who represents the city of Eastland and other municipalities as part of TAC’s consumer segment, said he knew all the people on the list, calling some “giants of the industry.” He reserved singular praise for one past member: Reliant’s John Meyer.

“I hope there are statues to him in the office building,” Dreyfus said. “He led the stakeholders when we developed these processes and when we developed the original protocols, and he really deserves all our honor and recognition. If you don’t know him, it would be really good to talk to somebody and find out what he was about and why he took the time to create this process.”

American Electric Power’s Richard Ross, the only member with 25 years of service, said over the phone that TAC and ERCOT’s stakeholder process “really does cast a very big shadow.”

“It cast a shadow to the north and had a heavy influence on my experience with trying to get SPP’s stakeholder process set up in much the same way, with the way we so transparently change rules and give everyone a free opportunity to comment and debate,” Ross said. “If you ever looked at the process in SPP, you would see a great deal of similarities from things that we copied from.”

Barnes recalled the “completely ridiculous process” in the zonal market that predated the current nodal framework, where the zones’ boundaries would be redefined every year. He said “millions and millions of dollars amongst companies” would change hands.

“It was incredibly contentious and also extremely entertaining to be a part of,” he said. “One particular year … it literally moved a large coal plant from one zone to the other. I just remember Richard [Ross] playing a very critical part of the final vote, which I think it probably took three or four attempts to get through.”

Ironically, Ross gave up his seat this year and has been replaced by AEP’s Erin Rasmussen, one of three new TAC members.

“I’m watching from afar this year, but thank you for 25 years,” Ross said. “Keep up the good work.”

Engie’s Bob Helton, another TAC veteran, saw his 18 years of service elevated to 19 in real time when ERCOT staff found a Robert T. Helton mentioned in the files.

“This has to be wrong, okay? It can’t be. I’m not old enough to have done it,” Helton said. “I’ve served with pretty much everybody that’s on that list and I’ve served with a lot of very, very good people. We’ve made a lot of good decisions to make this market, as Bill said and it’s been noted, as the best in the country. We’ve gone through a lot of adversity. We’ve had some fun.”

Large Load Issues Pile Up

When TAC got down to the more mundane business at hand, ERCOT staff told members that the grid operator’s large load interconnection queue had dropped from 237.2 GW to 232.5 GW in January after several cancellations in December.

The great majority of requests (199.3 GW, or 85.7%) are for standalone facilities.

“We do expect that there may be some additional projects that are cancellations as well,” ERCOT’s Agee Springer said, noting that large loads do not need to explain why they are pulling projects from the queue.

The grid operator plans to introduce a quarterly stability assessment (QSA) for large loads in February to support those preparing to energize. It would be one of the first times ERCOT has published a structured QSA framework for tracking readiness and energization of large loads, according to consulting firm Electric Power Engineers.

“You need to pay attention to the QSA’s dates. [Large loads] are coming much faster than you think,” Longhorn Power’s Bob Wittmeyer, chair of the Large Load Working Group, told the committee.

ERCOT’s Jeff Billo told members that staff will reveal a draft framework of the proposed batch interconnection process for large loads during a Feb. 3 workshop. These large loads are currently studied individually, but under the batch process, they would be grouped and evaluated all at once. (See ERCOT Finds Stakeholder Support for Batch Process for Large Loads.)

Billo said ERCOT will likely request a good-cause exception from the Public Utility Commission after a recent rule change that requires large loads go through a full interconnection study similar to those generators undergo. Assuming the board approves the process, staff will have to file protocol changes to codify the batch studies.

“This is necessarily moving quickly because there are a lot of projects, a lot of these large load projects that are being developed,” he said. “The customers who are developing those want certainty as to how this is going to work, how this is going to impact their project, so we want to try to provide that.”

Smith, Henson to Lead TAC

Members re-elected Jupiter Power’s Caitlin Smith and Oncor’s Martha Henson as TAC’s chair and vice chair, respectively, for 2026. It will be Smith’s third year leading the committee.

“I’m planning on this being my last term,” she said.

Smith noted TAC’s accomplishments during the year, topped by getting the Real-time Co-optimization Battery (RTC+B) project’s last items “across the finish line” before it went live. She pointed also to stakeholders’ endorsement of ERCOT’s first 765-kV projects and growing TAC’s relationship with the board.

