Washington’s first full-time climate change epidemiologist will go on duty starting July 1.

That epidemiologist will work for the Washington Tracking Network, a state health department program that aims to make public health data more accessible to the public, agencies and governments.

Rad Cunningham, senior epidemiologist and manager of the Climate and Health program under the Washington Department of Health, declined to name the new full-time climate change epidemiologist, saying she has not agreed to have her name released until July 1. Actually, Washington is hiring 1.25 full-time equivalent climate change epidemiologists. A quarter-time staffer will begin work for the tracking network on June 16.

The tracking network examines climate change data with an eye to predicting future health effects caused by global warming. The state program would provide this information to city and county governments and health departments as they prepare for the future. The two new epidemiologists are expected to analyze about 20 to 30 years of data and have a good grasp of what to tell various governments and agencies in about two years. Several states have this type of post, although it is not common, Cunningham said.

Washington’s leaders have blamed global warming for increased wildfires, problems with the state’s shellfish industry, a lack of water for farming and numerous health problems and other troubles.

Cunningham noted that an abnormally high heat wave last year was linked to the deaths of 157 Washington residents.

The state Health Department examines the climate change impacts to health with respect to air quality and wildfires, drinking water, extreme heat, pollen, agriculture and ocean acidification.

Global warming is linked to rising acidity levels in Washington’s warming sea waters, causing tiny oyster shells in Washington’s Dabob and Willipa bays to crumble faster than they can grow back. The problem has cut sharply into the state’s oyster harvests, which is a $270 million/year industry.

Sweltering heat — even by Texas standards — led to ERCOT finally setting a new all-time peak demand mark Sunday after several close calls last week.

Demand reached 74.9 GW at 5:10 p.m. CT, breaking the previous record of 74.8 GW set in August 2019. The record could be short-lived, as ERCOT was projecting demand to peak at 76.8 GW on Monday, threatening staff’s peak demand forecast of 77.3 GW for the summer.

That the record came on a weekend, when offices are empty, and during June is an indication of how unusually hot the weather has been in Texas. The state’s major cities have set daily records for high temperatures since Friday as an oppressive weather pattern settled over the south central U.S. The National Weather Service issued an excessive heat warning for North Texas on Sunday in anticipation of temperatures above 105 degrees Fahrenheit and heat indexes above 110.

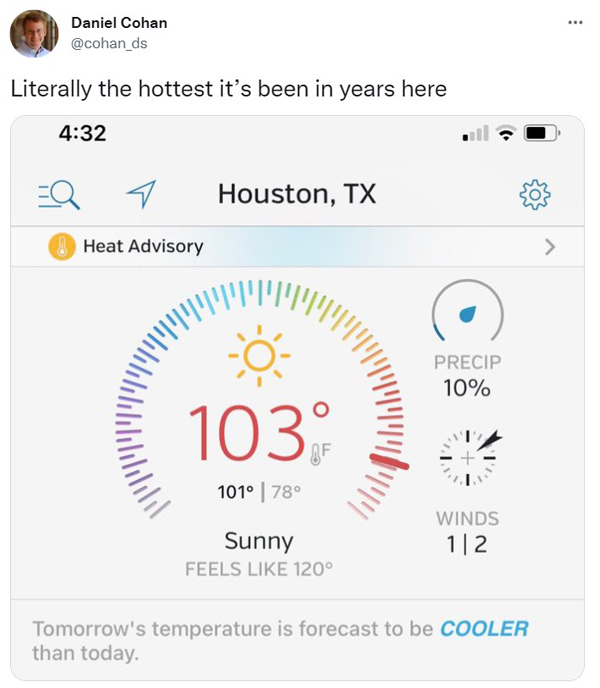

The heat index in Houston reached 120 degrees at one point Sunday. | Daniel Cohan via Twitter

The heat index was as high as 120 F on Sunday afternoon in Houston, where city officials activated the city’s emergency heat plan and opened cooling centers late last week. Austin also declared a heat emergency and opened cooling centers, where 100-degree temperatures are expected through next week.

“Welcome to the final days of spring in Austin,” tweeted University of Texas energy professor Michael Webber, sharing an image of triple-digit Austin-area temperatures (save for a 99-degree forecast for Wednesday).

Suddenly, ERCOT’s “extreme” maximum demand of 81.6 GW this summer doesn’t seem so improbable.

ERCOT has yet to issue a formal conservation alert. The grid operator still had nearly 5 GW in operator reserves during Sunday’s peak demand. Thermal outages were up slightly to 6.4 GW on Sunday, according to Stoic Energy President Doug Lewin.

The Texas grid was operating during the weekend under its third operating condition notice (OCN) since April. The OCN, intended to alert market participants of a possible need for more resources, was to expire Monday.

ERCOT officials have said they expect “sufficient generation to meet forecasted demand.” Indeed, the grid held up, despite scattered distribution outages in North Texas, lending a measure of comfort to Texans down on ERCOT since the disastrous February 2021 winter storm.

“Making it through this early heat wave should give some confidence in ERCOT for the rest of the summer,” said Joshua Daniels, an energy researcher at UT. “The bleeding has stopped; it’s time for rehab.”

