IESO has refined how it will work with the Ontario Energy Board (OEB) on the construction of a third transmission line into Toronto and broadened rules for prospective bidders to demonstrate their experience.

ISO officials disclosed the changes in an engagement session April 9, saying they were developed in response to stakeholder feedback on the estimated $1.5 billion HVDC line under Lake Ontario, the first transmission project IESO will award under competition.

Officials say the 65-km, 900-MW Toronto Third Line (TTL) is needed to meet a potential doubling of Toronto’s electricity demand by 2050.

Andrew Lee, an adviser for IESO’s resource acquisition, transmission development and procurement unit, announced version two of the Transmitter Selection Framework registry rules, published March 18. The revised rules are intended to provide “greater flexibility and additional clarity for prospective applicants,” while ensuring those seeking to participate “have demonstrated a baseline level of experience and competency,” Lee said.

The registry window will be open until about 60 days prior to anticipated launch of the procurement, currently set for Q1 2027.

The new rules will allow an applicant to cite more than one designated affiliate to demonstrate its organizational experience.

“That change was made in response to feedback and reflection on how corporate groups are often structured in practice,” Lee said. “In some cases, relevant experience may sit across multiple affiliate entities rather than neatly within a single one. Allowing reliance on more than one designated affiliate introduces flexibility and better reflects those realities.”

Limited HVDC Experience

Stephen Lachan, a supervisor for resource acquisition, transmission development and procurement, said the ISO will be flexible in evaluating the experience of prospective bidders, noting there are “only a handful of [HVDC] projects in North America.”

“The types of qualifying projects that we could consider include … an underwater HVDC transmission, underwater transmission in general [including AC lines], underwater linear infrastructure [such as] telephone cables or pipelines, or overland HVDC cables,” he said.

“The ISO is still considering the balance between stringent qualifying project requirements and increased market participation, and this is where we’re seeking feedback from you all today,” he added.

Pattern Energy’s Frank Davis questioned whether the ISO’s requirement that bidders demonstrate their capacity by having at least two “directors/officers with [qualifying project] experience” will be “definitive.”

“I believe in prior procurements … there was a bit of a wider net cast, like language like ‘managerial authority,’ as opposed to specific roles,” Davis said.

Past procurements required that the director/officer can bind the proponent organization, Lachan said.

“Much what we’re putting out today is … our initial proposal,” he said. “So, we do welcome feedback, and if there [are] distinctions that you think we should take into consideration as it relates to how we characterize a director officer within a proponent entity, I think we’re happy to take that on.”

IESO, OEB Roles

Nicole Kosonen, supervisor of resource acquisition, transmission development and procurement, said the ISO has dropped its initial model, in which the winning bidder would have received a contract covering all costs of financing, designing, building, operating and maintaining the line for the first 10 years of commercial operation. In year 11, the contract would have transitioned to traditional rate regulation under the OEB, which would approve annual revenue requirements for continued operation. (See IESO Removes Credit Requirement for Transmission Registry.)

Instead, Kosonen said IESO will select the bidder and approve its capital cost requirements, then turn the rate regulation over to the OEB when the design and build phase is complete. OEB will oversee the operational phase and approve costs related to operation, maintenance and sustaining capital.

“The benefit of this approach is that it enables the ISO to have oversight over the entirety of the capital costs, reducing the risk of shifting costs between the [ISO] contract and the OEB. The boundaries of the ISO contract and the OEB oversight are relatively straightforward, which will minimize implementation challenges,” Kosonen said.

“The actual determination of rates and payments to the transmitter will be determined by the OEB through their rate setting,” she added. “No contractual payments will be made from the ISO to the transmitter, and the transmitter will not start receiving payments until the line is in operation.”

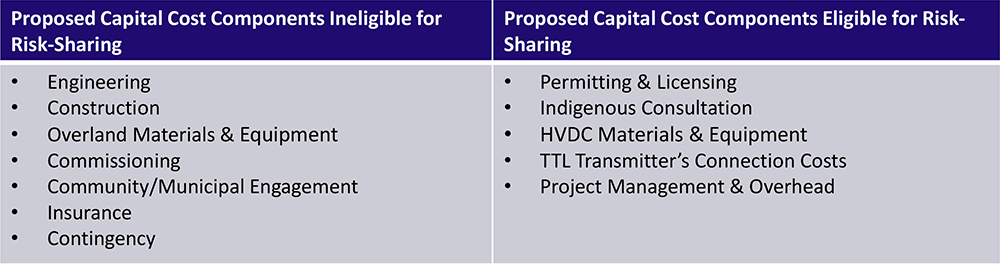

Ceiling Price vs. Target Price

To control costs, IESO is considering allowing bidders to propose a ceiling price, with any costs above the ceiling borne by the transmission company. It is also considering allowing developers to propose a target price for certain capital cost components, such as permitting and licensing, HVDC materials and equipment and connection costs. “If the transmitter is able to perform the scope of the activity governed by that target price for less than the contracted amount, then the difference is shared” between the developer and ratepayers, Kosonen explained.

‘Bankability’ Question

Adam Butterfield, Mott MacDonald’s practice leader for energy infrastructure in Canada, questioned whether the TTL project would be “bankable.”

“The linear infrastructure procurement world has kind of moved away from all-in fixed price [contracts] and is kind of looking more toward alliance or progressive design builds, where bidders put in their costs for the known amounts … and then once the development phase is completed and costs are a little bit more known, then there’s a negotiation on the actual construction cost.”

“I just worry that at the early stage you’re going to market with this, that bids are going to be based off wildly different assumptions,” he continued. “For example, no one knows what the subsurface conditions are along the route. So, you don’t even know how long your cable is going to be. We don’t even know where it’s going to tie in to the converter stations on either end. So, unless you provide a strawman for bidders to bid on, it’s going to be garbage in, garbage out. Everyone will put in a total bid price, but they’ll be vastly different, because [there] are just too many unknowns at this stage.”

Lachan said although the ISO is proposing to have all the capital costs subject to the IESO contract “that does not mean that we are suggesting that all of the capital costs … would be fixed. We are seeking to get a better understanding of which of the cost categories for this type of project need to have some sort of reasonable change provisions.”

Leave to Construct, ‘Engagement Fatigue’

Lachan said the ISO is considering whether the OEB’s “leave to construct” process — in which the regulator determines whether a project is in the public interest — is appropriate for the TTL project, “understanding that the ISO will be doing a competitive procurement where … a lot of the aspects of the regulatory review associated with the LTC will be captured.”

Denise Zhong, senior manager of transmission development and procurement, said the ISO has developed a digital guide to help municipal officials in the path of the TTL learn the basics of transmission and procurement concepts.

“I want to acknowledge … that ‘engagement fatigue’ is real,” she said. “Many communities and stakeholders are being asked to participate on multiple initiatives at the same time, often on complex technical topics. On top of that, the electricity sector itself can be difficult to navigate at times, particularly for those that are newer to transmission or competitive procurement processes. The intent is to support meaningful participation … without requiring people to become subject matter experts overnight.”

Next Steps

The IESO asked for the next round of written feedback by April 23 at engagement@ieso.ca. It said it will hold the next engagement session in May or June on refined procurement and contract concepts and documents.