“We have done a lot … but we’re looking at a lot of work, namely [dispatchable reliability reserve service (DRRS)] and the load ride-through requirements we need to get done by the first half of the year. So, it’s not all fun and games, but [I’m] excited.”

Tier 1 Project on Combo Ballot

TAC’s unanimously approved combination ballot, or its consent agenda, included a $117.4 million transmission build that was reclassified as a Tier 1 project and needing board approval.

South Texas Electric Cooperative submitted the project, which will accommodate a 300-MW ammonia plant near Victoria on the Texas Gulf Coast, costing an estimated $65.5 million. ERCOT’s Regional Planning Group analyzed eight options and chose one of four short-listed alternatives, all with higher price tags.

Staff attributed the cost increase and reclassification to the higher 138-kV rebuild capability standard on AEP’s portion of the project. AEP’s Doug Evans said tariff rates on some steel and aluminum items increased between 15 and 50%, also increasing cost estimates.

The project is expected to be in service in June 2028.

NPRR1304: Incorporate the Other Binding Document “Procedure for Identifying Resource Nodes” into the protocols to standardize the approval process.

NPRR1305: Add the Other Binding Document “Counter-Party Credit Application Form” into the protocols to standardize the approval process.

NPRR1311: Correct an error in the real-time reliability deployment price adders’ calculation for ancillary services when ERCOT is directing firm load shed during a Level 3 energy emergency alert in the RTC+B’s protocols, ensuring final ancillary services prices cannot exceed $5,000/MWh.

PGRR127: Outline the additional generators that may be added to the planning models to address the generation shortfall introduced by the implementation of House Bill 5066’s requirements and increased load growth. The PGRR would also add a supplemental generation sensitivity analysis for Tier 1 Regional Planning Group project evaluations to minimize the effects of the additional generation on transmission project evaluations.

PGRR132: Clarify that new resources must interconnect to ERCOT through a new standard generation interconnection agreement.

NERC and other stakeholders have endorsed FERC’s proposal to introduce new standards to improve coordination between the electric and natural gas industries, with some commenters urging the commission to go further in support of grid reliability.

Commenters were responding to FERC’s Notice of Proposed Rulemaking from October 2025 that would incorporate the latest changes to Version 4.0 of the Standards for Business Practices of Interstate Natural Gas Pipelines adopted by the Wholesale Gas Quadrant of the North American Energy Standards Board (NAESB) (RM96-1). (See NOPR Would Get Pipelines to Offer More Information for Grid Operators.)

NAESB’s updates include a revised standard that creates a central location on pipeline websites for information on critical events that RTOs and ISOs can use to assess potential impacts to their systems. Two new standards would facilitate the posting of applicable scheduled quantity information for power plants that are directly connected to gas pipelines and support the inclusion of geographic information of affected areas, locations and/or pipeline facilities by a transportation service provider when issuing a critical notice.

In its comments, NERC called the commission’s proposal “critical for reliable operations of both [the] gas and electric systems, providing a common platform for operational data exchange and unified situational awareness.” Observing that “the electricity sector is the largest consumer of natural gas,” the ERO highlighted its own efforts to promote gas-electric coordination.

These include NERC’s Electricity-Natural Gas Work Plan, presented to the organization’s Board of Trustees in August 2025. As part of the plan, NERC has updated its Long-Term Reliability Assessments to include natural gas impacts on grid reliability and is “reviewing updates to its tool for Situational Awareness for FERC, NERC and the regional entities … to better integrate gas system data.”

NERC also mentioned several reliability standards intended to address natural gas fuel issues, including EOP-011-4 (Emergency operations) and TOP-002-5 (Operations planning), both approved by the commission in 2024, along with TPL-008-1 (Transmission system planning performance requirements for extreme temperature events), BAL-007-1 (Near-term energy reliability assessments) and EOP-012-3 (Extreme cold weather preparedness and operations).

Other electric stakeholders joined NERC to back the commission’s proposal. The ISO/RTO Council wrote that the NAESB standards would “provide more timely and actionable information about gas system constraints and disruptions that may impact electric system reliability” while enabling “more effective coordination of operational decisions across the gas-electric systems.”