ERCOT again set records for June when demand averaged 73.9 GW and 74.4 GW during afternoon intervals on Friday and Saturday, respectively. Demand exceeded 70 GW at 12:45 p.m. Monday.

ERCOT has benefited from wind and solar energy, though both at times have been curtailed by transmission congestion. The renewable resources were supplying about 28 GW of energy Sunday afternoon, some 3 GW below staff’s forecast. The cheap energy helped keep prices under $100/MWh Sunday, with the exception of the Houston load center.

According to a demand and energy report posted last week, wind (32.4%) and solar (6.2%) accounted for 38.6% of ERCOT’s fuel mix in May. Gas resources provided 32.1% and coal 13.3% of the energy mix.

The developer of a renewable diesel fuel plant in Oregon is tackling its final two bureaucratic hurdles before beginning construction on the $2 billion facility.

If no hiccups occur, NEXT Renewable Fuels of Portland predicts a best-case scenario of opening a plant capable of producing 50,000 barrels of renewable diesel daily by 2025 at the earliest. The site is at the Port Westward Industrial Park in Clatskanie, which is about 60 miles downstream of Portland on the Columbia River.

NEXT is awaiting approval of an air quality permit from the Oregon Department of Environmental Quality and completion of a federal environmental review.

The project is supposed to produce around 2.1 million gallons of renewable diesel a day from various types of greases, plus cooking and fish processing oils imported from around the world. There is a distinction between “renewable diesel” and “biodiesel” in that renewable diesel fuel does not need modifications in the engines that it serves, NEXT spokesperson Michael Hinrichs told NetZero Insider.

Production of 50,000 barrels of day could provide the diesel needs for all of Oregon, he said.

The Clatskanie project is one of several renewable fuel proposals in the works for the West Coast. Hinrichs said there is a market for several renewable fuel suppliers in California, Oregon and Washington. “The demand is high enough on the West Coast that it can handle a number of these facilities,” he said.

This demand comes from a major push among the coastal states to replace petroleum-based diesel for trucks, ships and heavy equipment with renewable fuels that produce fewer carbon emissions.

Port Westward in Clatskanie was selected because it has a deepwater port to handle ships containing the raw materials, plus rail lines and truck routes linking it to the rest of the West Coast. “It’s an ideal location to build. … We kind of blend in with this industrial area,” Hinrichs said.

NEXT hopes to have its permitting completed in 2023 and expects to take two years to build the massive complex filled with storages tanks and processing equipment. The company has an agreement with local unions to use union labor in both construction and operation of the plant. It expects to hire about 3,500 people for construction and to have a permanent staff of about 240.

The company has a contract with BP North America plus some other sources — who have not yet agreed to be publicly identified — to provide raw material for the plant. NEXT is in contact with several fuel companies as potential customers.

The PJM Planning Committee last week unanimously endorsed study assumptions developed in the Resource Adequacy Analysis Subcommittee (RAAS) for the RTO’s 2022 Reserve Requirement Study (RRS).

The assumptions, which are similar to those used in the 2021 RRS study, will be used to reset the installed reserve margin (IRM) and forecast pool requirement (FPR) for delivery years 2023/24, 2024/25 and 2025/26, as well as to set the initial IRM and FPR for 2026/27, PJM’s Jason Quevada told the committee.

PJM uses each generating unit’s capacity, forced outage rate and planned maintenance outages to develop a cumulative capacity outage probability table for each week of the year, except the winter peak week. For the winter peak, PJM uses historical RTO-aggregate outage data from delivery years 2007/08 through 2021/22.

The new assumptions reflect FERC’s approval in August of PJM’s effective load-carrying capability (ELCC) method for determining capacity values for variable, limited-duration and combination resources (ER21-2043). (See FERC Accepts PJM ELCC Tariff Revisions.)

PJM told FERC that the ELCC construct recognized the “diminishing returns associated with greater levels of deployment for most ELCC resource types,” ensuring that the RTO doesn’t become overdependent on a single resource with “inherent limitations.”

Wind, solar, hydro and landfill gas variable resources and storage resources will be excluded from the 2022 calculations.

PJM will present the final RRS report to the RAAS and PC in September and will seek members’ approval in October. Posting of the final values is expected in February.

Interconnection Process Subcommittee Charter OK’d

Members unanimously approved the draft charter of the Interconnection Process Subcommittee, which is being formed to continue work on interconnection process improvements following the sunsetting of the Interconnection Process Reform Task Force (IPRTF).

Stakeholders approved a new interconnection queue process and a related transition plan developed by the task force in April. (See PJM Stakeholders Endorse New Interconnection Process.) The proposed rules will be filed with FERC by June 16.

Also at the PC meeting, Jason Shoemaker, manager of interconnection projects, provided an update on the RTO’s efforts to reduce the interconnection queue backlog.

Shoemaker said queues AG2 and AH1 will continue to be delayed, and AH2 and AI1 are also expected to be delayed. As a result, PJM is deferring project modification requests in those queues. PJM’s backlog priorities are AD2 and prior queues (65 studies); backlogged system impact studies (about 190); and queues AE1 through AG1 (about 800), he said.

