The U.S. Department of Energy has awarded $800 million to the Tennessee Valley Authority and Holtec Government Services to support construction of what may be the country’s first advanced small modular reactors.

DOE said Dec. 2 that the cost-shared funding is part of President Donald Trump’s energy dominance agenda, which includes a nuclear renaissance.

Both funding awards are $400 million and center on Gen III+ light-water SMRs.

TVA plans to place a GE Vernova Hitachi BWRX-300 at its Clinch River site in Tennessee and accelerate the deployment of other such units in cooperation with Indiana Michigan Power and Elementl Power. (See TVA First U.S. Utility to Request SMR Construction Permit.)

Holtec, which is shaping itself as a one-stop shop for SMR development — technology developer and vendor, supply chain vendor, and plant constructor — plans to deploy two of its SMRs beside the formerly retired Palisades Nuclear Generating Station, which it is preparing to restart.

The two awards constitute the bulk of the $900 million solicitation DOE issued in March to help early movers in the SMR sector reduce risks. The remaining $100 million will be awarded later this year, DOE said.

“Advanced light-water SMRs will give our nation the reliable, round-the-clock power we need to fuel the president’s manufacturing boom, support data centers and AI growth, and reinforce a stronger, more secure electric grid,” Energy Secretary Chris Wright said. “These awards ensure we can deploy these reactors as soon as possible.”

Holtec said the first-mover award would catalyze the first-of-a-kind deployment of its proprietary SMR-300, which it calls Pioneer 1 and 2. This supports its effort to build a repeatable, standardized, fleet-scale model, which was a core requirement of the DOE funding offer.

“We are energized by DOE’s confidence in our SMR-300 reactor, which we view as validation of our 14-year quest to develop a walk-away-safe and cost-competitive nuclear reactor,” Holtec International CEO Kris Singh said.

Similarly, TVA said the Clinch River project would serve as a national model for how to deploy SMRs safely, efficiently and affordably.

“With DOE’s support and the strength of our partners, we’re accelerating the deployment of next-generation nuclear — reducing financial risk to consumers and strengthening U.S. energy security,” CEO Don Moul said. “This is how we deliver reliable, affordable energy and real opportunity for American families.”

GE Vernova Hitachi Nuclear Energy is part of the coalition TVA put together to apply for the DOE funding. GE Vernova CEO Scott Strazik said in a news release: “The BWRX-300 is the only commercial SMR technology being built right now in the Western world, and this grant will accelerate its deployment in the U.S.”

Earlier in 2025, Ontario Power Generation broke ground on a BWRX-300 facility that eventually is expected to house four SMRs.

Electricity sector participants urged Congress to back cyber security programs as the House Committee on Energy and Commerce’s Subcommittee on Energy heard testimony on the efforts of nation-states and other actors to hack the bulk power system.

The Electricity Information Sharing and Analysis Center (E-ISAC) is the industry’s clearinghouse for information on cyber and physical threats that works with government and other sectors to reduce security risks, NERC Senior Vice President and E-ISAC CEO Michael Ball said at the Dec. 2 hearing.

“The threat landscape is complex,” Ball said. “It includes continuously evolving threats from sophisticated and very capable adversaries; among the most advanced are nation-states … which are very well-funded.”

Ball said “numerous public reports underscore how these adversaries focus on the electric sector” and cited China, Russia, Iran and North Korea as being “monitored closely.”

Chinese cyber threats have dominated risks to North America recently, as Russia and Iran are more focused on conflicts in their regions, Ball said in his written testimony. He said Salt Typhoon and other hacking groups to which attacks have been attributed are believed to be operated by China’s Ministry of State Security. Ball’s written testimony lists cyber attacks against other sectors, but that is no comfort for E-ISAC, he noted.

“The technologies targeted by Salt Typhoon are prolific across critical infrastructure sectors, including the electric sector, which makes repurposing tactics, techniques and procedures learned targeting one sector easier when targeting the next,” Ball said.

The rise in electricity demand most often linked to data center growth also offers new risks as Salt Typhoon targets those facilities. A NERC report from early 2025 highlights the risks sudden outages of large loads can pose to the grid, Ball said. (See Data Centers’ Reliability Impacts Examined at FERC Meeting.)

Just the fact that load growth is cutting into reserve margins increases the risk of any kind of event on the grid, including cyber and physical attacks, said Kenergy CEO Tim Lindahl, who was testifying on behalf of the National Rural Electric Cooperative Association.

“One of the concerns we have as we run the grid closer and closer to the edge is it becomes more and more critical to not have interruptions. Before, we could have a small event, and it wouldn’t have an impact on the reliability of the grid,” he said. “But as we push the grid to the limit with new load — data center load, or any kind of load — it just puts a microscope on any hiccup in the system that could happen.”

Any kind of event becomes riskier as the system is more tightly balanced, but Kenergy — a Kentucky co-op — is dealing with that by investing in new fiber-optic communication systems so it can better monitor its distribution system and help thwart attacks, Lindahl said.

‘Embracing Modernization’

The long-run solution to cybersecurity will include modernizing infrastructure control systems as much as possible because keeping them entirely separate from the internet has proved infeasible, said Harry Krejsa, director of the Carnegie Mellon Institute for Strategy and Technology.

“Digitization has swept our world so thoroughly that even national security networks that are believed to be air-gapped often are found to have accidental and unknown internet connections during regular security sweeps and efforts to ensure their ongoing defensibility from adversaries abroad,” Krejsa said. “The only way around this challenge will be through embracing modernization from top to bottom.”

E-ISAC CEO Michael Ball, Xcel Energy Vice President Sharla Artz, Kenergy CEO Tim Lindahl, Carnegie Mellon University’s Harry Kresja and Idaho National Laboratory’s Zach Tudor at the hearing Dec. 2. | House Committee on Energy and Commerce

The economic changes driving up electricity demand are already advancing that work, added Krejsa, who worked in the Office of the National Cyber Director under the Biden administration.

“The energy technologies powering this transition, from onsite generation and battery storage to smart inverters and virtual power plants, were designed from the ground up with software at their core enabling modern cyber security features and the ability to update and evolve in response to emerging threats,” Krejsa said. “They are also enabling a smarter, more distributed grid architecture, one that is more defensible, resilient and even self-healing, capable of quarantining disruptions and preventing cascading blackouts.”

That transition includes using components from China, which dominates manufacturing in general and “electrotech” specifically. Krejsa recommended a reshoring effort there, but noted also some of the most sensitive national security programs use Chinese components.

“I think it’s instructive to take a look at the case of the F-35, which does not have zero Chinese-made components,” Kresja said. “The defense industrial base, instead, makes a risk-informed prioritization decision about where the cut line is for components.”