National Grid, Consolidated Edison, Old Dominion Electric Cooperative and Washington Gas Light — filing jointly as the Utility Coalition — called NAESB’s standards “a meaningful advancement toward enhancing real-time operational transparency across” the gas and electric systems. But the utilities also suggested the commission “widen its aperture to … consider steps that can be taken to preserve and enhance interstate pipeline service reliability.”

These suggested steps include requiring annual reports from interstate pipelines on reliability metrics, revising its pipeline force majeure policy and reservation charge crediting policy to create reliability incentives for pipelines, and implementing “greater standardization of pipeline scheduling and confirmation practices.” The coalition added that the commission could direct additional modifications to NAESB’s standards to address pipeline reliability.

The American Gas Association also expressed support for adopting the NAESB standards, which it said would “promote greater gas-electric coordination and situational awareness during severe weather events.” AGA suggested possible future steps to further improve communication between the gas and electric industries, including updating the force majeure provisions, as the Utility Coalition said, and promoting investment in gas storage and demand response programs.

Finally, the Interstate Natural Gas Association of America endorsed adoption of the NAESB standards but requested the commission ensure its final rule in the proceeding is timed so the effective date of the modifications “does not occur during the winter heating period.” The association also asked that pipelines be allowed “the flexibility to implement the modifications on or before 180 days from the date compliance filings are due in this proceeding.”

As extreme winter weather descended on the Eastern U.S. and Canada, Hydro-Québec suspended power exports to ISO-NE on the New England Clean Energy Connect (NECEC) transmission line because of reliability concerns in Québec starting on the afternoon of Jan. 24.

The suspension continued throughout tight system conditions across the Northeast on Jan. 25 and into Jan. 26, with deliveries resuming late that evening.

“The polar vortex has brought extreme and sustained cold air across Québec,” Serge Abergel, chief operating officer for Hydro-Québec Energy Services, said in a statement. “The demand for power in Québec caused us to suspend deliveries over the New England Clean Energy Connect from Saturday afternoon until the present (with partial deliveries occurring between 1 p.m. and 3 p.m. on Sunday).”

He said Hydro-Québec expects deliveries to resume early Jan. 27, but he noted that “there could be yet further interruptions at peak hours over the next several days.”

According to ISO-NE data, NECEC deliveries dropped from about 1,100 MW to zero over a half-hour period midafternoon Jan. 24. Hydro-Québec sent power over the line for about two hours on the following day, sending up to about 600 MW before again cutting deliveries.

The loss of supply from the NECEC line appears to have significantly affected real-time energy prices: The ISO-NE real-time Hub LMP more than doubled during the 40-minute period NECEC cut supply Jan. 24, while the brief burst of supply Jan. 25 coincided with about a 33% decline in the hourly real-time LMP despite relatively steady demand.

Amid high prices in New England, ISO-NE has consistently been exporting power to Québec over the Phase 2 transmission line since the afternoon of Jan. 24, including about 830 MW during that day’s evening peak.

The NECEC line began commercial operations Jan. 16. (See NECEC Transmission Line Ready to Begin Commercial Operations.) The project includes supply contracts between Hydro-Québec and Massachusetts electric utilities requiring the company to send firm power to ISO-NE. The company does not have new capacity supply obligations associated with the line.

Hydro-Québec could face significant penalties for falling to meet the delivery requirements of the contracts. According to the power purchase agreement, supply interruptions that are not the result of a force majeure or a physical outage on the line can be cured by the additional deliveries within the same year or following year. Delivery shortfall during peak hours can only be cured during peak hours, and delivery shortfall in the winter can only be cured in the winter (D.P.U. 18-64, et al.).

“We are aware of the historic constraints on the Canadian grid due to the extreme cold,” said Maria Hardiman, a spokesperson from the Massachusetts Executive Office of Energy and Environmental Affairs.

“Hydro-Quebec is facing steep penalties for each day they are not providing power to Massachusetts, and we know they are working to resume power as quickly as possible,” Hardiman said. “Our contract ensures that ratepayers will still see lower-priced electricity, regardless of the power flowing over the line.”

Robert McCullough, principal of McCullough Research, said the suspension on the NECEC line appears to be a product of Hydro-Québec’s slim reserve margin for the current winter. According to the Northeast Power Coordinating Council’s 2025/26 winter reliability assessment, Québec had about a 1% reserve margin. Hydro-Québec’s peak load exceeded its 50/50 winter forecast by over 200 MW on Jan. 25.