Response to DOE Notice of Inquiry

PJM’s Pauline Foley briefed the committee on the RTO’s plan to respond to the Department of Energy Grid Deployment Office’s May Notice of Inquiry and request for information on how it should implement the “anchor tenant” and revolving loan programs under its Transmission Facilitation Program (TFP). The TFP is intended to aid the construction of grid infrastructure that improves reliability and resilience or increases interregional transfers. (See DOE Seeks Input on Tx Loan, ‘Anchor Tenant’ Programs.)

The program, authorized under the Infrastructure Investment and Jobs Act (IIJA), allows DOE to purchase up to 50% of the proposed transmission capacity of an eligible transmission line for up to 40 years. It can also make loans for the costs of carrying out an eligible project: new lines of at least 1,000 MW (500 MW for projects in an existing transmission corridor).

The IIJA also authorized DOE to enter into public-private partnerships to advance an eligible project in a National Interest Electric Transmission corridor or that is necessary to accommodate an increase in transmission demand across more than one state or transmission planning region. DOE is authorized to borrow up to $2.5 billion from the U.S. Treasury at any one time.

Responses to DOE were due Monday.

Transmission Expansion Advisory Committee

Generation Deactivation Update

PJM reported that it completed reliability analyses and identified no violations for the following generation deactivations:

Morgantown combustion turbines 1 and 2 (32 MW) in the PEPCO transmission zone (Oct. 1);

Carbon Limestone landfill (19.3 MW) in the American Transmission Systems Inc. (ATSI) zone (July 31); and

Cape May County landfill (0.6 MW) in the Atlantic City Electric zone (Aug. 5).

Members also heard second reads on proposed solutions to:

an N-1 thermal violation on the 345-kV Beaver-Hayes line resulting from the planned retirement of Sammis 5, 6 and 7 (1,504 MW) in the ATSI zone on June 1, 2023. The recommended solution includes replacing four 345-kV disconnect switches with 3000A disconnect switches; replacement of substation conductors; upgrades of transformer protection relays; and relay settings changes. The estimated cost is $2.1 million.

the March 31 deactivation of Avon Lake 9 and 10 (648 MW) in ATSI. The plan includes removing five 138-kV bus tie lines and one 345-kV bus tie line from the Avon Lake Substation; adjusting relay settings; and installing new fiber between the 345-kV and 138-kV yards to re-establish relay protection. The project, expected to be completed by April 28, 2023, has an estimated cost of $2.5 million.

Supplemental Projects

Members heard presentations on the following supplemental projects:

FirstEnergy outlined a 230-kV service request for a 30-MW load near the 230-kV line Doubs-Monocacy, with a requested in-service date of November 2022 (Need # APS-2020-012).

Dominion Energy presented more than a dozen supplemental requests, including new substations and additional distribution transformers to serve data centers and other sources of load growth.

NJ Offshore Wind SAA

Remaining reliability studies will be completed in July and August for selected scenarios in the 2021 State Agreement Approach proposal window to support New Jersey’s offshore wind projects, PJM’s Jonathan Kern told members. Scenario development and initial reliability studies are expected to be completed this month.

PJM is considering about 26 point-of-interconnection scenarios.

The New Jersey Board of Public Utilities is reviewing comments that were submitted in its OSW transmission docket (QO20100630), including responses to questions posted following four stakeholder meetings the agency held to collect feedback on the evaluation of the transmission proposals. (See NJ Seeks Efficiency, Savings in OSW Transmission Process.)

60-day Proposal Window Opened

PJM opened a 60-day window June 7 to receive proposals to address reliability and market efficiency needs on the 345-kV Crete-St. John, Crete-E. Frankfort, University Park N-Olive and Stillwell-Dumont lines.

Multi-Driver Proposal Window 1 will reflect the removal of queue project U3-021/AB2-096 and the inclusion of project AB1-089, PJM’s Sami Abdulsalam told members. PJM will evaluate the proposals in coordination with MISO. The window closes Aug. 8.

PJM noted an overlap in flowgates from the new window and 2021 Proposal Window 2 and said entities wanting to modify their 2021 proposals should submit new entries in the new window. Entities wanting to withdraw proposals from consideration must notify PJM to avoid future billing.

Abdulsalam said PJM is planning to open a proposal window for the 2022 Regional Transmission Expansion Plan between the last week of June and first week of July. PJM posted the latest preliminary models on May 23 and is reviewing FERC Form 715 analysis results from transmission owners while working on N-1-1 and load deliverability analyses.

California regulators are fine-tuning a set of draft rules that would transition the state to 100% light-duty ZEV sales by 2035, with a final round of proposed changes expected to be released for public comment this month.

The California Air Resources Board (CARB) held the first of two public hearings on the proposed Advanced Clean Cars II regulation on Thursday. Board members expect to cast a final vote on the rules in August.

Advanced Clean Cars II (ACC II) is a proposed follow-up to CARB’s current Advanced Clean Cars I rule. The ACC II regulation would apply to vehicles sold in the state starting with model year 2026.