Congress could help the power industry and advanced manufacturing parse which components are too sensitive to risk backdoors for Chinese (or other) hackers and which can be reliably sourced from anywhere, he added.

Actionable Intelligence Needed

Information-sharing is vital when it comes to emerging threats, and the Energy Threat Analysis Center (ETAC), set up in 2023 as a pilot program, has helped improve dissemination of information to utilities whose systems are under threat, Xcel Energy Vice President Sharla Artz said.

“The private sector must be supported by the government to address national security risks. An essential component of that support is the timely sharing of actionable intelligence about our adversaries, tactics and their motivations,” she added. “Armed with this intelligence, private-sector experts can proactively architect security into their systems, hunt for adversarial activity and mitigate the risks from these threats.”

ETAC already has shared important information with the sector on Salt Typhoon attacks, and Artz said Congress should authorize it to become permanent so the partnership can grow and evolve to address new threats.

“Explicit recognition of this program allows industry partners and DOE to shape the joint effort to address the evolving risk landscape and to incorporate needed partners in the work effort,” Artz said in written testimony.

E-ISAC’s Ball suggested authorizing ETAC to help further its mission, and he asked Congress to fund smaller utilities’ cyber defense and to reauthorize the Cybersecurity Information Sharing Act of 2015. The act is meant to facilitate information sharing and was temporarily extended to Jan. 30, 2026.

“Industry sources report that the law has enhanced response capabilities to cyber incidents and meaningfully advanced information sharing and cyber defense,” Ball said in written testimony. “As a private entity, expiration of the law has no immediate negative consequences on E-ISAC operations. However, the law does encourage information sharing with ISACs and other sharing relationships. Reauthorization would support the broader information sharing ecosystem and preserve a highly valued framework for the private sector.”

Ontario has approved a $26.8 billion CAD plan to overhaul four aging nuclear reactors that supply approximately 11% of the province’s electricity needs.

Ontario Power Generation said the refurbishment of Units 5 to 8 at the Pickering Nuclear Generating Station will extend their operation by up to 38 years.

The Ontario government announced the approval Nov. 26, saying the project would protect the province’s workforce and long-term energy security while building a more resilient, self-reliant economy in the face of U.S. tariffs.

The OPG facility on the outskirts of Toronto is one of the largest and oldest nuclear power stations in the world. Units 1-4 began operation from 1971 to 1973 and have been removed from service. Units 5-8 began operation from 1983-1986 and are licensed to operate through the end of 2026.

Units 5-8 are rated at 2.1 GW. Minister of Energy and Mines Stephen Lecce said the project would boost their output to as much as 2.2 GW.

The Pickering refurbishment was greenlit as OPG nears completion of a similar project at its Darlington Nuclear Generating Station, 17 miles east of Pickering, that is expected to cost $12.8 billion.

The Pickering project is larger and more complex, including the replacement of all 48 steam generators and the addition of a 1,500-meter deep-water intake structure, neither of which was needed for Darlington.

OPG said more than 7,000 lessons learned through the Darlington overhaul will help shape the Pickering project. The work is expected to begin in early 2027, after final licensing approval by the Canadian Nuclear Safety Commission, and continue through the mid-2030s.

Approval of the Pickering overhaul was not unexpected, but the plan is not universally supported.

Environmental Defence said Ontario’s government had locked the province into a high-cost, high-risk energy strategy that would steer away from wind and solar generation.

Lecce alluded to the opposition in his Nov. 26 announcement: “After the previous government’s attempt to shut down the facility, this refurbishment signals that we are doubling down on Canadian technology, Canadian workers and the Canadian supply chain to protect our economy from global instability.”

Nuclear is the leading form of transmission-connected capacity in the IESO grid as of September: 12.18 GW, or 32% of total nameplate capacity. In 2024, Ontario’s nuclear reactors generated 80 TWh of electricity, or 51% of all power sent to the grid.

The province expects nuclear to remain a central part of its energy portfolio in the future. This was emphasized in “Energy for Generations,” Ontario’s first-ever integrated energy plan, the front cover of which features a sweeping view of the Darlington station. (See Ontario Integrated Energy Plan Boosts Gas, Nukes.)

OPG is building what is expected to be the first small modular reactor in North America beside Darlington at an expected cost of $7.7 billion. (See Ontario Greenlights OPG to Build Small Modular Reactor.) Planned construction of three subsequent SMRs on the same site is expected to bring the total project cost to $20.9 billion.

I have been thinking a lot lately about how we do or don’t plan for technological transitions, like the current clean energy transition now underway in the United States and worldwide.

In his closing remarks at the United Nations’ climate conference known as COP30, Brazilian diplomat and conference president André Corrêa do Lago acknowledged the meeting’s failure, once again, to keep even a mention of a phaseout of fossil fuels in the final statement from the event. He pledged instead to begin work on a roadmap for a “just, orderly and equitable” transition away from fossil fuels and pointed to plans for an international conference focused entirely on such a phaseout, planned for April 28-29, 2026, in Colombia.

That such a conference is being planned is historic in and of itself, though how successful it will be remains an open question, given the ongoing influence of fossil fuel industry lobbyists at climate conferences. More than 1,600 fossil fuel lobbyists took part in COP30 in Belem, Brazil ─ one in every 25 attendees ─ according to a report from the nonprofit Kick Big Polluters Out.

But lobbyists are more a symptom than a cause. The real problem lies in the idea that we can in some just, orderly and equitable way plan for a transition away from fossil fuels. Technological transitions are by their very nature unplanned, disorderly and inevitably unjust.

One need look no further than the lightning speed with which artificial intelligence has become the dominant digital technology worldwide, permeating almost every aspect of our economic, social and political lives and throwing the U.S. electric power industry into a chaotic panic.

And, as in all technological transitions, winners, losers and collateral damage are inevitable.

K Kaufmann

The narrative from the Trump administration, some regulators and utility industry leaders is that to win the global race for AI leadership, we must keep existing coal and natural gas plants online and build even more to power the hyperscale data centers now springing up across the across the country.

Climate action is the big loser here. Rising greenhouse gas emissions and the increasingly catastrophic extreme weather events and other environmental upheavals they cause have been downgraded, in the words of Energy Secretary Chris Wright, to mere side effects of our digital society.

The collateral damage: developing nations and remote, rural communities ─ including those in the United States ─ that are most exposed and vulnerable to extreme weather.

Which is not to say we should not plan but rather refocus on things that can be planned for, things we can control.