McCullough attributed the slim reserve margin to “combination of bad weather, neighbors not able to help and insufficient maintenance on some of the dams.” NPCC’s report notes that Hydro-Québec’s available winter capacity was reduced by 5,594 MW because of maintenance and derates.

Abergel called the contention of insufficient maintenance “simply not accurate.”

In New England, ISO-NE peak load reached 20,182 MW on the evening of Jan. 25, slightly exceeding the region’s 90/10 winter forecast. Hourly Hub LMPs have reached as high as $777 $/MWh.

The RTO has avoided the need to take emergency actions throughout the weather event. It issued a precautionary alert on the morning of Jan. 25 and obtained a waiver from the U.S. Department of Energy allowing generators to override air permit limits to provide extra power.

Dan Dolan, president of the New England Power Generators Association, said the ISO-NE fleet “has performed exceptionally well this weekend using every different fuel and technology to maintain reliable, stable operations through arctic temperatures, heavy snowfall and even needing to send power to support our neighbors in Quebec.”

He highlighted the significant role oil generation has played in maintaining grid reliability. With gas generation limited because of high demand for heating, oil generation has consistently accounted for roughly a third of generation in the region since the suspension of deliveries on the NECEC line.

“Part of the diverse generation mix in New England is a large capability to use oil in periods of stress,” he said. “That has happened at a tremendous scale, which creates strain on fuel infrastructure. But the system is holding up through this first stretch.”

With more cold weather in the forecast over the next few days, “it is all hands on deck,” Dolan said.

The PJM Markets and Reliability Committee and Members Committee endorsed the RTO’s recommended installed reserve margin (IRM) and forecast pool requirement (FPR) for the third 2026/27 Incremental Auction (IA), scheduled to be conducted Feb. 24.

The vote is advisory to the Board of Managers, which determines the values to be used in the auction.

The IRM would fall from the 19.1% used in the 2026/27 Base Residual Auction to 18.6%, while the FPR would increase from 0.9170 to 0.9291. (See “Stakeholders Endorse IRM and FPR for 2026/27 Capacity Auction,” PJM MRC/MC Briefs: March 19, 2025.)

The inputs for the parameters were based on the 2026 load forecast, which predicted lower load in the long term and shifted the concentration of reliability risk toward the summer, though the majority still lies in the winter at a 55.9% loss-of-load expectation. (See Pessimistic PJM Slightly Decreases Load Forecast.)

Most resource classes would see a modest increase in their effective load-carrying capability (ELCC) ratings, with four-hour storage resources seeing the largest benefit, going from 50 to 54%. Owing to its stronger winter performance, offshore wind generation would see a decrease from 69 to 64% and onshore wind from 41 to 38%.

Paul Sotkiewicz, president of E-Cubed Policy Associates, said the influence load has on the amount of supply that resources can offer creates a dynamic that runs contrary to economic logic. The volatility of class ratings undermines the ability for investors to make sound decisions, particularly because the control they have over their assets’ ratings is limited. Pointing to the contributions solar made in maintaining reliability during the heat waves of summer 2025, he argued ELCC is making the RTO look shorter than it is.

“This calls into question the validity of PJM’s ELCC model because if we see load decreases continue in the future … as the load increases, capacity accreditation falls and the IRM goes up,” he said.

PJM’s Patricio Rocha Garrido said the relationship between load uncertainty and the IRM has always been present, including under the previous PRISM modeling software.

“What we’re trying to do here is determine what are the risk hours” and determine resource performance at those times, he said, adding that was also the goal under the equivalent forced outage rate demand (EFORd) accreditation paradigm.

Gregory Poulos, executive director of the Consumer Advocates of the PJM States, said several consumer advocates will abstain from votes on the IRM and FPR values because it seems stakeholders have little sway on the values the RTO is proposing. He said staff put in good work developing the values, but if it’s going to be more than a check-the-box exercise for stakeholders, there needs to be more of a process around how the numbers are produced and presented.

Responding to stakeholder questions on what the vote means to the board, PJM Senior Vice President of Market Services Adam Keech said he views the vote as pertaining to whether staff followed the process for determining the IRM and FPR values. If stakeholders feel those processes should be revised, that should be pursued through a separate process.