Advanced Clean Cars includes a ZEV program, which requires an increasing percentage of light-duty car and truck sales in the state to be zero-emission each year, plus a low-emission vehicle, or LEV, program that sets tailpipe emission standards for internal combustion vehicles.

Banked Credit Proposal

During Thursday’s hearing, CARB staff rolled out several proposed modifications to a previously released draft regulation based on stakeholder feedback. Some of the changes relate to the ACC system of credits awarded to automakers for providing ZEVs for sale in the state.

A draft regulation released in April proposed reducing an automaker’s number of banked ZEV credits remaining at the end of ACC I by dividing the total by four. Credits for plug-in hybrids, which are calculated differently, would not be affected.

Under the new proposal, ZEV credits and PHEV credits would both be reduced at the end of ACC I by dividing the total by two.

Anna Wong, CARB’s lead staff on the ZEV regulation, said the proposal is intended to allow automakers to benefit from overcompliance with ZEV requirements in previous years. But it’s designed so “they couldn’t just run over the program with just credits and not make any more vehicles,” she said.

“In California, there are a lot of ACC I credits that will be amassed — a lot,” Wong said.

The percentage of credits an automaker could use to meet ZEV requirements would be capped. But manufacturers could decide how to apply their allotment of credits over the first five years of ACC II, Wong said. For example, they could use all their credits in the first year, the fifth year, or spread them out over multiple years.

Durability Requirements

Other changes to the ACC II draft regulation would soften durability requirements for ZEVs.

The earlier proposal would have required ZEVs to retain 80% of their initial range after 10 years of driving by a typical customer. Under the new proposal, the 10-year requirement would be reduced to 75% in the first five years of ACC II.

In addition, enforcement of the requirement would initially be looser, without consequences for manufacturers that miss the mark by “just a trivial tiny amount,” Mike McCarthy, chief technology officer in the ZEV program, told the CARB board.

McCarthy said most automakers are on track to meet the 80% range requirement. Some industry leaders are even saying that their ZEVs will retain more than 90% of the original range after 10 years, he added.

But some ZEV makers are less experienced and don’t have 10-year-old cars on the road yet, he said.

“We do have to take into account that this is new for them and they are gaining experience,” McCarthy said.

The Advanced Clean Cars ZEV program applies to light-duty vehicles, and questions have come up regarding the light-duty classification.

Wong said that a large pickup truck with an internal combustion engine might weigh less than 8,500 pounds, a size that’s considered a light-duty vehicle. But when internal-combustion components are replaced with a ZEV battery, “It might cease to be a light-duty truck and become a medium-duty vehicle,” she said.

In that case, manufacturers currently have the flexibility to decide whether to count the vehicle as a light-duty vehicle in the Advanced Clean Cars program or as a medium-duty vehicle under CARB’s Advanced Clean Trucks program. Wong said CARB wants to retain that flexibility in ACC II.

100% ZEV Sales

In September 2020, Gov. Gavin Newsom issued an executive order requiring sales of all new passenger vehicles to be zero-emission by 2035. The proposed ACC II regulation sets out a legally binding and enforceable pathway for getting to 100% ZEV sales.

An earlier version of the ACC II proposal featured a more gradual route to increased ZEV sales in the state. But in April, CARB released a revised draft that ramped up ZEV sales more rapidly in the early years of the rule. (See New Draft of Advanced Clean Cars II Would Speed ZEV Sales.)

The agency is aiming to finalize the ACC II by the end of the summer so that the rules can take effect for model year 2026. The federal Clean Air Act allows California to adopt its own vehicle emissions program rather than following federal standards. But a two-year waiting period is required between adoption of the regulation and the model year to which it will apply.

Approving the regulation this summer will also give states that have adopted California’s ACC program a chance to update their own rules in time for model year 2026.

CARB expects to release a formal version of its latest revisions to ACC II in the next few weeks. That will be followed by a 15-day public comment period.

PJM’s Susan McGill last week reviewed a proposed issue charge and problem statement to improve processes for scheduling internal network integration transmission service (NITS).

The RTO said its current tariff makes little distinction between internal and external service requests, requiring all requests be studied to ensure sufficient headroom or need for system upgrades. Internal requests are for internal generation serving internal load; external/cross-border requests refer to external generation serving internal load or internal generation serving external load, respectively.

The initiative seeks to revise the tariff and manual language to differentiate between the two types of requests and reduce administrative burdens on entities using internal service.

The problem statement says the current tariff sets out the process for renewing cross-border service but is “not applicable to internal service requests because the internal generation and load served through internal service are already evaluated and maintained in the existing models used for studies under the Regional Transmission Expansion Process (RTEP).”

The current tariff “requires start and end date durations, creating additional administration burdens to ensure timely rollover rights for internal NITS.”

The issue charge proposes to make the following issues out of scope: border service processes associated with NITS; the RTEP process; the pseudo-tie request process; transmission service rates; and the process to integrate new service territory into PJM.

The committee will be asked to approve the issue charge at its next meeting.