Biden’s Implementation Blues

Lack of planning was a core problem in the Biden administration’s seeming inability to implement ─ at speed and scale ─ the clean energy programs authorized by the Infrastructure Investment and Jobs Act and the Inflation Reduction Act.

“Three years after the first of those laws passed, only a handful of federally funded projects had broken ground,” says a recent report from three former staffers at Biden’s Department of Energy ─ Ramsey Fahs, Alan Propp and Louise White. “This meant the political theory animating the administration’s approach ─ that the economic development generated by clean energy projects and industries would create a durable bipartisan coalition ─ was never truly tested.”

It also meant that President Donald Trump was able to quickly roll back programs and claw back funding, leading to a massive private sector retreat from previously announced multimillion-dollar projects.

“Years of work were undone in just a few months,” the report says, with at least 32 projects totaling $22 billion in investments canceled in the first six months of 2025.

Based on interviews with more than 80 DOE staffers, the report’s list of implementation blockers includes an absence of “clean, sector-specific deployment targets” and a reliance on “obligation metrics” ─ that is, money that was officially awarded but not actually spent ─ which resulted in a “false sense of progress.”

Other challenges included tangled decision-making processes and an overly cautious approach to risk management, resulting in long and complicated application and award processes.

Funded with $5 billion from the IIJA, the National Electric Vehicle Infrastructure program is a case in point. NEVI was aimed at installing DC fast EV chargers along major highways in every state, and when it was rolled out in February of 2022, the administration hoped to have the first chargers in operation by the end of the year. Hobbled by a range of federal, state and local requirements, the first NEVI station was opened in Ohio in December 2023.

Following Trump’s unsuccessful efforts to roll back NEVI, the most recent count has about 133 federally funded stations open in 16 states. Revised guidelines from Secretary of Transportation Sean Duffy have removed or minimized certain NEVI requirements, like ensuring that NEVI chargers benefit low-income communities.

What Fahs, Propp and White propose is that Democrats take a page from the Heritage Foundation’s Project 2025, the massive manifesto setting out plans for a second Trump administration, published in April 2023, and immediately start planning clean energy policies and programs, and recruiting staff for a future Democratic administration.

“Any attempt by the federal government to play an important role in advancing industrial and clean energy development across the United States will require a great deal more thoughtfulness and detail than even Project 2025 achieved,” the report says.

Essential parts of such a plan ─ let’s not call it Project 2029 ─ should include setting goals for “specific sectoral outcomes,” with strategies “designed to be actionable in a single term.” An administrative culture that promotes speed, decision-making and accountability for meeting goals and timelines will also be critical, as will more streamlined and flexible contracting practices, the report says.

For example, Build America, Buy America policies that require “lawyers to certify every bolt” of a project is domestically produced should be replaced with an approach that focuses on “a few high-impact sectors and provide[s] waivers or exemptions for low-value components and equipment with no domestic supply chain yet.”

The report also calls for more public-private partnerships, such as Trump’s recent deal with rare-earths supplier MP Materials, which “combined an equity stake, loans, warrants and a 10-year price floor and offtake agreement … [showing] how a sufficiently motivated executive branch can comprehensively derisk deployment in a key sector.”

(Certainly, under former Energy Secretary Jennifer Granholm, DOE pursued similar derisking partnerships, if not as blatantly commercial or raising concerns about conflicts of interest as Trump’s deals.)

The Need to be Feared

The other side of this conversation centers on how states and the clean energy industry itself are or aren’t planning for the dramatic swings in federal energy policy they now face ─ specifically the loss of federal tax credits, grants and other incentives and Trump’s ongoing war against renewables.

At the recent Solar Focus conference in Arlington, Va., sponsored by the Chesapeake Solar and Storage Association, known as CHESSA, Jigar Shah, former director of DOE’s Loan Programs Office, also called for a major cultural shift in the clean energy industry.

Too many businesses “are planning for the days that look like last year, and I think it’s important for us to recognize that those days are gone, and they’re never coming back, like even after the Trump administration leaves office,” he said.

Now leading a clean tech consulting firm, Multiplier, Shah delivered a typically provocative call to action. “Why do we have rules in place that make it impossible for us to integrate with electric utilities? … It’s not enough to be liked; you really need to be feared,” he said. “When people don’t deliver for us, they should lose their seats. …

“One of the biggest challenges that we have in this moment is that … there’s still a feeling that our industry doesn’t work unless it’s mandated, that people have to use us,” he said. Rather, with new Democratic governors in New Jersey and Virginia, the industry should be coming at them with clear, outcome-focused plans, for example, to build utility-scale batteries in key locations to improve system reliability, while reducing consumer electric bills by 20%.

“If we only achieve 80% of that stuff two years later, no one’s going to vilify us for that,” he said.

Speaking on the same panel, Sachu Constantine, executive director of the advocacy group Vote Solar, laid out what has become the industry’s standard argument for renewables as a vital solution to the growth in demand for electric power, driven by data centers, electrification and industrialization.

“We are the lowest-cost, fastest, market-scalable energy source out there,” he said.

But Constantine also said states should be seen as a testing ground for the new policies and regulatory structures needed to set goals and ensure outcomes that respond to that growth. “We shouldn’t be afraid of that. This is a chance, a generational chance, to create the regulatory scheme we want. We should look to the states and what they’re trying and what’s successful as a blueprint for what the future looks like,” he said.

Integrating and assigning value to solar, storage and other distributed resources as assets for capacity markets should be a top priority, he said.

Nicole Steele, another former DOE and EPA staffer, is now director of climate policy at Amalgamated Bank, a commercial bank that devotes 40% of its lending to climate solutions.

Like Shah and Constantine, she is similarly focused on outcomes, often at the local level, in a post-subsidy world where projects must be able to access market-rate capital. At EPA, she worked on the Greenhouse Gas Reduction Fund, which was intended, in part, to help fund state-level green banks.

With that funding still frozen by EPA, “there’s a whole shift coming together that really is looking at revenue bonds [for] supporting green banks,” Steele said. “We’re throwing our weight behind some of that work to really make sure that green banks are not only structurally playing a role ─ to not just be a lender, but to be the lender that can seed private sector capital and drive down the cost of that capital or make that capital more accessible.”

Why 1,600 Lobbyists?

So, is a just, orderly and equitable transition away from fossil fuels possible? I would never say never, but based on the analysis and insights of those who worked so hard for it during the Biden administration, what may be more likely and effective is a strategically planned and outcome-focused transition toward clean energy.

In other words, we need a plan with targets we can achieve within four years and then ensure we have the financial and administrative infrastructure to do just that.