PJM’s Suzanne Coyne presented the RTO’s Markets and Reliability Committee with revisions to Manual 28: Operating Agreement Accounting to clarify how resources are defined as offline for the purpose of determining whether they are eligible for lost opportunity cost (LOC) credits. (See “Stakeholders Endorse Quick Fix on Offline Resource LOC Eligibility,” PJM MIC Briefs: Jan. 7, 2026.)

Coyne said that while the governing documents state that resources that are offline when committed for secondary reserves are not eligible for LOC credits, the manual language can result in resources improperly being considered online if they begin operations between when they are dispatched and when the commitment begins.

The market clearing software has visibility into whether a resource is offline when it assigns a commitment; however, the settlement calculations consider only whether a unit is online when the commitment interval begins 10 minutes later.

The proposal would use real-time security-constrained economic dispatch data to determine whether a resource is online, unifying the discrepancy between dispatch and settlement, she said. If endorsed by the MRC in February, the language would be implemented March 1.

Must-offer Requirement for Self-Scheduling Resources

Mike Cocco, of Old Dominion Electric Cooperative (ODEC), presented a quick-fix proposal to define a capacity resource as having met its obligation to offer into the energy market if it self-schedules and provides its full output.

The quick-fix process allows a problem statement and issue charge to be brought concurrently with a proposed solution.

Cocco said the proposal would ensure that gas generation resources that self-schedule to ensure they are able to operate and consume fuel procured on ratable take contracts are not at risk of non-performance penalties if there is a performance assessment interval (PAI). Cocco said that all the parties he has reached out to, including PJM and the Independent Market Monitor, have said they interpret Manual 11: Energy & Ancillary Services Market Operations as already providing that protection, but he said ODEC believes that should be codified in the language.

PJM Senior Vice President of Market Services Adam Keech said the parameter-limited schedule (PLS) process is intended to cover these circumstances and questioned whether the proposal is meant to complement or replace that. When a resource owner seeks a PLS exception, it must meet a higher burden of proof that it has diminished flexibility because of the ratable take.

Cocco responded that the proposal as envisioned would not require generation owners to obtain PLS exceptions, but he wanted to consider the comment further and would reach out to PJM staff to discuss.

The proposal would revise the tariff to double the tangible net worth requirement to $2 million for those participating in financial transmission rights markets. For entities not participating in FTR markets, there would be a transition period in which the requirement would first increase from the current $500,000 to $1 million and then increase by $200,000 annually over five years. The proposal also adds a 3% fixed annual escalator.

The proposal would not change the alternative tangible asset threshold of $10 million for FTR participants and $5 million for non-FTR participants.

Consumer Advocates Form Residential Affordability User Group

New Jersey Division of Rate Counsel Director Brian Lipman announced the creation of an Affordability and Reliability for Residential Consumers User Group intended to reduce the impact on ratepayers of accelerating load growth from data centers.

Along with his agency, Lipman said the user group includes the Delaware Division of the Public Advocate, D.C. Office of the People’s Counsel, Illinois Citizens Utility Board, Maryland Office of People’s Counsel, Office of the Ohio Consumers’ Counsel and the Pennsylvania Office of Consumer Advocate.

Lipman said the group’s first meeting on Jan. 27 will include voting on the draft charter and the concept of revising governing documents to include affordability in PJM’s mission statement and Operating Agreement.

Vitol’s Jason Barker said he appreciated the goal of the user group, and while his company has no position on whether it should be formed, he objected to the announcement stating that consumer advocates only have 1% of the voting power in lower standing committees.

Barker said that when sector-weighted voting is accounted for in the MRC and MC, consumer advocates can have the power to sway votes. He pointed to the Critical Issue Fast Path process conducted in 2025 on large load growth, in which 10 consumer advocates cast votes that accounted for half the end-use customer sector, meaning those offices held 10% of the sector-weighted vote.

The 1% figure references the diluted voting power consumer advocates hold outside the MRC and MC, where each of PJM’s 1,111 members can cast votes.

Barker said it is typical for only about 10% of those members to vote in the lower committees.

PJM stakeholders Jan. 22 kicked off discussions on creating a “backstop” auction to be held in September at the insistence of the Trump administration and the governors of the RTO’s 13 states.

The Members Committee discussed the feasibility of holding such an auction and how the logistics of creating the rules for doing so should be balanced with other elements of the Critical Issue Fast Path (CIFP) proposal the Board of Managers selected for addressing large load growth Jan. 16.