‘Maximum Emergency’ Generation

Members heard a first read of PJM’s Package A, a collection of proposed manual changes addressing maximum generation status.

In response to concerns over fuel and emissions, PJM made a change last year to section 6.4 of Manual 13 to temporarily modify the remaining hours under which a resource may be offered as “maximum emergency generation.” The change, which members endorsed in October, allowed PJM to request resource owners move fuel- or emissions-limited steam units into the “maximum emergency” category if the resource’s remaining run hours fall below 240 hours (10 days), an increase from the manual’s original remaining run time of 32 hours. Unless required to meet local or regional reliability needs, the units would be restricted from operating during that status, unless their inventory rose above 21 days (504 hours).

The change set out similar rules for combustion turbines, except that they could be moved into maximum emergency status when their remaining run hours on all fuel types fall, or are expected to fall, below 24 hours, versus 16 hours in the original language.

The modifications had an expiration date of April 1, 2022, but the Markets and Reliability Committee eliminated the deadline in March to allow work on a permanent solution. The MRC also approved a problem statement and issue charge. (See “Max Emergency Changes Endorsed,” PJM MRC/MC Briefs: March 23, 2022.)

Changes to Deactivation Notification Requirements

PJM reviewed “quick fix” changes to Manual 14D: Generator Operational Requirements regarding the deactivation analysis timeline.

Current rules require notification of PJM at least 90 days in advance of the planned deactivation.

Under the changes, desired deactivation date would be no earlier than:

July 1 of the current calendar year for notices received between Jan. 1 and March 31;

Oct. 1 of the current calendar year for notices received between April 1 and June 30;

Jan. 1 of the following calendar year for notices received between July 1 and Sept. 30; and

April 1 of the following calendar year for notices received between Oct. 1 and Dec. 31.

PJM will study deactivations four times per year for all notices received prior to the study commencement dates (Jan. 1, April 1, July 1 and Oct. 1).

Deactivation notifications would only require good-faith estimates for a time period if the generation owner requests to mothball the unit.

PJM will notify generation owners by the end of February, May, August and September, respectively, on the results of their reliability analyses.

The committee will be asked to endorse these changes at its next meeting.

Operating Metrics for May

PJM reported an average load forecast error of 1.82% in May, with a peak hours error of 2.03%, both above the 25-month average, according to the RTO’s operating metrics.

The RTO continued its unblemished record in 2022 of exceeding its 99% balancing authority area control error limit (BAAL) goal, scoring a 99.8% in May, with 55 excursions totaling 88 minutes outside of limits.

There were four spinning events, three reserve sharing events with the Northeast Power Coordinating Council, 24 post-contingency local load relief warnings and four hot weather alerts.

PJM gave a second first read of a proposal to update rules governing variable environmental charges and credits and their inclusion in cost-based energy offers. Generation units receiving production tax credits or renewable energy credits must reflect them in their fuel-cost policies when submitting non-zero cost-based offers into the energy market.

The committee will be asked to endorse the package, which includes changes to Manual 15 and Schedule 2 of the Operating Agreement, at its next meeting.

Market Suspension

PJM’s Stefan Starkov gave a second first read of the revised PJM/Independent Market Monitor package of changes to the treatment of long-term market suspensions. The package, which is intended to address a gap in tariff language regarding how to settle the real-time market if prices can’t be determined, was revised to reflect feedback received at the May MIC meeting.

In September, the Markets and Reliability Committee delayed a vote on rule changes after representatives from Calpine and Vistra made a motion to defer pending further discussions at the MIC. (See “Market Suspension Vote Delayed,” PJM MRC Briefs: Sept. 29, 2021.)

Calpine said the proposal did not adequately address market suspensions lasting a week or longer, and that it was concerned with compensating generators for an extended period based only on their cost‐based offers, which are computed solely on short‐run marginal costs.

The original proposal would have had different rules for outages of more and less than six hours. Outages less than or equal to six hours would substitute the missing hours with available day-ahead or real-time LMPs or the average of adjacent hours. For outages of more than six hours, LMPs would be set at $0/MWh, with make-whole payments at the lesser of dispatched megawatts or actual megawatts using cost-based offers.

The revised proposal would use available DA or RT LMPs or the average of adjacent hours for all outages less than or equal to 24 hours. Pricing for outages longer than 24 hours would be set using a long-term market clearing mechanism incorporating the aggregate supply curve.

The curve would be based on hourly supply-demand intersections constructed from available offers (including available resources not running) and actual generation megawatts as a proxy for demand. Constraints would be ignored. Energy and ancillary services would continue to be calculated at five-minute intervals.

The committee will be asked to endorse the package at its next meeting.

DR/PRD Compliance for Weather-sensitive Load

Sharon Midgley, representing Exelon (NASDAQ:EXC) and Baltimore Gas and Electric (BGE), presented a first read of a problem statement and issue charge to consider an alternative demand response/price-responsive demand (PRD) compliance construct for weather-sensitive load, such as residential demand impacted by summer air conditioning.

Midgley said the current rules compare metered load under prevailing weather conditions to the peak load contribution (PLC) based on weather-normalized peak weather conditions.