Wright’s recent DOE reorganization ─ killing the Office of Clean Energy Demonstrations, the Office of Energy Efficiency and Renewable Energy and the Grid Deployment Office ─ continues his efforts to wipe any mention of renewable energy from the national consciousness. The National Renewable Energy Laboratory has been renamed the National Laboratory of the Rockies.

But even Wright must know, in his heart of hearts, that solar, wind, storage and other clean technologies are the future. In the first half of 2025, renewables accounted for 91% of new power on the U.S. grid. During the same time period, new solar and wind (403 TWh) more than covered new electric power demand around the world (369 TWh), according to U.K. industry analyst Ember.

The International Energy Agency expects renewable capacity worldwide will double, to 4,600 GW, by 2030 ─ still short of the international pledge at COP28 to triple renewable power over 2022 levels by 2030, but impressive.

The transition increasingly is being driven by the combined forces of economics and technology; clean technologies are frequently just better, more efficient and affordable.

Rising electric bills were a critical issue in off-year election wins for Democratic governors-elect Abigail Spanberger in Virginia and Mikie Sherrill in New Jersey ─ one that could drive more Democratic victories in the 2026 midterms. Both residential and commercial solar and storage provide one of the quickest ways to cut bills, with very small-scale, plug-in (and largely unregulated) “balcony” solar and storage systems gaining in popularity.

With more renewables on the grid, Americans may see that we don’t need new fossil-fueled generation and can retire existing plants, without threatening reliability or affordability.

The fossil fuel industry will bring all its power, money and influence to slow the transition ─ as it has, at least temporarily, in the U.S. But perhaps why the industry needed those 1,600 lobbyists at COP30 was fear and a dawning recognition that it will eventually become irrelevant.

Livewire columnist K Kaufmann has been writing about clean energy for 20 years. She now writes the E/lectrify newsletter.

MISO announced it will study 6 GW of mostly natural gas-fired generation projects in the second group of entrants under its interconnection queue fast track.

The grid operator accepted 15 proposals totaling 6.1 GW of new installed capacity Dec. 1. Natural gas additions account for almost 4.3 GW of the projects. In-service dates range from Dec. 1, 2027, to Aug. 6, 2028.

The largest gas plants MISO marked for study this time are Invenergy’s proposed 1.2-GW gas plant for Wisconsin Electric’s customers; Entergy Texas’ 820-MW Legend gas plant in Jefferson County, Texas, to serve industrial customers; and Entergy Mississippi’s pair of proposed 768- and 763-MW gas plants to accommodate load growth and data centers.

MISO agreed to study battery storage proposals from Ameren Missouri, Entergy Louisiana and DTE Electric that range from 208 MW to 350 MW. The second cycle study list includes solar and wind projects in Minnesota, Michigan and North Dakota.

“Cycle 2 builds on the momentum of Cycle 1 and reflects the continued demand for timely, reliable interconnection solutions. These projects are essential to meeting near-term reliability needs and ensuring new resource additions are online to meet load growth,” MISO Senior Vice President Aubrey Johnson said in a press release.

Johnson said MISO views the fast lane as “one of several tools we’re using to meet the evolving needs of our members and the communities they serve.” He added that MISO remains intent on cutting down the wait times in its regular generator interconnection queue through the annual megawatt cap and automated software.

Environmental groups have disputed MISO’s and SPP’s queue fast tracks at the D.C. Circuit Court of Appeals, arguing the processes are unfair and allow primarily fossil fuel generation to leapfrog lengthy queue lines while ratepayers fund grid upgrades necessary to host them. (See Enviros Challenge MISO, SPP Queue Express Lanes.)

MISO reported that so far, utilities and developers have submitted 51 projects totaling almost 30 GW for consideration in the expedited queue. The RTO accepts applications for the queue fast lane continually. It plans to leave its application window open until it has studied 68 interconnection requests or May 10, 2027, the application deadline for the final cycle.

MISO has committed to studying a maximum of 68 projects before it retires the temporary express lane process no later than Aug. 31, 2027. Of the 68 spots, 10 are reserved for submissions from independent power producers, with an additional eight set aside for entities serving MISO’s retail choice load in downstate Illinois and a percentage of Michigan.

The RTO said three of the first set of 10 fast-tracked projects have struck generator interconnection agreements, with the other seven poised to execute their agreements before the end of 2025.

MISO will announce another fast lane study cycle in early March 2026.

U.S. electricity outage hours reached their highest levels in a decade in 2024 due to the impact of Hurricanes Beryl, Helene and Milton, the EIA reported.

From 2014 to 2024, electricity customers averaged around two hours of outages a year unrelated to major events such as hurricanes or storms, interference from vegetation near power lines or “atypical” utility operations, EIA said.

Interruptions attributed to major weather events averaged four hours, the agency said.

In 2024, the major hurricanes added another seven hours to that figure — meaning the average customer experienced 11 hours of outages.

Outages are categorized by two metrics in the industry: The system average interruption duration index (SAIDI) measures the total duration of non-momentary outages, and the system average interruption frequency index (SAIFI) measures the number of outages in the year.

Nationally, customers averaged 1.5 outages last year. Hawaii led the country on the SAIFI, being the only state to see its power customers average more than four outages in 2024 — but the overall time they were without power was well below the national average. Hawaii had a high number of outages due to bad weather, volcanic activity, unexpected outages at oil companies and issues connecting new power plants.

Maine and Vermont took second and third place, though Mainers averaged nearly 30 hours in SAIDI and Vermonters just under 15 hours. Utilities in both states often have to deal with treefalls knocking out power, EIA said.

Maine customers averaged longer outages than customers in Florida, North Carolina and Texas, despite not being hit by any of the major hurricanes that drove the spike in SAIDI in those three states and nationally. Those Southern states saw customers average between 25 and 30 hours of SAIDI, about half the duration of South Carolina customers who averaged 53 hours of outages.

Hurricane Beryl knocked out power to 2.6 million customers in Texas in July 2024 while September’s Hurricane Helene left 5.9 million customers across 10 states without power, with 1.2 million of those in South Carolina. In October, Hurricane Milton knocked out power to 3.4 million customers in Florida.

Arizona, South Dakota, North Dakota and Massachusetts experienced less than two hours of outages in 2024, while South Dakota, Maryland, Illinois and Massachusetts all averaged less than one outage that year.

As you know, Westinghouse, its two (Canadian) owners, and the U.S. government announced plans for $80 billion of investment in new nuclear plants. Recent articles are here, here and here.

I’ve been skeptical about new nuclear for many years — whether it be microreactors for U.S. military bases, new nuclear generally, small modular reactors in Ontario, nuclear fusion or Vogtle, as I wrote about here and here. And the skeptic’s case remains powerful.