The White House’s National Energy Dominance Council (NEDC) and state governors, issued the same day as the board announced its choice, envisions a one-time auction that procures new resources for a 15-year commitment period. (See White House and PJM Governors Call for Backstop Capacity Auction.)

“The PJM board should file tariff revisions expeditiously, as PJM has already received stakeholder input through the 2025 [CIFP] process, and no further CIFP processes are necessary,” they said in a statement of principles.

In its announcement of its CIFP proposal choice, the board said the RTO’s existing backstop capacity procurement method should be accelerated: It is currently triggered only after three consecutive capacity auctions fall short of the reliability requirement. (See PJM Board of Managers Selects CIFP Proposal to Address Large Load Growth.)

“Accelerating a backstop capacity procurement is especially necessary in light of FERC’s recent decision on co-location and its request for more information on utilization of this backstop procurement framework,” it said in a letter to stakeholders.

Addressing the MC on Jan. 22, board Chair and interim CEO David Mills said both the government’s and the board’s proposals don’t bear any resemblance to the existing backstop. PJM’s load forecast shows data center demand is likely to rise for a significant amount of time. “A one-time auction is not going to scratch the itch completely,” he said.

Designing an auction able to provide certainty for the supply and demand side of the auction on that timeline will require the states and FERC to be involved and take ownership over the outcome, Mills said. What can’t be allowed to happen is for there to be extended fruitful discussions only for an uninvolved party to fire a flare in the final hours, he said.

Even with a backstop auction, Mills said there are significant barriers to getting new resources built, including transmission upgrades, financing, tariffs, siting, permitting and supply chain constraints. Significant new capacity is unlikely to be available until 2032.

Manager Vickie VanZandt said the challenges of siting transmission could impede any resource adequacy benefits a backstop auction might provide. States and transmission owners will have to work together to overcome the likelihood of immense public pushback against network upgrades required to make new resources procured through a backstop deliverable.

Pennsylvania Deputy Secretary of Policy Jacob Finkel said he could not underscore the gravity of a bipartisan group of 13 governors and the White House calling on PJM to conduct the auction. He pushed back against suggestions that the September deadline was meant to be before the midterm elections in November, saying nine months seemed to be workable.

“We want this RTO to work; we want to solve this problem, but changes have to occur,” he said.

Constellation Energy Vice President of Wholesale Market Development Adrien Ford said the feasibility of holding a backstop auction in September depends on the design PJM decides to adopt and whether it tries to build off the existing capacity product or define a new one.

She said Constellation has been working with Vistra to revise the backstop mechanism that a coalition of resource owners and data center developers proposed during the CIFP process that would build off the existing definition of capacity, triggering if a capacity auction cleared below 98% of the reliability requirement and allowing for up to seven-year commitments. The auction would be open to new or reactivated resources; existing resources with offers higher than the maximum price for the Base Residual Auction that cleared short; and traditional demand response. (See “Joint Stakeholder Proposal,” PJM Stakeholders to Vote on Large Load CIFP Proposals.)

Mills said his vision of success is a ready-to-launch mechanism that accomplishes what PJM has been asked to do: Establish a market mechanism that marries new committed demand to new supply. To get to that point, stakeholders will need to chew through a lot of details, but he said that’s within their capability. He said he believes that in four to six weeks, there will be great progress on creating a workable design.

Unintended Consequences

Mills also called for stakeholders to identify areas where unintended consequences could be created by running auctions to procure capacity outside BRAs. One such challenge could be the creation of an additional cycle of grid upgrades being triggered.

The PJM Public Power Coalition’s Carl Johnson warned that a parallel capacity auction with the potential to deliver higher value for sellers could cannibalize projects already in the interconnection queue. If a substantial number of planned resources that PJM expected to come online and offer into the Reliability Pricing Model instead seek to participate in a backstop auction, there would be no net change in the amount of supply available to the grid, and the market would be even more short.

The Natural Resources Defense Council’s Claire Lang-Ree said the success of the backstop auction relies on the other components of the board’s CIFP proposal. If the bring your own new generation (BYONG) and “Connect and Manage” DR pathways for data centers aren’t strong enough, she said it would be hard to see why they would want to participate in a potentially more expensive backstop auction.