Capacity compliance for DR and PRD is currently based on the firm service level (FSL), calculated as the PLC minus the amount of installed capacity the DR/PRD resource cleared in the capacity auction. Compliance is achieved if metered load is at or below the FSL.

Over the summers of 2018-2021, the actual peak load for BGE’s weather-sensitive residential customers averaged 13% higher than the weather-normalized peak load. The disparity was the largest in 2019, with weather-normalized load 22% lower than actual load.

The discrepancy means DR and PRD providers may not be able to offer the full capability of their programs into the capacity market because of unachievable FSL, Midgley said.

The committee will be asked to approve the issue charge at its next meeting.

Capacity Offer Opportunities for Generation with Co-located Load

PJM’s Lisa Morelli led a discussion on solution options for capacity offer opportunities for generation with co-located load. (See “Co-located Load Issue Charge Endorsed,” PJM MIC Briefs: Jan. 12, 2022.)

Enel X North America, which serves load customers with on-site generation, said capacity accreditation for such customers “is a ripe area for review, particularly given technological innovation and direction from FERC Order 2222 to fully value injections from generation sited with load as distributed energy resources.

“Load that is not station power [should be treated] as any other load,” Enel said. “Absent a transmission cost being allocated to the co-located load, these costs would be unfairly and unnecessarily passed on to all other ratepayers.”

Operating Reserve, Quadrennial Review

Members also continued work on an initiative to clarify operating reserve rules for resources operating as requested by PJM (See “Operating Reserve Clarification,” PJM MIC Briefs: Feb. 9, 2022) and the Quadrennial Review, which determines the shape of the variable resource requirement curve, the cost of new entry for each locational deliverability area, and the methodology for determining the net energy and ancillary services revenue offset for the PJM region and each zone.

The Memphis city utility’s hopes of leaving the Tennessee Valley Authority for MISO could be dashed by inflation and high interest rates that could slash potential savings, a consulting firm said last week.

GDS Associates compared the top two bids of the 27 proposals Memphis Light, Gas and Water (MLGW) received in response to its search for alternative energy suppliers as the utility met Thursday with its Board of Commissioners and the Memphis City Council. GDS evaluated the bids against MLGW’s long-term partnership option with TVA, scoring the proposals on pricing, performance guarantees, proven experience, and technical capability.

The consulting firm estimated the utility could save almost $31 million annually with the higher-scoring bid and $9.4 million annually under the second bid over a 25-year period that included the utility’s transition from TVA. The analysis assumed higher natural gas prices, higher capacity prices and higher interest rates than MLGW’s 2020 integrated resource plan, which predicted the city could save between $100 and $120 million if the utility left the federal agency for a power mix of natural gas and solar power.

Potential Losses in New Environment

However, GDS Power Supply Principal Chris Dawson warned that the savings could quickly nosedive and turn into losses if inflation, gas and capacity prices, and interest rates all increase by 2028. He said the lower-scored portfolio could saddle MLGW with about $100 million dollars of additional annual costs; the higher-scored bid could lead to $25 million in annual losses.

Dawson’s comments were met with audible rumblings in the conference room.

GDS Associates’ Chris Dawson | MLGW

“This is just a reminder about how the world can change. I’m not trying to be a harbinger of doom and suggest it will be like this in 2028 … but it could be like this,” Dawson said.

He said consumer demand and geopolitical events have quadrupled natural gas prices, increasing the risk involved in constructing a gas plant. He also pointed out that MISO’s April capacity auction cleared the highest-ever prices for its Midwest region.

Dawson said he believed MLGW would call for less emphasis on natural gas fired generation were MLGW’s IRP developed today.

A non-TVA arrangement will subject the utility to new risks, including regulatory permitting, a likely credit ratings downgrade, and construction delays, he said.

“Under your current situation with TVA, most of these things you don’t even think about. It’s an afterthought,” Dawson said. “I’m not suggesting MLGW can’t build out that infrastructure, but it’s not cheap, it’s not easy, and you don’t do it overnight.”

Concerned about its power costs, the utility began seriously considering a break with TVA in 2020 when it produced an integrated resource plan. It later issued an RFP based on the plan. (See Memphis Muni Mulls Move to MISO.)

MLGW is at a crossroads. It can select one of the bids and depart TVA for MISO’s energy markets, maintain its current arrangement with TVA, or sign a long-term partnership agreement (LTPA) that will lower costs but tie the utility to TVA for at least two decades.

The federal agency’s LTPA option will result in an immediate 3.1% reduction in base rate charges, keeping them steady through 2029 and allow MLGW to acquire up to 5% of its energy needs from renewable sources. However, the contract includes a stranded-cost obligation that will make the utility responsible for a percentage of TVA’s future investments and follow MLGW if it decides to later leave TVA. The LTPA also requires a 20-year termination notice; MLGW’s current agreement has a five-year exit notice.

“It’s not easy just to say, ‘Hey, let’s sign up for the LTPA and figure this out later,’” Dawson said. “I’m not even familiar with agreements that have 20-year termination notices.”