But a recent study from DOE’s Idaho National Laboratory (INL) leads me to think this recent announcement could be a vehicle for something important. Maybe very important.

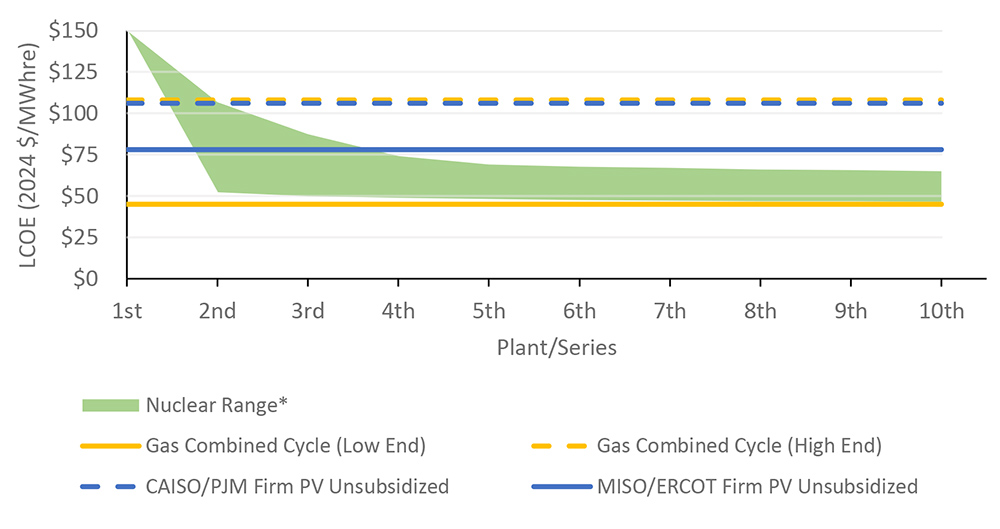

The NOAK Unit

The INL study makes a strong case that the cost of new nuclear plants could decline from the Vogtle experience as multiple units are constructed, until reaching a “mature” (“nth of a kind” or NOAK) cost of around $6,000/kW at around the seventh to ninth plant. The projected cost reduction from Vogtle’s $15,000/kW? About 60%. The chart from the study (see above) illustrates the cost reduction in terms of capital cost per kilowatt (a “series” is two plants).

You can read the study for the various drivers of the cost reduction.

The China Experience

The INL study bases much of its analysis on China achieving low and declining costs and construction times with its past completion of four AP1000 (Westinghouse design) units, and its 11 CAP1000 and CAP1400 units (adapted from the Westinghouse AP1000 design) now under construction, as listed here.

A separate Harvard study is featured in a recent New York Timesarticle, with more color here. A chart shows capital costs for new Chinese projects under construction at around $2,000/kW.

This Chinese capital cost is about one-third of what the INL study says is possible in the U.S. This would suggest that the INL NOAK cost is not just whistling Dixie.

Cost of New Nuclear Versus Alternatives

So what would the INL NOAK cost mean relative to the costs of other electric power generation?

Here’s a chart from the INL study showing the anticipated U.S. cost reduction in $/MWh Levelized Cost of Energy (LCOE) terms in the context of other generation costs.

Moderate scenario LCOE values: Representative of U.S. experience | DOE

The nuclear range is shown with and without an investment tax credit (ITC). You’ll see that with or without an ITC, nuclear costs start falling below firmed-up solar (based on Lazard estimates) after several nuclear units. And new nuclear cost falls within the broad range for new gas combined cycle cost (not to be confused with the very low cost of retaining existing gas units, even with carbon emission mitigation, as I’ve discussed before).

Importantly, these LCOE cost comparisons are before consideration of the social cost of carbon. If a social cost of carbon were incorporated, such as the $66/tCO2 discussed here, with a $/MWh equivalent of about $30/MWh, the above combined cycle costs would go up substantially. Another way of looking at it is to consider the social cost of carbon as roughly similar to the ITC financial benefit, so the social cost of carbon is rough justice supporting the ITC as an economically justified subsidy.

Location, Location, Location

The prior chart illustrates another important consideration. You’ll note that firmed-up solar in MISO and ERCOT has an LCOE about $30/MWh less than firmed-up solar in CAISO and PJM. This illustrates Lazard’s detailed analysis of the costs of firming up solar and wind, finding that LCOEs differ dramatically by region and by resource.

Given that solar and wind are much more expensive in some regions than in other regions, are the high-cost regions going to decarbonize if it means a permanent economic disadvantage? The only fix (absent nuclear) would be very expensive, difficult-to-site transmission to move power from low-cost renewable regions to high-cost renewable regions.

Nuclear is not location dependent. That could be important for high-cost renewable regions to reduce carbon emissions at competitive cost.

Getting There from Here

So new nuclear might be competitive, but here’s the rub: Who’s going to put up $14,000/kW for the first two units? Or $10,000/kW for the next two? Absent taxpayer (or tech bro or foreign country) financial support, new nuclear can’t get out of the starting gate.

We should recall that taxpayers footed the bill to get solar and wind going, starting almost 50 years with an ITC. EIA estimates that between 2016 and 2022, renewables received $84 billion in federal taxpayer support, while nuclear received $3 billion over the same period.

Assuming the INL capital costs, we can ballpark what it would take in taxpayer subsidies to buy down the cost of the first six nuclear units to the projected cost of the seventh unit (which yields an LCOE below firmed-up solar). Taking the cost differences and applying the 6,600 MW of six AP1000 units comes to $30.8 billion.

Taxpayer funds could be provided over time to match a schedule for outlays. The first two to three pre-construction years for a given plant wouldn’t require much money, but they would get the ball rolling.

An Elephant in the Room

Let me acknowledge a structural weakness in this plan: the creation of a monopolist, Westinghouse. Monopolies by nature raise prices and have limited incentive to be efficient, with poster child Vogtle as I’ve written before here and here.

But the situation here might be the exception to the rule if potential profits from future NOAK units, assuming price targets were achieved, were sufficient incentive for Westinghouse and its major vendors to contain costs on the subsidized first units. And the actual agreement could have financial features designed to incent cost containment.

The Actual Agreement

Regarding the actual agreement for the new initiative, one of Westinghouse’s owners said it expects it to be done around the end of the year.

The details of such an agreement are critical to any chance of success. Who’s doing what, when, how and where? What are the incentives to do what, when, how and where? Who’s qualified to do what, when, how and where? Who’s bearing the cost overrun and schedule delay risks of what, when, how and where? Who’s independently monitoring what, when, how and where? What are the enforcement measures to ensure everyone does what they commit to do, when, how and where?