The BYONG model would allow large loads to meet their own capacity needs with new resources, which would qualify for an expedited interconnection track. Large loads that do not participate in BYONG would be subject to curtailment through load-serving entities ahead of pre-emergency load management resources in a model similar to PJM’s proposed mandatory non-capacity backed load (NCBL) brought during CIFP — though the load would remain in the capacity market. (See PJM Revises Non-capacity Backed Load Proposal.)

Mills said those changes are another area that will require buy-in from states to be successful: Because PJM cannot distinguish between consumers directly, it will be up to state utility commissions and utilities to disentangle large loads from organic economic growth.

Greg Poulos, executive director of the Consumer Advocates of the PJM States (CAPS), said he is concerned an auction awarding multiyear commitments would shift risk onto consumers.

Consumer advocates and representatives of Pennsylvania Gov. Josh Shapiro’s office urged PJM to extend the price collar that limited capacity prices to between $175 and $325/MW-day for the 2026/27 and 2027/28 auctions. Finkel said the 2028/29 BRA is not going to be able to procure enough supply and will clear at the $550/MW-day maximum price, a jump in prices he argued would not come with any reliability benefit. (See FERC Approves PJM-Pa. Agreement on Capacity Price Cap, Floor.)

Paul Sotkiewicz, president of E-Cubed Policy Associates, said constraining capacity prices would ensure that a parallel backstop auction would cannibalize resources from RPM.

The winter storm that moved through Texas and much of the Eastern Interconnection over the Jan. 24-25 weekend cut power to hundreds of thousands of people and stressed the bulk power system, but it did not create major disruptions like storms earlier in this decade.

The storm dumped snow, sleet and freezing rain across its path, with the most power outages occurring on its southern edge — especially in the lower Mississippi Valley, according to the National Weather Service. Entergy Louisiana said Jan. 26 that most customers who lost power in its territory would be restored by Jan. 28, with some repairs taking a day longer.

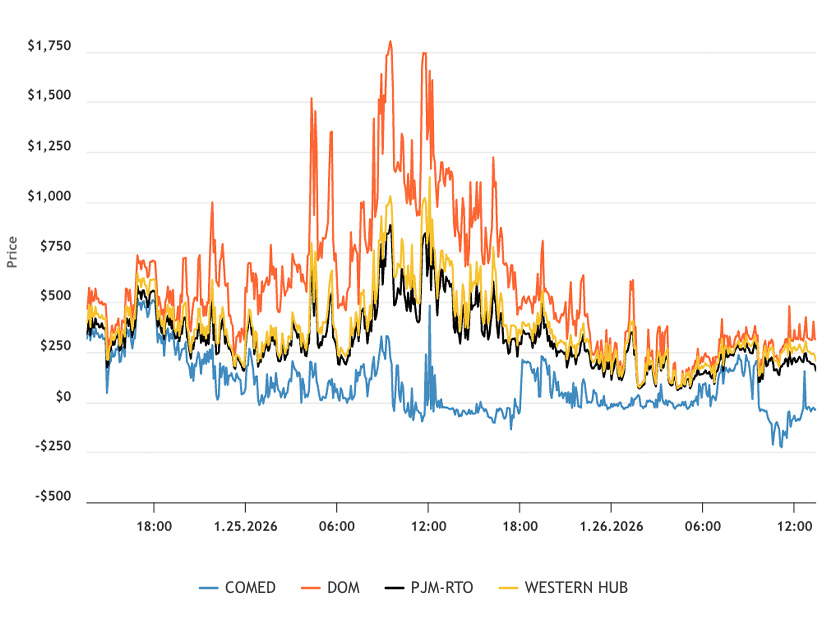

NYISO wholesale power prices briefly hit quadruple digits at about 11 p.m. ET Jan. 25 (Sunday), while the Dominion Zone in PJM saw prices above $1,000/MWh for much of the day.

PJM is actually expecting higher demand Jan. 27, with lower temperatures prompting it to issue a maximum generation alert and a low voltage alert. The RTO could break its winter peak record that day, as it forecasts peak demand of 147.2 GW, which would beat the mark of 143.7 GW set a year ago.

The RTO said that it could see peak demand hit 130 GW for seven straight days, which would be a first for winter.