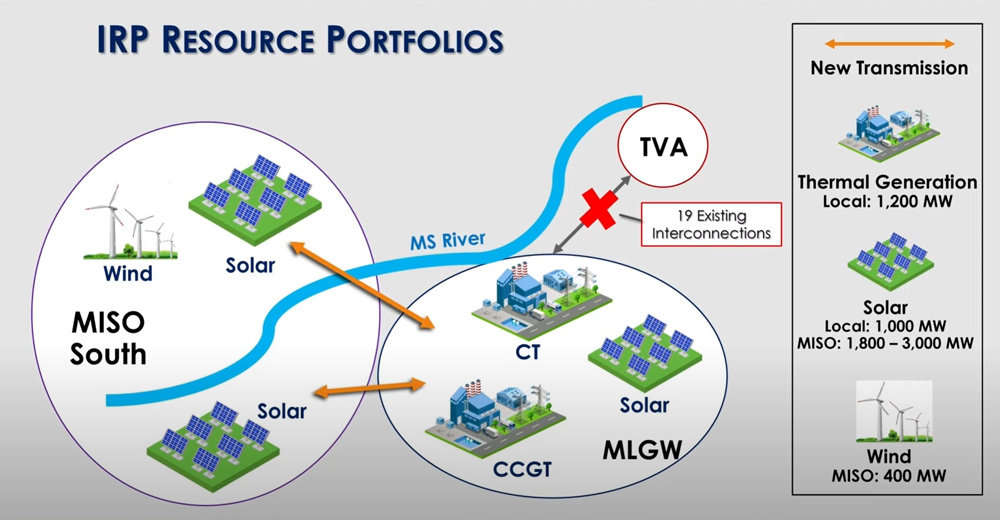

Options explored under MLGW’s IRP include connections to MISO to access renewables and building combined cycle plants and solar near Memphis | GDS Associates

MLGW is TVA’s largest wholesale customer, spending about $1 billion per year on electricity.

“It’s not lost on anybody that unlike pretty much any other one of TVA’s wholesale customers, MLGW does have a real opportunity to do something different,” Dawson said. “No wholesale customers have successfully left TVA. They have a certain type of protection, a certain type of legacy that revolves around their transmission system. That means if you leave TVA, you have to do a lot of work, I mean a lot of work and invest billions of dollars.”

GDS estimated that under the LTPA, MLGW will pay $78.77/MWh for energy from 2028 to 2047. If the utility leaves TVA for MISO and constructs its own transmission, it can expect to spend $78.20/MWh for energy in the same timeframe based on the best bids, Dawson said. He added he wasn’t surprised by those numbers and said that under the more independent MISO option, MLGW will own its transmission links and be able to control its destiny.

$1B in Tx Upgrades

A Siemens analysis prepared for MLGW concluded the utility will require 2,400 MW of new firm import capacity to MISO South should it leave TVA. The technology company said that would entail two 500-kV lines spanning the Mississippi River into Entergy Arkansas’ territory and a 230-kV line terminating in Entergy Mississippi’s footprint. Siemens said it would take seven to eight years to build the lines at a cost of about $1.2 billion.

GDS included the new transmission facilities in considering all the potential costs of leaving TVA.

“As a utility, you just don’t turn on a dime,” Dawson said.

MLGW Board Chair Mitch Graves said things have changed since the utility began exploring bids. He said supply chains have become strained, inflation is squeezing customers and energy prices have climbed sharply.

“All of that has to come in our decision-making process,” he said.

City council member Dr. Jeff Warren said MLGW might consider waiting for economic tensions to settle before proceeding.

“It seems that moving quickly on this may not be very prudent, but getting our ducks in a row for a longer transition may be something that we should be doing as a system,” he said.

GDS said it will finalize its evaluation of the bids and conduct negotiations with a short list of bidders.

MLGW CEO J.T. Young said utility executives will recommend a supplier to its board in August, opening a 30-day public comment period. The commissioners could vote on the issue in September.

The bids, currently confidential, will be made public for the August meeting.

The utility is accepting public comment on the masked bid data at PowerSupply@MLGW.org.

In what backers believe is the biggest deal of its kind, three owners of urban forests in King County, Washington, this month sold more than $1 million in carbon credits to Regen Network Development, a Delaware-based blockchain software company.

Regen’s $1 million purchase of carbon credits ensures that the two of the owners — King County and the city of Issaquah — won’t harvest the carbon-absorbing trees on a 46-acre piece of land. Issaquah is an outer suburb of Seattle in the foothills of the Cascade Mountains. Credits on the Mountains to Sound Greenway Trust land cover an additional 2.6 acres in the northern Seattle suburb of Shoreline.

Regen is collecting carbon credits from King County to offset its contributions to greenhouse gas pollution elsewhere when its overall carbon footprint is calculated.

“Our region is now part of the largest sale of urban forest carbon credits in U.S. history,” King County Executive Dow Constantine said in statement June 3. “We will steward the newly protected urban forests so they can continue to absorb carbon, contribute to cleaner air and water, and create more greenspace where people, families and communities can gather.”