If the requisite engineering, finance, economic, commercial and legal expertise for such an agreement doesn’t exist in the U.S. government, hire it from outside. There’s too much at stake to wing it.

Bottom Line

There are three established sources of carbon-free electricity: solar, wind and nuclear (putting aside hydro with its limited expansion prospects). With staggering need for more electricity, are we going to give up on one of the three — the only one that is not intermittent and not locational? As Wayne Gretzky (actually his father) said: “You miss 100% of the shots you don’t take.”

Let’s take a shot, America.

P.S. For the holiday season in these challenging times, here are some lists of happy music courtesy of some good folks on Maryland’s Eastern Shore. And here’s a classic video for the season by the Dropkick Murphys. The best of the holidays to you and yours!

New York is adding new leadership to its advanced nuclear energy initiative: Todd Josifovski, director of the $13 billion overhaul of an Ontario nuclear power facility, and Christopher Hanson, who chaired the U.S. Nuclear Regulatory Commission during the Biden administration.

The New York Power Authority announced the appointments Dec. 1.

Josifovski will become NYPA’s senior vice president of nuclear energy development Jan. 1. Hanson will serve as a senior consultant on financing and the federal permitting process.

Popular acceptance of nuclear energy has increased in recent years, and President Donald Trump has ordered the federal regulatory process to be accelerated and streamlined, but the process of building a new commercial reactor remains potentially slow, expensive and complex. Josifovski and Hanson are expected to help New York with this.

Josifovski has worked in clean energy and nuclear power development for more than 20 years, including at Ontario Power Generation, where he was a senior manager and then director of the refurbishment of the four-unit Darlington Nuclear Power Station. That project is nearing completion at an expected cost of $13 billion CAD. Josifovski currently is vice president of development at Peak Power.

Hanson joined the NRC as a commissioner in 2020, during Trump’s first term, and served as chair from Jan. 20, 2021, to Jan. 20, 2025. He continued as a commissioner until Trump fired him June 13.

His NRC bio notes that he previously accrued three decades of public- and private-sector experience in the nuclear fuel sector.

NYPA President Justin Driscoll said Josifovski and Hanson would play important roles in moving the state’s nuclear initiative forward.

“Todd has managed the development and execution of more than 7 GW of clean energy and nuclear projects, and his approach integrates technical rigor with pragmatic risk management, stakeholder engagement and a strong commitment to operational excellence,” Driscoll said. “Additionally, Chris’ extensive experience on the federal level will prove invaluable to NYPA as we navigate this next chapter and form lasting partnerships that will deliver firm, emission-free generation for New York state.”

New York has a challenging path ahead as it tries to expand and upgrade its grid. Its renewable energy buildout was behind schedule even before Trump began his second term, and his policies are expected to further impede progress.

As a result, the aging fossil fleet that policymakers want to phase out remains indispensable: 25% of total statewide generating capacity is fossil-fired plants that are more than 50 years old.

New York’s four commercial reactors — on the opposite shore of Lake Ontario from Darlington — are a combined 198 years old and draw half a billion dollars a year in ratepayer-funded subsidies to continue operation. The state expects to rely on their output into the middle of the century. Meanwhile, state policymakers expect to need more electricity as New York decarbonizes transportation and buildings.

The confluence of factors is such that NYISO opened its 2025-2034 Comprehensive Reliability Plan with this warning: “New York’s electric system faces an era of profound reliability challenges as resource retirements accelerate, economic development drives demand growth and project delays undermine confidence in future supply.”

The existing nuclear fleet provided 21% of the power produced in-state in 2024, NYISO said in the report issued Nov. 21; a scenario in which the four reactors are retired would create shortfalls in summer and larger shortfalls in winter.

The challenge facing NYPA — and now Josifovski and Hanson — is to move the advanced nuclear initiative forward not just quickly but safely and affordably, and with a politically acceptable siting mechanism.

NYPA has issued requests for information from potential developers and potential host communities on how best to do this. (See Wanted: N.Y. Community Eager to Host Nuclear Reactor.) Their responses are due Dec. 11.

Discussion about potential changes to the NYISO demand curve reset (DCR) process dominated a recent Installed Capacity Working Group meeting and will likely take up more oxygen in stakeholder meetings throughout the coming year.

“This project has the potential to deliver transformational changes to the market in the face of evolving grid conditions,” Michael Ferrari, NYISO market design specialist in capacity and new resource integration, told the working group Nov. 17 in presenting the project’s kickoff.

The Capacity Market Structure Review project identified the DCR as an area that needed improvement. The improvement project was prioritized for 2026, meaning NYISO has budgeted resources and labor hours for it.

Stakeholders have long complained that the DCR does not provide adequate price signals for new investment, value reliability contributions or provide sufficient consideration of long-term reliability impacts. During the latest DCR, stakeholders debated whether NYISO’s preferred proxy unit, a two-hour battery system, was appropriate or reflective of what might enter the market. In addition, stakeholders said the DCR has a steep learning curve, requires a lot of stakeholder engagement and provokes contentious debates during working group meetings.

Though Ferrari’s presentation noted all these concerns, “it doesn’t seem like the concerns expressed by Con Edison are in here,” a representative of the company said. “There have been multiple conversations on our end about concerns of higher costs to customers.”

Ferrari said stakeholder feedback highlighted in his presentation was “not a comprehensive list,” though the omission of price considerations was indeed an accident.

The presentation indicated NYISO would study how to improve or refine the definition of the proxy unit used to undergird the DCR process. The ISO also would look at restructuring the development of the net cost of new entry of the proxy unit, which sets prices for the curve; look at alternative curve slopes; and possibly develop a technology-agnostic approach to net CONE.

Stakeholders asked what a “technology-agnostic approach” meant with respect to net CONE. Ferrari said it meant NYISO was considering not choosing one specific unit to serve as the proxy for new generator entry to the market.

The ISO plans to issue a draft Issue Discovery Report at the ICAP Working Group’s Dec. 16 meeting. It will present the group with a detailed proposal of initial market design enhancements for consideration at a later meeting.

In New England, increasing winter reliability concerns are driving questions about how long the region’s aging fleet of oil-fired power plants can, or should, remain on the system.

Power generation from oil has declined dramatically in New England since the start of the century. The oil plants that have remained on the system have run less frequently, mostly during tight winter periods when gas generators have limited access to pipelines.

Several high-profile oil units have already retired, and the large oil resources that remain face significant retirement risks.

Continued reliance on aging oil generators has real consequences: The units are among the dirtiest in the ISO-NE resource mix, both in terms of climate-warming emissions and local air pollution that can have significant health effects on nearby residents.