“This is a formidable arctic cold front coming our way, and it will impact our neighboring systems as much as it affects PJM,” Senior Vice President of Operations Mike Bryson said in a statement. “We will be relying on our generation fleet to perform as well as they did during last year’s record winter peak.”

PJM asked DOE to issue a 202(c) order to allow it to dispatch every generator in its footprint at is maximum level without violating air quality laws — an order that remains in place through the end of January.

DOE issued a similar order to ISO-NE as New England deals with the same cold. One generator informed ISO-NE that it was running up against its permitted emission limits.

“This prolonged severe cold weather event is expected to result in a sustained high level of demand for electricity,” ISO-NE told DOE in its order application. “While the vast majority of generating units in the ISO-NE region continue to function adequately, some units may experience difficulty due to emissions/air permitting limitations or other operating constraints.”

A graph from PJM’s Data Viewer showing real time prices by different zones as the storm passed through its territory. Dominion saw the highest prices. | PJM

NYISO is facing the same winter weather as its two neighbors, announcing last week that it could see peak demand exceed 24 GW, which was near expectations for this winter, but falls short of its all-time winter peak of 25.7 GW set in 2014.

“Our assessment finds there are adequate resources to serve demand on the grid under forecast conditions, but we’ve also seen generators in recent winters challenged with accessing adequate fuel capacity during very cold conditions,” NYISO Vice President of Operations Aaron Markham said in a statement.

MISO also issued a cold weather alert that remains in place through the end of January as low temperatures impact its footprint. It also issued a conservative operations declaration covering the cold snap.

MISO saw prices peak at about $1,802/MWh on Jan. 23, although they averaged just $178.04 across its entire footprint, while prices were slightly lower by Jan. 25.

SPP Back to Normal Conditions

SPP had returned to normal operating conditions as of 12 p.m. CT Jan. 26, after expiration of conservative operations and resource advisories that were in effect during the storm. However, it extended its weather advisory — considered normal operations — through noon Jan. 28 to maintain awareness of potential weather-related effects on system resources.

A spokesperson said the RTO had sufficient generation and met reserve obligations in its 14-state footprint during the storm, with load reaching about 46 GW during the morning peak Jan. 26. Load is forecasted to remain in the mid-40-GW range through the remainder of the week. SPP’s winter peak record of 48.1 GW was set in February 2025.

“We did not experience any major transmission losses, but we did get reports of local outages, particularly in the southern portion of our footprint,” SPP’s Derek Wingfield said.

He said the grid operator remained in close coordination with neighboring systems throughout the event, providing energy exports as needed and as available generating capacity allowed.

“We will continue to monitor conditions closely and will issue additional advisories as necessary,” Wingfield said.

Stronger ERCOT Grid Performs

The ERCOT grid breezed through the storm, a marked contrast to the dayslong outages during the disastrous Winter Storm Uri of February 2021. Since then, winterization has become mandatory for power plants and critical natural gas infrastructure. ERCOT has also added about 40 GW of capacity since the 2021 storm to bulk up its energy supplies.

About 90% of the new generation added since 2021 has been wind, solar and battery storage. Batteries provided more than 7 GW of energy at 8 a.m. CT Jan. 26. ERCOT’s instant storage discharge record stands at 9.7 GW, set in December 2025.

Natural gas provided more than 50.8 GW of energy at one point Jan. 26, another record, according to Grid Status.

This comes after DOE granted ERCOT’s request for an emergency order under the FPA because of the storm. The order allows certain electric generating units to operate up to their maximum generation output in certain limited circumstances, despite federal or state environmental standards and requirements.

The order is effective until 11:59 p.m. Jan. 27.

Early demand projections of 83 GW failed to materialize. Demand is now expected to peak at around 78 GW on Jan. 27.

ERCOT did declare a transmission emergency late Jan. 25 because of the loss of generation and transmission-line issues in the San Antonio and Houston areas. The emergency was canceled during the morning hours Jan. 26.

ISO staff have also canceled the operating condition notice (OCN) issued ahead of the approaching cold weather system. OCNs are the first of ERCOT’s “four levels of communication issued in anticipation of a possible emergency condition” and are issued when the system’s safety or reliability is compromised or threatened.

More than 61,000 Texas customers were out of power as of noon Jan. 26, primarily in the northeastern region of the state where American Electric Power subsidiary Southwestern Electric Power Co. and Entergy Texas operate.