This sale comes in the wake of Washington launching a first-of-its-kind program to auction off carbon offset credits to preserve some of the Washington Department of Natural Resources’ forest land.

DNR duties include managing the state’s trust lands with the mission of producing revenue from property for various programs such as education. The agency routinely auctions off trees on its lands to be harvested for timber.

The new DNR program will set aside 10,000 acres of forests — with trees that began growing prior to 1900 — that have the potential to be harvested. Offset buyers will bid on carbon credits to keep those carbon-absorbing forests intact. This enables the DNR to achieve its mission of producing revenue from its older forests without having to harvest them for timber.

The new state program has identified 2,500 acres on DNR trust lands to be set aside this year in Whatcom, King, Thurston and Grays Harbor counties, stretching from northern to southern Puget Sound. Another 7,500 acres are scheduled to be identified next year.

Many details must still be worked out, including when the credits will be auctioned, what the minimum acceptable bids would be and the overall fundraising targets. The state plans to auction off 917,000 carbon credits in the first 10 years of the program.

As the U.S. and other countries seek urgently to reduce greenhouse gas emissions amid a backdrop of global energy market volatility, we are confronted with a fork in the road: the “chaotic” path for decarbonization, which at times appears to be the market’s current trajectory, versus the “coherent” path — the path we strive to follow.

What, though, will make the energy transition chaotic versus coherent, and why does it matter? The chaotic path is characterized by opposing extremes that reflect the current polarization around energy discourse — those ignoring the imperative to decarbonize, and those seeking a fossil-free end-state on an unrealistic timeline in terms of cost and risks to system reliability.

The coherent path involves embracing both rapid deployment of low-carbon energy resources and maintenance of sufficient fossil-fuel infrastructure to ensure continued energy security, affordability and reliability as our economy transitions toward net-zero GHG emissions.

Reid Capalino, SVP business development for LS Power | LS Power

According to the International Energy Agency’s (IEA) modeling, a long-term net-zero trajectory will see U.S. fossil-fuel consumption decline by more than half in the next 20 years, caused by enhanced energy efficiency and increased focus on renewables such as wind and solar. Yet in this scenario, fossil-fuels in 2040 will still serve nearly 40% of total energy demand, including oil for transportation and natural gas for power plants, industrial facilities and buildings. The expected decline in conventional gas-fired power generation is even more dramatic: an 89% reduction from 2020 levels.

As one of the largest owners of gas-fired assets in the U.S. focused on a sustainable energy transition, we fully appreciate and understand the long-term need to reduce unabated gas-fired generation to meet our climate goals. Simply emphasizing an end-state of 2040, however, glosses over several complexities in this transition, as reflected in the IEA’s modeling of a low-carbon future:

Much of the gas-fired generation decline would occur after 2030.

This decline would occur, in part, by aggressive deployments of emissions-reducing technologies, such as battery storage and those capturing and sequestering CO2 emissions from power and industrial facilities, which will require new policies to overcome economic and technical obstacles.

Throughout this transition, standby gas-fired generation will remain necessary to ensure energy reliability during peak weather events (e.g., extremely cold or hot temperatures) when renewable energy sources alone may be insufficient to balance supply and demand. Even as gas-fired generation shifts from providing energy (megawatt-hours) to providing capacity (megawatts), hundreds of power plants with some nexus to the natural gas system will likely need to remain in operation.

Unfortunately, states such as Illinois are mandating the retirement of gas-fired generators without adequately planning to replace the flexible capacity that such generators provide or analyzing the net impact that these retirements will have on GHG emissions.

Shortsighted retirement mandates will lead to a chaotic energy transition, thereby eroding the political support needed for the transition to progress. We should instead consider how maintained and repurposed fossil-fuel infrastructure can preserve reliability as we rapidly increase use of renewable energy — understanding that maintenance/repurposing of existing infrastructure and development of new low-carbon energy sources both require significant investments now.

So, what can we do to support a more coherent path for decarbonization?

Support long-term federal tax credits and state-level incentives for low-carbon energy sources, and advocate for policies that value the flexibility of gas-fired generators.

Advocate for tighter environmental standards to reduce fugitive methane emissions through the natural gas value chain, and support judicious investment in natural gas infrastructure, such as pipelines and associated compression/storage facilities to deliver gas when needed, liquefied natural gas terminals to help balance domestic gas markets, and upstream natural gas production to ensure a continued robust domestic supply.

Support efforts to deploy new zero-carbon technologies and repurpose existing fossil-fuel infrastructure, such as retrofitting carbon capture onto existing power plants and industrial facilities.

We urge everyone to understand where our energy system currently stands, where we want to be and what we need to do to get there. This process will require greater collaboration among companies, policymakers, activists and other stakeholders.

More coherence, not more chaos, is what we need to power our homes and businesses today while protecting the planet and strengthening the resilience of our energy system for tomorrow.

Paul Segal, who has been CEO of LS Power since 2011, is also a member of LS Power’s Management Committee, overseeing one of the largest independent power and transmission developers in the U.S.

Reid Capalino is senior vice president of business development at LS Power, leading the firm’s business development efforts with a focus on growing existing business lines and launching new ones.