But ISO-NE forecasts that growing winter demand, coupled with obstacles to offshore wind development and limits to the region’s gas supply, will increase the need over the next decade for dispatchable generators with fuel storage capabilities. This may force the region to keep the units online longer than many policymakers hoped, or to invest in adding dual-fuel capabilities to existing gas-only units.

Uncertainty remains, however, around when a significant spike in winter demand will materialize. And changes in the wholesale markets — including ISO-NE’s ongoing capacity market overhaul, evolving Pay-for-Performance risks and the introduction of longer-duration reserve products — could also have significant effects on plant revenues, making it difficult to predict how long the resources will remain online.

“You see a lot of the owners of some of these oil facilities caught in between and not being able to see a clear picture as to whether the ISO, the states and other policymakers want to try to preserve those facilities or drive them into retirement,” said Dan Dolan, president of the New England Power Generators Association.

“A lot of them have been driven into retirement or been driven into a place in which they are right on the cusp of financial viability,” he said. “I, at this point, don’t have a clear line of sight as to how some of those standalone large steam units are going to function.”

Changing Economics

The New England oil fleet is old: Most of the oil-fired steam units were built in the 1970s. As cheaper, cleaner and more efficient sources of energy have come online, oil generation has declined dramatically, dropping from 18% of the total energy production in 2000 to 0.3% in 2024, according to ISO-NE.

The steepest decline occurred between 2000 and 2010. Over the past 10 years, annual oil generation has fluctuated, often following the severity of winter conditions.

But the region has continued to see retirements and a declining amount of oil capacity on the system. Between Forward Capacity Auctions 15 and 18, capacity supply obligations for generators running on distillate and residual fuel oil declined from over 4,700 MW to about 3,500 MW.

“Many of these units are at risk of retirement,” ISO-NE noted in its draft 2025 Regional System Plan. “They run infrequently, are less efficient and are nearing the end of their economic life.”

As the resources have run less frequently, they have become more reliant on capacity revenues, while low capacity clearing prices have pushed higher-priced generators out of the market, according to ISO-NE’s Internal and External Market Monitors.

Potomac Economics, ISO-NE’s External Market Monitor, wrote in its 2024 annual report that “the sustained low prices led to 760 MW of retirement bids from units with on-site fuel supplies clearing in FCA 18,” which applies to the 2027/28 capacity commitment period (CCP).

With essentially no dispatchable generating resources in the region’s interconnection queue, “it will be critical to retain a large share of the existing dispatchable generation and avoid mandating retirements of fossil fuel resources,” Potomac wrote.

ISO-NE analyses have “made it clear that we need dispatchable resources, and we need a fairly significant quantity of readily available fuel for those dispatchable resources,” said Brian Forshaw, principal at Energy Market Advisors and a longtime NEPOOL participant. He emphasized that his comments are not on behalf of any of his clients.

“The challenge is going to be how to identify what the value of retaining that capability is, and then developing some kind of a market mechanism, or a reserve product or whatever else to compensate them enough to keep them around,” he added.

ISO-NE’s Capacity Auction Reform (CAR) project, a major multiyear effort, is intended to help better align capacity procurements with actual reliability benefits.

The project proposes transitioning the RTO from a forward, annual capacity market, with auctions held three years prior to the relevant CCP, to a prompt, seasonal market, with auctions held about a month prior to each CCP, which would be divided into winter and summer seasons.

The effort also includes significant changes to how much capacity value ISO-NE assigns to different resource types. Under the current rules, the capacity market typically accredits resources based on an audited value intended to capture the maximum output they can provide. The methodology does not account for outage rates and maintenance requirements, which ISO-NE instead factors into its calculations for the installed capacity requirement.

Under the proposed CAR changes, resources would be accredited based on their marginal reliability impact value, which is intended to capture contributions to reducing energy shortfall during extreme model scenarios. Accreditation values would account for a wider range of factors, including resource outage rates, maintenance requirements, stored fuel and intermittency.

The changes could have major implications for the capacity revenues available to different resource types, though it is still early in the process to predict how the project will affect various resource classes.

“It is vitally important that the ISO-NE markets accurately signal which resources effectively support reliability and how much capacity is needed,” Potomac wrote in its annual report. “This is necessary to avoid premature retirement of fuel-secure resources, incentivize generators to acquire inventory or firm fuel arrangements, and avoid overpaying for capacity that does not support reliability.”

The changes to accreditation will likely be both positive and negative for oil generators.

Accounting for fuel storage appears likely to increase the accreditation values for oil units relative to other resources, and multiple participants involved in NEPOOL discussions also said the shift to a seasonal market may push prices up in the winter, providing an additional boost.

However, oil-fired steam resources tend to have higher outage rates and greater maintenance requirements, which will likely limit their accreditation values, regardless of their stored fuel capabilities or potential winter benefits.

The shift to a prompt market would also allow resources to submit retirement notifications much closer to each CCP; it would reduce this notification deadline from about four years to about one. This would enable participants to make retirement decisions based on more up-to-date information about the conditions of the market and their resources.

“There’s so many variables and moving pieces to that design — it’s going to be hard to get a clear picture until we see more about how all those pieces fit together,” NEPGA’s Dolan said.

Some stakeholders also expect future capacity prices to reflect a perceived increase in PFP risk. Capacity scarcity events trigger the PFP rules, which penalize resources with capacity obligations that fail to perform and reward resources that deliver more than their obligations.

Some oil-fired generators have racked up significant penalties during PFP events in recent years. The resources generally require significant advance notice to ramp up and come online, making them ill-suited to perform during unexpected scarcity periods.

“I think it’s fair to assume that the higher Pay-for-Performance risk that people are now starting to perceive will work its way into the supply offers that will get submitted into the market,” Forshaw said, adding that this will likely put “some upward pressure on prices.”

New Mechanisms

Taking all factors into account, “the expectation is: Some of the older resources that do maintain significant inventories of residual oil are going to face challenges going into [the 2028/29] time frame and may consider submitting deactivation notices one year prior to the start of the delivery period,” Forshaw said.

With looming retirement risks and ISO-NE’s forecast that winter reliability risks will rise in the mid-2030s, it is important to begin discussions on potential solutions and new mechanisms, he said.

In a statement, ISO-NE noted it is evaluating “the potential addition of a longer response reserve product, such as a 60- or 90-minute reserve, to help manage uncertainties caused by the increasing variability of renewable generation and real-time system demand,” which may provide additional opportunities for oil resources.

The RTO also recently established a new Regional Energy Shortfall Threshold (REST), which is intended to define an acceptable amount of shortfall risk in the region. It plans to use the threshold to evaluate risks prior to each winter and summer season, as well as in long-term assessments. (See ISO-NE Proceeding with Shortfall Threshold After Positive Feedback.)

It has yet to determine how it would select and develop solutions to mitigate risk if the threshold is violated.

Data from long-term assessments “will guide evaluation of whether the possibility of exceeding the REST in those time frames requires development of regional solutions to mitigate modeled risks and, if so, when to begin to develop solutions; these efforts would be signaled in future annual work plans,” ISO-NE wrote in a statement.

The RTO has yet to deploy the threshold in long-term, forward-looking studies. ISO-NE’s probabilistic modeling for the upcoming winter indicates the region is well short of the risk threshold. (See ISO-NE Forecasts Minimal Shortfall Risk for Upcoming Winter.)

Forshaw emphasized the importance of establishing the process for addressing REST violations well before they occur, noting that major market reform frequently is a multiyear process.

If studies show high risks of energy shortfall because of a lack of fuel, it could make sense to procure fuel, or another type of energy, that would “only be used when we’re facing load shedding, rather than in the normal course of dispatch,” he said.

Interest in Dual Fuel

Regardless of potential new mechanisms or the specifics of the accreditation changes, some of the region’s aging oil generators may be nearing the end of their useful life. Resource owners that are willing to keep units online, waiting for a spike in capacity prices, may be unwilling to make large capital investments in the case of major mechanical failures.

This long-term outlook, coupled with the region’s winter gas constraints, has driven some increased interest in adding dual-fuel capabilities to existing gas plants, enabling them to burn oil during winter periods when gas prices spike or the units are unable to access gas.

“Given the slowdown on offshore wind and the other changes at the federal level that have really slowed down the scale and the pace of other clean energy entry, there’s been a lot of interest from state policymakers, ISO New England and others about exploring what capabilities exist out there for adding more dual fuel to make up this megawatt-hour gap that may be in front of us,” Dolan said.

Potomac wrote in its report that adding on-site fuel storage to gas-fired resources is “likely the lowest-cost strategy for addressing winter reliability concerns in the near-term in light of the issues with offshore wind development.”

However, there is uncertainty as to whether the states would allow the facility changes, or if the market would support the investments, Dolan said. He added that dual-fuel investments likely would require “over a decade of payback … and years of development to put it into place.”

He noted that the tensions and contradictions between state and federal policy have created significant development challenges for a broad range of resource types.

“It’s a really tricky environment, and I don’t have a clear answer of what to do about that,” Dolan said.

Clean Energy Solutions and Environmental Impacts

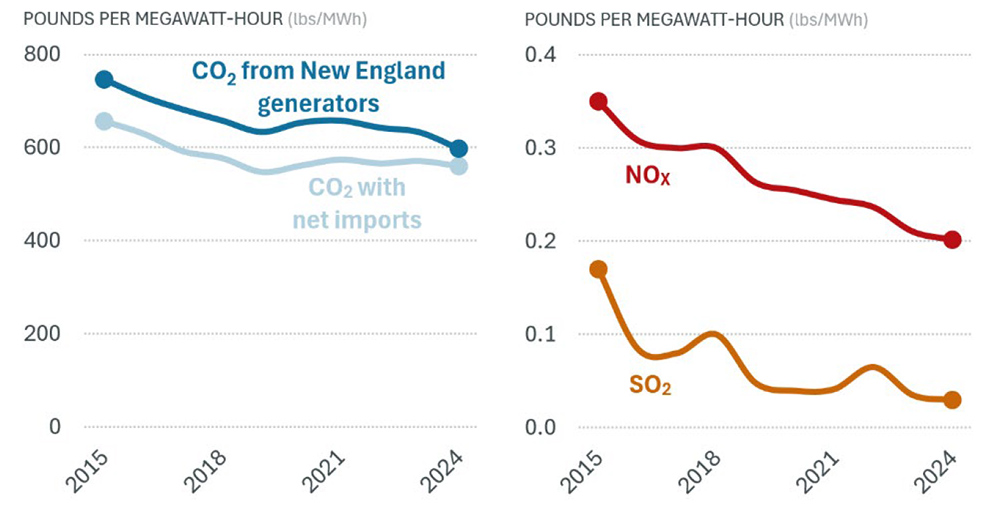

The decline in oil generation, and the replacement of inefficient oil and coal units with cleaner gas plants and renewable energy, has coincided with significant reductions in emissions from nitrogen oxides and sulfur dioxide, according to ISO-NE’s 2024 emissions report.

The RTO notes that between 2015 and 2024, sulfur dioxide emissions declined by 82% and emissions from nitrogen oxides dropped by 42%. This compares to a 15% decline in carbon dioxide emissions.

New England annual average emission rates, 2015 to 2024 | ISO-NE

Oil-firing power plants “are among the highest-polluting resources that we have,” said Joe LaRusso, manager of the clean grid program at the Acadia Center. “Many of them are located in communities that are overburdened with air pollution as it is.”

Nitrogen oxides and sulfur dioxide, along with fine particulate matter, are air pollutants associated with a range of heart and lung issues, child asthma, cancer, autoimmune diseases and neurological harm, according to the American Lung Association.

In Massachusetts, these pollutants were responsible for 2,780 excess deaths in 2019, according to Boston College researchers.

While it is difficult to attribute deaths to specific generation types or plants, the study notes that stationary sources, which include power plants, industrial facilities, and heating and cooking, were responsible for about 30% of fine particulate pollution in the state.

Concerns about health effects have motivated grassroots movements to block the development of new peaking plants. In Peabody, Mass., residents fought bitterly and, ultimately, unsuccessfully to stop the construction of a dual-fuel peaker, which came online in 2024.

Any efforts to add oil capacity in the region, or to implement market mechanisms propping up these units, would likely be met with opposition from environmental groups.

LaRusso said he is optimistic that three large projects nearing completion — Revolution Wind, Vineyard Wind and the New England Clean Energy Connect (NECEC) transmission line — will reduce the need for oil peakers, potentially pushing additional units into retirement.

NECEC is intended to supply the region with a consistent source of baseload power, while offshore wind performs best in the winter, when oil units run the most. Clean energy and consumer advocates also hope that aggressive demand-side initiatives will cause load to grow at a slower pace than is projected by ISO-NE.

In the long term, LaRusso said the resumption of offshore wind development in New England, the start of offshore wind development in Nova Scotia and increased bilateral power exchanges with Quebec could help the region meet growing winter demands while eliminating most of the remaining need for oil-fired generation.

“It seems that oil is going to follow the same path as coal, unless the demand curve starts rising so fast that batteries can’t keep up,” he said. “There are so many factors in play, but none of it appears to provide a rosy picture for an oil-firing plant.”